This week’s market report provides information on:

|

Wheat market

The price of wheat in the port of Constanța received a boost of 5 EUR/MT, reaching the level of 285 EUR/MT in the CPT parity. The price of feed wheat is 10 EUR/MT lower. Inland, the prices offered by processors have reached the level of 273-275 EUR/MT FCA Farms.

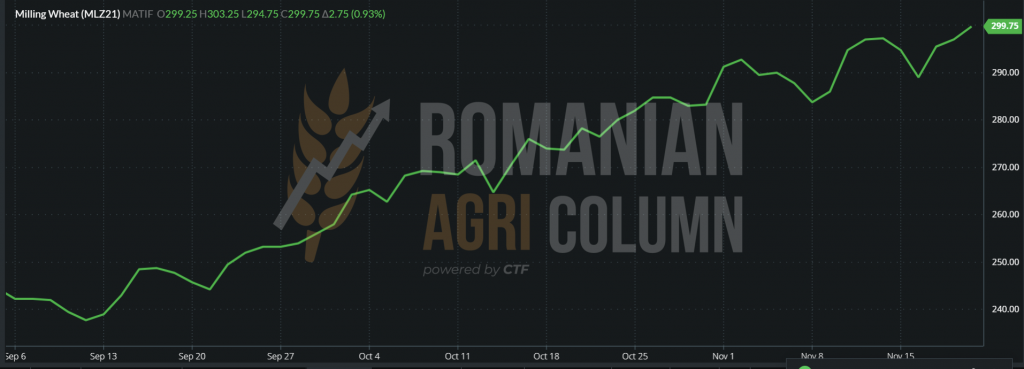

The fundamentals of the market have not changed, so EURONEXT generated indications of over 300 EUR in the trading session of 18 November 2021. In the right corner, top line, we have HIGH 303 EUR, MLZ21 from November 19, 2021, closing at 299.75 EUR.

EURONEXT: GRAPHIC TREND MLZ21 (November 18, 2021)

Wheat keeps generating tender, one after the other, as follows:

- OAIC Algeria tender concluded with the purchase of 750,000 tons, of which 250,000 originated in Russia, at an average price of 383 USD/MT, C&F parity.

- TMO Turkey goes out to auction for 385,000 tons of wheat on November 25, 2021.

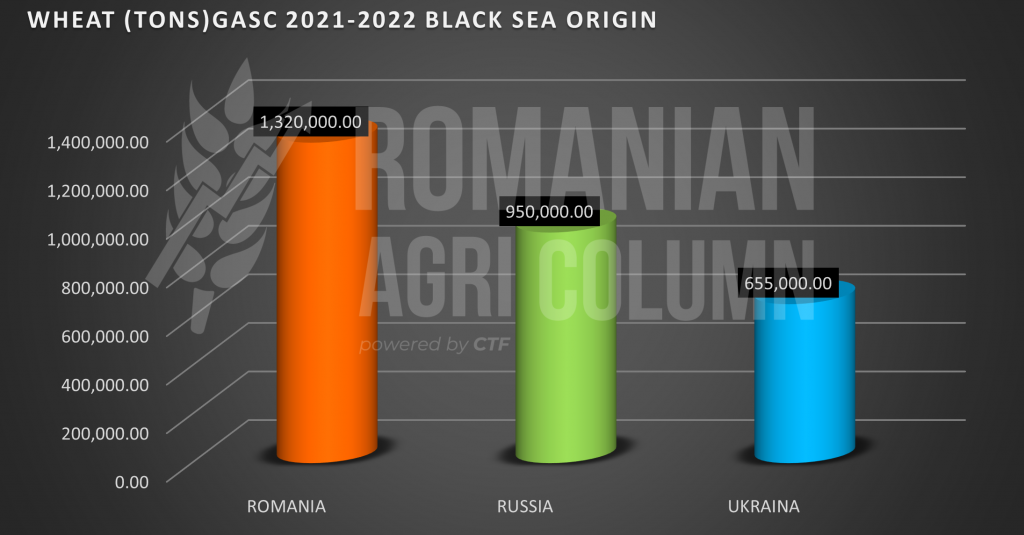

- GASC purchased a single batch of 60,000 tons of wheat of Romanian origin, at the price of 371.97 USD/MT CIF (346.97 USD/MT, FOB Constanța).

In total, we have a volume of 1,195,000 tons of wheat that moves from origin to destination, which decreases the supply in the countries of origin. Remaining a little in the GASC auction area, we must note that the price of wheat in the FOB Constanța parity is according to the EURO/USD parity, of 1: 1.133, at the level of 306 EUR/MT. By decreasing the auction costs, the fobbing, financial and storage costs until delivery, plus the exporter’s margin, we reach a level of 291-292 EUR/MT CPT Constanța. It is a difference of only 7 EUR/MT, let’s say, compared to what the port offers today.

With this lot sold to GASC, Romania consolidates its leading position as origin (Romania leads the Black Sea pack) in terms of wheat sales in this destination through GASC in the 2021-2022 season, with a cumulative total of 1,320,000 tons. Russia and Ukraine are currently in the next places.

European analyzes indicate a decrease in the use of feed wheat within the EU in favor of maize, due to the price difference. A very correct estimate by the Strategy Grains agency positions French wheat at 70% feed quality and 30% milling quality. Therefore, in the context of the existence of an alternative for industrial and feed use, the consumption of feed wheat could be reduced, given the replacement costs.

But in the Black Sea basin, the support is in place and the milling wheat continues to enjoy the same confidence and demand. Is it possible to go above this level? Certainly yes. We see in the transactions of the BSW stock exchange indications at the level of DEC21 that easily reach 350 USD, while MAR22 is traded at 364 USD.

