|

Today we publish the 50th analysis report of the agribusiness market and we conclude, together with it, the year of 2021. Thank you for all the trust with which you have honored us throughout this period and for the interest given to our analyzes. After an eventful 2021 in agribusiness, we wish you Happy Holidays! See you on January 10, 2022, when we publish a new report. See you soon, Romanian AGRI Column Team |

This week’s market report contains information on:

- Wheat market

- Barley market

- Corn Market

- Rapeseed market

- Sunflower seed market

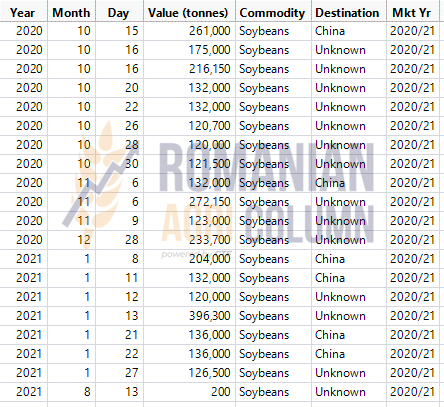

- The soybean market

- Constanța Port line-up

- EUR-USD parity

- Fossil energy

- Weather Forecast

Wheat market

Following the announcement made by the US Federal Reserve about the state of inflation and the levels of monetary policy that will be exercised during 2022, the markets have panicked and we are referring here mainly to Euronext and CBOT. As if anticipating the announcement, the problem was not whether, but when the US monetary policy would change, the two stock exchanges actually turned red. The largest decrease was in wheat, the American market registering a decrease of 31 c/bu, i.e., 11.4 USD. At the same time, the Euronext trading session closed down by more than 8 EUR, anticipating the effects of the Federal Reserve announcement.

The port of Constanța closed on Friday, December 17, 2021, in a static level determined by the state of uncertainty amid the Federal Reserve announcement, the displayed level being set at 271-272 EUR/MT.

The price of feed wheat quality is 11 EUR/MT, which is due to the higher volumes displayed by France and Australia in this respect, which has impacted the level at regional and, of course, global level.

Wheat buyers from the Black Sea basin are showing the same indifference these days. The difference between the level they want and the price request for the goods, i.e., BID and ASK, is 4-5 USD/MT. This is reassuring when it comes to purchases in the Black Sea basin.

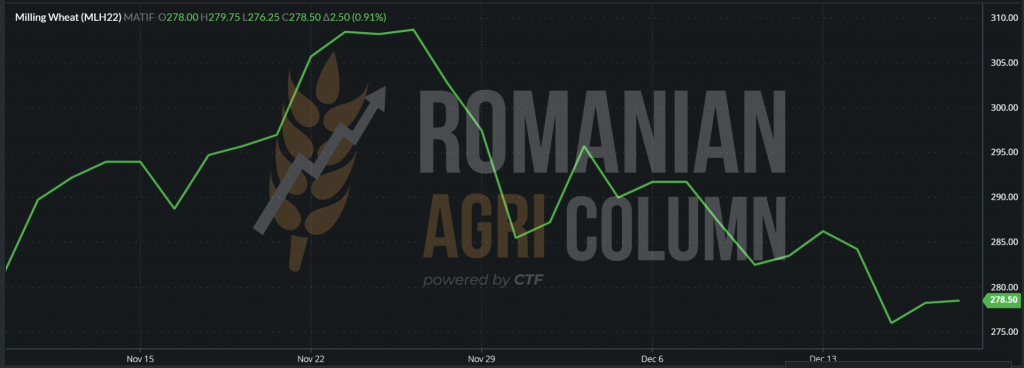

Euronext closes the December 17, 2021 trading session on the rise after the devastating effects of the US announcement on wheat prices. Thus, we see an increase of 2.5 EUR compared to the opening, a sign of recovery, given the fact that in the physical market things are anticipated.

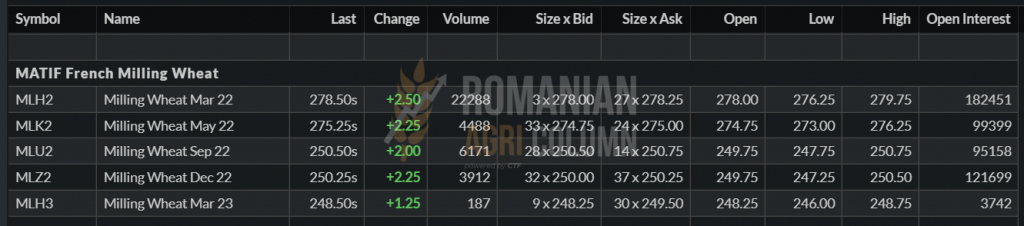

EURONEXT MLH22 closing of 17 December 2021 – 278.5 EUR:

We see how from a few elements demarcated by a short window of time, the price of wheat is degraded in consecutive stages. Between 7 and 15 December 2021, wheat indications were altered by panic induced by the possible effects of Omicron and the WASDE report, which made corrections to crop levels in some parts of the world.

During all this time, we have generated the urge to sell to Romanian farmers, in the media and in appearances on TV channels. Our hope is that many of them have understood and solved the problem of wheat stocks by selling the stored quantities.

EURONEXT MLH22 – to be watched December 7-17, 2021

But things are starting to get complicated, to get mixed up in the crucible of information and the effects of the weather. We live influenced by supply and demand factors, weather, political factors and the effects of investment funds, which move stocks through buying and selling actions (here also called trading algorithms that act in the context of aggregate supply and demand effects, weather, political factors and information).

What we see today and what we project next is a complex scenario, with effects that will manifest in a period of 15-25 days from now on. So let’s start by exposing the data:

Russia and Australia together bring in a surplus of 3.5 million tons. Argentina will bring an estimated surplus of at least 700,000 tons to 1.7 million tons of wheat. This will be reflected in the WASDE report of 9 January 2022, together with the NASS report, which will be released subsequently.

We therefore have a level of up to 5.2 million tons in surplus, which will release from the balance of PRODUCTION-CONSUMPTION up to the level of -4.5 million tons. The impact is great, because we set off with a deficit of 12 million tons.

Russia’s actions in the basin indicate to us practically exactly a bearish factor, i.e., a decrease in the price of wheat. Their attempts to lift the market are clearly anticipated by analysts and are not taken into account by trading algorithms. We note here, in addition to the increase in the tax to the level of 94 USD/MT, the announcements about the reduction of the export quota, which could be implemented starting with January 15, 2022. Because news that its level would be 9 million tons didn’t have any effect, the quota was then circulated downwards to a level of 8 million tons, i.e., a smaller volume of wheat allocated for export.

However, if we look at what Russian 2021 harvest volumes expose and at what level the latest WASDE report states, estimating the level of Russian exports so far, of about 19.5-20 million tons of wheat, it is very easy for us to we understand that everything is just an attempt to raise the price level in the Black Sea basin. A level which is low mainly due to lack of demand these days. Russian farmers are effectively subject to selling pressure, at a RUB/USD parity of 74.13/1.

So we have all the elements of pressure allocated to see a time horizon for the price increase or, why not, to limit the possible increase, which could occur, in any case, only until January 9, 2022, when a new WASDE report is generated.

