This week’s market report provides information on:

LOCALLY

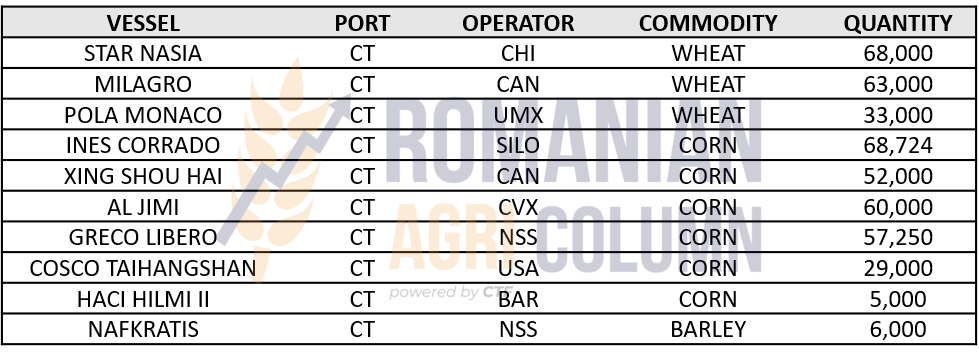

The drop in the price of wheat has begun and it continues. Wheat experienced successive shocks, despite appearances of recovery. The scenario we mentioned in the past issues takes a well-defined form and so we see wheat in the port of Constanța at a level of 257-260 EUR/MT, a decrease of about 12-15 EUR/MT compared to the beginning of the week.

Needless to say, there are a lot of unsold lots or sources that have generated inaccurate data, which have kept wheat for so long in the silos of many farmers.

Regarding the new wheat crop, we have two contradictory situations.

- The first is that things are not going well for the Romanian wheat crop at the moment. The drought is installed mostly in the region of Moldova, Bacău, Vrancea, Galați, Vaslui and partly Brăila counties. The same drought phenomenon is highlighted in the area of the southern plains, in Giurgiu, Teleorman, Călărași, as well as in areas from Bărăgan and Constanța. The only exceptions are the northwest, west, center and partly southwest of the country.

- The second is the price level offered for the new crop. The premium between SEP22 and CPT Constanța has decreased dramatically in recent days, at the same time, of course, with the contextual decrease on the entire price level of wheat. And so we see a level of 235 EUR/MT for the new wheat crop, with a negative premium of 13 EUR/MT compared to SEP22 EURONEXT. This is an indicator of reflection, which urges us to be careful.

In other words, buyers are also aware of the drought phenomenon and the level of the Premium was contracted in the desire to reward the forward sale.

235 EUR/MT is not a small and negligible level for the new crop, but we recommend a lot of caution in estimating the level to be sold forward. In the first scene, the field must be evaluated very well, in order to appreciate the state of vegetation with which the wheat will go on the road, the following weeks being critical for its development. Afterwards it should be sold, 1-1.5 tons maximum at this time. The drought may persist and the water level in the soil at this time in these areas does not indicate future health, unless March will generate excessive rainfall.

REGIONALLY

Although indications of a new crop appear to be more generous for European wheat, a wave of unrest is spreading. This is due to the appearance of an insufficient supply and use of nitrogen at European level, generated by high prices and the announcement by Russia that it will stop any supply of ammonium nitrate for a period of two months. The first option for working in this scenario is clearly a lower level of wheat volume at EU level. And in this case, we estimate for the beginning a lower level by about 2 million tons. But things may not stay that way, and in a few months, we may see a further decline in the potential of soft wheat. At the moment, the estimate calculated with a decrease of 2 million tons is 127.5 million tons, compared to 129.7 in 2021-2022.

