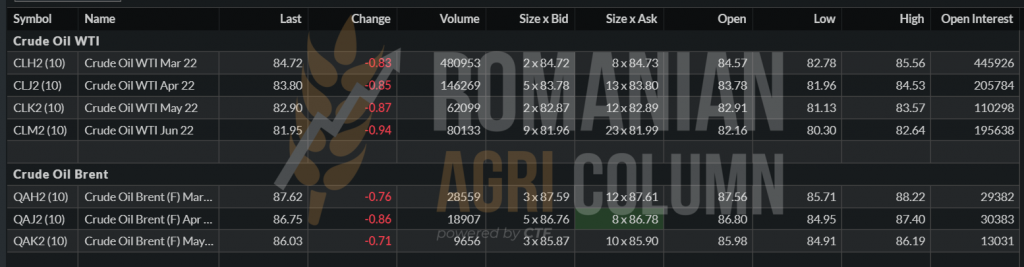

This week’s market report contains information on:

LOCALLY

Local wheat indications have risen in the past week. Thus, we noticed the transition from 263 EUR/MT to a level of 275 EUR/MT in the CPT Constanța parity. Some buyers purchased larger lots for 277 EUR/MT to secure their sales some time ago. Wheat remains in surplus in Romania. We have larger lots and they are starting to be sold. The expectation of a higher price than last year’s highs (towards the end of the year) is still maintained, although market conditions have changed radically.

What has been built in a week in terms of price, i.e., the difference between 263 and 275 EUR/MT, is nothing but the effect of price tensions in the Black Sea basin. If the tensions dissipate or disappear in the near future, we will see a price and logistics competition between the pool and the other origins, the USA, Argentina and Australia.

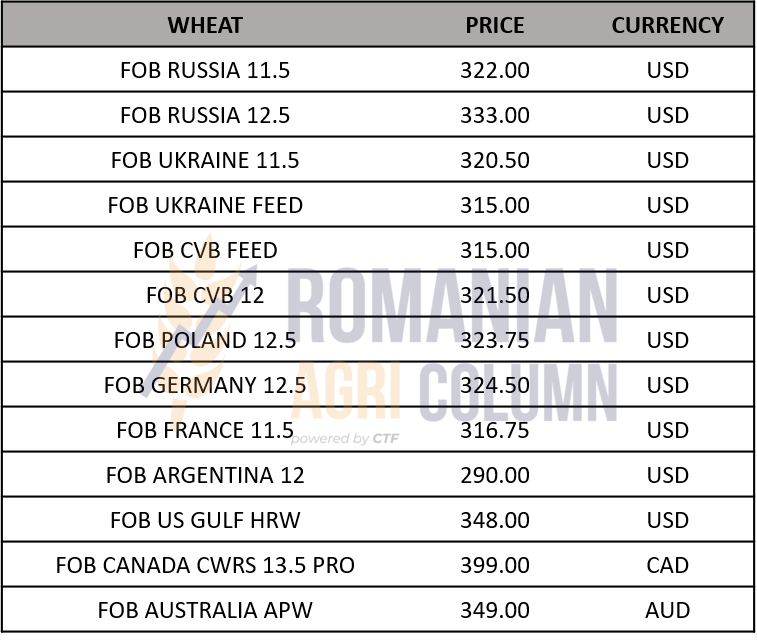

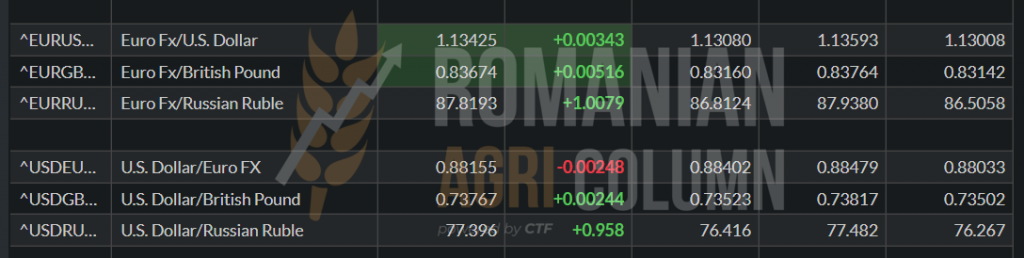

In the FOB CVB (Constanța-Varna-Burgas) parity, we note the indication 321 USD/MT, equivalent according to parity 1.134 with 283 EUR/MT. When extracting the fobbing costs, we have an indication of 276 EUR/MT, without the exporter’s margin included, which is perfectly aligned with the indications offered by exporters in the port of Constanța, i.e., 273-275 EUR/MT. The price of feed wheat is reduced by a minimum of 8 EUR/MT compared to milling wheat. CVB FOB indication is currently 315.5 USD/MT. It should be noted that both FOB CVB indications, PRO12 and feed wheat, decreased by USD 2/MT.

As for the new crop and its price, things have changed very little compared to last week. The indications of 228-234 EUR still reside these days, according to the EURONEXT SEP22 calculation, minus a premium of 16-20 EUR/MT, depending on the exporter. The difference for feed wheat is minus 5 or 6 EUR/MT.

We maintain the recommendation of forward sales of 1-2 tons per hectare to try to minimize market risk and leveling through a final average price that will cover the costs of setting up and raise the level of profit on the farm and, implicitly, that of profitability per hectare. A level of 20-25% sold now can balance the imminent harvest pressure, as shown by the potential in the Black Sea basin and the European Union at this time.

REGIONALLY

In the Black Sea basin, exports continue, but Russia’s monthly average is declining compared to last month’s monthly average between July and December (3.1 million tons/month this season versus 4.1 million tons/month last year). In contrast, Ukraine indicates a much higher level than the same period last year, taken as a monthly average (2.7 million tons versus 2.1 million tons).

