This week’s market report provides information on:

FOREWORD

INTROSPECTION INTO THE LOGISTICS COMPLEX

The port of Constanța is preparing for July, a month that will definitely mark historical records. Last month was just a test of abilities and the past few days have seen shipments of goods from the 2021 crop.

The month we are stepping into is one full of historical challenges due to the confluence of raw material flows that will come from two major directions. The first one is the Romanian flow of goods, because Romania steps in the days of wheat harvest, mixed with the rapeseed and barley harvest.

On the other hand, there are also the goods from Ukraine coming on the established routes, even if the path is very narrow at this time. Ukraine ships its goods and the main flow is, as we well know, corn, but in their country as well as in our country, wheat is beginning to be harvested.

The third flow that is beginning to be seen is that of neighboring Serbia, a country that has restricted exports at the dawn of the war in Ukraine and these days is preparing to raise barriers. This will release large stocks of goods, about 1 million tons of wheat and about 1.5 million tons of corn.

So we will have the most difficult month of 2022 and the difficulties are on the horizon. The logistics complex will be fractured into many segments that will not interlock accordingly. The transport will not connect according to the demand for available units, the time spent between Loading and Unloading will be substantially increased due to the heat wave that will slow down the movement.

Railway conditions already have a first victim, namely a train composed of Ukrainian wagons with goods that derailed in the area of Moldova. The barges will not be in sufficient numbers to be able to serve the demand and we anticipate a decrease in the Danube level, which will make the upstream terminals in Romania remain captive with goods.

Downstream, in the port of Constanta, the terminals work, and operational excellence is a norm implemented by the companies that operate them. But until the moment when the goods will be unloaded, from wagons, from trucks, from barges in the condition of FAS (free alongside vessel), time will flow inexorably.

The suffocation in the triage of the port of Constanța will be a brake that will condition the unloading rhythm of the wagons. If in the past years we had situations in which a train waited about 10-14 days before being allowed access to the designated terminal, in 2022 we will have much longer times. The authorities reacted as we know they do.

Reactivity is one of the features of our system. The lack of vision and anticipation in line ministries has always created insurmountable problems. This has been methodically happening for over 30 years due to the poor technical quality of the human resource. Unable to anticipate, effectively vegetating in the shadow of an easy job without responsibilities or measurable performance indicators, the actual crisis we are in and which was already measurable since February 22-23 was treated with appalling lightness. The lack of technical knowledge, the lack of responsibility, the hierarchy, and the autocracy of the directors have made this system be perpetuated for over 30 years. And now it cracks and cracks all over. We see rags on the railway structure, we see how they try to restore small parts of the railway to allow access to wagons from Ukraine, with teams of poorly equipped workers, with shovels, just like when the railway was built in the Wild West as it was called in that pioneering period: “the prairies of the United States of America.”

Returning to the port terminals, they have an operational discipline and a ship arrival time, set well in advance. This programming takes into account a very important parameter, namely, the cargo is waiting for the ship, not the other way around. This parameter in turn conditions the unloading of goods in terminals because we have many categories of goods that must be segregated on qualitative criteria. This slows down the reception, the bunkers do not support a change in flow without prior cleaning.

As a final conclusion of the above, we will face an extremely difficult period, one in which the logistics complex will be faced with extremely many problems, one in which we entered completely unprepared, just like a student who takes the exam without learning and understanding the lesson.

LOCAL STATUS

The port of Constanța closes on Friday, 1 July, with indications that value the milling wheat in a price range that starts from 345 EUR/MT and can reach 350 EUR/MT; the discount for feed wheat is 20-25 EUR/MT from the price of the milling wheat.

The wheat processing industry indicates similar values in the country, it is the time when the harvest pressure will supply the market with volumes so that the demand and supply in a free market will generate fair competition between the Internal and External Market.

Many farmers have not sold yet; those who waited extremely long actually missed moments of sale.

Some farmers sold between 20-40% of the crop. Those who sold did very well because in this way they collected the important moments in the market and consolidated the incomes of the farms.

In each report to date, we have provided consistent information about the market and its course. We offered coherence in the indications and in the Agrojurnal weekly appearances, every Sunday from 9.00-10.00 on the generalist station DIGI24.

Today, however, we face the acceptance of reality, namely, that despite the war as a political factor that has become a daily reality, we have long anticipated the correlation with the stock market factor that was determined by Federal Reserve policies to correct the indications of raw material prices.

In all this context on 29 June 2022, Egypt went out to tender for the purchase of 2022 crop wheat. And we see a sudden change in behavior. A massive wait and a slow and latent level of acquisitions, with low volumes purchased so far, in an attitude of “stockpiling” to conglomerate the interest in securing the volume.

The wait and then the massive inflow of the purchase was due to the lack of money initially so that later Egypt could access a loan of 500 million USD from the World Bank in order to support the subsidy of bread domestically and thus generated the tender for the purchase of wheat.

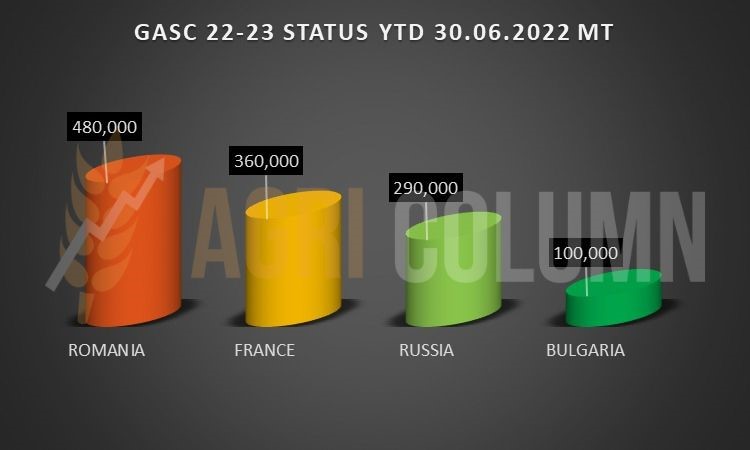

In conducting the tender, we saw the competitiveness of the European Union against Russia and thus France won its lion share in this transaction followed by Romania. We also noted the list of initial bidders with volumes that reached the level of 2.9 million tons of which 825,000 tons were purchased according to the summary below. Payment will be made by the Egyptian state upon delivery, so not 6 months guaranteed by credit letter.

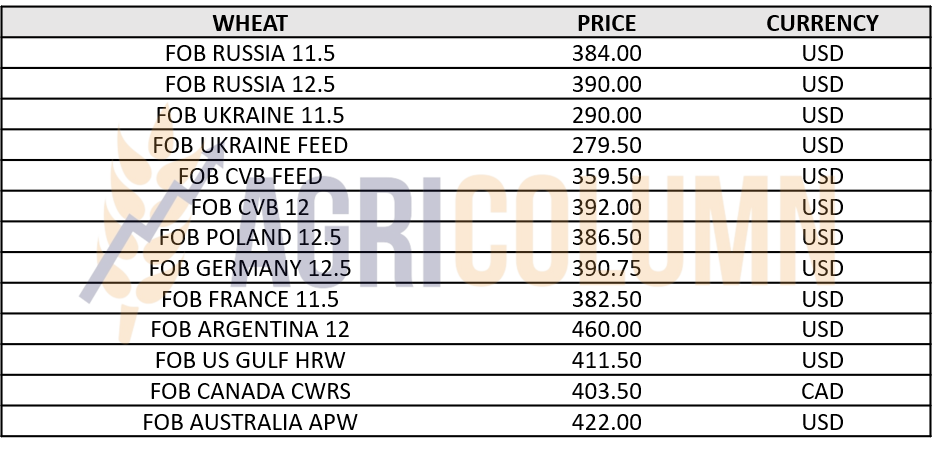

At a simple calculation, Romanian wheat has a FOB value of 384 EUR/MT.