Russia still has a long way to go before it reaches its current export program of about 15 million tons. The 8 million export quota is an example of a bluff with no chance of success. Romania has exported wheat at a level of 4 million tons so far, and Ukraine is also in direct competition in the basin. On the other side of the continent, France generates extremely important volumes for China, their cadence being extremely high. Last week we saw a doubling of volume shipments to China. However, the aggregation of data indicates that Algeria is in the first position of the acquisitions from France, with a volume of about 800,000 tons, followed by China, with 600,000 tons and, of course, the former French colonies, such as Morocco with 180,000 tons.

In this context, we also record a completed tender in Algeria (generated by OAIC, the body that controls these imports) and note the volume of about 700,000 tons purchased at an average level of 373 USD/MT. The variation is given by the means of transport, Panamax or Handy.

Jordan purchased 60,000 tons of new crop wheat at the level of 327.5 USD/MT, CFR Aqaba, with delivery July 2022. The level is one that reflects 259.5 EUR/MT FOB Constanța. Corrected with the fobbing cost, we have 254 EUR/MT in the CPT Constanța parity, without the exporter’s margin included.

Iran purchased 500,000 tons of wheat with delivery in January-February 2022, originating in Russia, Germany and the Baltic States.

We are also waiting for the completion of the tender generated by Turkey through TMO for the purchase of 320,000 tons, but this will come after the closing of the edition.

BSW (Black Sea Wheat) indicates recovery as well. The indications for January get a positive note in the same context.

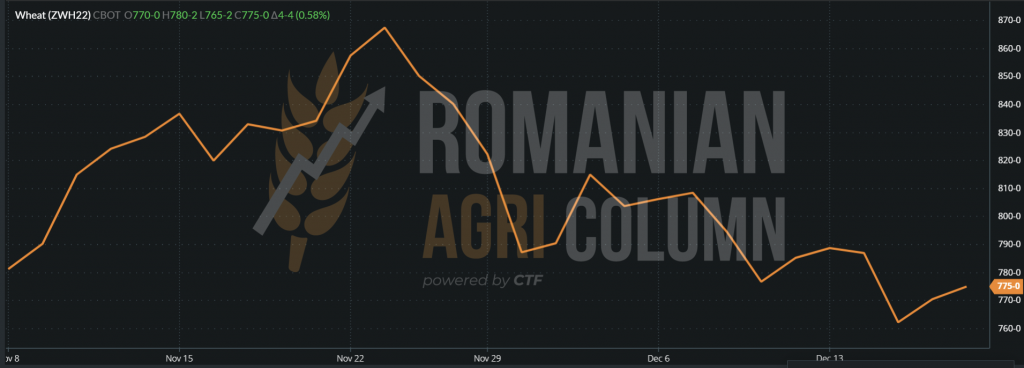

CBOT, in turn, is recovering slowly but positively. The closing indications of December 17 show us a level of 775 c/bu and we have a recovery from 756 c/bu, i.e., 21 c/bu or 7.71 USD.

CBOT ZWH22 – 775 c/bu = 284.76 USD

CBOT ZWH22 – December 7-17, 2021 trend

Let’s draw some conclusions before moving on:

- Wheat, which was most affected by the three elements, the Omicron panic, the WASDE report and the Federal Reserve announcement, is slowly returning to the 280 EUR/MT level.

- Wheat was hit the hardest, due to the long positions of investment funds. These long positions have been generated by the global negative balance between production and consumption.

- In terms of the 2021 crop, we estimate another report with a surplus in January. It will come from Argentina and will influence the price of goods.

- The only competitive advantage of the basin will remain for a period of 12 days to Romania, which will enter the business before Russia and Ukraine due to the postponement of the winter holidays according to the old Orthodox rite, which will leave Romania the only origin for 12 days. But are 12 days enough? What if the buyers think the same and will they wait 12 days? This scenario would be consistent, as the WASDE report arrives on January 9, 2022, in the middle of the competitive 12-day interval.

- The revaluation of positions in the physical market, especially in the yard of the 7 major exporters, could be a factor in getting things started in the sense that wheat could regain lost ground.

- But, judging correctly, a level of 280-285 EUR/MT CPT Constanța with delivery January-February 2022, is a fair one and much better connected to the global reality.

We now move on and move on to the next chapter, namely the 2022 crop. This crop is beginning to take shape in terms of volume estimation. In the same way, it outlines the first issues that we will take note of together.

But let’s start with the European area, including Romania, which is a major player in the two markets, the European Union and the Black Sea basin. Romania is an integral part of the origin market of the Black Sea basin, a basin that does not consist only of the two almost combatant countries, Russia and Ukraine. Romania is a pillar of stability and predictability in this regard. It is backed by its membership of the European Union and the North Atlantic Pact, predictability and support for trade in agricultural products in the Black Sea. And this must be made known and recognized by the members of the Black Sea basin.

Due to its volume and logistics already recognized in the port of Constanța, where we have the fastest terminal in Europe, called Comvex, Romania is this year a landmark in the way it has led sales to Egypt, having so far a 44%market share to this destination. Through these sales through GASC, Romania becomes a market marker, now, in the middle of the 2021-2022 season.

EU-27 WHEAT 2022-2023:

- The EU-27 forecasts a common declining wheat volume for the 2022-2023 season, from 129.3 to 127.6 million tons, a decrease of 1.7 million tons.

- The EU forecasts a decrease in wheat volume, adding durum in the calculation from 136.9 million tons to 135.8 million tons, a decrease of 1.1 million tons.

- Romania is listed with only 8.74 million tons out of an area of 2.07 million ha for the 2022-2023 season and with a yield decreasing from 5.01 to 4.22 tons/ha.

- France maintains the same level of soft wheat of 35.62 million tons (vs. 35.4 million tons in 2021), with an increasing yield of 7.28 tons/ha.

- Germany is forecast to increase the forecast volume of soft wheat to 22.2 million tons, from 21.45 million tons in 2021, with a yield of 7.6 tons/ha, compared to 7.37 tons/ha in 2021

- Poland is growing by 0.2 million tons, to the level of 11.7 million tons, with a yield of 4.9 tons/ha.

- Bulgaria has a forecast decrease from 7.17 million tons to 6.23 million tons, with a forecast yield of 5.34 tons/ha, decreasing compared to 2021, when it had 6 tons/ha.

Thus, Romania and Bulgaria will degrade the total wheat production of the European Union with the figures listed above. However, Romania maintains its 4th place in the European Union in wheat production, after France, Germany and Poland.

USA – Houston, we might have a problem! On December 16, 2021, the Central Plains of the United States were hard hit by a storm that crossed them. The essence of this storm was the power of the wind which blew at speeds between 100-150 km/h, at a temperature of 24 degrees Celsius. The effects were dramatic and multiple, starting with property damage and ending with wildfires in the fields.

The American winter wheat was actually burned by the combined power of the wind, aggregated with a high temperature of 24 degrees. From the first unofficial estimates, the damage assessment is based on the assumption that ½ (half) of the wheat has been affected. To what extent? How much was lost? It remains to be seen in the next period. Indeed, the US territory has not faced such a thing until now, i.e., summer storm in December. Moreover, the storms displaced extremely much dust, and this extremely hot dust was carried by the wind at the mentioned speeds and devastated many wheat fields. Until the official data arrives, we will insert some photos to see the terrible effects on the crops. The landscape is selenarian.