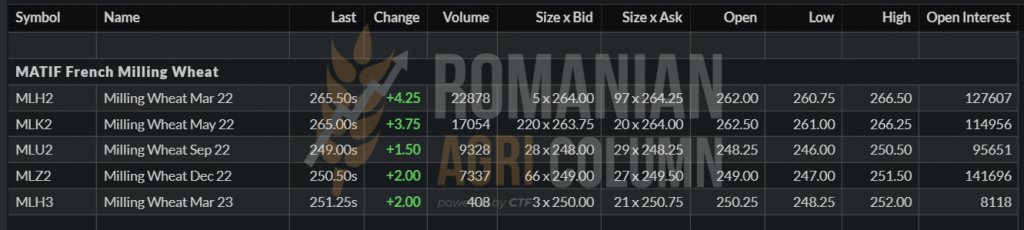

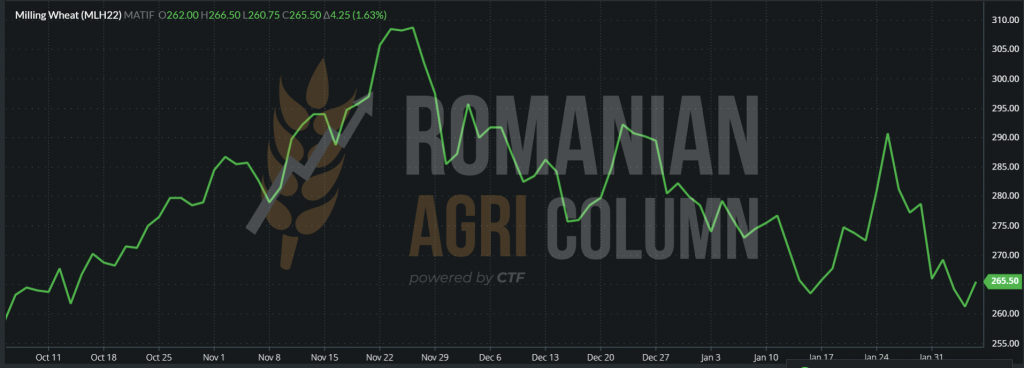

Returning to the 2021 crop, the EURONEXT indications have come to life and we see a return of 4.25 EUR/MT at the end of the trading session on February 4, 2022. Today, February 7, 2022, we could see a return to the level immediately below 270 EUR.

EURONEXT MLH22 MAR22 | 265.5 EUR (+4.25 EUR)

EURONEXT MLH22 MAR22 TREND GRAPHIC | We have returned to the level of October 2021.

Russia recently announced a deal with China for wheat sales. We welcome this agreement. If you can’t go west, go east.

Preliminary estimates are at 1 million tons. We also note the attempts to manipulate the market by estimates taken from the main news streams, as if the conflict starts, the price of wheat increases by 20-30%. None of these attempts mattered. Wheat is in large volume in the basin, Russia still has to export about 10-11 million tons, Ukraine about 7-8 million tons, Romania about 3 million tons, so that the destinations are relaxed and have entered the hand to mouth behavior mode.

The first signal of abundance was given by the last GASC tender, which aligned no less than 24 bids for both delivery periods. This means abundance, and these days, buyers are missing from the Black Sea basin. Any offer is bid at a level 10 USD/MT below what is asked (ASK vs. BID).

