This week’s market report provides information on:

AGRI TRADE SUMMIT, 22 FEBRUARY 2023

The Agri Trade Summit event, from February 22, in Bucharest, organized entirely by AGRIColumn, together with the event organizer Godmother as a partner, was a real success story. Farmers, Traders, Processors, Integrators, Brokers, Logistics Operators, Financiers, as well as companies from 14 European countries participated in AGRI TRADE SUMMIT, the first event of this kind in Romania.

First-ranking authorities welcomed the event, sending messages of confidence and support. Among them, we list: the Prime Minister of Romania, the Deputy Secretary General of NATO, the Minister of Agriculture of Romania, the State Secretary of the Ministry of Agriculture, the European Commissioner for Agriculture, the President of the Committee for Agriculture of the European Parliament, the Plenipotentiary Minister of Romania to the European Union, as well as USDA, through the regional representative for Eastern Europe.

Over the course of the day, more than 800 visitors met, discussed, and opened new ways of collaboration and cooperation.

Thus, Romania has precisely indicated its role and place on the regional and global agribusiness scene, a role awarded through work, dedication, and sustainable development.

This event has the role of strengthening business relations, facilitating cooperation, collaboration between Farmers and all Agribusiness Operators from Romania and the European Union. The event will have an annual regularity, so we invite you to save the date of February 22, 2024 for the next Agri Trade Summit.

We insert only a few moments captured photographically, apart from the 12 television stations that broadcast the opening live for 2 hours, during the AGRI TRADE SUMMIT event.

LOCAL STATUS

The indications of the Port of Constanța hover around the values of 265 EUR/MT.

New crop indications are 240-245 EUR/MT. The crop inverse is therefore 20-25 EUR/MT.

CAUSES AND EFFECTS

EXCERPT FROM PREVIOUS ISSUE: “For the new crop, there is also a term and a time of decision. Romanian farmers must be very attentive to the signals and generate cargo flow in the next 3 weeks. Judging by today’s state of crops in Romania, we have no reason to worry about volumes. But Romania must take the first step, farmers must be ahead of others in the market to preserve the potential of the new crop.”

Our forecasts are coming true and the wheat story is long over, as we have been repeating for many months. Farmers must proceed to sell wheat, old crop, and new crop. We are behind on sales and have no additional motivation not to make them. Indeed, it is the factors of production that penalize profit margins; indeed solidarity lines are hurting Romanian goods, but there is currently no solution. The proposition is extremely simple: the wheat must be sold. Otherwise, we will be left with the commodity that will carry over to the next crop and will, in effect, strengthen the already existing pressure on the market.

REGIONAL STATUS

RUSSIA remains captive to the same clear foundation: it must sell wheat, as much as possible. And we find it all in their commercial behavior. They are highly competitive and generate discounts between 5-15 USD/MT to capture volumes to deliver to Destinations.

In the absence of one of the favored recipients, namely Iran, their volumes are penalized, and this redirects them to other destinations. Five days after the introduction of the grain export quota (from February 15 to February 20), the Russian Federation reduced wheat supplies in annual terms by 7% to 412,000 tons.

Overall, total exports of major grain crops fell 7.4% to 474,000 tons in the February 15-20 period from 512,000 tons a year earlier. Daily grain deliveries fell to 95,000 tons from 102,000 tons a year ago, including wheat – to 82,500 tons from 88,500 tons. The price of Russian wheat continues to fall, and currently the price is 298 USD/MT FOB 12.5 protein.

Slowing grain shipments from southern Russian ports due to bad weather prompted local analysts to revise down their forecast for February wheat exports – from 4 million tons to 3.5 million tons. Overall, taking into account all ports and land exports, the volume reached about 28.1 million tons – 24% above last year’s total export figure.

UKRAINE reported 1.04 million tons of grain exports in the week ended February 23, slightly off the previous week’s pace, according to government data released on Friday. Liquidity on the basis of CPT in the domestic market continued to be limited, due to the lack of free storage spaces at the Pivdennyi, Odesa and Chornomorsk (POC) transboard terminals, as well as in the shallow water ports – Izmail, Reni and Chilia.

More and more sellers are beginning to look further afield, in the direction of sales across western borders, by rail and by road.

Ukrainian exporters recorded 383,323 tons of wheat set to go abroad in the reporting period, a 9% delay from the previous week’s pace, bringing total wheat exports up since the start of the 2022/23 marketing year to 11.1 million tons.

Turkey was the main destination, with approximately 84,329 tons of wheat heading to this country, followed by Bangladesh (76,064 tons), Romania (65,993 tons), Sri Lanka (51,980 tons), Kenya (30,583 tons), Spain (29,948 tons) and Poland (19,971 tons).

THE EUROPEAN UNION. Exports are slowing, forecasts are being revised downwards, French wheat is no longer having such a large weight in the calculations. A maximum of 1.5 million tons are still available for export in the next 4 months.

During the reporting week, 33,588 tons of wheat were loaded for a single shipment to Algeria, reflecting a 72% drop over the week. This somewhat facilitates the other Origins and somewhat encourages Romania to be able to compete with its outstanding export volumes.

EURONEXT – MLK2323 MAY23 – 280 EUR (-11.5 EUR vs. previous week)

EURONEXT WHEAT TREND CHART – MLK2323 MAY23

GLOBAL STATUS

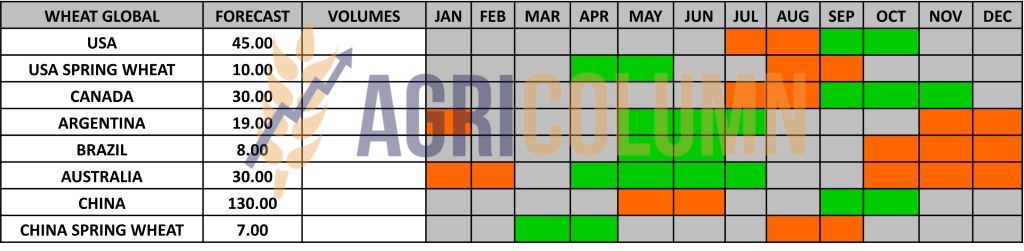

The USA receives forecasts of planted areas and what will be planted in the spring with wheat. And the figures released by NASS (North American Statistical Services) clearly indicate an increase in the areas allocated to wheat. Thus, compared to the October 2022 report, which indicates an area of 18.5 million hectares, the current one indicates an increase in the area by 1.5 million tons, i.e. 20 million tons. This clearly translates into an increase in crop potential which will be driven to a level of over 54-56 million tons. The US averages 3 tons of wheat production per hectare.

INDIA maintains export restrictions on wheat in an attempt to stabilize domestic prices.

EGYPT is setting the minimum domestic wheat reference price at 270 USD/MT to protect the country’s farmers from potential price drops and encourage them to grow.

CBOT WHEAT – ZWK23 MAY23 – 721 c/bu (-55 c/bu (20 USD/MT from previous week)

CBOT WHEAT TREND CHART – ZWK23 MAY23 = level 30 September 2022

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

TENDERS AND TRANSACTIONS

EGYPT GASC bought in the February 22 tender 240,000 tons of wheat of Russian origin (3 x 40,000 and 2 x 60,000 tons) for delivery between April 1-15, paying USD 317.5/MT in CFR parity to Grain Flower (GTCS). Payment is by LC (Letter of Credit), on delivery, and the purchase is financed by the World Bank, as Egypt still has difficulties with the availability of US dollars, which limits private trade.

