2022 was a year ruled by uncertainties from the start, a year that began under the potential specter of a regional conflict, which unfortunately materialized. It was a year that generated loss of human life, something that cannot be covered by any excuse or motivation.

In the global agribusiness scene as a whole, potential things that led to obvious market abuses were evident from the beginning. A mix of headlines and war facilitated the creation of a price launch ramp in major commodity categories. The headlines fueled stock market trading bots, straining indications, and generating panic.

Hedge funds have traded on these tensions and generated immeasurable profits. The war was the main theme, and the exploitation of every news did nothing but count more money in the accounts. In some areas, we even have clear certainty that there were connections, namely an invisible thread for many, which generated long positions 1-2 days before the statements of the Kremlin leader. And after these statements, the value of these stock positions increased exponentially.

Everything was happening on the scene of the Russian invasion of Ukraine and at the expense of human lives. We have seen incredible jumps in the price of raw materials. We have seen sunflower seeds jump to levels of 1,150-1,200 USD/MT. We have seen wheat at astronomical levels of over 400 EUR/MT and subsequently maize, which in turn generated unimaginable levels. What else can we say about rapeseed? 1,000 EUR/MT, fueled by the pre-existing condition of minus crop globally (Canada being the service culprit) and the potential of more than 6 million tons that had effectively evaporated from the market (the sum of Ukraine and Russia production).

We went through a year where Food was used as a Weapon by Russia without any shame, without any remorse. Blackmail practiced on a large, global scale had a discriminatory effect. On the one hand, the rich got richer. Profit margins increased by fueling and exacerbating the cost of logistics services for the transfer of goods from Ukraine to safe areas in the European Union. In the same landscape were the hedge funds, which generated substantial profits from the panic generated globally. And on the other side of the barricade, there were the people who needed to be fed. Without any difference in geographical position, they have fully absorbed the inflationary shock of rising commodity prices.

In times of war, the biggest profits are made, then the conditions for exacerbated enrichment are created, and the connection between the Stock Exchanges and the Fundamentals of the physical market has deteriorated. Russian crop potential was visible, but blockades and sanctions on bank transfers made this hardly tangible. Ukrainian potential was penalized by the impossibility of transferring across the country’s borders to destinations. Added to this whole complex was a severe drought, which bit ferociously from Europe’s harvest volume potential for spring crops, in this case corn and sunflower seeds.

Everything has turned into a hybrid war, conditioned by demand and the potential lack of supply. The states of North Africa, the poor states of central Africa, the poor area of the Middle East and the Arab countries of the Gulf were the stage of the theater staged by Russia, with turntables created through India and Pakistan, with companies registered in Dubai, with underground movements of traffic using Syria for Ukrainian wheat looted from the territories that were and are under Russian occupation.

But as usual, this agribusiness market has winners and losers alike. And the losers were those who believed that everything was going on an unstoppable spiral, on a price evolution that would not stop. It was a mistake generated by a lack of technicality, a lack of maturity and trust in accurate and timely information. Thus, today we are faced with a phenomenon that was exacerbated over the summer, the so-called retention. Romania is, in turn, placed on this stage. Many, many lots of goods sit in barns in the ephemeral expectation that prices will return. But the market acts differently. Always what rises and falls, returning to the normality of the days.

Romania has a market affected by the transit of Ukrainian goods, given the fact that many of them have found an outlet in domestic processing, due to the price discounts applied. Romania was equally affected by the lack of efficient logistics, which caused the availability of transport to generate a lack of competitiveness in Romania for domestic goods. Romania was also affected by the lack of confidence and maturity of many regarding the global physical foundations and, therefore, by the lack of decision in choosing the moment.

For these reasons, retention has proven to be, despite the information and advice we generate, an extremely damaging choice. Nothing lasts forever, famous saying states. And so the physical foundations began to reveal the truth. “Russia must sell wheat” is one of our repetitive statements, which implicitly led to its positioning in this blackmail.

You can’t do this forever, this game can’t be played for long, because if you don’t sell, you don’t have income and, by implication, you can’t support the local production cycle. Russia had to release a grain route from Ukraine. Through the grain corridor, Ukrainian goods began to circulate.

Moreover, Russia lost the start of wheat sales. The European Union scored excellently in this department at the start of the season and benefited from high price levels. Russia needed to sell and began to practice aggressive discounting. The boomerang backfired on them. The export tax was melting away to stimulate sales, and little by little, prices began to fall. On the opposite side of the scene, hedge funds were also brought back to their pre-conflict state.

The Federal Reserve has generated a policy of increasing interest rates to slow down and reduce the level of inflation. But let’s remember that the FED also printed 16 trillion dollars without a positive yield. So it was very cheap money. Due to the appreciation of money, funds began to divest large volumes of positions in the CBOT and EURONEXT. Every time the FED raised interest rates, we also saw an effect in the price of agricultural commodities.

The connection of certain hedge funds to certain areas of Russia still exists, but we are seeing a general lack of reaction to panic-generating headlines. The other day, a Turkish floating crane in Kherson was destroyed by Russia. The effect was not the expected one. Nobody blinked.