FULL DETAILS – GASC EGYPT TENDER, 29 JUNE 2022

ROMANIA leads the GASC sales to Egypt in 2022-2023 so far.

CAUSES AND EFFECTS

Prolonged retention of goods and not engaging them in the market will create a feeling of frustration that will lead in many cases to a prolonged retention, in the case of farms that have storage space.

Farmers in areas affected by extreme pedological drought suffer the most. With productions between 2 and 3 tons per hectare, the latter cannot cover the costs of setting up and the balance of income and expenditure will bear the negative shock.

The wait was not a key to success, the level of 415 EUR/MT offered on peak days in the port of Constanta was just a scaling on the commodity market of the conflict in Ukraine correlated with stock market inflation by Funds fiercely looking for positive margins for the money that had no margin.

We will have, according to the independent systems for measuring the vegetation indices, a crop of over 9 million tons in the end. This does not endanger the internal food security in any way, but also generates a substantial surplus for export.

The technicality of sales is an extremely important chapter for farmers. The prolonged wait generated by the sight of a historical price created a misunderstood security. The foundations of this world are completely different. Global food security is the main parameter in maintaining social order and stability and it was extremely predictable that the “pain threshold” or “affordability limit” was reached.

Proper information and sales structuring is a farmer’s most useful ally. And tradable insurance instruments are extremely valuable. They effectively secure the financial interests of the farmers, while leaving the freedom of choice in the physical market at the time of sale. And as the best example is the mathematical one, a price difference taking as a benchmark, not the peak, but a figure of 400 EUR/MT compared to the level we estimated to be related to Monday, namely 330-335 EUR/MT means a minus of 70 EUR/MT, which multiplied by 4,000 tons, say, leads to the figure of 280,000 EUR, with a minus in front of course.

Proper information and sales structuring, covered by tradable insurance are the elements of revenue control and securing them in the extremely complex set of trade. We provide you with all the details and implicitly the access to the tradable insurance instruments. Romanian farmers must modernize and be actors with a response in the local, regional and global agribusiness scene.

Large traders have them and use them, thus securing any transaction they make in the market, whether we are talking about buying volumes from farmers, or we are talking about selling them to Destinations. In short: [email protected] gives you the necessary details and how to access these services for insurance and structuring sales of goods.

REGIONAL STATUS

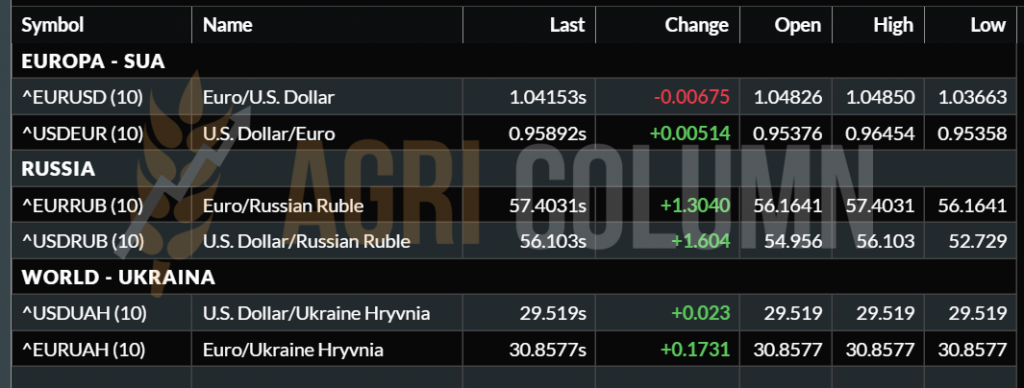

RUSSIA was still under immense pressure, as I stated in the last issue. Russia is not competitive at all in the export of wheat, their main resource, and weapon used as blackmail. In the last GASC Egypt tender, this was highlighted. All their Kremlin-affiliated analysts have failed to influence the market so that the world can fall into the trap that they can blackmail the world with their volume of wheat. The Russian domestic market pays much less for wheat than before the invasion of Ukraine. The ruble has strengthened against the US dollar and the ratio today is 56 rubles for 1 US dollar. Before the invasion, we had a level of 75 rubles for 1 USD.

A summary calculation, taking as a benchmark a random price of 400 USD/MT, in the FOB Novorossiysk parity, indicates a level of export tax of 140 USD/MT. Apart from the fact that this tax fed the Russian war machine, it reverted to the Origin – that is, the price fell in the yard of the Russian farmer.

If we extract the fobbing costs of a minimum of 20 USD/MT, the margin, and the transport of the goods from the FCA Farm parity we reach a maximum level of 200-210 USD/MT. For convenience, we keep the 200 USD level as a benchmark in the FCA Farm parity. From here we have, 200 USD * 75 rubles = 15,000 rubles before the conflict, compared to 200 USD * 56 rubles = 11,200 rubles. A minus of 3,800 rubles per ton in the farmer’s yard.

If we take the calculation to the export price with the export tax included, things get a much bigger difference:

Before the invasion: 400 USD * 75 rubles = 30,000 and currently 400 USD * 56 rubles = 22,400 rubles. Thus, apart from the fact that they are not competitive at all due to the tax, they lose money for every ton sold due to the USD/RUB parity.

Thus, from July 1, 2022, Russia changed the taxation from USD to RUB. Therefore, the level from which the taxation starts is 15,000 rubles, i.e. 268 USD (according to the parity of 1 USD: 56 RUB). In these conditions, in which the price estimate in the parity of FOB Russian ports is 387 USD/MT, subtracting from the FOB price the level from which the taxation starts of 268 USD, results from a value of 119 USD which is subject to taxation by 70%.

The actual tax export displayed by MOEX is 85.20 USD, down from 146 USD. The difference of 61 USD will be reflected in the future price of wheat in weighted form. That is, it will influence the declining global market, but it will be used as a space for maneuver to facilitate the export of Russian wheat. And Russian exports, which are under maximum pressure to be sold, are also fueled by the internal pressure of the harvest. The level of 42-45 million potential tons to be exported is composed of the own crop from 2022, the rest not exported from last season, and the theft of wheat from Ukraine.

UKRAINE remains at the same production level estimated at 22 million tons, but information indicates that export licenses for wheat are suspended. It is a logical move due to the fact that the richest area of wheat production is in the South-East, even in the middle of the war, and the harvesting and transfer of goods cannot be controlled. In other words, Ukraine will try to provide food for the population.

The EUROPEAN UNION receives a degradation of over 5 million tons allocated to wheat for consumption. Starting from a forecasted level of 130.40 million tons, the new projection is 125 million tons with the largest reductions allocated to France and Spain.

