This week’s market report provides information on:

LOCALLY

Local indications of wheat have declined. From the level of 405-408 EUR/MT, they decreased to 400 EUR/MT in the CPT Constanța parity. The price difference down to the feed quality is also significant, representing a minus of 20 EUR/MT. We explained in the last issue what this difference is and what it helps. However, for the sake of equidistance, we must mention that an exporter who receives a lot of feed wheat will have special logistical problems. A percentage higher than that of milling cannot solve the equation of the mix in order to have an average related to the contractual quality signed for export.

Thus, he has to store those goods in the port and wait or find a buyer. This situation blocks the storage space in the port. He can no longer receive other goods in the cells blocked with feed wheat and this diminishes the logistical capacity. Partial blockages can happen in the port.

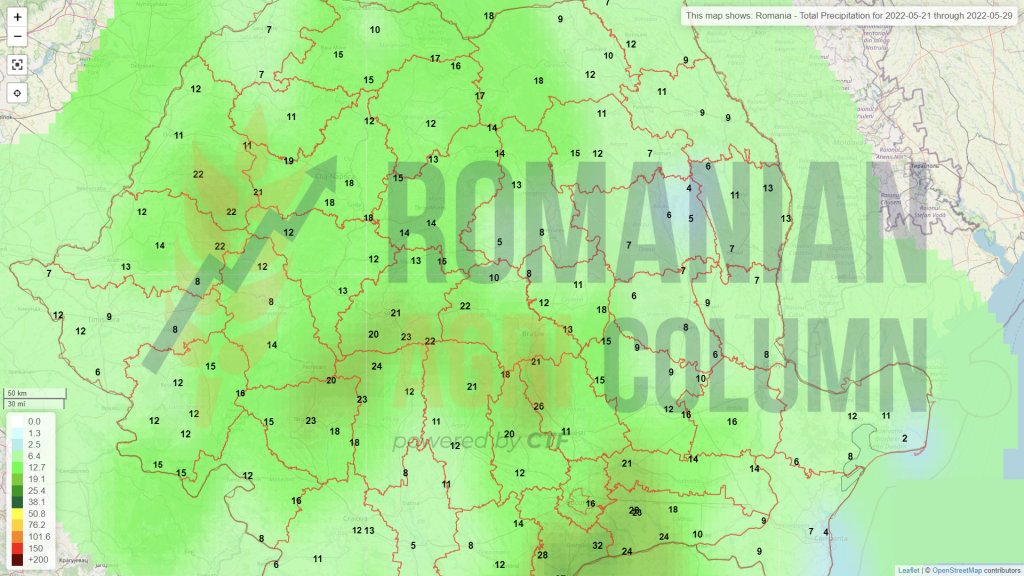

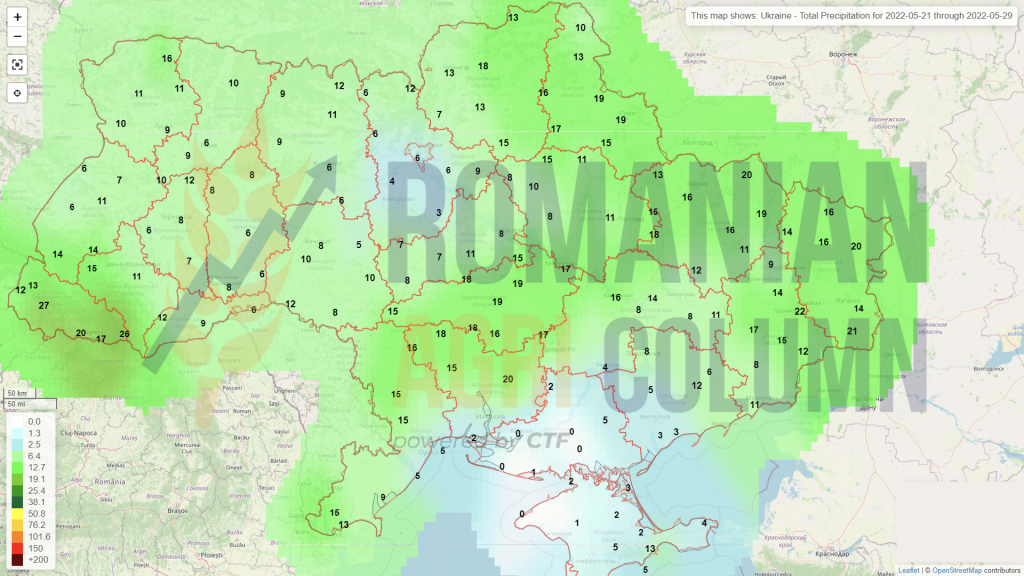

In Romania, about 36 hours of rain released an average of 10-20 liters/sqm, which gave a boost to wheat. But nothing can be seen going forward. The specter of a dry period is in front of us and until June 4, 2022, there will be no rainfall.

Growing logistics price will also create huge problems. The difference between today and the time of harvest is at least 40% in costs. If a car transport cost of 20 EUR/MT is charged for a distance of 200 km today, at the time of the harvesting campaign this cost will be driven up to the area of 30 EUR/MT.

The cost of fossil energy, i.e., fuel, which contains excise duties, contributes greatly to this, and it is very difficult to develop a process in which agribusiness users, whether farmers, transporters or buyers, can be differentiated in order to benefit from certain compensation measures.

In addition, the pressure on goods in Ukraine has a definite impact on logistics. Transport companies have the option to choose and will naturally choose higher revenues.

REGIONALLY

UKRAINE estimates problems with wheat harvesting, especially in conflict areas, where its share is particularly high. This summer, Ukraine will endanger three crops – one in the last year that cannot be exported in its entirety, one in this year that will not be fully harvested and one in the following year that will not be fully planted, declared the Minister of Agrarian Policy on Food of Ukraine, Mykola Solsky, May 18.

He added that Ukraine will harvest 50% of last year’s crop, as most of the winter wheat was planted in southern and eastern Ukraine. These regions are under active military activity, so farmers cannot and will not harvest in these areas.

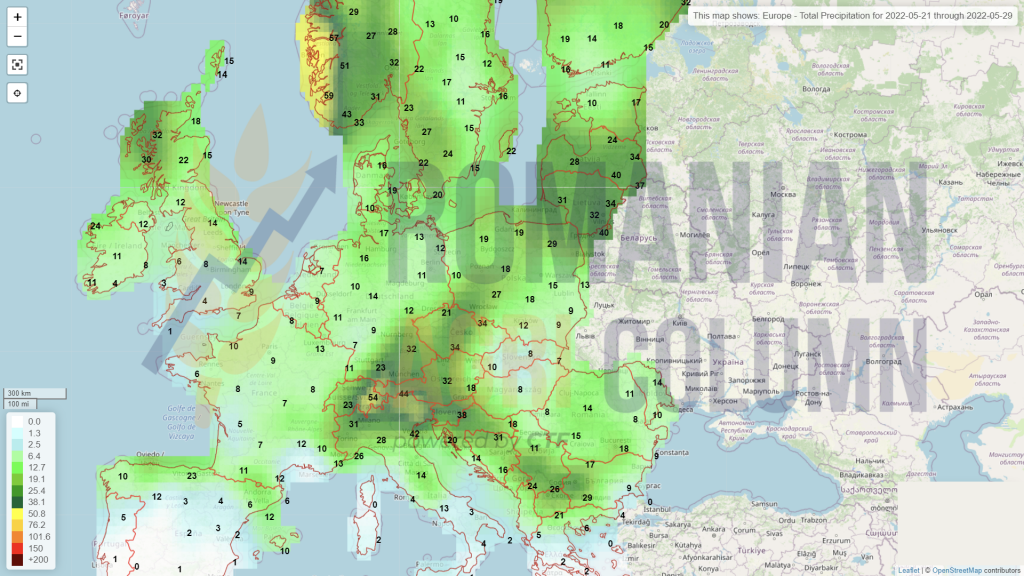

FRANCE has particular problems, as the wheat crop is in danger. If last week the rate of good to very good was at 82%, this week the rating of the French crop fell to 73%. Spain faces the same problems and there is a long way to go until the harvest, so without rainfall, the wheat will deteriorate sharply. We maintain the forecast for the French crop at 32 million tons of milling wheat, compared to 35 million tons in the initial forecast. But things can turn out even worse.

