This week’s market report provides information on:

ROMANIA CROP FORECAST 2022

We start our report with the 2022 crop forecast, related to the 2022-2023 agricultural year. What needs to be added is that we still need rainfall and lack of heat waves from the end of July, beginning of August.

There is another parameter that must be taken into account, namely the recent low temperatures, which will delay the harvest by at least 7-10 days. And this will lead to an increase in prices, due to a concern for lots sold for export with shipping in the second half of June.

LOCALLY

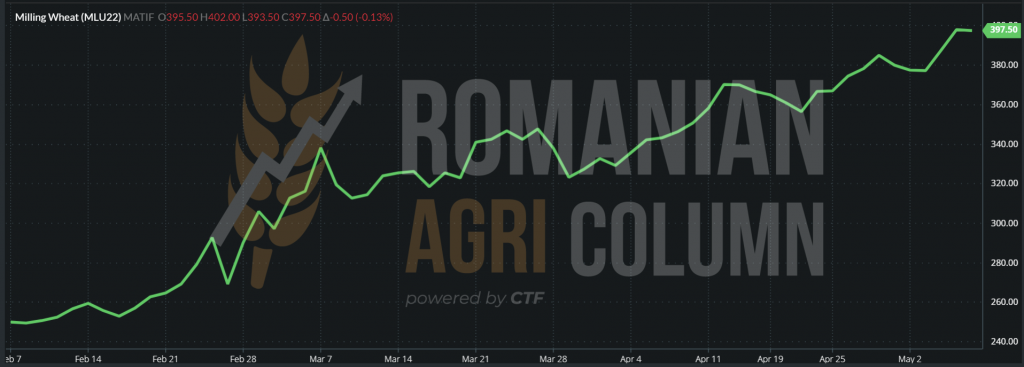

The local indications of wheat were raised to the level of 370 EUR/MT in the parity of CPT Constanța, due to the rally generated by EURONEXT. For the new crop, the indications were at EUR 365/MT.

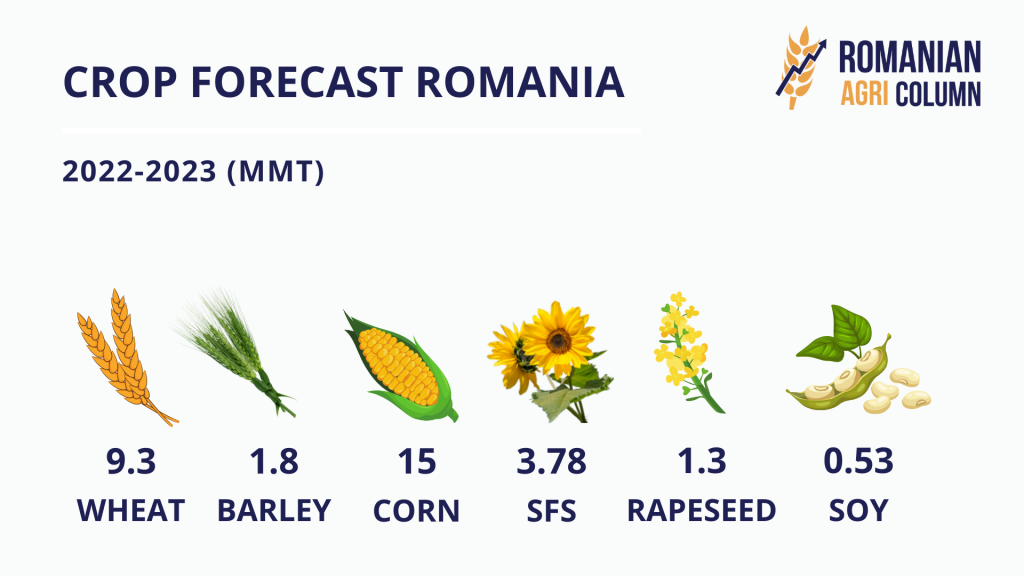

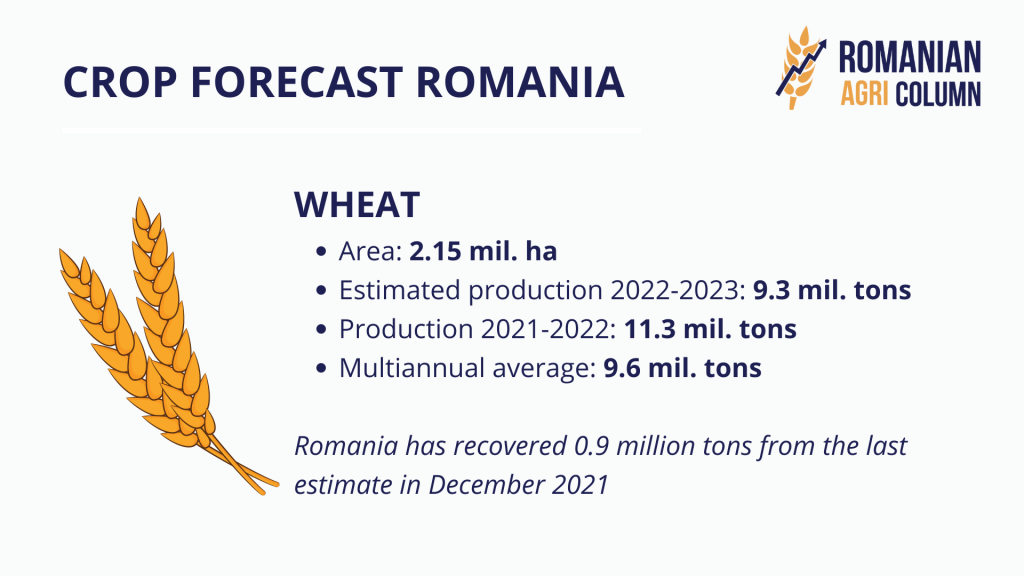

The working premises of the Romanian crop are good for this moment. The recovery came from the rains that have crossed Romania lately. This allowed for a recovery that no longer seemed possible. From a forecast indication of 8.4 million tons at the beginning of December 2021, with a late sowing and unevenly emerged areas, we have reached a forecast of 9.3 million tons. It is a recovery of 0.9 million tons. It is perfectly true that wheat needs more water, and the coming weeks are critical. It is again perfectly true that the areas affected by the pedological drought will not give the expected yield. But at the moment, these are the working premises that we use in our analysis.

REGIONALLY

UKRAINE will generate a crop level of only 19.4 million tons, compared to 33 million tons last season. We all know the causes, but they still have a difference of about 5-6 million tons left in the country and not exported. The exact figure is difficult to estimate due to the systematic theft of grain by Russia.