EURONEXT DECREASES FRIDAY, 1 JULY 2022, IN RESPONSE TO THE CHANGE OF THE RUSSIAN TAX. MLU22 SEP22 334.50 EUR (minus 15.75 EUR)

EURONEXT TREND GRAFIC MLU22 SEP22

GLOBAL STATUS

The USA issued the report of areas and stocks related to 30 June 2022. We find the negative differences from year to year in terms of wheat stocks allocated according to the grid, on the farm, outside the farms and the rate of disappearance. Regarding the allocation of areas, referring to the sowing intentions of 1 March 2022 compared to what was done, we have a negative difference of 107,000 hectares that will influence the total production, depending on the yield of spring wheat. For now, however, American spring wheat looks very good, being the beneficiary of recent rainfall.

CANADA indicates the same positive status and the forecast remains at over 33 million tons.

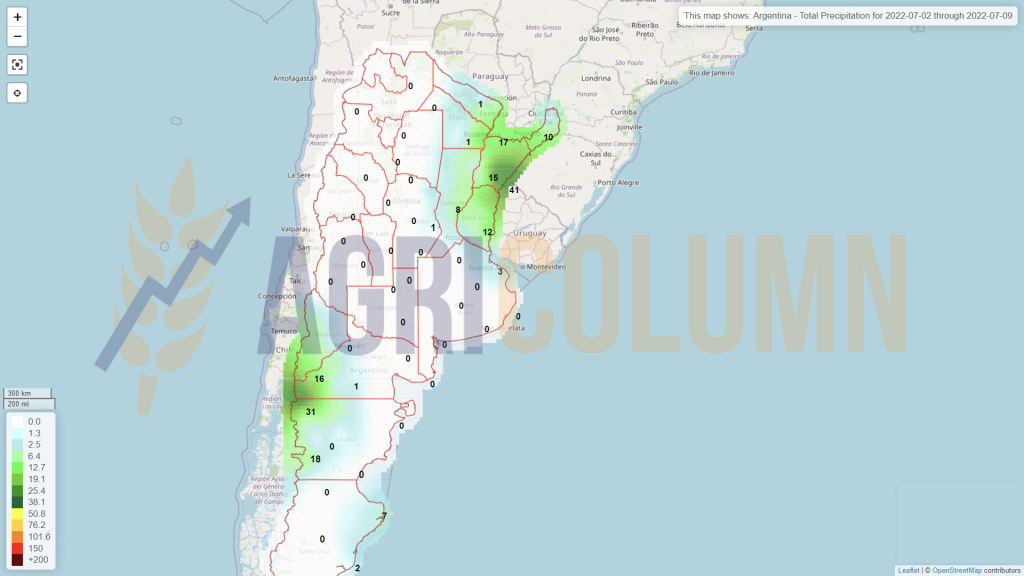

ARGENTINA does not look good at all due to the lack of precipitation that affects the rhythm of sowing.

INDIA admits below 100 million tons in terms of production volume, but cooperation with Russia is not a cause for concern, as they are already exporting more than 1.6 million tons of wheat.

In the international line-up can be identified an expedition Novorossiysk/Tuapse – Nahva Sehva July 1-15 50,000 tons.

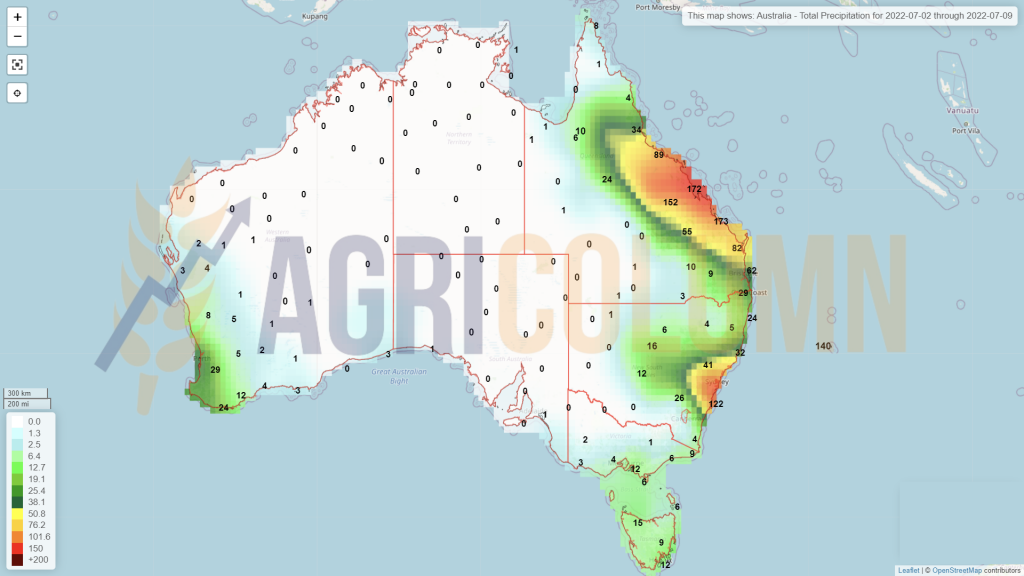

AUSTRALIA indicates the same very good state of vegetation, and the indications remain at 32 million tons.

TENDERS

- OAIC Algeria purchased 740,000 tons of wheat in an tender. Delivery 1-15.08 and 16-30.08. The origin appears to be European. The price estimate is 445 USD CIF due to the fact that OAIC Algeria does not provide details.

- JORDAN purchased 60,000 tons of wheat at tender from CHS at a price of 445 USD CIF Aqaba with delivery 16-30.09.

- SAGO – SAUDI ARABIA purchased 495,000 tons of wheat in an international tender for delivery from November 2022 to January 2023. SAGO said the average price for purchased wheat was $ 441.93 per ton. The origins offered were the European Union, the Black Sea region, North America, South America and Australia, the seller having the option to select the supplied origin.

CBOT STEP DOWN AFTER NEW LEVEL OF RUSSIAN TAX WITH 38c/bu (13.96 USD), ZWU22 SEP22 step down at 846c/bu.

CBOT GRAPHIC TREND ZWU22 SEP22. The same level as the days when war started.

Russia’s announcement of the tax change has led to a decline in the wheat market since the beginning of last week. On Friday, it was only the culmination of the ruble tax set that generated a low level of taxation, which induced a room for maneuver for Russia in an attempt to become competitive again.

The effects of the FED still create shock waves at the collateral level. The funds leave positions at expiration and the end of JUL22 as an indication amplifies this.

The imminence of new interest rate increases in July 2022 and, implicitly, the increase in the price of guarantees make the caution of funds to be maximum at this time.

The weather is also a correction factor in the stock markets. US rainfall projections facilitate stock market declines. Energy also has a share of the decline.

The physical market is corrected but it will trade according to supply and demand and it will be no surprise for anyone to trade at a price equal to Euronext SEP22 in the parity of CPT Constanța 2022 wheat crop.

Retraction of Sellers and retention of volumes will be an implicit and anticipated phenomenon. Farmers who waited and did not sell, fueled by the concept that growth will not stop, will store the goods. But getting used to the current price level will come in time like anything in this world.

Investment Funds will return to growth after these liquidations of over 8 billion USD. It will, however, be a compliant and customary action governed from now on by the financial cost of guarantees, weather, and volumes of goods.

Declining volumes of goods from the European Union will be offset by the Black Sea basin, Russia has clearly stated its intention to get out of the pressure it is in, and the Northern Hemisphere through Canada, the US through spring wheat, and Australia through volume will restore a balance in terms of volumes.