We have some very strange signals and we want to evoke them because they intertwine and could impact the commodity market:

- The United States has negotiated an agreement with Venezuela for the delivery of oil.

- German companies have opened ruble accounts to pay for Russian gas and oil.

- Italy did the same. OMV similarly opened accounts in rubles.

- And Russian wheat is sold via Kazakhstan. This state has registered companies with Russian capital that carry out wheat trade in its territory, with means of transport registered in Kazakhstan. It is a gateway to destinations in Southeast Asia and we do not exclude from this game India, which announced through its Prime Minister a crop level of 105-106 million tons on May 19, 2022.

Russia will reconfigure wheat sales flows, and this, coupled with what I have described above, as well as the fact that more than 1,000 Russian companies are registered and active in neutral Switzerland, clearly indicates who is actually in control of the wheat route.

The estimate of the Russian crop remains at 82 million tons, but it will have to export a level of 39-41 million tons, because they have a surplus that has not been exported since this season. So, if we look at trade flows at 205 million tons, Russia will have a market share of 20%, which is an extremely high and extremely dangerous level for global food security, especially since it effectively blocks a level of wheat export from Ukraine, currently estimated at 10 million tons. We add here the rest left unsold from last season of about 6 million tons.

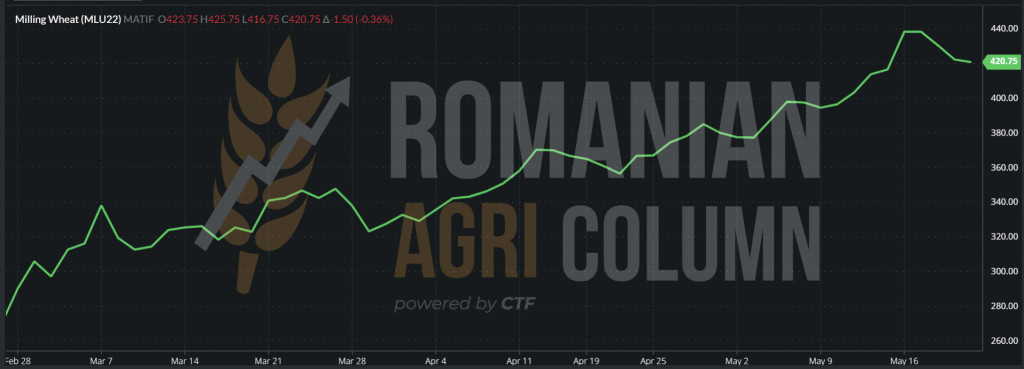

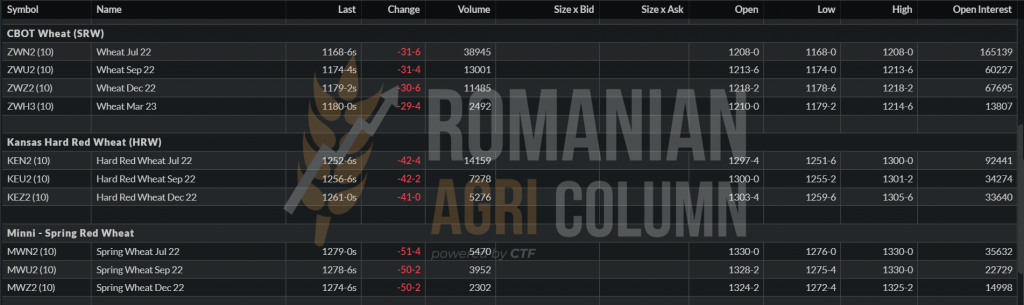

EURONEXT WHEAT – MLU22 SEP22 – 420.75 EUR

EURONEXT WHEAT TREND GRAPHIC – MLU22 SEP22

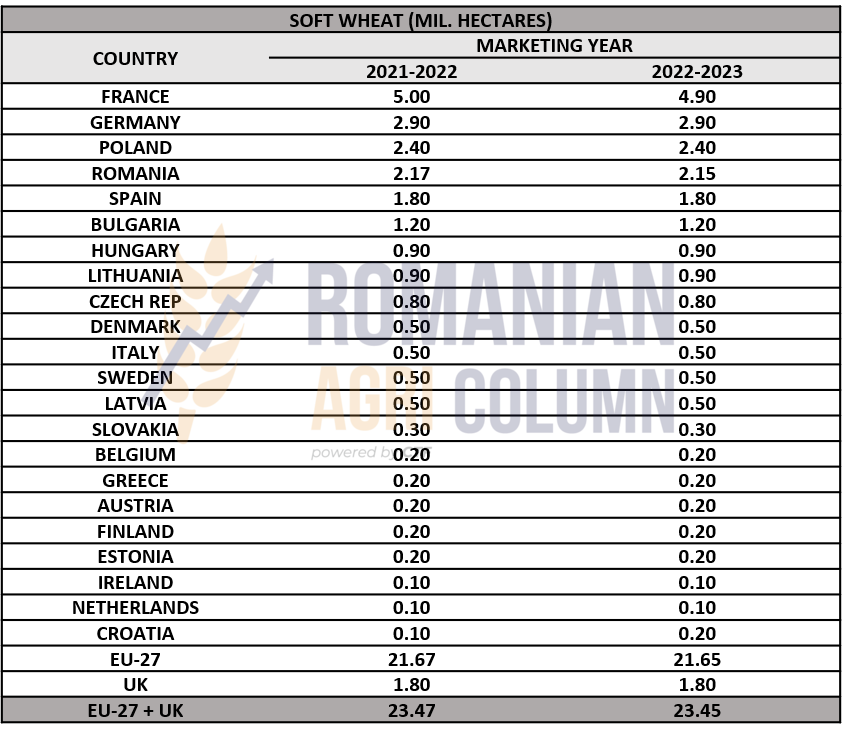

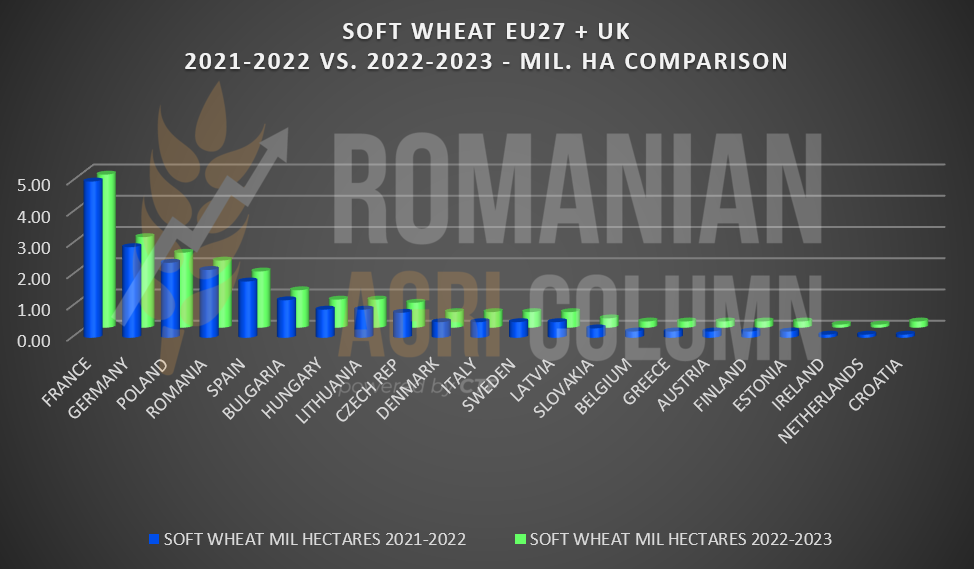

Please find below a reminder the levels of European surfaces, 2021-2022 vs. 2022-2023

GLOBALLY

United States. American wheat is deteriorating every day. The drought has taken over the entire south of the Central Plains and there are no signs of improvement at all. Even the state of Kansas is caught in this carousel of drought. The Kansas Crop Quality Tour Council for Northern States estimated productivity at 39.5/bpa, down from 59.2/bpa in 2021. That is, from 4 tons/ha, they have reached 2.6 tons/ha. Heat and dryness have greatly contributed to this low yield. Time will certainly certify our assessments, as we maintain the American wheat crop at 44 million tons, compared to 47 million tons, according to USDA May 12, 2022.