So, let’s go back home. So let’s go back to a market that works on physical and by no means political foundations generated by war. This conflict will continue, but we do not know how long. But the winter that has arrived penalizes the combatants, who will winter in a state of strengthening their current positions, then in the spring they will start again with much more ferocity.

And in the commodity trade, both lose. Russia will not meet its export schedule. The weather is adverse in the Sea of Azov (a problem closed, as Putin says, but we’ll see) and likewise in the Novorossiysk area of the Black Sea. Storms, snow, and strong winds make it impossible to load and ship volumes contracted by Russia. Their wheat cannot be shipped and clearly this further burdens the volumes that will remain unsold. The decline in the price of wheat will certainly continue in the coming days. The Winter Holidays are also an extremely powerful reason.

Ukraine can no longer ship corn. Its quality is penalized by drying costs and, in the European Union, this is already being felt. Regardless of the level of the discount, the product is no longer in high demand. The exchange is carried out in recipes with feed wheat. The Ukrainian corn that remained in the fields unharvested will have an industrial destination, i.e., the manufacture of ethanol. And significant amounts remained unharvested. We estimate a minimum of 12 million tons. However, the European Union is in full import activity and today we see a level of 13.2 million tons of imports, double compared to last season, in the same period. Argentina and Brazil will play a major role in the path of corn prices. Argentina’s drought is not generating increased seeding, and Brazil’s Rio Grande del Sul is starting to feel water shortages.

Sunflower seeds are also under extreme pressure due to competition with palm oil. This means that the Asian focus is directed towards palm oil, and sunflower oil remains somewhere on the sidelines, prey to the competition between Russia and Ukraine, which discount massively just to sell. But here things will be marked by the lack of raw material. Russia left 2.1 million tons of seeds in the field, and Ukraine finished harvesting 0.5 million tons short of the initial forecast of 10.5 million tons. The European Union is covered today in terms of processing, but let’s not forget that its production was severely penalized by the drought and progressively degraded from 10.9 million tons to 9.45 million tons. Here, apart from the correlation with soybean oil and palm oil, we have another actor, namely Argentina, which is suffering from extreme drought, and the estimated sunflower crop of 4.2 million tons may not be touched.

Rapeseed, for its part, is affected by the decisions of the EPA (Environmental Protection Agency) in the USA, which mandated the mixing of vegetable oil in fuel at only 1%. This has severely penalized the level of canola and rapeseed on the Canadian and European stock quotes, dragged down by the decline in soybean oil indications. Canada, however, returned to positive indications on the background of stock reports, which degraded the crop level by 5%, more precisely by 1 million tons. However, Europe did not benefit, as distant Australia generated a record canola crop of 7.2 million tons, 0.5 million tons more than forecast.

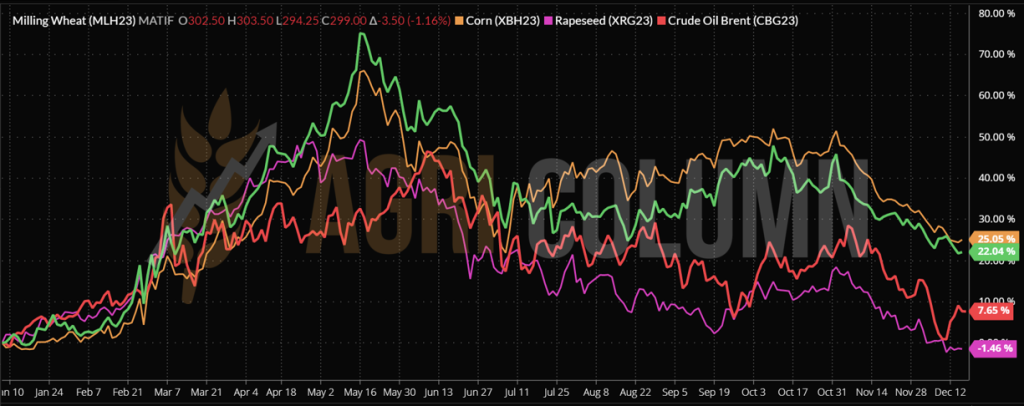

Now the stock market, the weather, the supply and demand, the fragility of the frozen conflict in the winter tell us that we are back where we left off. We are returning to pre-conflict levels. Corn, wheat, rapeseed, oil are slowly returning to acceptable levels, so to speak.

New crop projections are positive, the Northern Hemisphere has nothing to fear currently. Perhaps only the US, with 74% wheat in poor vegetative state, has problems (but even there, snow can solve this problem). China, on the other hand, is coming out of lockdown and will implicitly increase consumer demand, which will activate origins. But we have a big question mark for China. It’s a deep drought there and we must be very careful about what’s going on. Chinese New Year arrives in January, the year of the Water Rabbit, but after February 5 all festivities end, and the focus will turn to feeding the population.

We have a year 2023 in front of us full, in turn, of uncertainties. What we need to do is to pay increased attention to the right indications, to trust the good indications and to act without relying on what we have experienced so far. The world is changing, and we must reinvent ourselves along with it.

Merry Christmas and a Happy New Year. See you soon!

Cezar Gheorghe