This week’s market report provides information on:

LOCAL STATUS

The indications of the port of Constanța range between 370-375 EUR/MT, with a substantial discount of 20 EUR for the feed quality. We have been mentioning the decline in wheat for a long time and we hope that many farmers have fully understood our message. There are fundamental factors in the market that govern supply and demand, and they have been indicating this decrease for about 3 weeks.

Romania will harvest a volume of 9 million tons. This is a certainty. Of course, we have areas with very big problems, we know which they are and we will not evoke them again, but the other areas will balance the harvest volume at national level.

For the 2021-2022 season, things are almost over. According to the data we have, by the beginning of June, Romania had shipped to the export market a volume of over 6 million tons of wheat. However, the intra-Community volume is missing from this figure. With this volume, we believe that Romania easily exceeds the level of 7 million tons, gathering here also June 2022 in its entirety.

CAUSES AND EFFECTS

For the very big difference between the milling wheat and the feed wheat, we can already draw a parallel between the first batches of barley harvested and the wheat that will follow. We may have a large share of feed wheat.

The Test Weight is the one penalized by the lack of water, a lack that affected the wheat exactly during the period when it was growing. Thus, the effect of barley could be found in wheat. It is a first signal that puts us in a position to wait for what is to come. The price difference set today as an indication clearly draws the line of expectations in the next period.

The rains that are coming these days could also delay the harvest of wheat and favor the emergence of certain diseases, but hopefully this will not happen. But an overlap with the rapeseed crop may be encountered and from here also the operational problems at the reception of goods in silos and bases.

REGIONAL STATUS

THE EUROPEAN UNION reduces the forecast for soft wheat from 126.4 million tons to 124.4 million tons. So we have a negative difference of 2 million tons in production. France will generate only 33.5 million tons of soft wheat, a figure that is close to our forecast, being, practically, the decrease that affects the European Union.

UKRAINE remains at the same level of production estimated for the current season, i.e., 19.5-20.5 million tons, with a minimum export potential of 10 million tons.

RUSSIA continues to target high numbers of 87-88 million tons of production, according to local analysts. Identically, in terms of export figures, they forecast levels of 42 million tons for the 2022-2023 season.

BULGARIA indicates a crop level of 5.5-5.8 million tons of wheat. However, local analysis factors support 6 million tons.

CAUSES AND EFFECTS

THE EUROPEAN UNION, despite the decrease in production, is balancing from the unexecuted export of 2 million tons in the 2021-2022 season. For the most part, it is French wheat which, as we recall, did not have a very high percentage of milling quality, and thus the share of feed wheat was much higher. So a zero sum game at European level. What is not realized in terms of volumes is offset by why it was not exported.

RUSSIA, however, is viewed differently by the USDA. The report, which you will find separately, sees Russia at a production level of only 81 million tons, 7 million tons lower than local analysts. Is the difference only from the analysis of the figures and then the USDA admits? Or does the difference come from the fact that Russia takes over Ukrainian goods from the occupation zones? As reported by Russian Defense Minister Sergei Soigu, 10 million tons of Ukrainian goods will be shipped through already occupied ports. It is primitive and intolerable to steal the food of another people and use this food as a weapon of blackmail against the hopeless populations of Africa.

The image we are recording today is of an attacked country, from which everyone wants to bite a piece. Russia’s negotiations with Turkey without Ukraine have provided at least a hilarious picture. How to negotiate for someone in a desperate state without him being present? President Erdogan is thus creating an asymmetrical atmosphere of negotiation, from positions of strength, without the other party being involved. Expectations could not be confirmed. Nothing was concluded.

Everyone appreciates Turkey and respects its geo-strategic position, with its two gates to the world, the Bosphorus and the Dardanelles. Everyone appreciates the hardworking Turkish people and their big heart, full of good feelings, but the approach in this case was not a balanced one.

Turkey is a factor of stability and predictability in the Black Sea area and must play this role of power with a lot of balance. And in this very worthy of the Middle Ages complex, Syria has so far received 100,000 tons of stolen wheat.

The balance we see today in the wheat market will not last long. Harvesting will begin in the European Union and the latter must find operational tools to channel wheat exports from Ukraine in a coordinated and disciplined manner so that it can meet demand from Africa and the Orient.

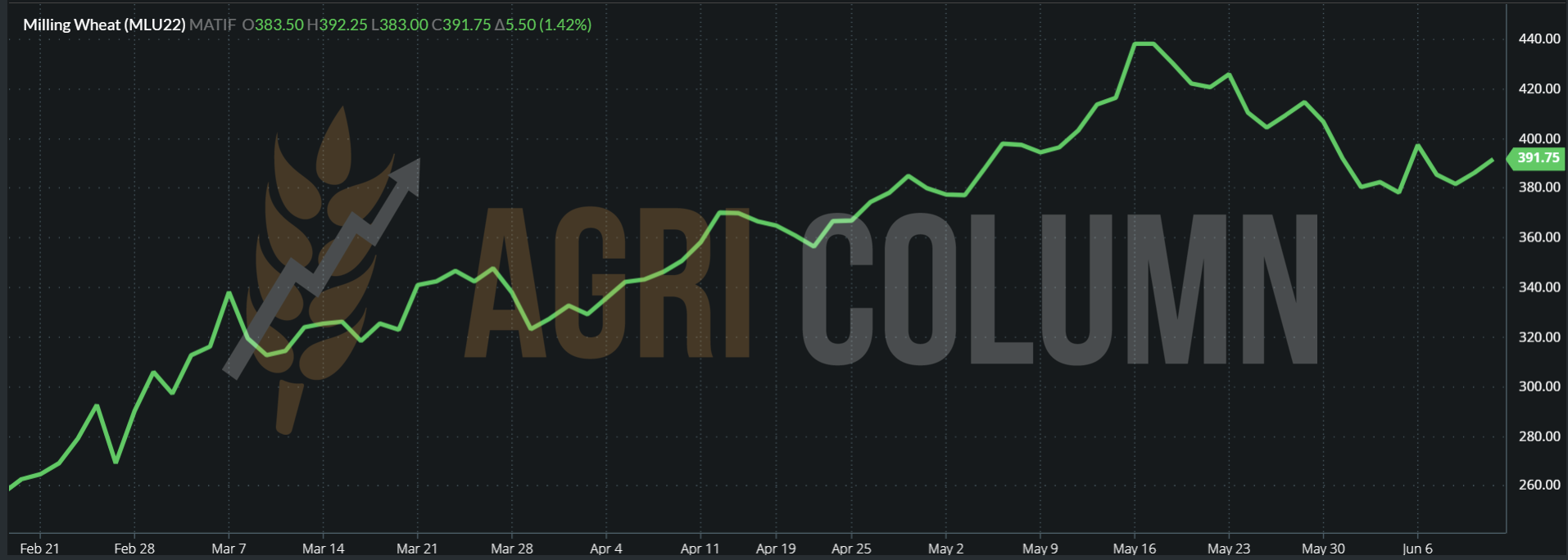

EURONEXT closes with an increase of 5 EUR after the release of the WASDE report. Otherwise, the harvest pressure and the stabilization provided by the failure of talks between Russia and Turkey, where Ukraine was not invited, have generated a calming of trends.