GLOBALLY

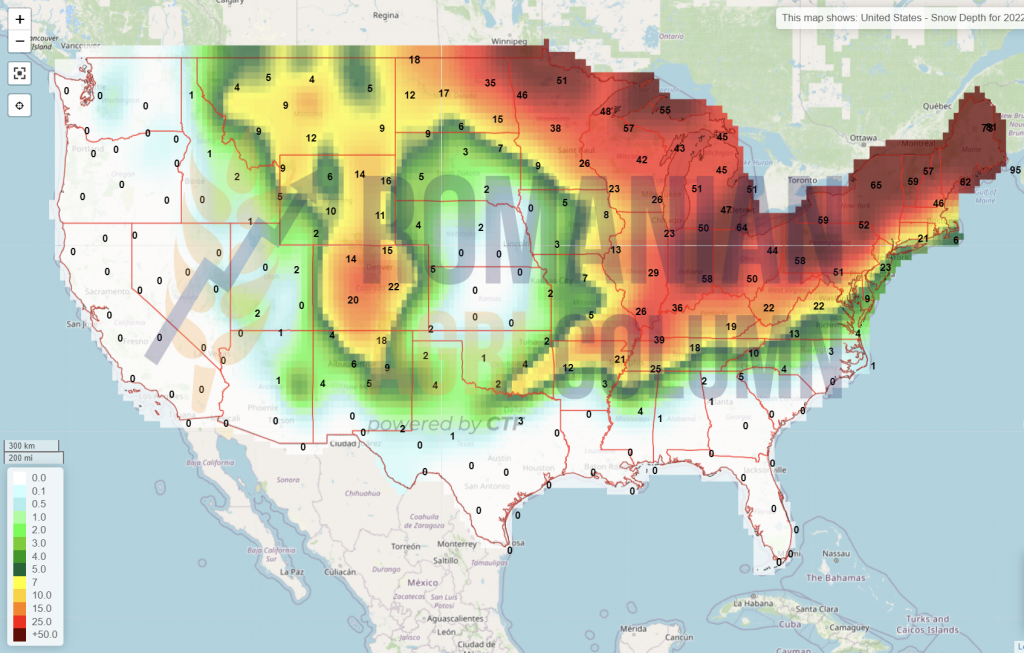

In the US, in the Central Plains, there are very large areas that are not covered in snow at this time, and the question marks that have been raised since December 2021, following extremely hot dust storms, remain current, especially as temperatures are forecast. lower than normal for this period, up to 5 degrees. The main problem remains the difference between day and night, which, in the case of uncovered areas in the Central Plains, can create problems in the short term. The estimate of uncovered areas in the Central Plains is at the level of 45%.

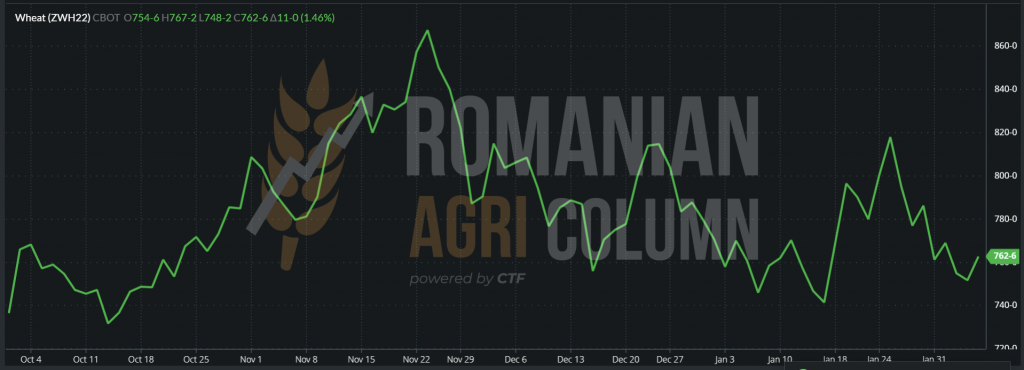

Let’s see how the trading session of February 4-5, 2022 goes, which enhances an increase of 11 c/bu so far, i.e., 4 USD.

CBOT ZWH22 MAR22: 763 c/bu (+11 c/bu = +4 USD)

CBOT ZWH22 MAR22 TREND GRAPH

CBOT is the preferred place for investment funds. And we have two very important landmarks in the next period of time. The first is the WASDE report generated by the USDA, which will be released on February 9, 2022. The second benchmark that will mark the stock market indications will begin on February 18, 2022. This is when the MAR22 contracts start to expire and we will certainly see a much higher rate of exit or roll-over rollovers. The USDA will generate a neutral wheat ratio. No changes will be seen, as wheat is no longer harvested anywhere in the world. The adjustments will be to Trade and Consumption, so we expect discounts on both indicators. The stocks could also generate a balance, but nothing is expected yet. With the reduction of Global Trade and Consumption, wheat will have a bearish trend.

FAO-AMIS releases February report and we have a WASDE preview:

Wheat production in 2021 is growing as a result of this month’s upward revision, which is mainly due to higher production in Argentina and Australia.

Use in 2021/22 has decreased, due to a slower anticipated increase in feed use.

Stocks (as of 2022) have risen following revisions, especially in the Russian Federation and the US, due to lower exports.