WHEAT CONCLUSIONS

- American production is called into question, the effects of wild dust storms quantified in figures are not yet known.

- Lower European production at this time due to declining use of fertilizers, especially in Romania and Bulgaria.

- A production that did not reach the level of sown area in Russia and Ukraine and that officially entered the state of dormancy, which can be surprised by the extremes of the weather.

- There are many question marks for the 2021 crop, but we have enough work in our analysis to say that it cannot go up in the next period, a period that includes the winter holidays, unless something unforeseen happens. But, as we well know, the unforeseen is only the latent state of potential between Russia and Ukraine.

2022 SHOWS TO BE EXTREMELY CHALLENGER.

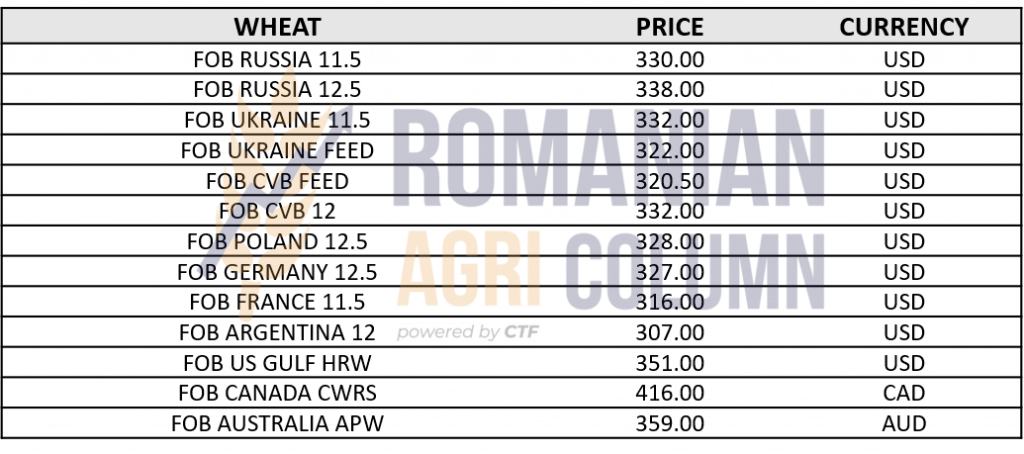

PRICE INDICATIONS IN VARIOUS ORIGINS

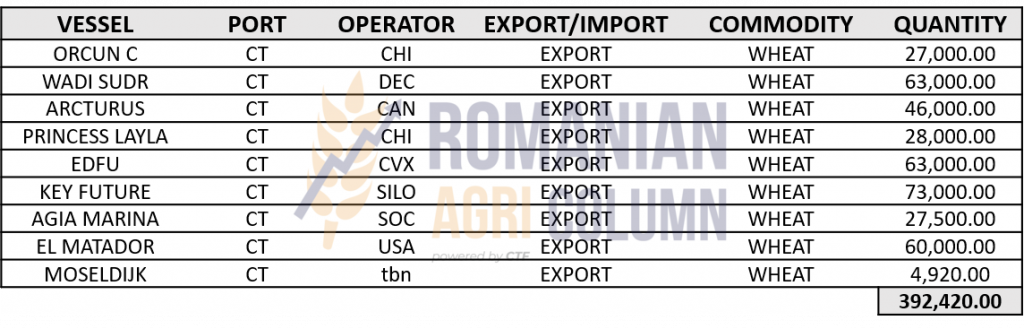

WHEAT LINE-UP CONSTANȚA

Barley market

The price of barley in the CPT Constanța parity also deteriorated significantly after the wave of events that considerably weakened the wheat and we thus see the level from December 17, 2021 at 235 EUR/MT. The decrease is considerable, but at the levels that still exist in Romania, we hope that they have been liquidated in a timely manner. In the next period, there are no potential major transactions in the regional barley market.

Corn market

The indications of corn in the CPT Constanța parity are at the level of 233 EUR/MT. The same complex of factors as wheat have degraded the price of corn in the Black Sea basin – the panic induced by Omicron, the WASDE report and the intervention of the Federal Reserve.

However, maize has not been as impacted as wheat, with investment funds not being as exposed in terms of net long positions. Thus, the negative difference was initially 5 euros, after which, successively, the indications returned to 233 EUR, which we see today exposed as a level of acquisition in the Port of Constanța.

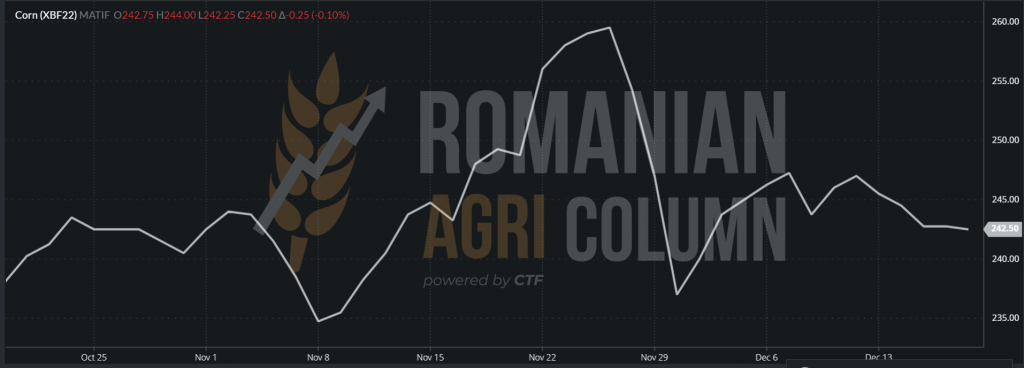

At the close of 17 December 2021, EURONEXT indicated a level of 24.5 EUR XBF22.

XBF22 MATIF CORN TREND – the impact of December 7th was not as strong as in the case of wheat.

However, interesting things are happening in the Black Sea basin and in South America. And we want to shed light on the harvesting process in Ukraine.

The latest indications received from Ukraine show that it is heading towards a potential 43.7 million tons out of 5.47 million hectares, with a productivity estimate of 8 tons per hectare. However, this quantity is bunker weight, so it does not extract the excess water and, if we estimate correctly, the end will be around 41 million tons, 3 tons above the USDA’s and our estimate. This will certainly unbalance the price level in the Black Sea basin much faster. Why is that?

- As the quantity is higher, it has to find its way out much faster than before. We saw March-April in excess on the market, but we might see February in the same way.

- The Brazilian SAFRA will be harvested starting in January, seconded by the Argentine corn crop. A South American pressure point will be created, as the logistics in South America are competitive with that in the basin. It is easy to see how the Brazilian corn will create the first pressure in the Black Sea basin. Then the Argentine corn will come in later. Their aggregate volumes with the additional Ukrainian volume will negatively offset the price.

- However, SAFRAS MERCADO in Brazil indicates a decrease in the level of the first Brazilian corn crop, from 25.7 million tons to 21.6 million tons.We note the forecast, but it is not long before the start of the harvest, so we will be able to validate it soon.