EURONEXT WHEAT – MLU22 SEP22 – 391.75 EUR (+5.5 EUR) at the close of June 10, 2022

WHEAT TREND GRAPHIC – EURONEXT MLU22 SEP22

GLOBAL STATUS

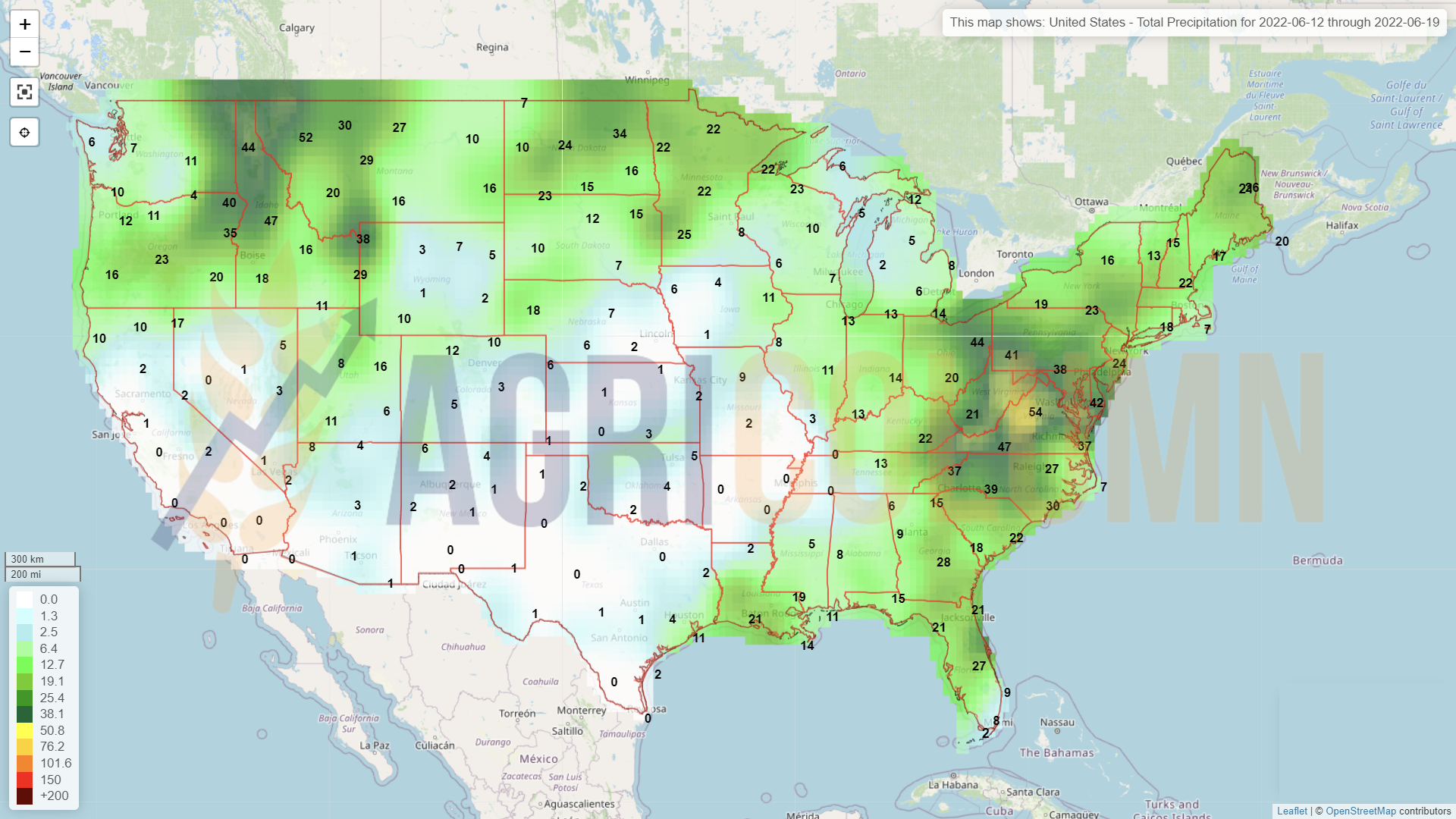

The United States did not want to indicate a deterioration in the wheat crop. They claim that they will have the same level as the one indicated in the WASDE report of May 12. But we all know that things are not real. We’ll see about that later in the August WASDE report. Everything is so predictable. The USDA has ignored the abandonment of winter wheat crops in Texas and Kansas, knowingly ignoring the spring wheat regime again, all because of the global social balance it wants to maintain.

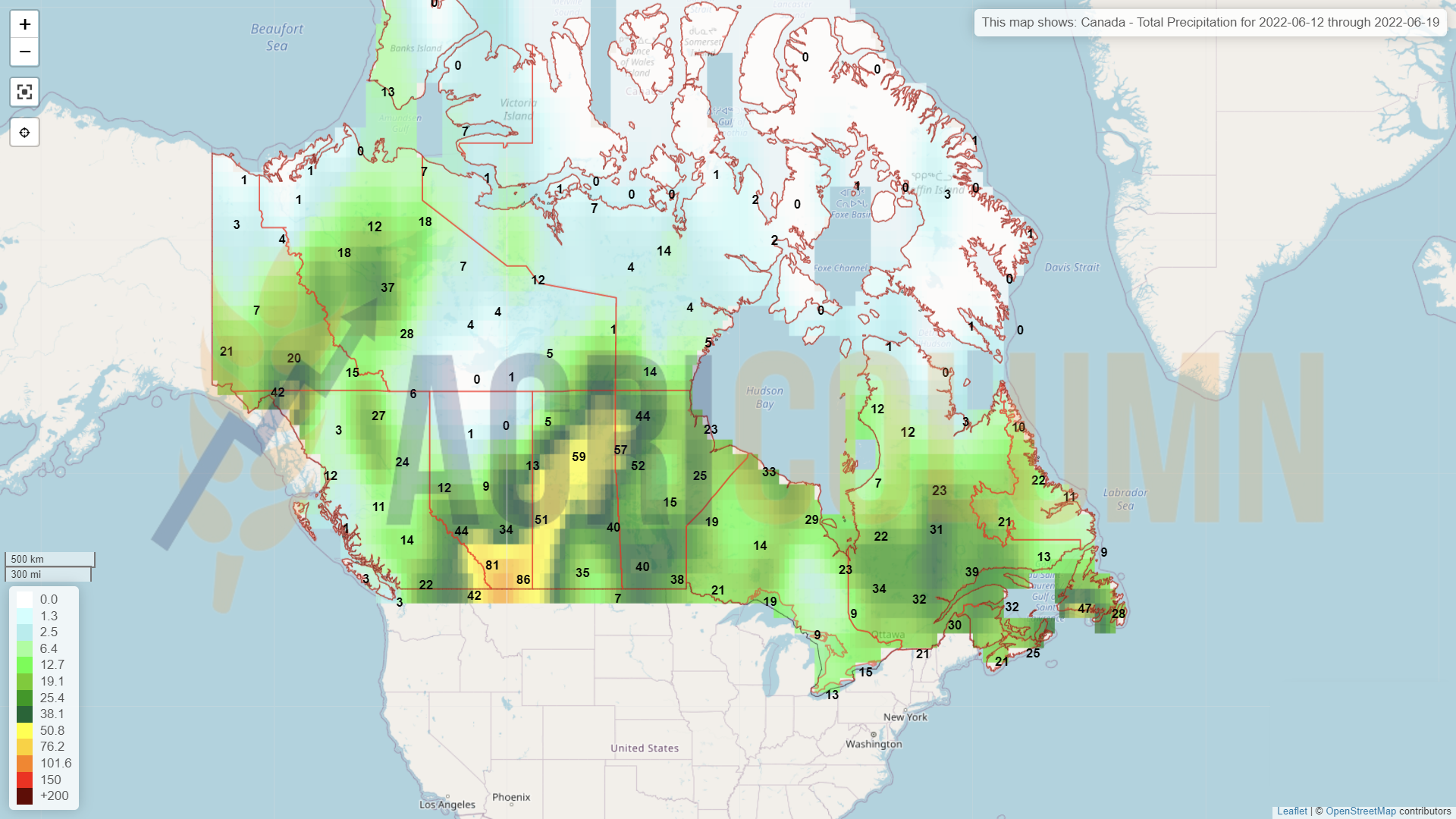

CANADA remains in the same predicted good harvest status as in the previous report, so we have no changes.

ARGENTINA, Rosario Grain Exchange via Reuters. After the increase announced some time ago, Argentina drops the forecast to only 18.5 million tons, compared to 19.5 million tons. “This harvest cycle begins with the worst soil moisture conditions,” the stock exchange said in its monthly report, adding that about 80% of the key Pampas region is in dry to very dry conditions. Farmers planted 17% of the estimated area for wheat, about 13 percentage points after the same stage last season, according to the stock exchange. Rainfall will be key to helping full planting by early July, but the weather is not encouraging.

INDIA. Local sources suggest that the value of 99 million tons indicated as harvest level is no longer current, but in fact the new figure is much lower. The figures (some exaggerated, we assume) outline the value of 95-97 million tons.

PAKISTAN raises the required level of imports from 2 to 3 million tons of wheat as long as the stifling heat persists.