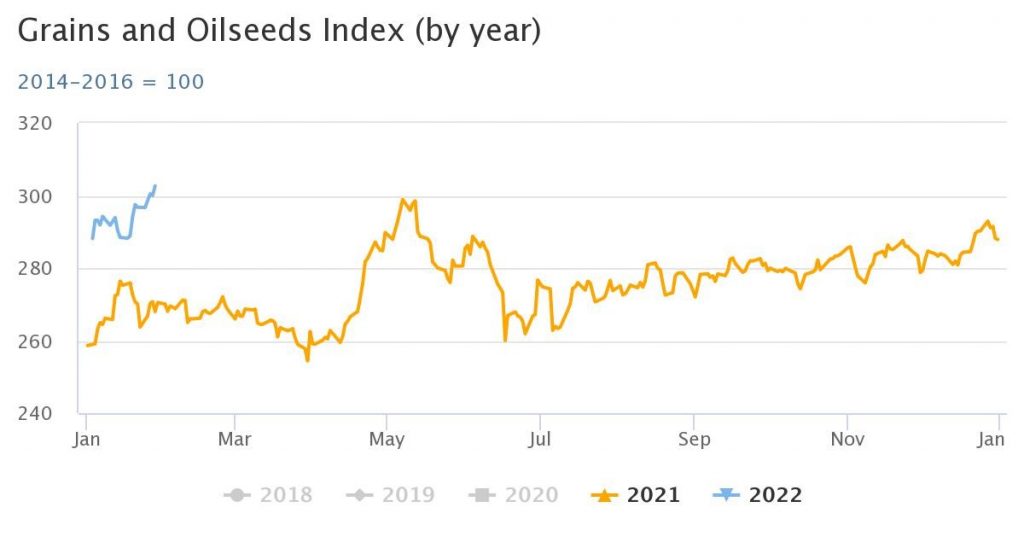

We also include the analysis of the FAO Price Index for Cereals and Oilseeds. We compare with last year the yellow line. Source: AMIS-FAO.

PRICE INDICATIONS IN VARIOUS ORIGINS

ANALYSIS

- Wheat is in a clear decline from the volumes in the Black Sea basin.

- Black Sea Wheat (BSW) indicates a lower level for March compared to February (314 USD vs. 321 USD).

- WASDE will generate a report that will lead to neutrality, at best.

LOCALLY

Barley returns and indicates a price level that does not seem to be real – 250 EUR/MT in the CPT Constanța parity. We say this because the difference between it and milling wheat is only 8-10 EUR/MT. The need for coverage for contracts already concluded creates these working premises in the same low-liquidity market.

The new barley crop is quoted at 215 EUR/MT, remaining constant over the period since the last report.

REGIONALLY & GLOBALLY

Russia indicates a price level of 300 USD/MT in FOB parity, increasing by 3 USD compared to last week, with the same difference from wheat, of 10 EUR. Australia remains stable at the same indicative level of 264 USD/MT.

Russia has indicated lifting restrictions on the supply of barley to China, so a new destination has reappeared on the map for Russia.

LOCALLY

The indications of corn in the local market fell by about 5-7 EUR/MT, the port of Constanța indicating a level of 245 EUR/MT in the CPT parity. As we said in previous issues, corn is in the midst of a life cycle of price progress and the health of its quotations is generated by South American problems. In the parity of CVB (Constanța-Varna-Burgas), the price decreased by about 1.5 EUR/MT, to the level of 251.5 EUR/MT. Thus, the price offered for goods in CPT parity is equivalent to reality, and there is demand.

REGIONALLY

The easing, at least for a while, of the tense situation between Russia and Ukraine generates trade and supply. Thus, we can see the price of corn falling due to a window of time generated by the lack of bad political news. In Ukrainian ports, the price of corn has deteriorated in recent days, due to rising volumes, but not at a very high level, but about 1-1.5 USD/MT.

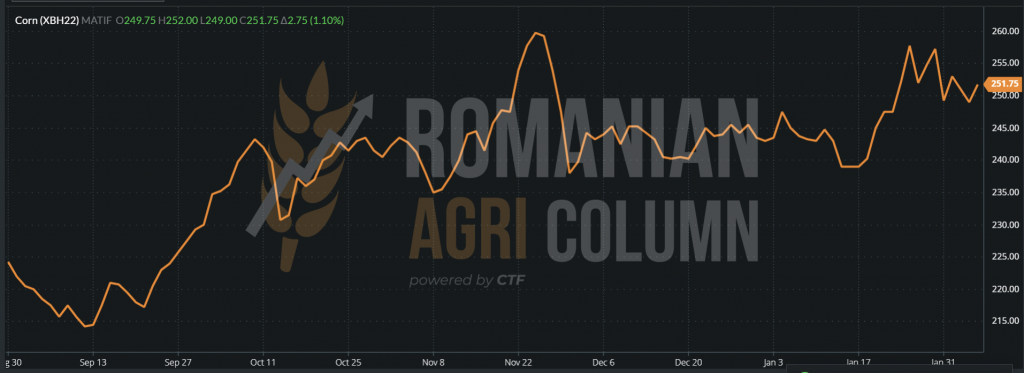

On EURONEXT maize has fluctuated, as in the case of wheat, due to investment fund transactions, but not on a large scale.