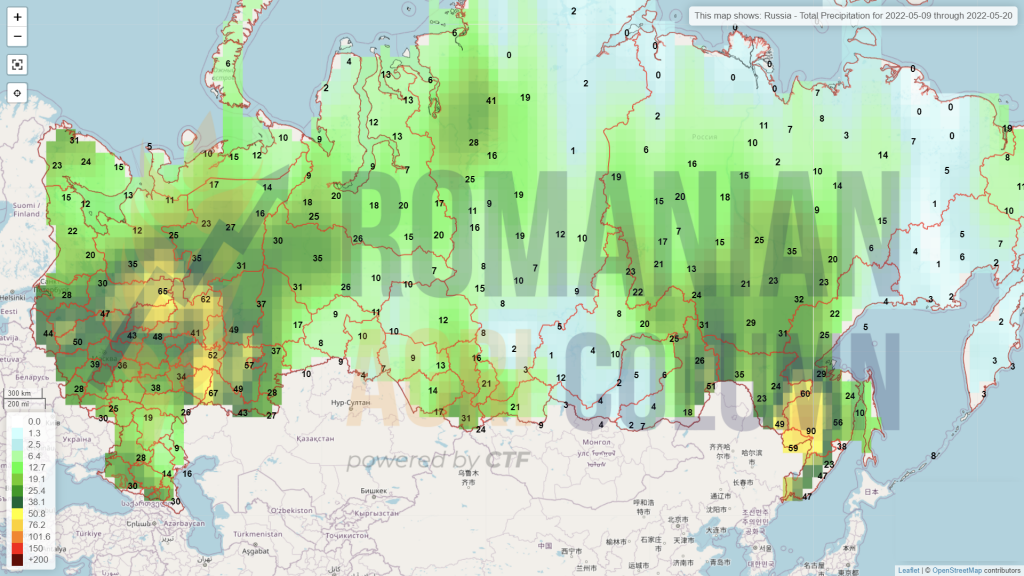

RUSSIA will generate a level of 82.5 million tons, not the 85-87 million tons they propagandistically display. We got used to the expression bunker weight and we take it with the necessary reservation.

FRANCE reports significant problems during this period, according to Reuters. France’s dry and hot weather over the next 10 days, after several months of low rainfall, will cause irreversible damage to cereals in the largest grain producer in the European Union, a technical institute said on Thursday, adding to concerns about tight global supplies. Between January 1 and May 10, France received about 30% less than the average rainfall of the last 20 years, making the soil sensitive to dry weather.

European wheat markets have been on the rise in recent days due to dry weather concerns in France and other major producing countries at a time when the war in Ukraine has reduced grain supplies.

EURONEXT reacts to news from France | WHEAT MLU22 SEP22 – 397.50 EUR

EURONEXT WHEAT TREND GRAPHIC – MLU22 SEP22

GLOBALLY

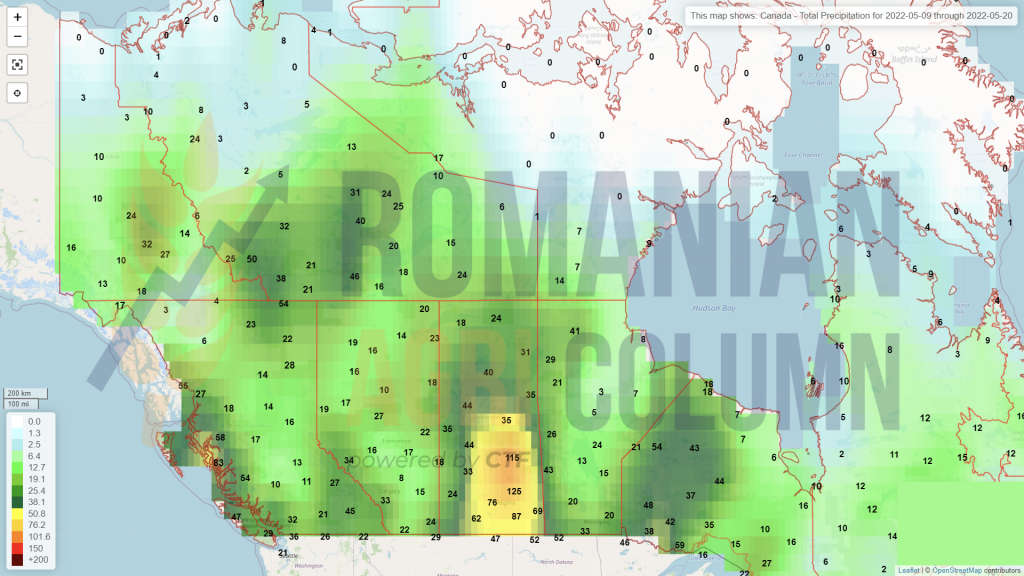

CANADA indicates a decrease in stocks of about 36% compared to last season in the same period, but at the same time, forecasts a wheat crop of 29-30 million tons. We will follow closely and see.

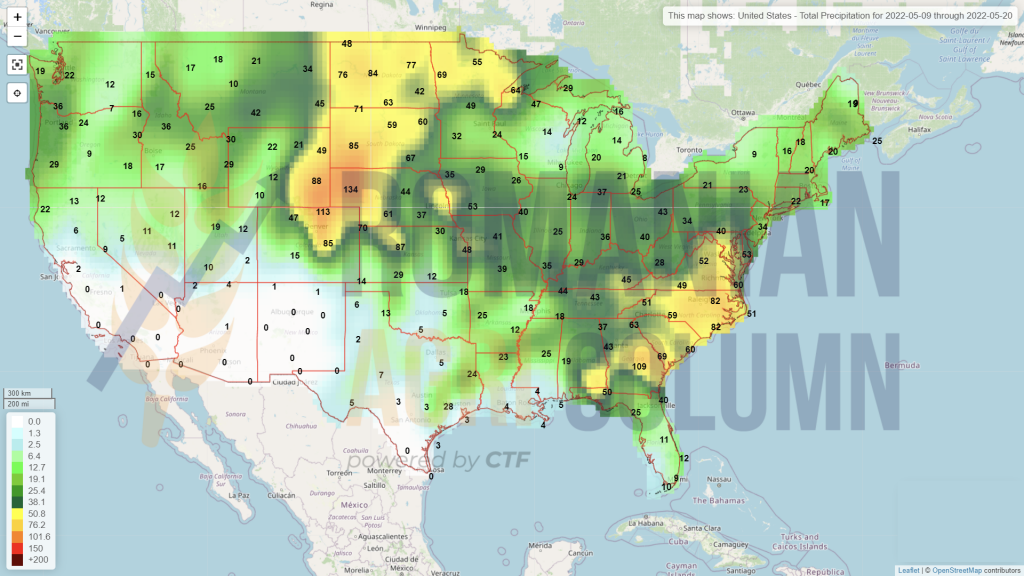

The United States have the same drought problems in the south of the Central Plains, while in the center and north they have received so much rain that lakes have formed in the fields. The problems will be generated in the chain and are related to the permeability of the soil which, due to the lack of water, has formed a crust. This does not allow leaching into the soil and the wheat actually stays in the water. One solution would be to evaporate quickly, but the temperatures are not so high.

INDIA – from ecstasy to agony in just 10 days, from the claimed status of wheat exporting country to country that has already lost 7 million tons of the forecasted harvest. And these are just conservative estimates, from potentially 111 million tons to 104 million tons in just a few days at 62 degrees. Indeed, a giant furnace covered India and Pakistan, which makes us cautious and always attentive to the climate. Weather is the ultimate factor in agribusiness.