Russia’s move to change the tax in rubles is moving in two directions. The first is to support farmers who received much less money on their wheat due to the appreciation of the ruble against the US dollar. The second is the intention to become competitive in the market, the factors accumulated from sanctions and high prices have placed it at a much lower level of export in the last 8-9 months.

Withdrawal of funds from stock exchanges, aggregated with the price of the latest international tenders, clearly indicate an oligopoly formulated by multinational companies operating in the physical market interconnected with investment funds.

This oligopoly always forms the points where profit accumulates; their interconnectivity generates profit in the physical market when the investment funds are withdrawn because they will buy at a lower price level in the physical market (generated by the decrease of stock exchanges) than the level at which they made sales.

And the reverse is when the interconnected funds artificially raise the market based on headlines (rumors, news) and then come out performing profit taking at an interval of 2-3 days, the companies in the physical market remaining dormant all this time. This global oligopoly does not lose in a moment, but only artificially creates the environment. Artificial price increases have also scaled the cost of fertilizers, the logistical cost and ultimately the extraction of money from the population to meet the negative margins generated by the excess financial liquidity caused by printing money to support savings during the pandemic. Looking at it objectively, a ton of wheat looks the same when it costs 180 euros and when it costs 400 euros.

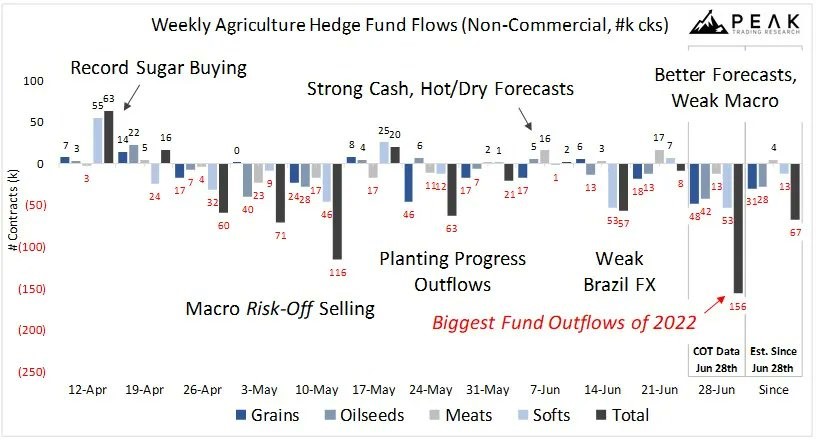

PREVIOUS WEEK SUMMARY, Credit Peak Trading Services. In the lower right, we have the indication to leave the positions with the highest level in 2022

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

LOCAL STATUS

The indications of the port of Constanța for barley vary between 300 and 310 EUR/MT, depending on the coverage of the Exporter and the urgency of the coverage. July will continue to generate barley exports, Romania being at this time a sustainable and predictable origin. Sales made with October 2022 deliveries indicate at this time a decrease in price, the correlation with the price of feed wheat is a benchmark.

The barley price will be repositioned after the decreases that took place on the stock exchanges on all levels of products.

The Romanian barley crop is below last year’s indicators. Yields per hectare are not the desired ones, especially in the areas affected by extreme and moderate pedological drought, the impact was felt by farmers through productions of 2-3 tons per hectare accompanied by a substantially reduced of test weight.

REGIONAL STATUS

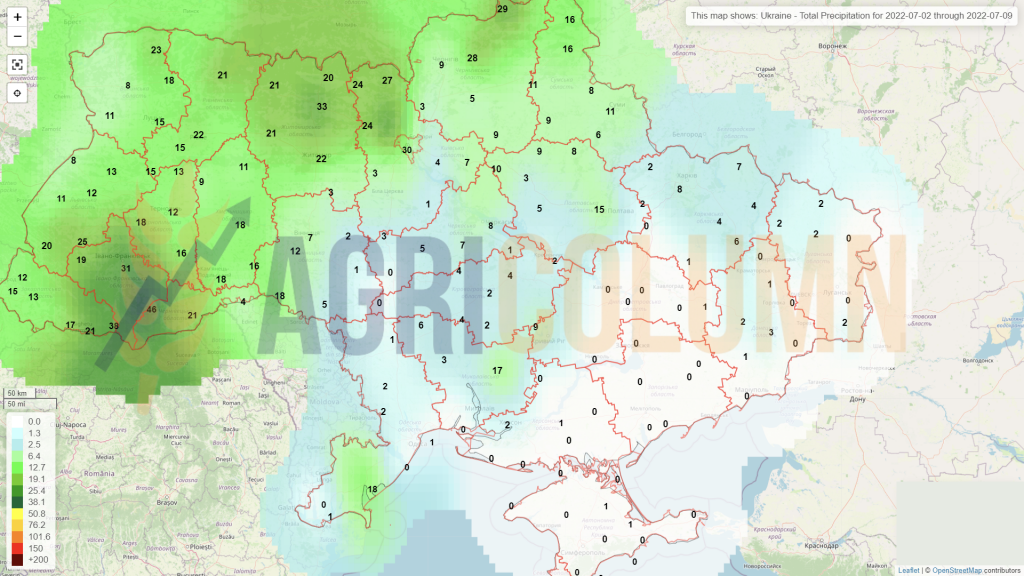

UKRAINE. The first harvested areas do not indicate satisfactory production. The expected production of 5.7 million tons could be lower. In the Odessa region the yield is about 2 tons per hectare which is ½ from last year’s yield. The export cannot be done so that the barley in this region will be stored in warehouses by farmers.

EUROPEAN UNION. After France with a 5% lower barley yield, Germany indicates the same percentage of barley yield.

JORDAN intends to buy barley by tender but until now we have no definite data on volumes and price.

CAUSES AND EFFECTS

Low yields in the European Union are not disastrous, so production is below last year’s level without the effects of rising prices.

The price of barley follows the correction curve of the other raw materials and starting today, we could see the level of 285-290 EUR/MT in the CPT Constanța parity.

Demand will continue steadily due to the reduction in volume in the European Union and the lack of volume in Ukraine but the price will be corelated to the price of feed wheat.

LOCAL STATUS

The local corn market indicates through the port of Constanța the level of 260-272 EUR/MT in the CPT parity for the new corn crop. Quotations subsequently decrease with the levels indicated by the stock exchanges. On the last day of last week, the degradation was 10 EUR. The old crop is also purchased sporadically. The impact of the quotations of Ukrainian goods in DAP Halmeu, DAP Reni, and DAP Constanța is undoubtedly felt.

But what we need to know is the level of port services for Romanian goods versus Ukrainian goods. These are separated by a considerable gap. If for the Romanian goods the fobbing values are at the level of 7.5-10 EUR/MT, the Ukrainian goods have operating costs of 30 EUR/MT.