EUROENXT XBH22 MAR22: 251.75 EUR at the close of 4 February 2022

EURONEXT XBH22 MAR22 TREND GRAPH

What should be observed in the graph is the level where it started and the peak reached in the NOV21 period. This graph also shows that there is a clear correlation between corn and wheat, and any future decline in wheat could also lead to corn on a downward slope. The difference between them today is about 15 EUR/MT, and it should normally be at a level of 25 EUR. The 2020-2021 season was a whole other story, because the pedological drought affected the reservoir of origin in the Black Sea basin and thus we had the unprecedented situation of having a corn more expensive than wheat. But this year, we have a rich crop. Ukraine, with the 40 million tons, fully supplies, as well as Romania, Bulgaria, Serbia and Hungary, in turn.

Regarding the EU’s 2022 crop, it is forecast to be up to 3 million tons lower, from an estimated 68.7 million tons to 66 million tons. Surely this is due to the price of fertilizers, which will lead to a lower yield of production. But the weather can also be detrimental to the new corn crop. The drought in Romania, southern France and Spain are unfavorable signs from now on.

GLOBALLY

American volumes are penalized by competition between origins, an aspect that we have been estimating for some time. Specifically, a sale of 380,000 tons of corn from the 2021 crop was canceled, which indicates the wish for a cheaper commodity. And where is corn cheaper than in the Black Sea basin?

At the same time, China announces a volume of 28.3 million tons as an import level for 2021, exceeding the initial forecast of 26 million tons. It is a sign of a supply need that will continue steadily in the next period, with the price of corn returning, as we estimate, to trading levels which indicate it as the main element in feed, to the detriment of feed wheat, which China wanted to use as a substitute. Corn protein cannot be effectively replaced by feed wheat, and we remind you of the question we raised since November last year: Not if, but when will China return to corn? The question has an answer today.