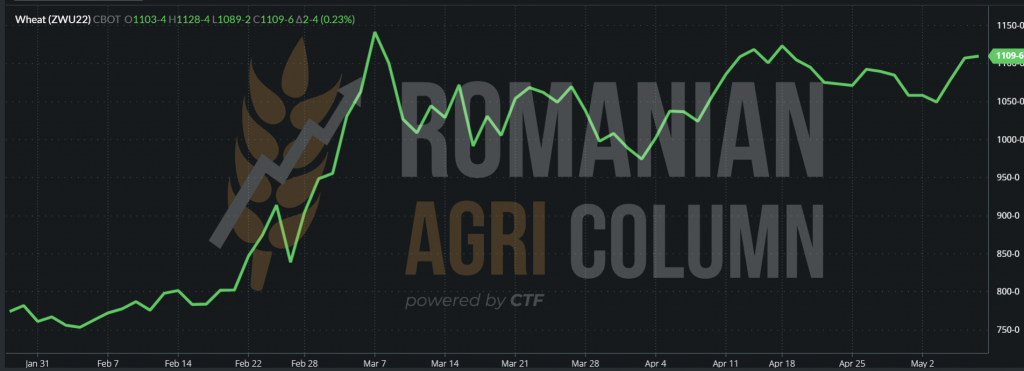

CBOT is slowly returning to growth after a nightly Profit Taking.

CBOT WHEAT ZWU22 SEP22 – 1,109 c/bu (OC = NC)

CBOT WHEAT TREND GRAPHIC – ZWU22 SEP22

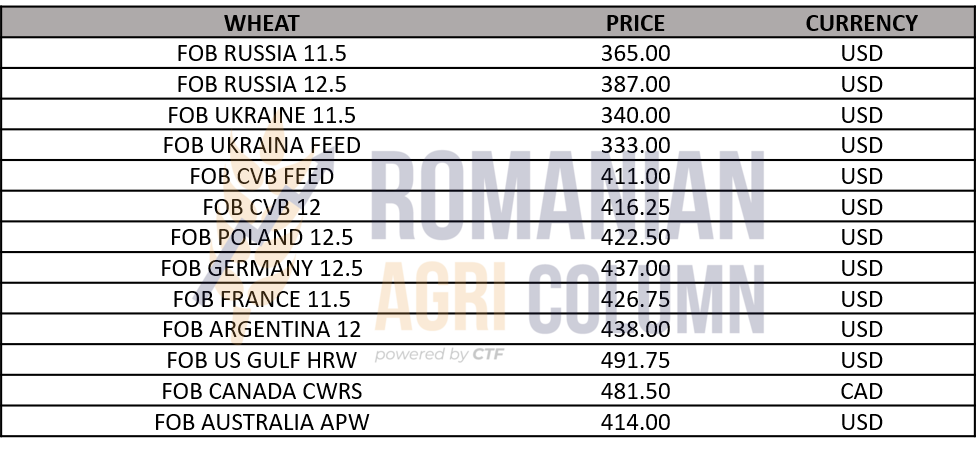

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

ANALYSIS

- Global wheat production is forecast at 780 million tons, down 12.7 million tons from last season.

- WHEAT is an element that will be difficult to control this season.

- We have less good news from the Black Sea Basin.

- We also have no good news from France.

- The United States has long generated pessimistic indications.

- India is actually putting gas on fire right now through the problems it is facing.

- One thing is certain for farmers, which is that wheat is in demand. But at what price? Fertilizer cost estimates for the autumn indicate a doubling, and the EDF announces a further 0.7% increase in interest rates in early June.

LOCALLY

The indications of the new barley crop, because we will only talk about it from now on, are set in a very large range, which starts at 320 EUR/MT and stops at 340 EUR/MT. This gap is only due to the poorer coverage of some exporters who sold to destinations in the Middle East in December 2021, and are now looking to cover. Not having a direct relationship with Euronext to be hedged, barley is currently causing significant losses in the profit and loss accounts of some exporters.

In Romania, the barley production forecast is lower than last year by about 0.1 million tons, so far. The main source of decline was the lack of rainfall in the fall of 2021.

REGIONALLY & GLOBALLY

The forecast of global barley production is increasing compared to last year globally, to the level of 148.6 million tons, compared to 146.1 million tons in the 2021-2022 season.

Production increases for Russia from 17.6 million tons to 19 million tons, Turkey from 5.8 million tons to 7.5 million tons and the EU from 52.2 million tons to 53.1 million tons. Canada is also on the rise from a disastrous year of only 6.9 million tons to a forecast of 9.9 million tons in 2022.

The decreases in forecasts are accounted for in Ukraine, of course, from 10 million tons to 5.8 million tons. Australia will also generate reduced production from 13.7 million tons to 10.9 million tons.

ANALYSIS

- Barley is already creating a precondition for growth due to global demand.

- The port of Constanța raises the prices because the coverage is reduced, and the goods are sold with delivery in the second half of June.

- The prices at which the lots were sold before the Russian invasion are already creating gaps in the exporters’ profit accounts.

LOCALLY

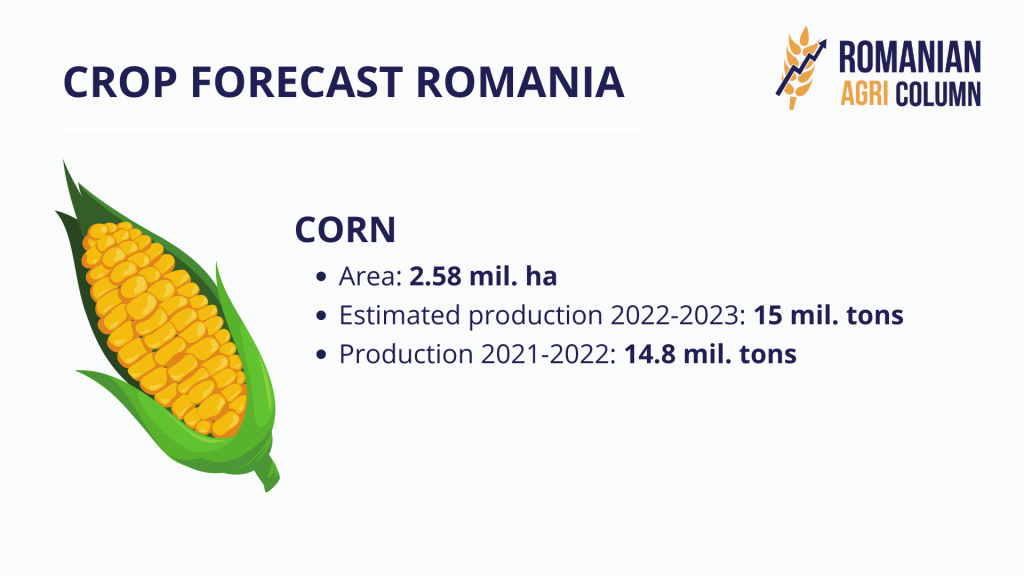

The indications of the old corn crop in the CPT Constanța are at the level of 320 EUR/MT. As for the new corn crop, it is priced at 318 EUR/MT, so there is not much difference at this time.

Romania has finished sowing corn and we are at a level of 2.58 million ha, according to the forecast. The intended area has decreased due to the conversion to sunflower. Fertilizer costs and a potential lack of rainfall were the main reasons for abandoning maize in favor of sunflower crop.