The date of February 28, 2023 will generate two more extremely interesting auctions. TMO Turkey will purchase 790,000 tons in the auction, and MIT Jordan will again generate a tender for 120,000 tons of wheat.

CAUSES AND EFFECTS

BLACK SEA BASIN. February 24, 2023. One year since the war began. And, apart from Putin’s characteristically perpetuated threats, nothing new on the front. Russia tries to retake positions; they are pushed back and the clampdown continues in the totally absurd way we have seen for a very long time. Putin gives delusional speeches in an attempt to motivate his population. But there, too, generations are changing, and young Russians do not believe in his oppressive and totalitarian regime.

China chimes in with a somewhat neutral statement that avoids pinning things down, but hints with key words, warning of the proliferation of nuclear weapons and suggesting the need to stop the war that is causing the loss of human life.

Otherwise, just a duel of statements between Biden and Putin. But Putin is targeting, at least for now, a disruption of the balance in another area to disguise the attention. He also knows that he cannot support the occupation of an airport in the Republic of Moldova with an airlift. Any Russian transport aircraft trying to pass through Ukrainian airspace will be an easy target, just like a clumsy duck in flight. Other attempts disguised under the civilian presence of supporters at matches were stifled in disguise by services belonging to other countries.

When it comes to wheat trade, Russia doesn’t have many options. We could say that it has only one, namely to sell wheat. Any attempt to manipulate the market by “analysts” has absolutely no effect. Professionals in the field know Russian Maskirovka and completely ignore it. Even the increase of wheat export tax to 70 USD/MT indicated the “hunger” of capital in Russia. The war machine must be fed.

Russia has a lot of wheat to export and maybe it will. Russia is artificially trying to induce presumptions in the case of the new wheat crop as well, as if it is not in good condition. What can we say? This happens every year, certain surfaces can be lost. But Russian stocks are high and spring wheat will be sown soon. Apart from that, the occupied territories of southern Ukraine as well as Crimea can supply them with quantities. Let’s not be afraid, Russia has exploited the southern part of Ukraine in its own interest, capturing the goods and supplying them to countries in the East.

FUNDS, as we predicted in the previous issue, are massively liquidating and effectively bleeding the wheat market. It was normal for this to happen. In a few days we are right into, we might say, the next year. The MAY23 wheat indication is for seasonality and supply calculations are already being made for a maximum of 3.5-4 months. The CBOT-generated drop of 55 cents/bushel or 20 USD/MT very accurately indicates this. EURONEXT is sure to agree with the CBOT on February 27th and 28th.

PHYSICAL FUNDAMENTALS are clear at this time. Wheat has demand coverage and in the short to medium term there will be no coverage issues. The countries of the Black Sea basin have sufficient stocks to meet the demand. We list here Russia, Ukraine, Romania, and Bulgaria. Serbia and other European Union countries follow in line.

Moving to the Antipodes, we clearly see wheat stocks in Australia that can, in turn, cover the demand from wherever it comes and can generate competition even in the European Union. Across the ocean, in the US and Canada, there is sufficient wheat stocks, and these two origins are also behind in stocks.

The Argentine Origin is offset by the rest of the Global Origins.

And NASS, through its stock and acreage forecasts, once again certifies the existence of wheat as a raw material.

CEREAL CORRIDOR – UKRAINE. The deadline for the end of the period is fast approaching, more precisely on March 18, 2023, and the parties involved are generating discussions about its extension. Russia shows obvious dissatisfaction with this aspect.

One thing is very clear and certain. Russia agreed to this corridor. Yes, indeed, she used it to handle her goods, in turn. Its style was characteristic, it delayed as much as it could the inspections in Istanbul to narrow the Ukrainian flow. And, apart from the narrow one, they achieved something else, namely: they made Ukrainian goods more expensive, for the simple reason that waiting for inspection costs money. Shipowners charge and it’s all reflected in the price of the goods. So Russia got what it wanted – the elimination of competition from destinations. And we mean wheat, corn, and sunflower oil here. Suffocation and Expensive. These two parameters were pursued and achieved by Russia.

We believe that this corridor will be extended, because apart from the above, Russia has another advantage, which is that it appears to the world as a humanitarian factor allowing food to circulate. Yes, it is a form of blackmail with great commercial benefits.

However, closing the corridor would not increase the price of goods. Why? It is extremely simple: The pressure will shift to the countries on the eastern flank of the European Union. Ukrainian goods transiting at these times will increase their volumes, exerting pressure on the selling prices of local farmers, maintaining, or even lowering the price level.

The advantages of Ukrainian goods are obvious: they have no tariff or technical (sanitary-veterinary) barriers for access to the European Union.

But I have a very pertinent question: what will the European Union do soon? Because, as things stand today, autumn crops in the EU are looking good. Wheat looks in shape, rapeseed too, with more area allocated in the seeding programme. The crisis of disgruntled farmers will spread within the Union soon because this competition is unethical.

- EU farmers have high production costs compared to Ukrainian farmers.

- Farmers in the EU follow European norms, rules and procedures, which is not the case in Ukraine.

And here we are talking about unfair competition, not about anything else. All sympathy for the farmers in Ukraine, but the competition is unfair, clearly looking at the imports of Ukrainian goods that not only transited through Romania, Poland, Hungary and Bulgaria but remained in these countries.

CONCLUSIONS:

- Wheat has no motivation to grow explosively.

- The wait is fleeting, and stocks must be sold.

- Time is running out and April and May are closer than we think.

- Global stocks ensure the transition for the next 4 months.

- Crops in the Northern Hemisphere indicate positive notes in terms of vegetation status.

- Crops in the southern hemisphere exceeded forecasts.

LOCAL STATUS

The feed barley price indications remain in the 240-242 EUR/MT indication area, CPT Constanța parity.

Price increases were noted for a short period of time on the back of short demand for spot supply from certain buyers who had to fill vessels awaiting loading, and the level offered for these spot requests was 250 EUR/MT.

REGIONAL STATUS

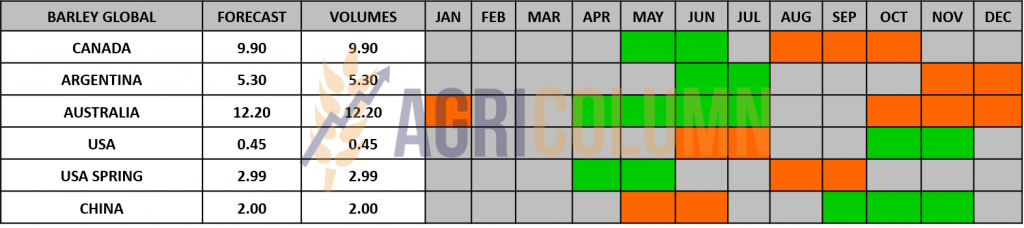

RUSSIA. Barley export duty rose again this week to 51.73 USD/MT.

UKRAINE. The weekly volume of barley exports rose to 59,794 tons, and the total volume exported since the start of the 2022/23 season rose marginally to just over 2 million tons.

TENDERS AND TRANSACTIONS

MIT JORDAN bought 60,000 tons from AgrochIrnogi at 295 USD/MT for delivery in the second half of July.

TMO TURKEY seeks through a tender 440,000 tons for delivery on March 10 – April 10 or April 11 – May 11, in the ports of Iskenderun, Mersin, Izmir, Bandirma, Derince and Samsun. The deadline is March 2, 2023.