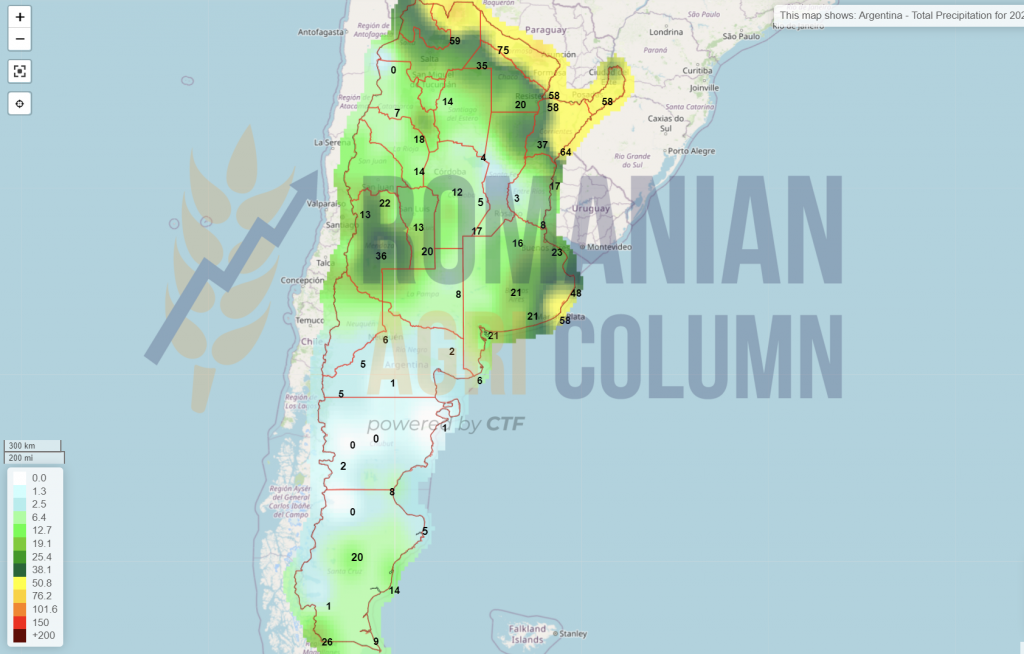

South America is experiencing heavy rainfall, especially in, with an estimated rainfall of between 190-240 liters per square meter, until February 18, 2022. The beneficiary of the rains will be Safrinha, the second corn crop, but at the same time, the estimates near the arrival of the report are negative for both countries. Argentina has recently entered the carousel of production cuts, but it was obvious against the background of the drought and the heat wave it faced during January 2022.

The prerequisites for a bullish report for maize are in place, but we look forward to seeing how consumption and stocks will, in turn, affect the global balance.

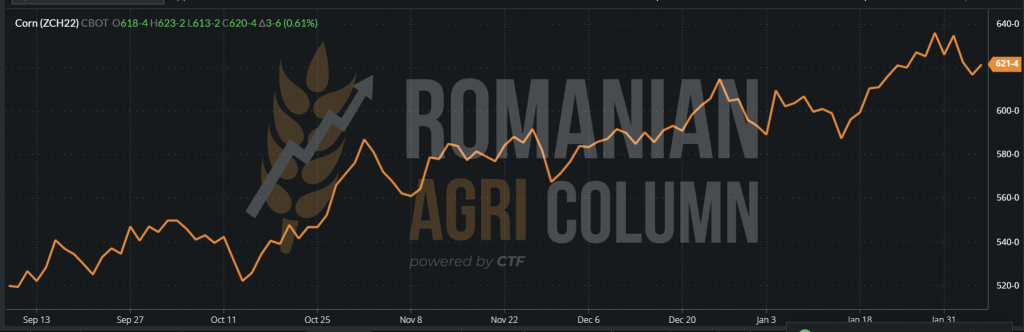

CBOT closed the trading session from February 4-5, 2022 at 620 c/bu, a decrease compared to the level of February 1, 2022, when the indications were at the level of 636 c/bu.

CBOT ZCH22 MAR22 TREND GRAPHIC

Also, this chart shows the progress of the corn price, and what we have seen in terms of increases and decreases in the last week are only shares of investment funds, which enter and exit technical positions. As in the case of wheat, we see on the horizon the date of February 9, when the USDA report will be published, as well as the date of February 18, the time when the stock market positions that refer to MAR22 ZCH22 will be liquidated or will move (roll-over).

FAO-AMIS REPORT – February 4, 2022

Corn production in 2021 has remained virtually unchanged and is still estimated at a record high, up 3.7% from last season, supported by higher crops in Argentina, China, the EU, Ukraine and the United States.

Use in 2021/22 decreased, but continued to increase by 2.5% compared to 2020/21, mainly due to higher use in Brazil, Canada, China and the USA.

The trade forecast for 2021/22 (July/June) has been slightly revised downwards due to weaker-than-expected demand from China and Turkey.

Stocks continued to rise and are expected to rise above initial levels by 2.7%, with most of the growth concentrated in China and the United States.

PRICE INDICATIONS IN VARIOUS ORIGINS

ANALYSIS

- Corn remains on traction due to global demand.

- Origins are beginning to compete with each other (e.g., the US with the cancellation of the maize batch).

- South America, despite the cuts, remains a fierce competitor to the United States and the Black Sea basin. Proof is the price level in FOB Argentina.

- Degradation in partnership with wheat could come after February 15-20, 2022, when Ukrainian logistics operations will be able to resume in force. As a small detail, again on Tuesday, Odessa and Chornomorsk were closed due to snowstorms.

LOCALLY

The indications for rapeseed for the old crop are at the level of 690 EUR/MT FOB CVB. The interest of the exporters no longer exists, the quotations are no longer displayed for the old rapeseed crop.

The new rapeseed crop is quoted under the indication AUG22 minus 10 or minus 5 EUR, DAP Processor or DAP Constanța. The status of the rapeseed crop as a state of vegetation is unchanged from last week. There is concern about the level of water supply in the soil and the obvious lack of rainfall, which can be seen in February 2022.