The projection currently indicates a level of 15 million tons, but conditioned by the rainfall in May, as well as by the excessive heat between July and August.

REGIONALLY

The same status as before, with Ukrainian goods trying to make their way through the war, with a huge number of wagons trying to make their way to the EU, with congestion in ports and with Russian attacks on Ukrainian transport routes. And these blockages slow down the pace.

The situation is difficult on the border with Romania. It takes 35 days to pass through the checkpoint Vadul Siret – Dorneșți (4,422 wagons) and 22 days to pass through Dyakovo – Halmeu (1,034 wagons).

The largest number of wagons go to Poland. At the Izov – Hrubieszow checkpoint, 9,953 wagons are accumulated. It takes 19 days to pass.

Ukraine announces a full stop due to these blockades. Transit is extremely difficult, and logistics have become extremely expensive. Why? Because in such situations one always takes advantage of the one who has the weakest position, in this case, the Ukrainian farmer. In the absence of options, he is forced to accept such pecuniary compromises, some downright hilarious, such as “are you selling the goods at this price or are you waiting for the Russians to take them from you?” Sad, but extremely true, unfortunately. The war gives rise to such situations which, no matter how we judge them, are also facing the farmer.

European crop forecasts indicate a total of 9.3 million ha in terms of maize sowing. All indications lead to a forecast level of about 71 million tons.

EURONEXT closes in deficit, fueled by the profit taking of investment funds.

EURONEXT OC AUG22 XBQ22 – 360 EUR | NC NOV22 XBX22 – 344.5 EUR

TREND GRAPHIC – XBQ22 AUG22 OC (OC = OLD CROP, NC = NEW CROP)

GLOBALLY

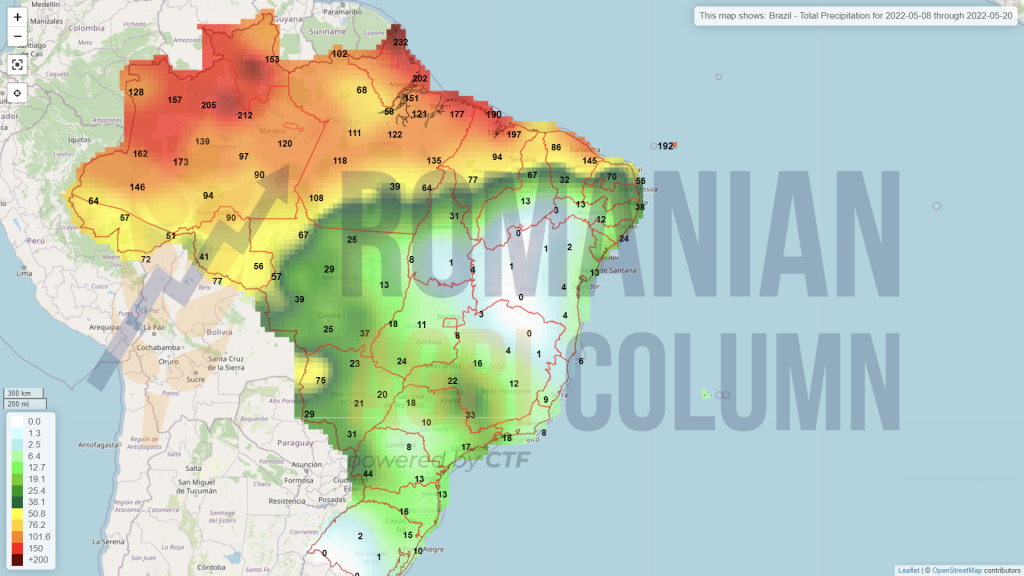

BRAZIL highlights last week’s big question mark. Rainfall forecasts are almost non-existent for the next 12 days, and longer-term forecasts of 20-25 days do not indicate improvement. Exactly at the time when it is critical for its development, the Brazilian crop will not have water. Thus, the volume of cargo resulting from Safrinha will shrink a lot compared to today’s estimates.

Harvesting will begin in mid-June and will impact the market. A large volume of goods will enter the market and will take over a large part of the demand for destinations. It will be a time that will coincide with the start of harvesting in Eastern Europe and the impact will be felt only by the owners of old corn stocks. Brazil’s total crop will account for about 115-116 million tons.

US is in the same stage of delay in sowing and things are not going well at all due to rainfall. By the beginning of May 2022, American farmers had sown about 15% of the area with corn, behind a multiannual average of 33%. But we repeat the message from the last issue, that the gap can be recovered. We saw forecasts in 2018 that did not give chances to the American corn, with sowing on June 1 and plants that did not exceed the ankle of the scout Michel Cordonnier. But in the end, it was good, it was a crop.

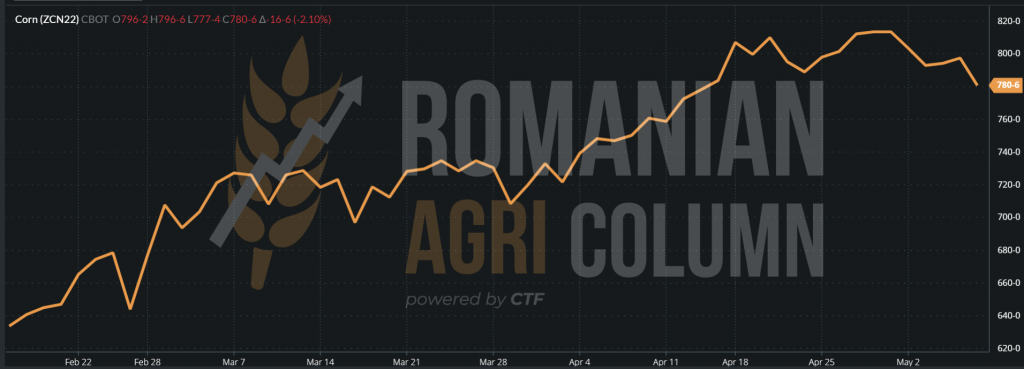

CBOT shows declines in Profit Taking and fueled by logistical bottlenecks in China due to the COVID ZERO policy.

CBOT ZCN22 JUL22 – 780 c/bu (-17 c/bu)

CBOT CORN TREND GRAPHIC – ZCN22 JUL22

CORN INDICATIONS IN MAIN ORIGINS

ANALYSIS

- Corn has support, at least until mid-June 2022, when the second Brazilian crop will arrive.

- Ukrainian flows stop due to the long waiting time at the Romanian and Polish borders.

- The United States has delays in sowing, which, for the time being, creates the preconditions for sustaining the old corn crop. But they will definitely recover.