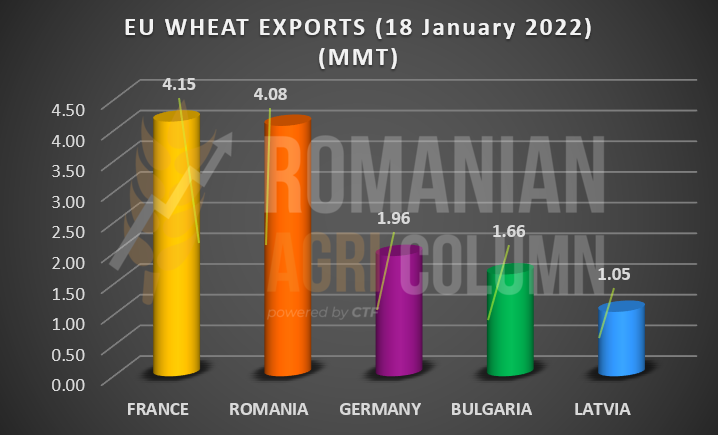

In the European Union, we register a level of 15,324,000 tons of exports until January 18, 2022, for the marketing year 2021-2022. Compared to last season, the monthly average between July and December is increasing from 2.2 million tons to 2.5 million tons. At the top of the list is France, with 4.15 million tons, followed by Romania, with 4.085 million tons. Germany follows in the top exporters with 1.96 million tons, and the fourth position belongs to Bulgaria, with 1.66 million tons. The last of the top 5 to be noted is Latvia, with 1.05 million tons exported until January 18, 2022.

The Black Sea basin market remains tense due to Russia. Thus, Romania and Bulgaria are intensifying their competition in the sale of wheat to Russia and Ukraine, becoming much more competitive. If we take into account the level of export tax set for the following week, amounting to 95.8 USD/MT, we note a price level for PRO 12.5 wheat in FOB Russia of 333 USD/MT.

Ukrainian wheat remains at the same price level, namely 320.5 USD/MT in FOB parity for PRO 11.5 quality.

In the EURONEXT plan, we see the increase based on the Russian-Ukrainian tension, but, as we anticipate, we also see a rebound generated by a high level of unrest that has decreased as a potential after the last meeting between Blinken and Lavrov, which did not reach any result, but bought each other time.

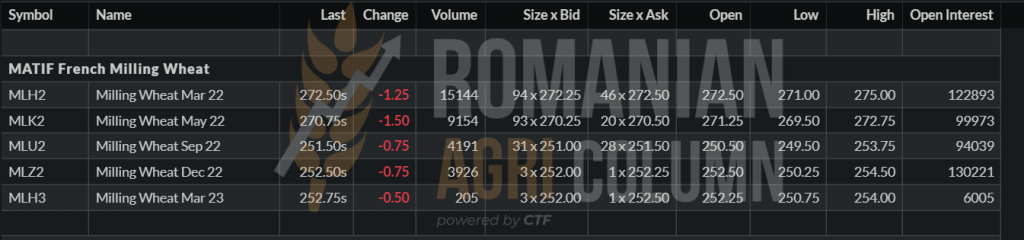

EURONEXT MLH22 – 272.5 EUR at the close of 21 January 2022.

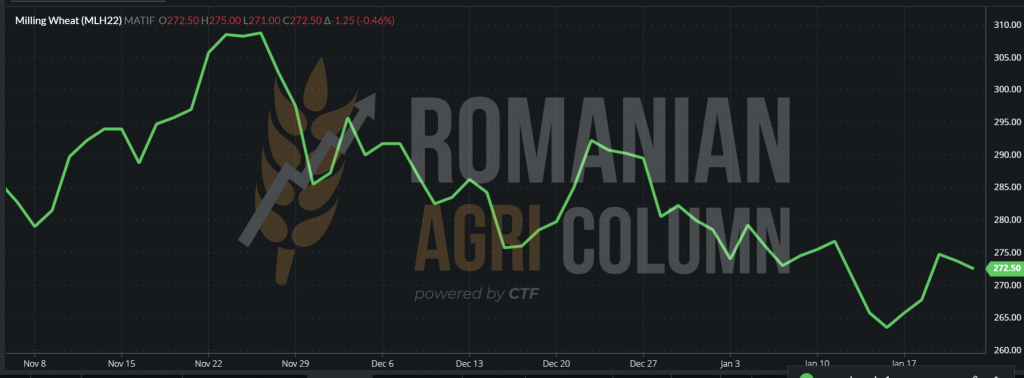

EURONEXT – MLH22 GRAPHIC. We note the decrease of EUR 2.5 at the close of January 21, 2022.

GLOBALLY

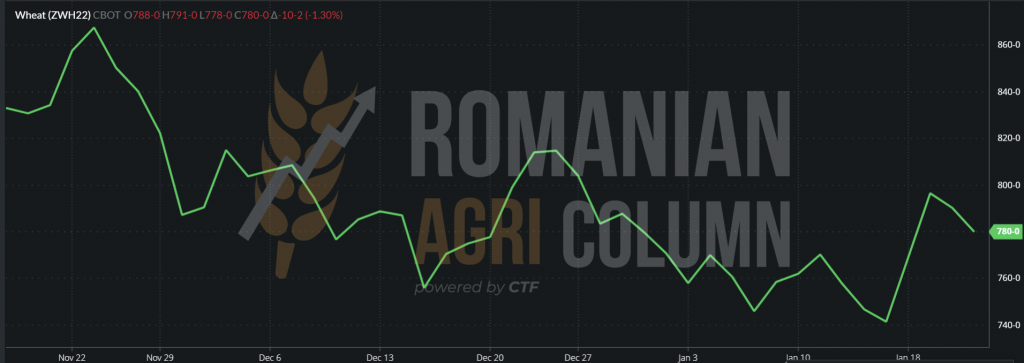

In terms of global wheat trade, we note that the US has had a very high level of wheat exports since the beginning of 2022. This intense activity was instantly reflected on CBOT, where the investment funds came in for the opportunity to make a profit.