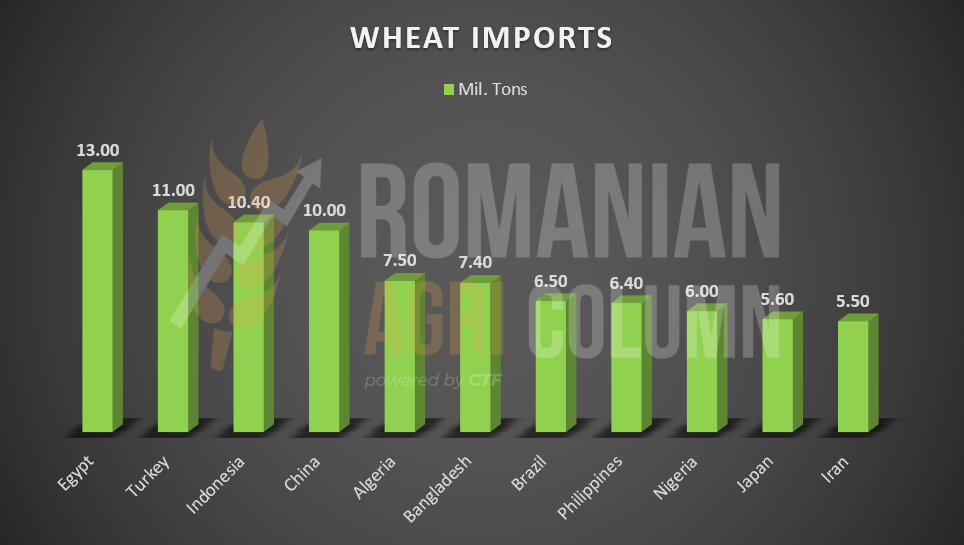

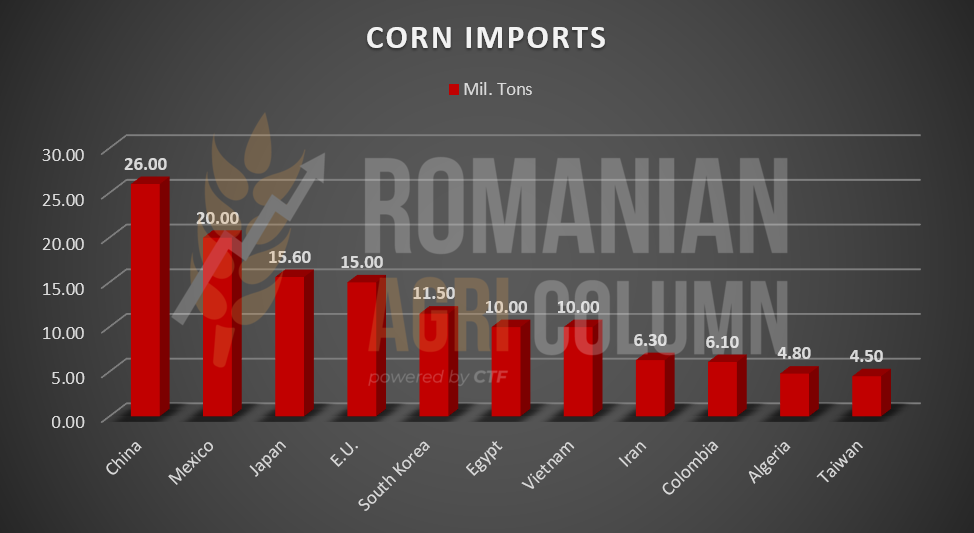

The Black Sea Basin once again shows its importance in supplementing wheat destinations, this social element essential in feeding humanity. For a good visual effect, we will insert a chart containing the main destinations that are supplied from the Black Sea basin, as well as their import levels.

In Russia, the status of winter wheat indicates a gap of at least 0.9-1 million hectares between the sowing plan and the level achieved. Russian wheat is already in a combined stress, water and heat, generated by the lack of rainfall, along with the appearance of very low temperatures. However, we also notice snowfalls in the Russian middle region from west to east, so that part of the sown wheat benefits from protection against the cold. The estimates of the Russian crop are on a very large gap, between 75 and 84 million tons. Nothing worth considering yet. Russia can recover in the spring by sowing wheat on the remaining area.

Ukraine is also having difficulty sowing and the window has already closed. Ukraine therefore remains with only 6.2 million hectares sown, out of an estimated 6.7-6.8 million. Water stress is also present in Ukraine. The lack of rainfall has caused problems and preliminary estimates already show a decrease in production from the two factors combined, smaller area and water stress, from the 32 million achieved this season to 27 million tons next. But it is too early to say. We have just passed the middle of November 2021. Many things and events can happen.

Romania has already reached the level of 2 million hectares sown, out of a total of 2.15 estimated and our assumptions are that by November 25, the remaining 150,000 hectares to be sown will be achieved. The vegetation condition of the wheat is in optimal conditions at this moment, the rainfall and the mild weather favoring its development.

At European level, we have a total indication of 21.6 million hectares sown with wheat:

- France – 4.9 million ha

- Germany – 2.9 million ha

- Poland – 2.4 million ha

- Romania – 2.15 million ha

- Spain – 1.8 million ha

- Bulgaria – 1.2 million ha

These countries are the main exponents of European wheat cultivation in terms of area size. The United Kingdom also indicates an area identical to that of the previous year, of 1.8 million hectares.

On the other side of the Atlantic Ocean, American wheat sales do not excel. In the previous week, their reports indicated a delay of 21% compared to the same period last year.

However, regarding the planting of American winter wheat, it reached the level of 94% of the estimated 18.9 million hectares, with a ratio of 81% sprouted and 46% in good to excellent condition. The conditions are promising for American wheat crop.