LOCALLY

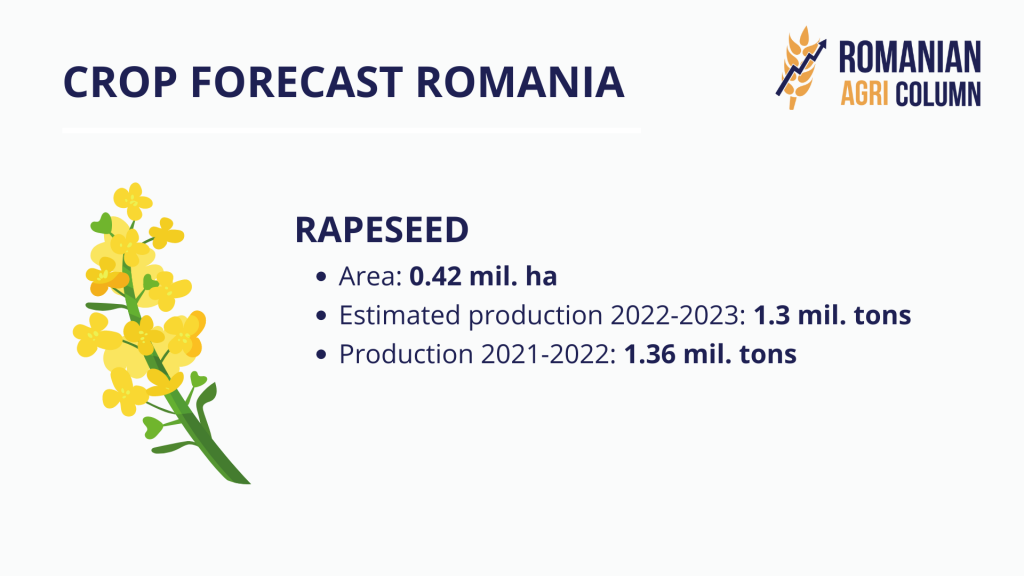

Locally, rapeseed indications are found in the same parameters, i.e., AUG22 minus 5 EUR/MT in the CPT Constanța parity or DAP Processor. Romanian rapeseed is in bloom and it is the season in which we actually see the country yellow. It is a painting that fascinates us every year, that tells us the promising crop projection. And at this point we can generate the 2022 crop projection, corresponding to the agricultural year 2022-2023. Romania started with about 417,000 hectares and now, after a rainfall free autumn and a winter with very poor rainfall, we are left with about 390,000 hectares, which will generate 1.3 million tons, i.e., 0.6 million tons less than in the 2021-2022 season.

In terms of price, rapeseed has generated, according to our estimates in the fall of 2021, an increased profit margin. We were stating then, beginning with September, the areas where rapeseed will start to receive price support, due to demand and lack of available volumes globally.

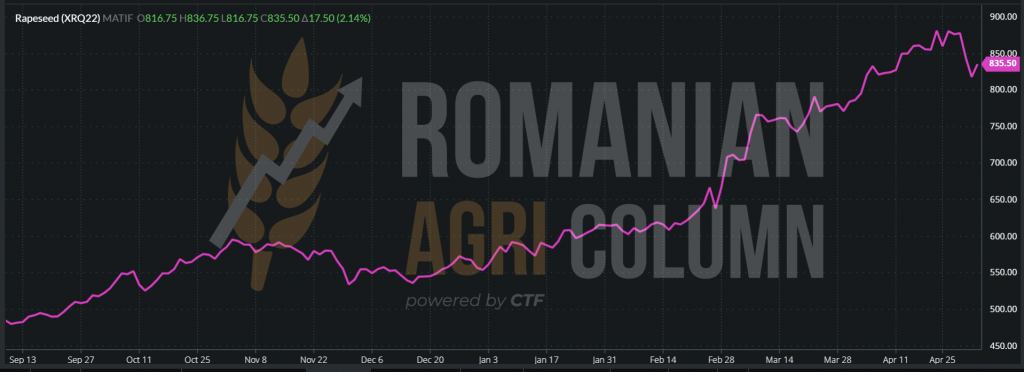

Let’s look at the chart below and see the course of rapeseed from August 2021 to the present and calculate the level from which it started (480 EUR/MT) and the indicative level today (835 EUR/MT). The indications are 355 EUR/MT higher. We have, practically, the confirmation of the profit margin of the rapeseed crop in a single image.

RAPESEED TREND GRAPHIC – XRQ22 AUG22 (SEP21 – MAY22 = +355 EUR)

REGIONALLY

The recent dramatic drop in Euronext of around 45-47 EUR in a single session was not unexpected. We have been announcing the liquidation of MAY22 positions for a long time and they have happened accordingly.

Added to this is the fact that at the moment the processing units are only looking at the sunflower seeds for the last month of the AMJ band (April-May-June). After mid-June, processors will perform annual revisions and wait for the new rapeseed harvest. In the context of the decline was Germany’s announcement of its intention to change the use of rapeseed oil from industrial to human consumption. This put even more pressure on the sharp decline in Euronext.

The European Union, even if it has contracted a little in terms of volume, will generate 18 million tons. The question remains how much Ukraine will be able to deliver. And what volume?

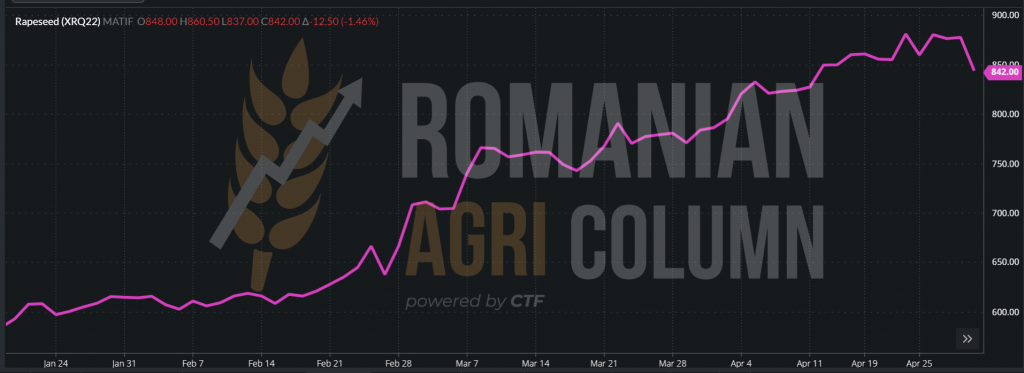

EURONEXT joins the profit trend and goes down. EURONEXT XRQ22 AUG22 – 842 EUR (-12,5 EUR)

RAPESEED TREND GRAPHIC – XRQ22 AUG22

Canada remains at an estimated 19 million tons of production for the time being, following a 7% drop in area. Australia is currently robust at 4.85 million tons.

An additional growth factor will be generated by China when it stops the COVID ZERO process. Demand in this area of the world, combined with that in Norway, are boosting the price of rapeseed.

CANOLA INDEX decreasing. NC RSX22 NOV22 – 1078.9 CAD (-12.1 CAD)

ANALYSIS

- Rapeseed resumes its ascent, being fed by demand. In light of the latest developments, oil, in turn, is on the rise.

- There will be moments of pressure near the harvest, but the trend in general will be an increasing one, if we look at things in the perspective of the next 7-8 months.

- We have a cycle of repetitive demand and supply, which will be installed once the first combine harvesters enter the rapeseed fields.

LOCALLY

The local indications of sunflower seeds amount to 825-840 USD/MT in the parity of DAP Constanța or DAP Processor. It must be said that this is the last moment to sale. The factories will enter the annual overhaul and then start processing directly on the new rapeseed crop, so that all the old crop stocks will be aligned with the price of the new crop.