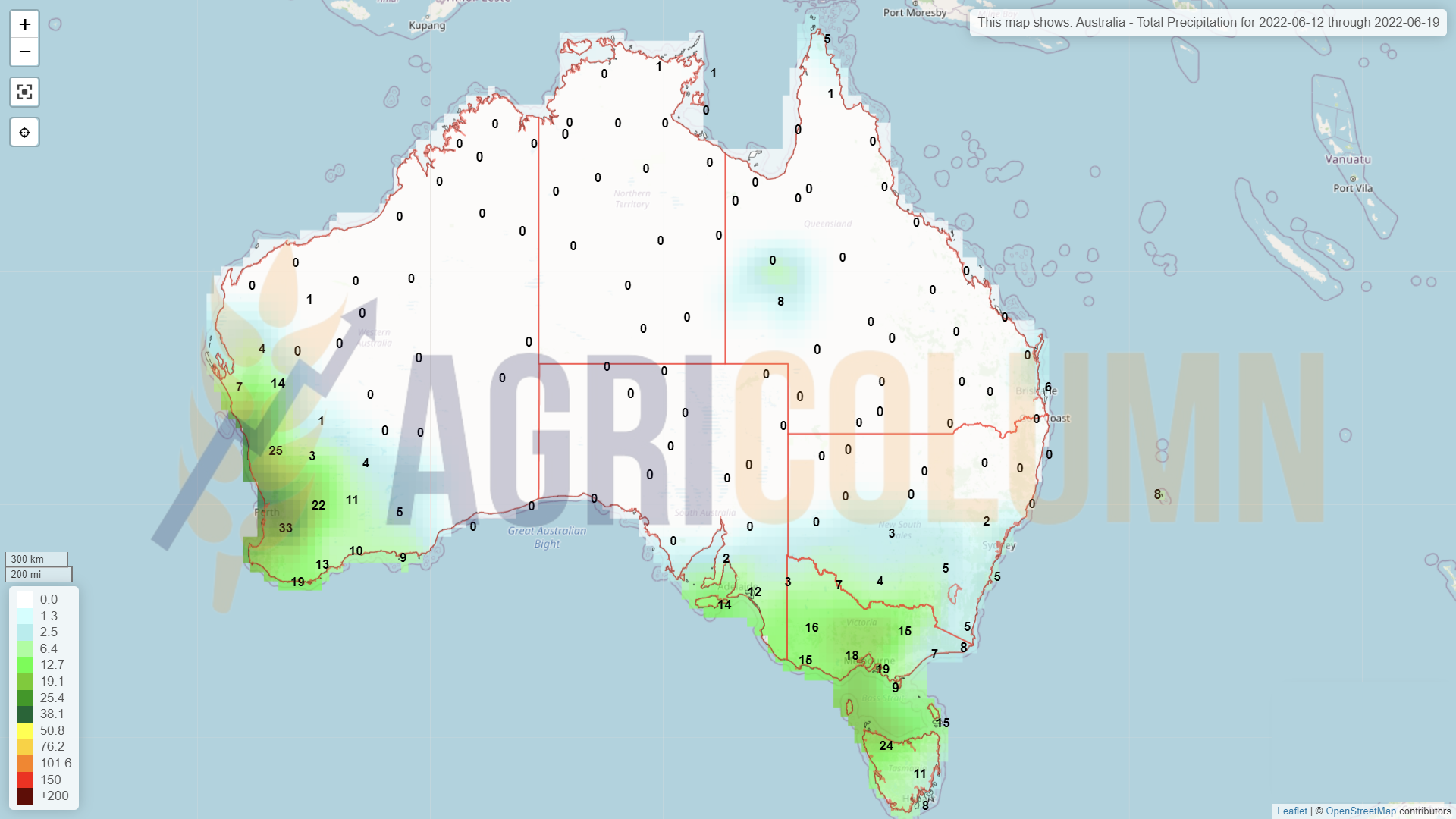

AUSTRALIA will generate a very good crop this year, of at least 32.5 million tons. It only partially rebalances the global deficit, but counts in the overall supply and demand plan. 2 million tons are not to be neglected.

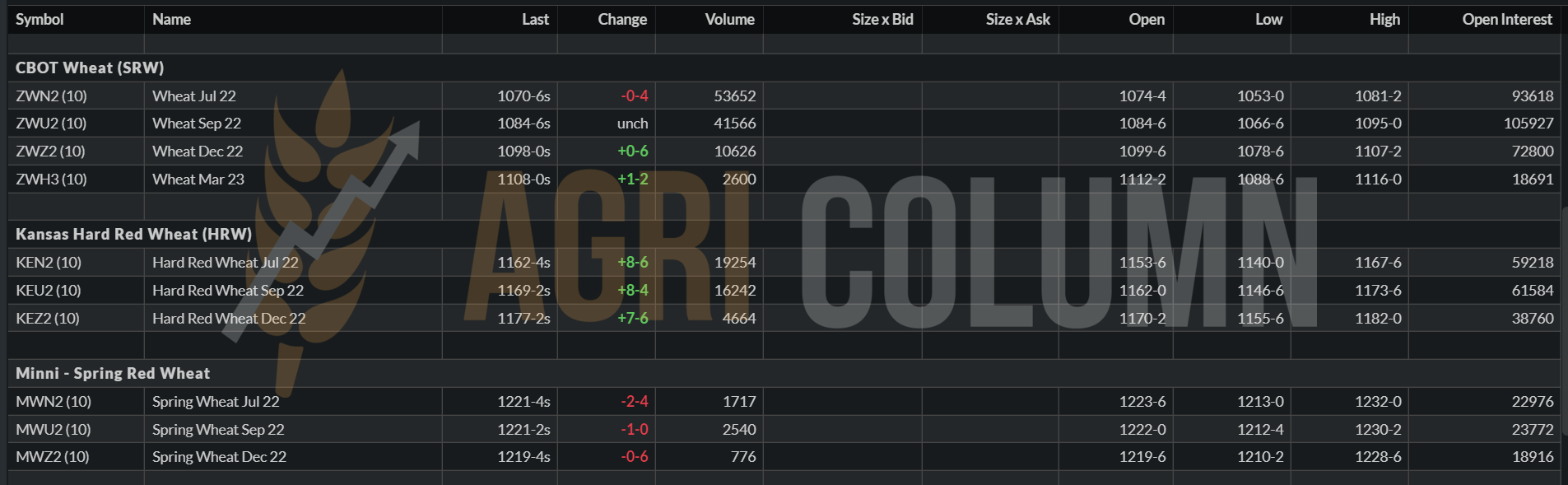

CBOT does not respond positively to the USDA report. It remains static due to the balance generated. CBOT balanced, Kansas rising due to dropout rate, and Minneapolis declining.