- WASDE in January 2022 will also generate additional pressure by allocating Brazilian and Argentine forecasts together with the Ukrainian supplement, which will increase global maize production and thus a full stop and a deterioration in the price of corn.

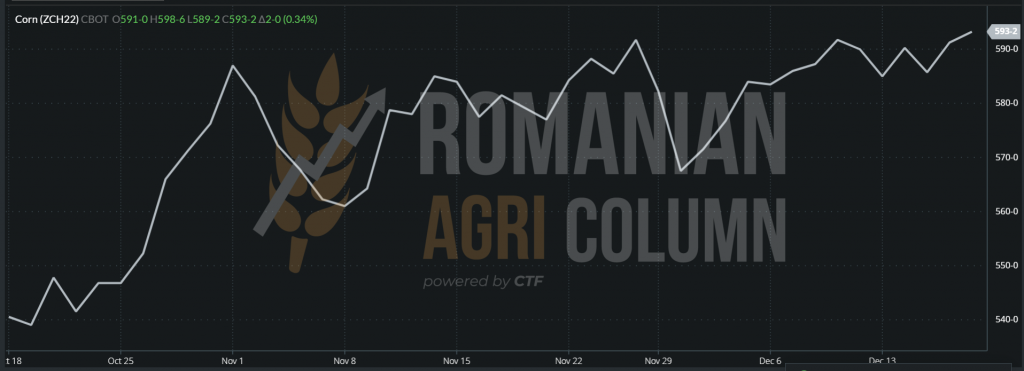

CBOT at the closing date of December 17, 2021 – ZCH22 – 593 c/bu = 233.45 USD (+2 c/bu)

ZCH22 CBOT GRAPHIC – American corn growing between December 7-17, 2021

Why does American corn price rise? Because the level of exports is in trend and we note the transactions of last week, as follows: 1,300,000 tons Mexico + 650,000 tons other destinations, to which we add a sale of 745,000 tons for the season 2022-2023 also in Mexico.

CORN CONCLUSIONS

- Pressure will form from additional Ukrainian volumes.

- The second pressure center will come from South America. Brazil and Argentina, with the help of logistics, will push the goods to the destination China and China’s neighboring countries – Vietnam, South Korea, etc.

- The WASDE report of January 9 will correct the position of Ukrainian corn in a positive way and we want to see if the Brazilian Safra is also corrected.

- American corn is growing slightly due to sales to the most important customers of the season, Mexico and Canada.

- China is still set at 26 million tons, but there are signs of new outbreaks of swine fever, so there may be surprises in this regard. If the pig farms become more acute and depopulated, consumption will decrease and implicitly the import of corn. The market will correct negatively. But let’s not anticipate, but rather wait for full reports, which may or may not validate this information.

- Thus, we will note the decrease in the price level in the Black Sea basin. And that will happen with the release date of the USDA report.

FOB PRICES VARIOUS ORIGINS – CORN

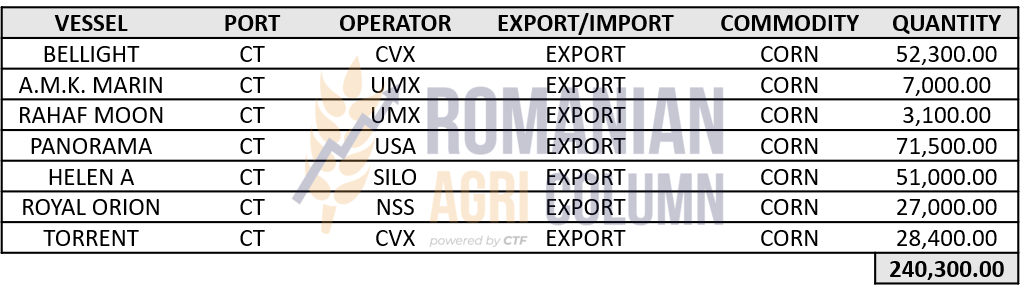

LINE-UP CONSTANȚA – CORN

Rapeseed market

The indications for rapeseed for the FEB22 sequence are increasing, with the indication posting a closing level on 17 December 2021 at 729 EUR, increasing by 6.5 EUR. This once again indicates the support generated by the lack of volumes.

The port of Rotterdam indicates on 17 December 2021 a price level for rapeseed oil in the FOB parity of 1,510 EUR/MT, increasing by 85 EUR/MT. This indicates a lack of coverage in oil sales and thus, overbidding to cover open positions is the only action that traders can take at this time.

Rapeseed quotations in the FOB CVB parity are indicated at 807 USD/MT, increasing by 5 USD/MT. Converted into EUR and brought to CPT parity, the price reflects the level of 710 EUR/MT, without the exporter’s margin included.

EURONEXT XRG22, 17 December 2021 – 729 EUR (+6.5)

The inverse crop must be calculated by the difference between the sequence XRK2 MAY22 (669 EUR) and the sequence XRQ22 AUG22 (545 EUR). We thus reach a level of 124 EUR price difference between the old and the new crop.

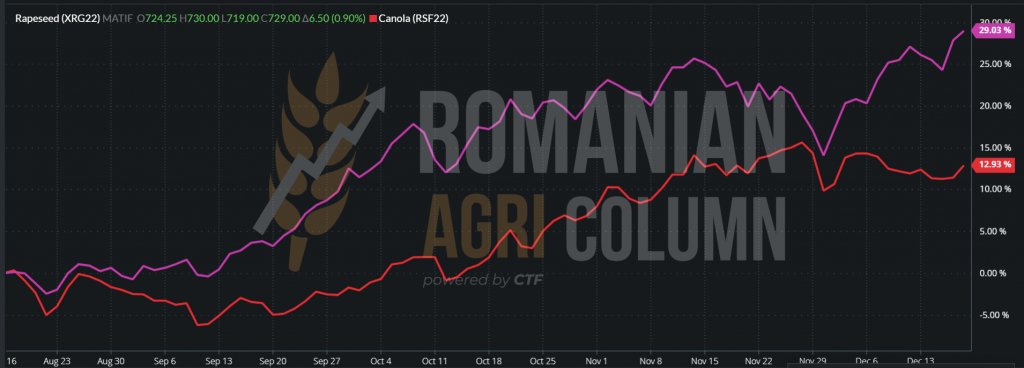

Canadian canola indications are growing again, a sign that support from the higher level of the Australian crop has not generated enough volume for the price to fall.

RSF22 – 1,014.3 CAD (+13.3). At EUR-CAD parity of 1.45, the indication is equivalent to 700 EUR.

Euronext rapeseed chart (magenta) – Canadian canola (red)

As a crop update, we note India in a positive production review, from 8.5 million to 11 million tons forecast, which will impact the market for crude rapeseed oil destined for VEGOIL, i.e., in the complex of vegetable oils. The volume of cargo will put pressure on palm oil, soybeans and sunflower as it is used in India mainly for human consumption.

Sunflower seed market

Current indications for sunflower seeds are at the level of 620-630 USD/MT in the CPT Constanța parity, after the lack of buyers in the Black Sea basin (and we refer to crude oil) caused the price of the latter to fall to level of 1,310 USD/MT, a level difference of 100 USD/MT.