The price of the 2022 sunflower seed crop today is between 730-750 USD/MT as an indication. And the primary indication of Bonus for seeds with a high content of Oleic Acid, is quoted between 25-40 USD/MT. The demand from HORECA at European level comes after the end of restrictions imposed by the pandemic and we see an increase in the bonus for HIGH OLEIC and, additionally, the reduction of the flow of crude oil from Ukraine is another factor.

In terms of figures, Romania increases the area sown with sunflower, from 1.15 million ha in 2021 to about 1.35 million ha in 2022, due on the one hand to the re-sowing of areas with very low potential of the autumn crops, and on the other hand, of the decrease of the corn area due to the risk factor called WATER and of the increase of the costs with the afferent fertilizers.

We therefore see an increase in crop potential to around 3.78 million tons, which is a first for Romania, in view of reducing the flow of crude oil from Ukraine. This was the main reason for the increase, which was, of course, associated with the level of commodity prices.

The level of rainfall has stimulated the rise and, with all the attack of the harmful Tanymecus, the premises of a good crop are in place today. The water supply from the soil, associated with the future rainfall, give a very good touch to the Romanian sunflower crop at this moment. We must also associate the fact that the vegetative stage is between 123-129 days, so that the sunflower will avoid any heat waves that have the potential to return in early August 2022.

REGIONALLY

Ukraine manages in April 2022 to transfer to Romania a flow of about 110,000 tons of sunflower seeds to Romanian processing units. However, this is penalized in Ukraine by extremely high logistical costs. As a telling example in this regard, a batch of Ukrainian goods logistically cost about 120 USD/MT. It is an extremely high price paid by Ukrainian farmers. And respecting objectivity, we must say that it is not their fault. They only bear the effects of the Russian siege.

A Ukrainian farmer has to sell the goods, but, as in such situations, everyone in the trade-logistics chain tries to make as much profit as possible. Even with the derogation to logistically support car transport (exit of Ukrainian drivers), the costs are very high.

Ukrainian farmers have two options: either sell the goods at a major discounted price, or wait for the Russians to take their goods (or sell them in the happiest case). It is a situation that must be accepted and rated at the lowest risk.

However, development in Ukraine will go through stages and we hope that the war that is actually devastating will have an end in a shorter time than is seen today. As a forecast, today we see a production of only 9 million tons of sunflower seeds, compared to 16.8 million tons last season. But we must also see what remained unprocessed/exported, i.e., a volume of about 4 million tons.

GLOBALLY

We note the attempts of certain areas of the world to increase the areas allocated to the sunflower crop. But we must say that one factor to consider is the climate, along with the experience in cultivation, which may be deficient in some areas of the globe. Take the USA as an example. American farmers focus on corn and soybeans. Wheat is also in their attention, but it does not have as much weight as corn. Climate adversity is a risk factor for sunflower cultivation, its height and calatidium are unlikely to withstand areas exposed to storms, winds and tornadoes in the United States.

In Canada, many years ago, I met a farmer with a sunflower crop in the Winnipeg region. After the introduction and the exchange of courtesies, I noticed a different accent. And the farmer reinforced my assumption, namely that he is not a Canadian native, but of Serbian origin, so he is a man who comes from European specificity, related to sunflower cultivation.

Because yes, we repeat, the sunflower crop has a European and Black Sea basin specificity. The climate and soil here allow for good yields, and the cultural and European specifics of the basin are geared towards the consumption of sunflower oil. The rest of the vegetable oils are just niche markets.

In conclusion, the global crop of sunflower seeds will be only 51.4 million tons, compared to last year which had a volume of 56.7 million tons. The result is a production deficit of 5.3 million tons.

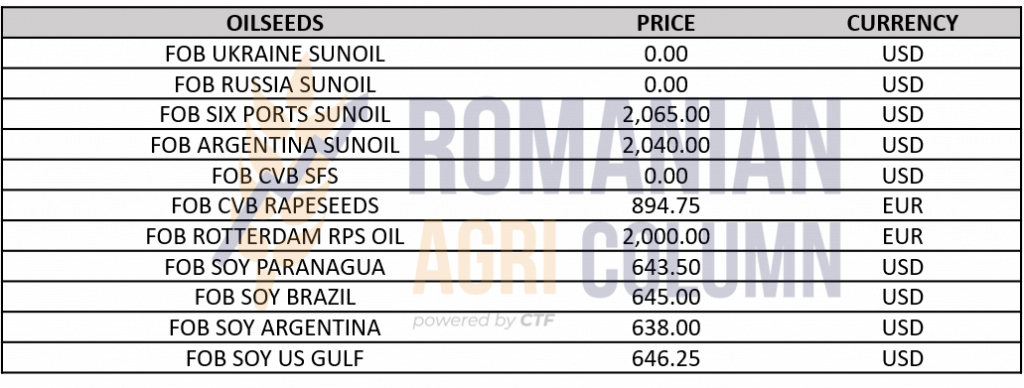

CSFO AND OILSEEDS INDICATIONS IN MAIN ORIGINS

ANALYSIS

- Demand for sunflower oil at European level will remain strong.

- Crude oil flows in Ukraine are not set at the level of previous years.

- Today’s price level is just the beginning. 820-840 USD/MT will be a landmark in a fairly short time.

- The feeling of profit fuels the appetite of farmers to increase the crop rotation dedicated to this crop.

- An average of 2.8-3 tons/hectare completely solves the cost calculation per hectare located at the level of 1,100-1,200 USD/MT.

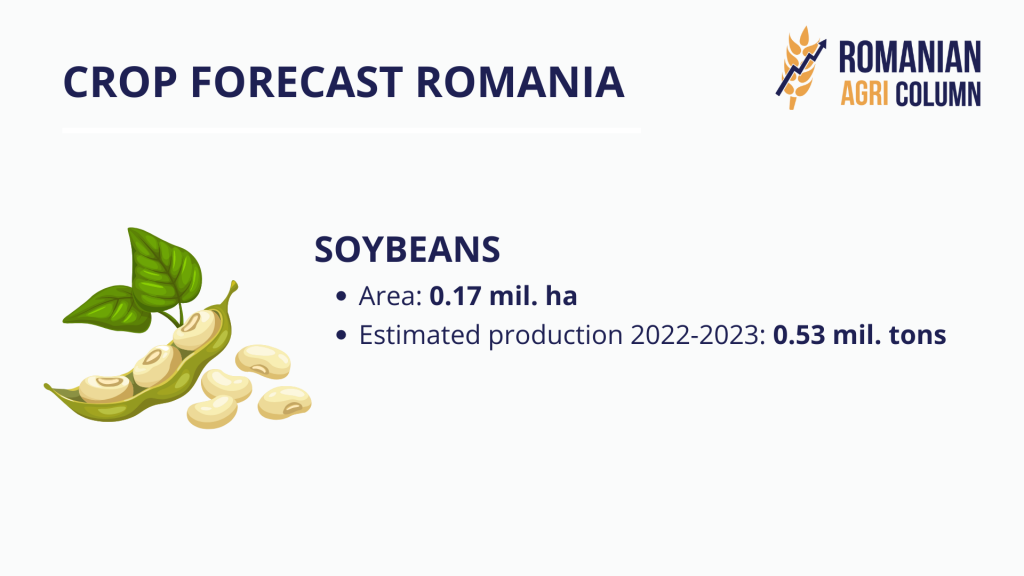

LOCALLY

As I said in the last issue, the local soybeans are no longer of interest to Romanian processors. Thus, they will be used in small processing units for the production of Full- Fat, with the help of extruders attached to the dairy or meat cattle business. The product resulting from extrusion is extremely high in caloric potential, so there is a niche that can be exploited in this context.