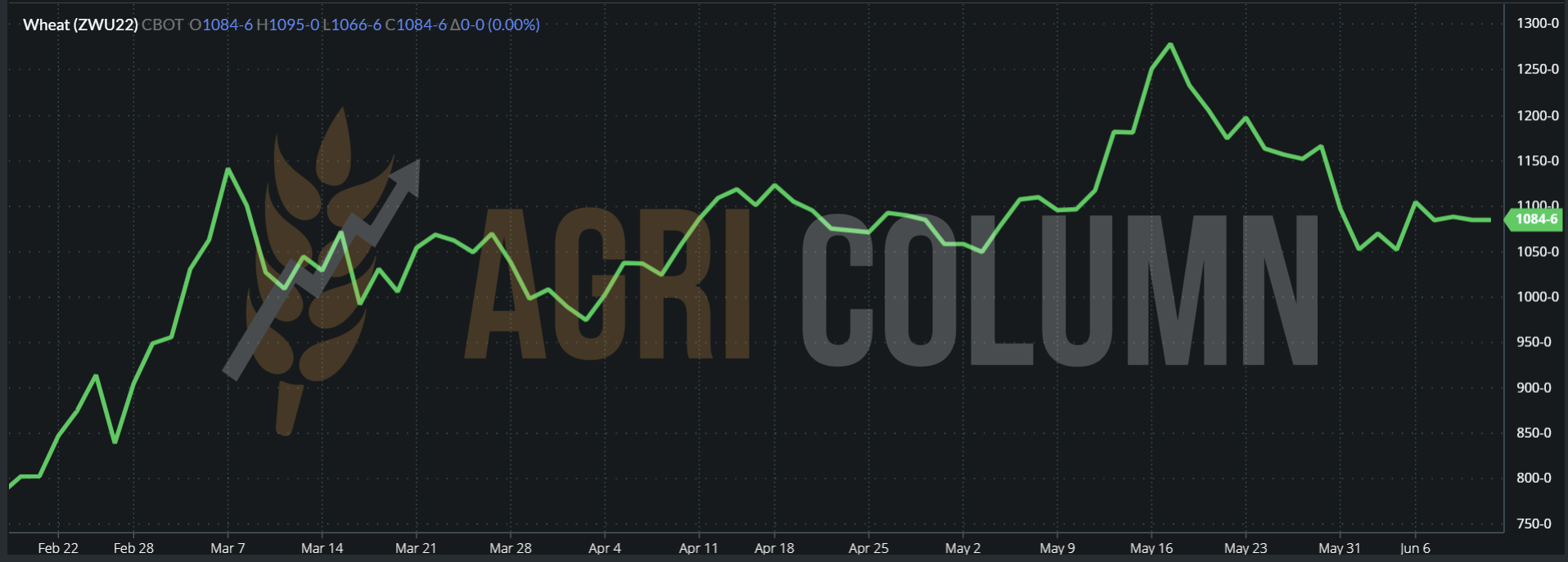

CBOT ZWU22 SEP22 1,084 c/bu = 398.3 USD

WHEAT TREND GRAPHIC – CBOT ZWU22 SEP22

CAUSES AND EFFECTS | ANALYSIS

What’s most important is not over yet. Whoever believes in the stabilization and predictability of an identical route as in previous years should be more cautious.

We are well past June 8, the date of the apparent negotiation of an export corridor for Ukrainian goods. We are well past June 10, the date of the release of the WASDE report, which kept the global volume and stock forecasts in balance.

However, June 14-15 is when the FED will announce the change in interest rates. This is a major point of reference. If we do not record price declines due to the much higher financial cost to be borne by investment funds and, implicitly, their exit from the long positions on the stock exchanges, we can say that we will have another route.

What is certain, however, is that the global wheat balance is negative, but it will be balanced by lower consumption. Wheat will no longer be used for industrial purposes, and the goods that are blocked (they exist) will eventually find their way.

There are already massive discounts on Ukrainian goods for the new crop in the Western Frontier DAP parity, this already affecting the price levels for Polish and Romanian farmers alike.

But let’s not forget where we started, from February 23, 2022, when wheat had an indication of 260-265 EUR in Euronext. And today, we are at 392 EUR in the same direction. We are talking about a difference of 130 EUR, for which Putin is indeed to blame, speaking in the context of feeding the planet. From 180 EUR to 265 EUR, the hedge funds, which have effectively crushed the commodity market in order to generate positive margins for the money printed with the ruthless during the pandemic, are to blame. We have a 50% -50% amount of guilt, with the mention that the military invasion of the Russian army also means loss of human lives. And life is priceless.

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

LOCAL STATUS

The indications of feed barley in the CPT Constanța parity are maintained around 340 EUR/MT. The declining effect of wheat, as well as the difference between milling and feed wheat, also attracted the price of barley to this level.

The problems at the beginning are obvious and we do not have a positive image of the tonnage and quality of feed barley. The first areas harvested in southern Romania show a low production per hectare, between 3.5 and 5 tons and a very low Test Weight, between 52-57 kg/hl (TW).

These are not good conditions, but farmers are confident that the situation may change as the harvest progresses, especially as it begins from the south to the north.

REGIONAL STATUS

The production of the European Union is starting to decrease, so it is not just a problem of Romania. Forecasts currently indicate a lower level of 1.4 million tons, starting at 51.7 million tons and falling to 50.3 million tons.

LOCAL STATUS

The indications of the local market range between 305-307 EUR/MT in the CPT Constanța parity. The level remains constant and is naturally in line with the status of the Romanian crop in full vegetation stage.

The old crop corn ranges between 315-320 EUR/MT and interest remains constant. To date, Romania has exported over 4 million tons of maize, without taking into account intra-Community trade. There is still shipping time left and we believe that a minimum of 6 million tons can be reached.

CAUSES AND EFFECTS

The precipitations that have fallen in the last days bring their beneficial contribution on the Romanian crop. At the same time, they relax the buyers, who no longer see on the horizon the specter of a drought that can call into question the availability of goods.

In the short term, in agreement, of course, with the stock markets, this could be a negative signal for the price of corn. Any disturbance in the landscape, whether due to the weather or due to the discount on Ukrainian goods, will affect the local price in either a positive or negative sense.

REGIONAL STATUS

The European Union increases its crop forecast by 0.1 million tons, from 66.7 million to 66.8 million tons. It is not a significant increase, but it is important for the future trend of the European corn crop.

UKRAINE is high in the crop forecast to the level of 25 million tons, starting from a maximum of 20-22 million tons. The effect can come from two directions. One is the one in which the Ukrainian farmers managed to sow a much larger area than the initial forecast. And the second is related to the remaining 2021-22 crop difference that was not exported. In any case, an additional 4-5 million tons are welcome in the European supply chain, knowing that the European Union is counting on imports from Ukraine, especially Spain, which is having huge problems this year due to the drought.

RUSSIA is up by 1 million tons in harvest volume forecast and we note 15.5 million tons. Their export forecast is a maximum of 5 million tons penalized by the level of the floating tax.

CAUSES AND EFFECTS

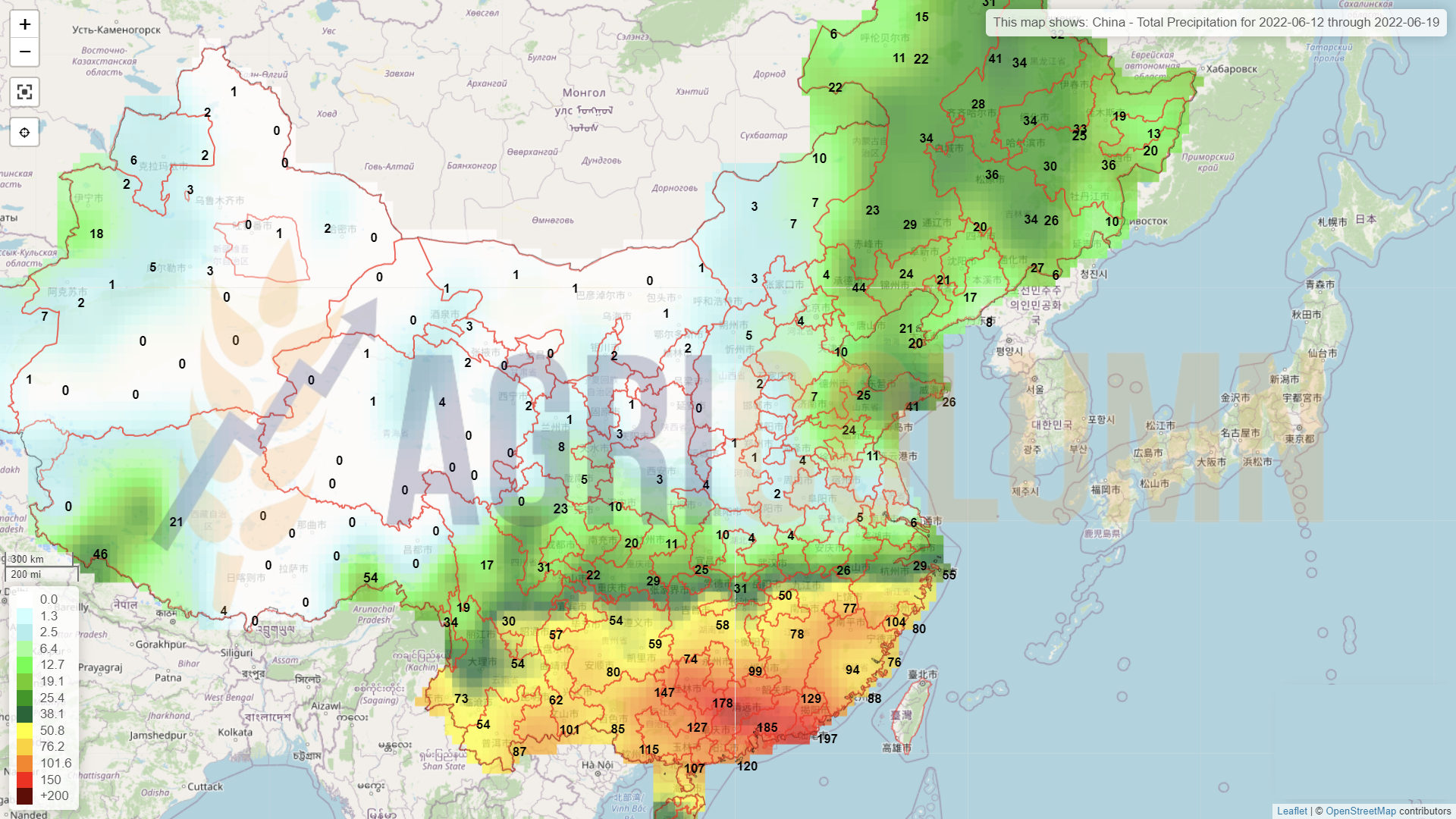

The design and creation of green corridors for Ukrainian goods would be an enhancer of interest for the Black Sea basin area. It would provide the necessary fluency and volume to meet demand from the Union and Asia, especially China. The cost of transportation is much lower for the origin of the Black Sea than the United States.