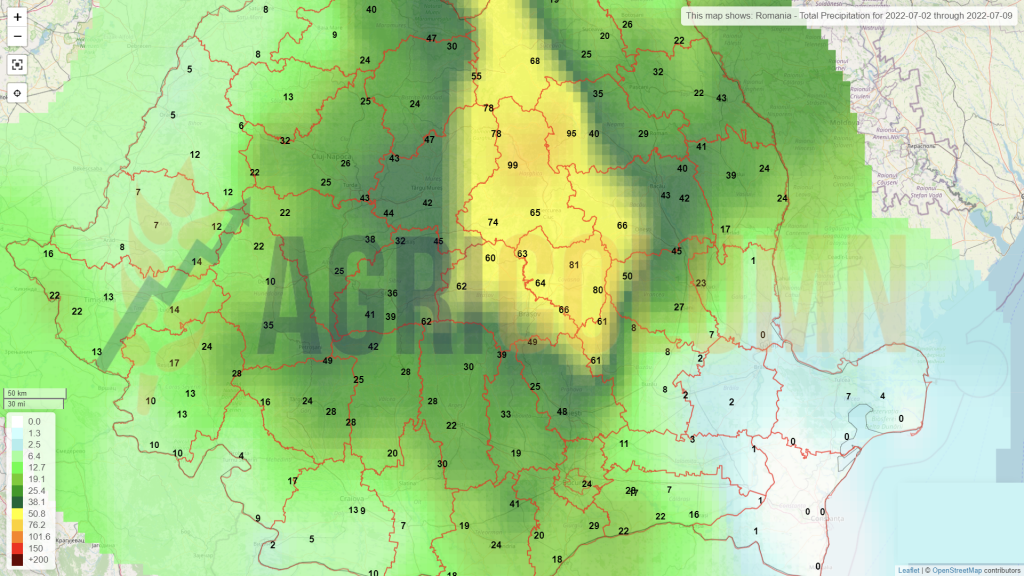

Romanian corn is in full vegetation and still looks good. We still say this because we have deep signs of concern about the crop. During the winter, the water level in the soil was not completed from snow falls and rains and is now at a critical level. Aggregated with the heat wave that is crossing our country these days, these two factors could lead to a degradation of the corn crop.

Especially in areas with excessive and moderate pedological drought, we could see a dizzying drop in the national harvest volume estimate. The heat wave that crosses Romania on the background of the lack of precipitation generates the formation of the crust at ground level and thus even the future, potential rains, will not have the desired effect. The water will evaporate from the soil covered with crust, making it impossible to leach into the soil. The crust plus temperature will quickly contribute to the evaporation of water, whether it comes from rain or last-minute irrigation as the final solution for saving crops.

CAUSES AND EFFECTS

The decrease in price is a reason to wish to conclude forward contracts. Price volatility and the downward trend led to this desire: 2 tons per hectare, a maximum of 3 are desirable to be signed.

Future signs do not indicate a return of corn in the price trend. The weather factor is favorable on other continents and influences, together with the decisions of the Federal Reserve, the price in a negative trend.

REGIONAL STATUS

UKRAINE indicates the same good status of the future corn crop, namely 27.7 million tons of total production. But the problems are the ones we all know and have seen absolutely no improvement. Collaborating with our colleagues in Ukraine, we tried in an exchange of information to better understand certain phenomena.

And what has not seen in public are things related to actual trade. This trade aims only at profit in a way that has become cross-border, without taking into account the possible damage it creates in crossing certain areas.

The other day I noticed a maximum exaltation at the level of traders’ associations in Europe, celebrating as a great victory the fact that the Romanian State gave up the veterinary sanitary certificate for Ukrainian goods, especially corn. We were extremely surprised by this undisguised joy generated by COCERAL and some of their exponents. At the same time, COPA-COGECA disagrees with this measure because all traceability and control of goods from a qualitative and fiscal point of view effectively disappears. From the very beginning, we want to emphasize very clearly that we have all the empathy for Ukrainian farmers and that is why we are pointing out certain things, in order to have access to information publicly.

Traders that operate in Ukraine had stock-pilling behavior in the run-up to the war and amassed impressive stocks of goods. These goods had a purchase price granted with that period, so very low compared to what we see today.

All the effort of the traders is directed in fact for the extraction of the goods from Ukraine, of the lots bought contractually, because the force majeure does not exonerate you from contractual execution in this case but only postpones it. Thus, all the combined effort of many traders is directed only to profit effectively.

The goods are contractually fixed and must be extracted because the profit considering only a price difference between the data before the start of the war and those of the days we went through is really dizzying. The humanitarian stories in front of the actions are just smokescreens so as not to generate questions and discussions. But in the back, the goal is clear and well defined, the profit in this case, the big profit.

Returning to the elimination of the obligation to present the veterinary health certificate, we have some immediate problems to indicate and we bring them to your attention.

DISPOSAL OF THE VETERINARY HEALTH CERTIFICATE is a totally wrong decision. In this way, absolutely nothing can be controlled regarding the qualitative condition of Ukrainian goods as well as their destination.

Recall that the 2021 crop of Ukrainian corn had some problems in term of humidity and therefore needed drying from 18-22% humidity to the commercial standard of 14%. Due to the high costs of gas (drying process) and the availability of dryers, these goods were stored without this process being carried out in most cases, taking into account a crop of 42 million tons of maize. Today, after so many months of stagnation, that commodity is actually depreciated and full of mycotoxins. The high level of aflatoxin, an element that seriously harms human consumption but also the feed destination, must also be discussed.

In addition to these qualitative parameters that will be omitted from control, we must also remember that the cargo that is actually blocked in the 70-80 captive ships in Ukrainian ports in February is depreciated. You can’t store cargo transfer, to ensure aeration and fumigation operations for so long in ships’ barns. By eliminating the veterinary health certificate and compliant quality checks, Pandora’s box has been opened and, thus, dangerous goods will enter the EU in terms of Food & Feed Safety standards, according to European legislation. There will be no more implicit traceability. The goods will lose track after crossing the border and no one will be able to control the real destination or the quality condition. Due to the low price that naturally provokes temptations, it will be purchased by processors in Romania that will generate products that are potentially harmful both to the country’s population and to the livestock and poultry industry.

RUSSIA also changes the export tax on corn and thus it is lowered from the level of 88.66 USD/MT to 40.16 USD/MT. 48.50 USD disappear according to the same formula as for wheat. We also have the same production forecast status, namely 15.5 million tons, with an export level set at 5 million tons.

THE EUROPEAN UNION has the same forecast status but with a correction of 2 million import level. Thus, this level increases to the value of 15 million tons.

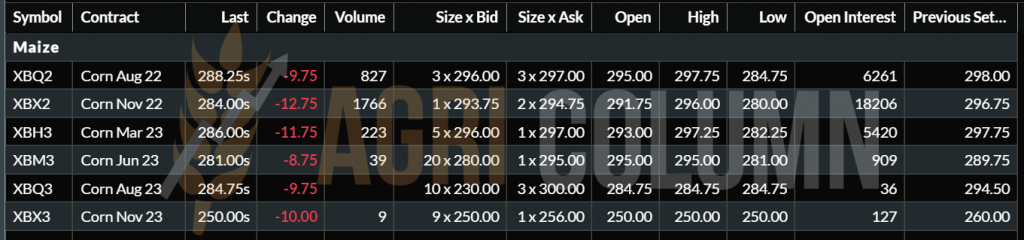

EURONEXT CORN XBX22 NOV22 284 EUR (minus 12.75 EUR)

CORN TREND GRAPHIC – EURONEXT XBX22 NOV22

GLOBAL STATUS

Through the NASS report, the USA indicate higher stocks of corn nationwide compared to June 2021. At the same time, comparing the sowing intention from 1 March 2022 we see an increase in area by 175,000 hectares at a yield displayed by the last USDA report, namely 11.10 tons per hectare, which will bring a surplus of 1,925,000 tons of corn in American production.