BARLEY PRICE INDICATIONS IN MAIN ORIGINS

GLOBAL STATUS

CANADA. Barley exports during the week totaled 135,000 tons, a 10% increase from the previous week’s pace. The total figure for the current marketing year stands at 2 million tons, an increase of 19% over the previous year.

LOCAL STATUS

Corn indications in the port of Constanța are starting to decrease, so for spot deliveries we are recording levels of 260-262 EUR/MT. For April deliveries, levels of 267 USD/MT can be achieved.

CAUSES AND EFFECTS

Corn is starting to lose ground nationally in terms of prices. It is an effect generated by the USDA’s NASS report as well as the IGC’s global production, stocks and consumption reports. It was a predictable thing, because from these reports emerged the conclusions that we listed in the previous issue. One of them clearly referred to wheat as a price driver. Technically, the price of corn was equal to that of wheat and the differentiation according to the factor of Demand and Supply had to be taken into any supply formula. Romanian farmers should not wait as in the case of wheat. Waiting could cost a lot in the near future.

REGIONAL STATUS

UKRAINE. Ukrainian corn has problems, starting with reduced liquidity due to congestion in the Corridor (making storage spaces very limited as a side effect of Russian delays in inspections in Istanbul) and ending with some quality issues that are penalizing the commodity Ukrainian clearly and directly. Thus, many suppliers of Ukrainian goods are looking for the roads of the west, by rail, road and river.

The weekly volume of corn declared for export rose to 604,470 tons, which represents a delay of 7% from the pace of the previous week and brings the total volume of corn exported since July 1 to 17.8 million tons.

In the reported week, China remains the main destination for Ukrainian corn, with 138,076 tons declared, while 113,000 tons were declared for delivery to Romania – the main transit destination from which grain is re-exported. This was followed by Hungary with 56,190 tons, the Netherlands with 7,426 tons, Italy with 44,948 tons, and 40,177 tons went to Kenya. Finally, approximately two cargoes of approximately 34,500 tons were listed as bound for Poland and Israel.

RUSSIA. The corn tax increased to 30.25 USD/MT. The calculation of the index for corn and barley currently takes into account transactions recorded on the basis of loading in the ports of the Caspian Sea, as well as in the ports of the Sea of Azov and the Black Sea.

EURONEXT CORN – XBM23 JUN23 – 279.5 EUR (-11.25 EUR vs last week)

EURONEXT CORN TREND CHART – XBM23 JUN23

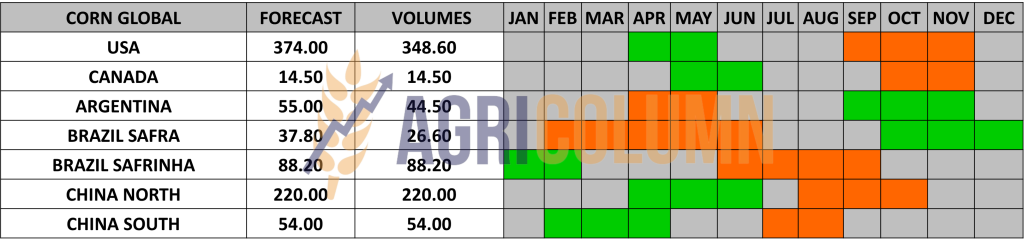

GLOBAL STATUS

USA. NASS forecasts higher US corn stocks. At the OCT22 report, US stocks were 43.5 million tons, and at this date they are 46.5 million tons, taking into account the disappearance rate (consumption). Also, the seeding forecast was raised from 35.85 million hectares to 36.84 million hectares, representing an increase of 0.97 million hectares. This increase associated with a yield of 11 tons per hectare indicates an increase in the North American volume forecast. U.S. net corn sales reached 823,300 tons in the week to Feb. 16, beating analysts’ expectations but down 20 percent from the previous week, according to weekly USDA data released Friday.

ARGENTINA. BAGE once again reduces the volume forecast for Argentine corn, from 44.5 million tons to just 41 million tons. Acreage rated good to excellent for corn fell 2 points to 9%, while moisture is rated favorable in 40% of the area, down 5 points from the previous week.

Farmers’ sales for the 2022/23 maize crop rose 185.7% to 460,000 tons in the week to February 14, while sales for the 2021/22 crop fell 1.5% to 655,000 tons.

Cumulatively, a total of 7.8 million tons of the 2022/23 crop has been sold to date, down 49.2% from the 15.4 million tons seen at the same time last year.

Meanwhile, total sales of the old crop reached 46.3 million tons, down 4.5% from last year.

Export license applications for the 2022/23 crop were 10.4 million tons, down 53.2% from the same period in 2022.

BRAZIL continued Safrinha corn plantings at the same slow pace but recovered some of the previous week’s gap. Brazilian exports slowed down a bit, after competing with the US for a long time and generating significant export volumes.

The rains, however, are still causing delays in Safrinha sowing, and the time window for this process is narrowing.

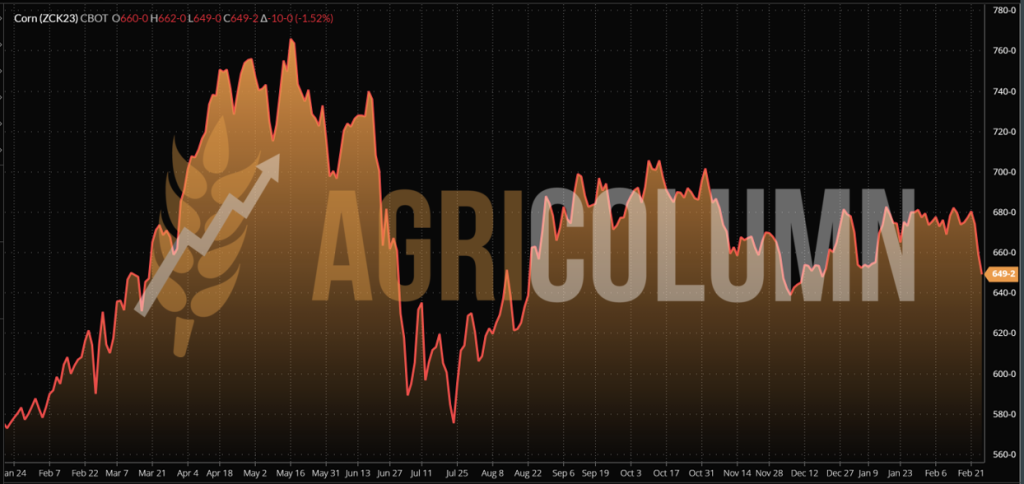

CBOT CORN ZCK23 MAY23 – 649 c/bu (-28 c/bu = -11 USD/MT from last week)

CBOT CORN TREND CHART – ZCK23 MAY23

CORN PRICE INDICATIONS IN MAIN ORIGINS

CAUSES AND EFFECTS

EXCERPT FROM PREVIOUS ISSUE: “But we must be aware that this price platform will not remain at this level indefinitely. With each passing week, it erodes. Why? It is extremely simple. The South American volumes will be known, and at this moment, we do not think that they will be able to decrease, so the premises could reverse, and we could see corn at the level of 245-250 EUR/MT in the CPT Constanța parity.”

And so, based on what we forecast last week, corn is starting to lose ground. Factors generated by IGC through forecasting associated with the report generated by NASS lead to this state of affairs. NASS basically points to high US stocks and much higher seeding forecasts driven by fertilizer prices. So, we have a good ratio for American farmers, an impulse to grow more corn.