The lack of buyers in the pool is fueled by buyer coverage for December 2021 and partly January 2022. Processors are covered until the end of January, and farmers are in the same state of not selling the goods, even in conditions of deteriorating prices. We are in a Mexican stand-off and whoever blinks first will lose.

We note the lower volume of exports of sunflower seeds from Russia of 20,000 tons and 40,000 tons from Ukraine, a volume also very small. This is provided that Ukraine does not reimburse VAT and has a 10% raw material export tax. However, the vision of at least 200,000 tons of raw material export originating in Ukraine is quite far from reality at the moment.

In Romania, the level of stocks is at a maximum value of 780,000-800,000 tons and we are waiting after the holidays to see the evolution of the market in the sense of the pressure exerted by the buyers of crude oil, which generates pressure through processors on farmers. We repeat once again, whoever blinks first loses.

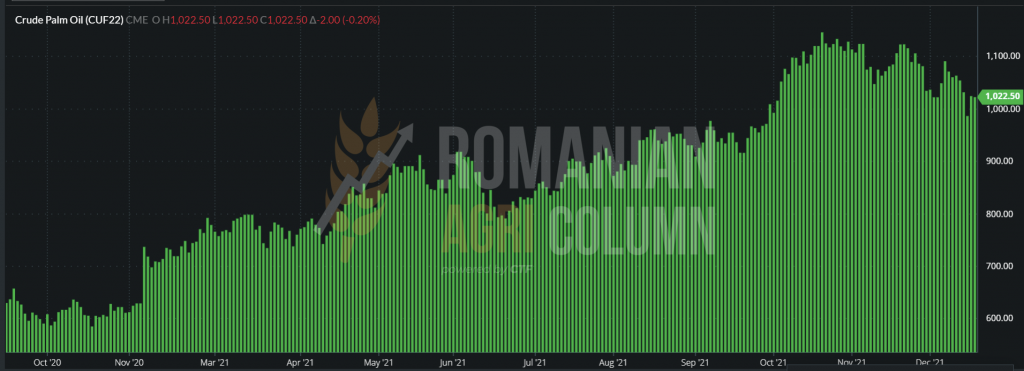

Below you will find the stock quotes of the other colleague of the VEGOIL complex, palm oil, in MDEX Malaysia and NYMEX.

INDICATIONS MDEX MALAYSIA PALM OIL – source: Barchart

INDICATIONS OF NYMEX PALM OIL CUF22 JANUARY 2022

The soybean market

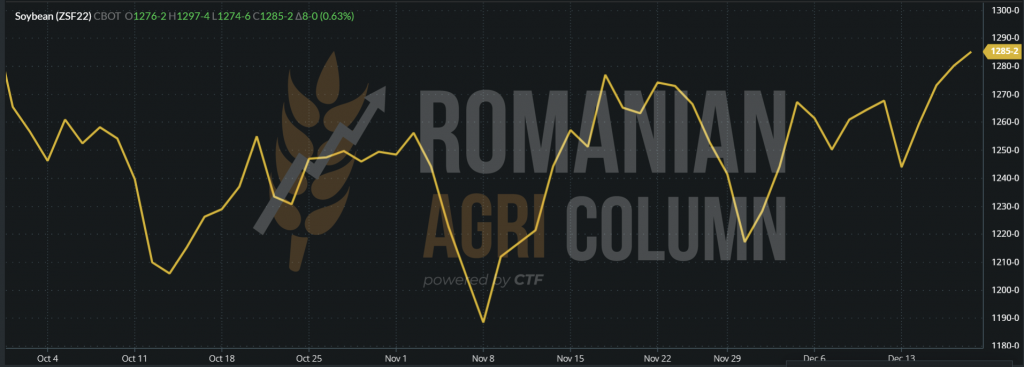

Soybean yields are on an upward trend in American soybean sales. CBOT quotes record positive values in the last time interval. Thus, from the lowest interval we recorded at 1,990 c/bu, the closing of December 17, 2021 generates a level of 1,285 c/bu, i.e., 472.15 USD. The difference between the lowest level and today’s is 31 USD recovered from soybeans.

Thus, the soybean quotation in Romania should be granted at least 20-25 USD/MT compared to the previous levels of 620 USD, especially since the local soybeans are non-GMO.

CBOT ZSF22 – 1,285c/bu (+8 c/bu)

TROT SOY CBOT ZSF22 – November 8 (1,190 c/bu) – December 17 (1,185 c/bu) – an increase of +85 c/bu = +31 USD

USDA confirms 1.3 million tons of soybean sales, including 985,000 to China.

Furthermore, Argentina maintains its volume level of 49.5 million tons, and Brazil the one of 142 million tons, to which we add the North American one of 120 million tons. Brazilian soybean exports are confirmed by CONAB at the level of 90 million tons. The Brazilian crop appears gigantic on the horizon, and its pressure on the American crop will be commensurate. Brazil will start harvesting once January 2021 is over.