BRAZIL indicates an increase in the crop by 3.3 million tons, from 116 million tons to 119.3 million tons. Logistical problems start to appear in Mato Grosso due to insufficient storage space and it is obvious in this way the surplus of Safrinha after Safra (the first crop) was disappointing. The forecast for the future crop is 126 million tons, so the minus of this season will not be 10 million tons, but only 6.7 million tons, a deficit that can be balanced from the 2021 level of the USA.

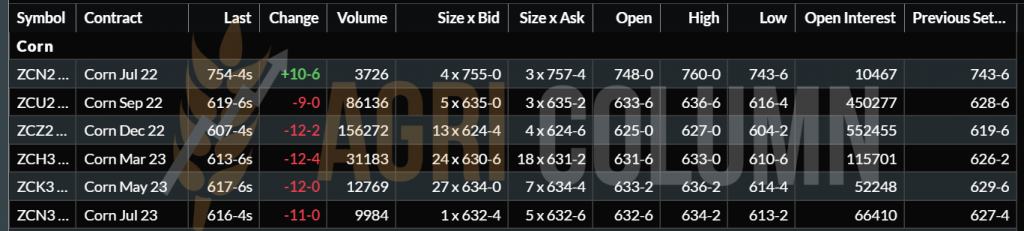

CBOT ZCZ22 DEC22 607c/bu, minus 12c/bu. The effect of the liquidation of positions by investment funds is also manifested in maize. Will we see it at 550c-570c/bu? All current indications lead to this level.

TREND GRAPHIC OF CORN – CBOT ZCZ 22 DEC22

CAUSES AND EFFECTS

Corn is in line with the massive decline generated by the two associated factors, the FED and the investment funds leaving after liquidation of positions.

Will we see more growth? Certainly, but not so spectacular. The weather is a factor in lowering the price at the moment, the safety of crops in North and South America generates confidence in the short and medium-term.

The crops of the European Union and Ukraine are equally well looking and the only problems on the horizon are those related to weather and logistics for export from Ukraine.

The negative revision of the Russian export tax will bring a marginal negative decrease, but it should not be neglected because Russia’s intention is to use part of Ukraine’s corn crop in its own interest.

The corn will not return to 340-350 EUR/MT in the CPT Constanța parity. We have a difference of 80-90 euros between these two benchmarks and even if there will be increases, they will not be so strong. Only an armed conflict on a European or global scale can change this status within 2-4 months. But no one wants that for sure.

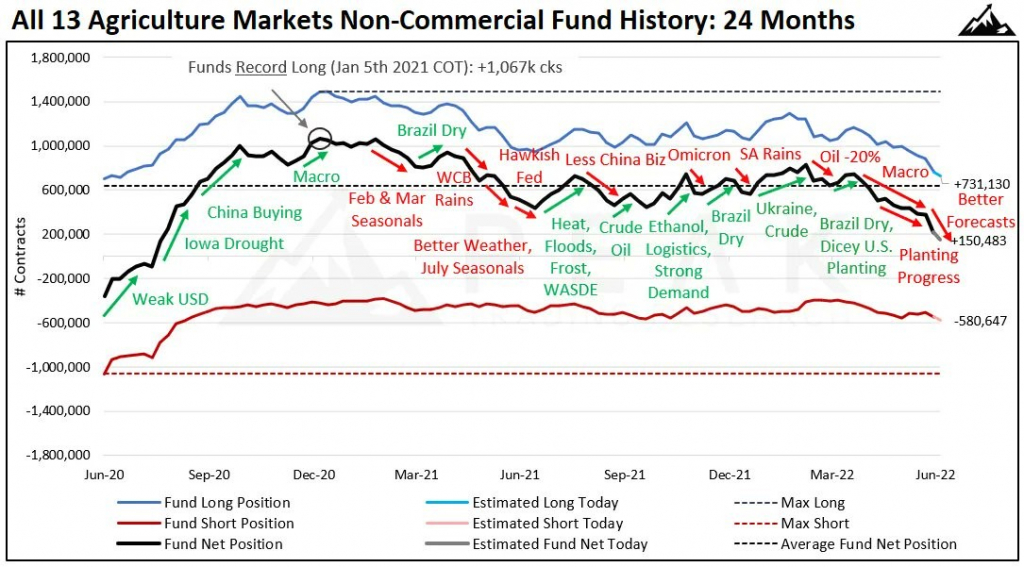

We insert another chart of the funds’ activity, with the main indicators that marked decreases or increases of quotations and implicitly of positions. Credit: Peak Trading Research

CORN INDICATIONS IN MAIN ORIGINS (old crop)

LOCAL STATUS

Things are going according to the script written in the last two reports. Namely, the harvest pressure is used to generate a much higher elasticity than the indication XRQ22 AUG22 in terms of negative discount. We have many indications for processors as well as exporters. At the positive pole, we have AUG22 minus 10 EUR/MT for the goods delivered in the CPT Constanța parity, while at the opposite pole, we have an indication from the processors of AUG22 minus 50 EUR/MT in the delivery parity DAP processor warehouse.

In other words, farmers have to test the market very well before selling the goods spot. Because these days rapeseed is fully harvested in Romania and we can no longer talk about forward contracts.

The days when quotes were at impressive levels are gone and many farmers regret the lack of decision, the lack of information, and why not say, the lack of courage to benefit from tradable insurance called Hedging which does nothing but secures a price at all times The farmer believes that it is optimal, eliminating the market risk factor and the default by not delivering the goods. Farmers only need to write to [email protected] to access this way of securing through trading insurance.

CAUSES AND EFFECTS

The main factor is of the abundance of the crop and the idea clearly outlined by the buyers that the goods exist and the farmers will retain the goods. Thus, against the background of the farmers’ hope to see much higher quotations compared to today, the processors and exporters will see themselves quietly processing and trading with the other products because the goods exist and are not traded.

It is the discouraging effect of the price degradation and the subsequent action of the farmers in making the withholding without having specialized information but only hope for a future price increase. The volatility of rapeseed is obvious. The steep descents seen for four days were not offset by a single day’s ascent.

REGIONAL + GLOBAL STATUS

THE EUROPEAN UNION once again falls below 18 million tons of the crop forecast. The enthusiasm generated by raising the forecast to 18.40 million tons has evaporated due to the heat and today the indication is at the level of 17.9 million tons.

CANADA indicates the same positive forecasts with some small problems but cumulatively remains at the same level of over 20 million tons.

AUSTRALIA remains the same in scenario so far and no short-term problems are forecast in the 5.8-million tons forecast.

As a global cumulation, rapeseed volume forecasts remain positive even with the EU correction applied. This positive volume trend will only maintain the current price level of rapeseed if it does not degrade it further by combining the factor of attempts to stop inflation globally.