Also, the temperatures forecast to be rising are worrying. A positive 15 degrees during the day could trigger the rapeseed to emerge from hibernation and enter vegetation. This could cause significant damage if we experience negative temperatures of minus 8-10 degrees in the next period. Winter has not come to an end and unforeseen events could occur.

REGIONALLY & GLOBALLY

EURONEXT quotes are naturally connected with the cost of fossil energy and the threshold of 93 USD/barrel displayed in Brent oil provides a level of rapeseed support around 615-618 EUR/MT in the indication AUG22. The scenarios we see in the next period are closely related to oil prices and weather. These are the two closely linked volatility factors that can influence the price of rapeseed and the inverse crop.

Depending on the two factors, the price may increase, the premium may decrease and the inverse crop may be maintained or decrease, in turn, as we move into April. Then Canada will start sowing the new canola crop and things will take on a new dimension and other factors to follow.

For now, it is premature to generate directions. We maintain the status of observers, with the clear mention that rapeseed has support and we do not see at this moment any reason for obvious price degradation.

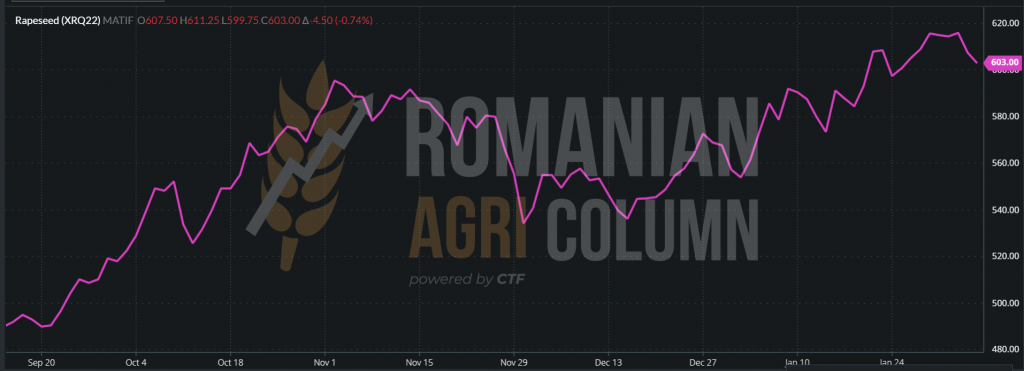

EURONEXT XRQ22 AUG22 at the closing date of 4 February 2022 | 603 EUR

EURONEXT XRQ22 AUG22 TREND GRAPH

ANALYSIS

- Rapeseed remains supported by the price of fossil energy.

- Commuting of 10-13 EUR is already a habit and we can see them in the chart.

- Although the harvest is far away, the weather will be the main factor that will play an important role in the 2022 season.

LOCALLY

Locally, sunflower seed quotations have gained traction. The price level offered under the FCA has reached 675, even 680 USD/MT for larger batches. The batches are starting to be traded and this is a beneficial one for the Romanian processors which thus show their competitiveness in relation to the intra-community and export trade market. In the port of Constanța, the levels indicated for larger batches have reached the level of 690 USD/MT and it is natural, if we look at the logistical difference between the processing units and the port of Constanța.

The level of domestic stocks is enough for processors at the moment, but movements in the demand for coverage from European destinations indicate the same pace in the European Union. Demand dynamics are also present for non-EU destinations, a sign of market thaw, driven by factors in the VEGOIL complex.

REGIONALLY

Across the border, in Hungary, the indications of the processors located in the immediate vicinity of Romania are at the level of 705-708 USD/MT. However, they work with the oil content parameter and this is beneficial for both parties, if the seller knows this indicator of the goods offered for sale. The additional bonus ratio is 1:1.5 or 1:2, which means that a commodity with an oil content higher than 44% receives in addition those percentages expressed above at a divisible level.

Regarding high oleic seeds, the interest is quite high on the Romanian market, but the bonus level is not as high as in Hungary (bonus of 54 USD/MT in Hungary, compared to 20 USD/MT maximum in Romania).

Our neighbors in Hungary also indicate levels for the new sunflower seed crop and they are currently priced at 590 USD/MT, with a High Oleic seed bonus of 45 USD/MT.