Couple this with the potential closure of the Grain Corridor and the pressure coming from Ukraine in terms of volumes offered for sale at a higher discount than today and we see the balance of corn balanced in terms of production, consumption, and stocks. This is obviously putting pressure on its price, as the loss on the CBOT associated with liquidations points to a minus 11 USD/MT. This is also reflected in the physical market.

That’s why we think we could soon see lower price levels than today. The price support platform no longer makes sense at this point and with all the potential declines in Argentina, demand is covered. The US has large stocks, Ukraine exports and the European Union is almost covered. If we also take into account Brazil with the very good sales of Safra and the potential of Safrinha, we have a correct and complete picture.

In addition, the FED will further correct interest rates, and oil prices appear to be stable globally. Moreover, we are coming out of winter, and the price of gas no longer has a basis for growth, the Russian blackmail was bankrupt in this regard.

LOCAL STATUS

Rapeseed quotations in the port of Constanța fluctuate according to EURONEXT. Indications vary from buyer to buyer depending on their interest, between the indicative level of 510 EUR/MT (which shows lack of interest) and the highest price level offered of 520 EUR/MT, there is still a difference notable.

CAUSES AND EFFECTS

Romania has a problem today. Rapeseed stocks are at a high level and some estimates lead to figures of around 0.4 million tons. It is an extremely high level; Romania did not have such stocks in this period of the year.

This product must be sold, the ephemerality of a very high price no longer has any foundation in the physical market. Otherwise, these volumes will move to the new crop and will create additional pressure on the new crop, from the price point of view. Rapeseed must find its way. The new crop must also start moving in the sense of forward contracting.

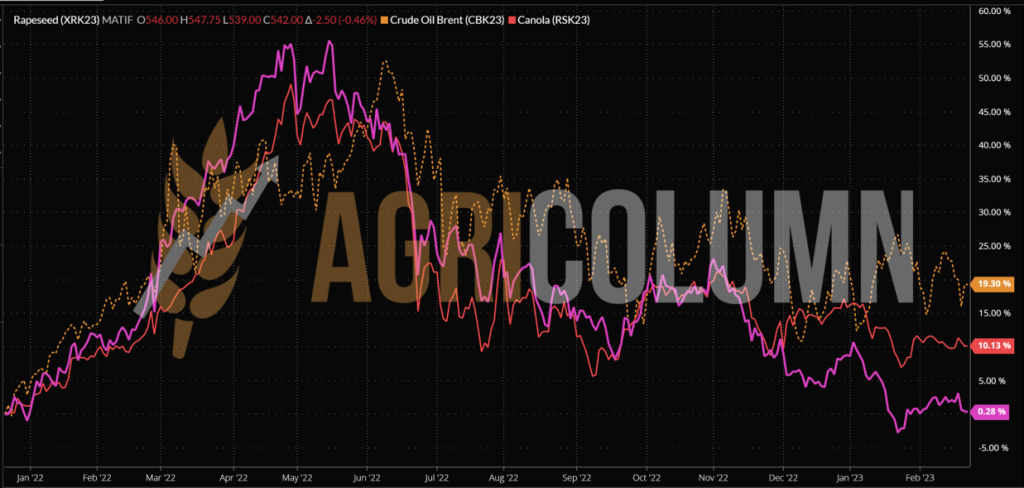

EURONEXT RAPESEED – XRK23 MAY23 – 542.50 EUR (-8 EUR vs. last week)

EURONEXT RAPESEED TREND CHART – XRK23 MAY23

REGIONAL STATUS

The EUROPEAN UNION is going through a good period from the point of view of the rapeseed vegetation stage. Forecasts remain the same and no problem is indicated at this time. In terms of imports, coverage is sufficient from the two main sources, Ukraine and Australia.

GLOBAL STATUS

CANADA. The weekly pace of CANOLA exports increased by 4.7% to 190,800 tons, bringing total exports since the start of the season to 4.89 million tons, up 30.7% from last year.

ICE CANOLA RSK23 MAY23 –819.7 CAD (same as previous week)

ICE CANOLA TREND CHART – RSK23 MAY23

COMPARATIVE GRAPH. PETROL-RAPESEED-CANOLA CORRELATION

CAUSES AND EFFECTS

EXTRACT FROM THE PREVIOUS REPORT: “We think it’s a good time for a forward sale. Under the condition of a production of at least 2.5 tons per hectare, an operational margin of 25-30% of the investment value per hectare can be captured.”

The past week warranted the forecast and the technicality of the conclusions that you find above in the extract. We thus reach the end of February 2023 and the harvest of the season in the Northern Hemisphere can be well estimated.

In other words, there is no reason to see sudden spikes in the price of rapseed, only potential spikes generated by spot demand or temporary lack of coverage.

Canada and Australia will go into seeding in at least 45-60 days, so there is plenty of time until then. But with the way the weather is in the two countries at the moment, there are no reasons for concern about raising the price level. Moreover, Australia is extremely competitive in the export of rapeseed, which means that the demand is covered, and the price does not undergo positive changes.

LOCAL STATUS

Port Constanța quotes sunflower seeds at values between 530-535 USD/MT.

Processors are correlating and indicating a trading base of 520-525 USD/MT at DAP Processing Units parity.

CAUSES AND EFFECTS

At the moment, we have a slow tempo of demand caused by the congestion of crude oil in the port of Chornomorsk and the lack of ships that need to arrive to load. It is something that, combined with the USD that has strengthened in the last week, creates pressure on the price of the raw material.

REGIONAL STATUS

UKRAINE. There is a lot of logistical pressure right now in Ukraine. Oil already produced cannot be delivered and this lowers the price level. Local processors are no longer interested in paying high price levels for the raw material, as they no longer deal with oil, stocks are high.

RUSSIA imposes export tax on sunflower oil starting March 1, 2023. The starting level of the tax is 27.1 USD/MT.

GLOBAL STATUS

PRICE INDICATIONS FOR OILSEEDS AND CSFO IN MAIN ORIGINS

CAUSES AND EFFECTS

Sunflower seeds are feeling the pressure of lack of demand at the moment. Palm oil is what drives the VEGOIL complex eight now.

The strengthening of the USD is another factor adding to pressure on sunflower seed prices. The Russian export tax on crude sunflower oil is a factor that should provide support ($27/MT).

The month of March is the one that will define the trajectory of the seed price, and that until around March 15-20. The closure of the corridor will increase the pressure on the price of the raw material, as it will find its way through Romania, Bulgaria and Poland, and this aspect impacts through discounts and the fact that the added value through processing will be captured locally through import and re-export or intra community trade.

LOCAL STATUS

In Romania, the price indications for soybeans are at the level of 560 USD/MT DAP processing units for non-GMO soybeans.

REGIONAL STATUS

UKRAINE. Weekly oilseed exports fell in the week ended February 22 due to delays in inspections in Istanbul, which make it difficult for ships to arrive on time for loading. Soybean exports during this period fell to 80,641 tons, with a substantial volume delivered to the Netherlands (30,357 tons). Thus, the total volume of soybeans exported since September 1 reached 2.1 million tons, approximately 122% higher than last year.

GLOBAL STATUS

USA. Weekly US soybean export inspections were reported at 1.58 million tons, according to the USDA. The top destination was again China with 1 million tons, or 63% of all US soybeans inspected for export during the week. Other relevant destinations were Germany (192,903 tons), Egypt (90,303 tons), Indonesia (76,947 tons), South Korea (48,723 tons) and Mexico (39,354 tons). Total inspections at the start of the 2022/2023 marketing year reached 41.39 million tons, up 3.6% from the 39.97 million tons recorded a year earlier.