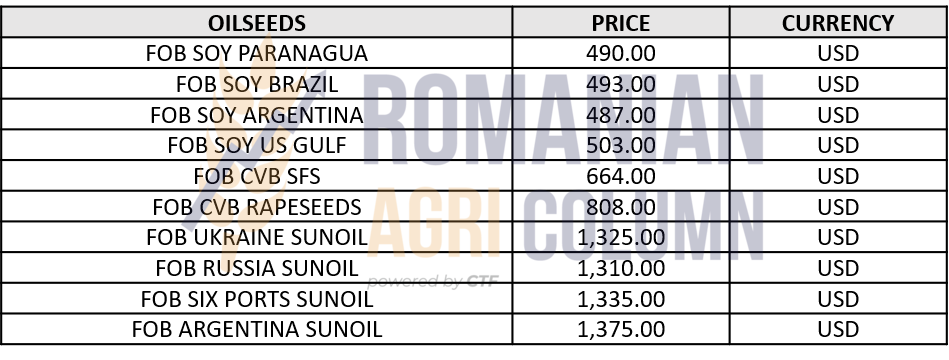

INDICATIONS FOB OIL OILS VARIOUS ORIGINS

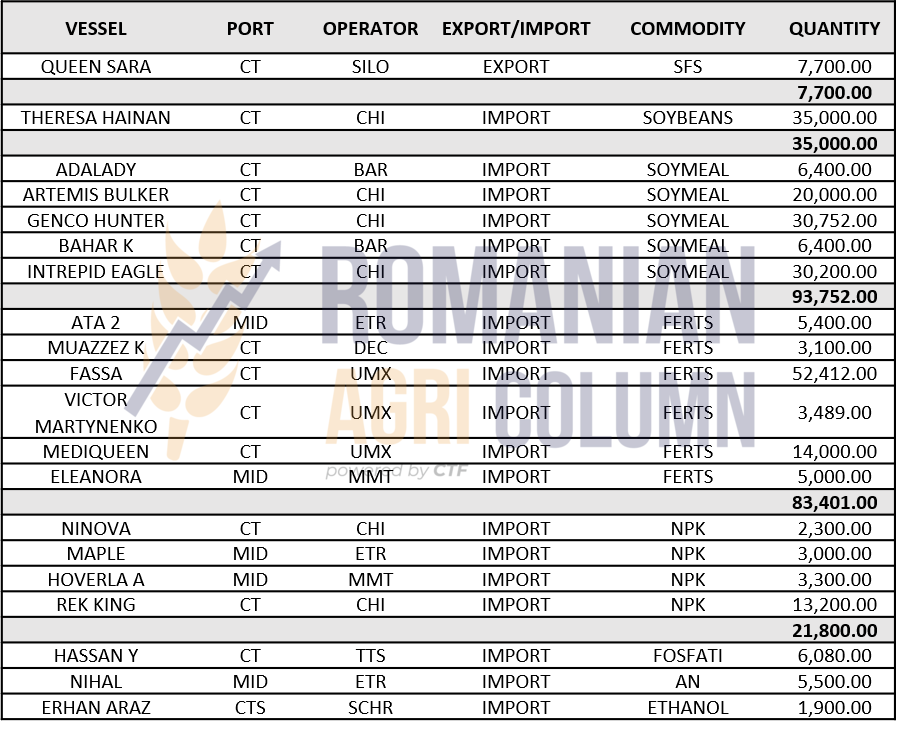

Line-up Constanța export-import various commodities

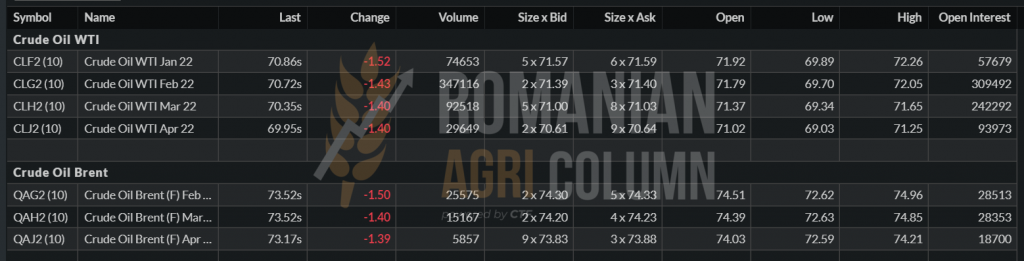

Fossil energy

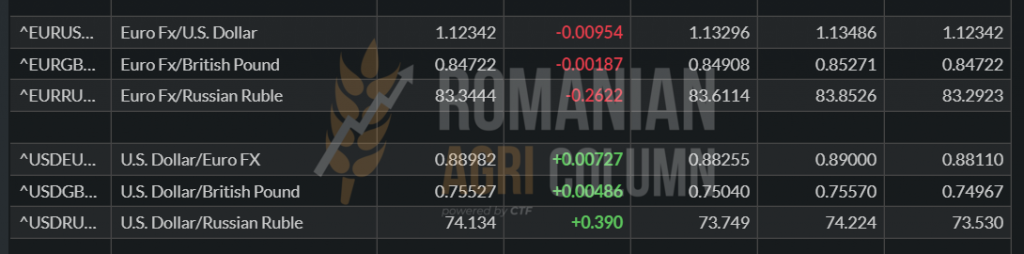

EUR-USD parity

EUR:USD = 1:1,1234

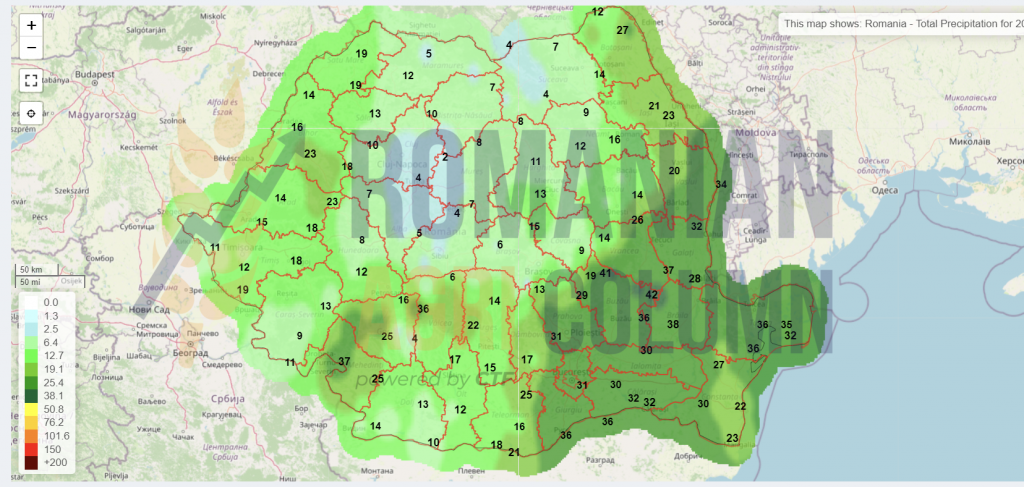