We are also considering a possible very aggressive intervention by the FED on 14 June 2022. If this happens and the intervention is extremely hard on interest rates, we recapitulate the scenario of December 2021, when, following the FED intervention, commodity prices fell by about 30-40 EUR/MT in less than 48 hours, from 295-300 EUR/MT to 255-260 EUR/MT (Euronext wheat).

If the FED does this, it will remove all less capitalized speculators from the stock market because they will not have enough guarantees to maintain their positions. And we have already seen in recent days the liquidation of wheat positions on CBOT in particular, as well as on Euronext. Are we on the verge of an obvious recession? If it doesn’t come in June, it will definitely come at the end of the year. It is a scenario that I mentioned in December 2021.

Quite simply, what is the difference between one ton of 180 EUR and one ton of 400 EUR? Nothing but an exacerbated wilderness of funds fueled by the need for margin to offset the money printed globally to combat the effects of the pandemic. And this has led to an exacerbation of commodity prices, starting with fossil fuels and continuing with the onslaught of daily food.

CBOT closes in absolute red for two days, as if confirming the liquidation of the net long positions of investment funds. Chicago, Kansas, Minneapolis, everything is red, regardless of the disaster on the plains. Here’s the question mark.

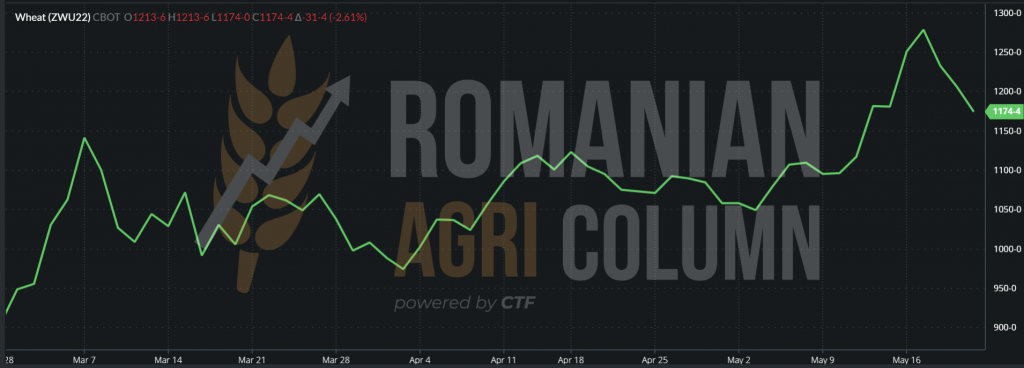

CBOT WHEAT TREND GRAPHIC – ZWU22 SEP22

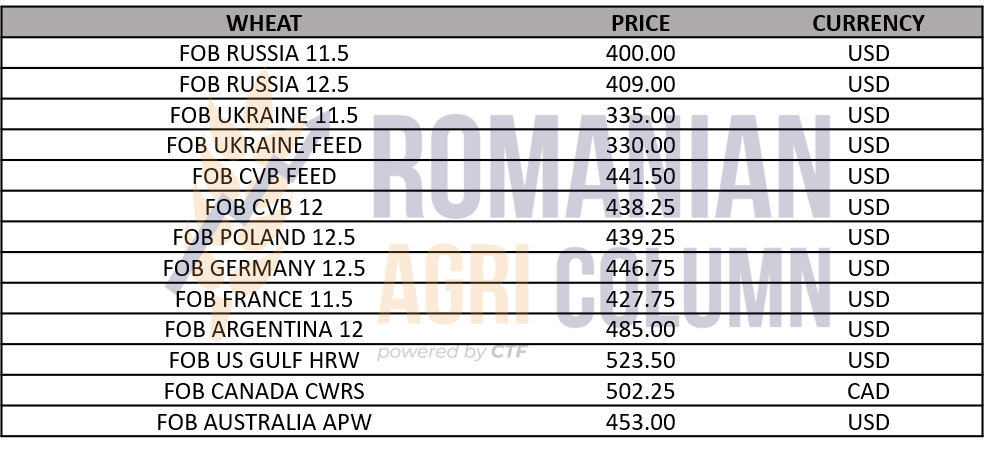

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

ANALYSIS

- Wheat is degrading in Europe. France and Spain have high red flags.

- Wheat is degrading in the United States. Kansas has been hit hard by the relentless drought.

- Russia is consolidating its position by creating new flows of goods.

- Investment funds are massively liquidating positions, as if waiting for aggressive action by the FED.

- If things go this way, the recession will take place in mid-June 2022.

LOCALLY

The indications of feed barley in the port of Constanța have seen a rather high increase. This is due to the lack of supply from exporters and the feeling that the second half of June is fast approaching. Thus, we recorded levels of 365-368 EUR/MT.

We do not deny the possibility that certain lots can be traded at 370 EUR/MT.

REGIONALLY

There are problems developing in France. Barley is declining in volume melted by the heat of these days and associated with the long-standing pedological drought.

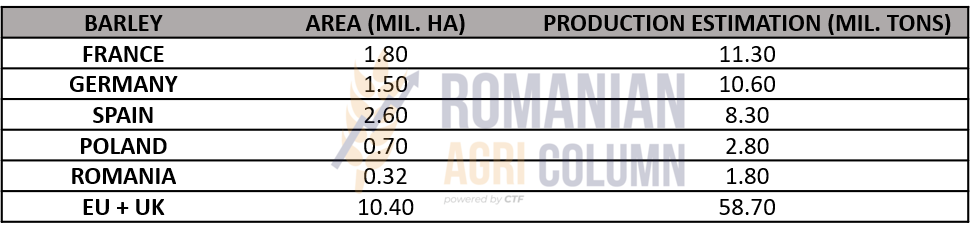

The table below shows the areas sown with barley in the main producing countries in Europe and the estimated yields. But France and Spain have red flags on them for the reasons set out above.

ANALYSIS

- The imminence of deliveries increases the price of barley in the port of Constanța.

- France and Spain will reduce the estimated volume level to be harvested and will implicitly generate a higher price overall.

- One week ago, the price in Constanța was at the level of 330-340 EUR/MT CPT, while in Rouen the indication was 370 EUR/MT. Today, Rouen is at 390 EUR/MT for July delivery, while Constanța is at 368 EUR/MT. We all understand the pattern that applies.

LOCALLY

The indications of the old crop corn are at the level of 335 EUR/MT in the CPT Constanța parity. The transactions are carried out and the activity of the port is very intense these days. The price indications for the new maize crop are at 315 EUR/MT.