EURONEXT XRQ22 AUG22 – 669.25 EUR (minus 24.75 EUR)

RAPESEED TREND GRAPHIC – EURONEXT XRQ22 AUG22

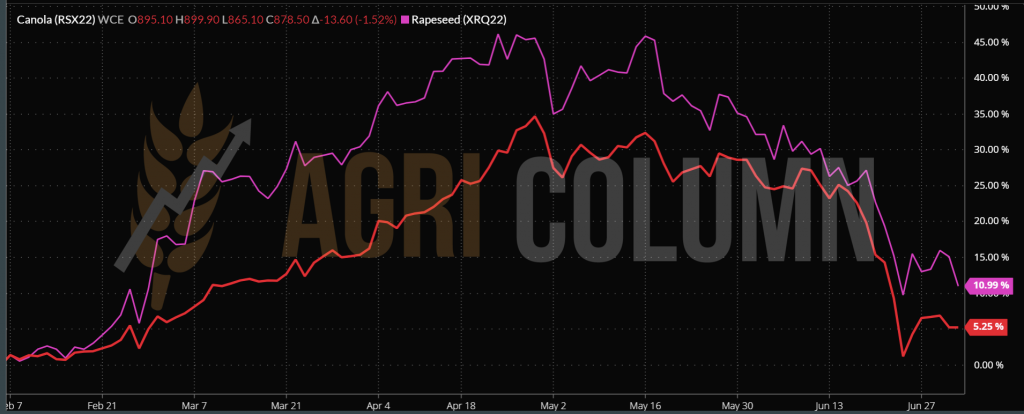

ICE CANOLA (closed on 1 July 2022 – National Day of Canada).

RSX22 NOV22 – 878.50 CAD (minus 13.60 CAD)

TREND GRAPHIC – ICE CANOLA RSX22 NOV22

COMPARISON EURONEXT VS ICE CANOLA

Indonesia is trying with new measures to stimulate the export of palm oil and thus the supply is richer in the complex, the latter decreases in price affecting on the principle of communicating vessels and colleagues of the VEGOIL complex, soybean oil, sunflower oil and by correlation and rapeseed oil.

Petrol also decreases, driving rapeseed oil on the same slope due to the double role of it: that of food and industrial use in Biodiesel.

Investments in processing units for biodiesel production are put on hold and some facilities are actually sold (Cargill in the UK).

LOCAL STATUS

The indications of sunflower seeds have seen a small positive boost. Romanian farmers manifest by the refusal to sell. It’s only logical. If we look at the difference between two weeks ago and today, we see a steep drop from 690 USD/MT to 560 USD/MT.

In fact, the indications of processors and exporters are at this level today. But as we mentioned in the last issue, 575-580 USD/MT is the correct and current price of the new crop.

In the case of sunflower seeds with high oleic acid content, the bonus indicates the positive premium of 35-40 USD/MT for oleic acid content of at least 82%. And here we have an opinion that this level must be much higher. The pandemic has passed and the demand for HoReCa in the European Union has increased substantially, which implicitly means the demand for HOSO (High Oleic Sunflower Oil).

This clearly indicates a need to fill in and therefore the bonus should reflect the growing demand. But buyers rely on harvest pressure at this time and do not rate the bonus at a higher level. Our vision for the bonus level is currently at a minimum of 55-60 USD/MT, except to eliminate another growth potential granted with the demand and implicitly with the price of linoleic sunflower seeds.

CSFO AND OILSEEDS INDICATIONS IN MAIN ORIGINS (old crop)

GLOBAL STATUS

The US report from NASS indicates a higher level of stocks compared to the same period last year. But in terms of sowing, we have a negative report compared to the intentions of 1 March 2022. At the mentioned date, they had an intention to sow 90,955 million acres, i.e., 36,824 million hectares. The report indicates the sowing of 88,325 million acres, i.e., 35.76 million hectares, a minus of 1.06 million hectares. What is translated into production per hectare will generate a lower crop level of at least 3.2 million tons of soybeans. This leads the US soybean crop from a forecast level of 126 million tons to one of 123 million tons in the 2022 season.

BRAZIL presents no change in status. The forecast us still149 million tons.

ARGENTINA remains at 55 million tons.

PARAGUAY remains unchanged at the quota of 10 million tons.

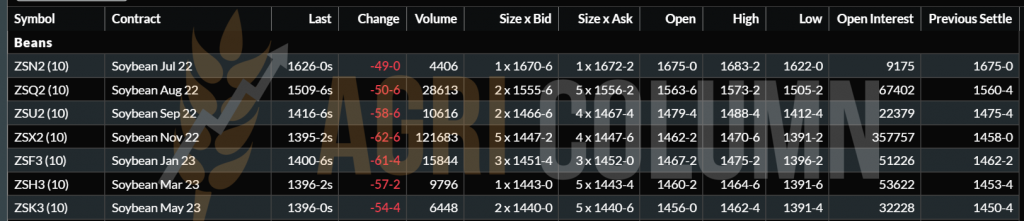

CBOT SOYBEAN ZSX22 NOV22 – 1,395 c/bu (minus 62 c/bu)

SOYBEAN TREND GRAPHIC – CBOT ZSX22 NOV22

CAUSES AND EFFECTS

Soybeans are receiving the strongest shock through the massive outflow of funds from the CBOT. A decrease of 62 c/bu (22.78 USD) is very high for a trading session.

Looking at the indication MAR23, we notice an equivalence with NOV23 which means a distrust in the future route of soybeans. Volumes in South America are extremely generous in forecasting that there is no potential for price increases.

But this is about the artificiality created by the oligopoly and the fear of the future recession generated by the FED in attempts to curb inflation. Mr. Jerome Powell, the president of the Federal Reserve, said he wanted a smooth landing and so far all signs indicate this.

In conclusion, soy is not an element of future surprises in terms of short-term price increases. The weather will be the referee in this whole complex.

But we will see further price declines in the future due to the actions the FED will take, and the other categories of agricultural commodities will not be forgiven.