Locally, the soybean area indicates a level of 170,000 hectares with a projected production of 530,000 tons.

REGIONALLY & GLOBALLY

US maintains its 120-million-ton harvest level achieved in 2021-2022, but is lagging behind in exports. At the moment, US exports are 16% behind last season. The current level of exports to the United States is 46.6 million tons. Sowing continues in the United States. The percentage is increasing compared to the latest estimates, reaching the level of 8%. But last year, the level over the same period was 13%, and a multi-year average reaches 22%. However, there is enough time to recover the gap.

BRAZIL will complete the harvest of soybeans with a final level of 125 million tons. They are minus 2 million tons according to the USDA, and their export level is currently 77 million tons, with an estimated domestic processing of 48 million tons.

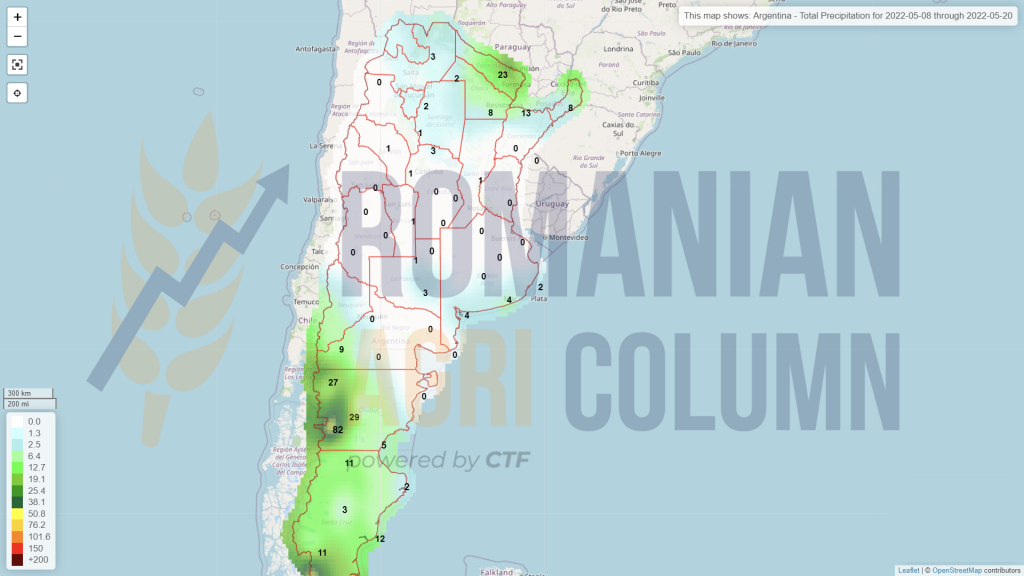

ARGENTINA raises the level of production in the harvest (42% harvested) by one million tons, reaching 41 million tons.

CHINA has an import level of 91 million tons in the marketing year 2021-2022, down from 9% last year so far. China also indicates an increase in soybean area for the 2022-2023 season by 17% year-on-year. The estimated production generates a level of 26% in addition to the 2021-2022 season.

As a global projection, 2022-2023 indicates a recovery of soybean volumes around 385 million tons, 10% more than in the 2021-2022 season.

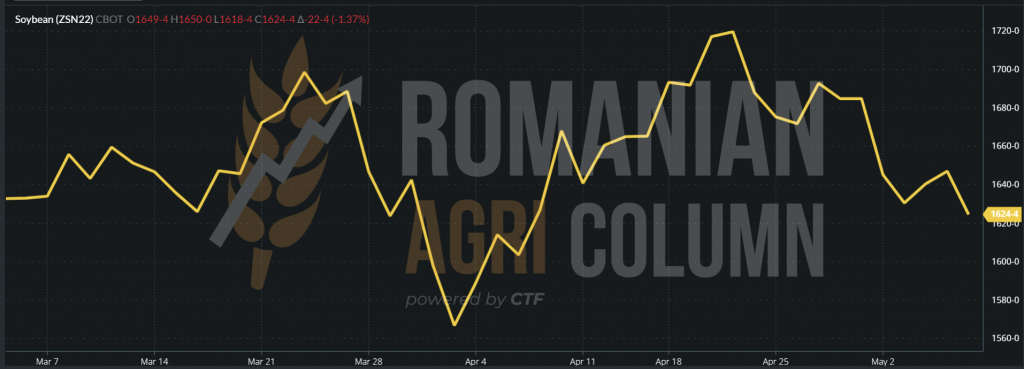

CBOT is in the same profit taking game. ZSN22 JUL22 – 1,624 c/bu (-22 c/bu)

GRAPHIC TREND SOYBEAN ZSN22 JUL22

ANALYSIS

- The decrease in soybean imports from China causes the decrease in the price of soybeans on CBOT.

- The growing forecast of soybean cultivation in China is having the same effect.

- The funds carry out Profit Taking and, in turn, lower the indications.

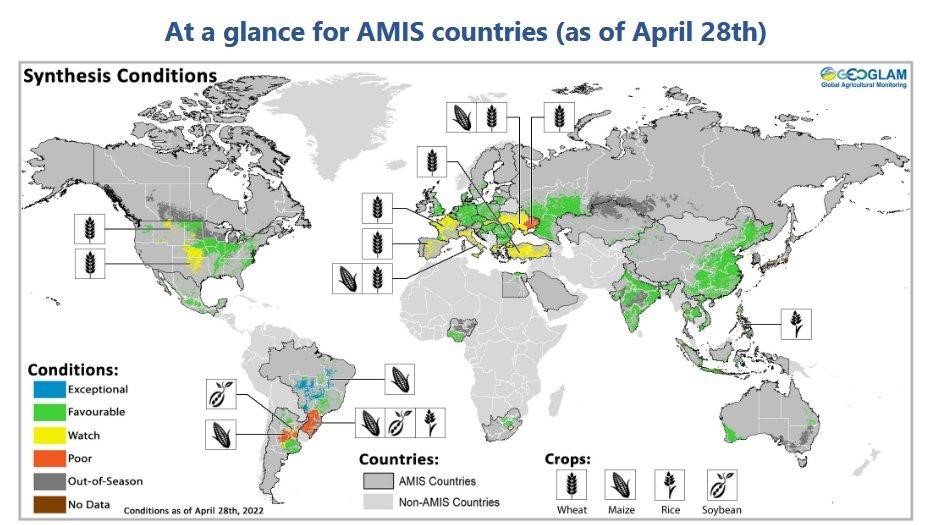

CROPS VEGETATIVE STATE

We conclude the analysis of the commodities with a satellite image generated by Geoglam, which indicates a favorable vegetative state of Romania at the moment.