And to be clear, the Black Sea region is not just about Russia and Ukraine. It means Romania and Bulgaria alike. Russia is not alone in the Black Sea basin and does not own it. Recently, due to its hostility, it has even been declared a state threat to NATO’s eastern border. Anyone with access to the Black Sea is part of the Black Sea basin, regardless of name or territorial size.

If Romania has a very good corn crop, and Ukraine will be able to generate commodity extraction channels, then the aggregate quantities in the two countries will be a volume not negligible for the Asian partners.

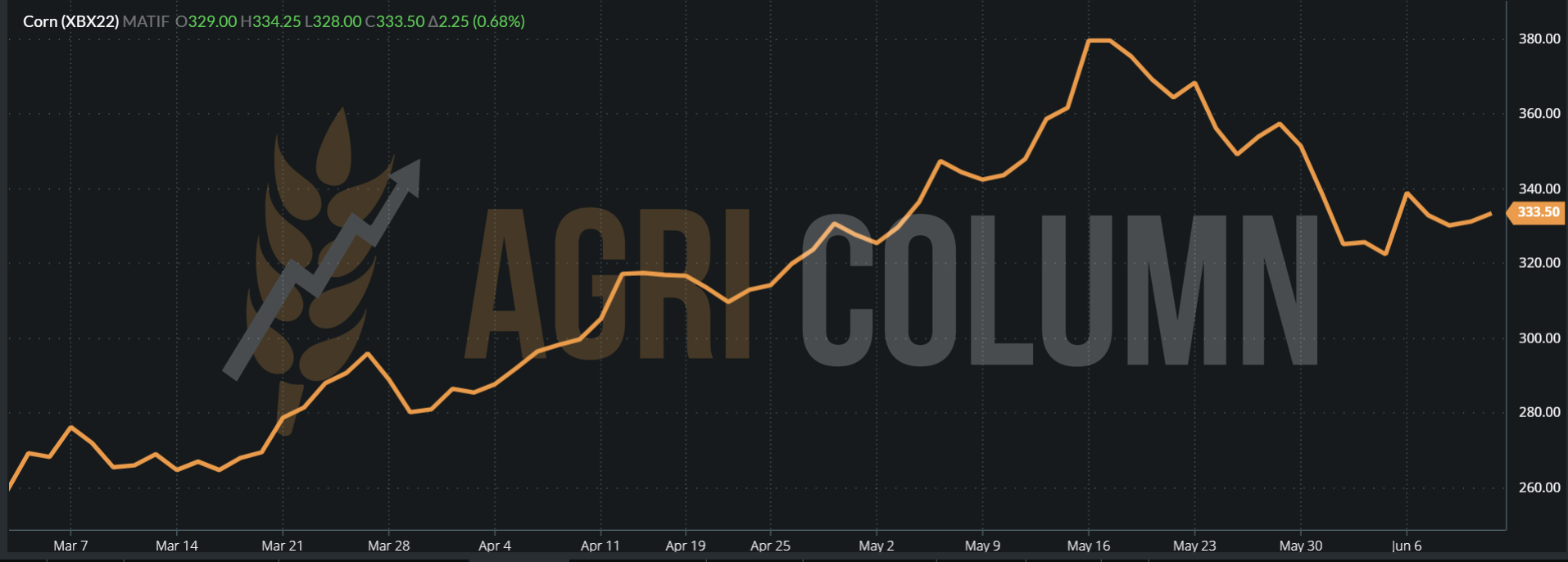

EURONEXT, with much neutrality after WASDE, increases by 2 EUR.

EURONEXT XBX22 NOV22 – 333.5 EUR (+2.25 EUR) at the close of June 10, 2022

EURONEXT TREND GRAPHIC – XBX22 NOV22

GLOBAL STATUS

The United States does not dare to guarantee Barchart’s forecast, namely the decline in productivity per hectare generated by the late sowing of American corn.

The Barchart forecast indicates declining productivity from 177 bu/acre to 174 bu/acre. Translated into the European metric system, it means that instead of 11.1 tons/ha, the US will generate only 10.92 tons/ha. Multiplied by the number of hectares sown in the US, we reach a decrease in total production of 7.6 million tons. Starting from a lower production level compared to 2021, due to the reduction of areas (high costs of fertilizers), 368.3 million tons compared to 386 million tons, today we reach a volume forecast of 360.7 million tons. But, as I said, the USDA does not seem willing to guarantee other forecasts.

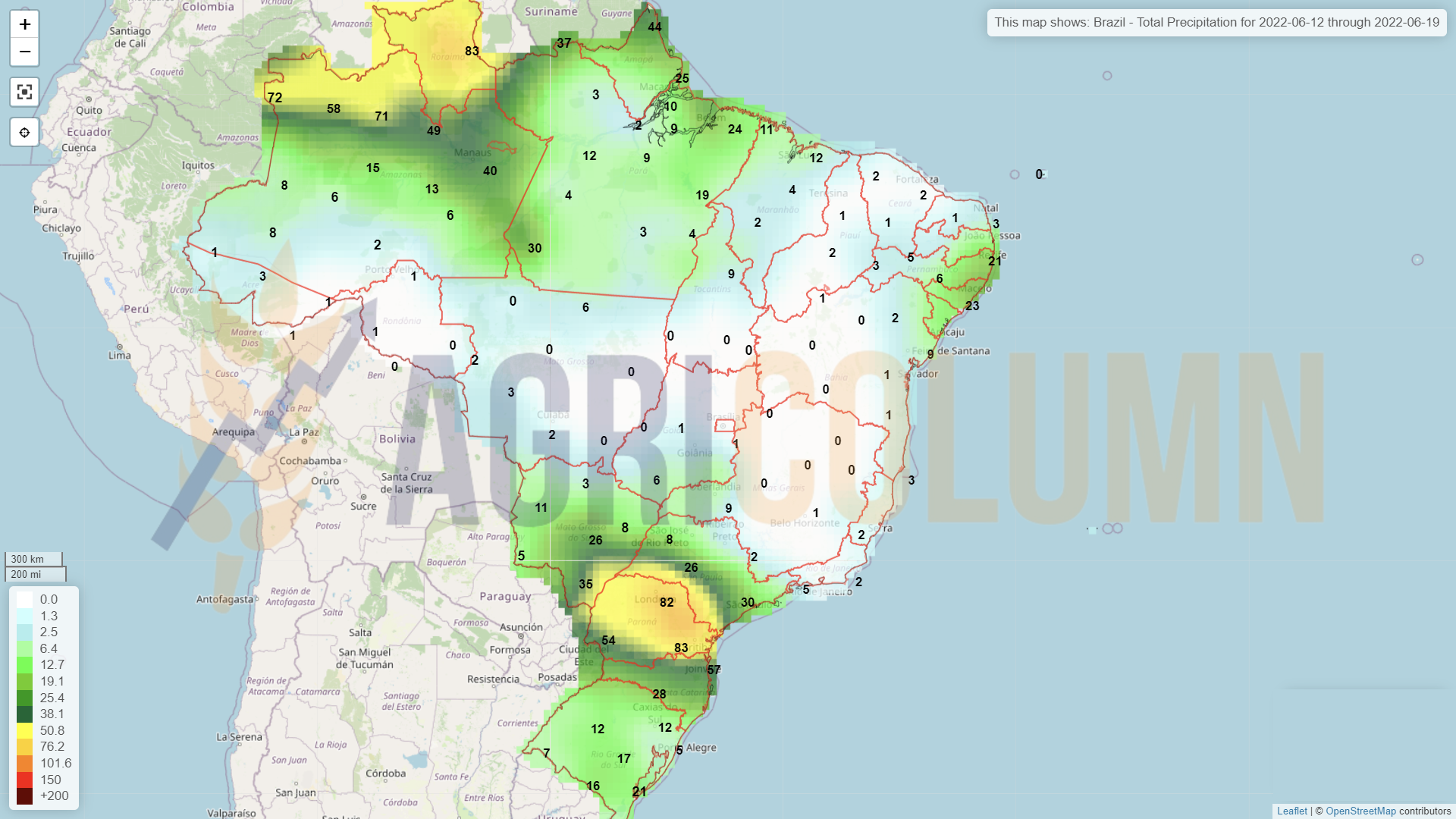

BRAZIL has no changes in Safra + Safrinha this season and remains at 116 million tons. However, the forecast for the next crop is 126 million tons.