BRAZIL. The weekly progress of the soybean harvest showed a mixed picture in all regions, according to figures published by the food agency Conab, the agricultural institute of Mato Grosso, IMEA, and the local consultancy Agrural. Brazil’s soybean crop reached a 23 percent completion rate on Feb. 18, Conab. The percentage is lower than Agrural’s estimate of 25% for February 16, but in both cases, weekly progress was led by Mato Grosso, where soybean harvesting work was 60% complete as of February 17, according to IMEA. In other regions, the soybean harvest continues to advance at a slow pace and raises concerns about potential quality issues.

Brazil’s soybean exports in February were expected to reach 8.3 million tons, 1 million tons less than the previous estimate of 9.3 million tons, grain exporters’ association Anec said.

ARGENTINA. Soybean production was adjusted by the Buenos Aires Grain Exchange to 33.5 million tons, 4.5 million tons less than the previous estimate, as a result of early frosts on the western edge of the agricultural area, lack of rainfall and of the heat recorded at the beginning of February. The severity of the damage caused by the high temperatures remains to be assessed in the coming weeks, and then the production estimate is likely to undergo a further update.

Soybean acreage rated good to excellent fell to 3% of total crops. Areas considered dry are now at 71%, and areas considered optimal and suitable are at 29%.

Argentine farmers’ sales of new crop soybeans rose to 239,000 tons in the week to 15 February. Thus, total sales of the 2022/23 crop reached 3.7 million tons, less than half of the total sales of 7.8 million tons reported at the same time last year.

CHINA. Soybean processed volumes fell to 1.82 million tons last week, according to data from the National Grains and Oil Information Center (CNGOIC), as processors ran out of soybeans, adding to relatively grains of soybean meal.

Soybean stocks at major processing plants reached 4.19 million tons on February 18.

Soybean meal stocks rose to 620,000 tons on February 17 amid weak feed consumption demand.

Soybean oil stocks were steady for the week, reported at 680,000 tons on February 21, as the pace of buying eased alongside reduced processing activity.

CBOT SOY ZS K23 MAY23 – 1,519 c/bu (-3 c/bu vs. last week)