This was reflected in a sharp increase in wheat yields. The American export associated with the tension in the basin brought the American wheat to 800 c/bu, starting from a level of 740 c/bu.

But things soon changed. As we noted above, the break in the US-Russian negotiations has tempered the enthusiasm of the funds and thus we record the decrease to 780 c/bu. In other words, we gained a level from 740 c/bu to 780 c/bu, that is 14.7 USD.

CBOT XZWH22 – 780 c/bu (-10 c/bu) at the close of the trading session from 21-22 January 2022

Regarding the most important global tenders, we note:

- Iran with a purchase of 195,000 tons of wheat from Russia, Germany or the Baltic countries. But Iran has a long way to go in recovering from the severe drought that hit the country last season. The indication of the need for imports remains at about 7 million tons.

- Jordan is launching a new tender in an attempt to buy 120,000 tons of wheat with closure on 1 February 2022.

INDICATIONS OF WHEAT PRICES VARIOUS ORIGINS:

ANALYSIS

- The wheat market is driven up by two associated factors – tensions in the Black Sea basin, to which is added the enthusiasm of American sales since the beginning of the year.

- Romania and Bulgaria are much more competitive than Russia and Ukraine in terms of wheat sales.

- The new wheat crop is currently in good condition at the level of the Black Sea basin.

- At the level of the European Union, based on the good start taken in autumn, Western and Central Europe are in very good condition. Some isolated problems are found in Poland, the Baltic States and Scandinavia. In contrast, Eastern Europe is experiencing a milder temperature regime for this period. However, the forecast indicates a cooling of the weather in this region as well, due to the movement of a wave of cold air from the polar origin.

- If the status quo remains the same, and we are referring to the fact that there will be no conflict in the area, wheat will have a decrease in price in February. Russia’s export program is still a long way off, and the tax will force Russian farmers to start selling quickly in mid-February, when we will all see much better crop forecasts.

LOCALLY

The indications of the port of Constanța regarding the feed barley remain at the level of over 240 EUR/MT. In the case of larger batches, they may amount to 245 EUR/MT. However, liquidity is quite low, provided that demand is strong for this raw material.

REGIONALLY

TMO Turkey has concluded a tender in which it has purchased a quantity of 345,000 tons of barley. On average, prices ranged from 316 USD/MT CIF Tekirdag to 326.8 USD CIF Izmir. Compared to the previous tender, the sales values decreased by an average of 31 USD/MT. In the same EXW Antrepo auction, we note the prices of 322.8 USD/MT Samsun and 331.8 USD/MT Izmir, about 37 USD/MT lower than the previous auction of December 23, 2021.

Barley prices in the Black Sea basin are at the level of 295 USD/MT FOB Russia, increasing by 2 USD/MT compared to the previous days.

As for the future crop, it is under normal auspices for this period of time in the Black Sea countries, Ukraine and Russia, respectively, as well as in the countries that make up the European Union.

GLOBALLY

Algeria bought 205,000 tons last week, and Jordan is launching a new tender for the purchase of 120,000 tons, closing on February 1, 2022.

Nothing changed in the global status of barley. The deficit between production, consumption and stocks remains. This is practically the global demand for fodder barley.

The price of barley in the southern hemisphere is 261 USD/MT FOB Australia.

LOCALLY

Price indications in the port of Constanța have increased to the level of 240-243 EUR/MT in the past few days in the CPT parity. This support comes from the fear of rising tensions in the Black Sea basin, knowing that Ukraine is the main reservoir of corn. Romanian farmers are starting to trade corn, just as we said in the last issue, as it is a necessary thing to consolidate the capital in the preview of the spring works that will arrive soon. CVB FOB indications are currently 252 EUR/MT. Extracting the fobbing costs, we have an indication of 243-244 EUR/MT CPT, without the exporter’s margin included and without financing costs.

Romanian corn reached the export level of 2,400,000 tons in the 2021-2022 season until January 16, 2022.

REGIONALLY

Ukrainian corn supports the price of corn in the Black Sea basin through sales to China. Ukraine currently has a corn crop of 39.7 million tons, according to Ukrainian analysts. In the FOB Ukraine parity, maize is quoted at the level of 278-279 USD/MT, which reflects 245-246 EUR/MT.

EU imports of maize currently amount to 8,260,000 tons. Spain is among the top importers with 3.3 million tons, followed by the Netherlands with 1.55 million tons. The top is completed by Portugal, with an import of 0.92 million tons, Italy with 0.72 million tons and Ireland with 0.58 million tons.

EURONEXT indicates a healthy level of maize at the moment, helped by the South American problems, especially the Brazilian ones, and the political problems in the Black Sea basin.

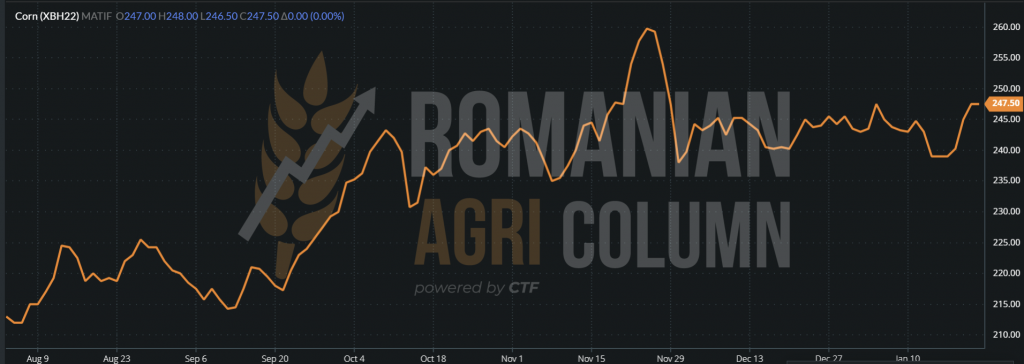

EURONEXT XBH22 MAR22 – 247.5 EUR at the close of January 21, 2022.