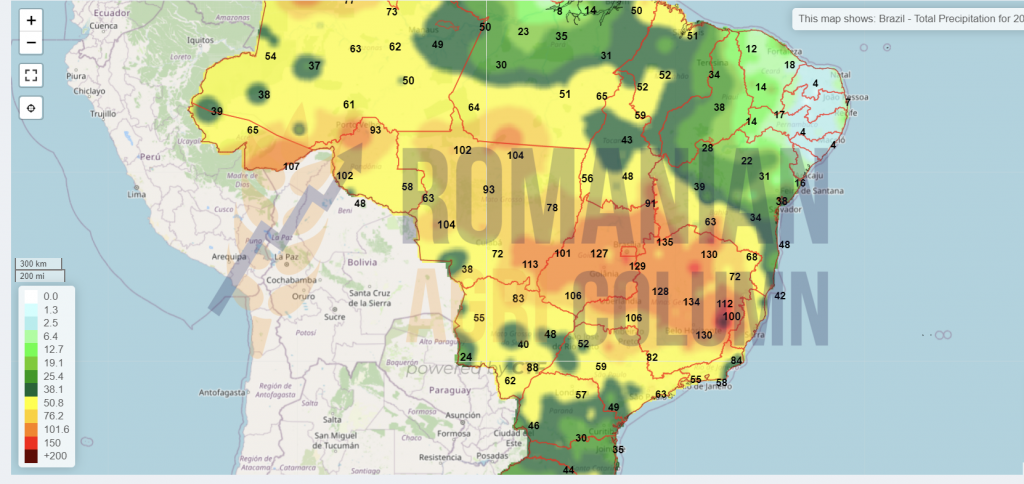

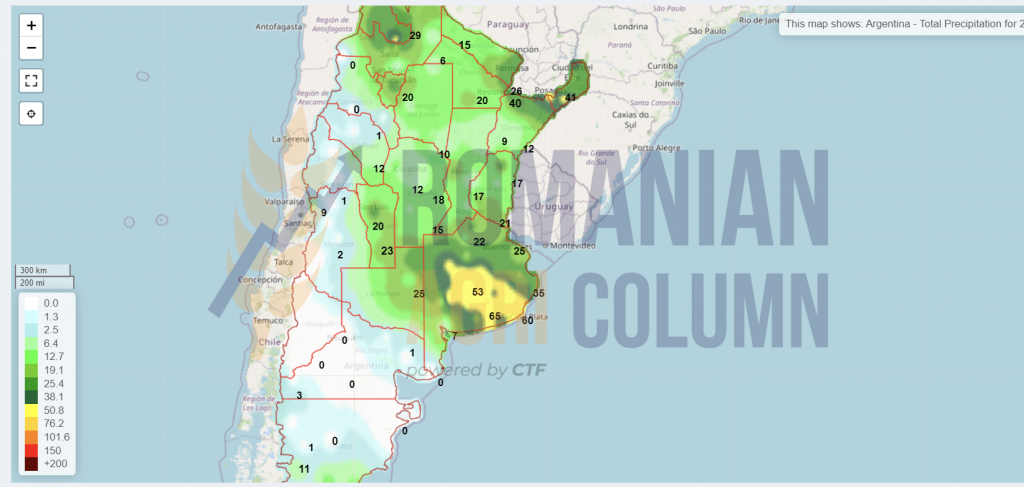

Argentine wheat indicates a harvest estimate of at least 19.5 million tons, and Brazilian wheat 7.8 million tons.

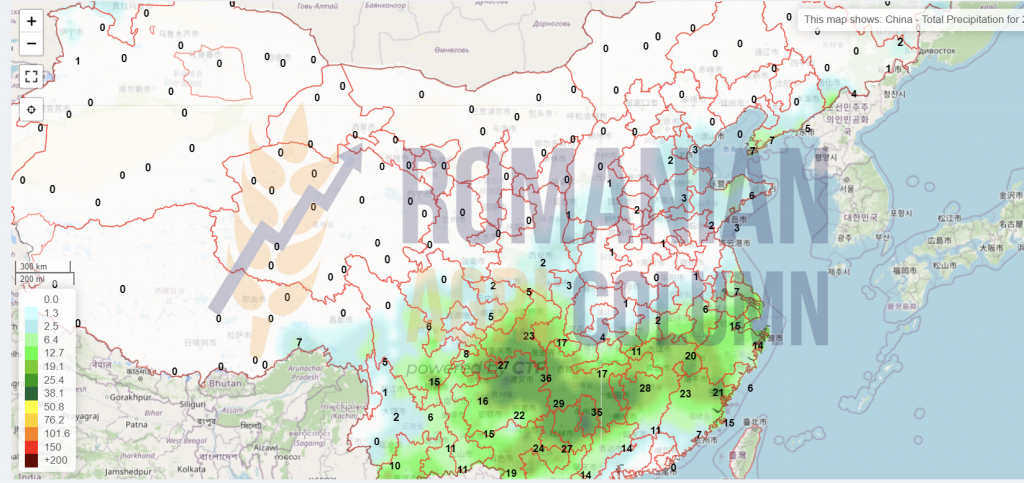

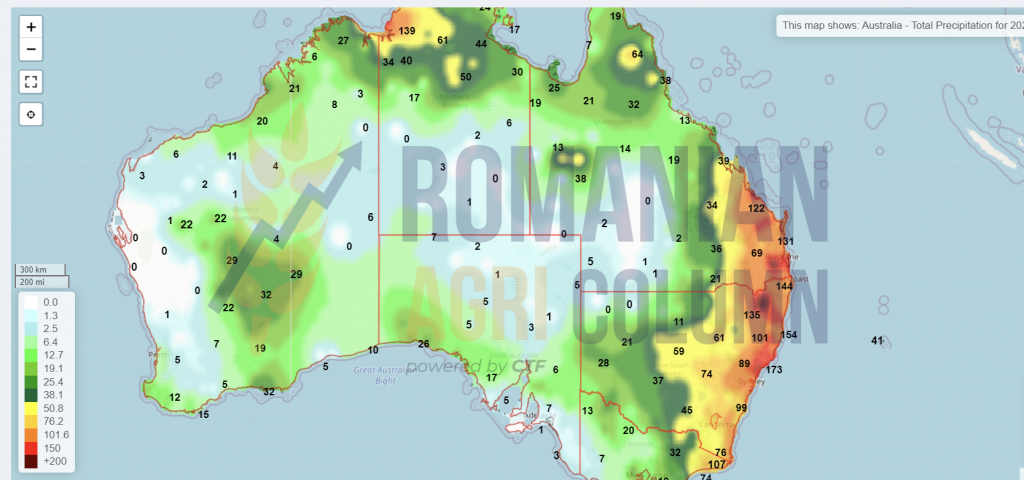

China’s wheat production is reflected in the level of 137 million tons, that of India of 106.5 million tons, and that of Australia of 32 million tons, but in this origin, rains and floods will certainly penalize the quality.

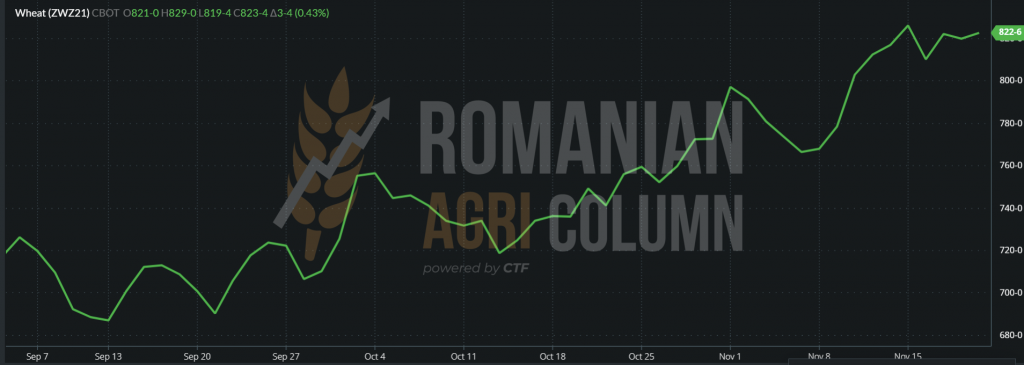

CBOT indicated at the opening on November 19, 2021 a level of 823 c/bu, i.e., 305.7 USD.