SOY GRAPH TREND – ZSK23 MAY23

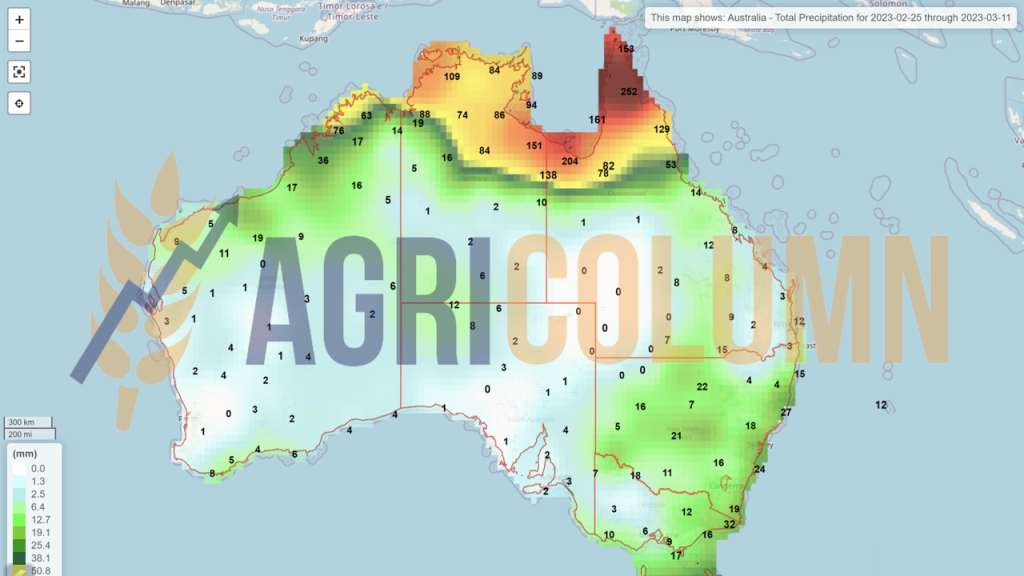

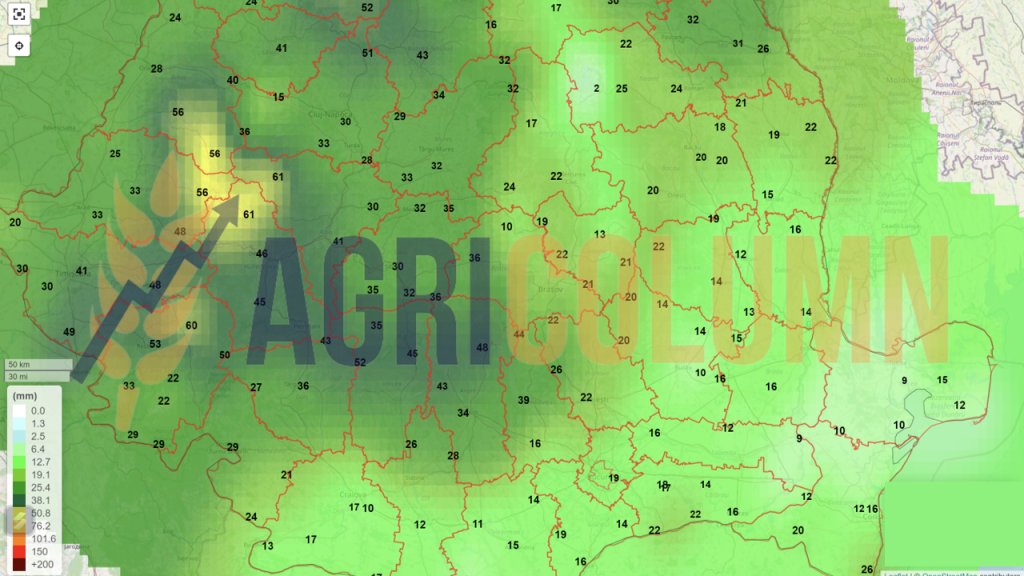

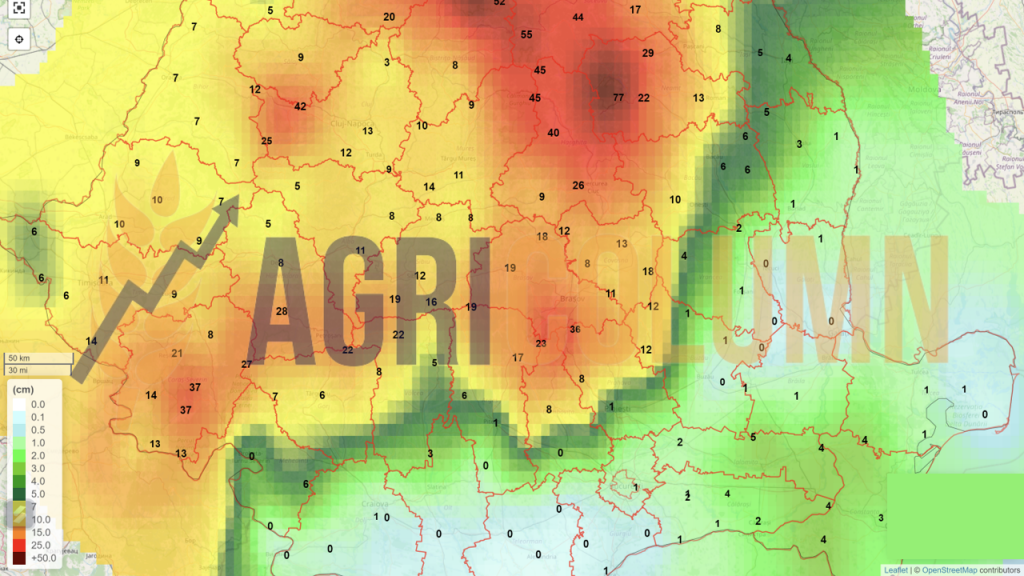

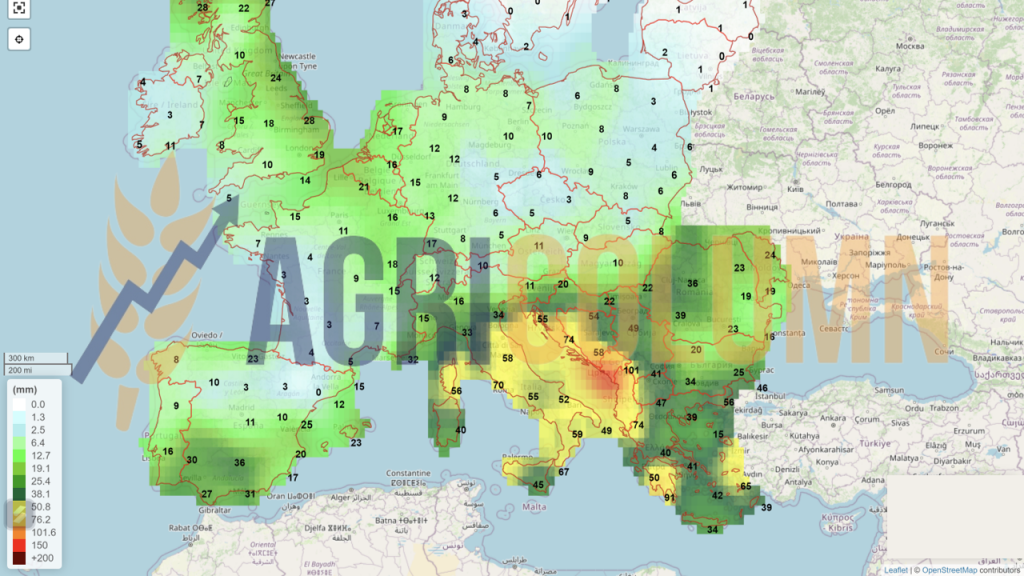

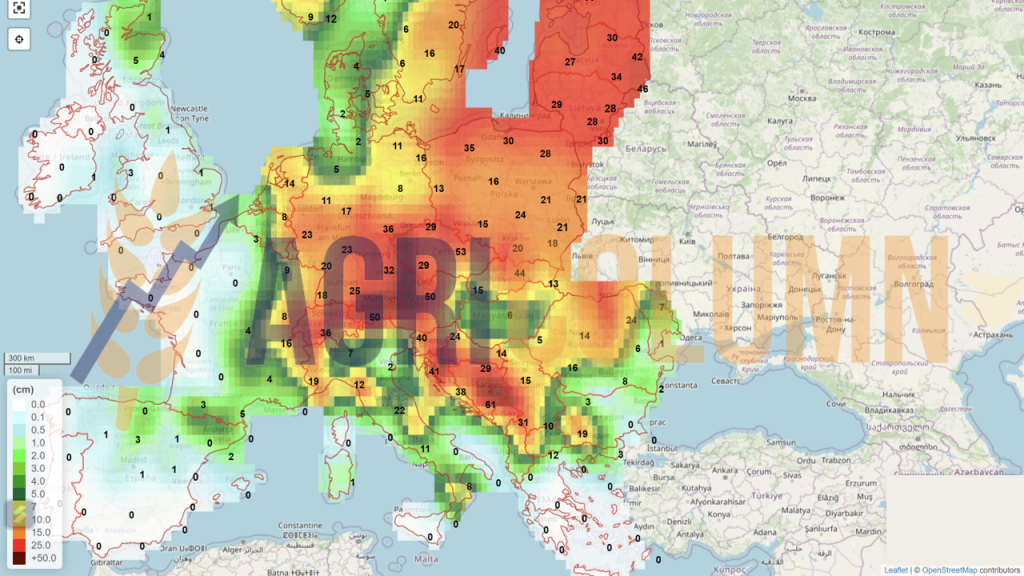

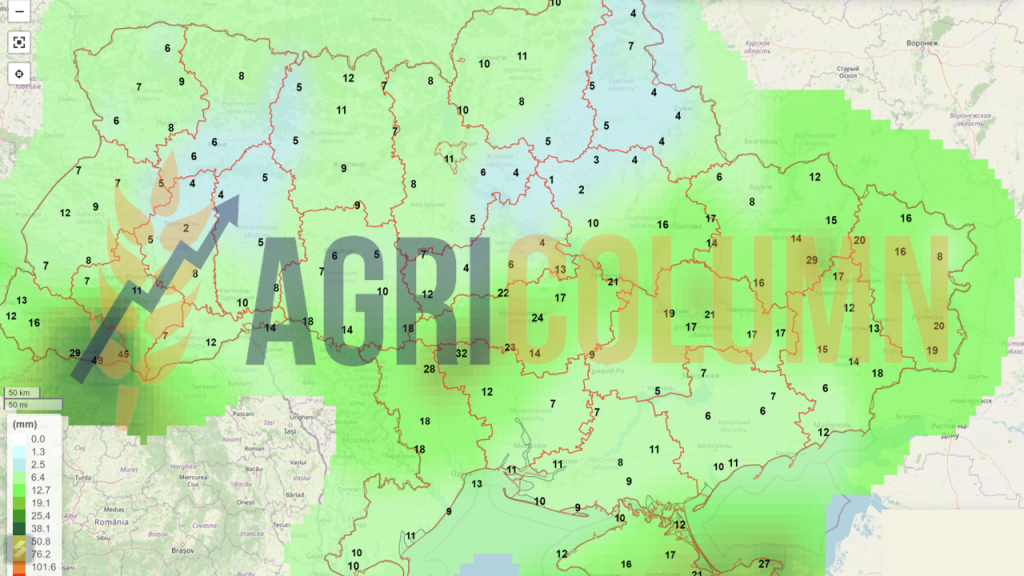