ARGENTINA remains unchanged at 53 million tons, with a future harvest volume indication of 55 million tons.

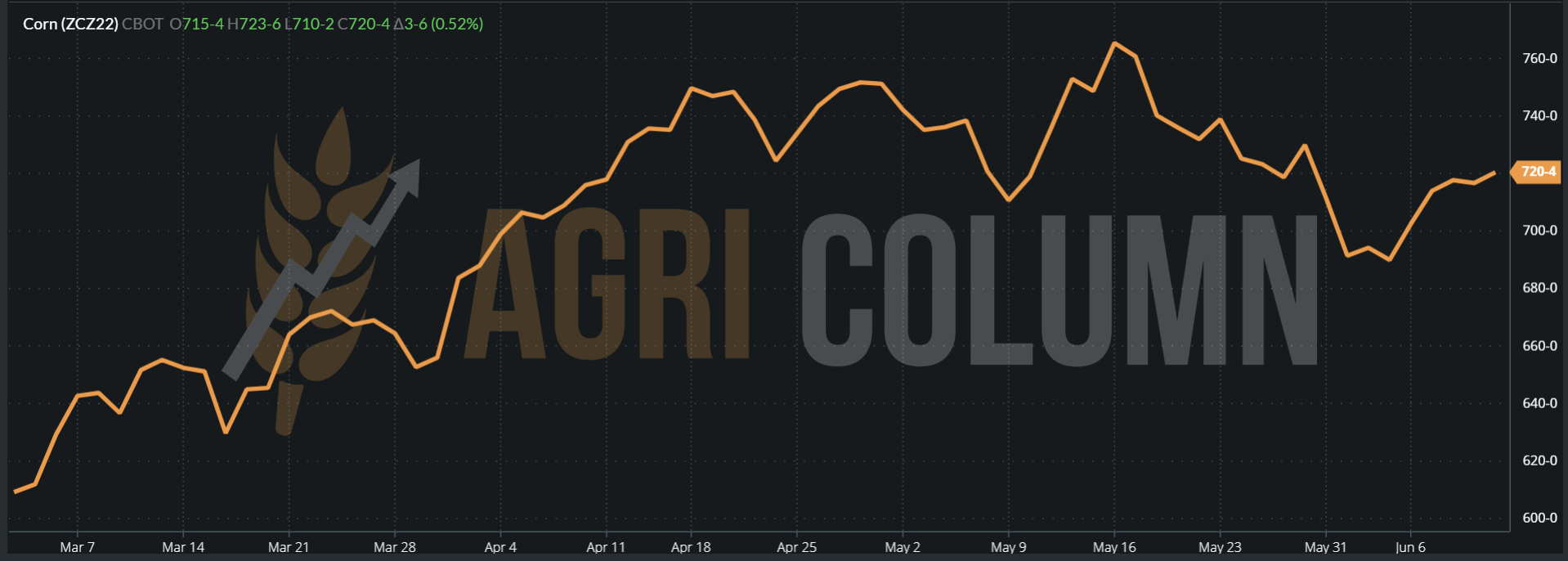

CBOT raises very little, in accordance with the conclusions of the WASDE report, only 3 c/bu. CBOT CORN – ZCZ22 DECE22

CBOT CORN TREND GRAPHIC – ZCZ22 DEC22

CAUSES AND EFFECTS | ANALYSIS

A major risk is posed by hurricanes forming off the coast of the United States. Let’s remember how they devastated Louisiana and how they actually blocked access to American goods for export.

The second factor to consider remains the June 14-15, 2022 and the FED announcement. We don’t insist on it anymore, we just remind you of it.

Otherwise, the overall balance of maize is a stabilized one, and if the right weather is combined with the creation of the Ukrainian corridor, we will see a positive (but not excessive) course in the life cycle of the price of maize. But wheat plays as a referee and can bring corn in the game of maximum volatility.

CORN INDICATIONS IN MAIN ORIGINS

LOCAL STATUS

The indications of rapeseed at local level vary from AUG22 minus 5 EUR/MT in the CPT Constanța parity to a range of AUG22 minus 10-12 EUR/MT for delivery to Processors. It is natural, because the difference is reflected in the transport quotations, given the distance between the farm and the processor and depending on the proximity between the farm and the port of Constanța.

Rapeseed still indicates very good volume forecasts. Some areas have been affected by hail, but we do not identify anything of concern in terms of the areas affected, linked to the forecasted volumes.

CAUSES AND EFFECTS

The incoming and future rains could delay the harvest, subsequently generating a mix at harvest, i.e., the wheat to enter harvest during the period when the rapeseed is also harvested. We will then witness the beginning of blockages at the reception of goods, especially at locations where the reception is carried out for only one product.

REGIONAL STATUS

The EUROPEAN UNION remains within the same volume parameters of 18.4 million tons. Nothing changed here.

UKRAINE remains in the same status, with some sources indicating 2.4 million tons and others 2.6 million tons as harvest volume. However, the discounts applied for goods from this origin are interesting. We see indications at the western border of Ukraine of 750 EUR/MT. However, our sources indicate a much higher level of discount, namely AUG22 minus 80 EUR/MT. With a transport cost of maximum 30 EUR/MT to the cargo processing units, we reach a value of AUG22 minus 50 EUR/MT, which is a very big discount.