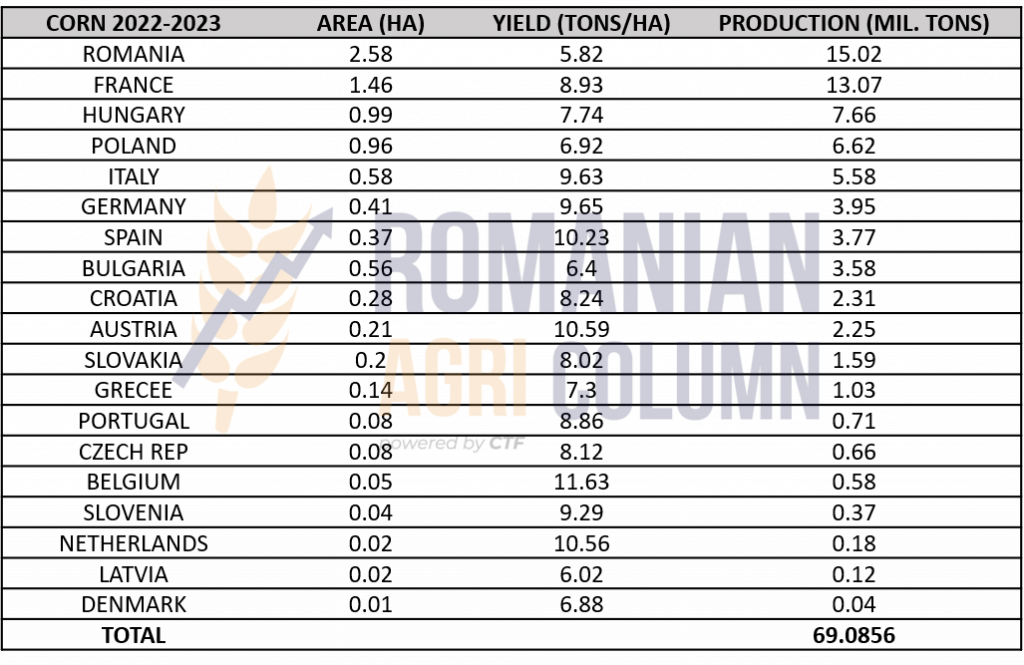

Romanian corn is sown and we see the surface degradation that we anticipated. Starting from an estimate of 2.63 million hectares, it decreases to 2.57-2.58 million hectares. This area is expected to generate a production of 15 million tons. But here too the weather factor will play the main role.

The weather does not indicate precipitation between May 21 and June 4, 2022, which is already a danger in terms of volume projection. We certainly remember the 2020 season and raise a red flag of imminent danger. In 2020 we did not have a rainy winter and so the water supply in the soil was very low in the spring. A few drops of rainfall helped in the emergency and all the farmers were very happy. But they ignored the heat from June to July, as well as the depletion of the water supply in the soil. The first layer of water seeped deeper and was quickly depleted. The surface layer ran out of water and formed a crust, so irrigation was just an unnecessary expense. The water that fell on the ground evaporated instantly, without the possibility of infiltrating the soil.

Enthusiastically, the farmers signed forward contracts on large quantities and thus ended up in the unfortunate situation of not being able to quantitatively execute the contracted volumes. From now on you know the disaster and the cleavage between farmers and buyers. We sound the alarm to temper the enthusiasm generated by the state of today’s cultures. A dry summer will follow and we insist on drawing attention to the fact that any forward signing will lead to drastic penalty costs and financially painful penalty costs.

We say this by measuring the price difference between the indications EURONEXT NOV22 of 365 EUR/MT vs. 315 EUR/MT indications CPT Constanța. Here we have a difference of 50 euros which is not realistic. Let’s not forget that there is a war near us, and the largest corn producer in the area, Ukraine, is under siege. The security of 315 EUR/MT is based on the discounted Ukrainian goods, which are posted at the level of 275-290 EUR/MT CPT Constanța, i.e., at a level of 25-40 EUR below the price of Romanian goods.

REGIONALLY

UKRAINE is starting to move much better on the corn supply corridors, in particular. And we note how the level of exports increases compared to last month to the level of 1.4 million tons (all commodities). However, corn is the highest volume of all goods. The problems of Ukrainian farmers do not stop there. They are actually obliged to discount the goods in order to be able to ship them. The new crop is coming from behind quickly and they will have nowhere to store it.

On 19 May, the European Parliament called for a one-year suspension of EU import duties on all Ukrainian exports to support the country’s economy. This temporary trade liberalization, backed by 515 votes, is a response to the impact of Russia’s war on Ukraine, which is hampering the country’s ability to trade. Measures have been accelerated to allow adoption in plenary. They will completely eliminate import duties on industrial products, import duties on fruit and vegetables, as well as anti-dumping duties and safeguard measures on steel imports for a period of one year.

Taraş Vysotsky, Ukraine’s Deputy Prime Minister for Agricultural Policy, said that most of the restrictions and quotas in the free trade agreement with the EU cover primarily agricultural and food products. The quota for honey was exhausted in two weeks, for poultry, tomato paste, apple juice, cereals and oilseeds – in a few months. For dairy products, the share was much lower than the Ukrainian production capacity.

But this will be done through a Green Corridor, the generic estimate being 20 million in 3 months. As a supplement to this issue, you will find after the price indications of fossil energy and the main exchange rates of currencies, an analysis made by me, Cezar Gheorghe, which was published a few days ago in ZIARUL FINANCIAR, the printed edition and online on ZF CORPORATE.

According to Ukragroconsult, since the beginning of Russia’s war against Ukraine, international traders working in Ukraine have stopped buying grain and are actively starting to ship volumes already purchased through Danube ports and western borders to EU ports and buyers. The creation of new supply chains and good price conditions on domestic and global markets have intensified the purchase of maize not only for foreign exchange contracts with delivery to ports or border crossing points, but also for the ex-farm hryvnia. Rail transport of corn to the western border stations is limited by a convention to Romania, Moldova and Poland. Ukrainian Danube ports in Reni and Izmail improve logistics and increase transboarding.

We clearly deduce from the above the pressure applied by Ukrainian goods on the markets, especially those they cross, Romania and Poland. We suspect that Polish farmers are not happy about this either and want support measures.

There is a big enough issue here that needs to be addressed fairly and transparently. We understand that international traders also want to make a consistent profit and it is perfectly legal. But the conditions are exceptional and we want to apply protection measures for Romanian farmers. It may be helpful for Ukrainian farmers’ associations to communicate effectively with Romanian and Polish farmers’ associations. Communicating and addressing issues can lead to cost-effective solutions for both parties.

We therefore invite the farming communities of Ukraine to dialogue and communication. The contact address is [email protected] .

The EU does not indicate a state of health in terms of the 2022 maize crop. Although the table below and the graph show 69 million tons, our primary indication is a maximum of 67 million tons at this time. The level of EU imports will be at least 15-16 million tons. The dry weather will make its mark on the European crop in the same way we described the Romanian one.

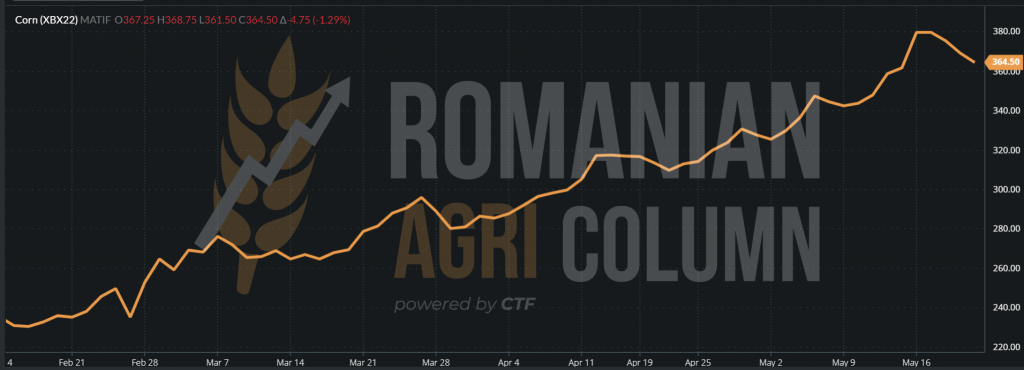

EURONEXT reacts negatively to the announcement of the lifting of tariff barriers with Ukraine and to the news of the creation of the Green Corridor.

EURONEXT CORN XBX22 NOV22 – 364.5 EUR (-4.75 EUR) at the close of May 20, 2022

EURONEXT CORN TREND GRAPHIC – XBX22 NOV22

TENDERS

TURKEY is launching a tender on May 26, 2022 for the purchase of 150,000 tons plus 175,000 tons of corn. Given the specifics of Turkish ports, i.e., many and small, we believe that the goods will come from Russia. Coasters and handies will generate batches of 20,000-25,000 tons. We do not exclude the Romanian and, why not, the Ukrainian origin.