EURONEXT – CORN TREN GRAPHIC – XBH22 MAR22. European maize is set in a range of between 238 EUR and 245 EUR.

What to look for is the NOV22 crop inverse, which is at the 20 EUR level. In other words, if someone wants to sell today the new corn crop, the one that will be sown in the spring, will have a price level of NOV22 minus 10 EUR related to CPT Constanța.

GLOBALLY

The US is starting to massively sell corn. Last week’s closing finds a million tons in the North American sales account. The destinations of this figure of 1 million tons are Mexico, Japan and a destination still unknown.

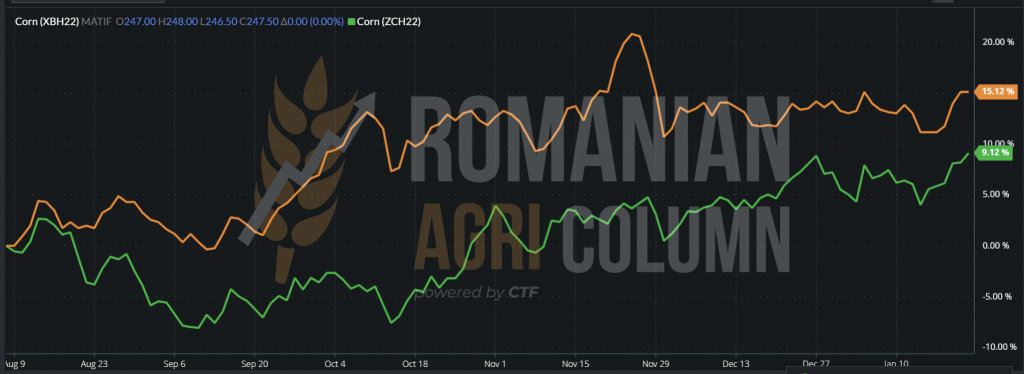

CBOT reacts to these sales levels and raises the indication ZCH22 to 616 c/bu.

CBOT ZCH22 TREND GRAPHIC – the level above any previous indication can be observed, starting with August 2021.

PRICE INDICATIONS IN VARIOUS ORIGINS

ANALYSIS

- In the short term, corn has increased in indications because of two reasons – the South American weather and the problems between Russia and Ukraine.

- We still maintain at the working hypothesis that competition between South American and pool origins will put pressure on the price.

- In the absence of a conflict, Ukraine will accelerate sales after mid-February, creating additional pressure on the Black Sea basin.

LOCALLY

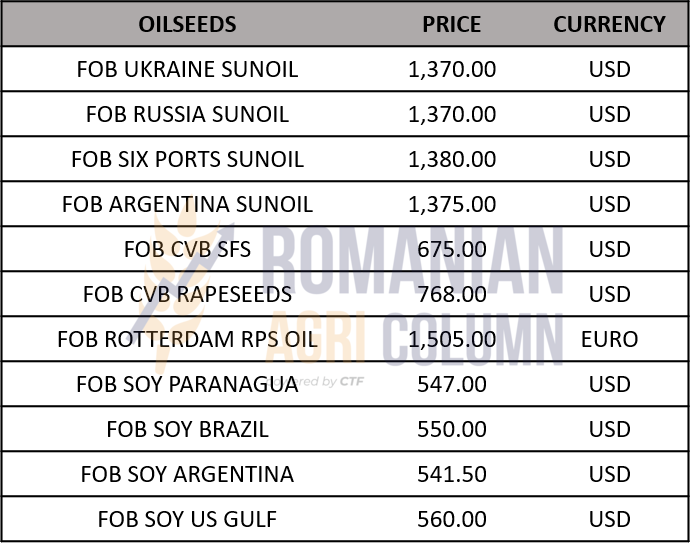

The old rapeseed crop is almost non-existent in Romania. Despite the support provided by the demand, large batches of rapeseed are not found in the offer of Romanian farmers at this time. The CVB indication for rapeseed is currently at the level of 770 USD/MT FOB CVB, which, converted into EUR, at the parity of 1.134 and brought to the level of CPT Constanța indicates 670 EUR/MT, without the exporter’s margin excluded from the price.

The new rapeseed crop is in the same dormacy state. In most cases, the fields are protected from falling snow. In other places there is no protective snow, but the night temperatures are not so low that there is a danger of frost. Romania remains at the 415,000-417,000 hectares sown so far.

We maintain the recommendation to sale through the AUG22 minus Premium mechanism (which can vary between 10 and 0 EUR), with a volume level of maximum 1 ton/hectare, so that the future potential can be preserved by the seller.

REGIONALLY

The rapeseed crop is in very good condition at the moment in western, central and northern Europe due to the good start taken in autumn. In some parts of Poland, Scandinavia and the Baltic States, there are still some problems with the frost, but at the moment there are no signs of concern to make estimates of potential volume losses. Temperatures in Western Europe are normal for this period, while Eastern Europe is rather a bit positive, but not in a worrying way.