WHEAT CBOT ZWZ21 TREND GRAPH

But what should not be neglected is the fact that in the case of both stock exchanges we have DEC21 indications, and it will move towards MAR22 in both cases. So, on November 22, we will start to see liquidations of positions and roll-over for MAR22, which could create some turbulence. Also, this week, between November 25-26, Thanksgiving Day takes place, a specific US holiday, which will keep the North American market closed. And at the beginning of next week, on November 30, there will be a Christian holiday common to Catholic and Orthodox rites, so it will be the turn of the European market to be closed.

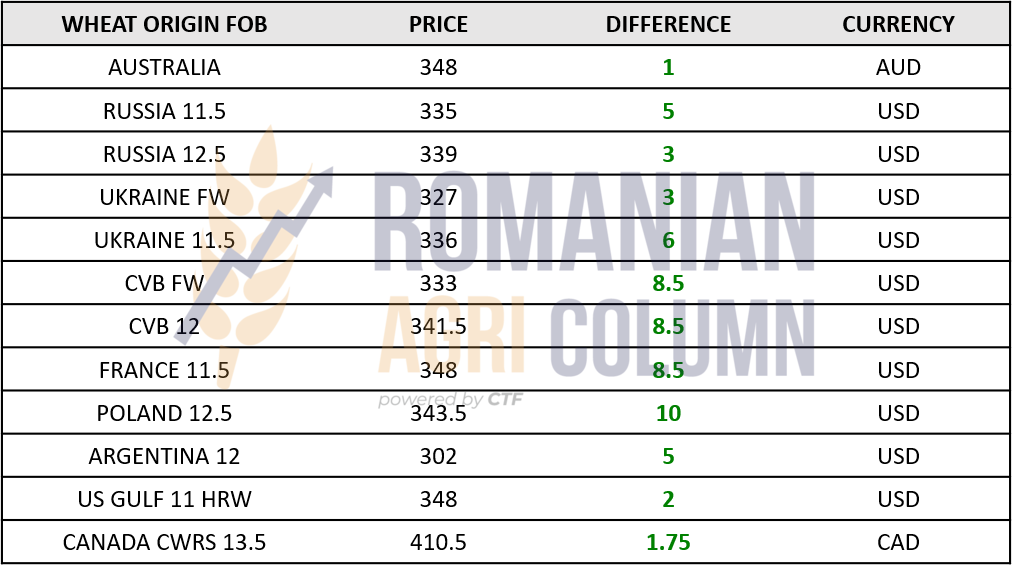

GLOBAL INDICATIONS FOB ORIGINS

ANALYSIS

- Demand is high for milling wheat. 1,195,000 tons will be auctioned until November 25

- The traction of wheat on corn is visible. The Euronext spread is about 50 EUR.

- BSW indicates 350 USD DEC21 and 364 USD MAR22, which indicates confidence in the robust demand for wheat in destinations.

- There will be a quiet period due to the end of November holidays, which will take place in North America (November 25-26), as well as in the Christian world (November 30).

Barley market

The indications of the feed barley acquire consistency and we note the increase of the indicative quotations to the level of 245 EUR/MT in the parity of CPT Constanța. The upward trend is due to increased demand from Turkey, as well as a negative balance of production and consumption of about 4 million tons globally. Of course, the feed wheat also has its contribution in this growth, effectively pulling after it the feed barley in the replacement scheme in animal feed.

Turkey has launched a tender for the purchase of 370,000 tons of barley, exactly in the context specified above, which will take place on 23 November 2021. In the next issue, we will present the result of the tender, but we believe we will see an improvement in the price of barley in the port of Constanța, in this context.

The indications of the Black Sea basin show a level of 298 USD/MT FOB Russia, equivalent to 262 EUR/MT. In this quotation, we estimate that the port of Constanța could easily raise the level up to 250-253 EUR/MT in the CPT parity, but since barley is not a commodity that sells in large volumes, the exporter’s margin is much higher than in the case of wheat, for example.

Australian barley has an indication of 283 USD/MT and the level is static, without positive progression.

Regarding the 2022 crop, we see the following areas sown in the fall of 2021, to which are added the areas that will be sown in spring with barley.

Corn market

The indications of maize in the CPT Constanța parity remain firm, at around 240-242 EUR/MT. However, we note problems with the humidity of corn, which has more and more consistent values, reaching up to 19% compared to a standard of 14.5%.

Despite the goodwill of the exporters, the humidity level at the reception is very high and the dryers installed in the export terminals do not cope. We see, therefore, many transport units rejected once they exceed the level of 19% humidity.

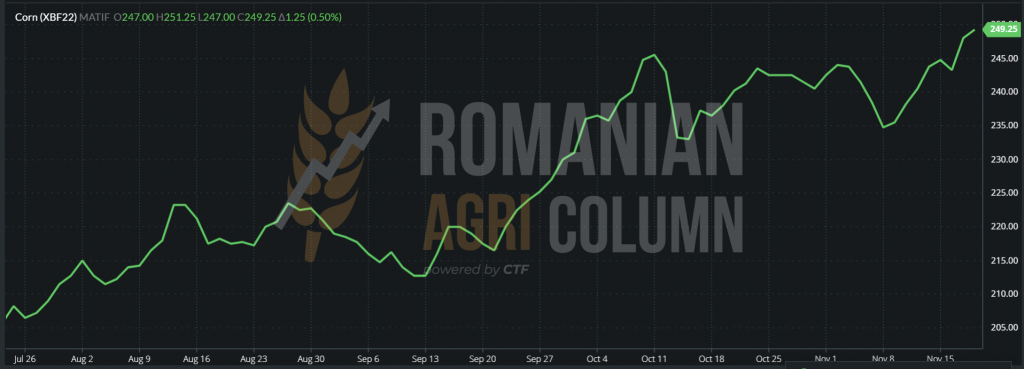

In the European stock market plan, we see how the corn finds support and traction, so that the indications for November 18, 2021 are at the level of 249.25 EUR, after during the trading day, the level of 250 EUR had been exceeded. The Euronext basis is reflected within normal limits in the physical market, in the port of Constanța, in the context in which production is higher than consumption. BASIS minus 10 EUR = 240 EUR.

EURONEXT XBF22 – 249.25 at the close of November 18, 2021

EURONEXT XBF22 CORN GRAPH – the trend is increasing compared to November 9, 2021, the date of the USDA report

Harvesting continues in Romania, the northwest, northeast, and the center of the country being in full swing at this time.