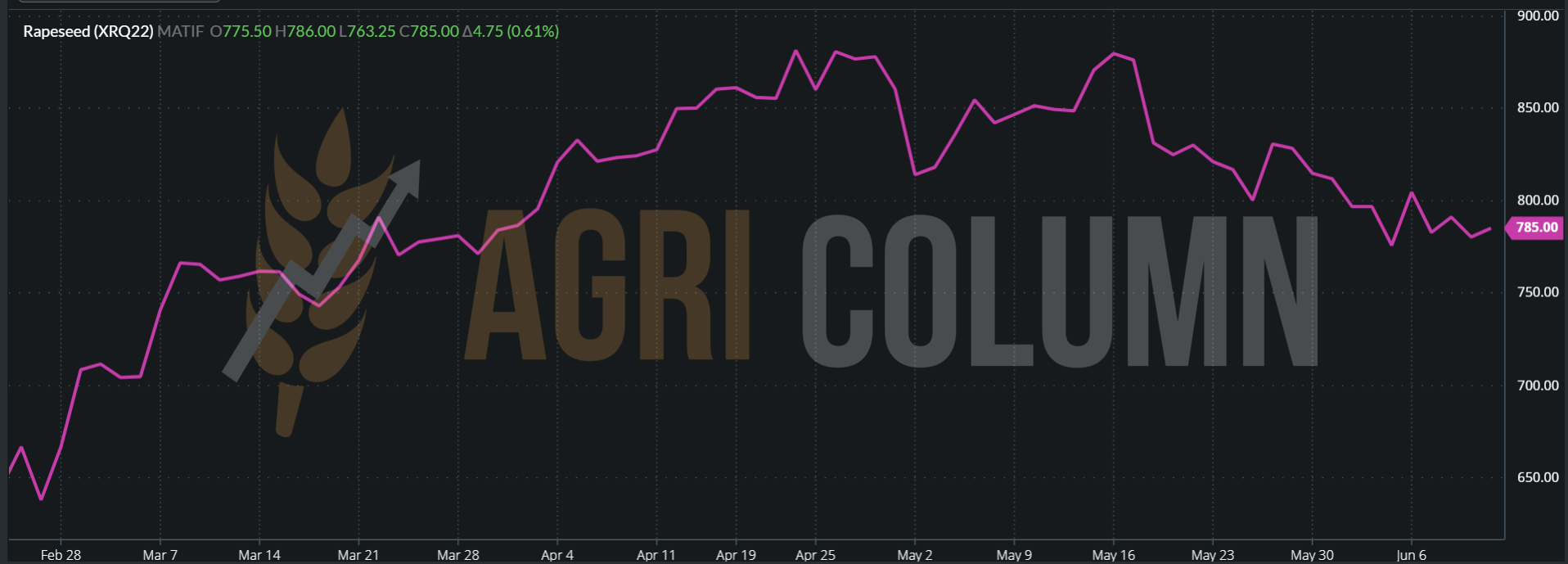

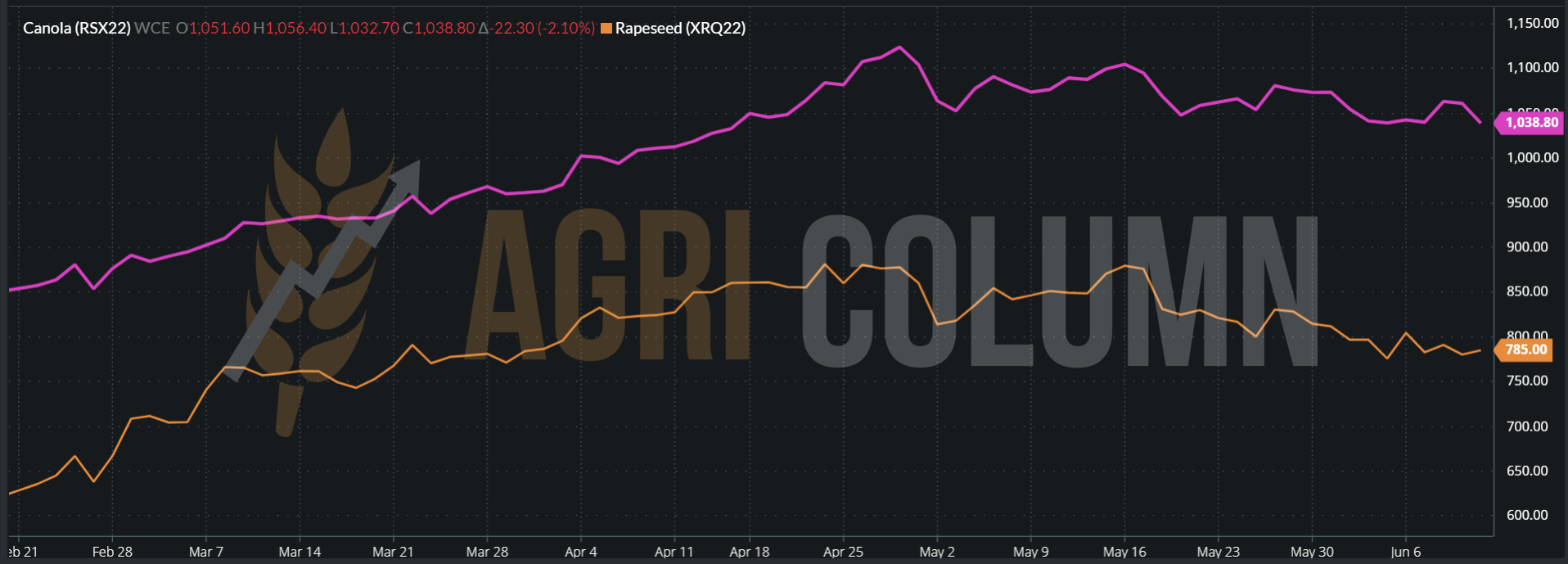

EURONEXT is down, according to our estimates, granted by ICE CANOLA, influenced by time and volume factors.

RAPESEED – EURONEXT XRQ22 AUG22 – 785 EUR

RAPESEED TREND GRAPHIC – EURONEXT – XRQ22 AUG22

CAUSES AND EFFECTS

The influence of the state of Canadian crops, associated with the status of Australian crops, puts pressure on the price of rapeseed. The forecasted volume generates the decrease. The correlation with petrol exists and is the factor that still holds rape at this level.

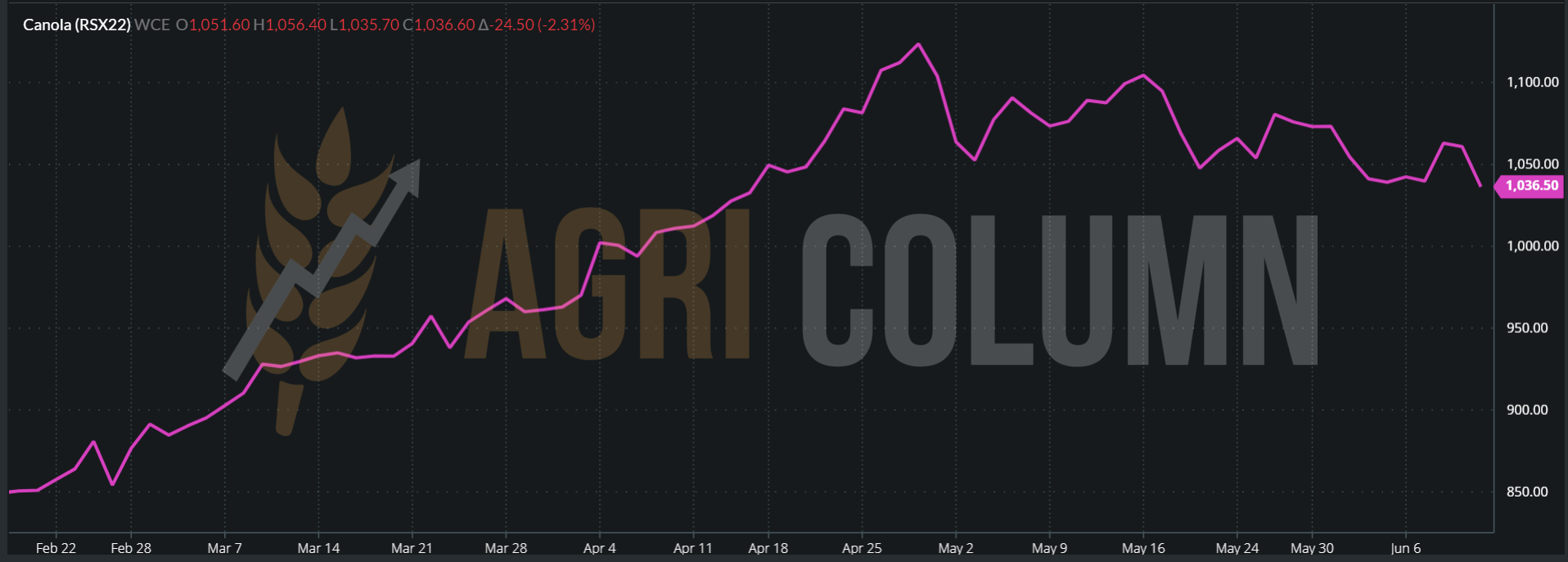

ICE CANOLA loses every indication and influences European rapeseed.

ICE CANOLA RSX22 NOV22 – 1,039 CAD

ICE CANOLA TREND GRAPHIC – RSX22 NOV22

EURONEXT XRQ22 AUG22 (ORANGE) AND CANOLA RSX22 NOV22 (PURPLE) COMPARISON

ANALYSIS

- Rapeseed loses ground and is reconfigured in price around 780 EUR.

- Despite rising oil prices, Canada’s potential reverses the price trend, balancing the volume of last year’s shortage of raw materials, which in turn created a surge.

- For any profit calculation, in the case of a 3 ton/ha crop, rapeseed remains a farm profit pillar, even at EUR 780/MT.

- The months of November-December will bring an increase in the indications of rapeseed globally, more precisely, then the demand will be repositioned for a new period of interest.

LOCAL STATUS

The weather clearly indicates a positive potential for sunflower crop in Romania and thus, subject to past and expected rainfall, prices begin to fall below the level of 700 USD/MT. Practically, the port of Constanta pays a level of 690 USD/MT. Processors go on a range of 680-690 USD/MT. Sales of sunflower seeds are still timid. Volumes are traded, but we do not currently see more than 80,000-95,000 tons of the new crop being traded.