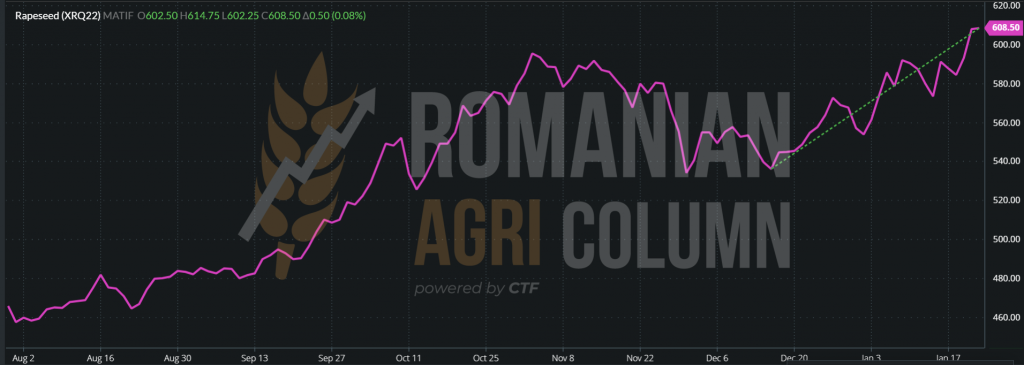

Rapeseed quotations at Euronext level further indicate the lack of liquidity and the desire to acquire Western European processors, so we are already looking at the indication MAY22. We are only a few days away from February and the sell-off or roll-over process will start soon on Euronext. The MAY22 indication takes us to the area of 700 EUR, which translates into “we will be able to estimate the new crop soon”. And the inverse crop at the moment is about 90 EUR, referring to the difference between MAY22 and AUG22.

EURONEXT MAY22 – 697.5 EUR | AUG22 – 608.5 EUR at the close of January 21, 2022

The XRQ22 AUG22 indication went up by about 70 EUR from December 2021 until today, a sign of support for the new crop, amid the lack of predictability of crops at European level and the Black Sea basin. Another contributor to AUG22 is fossil energy, which is rising in BRENT and WTI quotes.

XRQ22 AUG22 GRAPHIC | DEC21 + 70 EUR

GLOBALLY

There is not much to say here, apart from the Canadian canola transactions, which looked positive at the close on January 21st. Canada is out of season, and April will be the start of the season. Australia is also out of season. Harvesting is over and now they are just trading.

CANOLA – RSH22 MAR22 – 1,022 CAD versus RSX22 NOV22 – 827 CAD (+1.50) | INVERSE CROP = 195 CAD

ANALYSIS

- The state of the European rapeseed crop’s vegetation is normal for this period of time, with certain temperatures higher than normal for this period in Eastern Europe, but also with areas affected by frost in northern Europe.

- Ukraine and Russia maintain the same status quo, with snow covering crops.

- The new crop is starting to reduce the reverse of the MAY22 indication, a sign of a lack of predictability in terms of volume forecast, as well as a clear sign of very thin stocks of global rapeseed oil driven by demand.

- Rotterdam indicates 1,505 EUR/MT in FOB parity, a sign of extinguishing the “fire” generated by the lack of coverage of processing units in Western Europe, even if temporarily.

LOCALLY

The general indications are somewhat unchanged in Romania. 640 USD/MT is the norm. For small farmers, this price is also reduced by 10 USD, due to the small volume offered for sale. Romanian farmers with quite significant quantities are waiting for the positive signal that can boost the price level they can get on the kept lots. In the FOB CVB parity, the indications remain at the level of 675 USD/MT, which is equivalent to a level of 660 USD/MT in CPT Constanța.

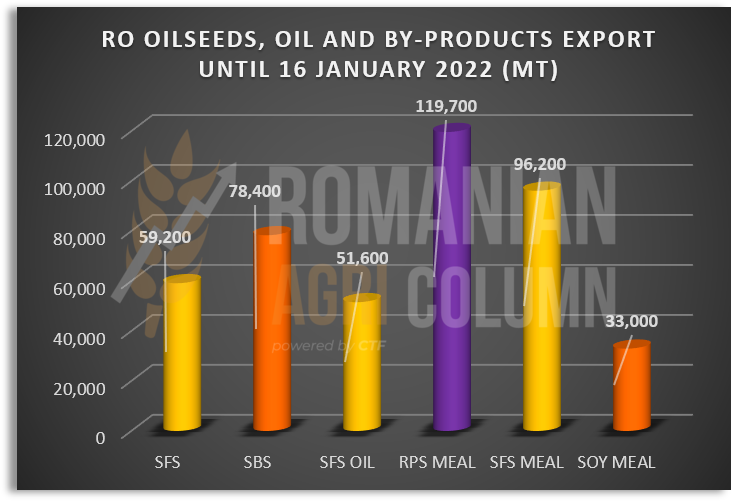

ROMANIAN EXPORTS OF OILSEEDS, OILS AND BY-PRODUCTS DURING JULY 1, 2021 – JANUARY 16, 2022

REGIONALLY

In the Black Sea basin, we see fluctuations in the price of seeds and sunflower oil. In our neighborhood, in Bulgaria, processors from Varna pay 660 USD/MT, while in the country it is traded at the level of 650 USD/MT FCA.

In the western part of Romania, sunflower seeds are traded at a level of 650 USD/MT for goods delivered to the processing units in Hungary, plus the oil bonus.

In Ukraine, the level of sunflower oil increases to 1,370 USD/MT, an increase of 12.5 USD/MT. From some sources we have data indicating an estimated level of 1,390 USD/MT in FOB Ukraine soon. Russia is also raising the price of crude oil by 20 USD/MT to 1,370 USD/MT.

GLOBALLY

Although the pessimistic forecasts of recent times (with a higher harvest than last year, which we explained in detail in the previous issue) indicate a decrease in the price level associated with lower consumption, let’s not forget a few parameters which could support the VEGOIL complex:

- Global levels of sunflower oil are extremely thin, i.e., low, and a rule says that in the first year of recovery, support in commodity prices must remain for restocking.

- The rise in palm oil prices, in turn, supports the level in the VEGOIL complex.

- Soybean oil also provides support.

- The weather in South America is making its mark and raising the price of soybeans.

- And inflation, which is showing no signs of easing, is another external factor supporting the price of crude oil.

Below you will find the closing levels for soybean and palm oil, which are appreciating, especially palm oil.

PRICES VARIOUS ORIGINS:

ANALYSIS

- Sunflower seeds are gaining support from palm and soybean oil.

- Inflation is also contributing to the 20 USD jump in sunflower seeds.