Nevertheless, the American market has its problems, which we know all too well at the moment and we recall the very slow pace of exports to China. At the same time, Mexico reached a level of almost 18 million tons of corn imported from the USA. In terms of harvest level, the USA is at 93%.

The center of interest at the moment is in the Black Sea basin and, more precisely, in Ukraine. Here things get a special consistency, which makes China supply itself in very large quantities. The USA wonders why China does not come to buy goods, preferring the Ukrainian origin.

However, the support in the price of Ukrainian goods also comes from the adjacent drying costs, which are included in the price of the goods. According to estimates generated by local Ukrainian sources, the crop is extremely rich and goes to the level of 40 million tons. But things are not as they seem, because the goods come with very high humidity and, if we release a number of 7.2% humidity in addition to the standard, we get only 37 million tons of corn. So the support in the price of goods in the basin comes from excess moisture, as well as from what we already know, namely better logistics than the US GULF.

If we add the industrial demand in the USA, in this case ethanol, which has very low stocks and therefore requires corn, as well as the printed traction of wheat, we no longer support the degradation at the level of 230-233 EUR/MT that we saw for some time and that was practiced by most buyers from the port of Constanța (except for a very strong one, which stood at 240 EUR/MT).

According to our assessments, corn will follow the wheat route, but at a much slower pace. The traction of wheat, the industrial demand, the drying costs make it not to suffer a degradation, but even to gain serious ground in this context. In addition, the moisture that will be extracted will generate a lower level of crop in European and Ukrainian origins, so that in the next USDA report, we will be able to see negative volume corrections.

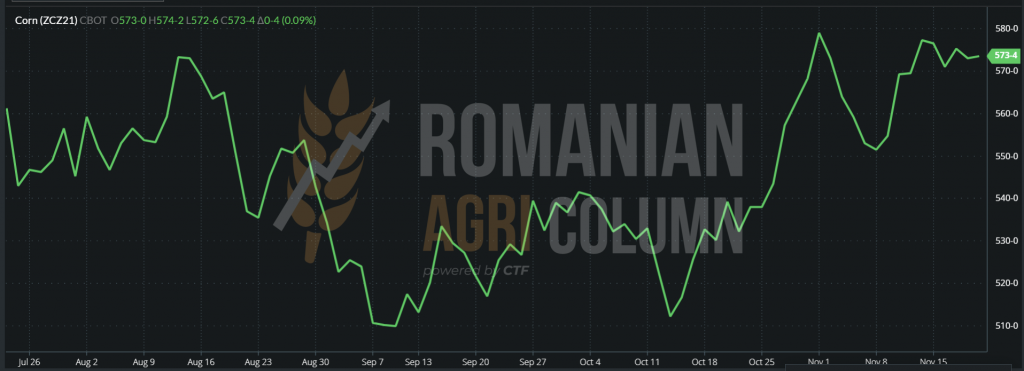

CBOT reacts in this regard and the indications it generates are at the level of 573 c/bu, i.e., 225.58 USD for ZCZ21 – DEC21. But let’s not forget two things:

- from November 20, the funds will start liquidating the positions, as well as the roll-over on the indication MAY22

- Thanksgiving Day is fast approaching and US markets will be closed from November 25-26.

CBOT ZCZ21 -DEC21 TREND

For a better representation, we insert a graph of the countries with the highest degree of corn imports:

ANALYSIS

The traction of corn is generated by:

- US industrial demand (ethanol)

- Drying costs generated by goods with higher humidity

- China supplies itself from Ukraine

- Wheat, which supports corn

- The price in FOB CVB remains at the same level of 250 EUR/MT, Ukraine at 274 USD/MT FOB

Rapeseed market

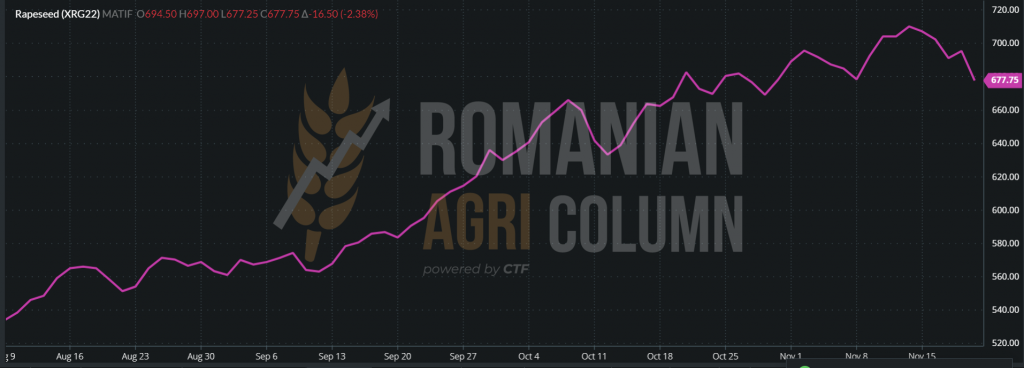

As usual, rapeseed has ups and downs. The last drop from 708-710 EUR/MT (Euronext) was generated by the declining level of fossil energy, the demand for rapeseed oil in the FOB Rotterdam parity, as well as the generation by investment funds of a “profit taking” simultaneously with the other goods on the stock exchanges.

We recorded the level of 677.75 EUR, decreasing by 16.5 EUR, at the end of the session of November 19, 2021. XRG22 = EUR 677.75 EURONEXT

We also note the crop inverse, which remains at the level of 110 EUR, in direct comparison with AUG22 (567.75 EUR). The new season is still far away and the estimates of the new crop are only at the level of planted areas. In this context, however, we have clear indications, as follows. EURONEXT XRG22 TREND – November 19, 2021

JAN22 CANOLA has exceeded the level of 1,015 CAD in trading at HIGH level (top right image), a sign of lack of liquidity at commodity level. It is obvious at this time, when the Canadian crop did not exceed the level of 14 million tons, compared to the 21 initially estimated.

Closing of November 19, 2021 – 1,005 CAD, decreasing by 9 CAD.