GLOBALLY

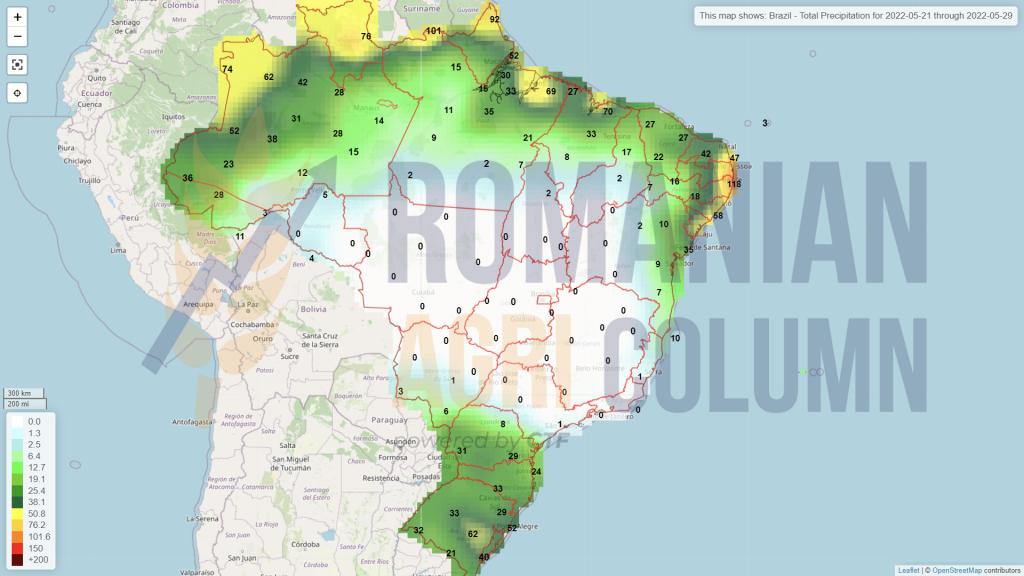

BRAZIL is facing major problems with the second corn crop, Safrinha. Apart from the persistent drought that I have described and which insists on not bringing precipitation to the Mato Grosso area, the southern region of Paraná is experiencing problems these days due to the frost. This can damage Safrinha and can cause volume loss. Already from the forecast of 92.2 million tons, Safrinha decreases to 87.6 million tons. So we have a decrease of 4.6 million tons so far. If we add the loss of about 5 million from Safra, we reach 10 million tons difference from the forecast. We will follow Brazil closely. We have about 25 days until the harvest of Safrinha.

The US is lagging behind the sowing program and we note the level of 50% on May 15, 2022. By the time this report is published, we believe that it has advanced slightly to at least 60% of the sowing area.

US corn sales are strong. As in the case of Brazil, the pace remains high and the cycle is in full swing. Favorite destinations are China, Southwest Asia, Southeast Asia, Mexico and Canada.

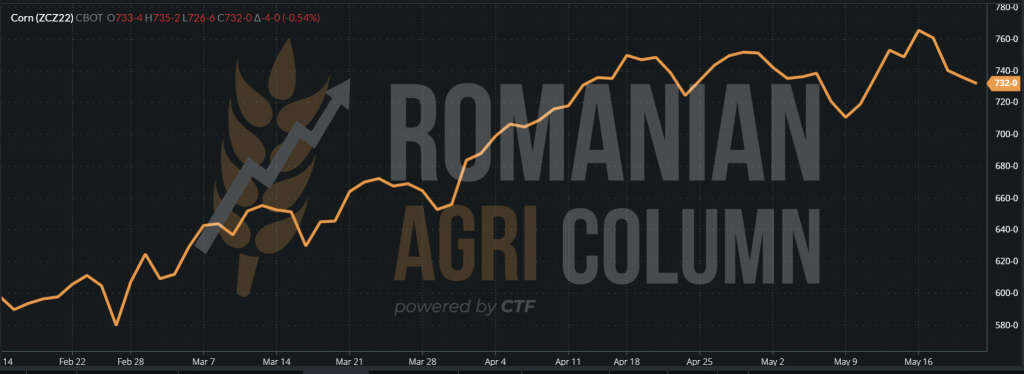

CBOT CORN – ZCZ22 DEC22 – 732 c/bu = 288.18 USD (-4 c/bu = -1.57USD)

CBOT CORN TREND GRAPHIC – ZCZ22 DEC22

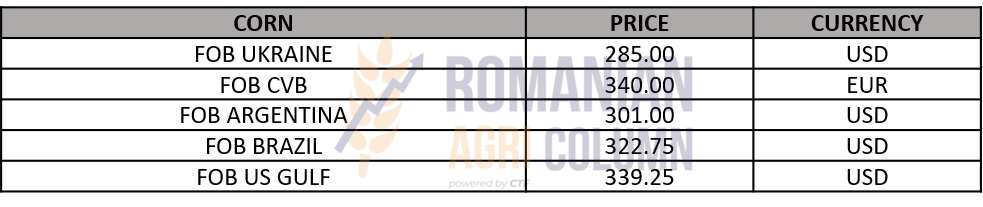

CORN INDICATIONS IN MAIN ORIGINS

ANALYSIS

- Logistics problems in Ukraine are trying to be solved by creating the green corridor. But far from being realistic, this project involves much more than desire and political statements.

- The price pressure will affect Romanian farmers as well as Polish farmers. Ukrainian goods are discounted, generating differences of 30-40 EUR/MT in the same parity, CPT Constanța.

- On the other side of the ocean, Safrinha is declining by an estimated 5 million tons due to the drought in Mato Grosso. The southern region of Paraná is facing frost, which will lead to further declines in Brazilian production.

- The United States is moving slowly but surely toward the end of the corn sowing campaign.

LOCALLY

We refer to an estimated volume level of 1.3 million tons. The USDA suggests 1.35 million tons, but we prefer to be conservative until the end. Hailstorms can destroy large areas at the last minute and we prefer to remain cautious in this regard.

Regarding the price regime, we notice a relaxation of the buyers due to the proximity of the harvest time. And we see how the difference from XRQ22 AUG22 is increasing. If a while ago the indications were minus 4 EUR compared to AUG22, today the margin has increased to minus 8 EUR/MT.

It is clearly and practically the beginning of the harvest pressure, which is exerted with the same repetitive cadence every year. Approaching the time of harvest generates this behavior called harvest pressure. The lack of storage space, the high cost of logistics by about 30% compared to last season, the need to sell, all these things build the speculative scenario of harvest pressure.

Moreover, the effect may be exacerbated by the fact that rapeseed is a cash commodity. It comes with a maximum contribution in the balance of profit and loss of the farm.

REGIONALLY

The European Union indicates a rapeseed production in parameters. However, the surprises that will come from the combination of drought and violent storms that find their place during this period on European territory are not excluded. We all know that June is decisive for the rapeseed crop at EU level and the balance is very fragile. We are still appreciating a lower crop in the European Union due to lack of water and extremely hot weather. Spain and France will be crossed by heat waves with temperatures between 34-39.5 degrees Celsius.

In Ukraine, in areas affected by war and in areas where fighting is taking place, farmers will certainly not harvest. They have no choice. There is no motivation to risk one’s life because of the behavior of Russian troops who kill at random and without motivation.

However, Germany fully contributed to the shock caused by the indication XRQ22 AUG22, by expressing the intention to legislate the replacement of rapeseed oil in the composition of biodiesel. The stated intention is to replace rapeseed oil with 100% used cooking oil by 2030. It is a commendable thing, so a slow transition would be made. Investments in biodiesel plants are very large, and these giants cannot be ignored.

But the quality of rapeseed oil for human consumption will be raised. The level of erucic acid is quite high in European rapeseed, and this leads to heart disease in adults. And it is strictly forbidden for children up to 10 years old. You can mix rapeseed and sunflower oil, but the ratio is 1:5.