- The price of sunflower seeds in Ukraine has also risen to 21,200 UAH/MT, equivalent to 748 USD/MT (VAT included).

LOCALLY

The price of soybeans is also jumping in Romania, the level easily rising around 650-660 USD/MT. The stocks kept so far can find their optimal capitalization at the moment.

GLOBALLY

The problems are exacerbated in South America, where we are recording new volume cuts and we are referring here, not to Brazil, but to Paraguay. This origin is degraded from 11 million tons to around 5 million tons, this after harvesting 50% of the surface.

In Brazil, things are exactly as we presented them in the last issue. The figures indicate a decrease in production of 8 to 9 million tons, from 142 million to 133-134 million tons.

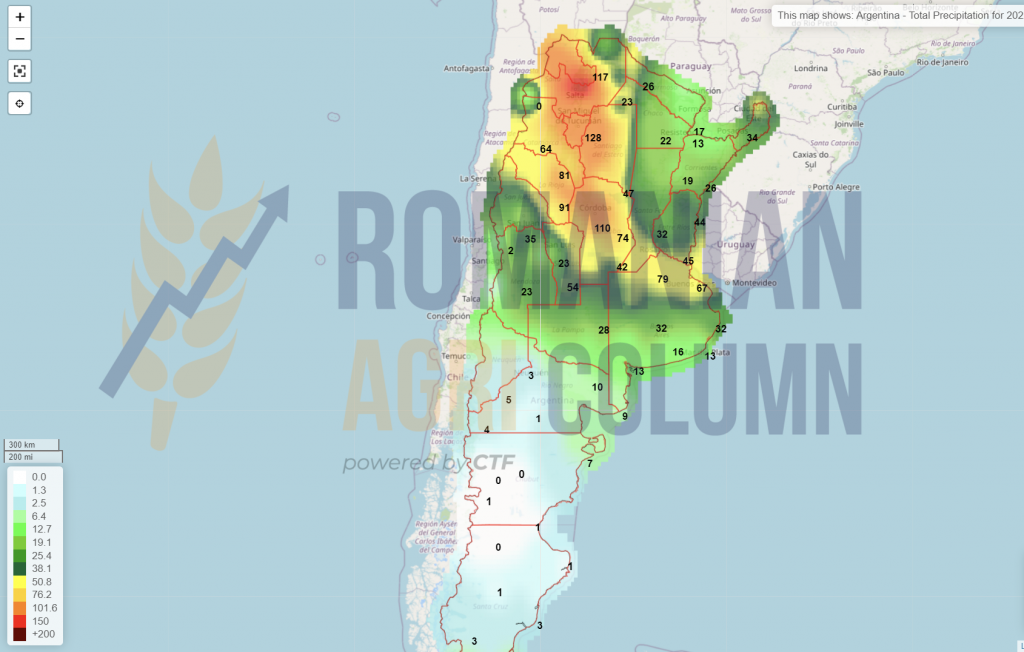

Argentina is in the final stages of planting soybeans and it seems that soybeans in Argentina have the best auspices, because the rains have appeared in the Argentine landscape.

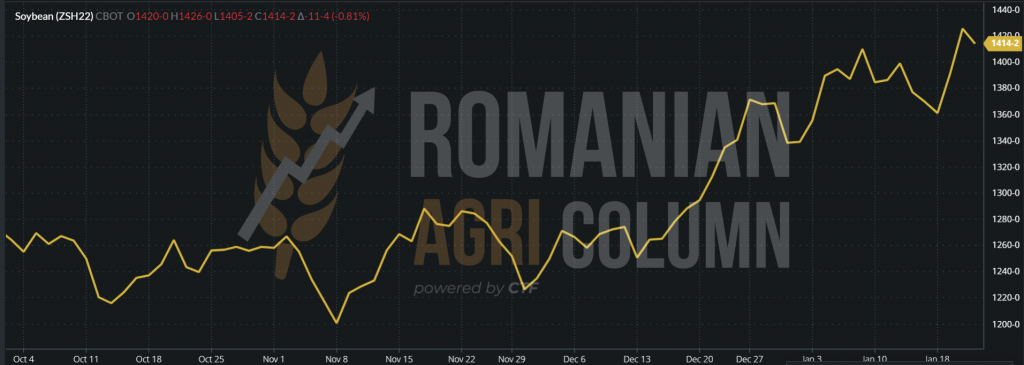

In terms of the stock market, CBOT is setting new levels. At the close of January 21, 2022, the indication ZSH22 MAR22 had the level of 1,414 c/bu, even if it is a decrease compared to the opening level of 1,414 c/bu.