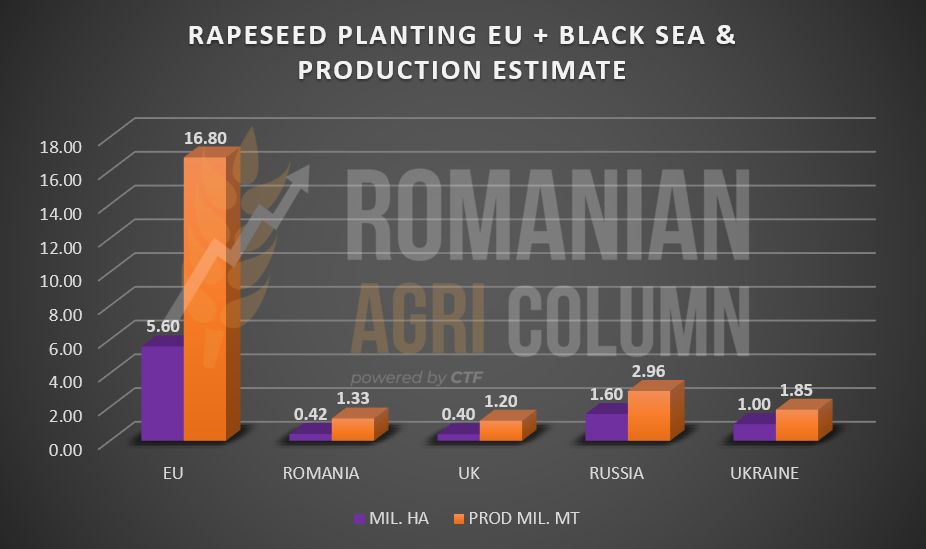

For rapeseed, we are already moving into the 2022 crop estimates and we observe the following planting statuses at European level, in Great Britain and in the Black Sea basin, in this case, Russia and Ukraine. We insert the chart with the sown areas and the estimated yields based on the productivity of 2021. Of course, what follows will depend on the weather, but we have nominal indications on each region about planting and production estimation.

We therefore have, at EU level, a planted volume of 5.6 million hectares, with an estimated production of 16.8 million tons, Russia of 1.6 million ha and a production of about 3 million tons, and Ukraine, with 1 million ha and 1.85 million tons. We also detached Romania, with about 420,000 hectares and an estimated production of 1.33 million tons and we are already looking at the end of February, when we will understand what really comes out of winter, when we will see how many hectares have withstood.

Sunflower seed market

As we said in previous issues, the degradation will stop and the price of seeds will increase. But time has taken us forward and we see how the price has started to rise. At the level of CPT Constanța, the indications are at the level of 660 USD/MT.

However, according to our information, the price level for sunflower oil in Ukraine has started to rise and we see an indication for CSFO of 1,410 USD/MT FOB, increasing by 22 USD/MT.

This increase is not accidental. Our estimates of the volume of the Ukrainian crop were not wrong. It was lower than the initial level. Ukraine therefore closes at 15 million tons, compared to 15.5 million tons initial estimate. Moreover, the price of sunflower seeds in Ukraine increases to a level of 20,000 UAH/MT, equivalent to 755 USD/MT, from which we extract 20% VAT and results in 630 USD/MT.

However, in this condition, Ukrainian farmers are not satisfied and the volume of sales is very low. It is at a level of 34%, while the average of the last 5 years reached 52-53% during this period. In this situation, processors face a first problem, because they have nothing to process. The processing program included a three-month stock, but at this time, they have raw material for only one month. Indeed, they are forced to reduce the production margin, the so-called crush-margin, and to pay higher prices on the goods, just to have them.

In addition to the above, we note the growing demand for crude oil, which puts additional pressure on its price. Russia, with the export tax raised to the level of 276 USD/MT, cedes its origin in Ukraine and thus, the latter becomes the main preference in origin.

Moreover, the FOB CVB indication increases to the level of 708-710 USD/MT, which, translated in the CPT Constanța condition, should be equivalent to 690-693 USD/MT, visibly differentiated from what we see today as the primary indication.

Like Ukrainian farmers, however, Romanian farmers want a much higher price level than what is offered today, being aware of the importance of goods and their volume limit. The beginning of December could therefore bring earlier the levels we estimate, namely 710-720 USD/MT in the parity of CPT Constanța or DAP Processor.

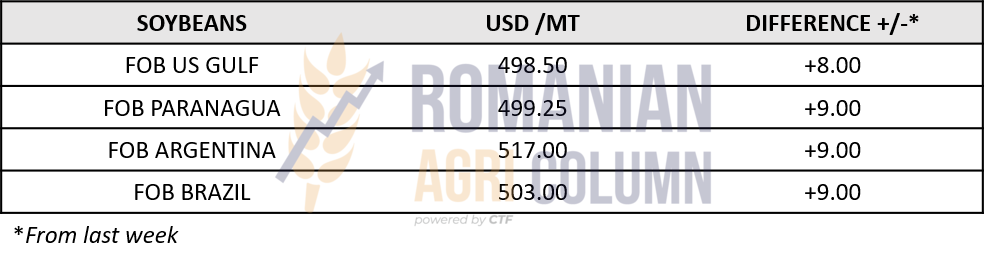

The soybean market

In Romania, last week’s levels are maintained (620-630 USD/MT), with a very low appetite of local processors. The purchases will be made in the short term and then will reduce the level of the purchase and, implicitly, of the price.