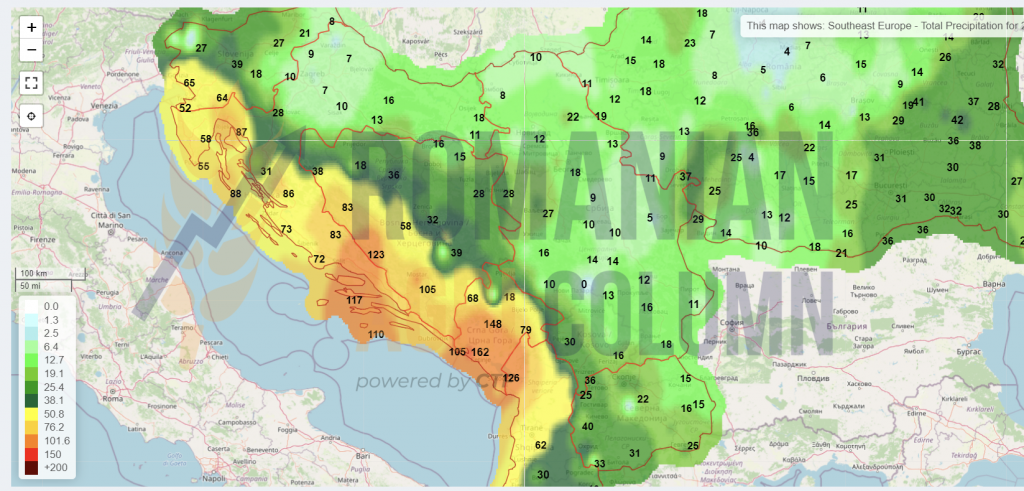

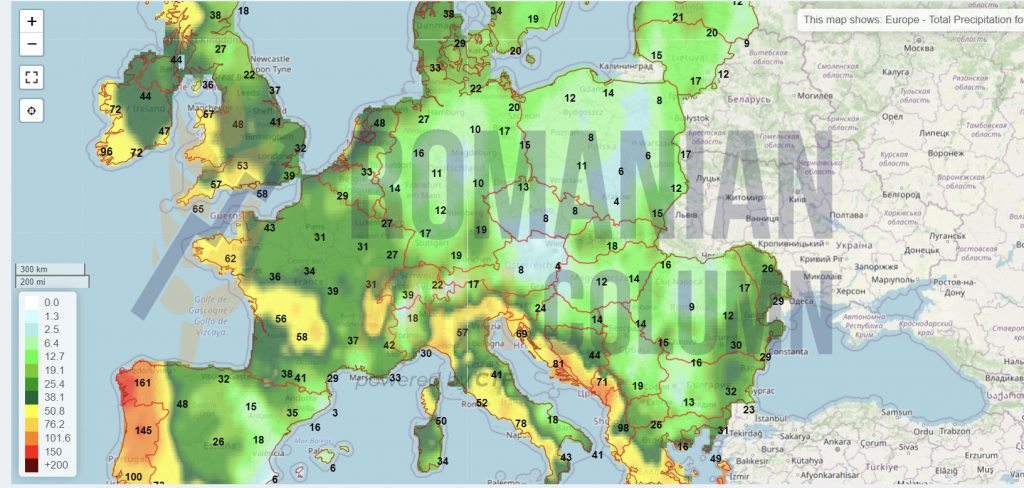

Weather forecast

18-31 December 2021

Romania

Serbia

Europe

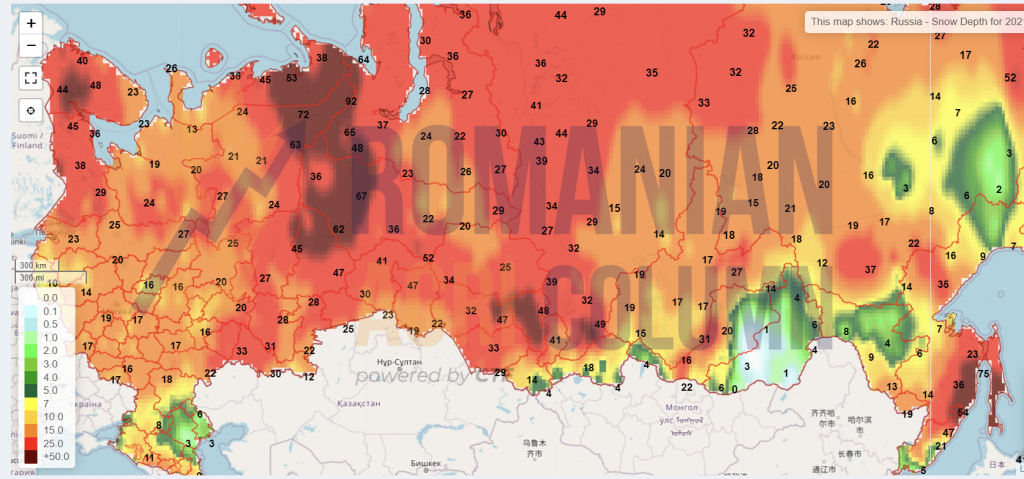

Russia (snow)

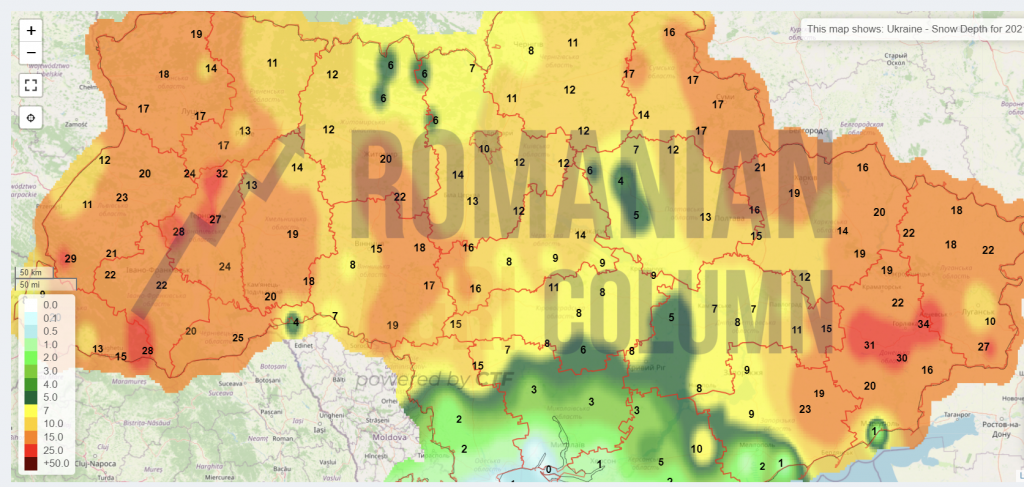

Ukraine (snow)

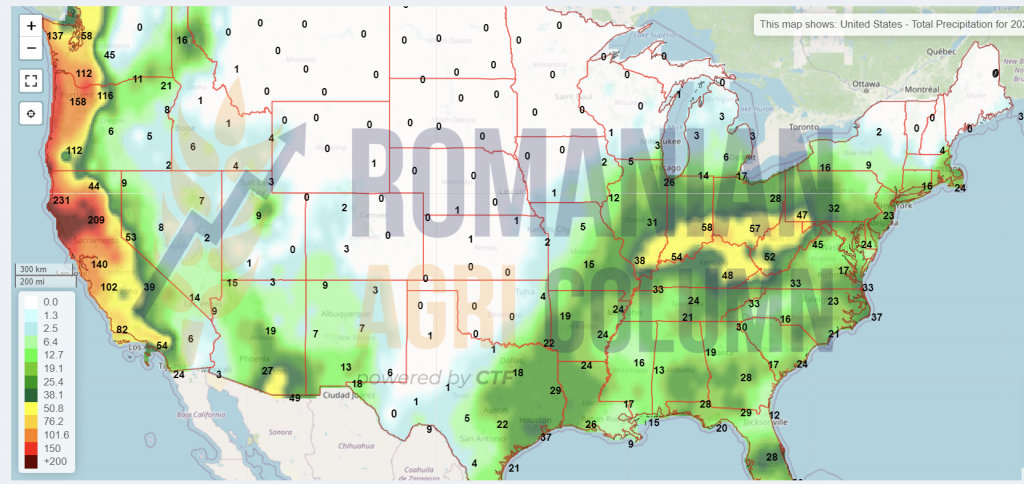

USA (rain)

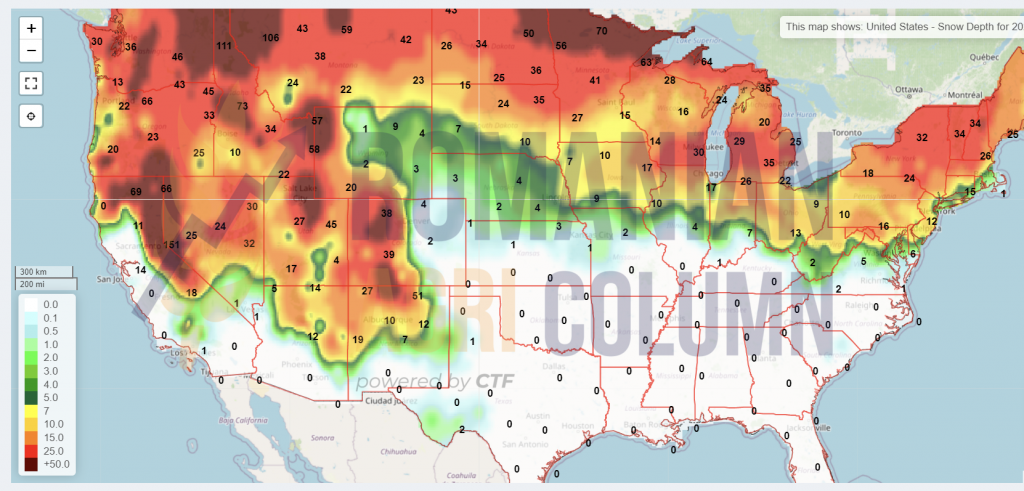

USA (snow)