ZSH22 MAR22 GRAPHIC – 1,414 c/bu

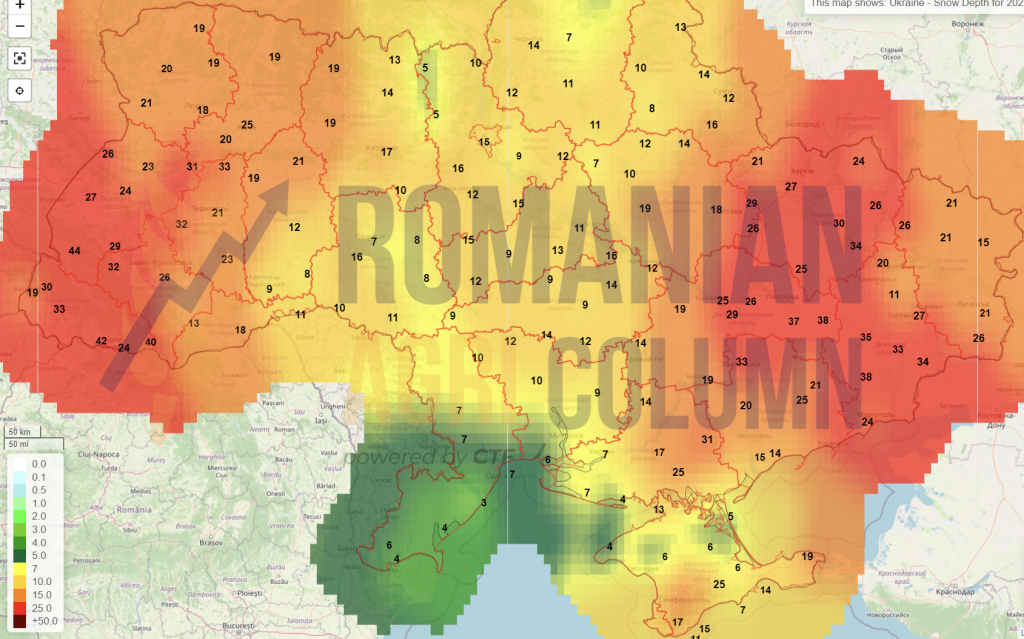

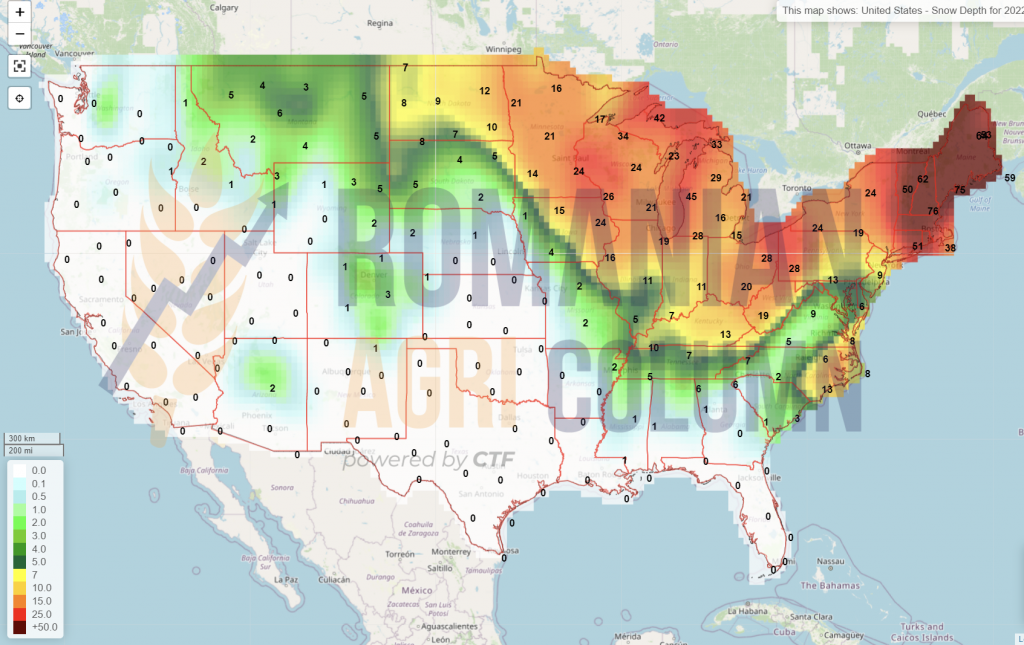

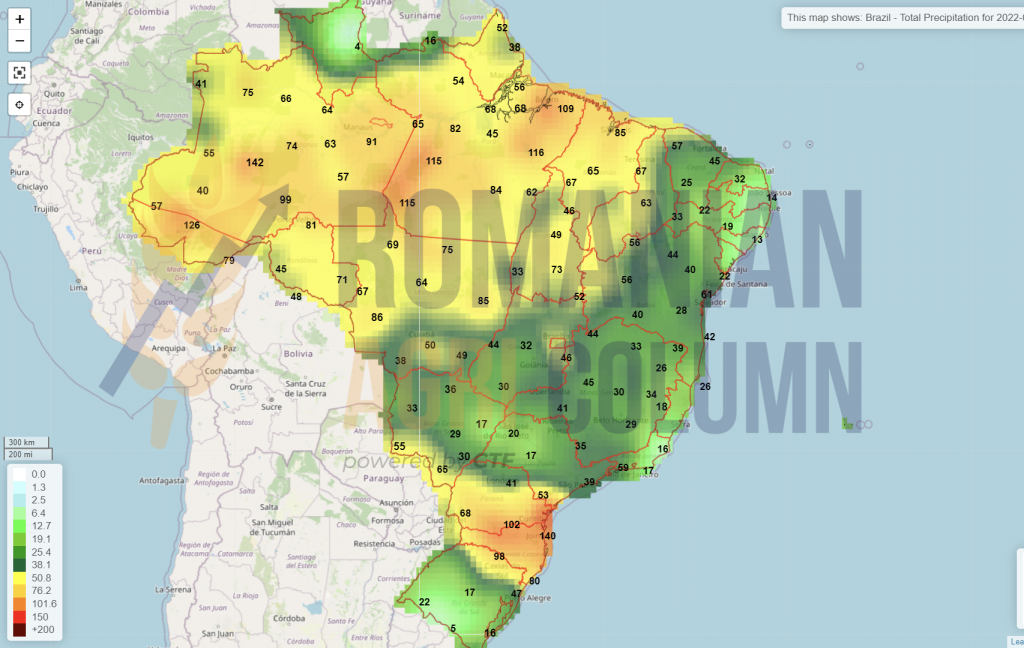

22-30 January 2022

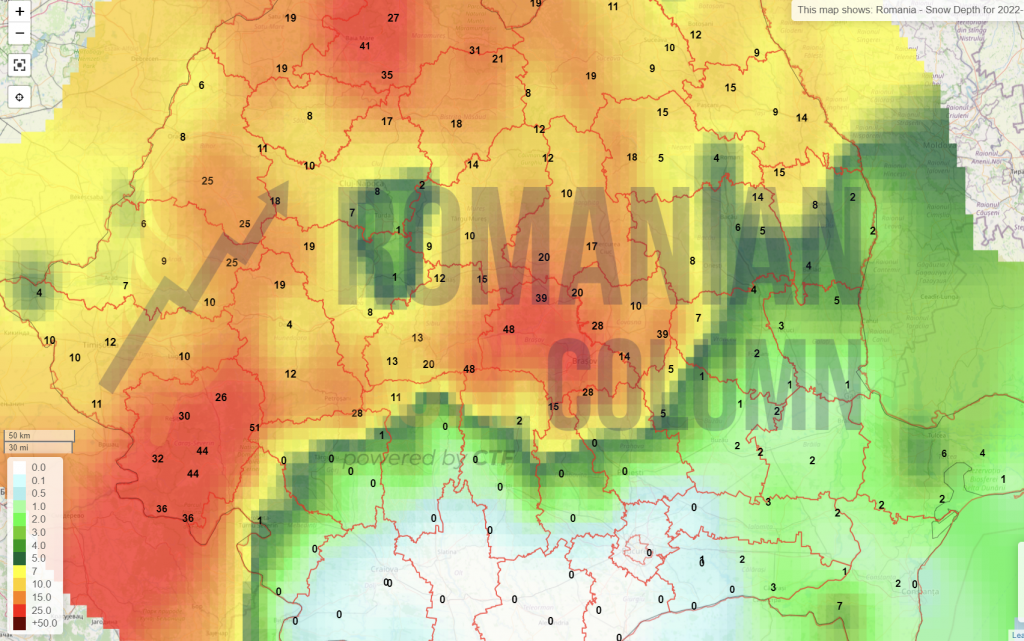