The old crop is still traded at a level set at 700 USD/MT in the CPT Constanța parity, but it faces competition from the Ukrainian goods that cross the Romanian border. The latter are traded at the level of 680 USD/MT.

The volume forecast attached to Romania remains unchanged at 3.6-3.65 million tons.

Romanian sunflower seeds are seeing an increase in the interest of the surrounding countries, waiting for August, and we note companies from Serbia and Bosnia that are trying to access the Romanian market for origination. It is a sign that strengthens once again the premise that Romania is the reservoir of origin and this creates options for Romanian farmers. Options, in turn, create competition and it is a very healthy thing to do in a free market with self-regulating mechanisms.

CAUSES AND EFFECTS

The weather is the driving force behind the price of sunflower seeds. Precipitation and crop development are linked to lower prices. The phenomenon practiced by processors is also repetitive, which during this period and until the moment of harvesting will try to slow down the development of the price of the raw material.

The calculation takes over the logistics as a whole and discounts the goods with the difference between the location of the Processor and the Port of Constanța. Because, of course, the farmer no longer has to cover this distance with his own means or with transport units rented/made available by the Buyer.

REGIONAL + GLOBAL STATUS

We have the same status as last week, with the European Union’s crop forecast at 10.9 million tons, which in turn puts pressure on the price of raw materials.

Ukraine remains unchanged, with a forecast of 9.5-10 million tons, compared to 16.5 million tons in 2021. However, we record here an increase in the price level in terms of trading. Thus, at the western border of Ukraine, the levels rose by 5-10 USD/MT, in some cases reaching 690 USD/MT. Instead, the price level for crude sunflower oil has shrunk. In the same parity, the western border, it is offered at levels between 1,550-1,650 EUR/MT. For accuracy, we also mention that the indication 6PORTS decreases to 1,900 USD/MT for June 2022.

Russia is raising the export tax on crude sunflower oil to 520 USD/MT.

The overall harvest volume is further amended by 6 million tons. The disappearance from the 2022 crop of 7 million tons in Ukraine is offset by 1 million by the European Union.

CAUSES AND EFFECTS

The Russian oil tax, combined with the fact that the Russians will try to control the crude oil market in Ukraine, would mean a support for the price of crude oil, given that they have taken over sales in India as the main beneficiary.

A factor in compensating for the drop in prices could be the price level for crude palm oil, which is causing problems on Malaysian plantations. There, the Indonesian workforce is restricted for bureaucratic reasons and the problems are exacerbated because the farms are not operated.

And finally, the weather could play a key role. The danger has not passed, extremely high temperatures can endanger the sunflower crop.

CSFO AND OILSEEDS INDICATIONS IN MAIN ORIGINS

ANALYSIS

- Sunflower seeds have a level that seems to create the conditions in which demand meets supply.

- Last season’s fireworks went out and what we see today in terms of price is a quiet effect. The volumes are visible, the demand exists. We emphasize normality as an element that will govern the price of sunflower seeds in the next 20-25 days.

- Today’s price level, given a generous volume forecast, naturally leads to another pillar of farm stability in the form of income.

- PS: last year’s rallies will not happen again. The foundations are in place and logistics will create corridors for Ukrainian goods to meet demand from the European Union.

LOCAL STATUS

Nothing changed in the price regime for soybeans. 640 USD EUR/MT is the indication of local processors. Of course, traders who will deliver the goods for export or intra-Community will add to this price, but the sellers are not yet decided on when to contract.

REGIONAL + GLOBAL STATUS

The US is not reacting again and is not reducing the soybean volume level forecast for this season. Barchart generated a lower volume by over 5 million tons, coming from the difference in productivity per hectare, and this is significant, from a level of 3.46 tons/ha to 3.32 tons/ha.

BRAZIL remains unchanged in forecasts, as does ARGENTINA.

CBOT, on the other hand, falls sharply after the WASDE report, with trading algorithms reacting instantly and reducing positions. CBOT ZSX22 NOV22 – 1,568 c/bu, = 576 USD (-14 c/bu = -5,15USD)

CBOT SOYBEAN TREND GRAPHIC – ZSX22 NOV22

CAUSES AND EFFECTS | ANALYSIS

High yields compared to last season are already driving down the price of soybeans on a downward slope. Please compare the indication JUL22 with NOV22 and you will immediately notice the difference.

This engages in the VEGOIL complex. The production of sunflower seeds causes the price of oil to fall in the complex.

Palm oil also generates volumes for the next season and the bureaucratic ways that ban Indonesian workers from entering Malaysian plantations today will be fought in the end.

In other words, the price of soybeans has gone out. By the way, the price fireworks for sunflower seeds have also been extinguished and we do not see a recovery, for the simple fact that there are not strong enough reasons for this to happen. The goods will find their way from Ukraine, the European production indicated an excellent volume, the soybeans are also high. The basics tell us that we should not be meaningless players. The goods must be secured. Harvest pressure will begin or rather has already begun.

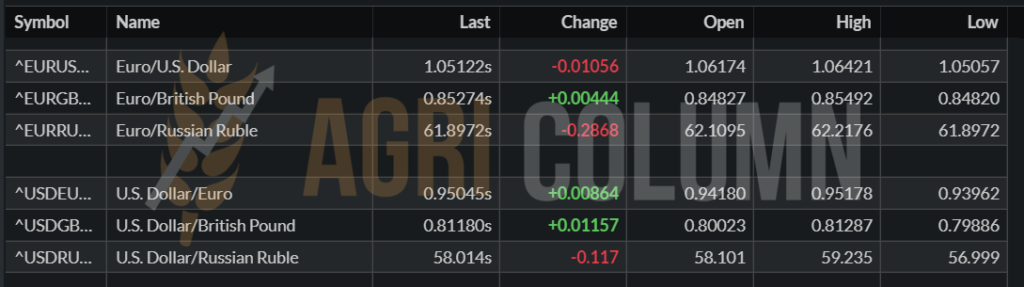

EURO/USD 1:1.05 USD/RUB 1:58 !!!

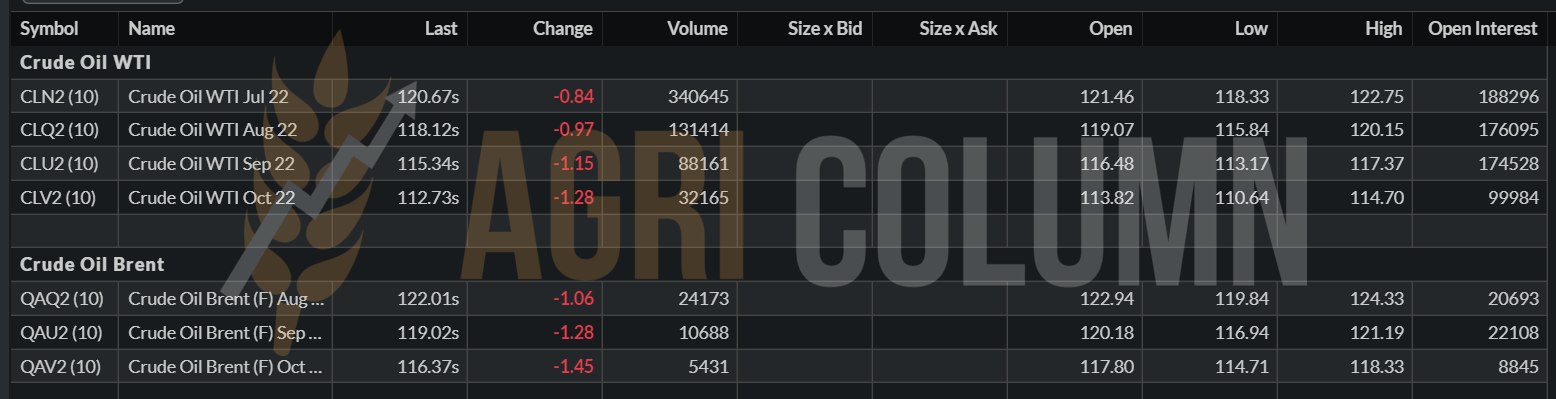

BRENT – 122 USD/barrel | WTI – 120.67 USD/barrel

12-19 June 2022

Romania

Europe

Ukraine

Russia

Canada

USA

Brazil

Argentina

China

Australia