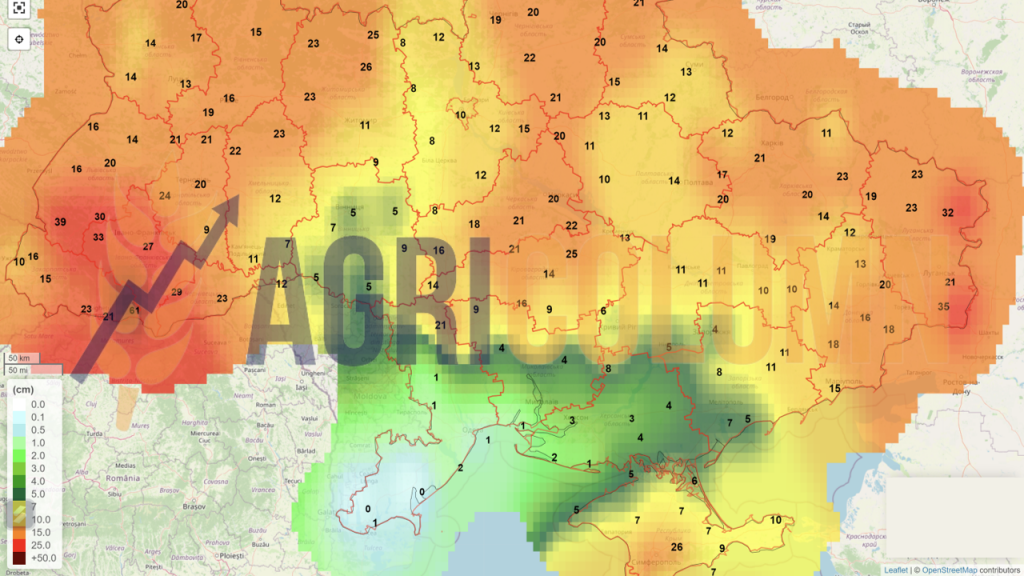

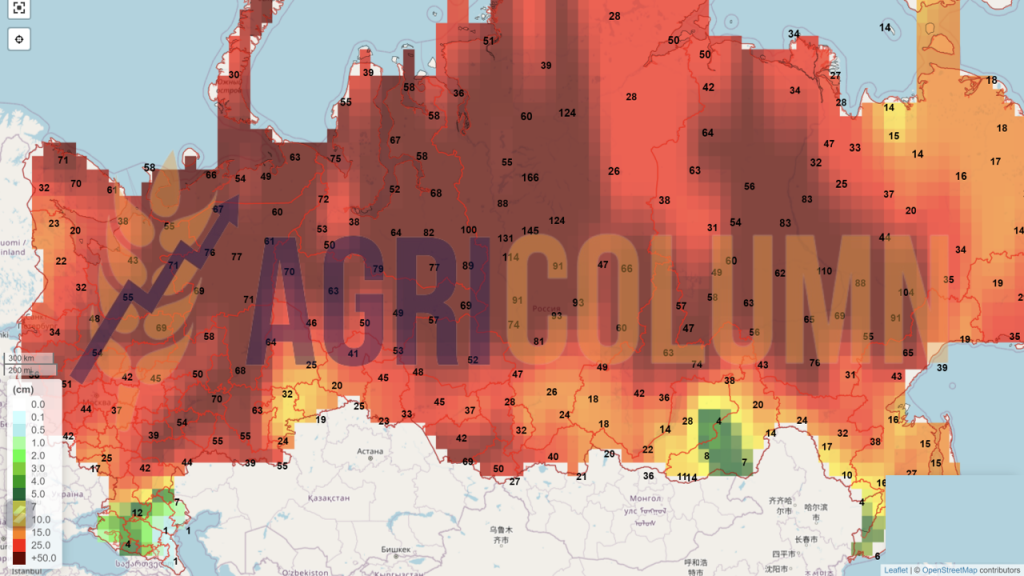

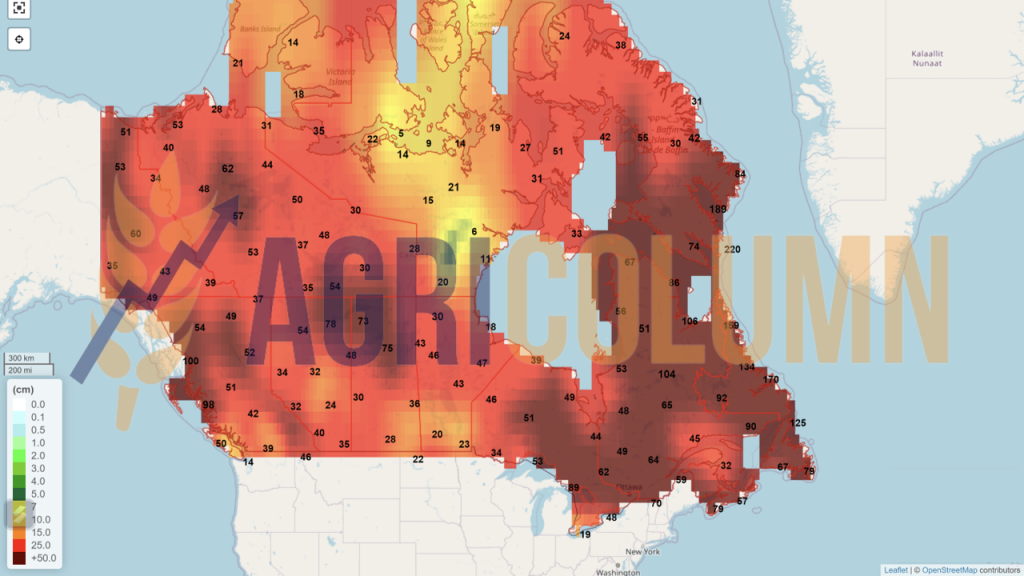

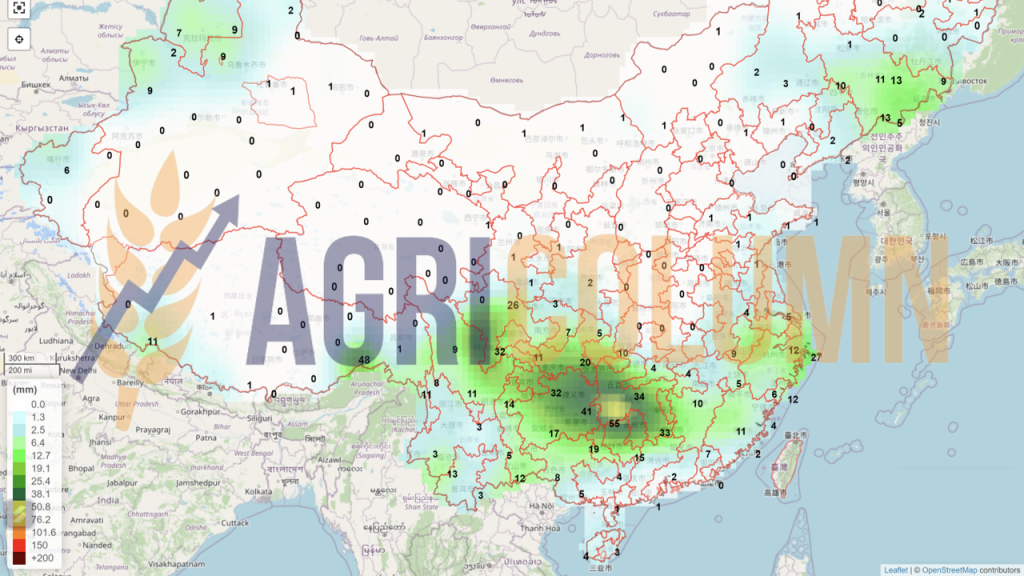

February 25 – March 11, 2023

Romania (rain)

Romania (snow)

Europe (rain)

Europe (snow)

Ukraine (rain)

Ukraine (snow)

Russia (snow)

Canada (snow)