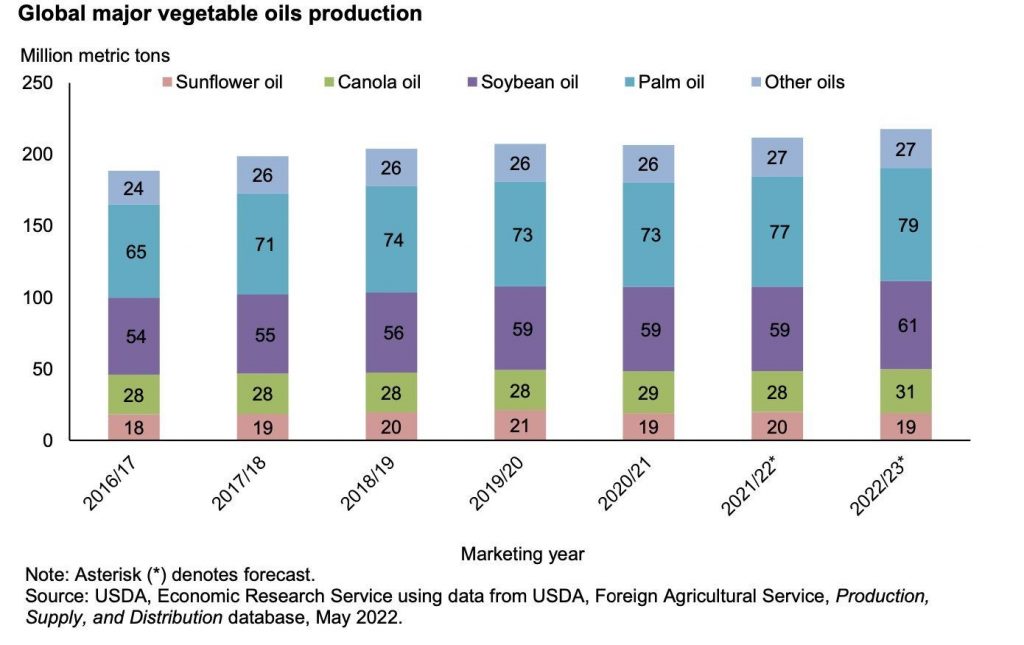

And if we calculate the yield of rapeseed oil at 42%, we have a projection of almost 7 million tons of crude oil at European level coming from a production of 17 million tons. The European projection of sunflower seeds is 10.9 million tons with a yield of, say, 44%, which leads to a level of 4.8 million tons of crude oil.

The proportion is clearly in favor of rapeseed oil in terms of volume. This is a question that needs to be answered. A possible solution would be canola, which is GMO hybrids grown by Canada. The name CANOLA itself is just an acronym for CANADIAN OIL LOW ACID. That is, a GMO hybrid that has inhibited the erucic acid content to the lowest levels. However, we are aware that the European Union does not allow the planting of GMOs. In the end, we believe that this issue is related only to Research and Development and higher genetics overseas. And everything leads to the financial factor. As always.

As a regional conclusion, Germany has made political statements lower the price of rapeseed by EUR 45/MT. The fall in the price of oil, fueled by the US agreement with Venezuela to supply crude oil, has also been a generator of declining oil prices, but not as high as the German political statement.

Indonesia has announced that it has lifted absolutely all restrictions on palm oil exports, which has led to a sharp drop of rapeseed on Euronext, so that after only two days they returned and announced that they will keep the export restriction option for 10 million tons, in order to control the inflation of prices in the local market. Honestly, such things are not to be done. You can’t manipulate prices this way unless you’re a stockbroker.

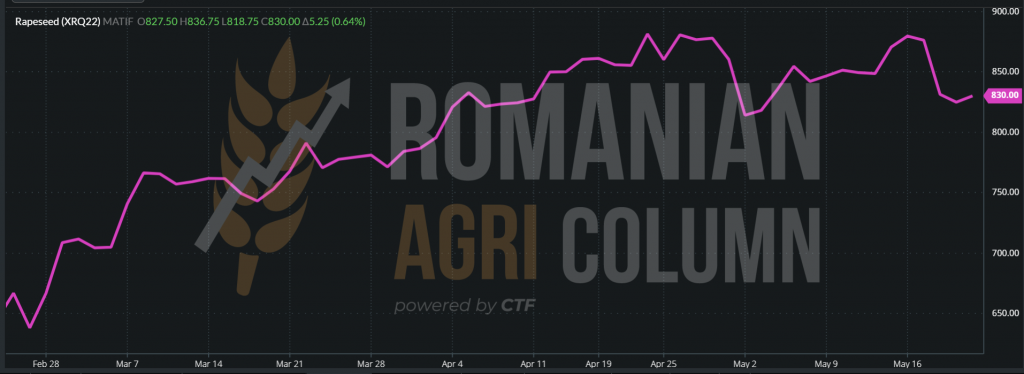

EURONEXT XRQ22 AUG22 – 830 EUR (+5.25 EUR) at the close of May 20, 2022

EURONEXT RAPESEED TREND GRAPHIC – XRQ22 AUG22

GLOBALLY

From across the Atlantic we get news that raises and will support the price of canola and, implicitly, European rapeseed. Canada announced on Wednesday that China has lifted restrictions on imports of canola from Canada, although trade is likely to be limited for the time being due to low stocks. China suspended two exporters in March 2019, citing pests, but political tensions were also high at the time.

Thus, ICE CANOLA quotations have increased, waiting for the potential for a new crop.

RSX22 NOV22 – 1,058.70 CAD (+10.8 CAD)

ANALYSIS

- The weather will be the determining factor in the European price spiral.

- Canada will also be an important arbiter in the whole complex. Half of the global rapeseed-canola is grown in Canada.

- Oil will have its place in the equation, as will the VEGOIL complex, where rapeseed wants to be included, thanks to Germany.

- China’s green wave to buy Canadian canola will boost prices for new rapeseed crops.

LOCALLY

The local market for sunflower seeds remains at the same rates as in previous days, namely 750 USD/MT for the old sunflower seed crop. We also notice the indications of the new crop, which are starting to rise to the quotations of the old crop, so we can talk about balancing them around 750 USD/MT.

It is the beginning of the life cycle of sunflower seeds, in terms of prices and the stage of vegetation. The supreme factors that will influence the road in vegetation and the price will be the weather and politics. The specter of war does not dissipate in any way.

REGIONALLY

The status remains unchanged. Ukrainian sunflower seeds are trying to find their way, but it is extremely difficult. Weak batches of 20,000-30,000 tons cross with great difficulty towards Romania.

- They will not exceed 4 million sown hectares and the level of harvest volume they will generate will be a maximum of 9.85 million tons.

- The sowing forecast raises the level to about 800,000 hectares, with an estimated production of 1.8 million tons.

- It indicates a number of 720,000 hectares, with an estimated production of 0.85 million tons.

- We have a number of 1.3-1.35 million ha, with an estimate of 3.62 – 3.75 million tons.

- EU + UK. We have an aggregate figure of 4.8 million hectares, with an estimated 10.9 million tons.

Again, Romania sets the standard in terms of area and volumes. Looking at the percentages, our country indicates 28% of the total area and a volume of 34% of the total production generated at EU + UK level.

We indicate these figures in order to understand the very important role that Romania has in the European VEGOIL complex. 34% by volume means that you are a raw material generator that supports the vegetable oil industry in the European Union and I would like to emphasize once again the level of added value that is being transferred, instead of remaining local.

If we look at the yields per hectare, France generates 2.25 tons/ha, Spain 1.18 tons/ha. Romania generates 2.78 tons/ha. These are figures that reflect Romania’s potential and I cannot help but associate with Ukraine, which, in the same way, generates raw materials in a very large volume, of about 16.5 million tons on an area of 6.3 million hectares. Their national yield of 2.62 tons per hectare underlines the role of land and water. But Ukraine processed the raw material domestically and did not export it. Here is the big difference and here you can see where the added value remained.

GLOBALLY

Globally, we will explore the potential of sunflower seeds with the help of the USDA.

And what do we highlight in this USDA-generated chart? Firstly, the low level of sunflower seeds, which is 6 million tons lower than last season and 2 million tons higher than in the dry season of 2020. There are very clear signs of reduced raw material in volume, which will feed the VEGOIL complex to the CSFO (crude sunflower oil). However, if we go through a hot and dry summer, the premises of volumes may worsen. The first indications of what the summer of 2022 will look like are not positive. We will have a dry and hot summer in the European Union.