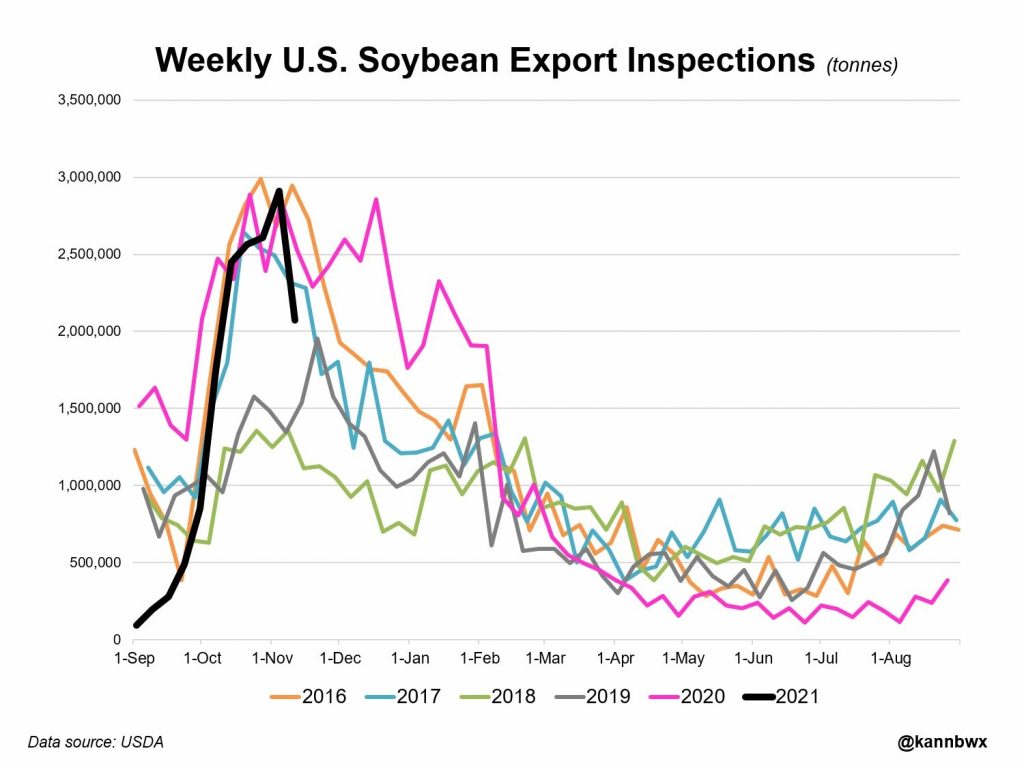

Soybeans maintain last week’s trend, which is slightly higher than the USDA report. The difference is visibly growing, fueled by US export transactions. In week 45, we noted a level of 2.9 million tons, for which the export inspection from the USA was requested. However, the level is visibly declining compared to previous years.

We insert a comparison, source Karen Braun, @kannbwx. After reaching the peak of 2.9 million tons, we see the decrease through the black line. In total, compared to last year, the American export of soybeans has a minus of 33%.

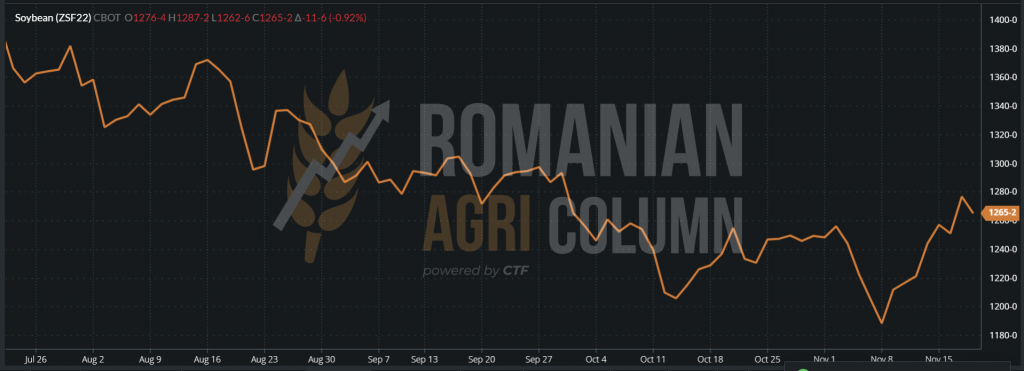

CBOT falls sharply, after rising to the level of 1,280 c/bu due to the profit-taking action of hedge funds, which clearly signaled distrust in soybeans.

CBOT – closing on November 18, 2021 – 1,265 c/bu = 464.8 USD

The indications from the main origins, North and South America, are increasing, with an average of 9 USD/MT, a sign that the CBOT trend is following and that there is constant demand.

CBT ZSF22 SOYBEAN TREND – JAN22 at the closing of November 18, 2021

In the US, the soybean harvest has reached 92% and we estimate that in about a week, it will end. Argentina and Brazil are under planting and maintain their estimated levels of 49.5 million tons and 142 million tons respectively, indicating an aggregate level of the three major origins of 311.5 million tons. China will consume 100 million tons of this volume.

China, on the other hand, has a shortage of soybeans, which reduces domestic stocks and thus reduces processing activity. In November, import forecasts reach the level of 8 million tons expected to arrive.

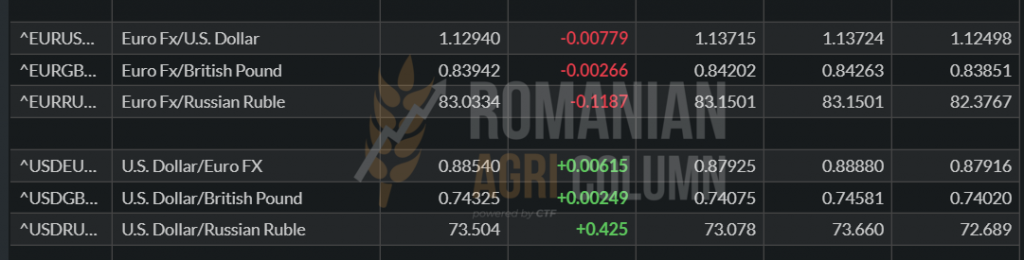

EUR-USD parity

USD strengthens strongly against EUR – 1: 1.1294

Fossil energy

We notice a calming of the BRENT and WTI indications, which drop below 80 USD/barrel