Romania (snow)

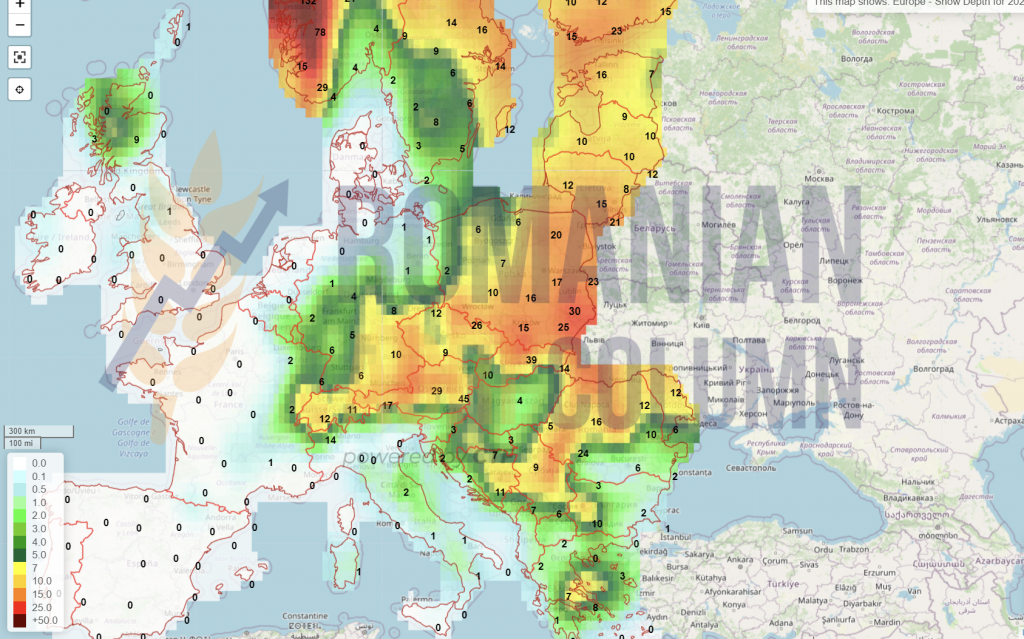

Europe (snow)

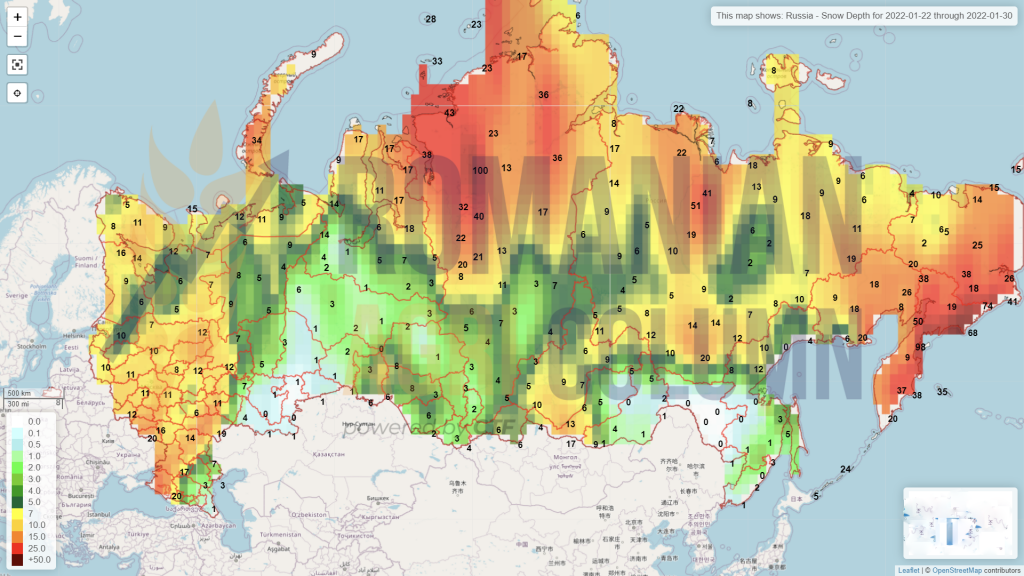

Russia (snow)

Ukraine (snow)

USA (snow)

Brazil (rains)

Argentina (rains)

China (snow)

Australia (rains)