Therefore, the lack of soil water supply as a result of moderate and extreme pedological drought in some areas of Romania and the European Union, associated with high temperatures, will decrease the forecasted volumes. If things go that way, we will have an inflationary spiral in commodity prices. And this, combined with the volume of crude oil that Ukraine will not be able to sustain, will create problems in the European supply chain.

What does the USDA tell us about sunflower oil? A decrease in volume to 2020 of only 19 million tons. A difference of only 1 million tons. However, if we analyze the needs of the European Union for consumption and state the figure of 200,000 tons of crude oil needed coming from Ukraine, we understand that we are talking about 5 months of supply, i.e., almost half a calendar year. It is still a very tight bid signal. It is a sign that things are not at all simple, even in the case of a favorable summer.

And the war in Ukraine is far from over. Russia is playing bluff again. They are sending false proposals to the UN, demanding that sanctions be lifted in exchange for unblocking Ukrainian ports. It’s just another Russian lie. They do their best to keep bombarding and moving the goods on turntables in Kazakhstan and India.

In fact, many German distribution companies have opened accounts in rubles. Switzerland is full of Russian subsidiaries and moving goods, and China will sign a trade agreement with Russia for oil supplies. It is a new bait thrown at the world and the UN has caught on to it this time.

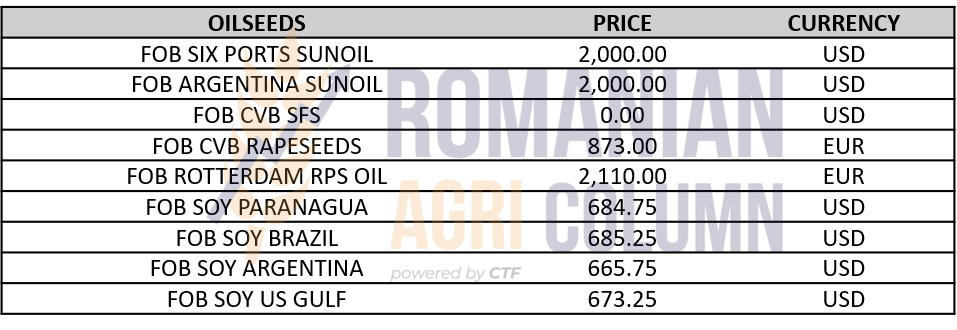

CSFO AND OILSEEDS INDICATIONS IN MAIN ORIGINS

ANALYSIS

- The sunflower decreases in global volume. Of course, Ukraine is the cause of the disappearance of 6 million tons of the projected global volume.

- Sunflower oil is declining globally by 1 million tons. It doesn’t look like much, but it is. It brings us to the level of 2020.

- The weather will be the determining factor in the evolution of the price of sunflower seeds. The low water supply in the soil, associated with a dry summer, could reduce volumes and increase prices accordingly.

LOCALLY

The sowing forecast is 170,000 hectares at the moment. Soybeans need a lot of water and crop rotation is needed for this profitable crop. The coupled support system is an element that supports soy in Romania, but we are far from potential at the moment. From this point of view, we are a net importer of North or South American origin.

Price indications are not present in the market yet, given the period in which we are.

REGIONALLY

EU + UK indicates a production forecast of 2.9 million tons. France has an area of 0.16 million ha, with a forecast of 0.43 million tons. Romania naturally joins here, with 0.17 million ha and a forecast of 0.5 million tons.

GLOBALLY

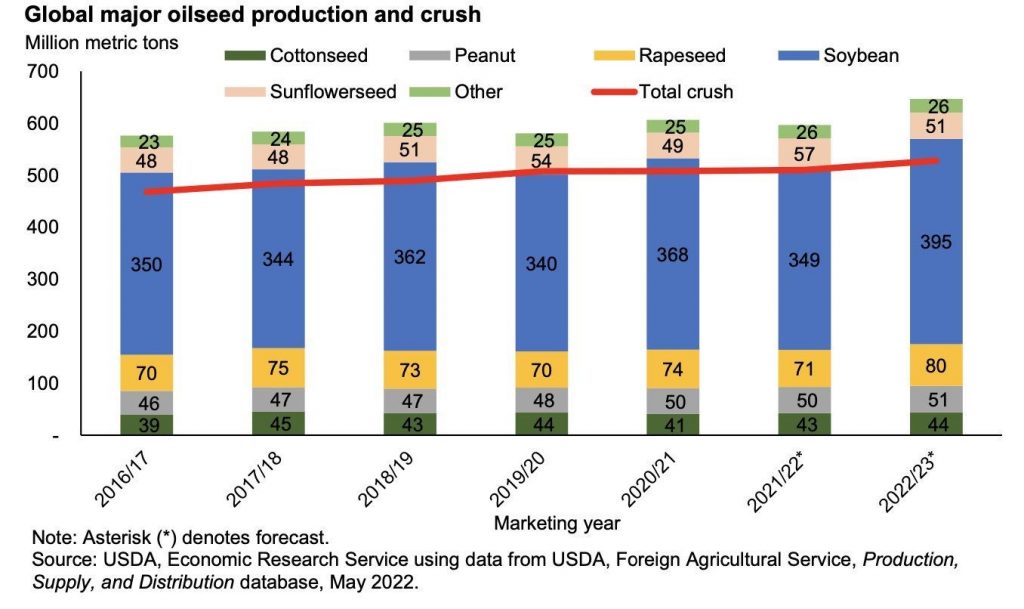

Soybean production is growing for the 2022-2023 season. And we have in comparison May 2021, with a level of 349.37 million tons, compared to the current forecast of 394.7 million tons. The ending season was largely driven by the drought factor. The new season looks optimistic and so we have an increased forecast of 45.32 million tons this season. Forecasts are estimates, of course, but we note here Brazil, with an increase of 24 million tons, up to 149 million tons; Argentina with 9 million tons, up to 51 million tons of production; and Paraguay with an increase of 5.8 million tons, up to 10 million tons of production. The US will add 5.6 million tons and reach a level of 126.3 million tons.

Soybeans are moving and we note transactions here, due to the lower volume for the 2021-2022 season, with the US in the forefront of sales. Normally, soybeans are in the midst of a price cycle, and even though China has a lower appetite due to lockdown and lower default consumption, soybeans are traded at this destination.

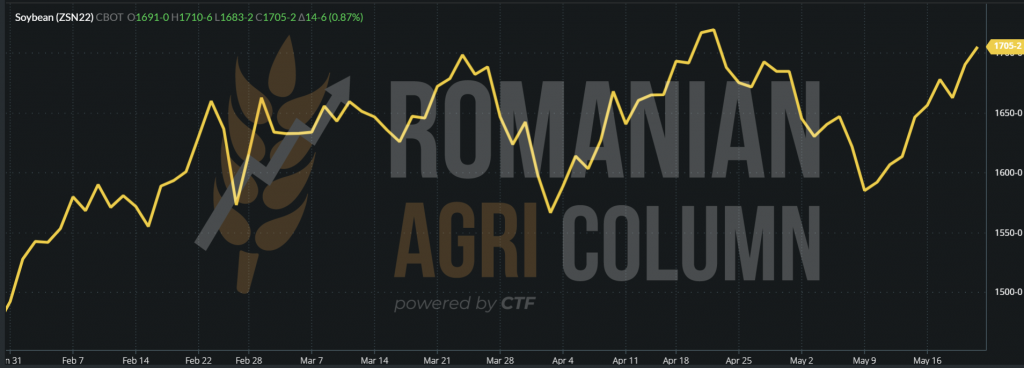

CBOT indicates health and implicit traction in soybean prices.

CBOT ZSN22 JUL22 – 1,705 c/bu = 626.5 USD (+14 c/bu = +5.15 USD)

SOYBEAN TREND GRAPHIC – ZSN22 JUL22

ANALYSIS

- The 2021-2022 crop is supported by small volumes and low stocks.

- The spill will occur with the next crop. The estimated 12% increase in volume will lead to a decrease in price. The difference in indications JUL22 vs. NOV22 is visible – minus 184 c/bu, i.e., 67.6 USD.

- Balancing and calibration will be done by consumption due to higher accessibility, defined by a lower price.