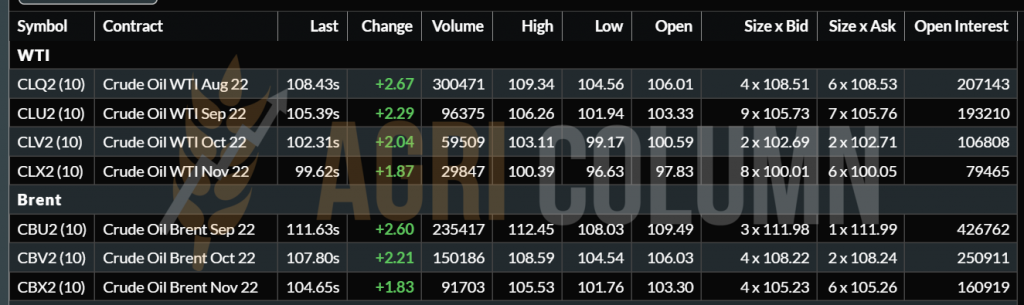

BRENT 111.63 USD/barrel | WTI 108.43 USD/barrel

2-9 July 2022

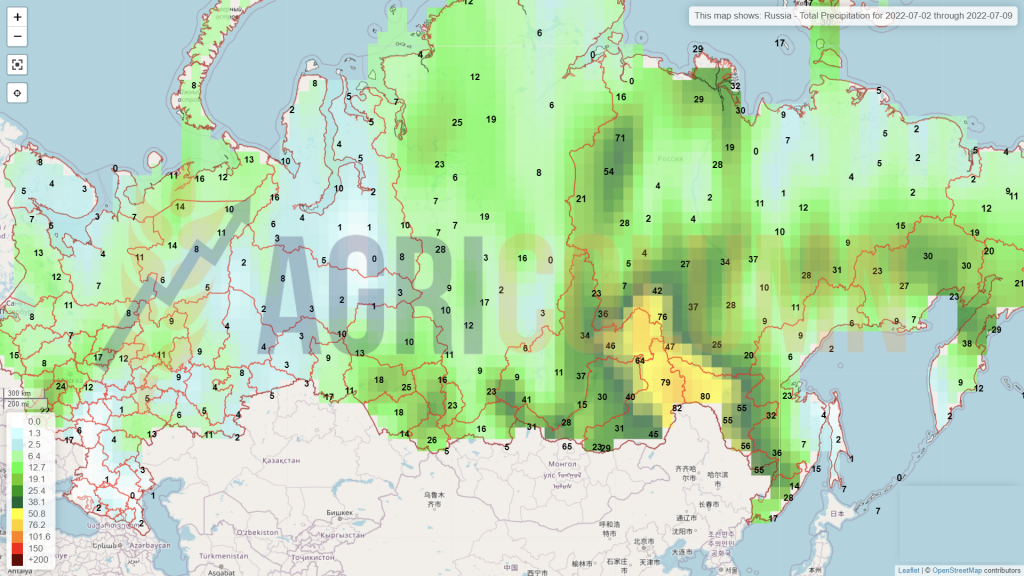

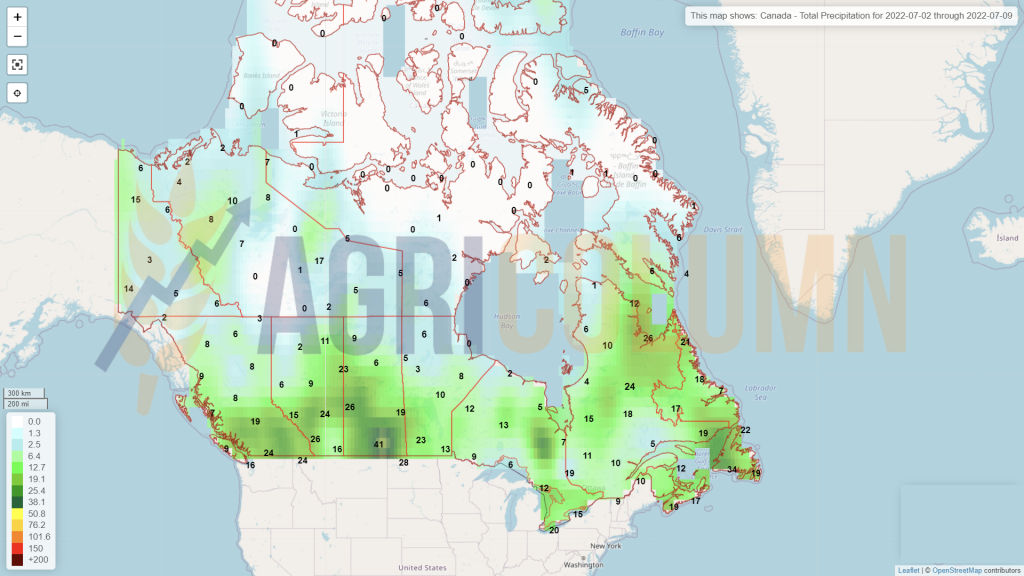

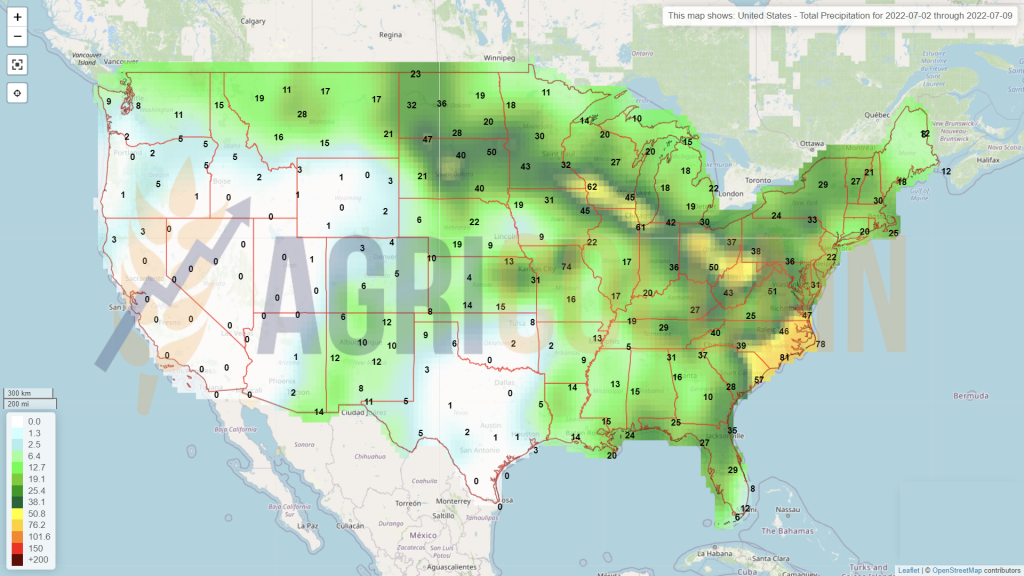

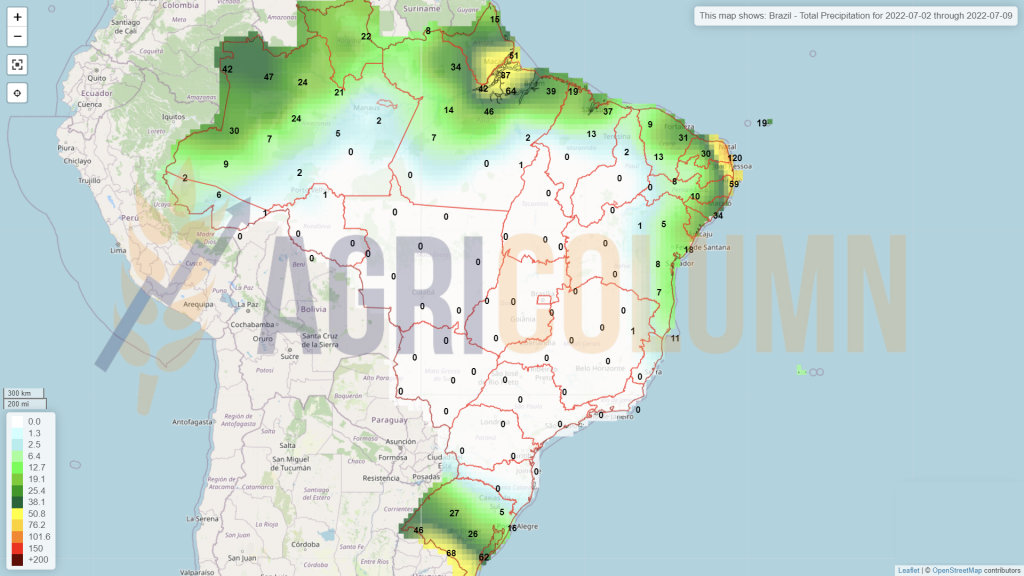

Romania

Europe

Ukraine

Russia

Canada

USA

Brazil

Argentina

China

Australia