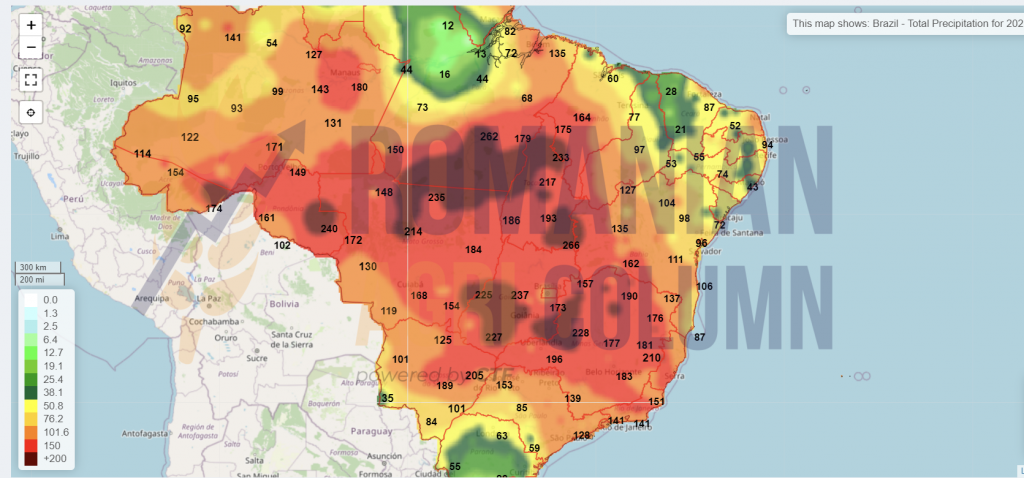

Brazil

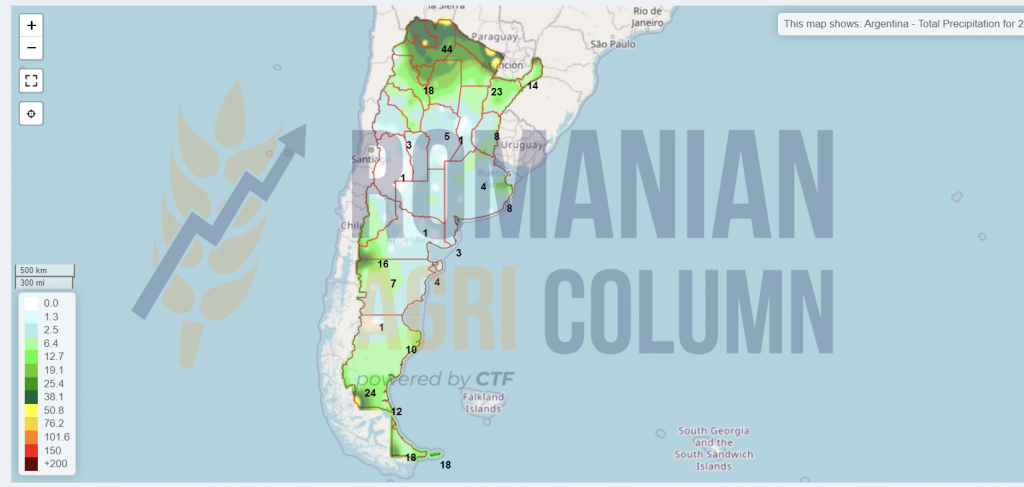

Argentina

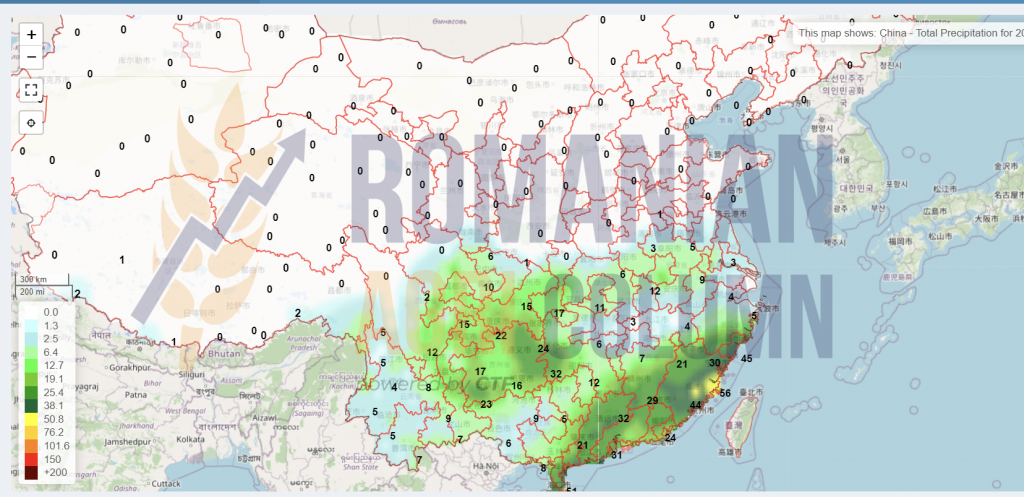

China

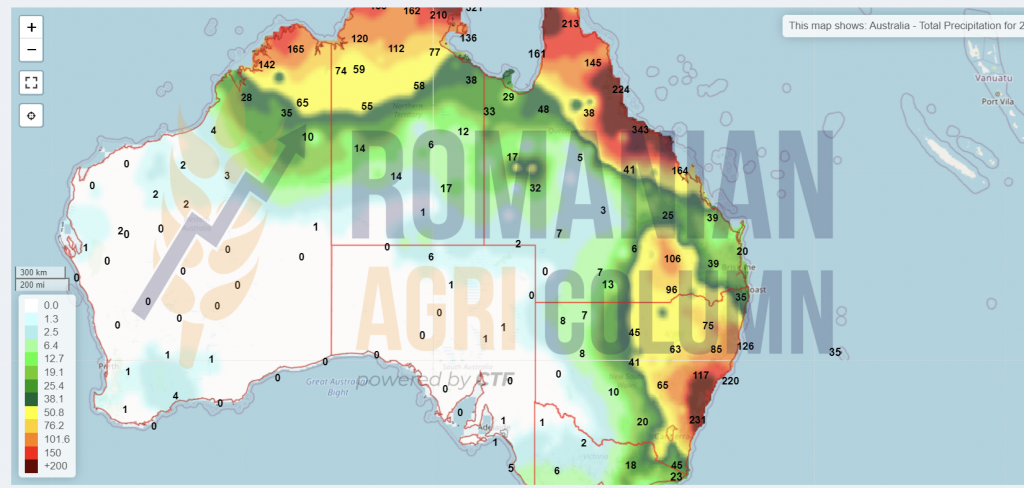

Australia – the rains come back

© Romanian AGRI Column, 2021, all rights reserved