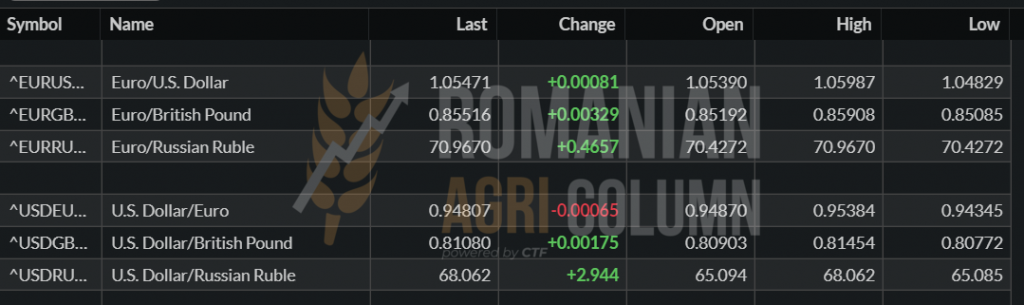

EUR/USD 1: 1.054 | USD/RUB 1:68

WTI and BRENT oil quotations

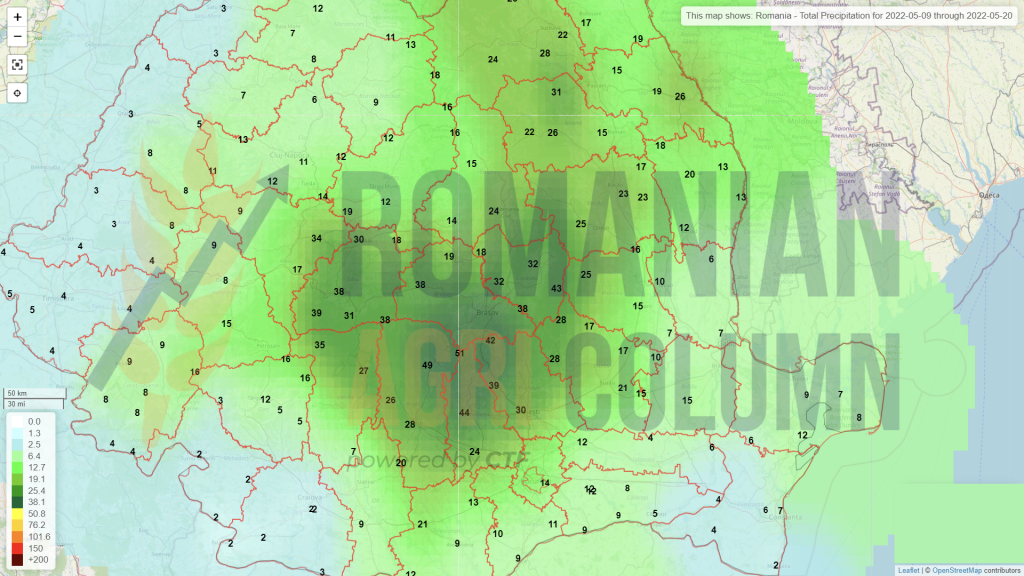

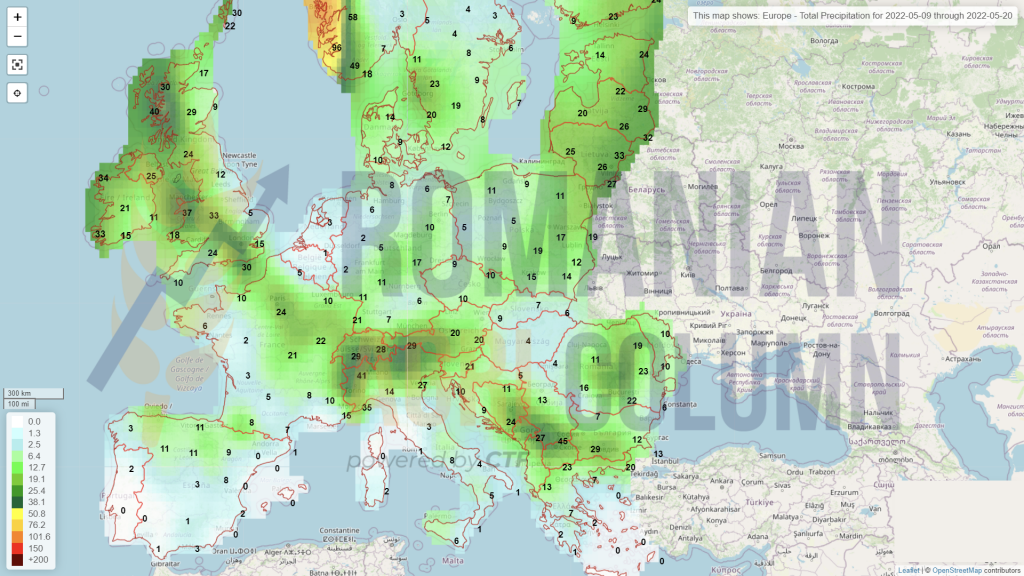

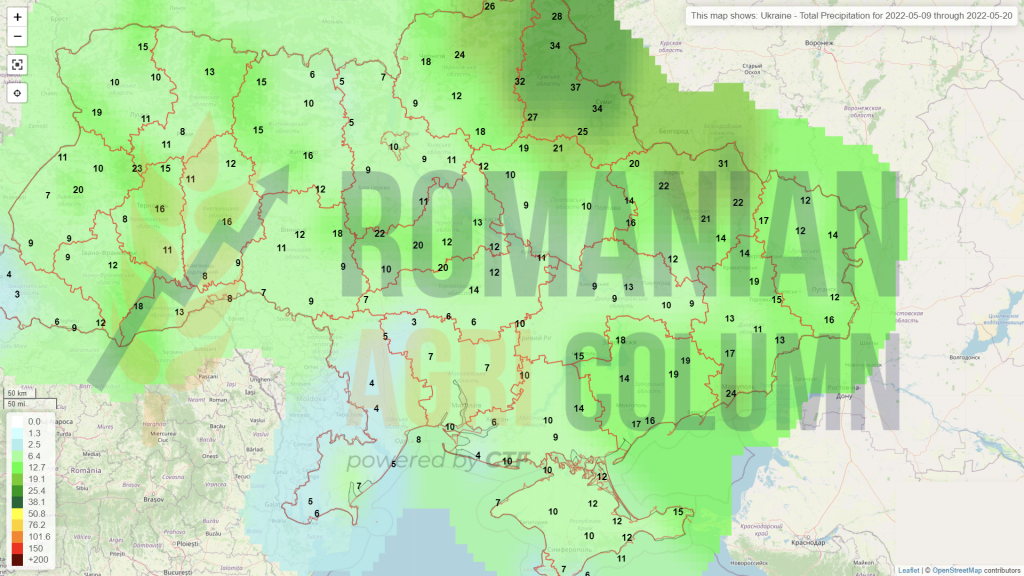

9-20 May 2022

Romania

Europe

Ukraine

Russia

Canada

USA

Brazil

Argentina

Southern Black Sea

China

Australia