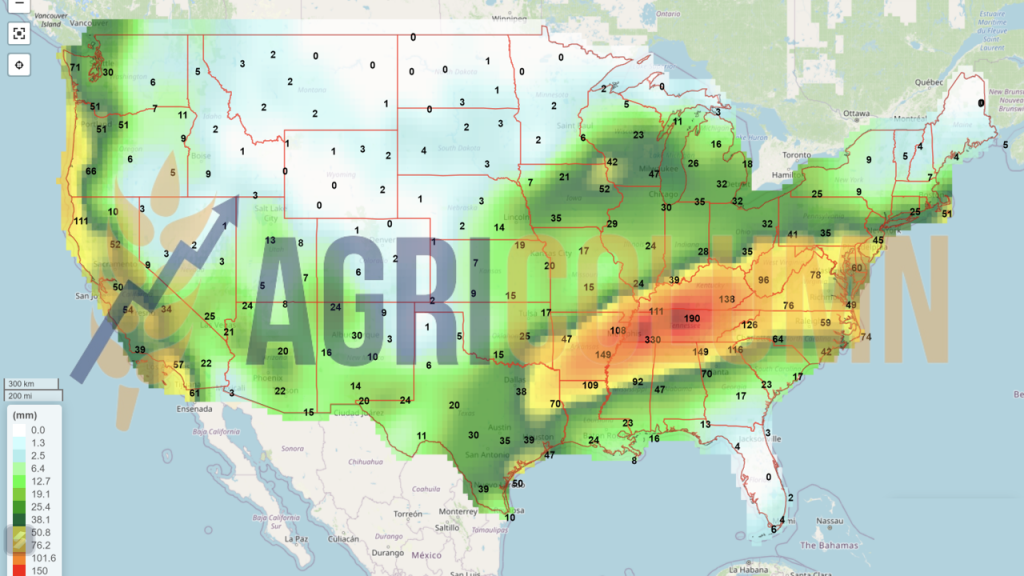

USA (rain)

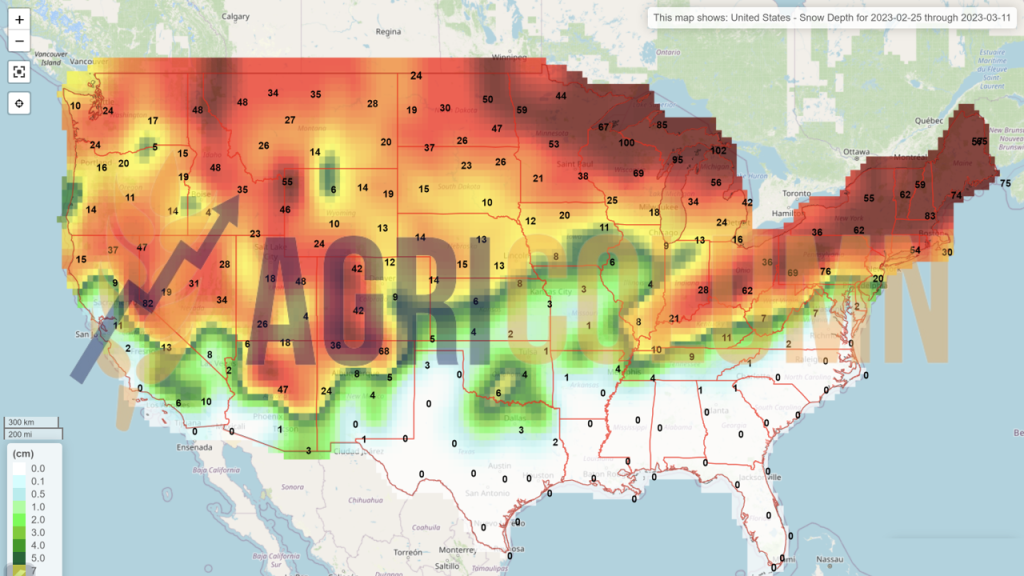

USA (snow)

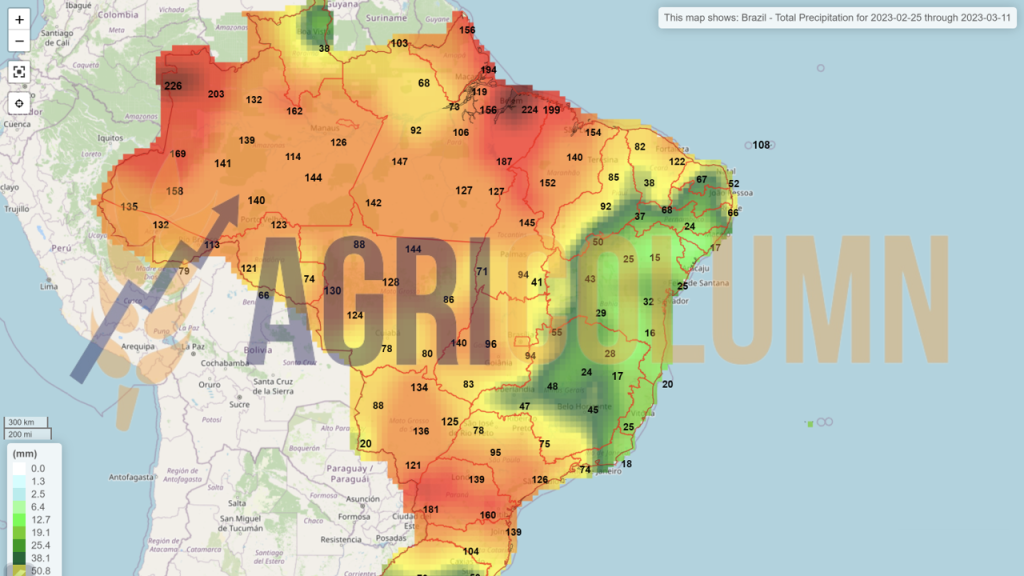

Brazil

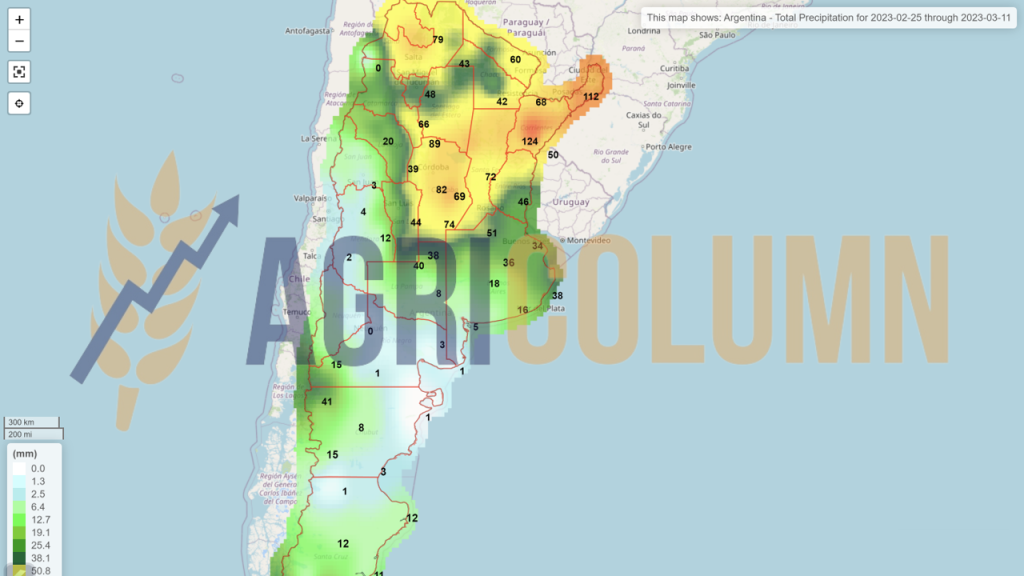

Argentina

China (rain)

Australia