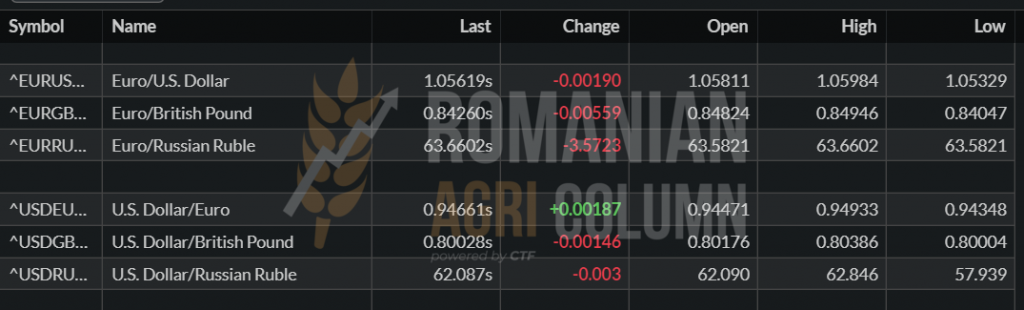

EUR:USD 1:1.056 | USD:RUB 1:62

The ruble is stronger!!!

WTI JUN22 – 113.23 USD/BARIL | BRENT JUL22 – 112.55 USD/BARIL

GREEN CORRIDOR SUPPLEMENT – 20 MIL. TONS IN 3 MONTHS

THE GREEN CORRIDOR AND ANALYSIS OF EACH SEGMENT OF EU PROPOSALS

Judging by the European Union’s proposals for the green corridor and the 20 million tons project in 3 months, we analyze the viability, obstacles and realism in each segment.

- ROLLING STOCK AND TRANSBOARDING: Invitation to all EU countries to send rolling stock to border crossing points to pick up quantities of goods. A simple arithmetic reveals the impossibility of transferring this amount of goods across the border.

To transport 20 million tons you need to load 400,000 wagons or 800,000 trucks. The European Union can replace the green corridor with, say, 10,000-20,000 wagons. You don’t need more, because you can’t actually load in a timely manner. The loading time of a 40-car train is 48 hours.

Suppose that the collective effort will generate a level of 24 hours on the loading of a complete train. We open the border points and assign each one a level of 4 loading lines. We note a maximum number of 8-10 border crossing points, although, if we count these, they are: Reni, Giurgiulesti, Halmeu, Dornești, Izov-Hrubeszew PL and the other Polish crossing points, as well as the one in Hungary.

Mathematics gives us the following results:

10 crossing points * 4 loading lines * 90 days = 3,600 trains, i.e., 144,000 wagons.

In short, only 7.2 million tons in the three months. And this in the condition that everything must work with the precision of a Swiss watch.

- Let’s not forget that trains have to be maneuvered, so locomotives are needed.

- Let’s not forget that the goods must be brought by Ukraine to the border and this means volume of wagons and unloading. You can’t actually unload goods between rails or sideways.

- Let’s not forget that we need transboarding and loading equipment. Where, how many, how are they positioned and how will they operate? They will have to be arranged either between trains or separately.

- Let’s not forget that the goods must be checked qualitatively and weighed, so the 24-hour deadline for a complete train of 40 wagons is completely out of date and out of reality.

ASSOCIATED RISKS: Romania’s railway infrastructure is quite precarious. Let’s not forget the wave of accidents only last year, which culminated in the disaster of the accident in Fetești.

In this context, heat will play a major role. The phenomenon of rail dilation as well as speed and traffic restrictions (passenger trains have priority in the summer season on any route to Constanța) will be real challenges.

We will have multiple congestions throughout Dornești, Halmeu, Reni.

But the biggest problem is the very sharp rise in logistics costs. All private operators in Romania will take over contracts where they are better paid. Thus, the loading-distribution centers in the Romanian silos will be faced with two problems – the availability of the wagons and the very high costs associated.

- BORDER FORMALITIES: Supplementing staff with flexible formalities and integrating goods into the Union without going through mandatory requirements. This is another very difficult element to fulfill, given that at Union level, it is very easy to move from one state to another. Customs workers are almost non-existent and need training to retrain. That takes time, financial and human resources.

THE ASSOCIATED RISKS ARE FINANCIAL. If customs restrictions are lifted, the 9% VAT will no longer be collected by the authorities. Also, without sanitary-veterinary certifications and controls, any goods can enter Romania and I mean the depreciated goods, contaminated with mycotoxins, pesticide residues, benzopyrenes, as well as genetically modified goods.

We need to understand that Ukrainian goods have been parked in storage for a long time, and we must not overlook the excessive humidity during the harvest of Ukrainian corn in the fall of 2021. Then there was a major problem, because it still had to be dried and there were not enough facilities to perform this process. The goods arrived from the field with a humidity of 20-22% and, certainly, this affected the quality of the goods that were introduced in the storage locations.

- STORAGE OF GOODS IN THE EU: The storage of the goods for a period of time in the locations in Romania is somewhat difficult, given the fact that Romania starts harvesting in a maximum of 30 days. And we wonder what owner of a silo or storage base will occupy its storage space with goods from Ukraine, when the harvest will arrive in waves in Romania, i.e., barley, rapeseed, wheat, sunflower and corn? Who will block the space while waiting for their own crop? It’s a two-way question. One is about the time of sale of the crop, because it wants to preserve its potential future, in the conditions dictated by the weather globally. The second sense is about costs. Electricity and fossil energy have reached very high levels and prices for services have reached a level of 70% compared to last year.

ASSOCIATED RISKS: the exponential increase in the costs of providing services on the Romanian market. As the market is presented today, prices have increased by 50-70% on all levels of services: reception, conditioning, drying, aeration, fumigation, recirculation, storage and delivery. It will be an option that any silo/base owner will take – at a higher income he will prefer goods of Ukrainian origin, to the detriment of Romanian goods.

- PORT OF CONSTANTA. The takeover capacity of Constanța port is the weakest link in the chain. Triage is not capable and does not have the operational power to take over this estimated volume of cargo. If we judge only 500,000 tons per month, we have a number of 10,000 wagons that must be received and directed to the terminals. The port of Constanța is traditionally blocked during summer, when the wheat harvesting campaign begins. Logistics in the terminal begins with the end, in the sense that the goods are waiting for the ships, not the other way around. The storage capacity of a terminal is 180,000-220,000 tons, in the case of high-performance ones. However, this capacity is divided into commodity categories: barley, rapeseed, old crop corn, milling wheat and feed wheat. And a metal cell in the port of Constanța has a capacity of 8,000-10,000 tons. This means that if you put 4,000 tons of corn in an 8,000-ton cell, you can’t put anything there but corn. So space is being lost.

The terminals are assaulted by cargo offers originating in Ukraine. We are talking about corn, wheat, sunflower seeds and crude oil. We note very large discounts between Ukrainian and Romanian origin. For wheat and corn, the discount reaches 35 EUR/MT. Naturally, the buyer goes for the cheaper goods. Logistics costs are extremely expensive. The transboard in Giurgiulești reached 30 EUR/MT, the barge from Brăila/Galați to Constanța doubled from 10 to 20 EUR. One ton of sunflower seeds cost only 120 USD/MT for the logistics fraction between Ukraine and crossing the border into Romania. Transboard services are actually being auctioned off and whoever gives the most comes first.

ASSOCIATED RISKS: decrease in the value of Romanian goods. Romanian farmers must be competitive in the face of this flow of goods. Because a value of 0.5-1.2 million tons of goods per month that will penetrate Romania actually means a maximum value of 50% of what Romania produces in 2022. Thus, the Romanian goods will be corrected with the discount that the Ukrainian goods have. The costs of setting up one hectare in Romania are much higher than the costs of setting up in 2021 in Ukraine. I fully understand the need to sell these goods, but this discounted flow of goods will reach lower prices in the EU, with all the benefits at the end of the supply & demand chain, whether in the EU or in areas in desperate need of goods. (North Africa, West Africa, Central and Sub-Saharan Africa).

21-29 May 2022

Romania

Europe

Ukraine

Russia

Canada

USA

Brazil

Argentina

China

Australia