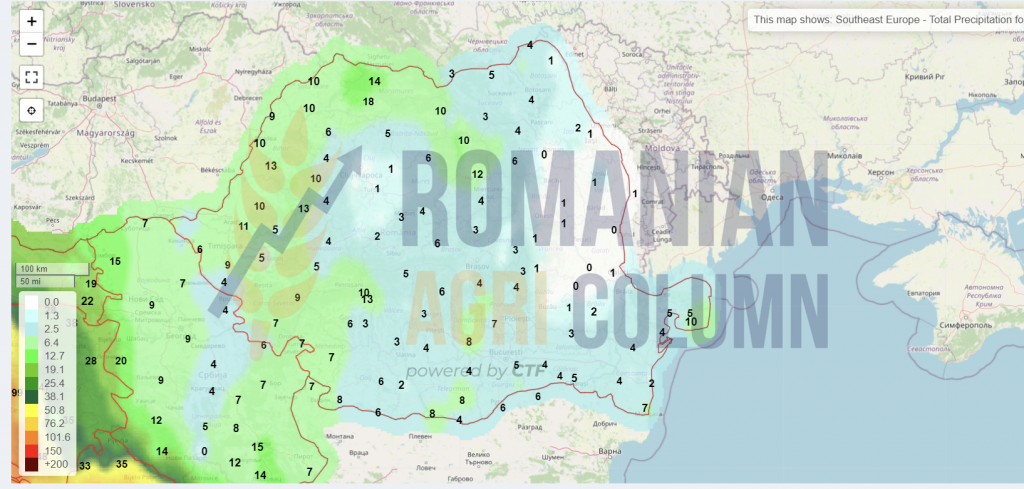

Weather forecast

19-28 November 2021

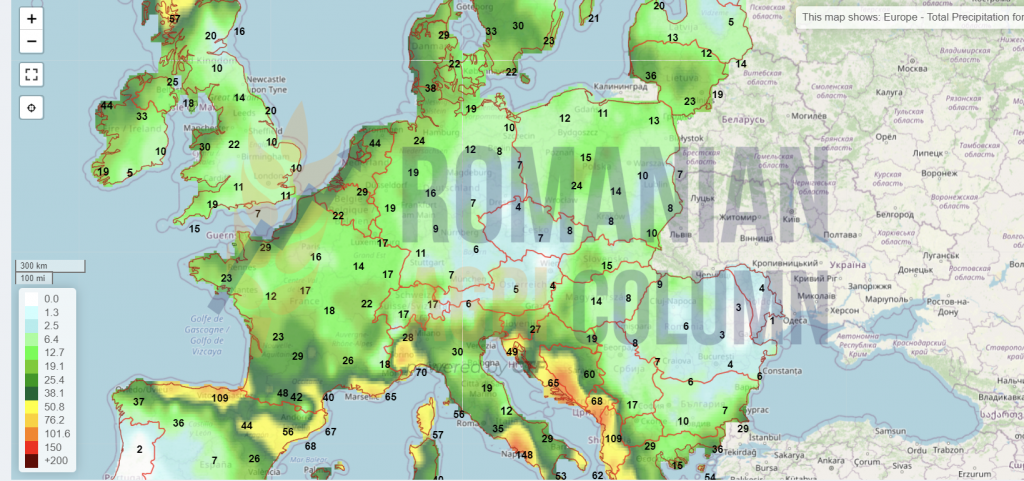

Romania

Europe

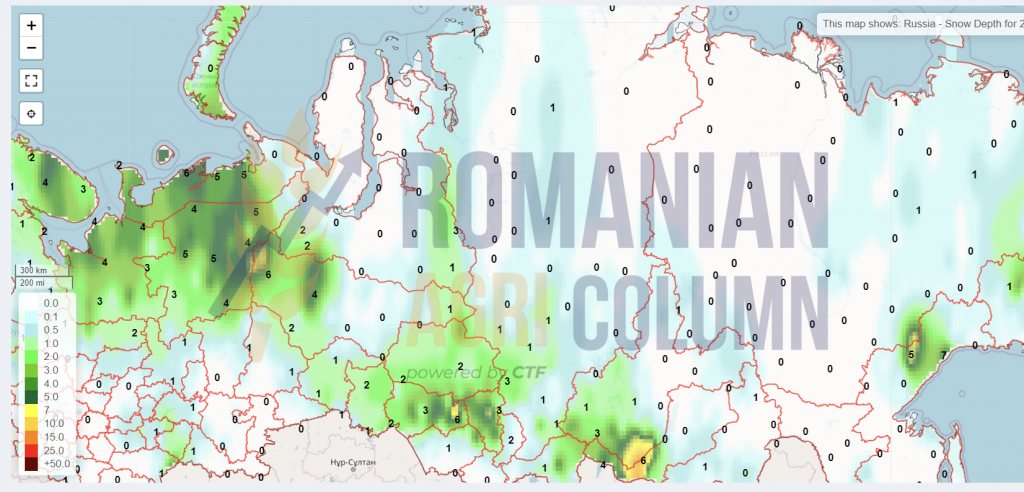

Russia (snow)

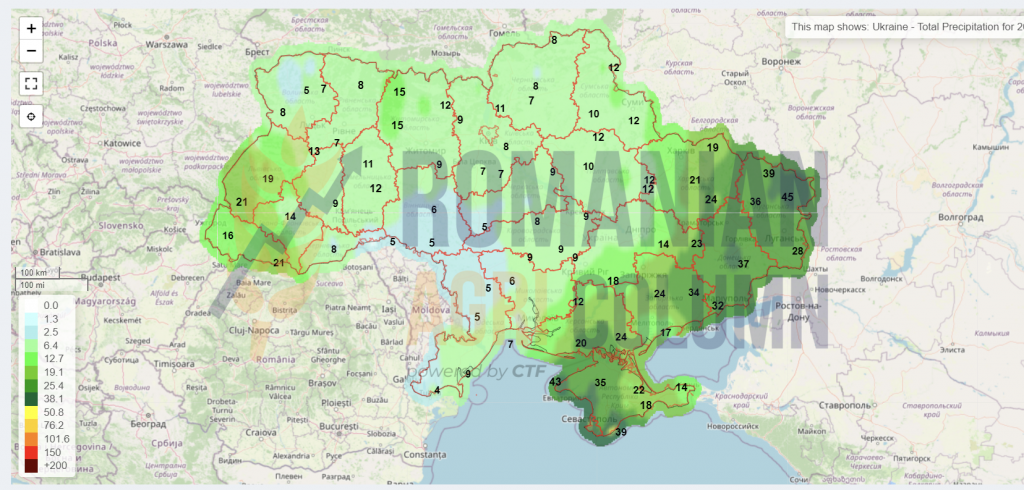

Ukraine

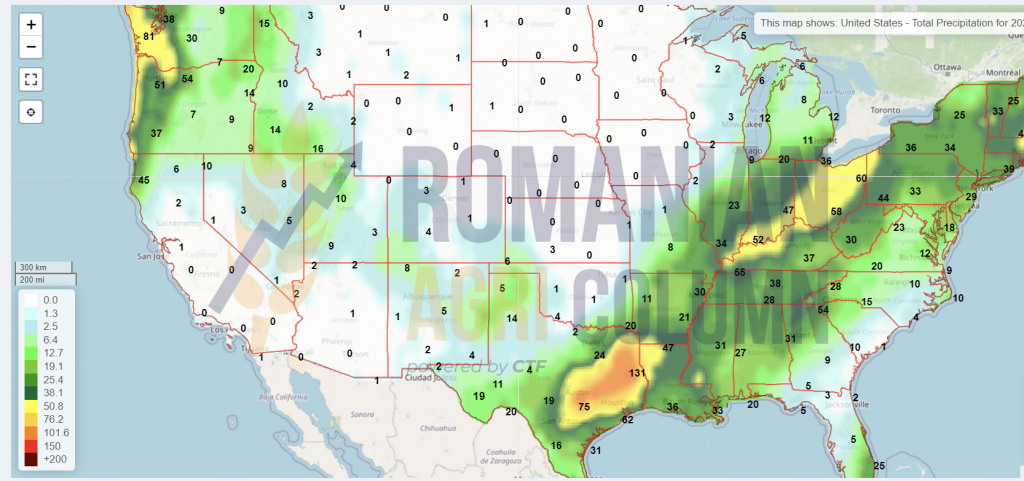

USA

Brazil

Argentina

China

Australia

© Romanian AGRI Column, 2021, all rights reserved