Ukrainian oil market has experienced a momentum in the same positive direction. The ASK has reached the level of 1,430 USD/MT, while the BID is reflected at the level of 1,390 USD/MT. These two levels fluctuate daily by 5-10 USD/MT, depending on the demand displayed by buyers.

Russia raises the level of crude oil export tax from March 1, 2022 to 260.1 USD/MT, increasing by 10 USD/MT. This indicator shows the interest of buyers in sunflower oil.

Let’s take a look at the future and, based on Platts estimates, look at the indications for sunflower oil (CSFO) in the Black Sea basin. What we must keep in mind is the price that remains constant throughout the spring and summer until the new crop, where it suffers a degradation of 55 USD/MT. But this inverse crop is logical and normal for crop exchange.

Of course, these are just estimates, but they should be seen as a market demand, which maintains the price level of CSFO in the year we are going through. In other words, the price of seeds will remain high in 2022. Price changes will be made at the crop exchange.

GLOBALLY

In the VEGOIL complex, palm oil is an indicator that raises the price level during this time period. The two largest palm oil-producing countries, Malaysia and Indonesia, indicate production difficulties. Thus, Indonesia restricted 20% of the export level to secure the needs of the internal market. Let’s not forget that it has a population of 270 million inhabitants. Indonesian palm oil stocks at the end of 2021 were 51% lower than last year.

Malaysia indicates a 25% increase in stocks compared to last year, but has a negative indication of stocks of minus 21% as a 2-year average and minus 51% compared to the average of the last 3 years. Production in the last calendar year was the lowest from 2007 to date, with a decrease in production of 5% compared to last year and minus 44% compared to 2 years ago.

The cumulative exports of palm oil of the two countries represent 55% of the major global trade in vegetable oil, which is an important indicator of the VEGOIL complex.

On the morning of February 3, 2022, the MDEX indicated a positive opening at 1,362 USD/MT.

Soy, in turn, supports the VEGOIL complex through the extremely high indications of beans and, implicitly, of soybean oil. But we will talk about this in the chapter on soybeans.

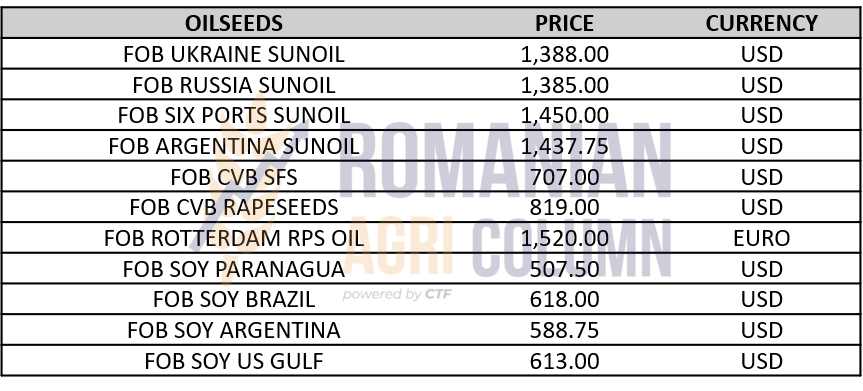

OILSEEDS PRICE INDICATIONS IN VARIOUS ORIGINS

ANALYSIS

- Sunflower oil has strong support from colleagues, palm oil and soybean oil.

- Sunflower seeds benefit from price increases and it is a sufficiently motivating time for stockholders to trade the lots kept from the time of harvest. In other words, the rally started a few days ago and its duration depends on the supply of destinations. March is one in which, towards its end, the indications could degrade, having the same conditions as today. But the market has taught us that it is volatile and new perspectives can emerge at any time.

- From 620 to 690 USD/MT is a potential that was worth the wait, now it only needs to be harvested and incorporated for the benefit of the farms.

- Argentina is at a 23% harvest level. Production is estimated at 3.4 million tons, according to BAGE, and the USDA indicates 3.15 million tons. As the harvest continues, we will see what the end result will be.

LOCALLY

In Romania, soybeans are offered at the level of 660-670 USD/MT FCA Farms. Quantities still exist, but seeing the increases on the CBOT, farmers tend to wait a few more days, trying to take advantage of this favorable context.

GLOBALLY

Ongoing problems in South America are generating substantial increases in the US stock market and in the demand for soybeans for export.

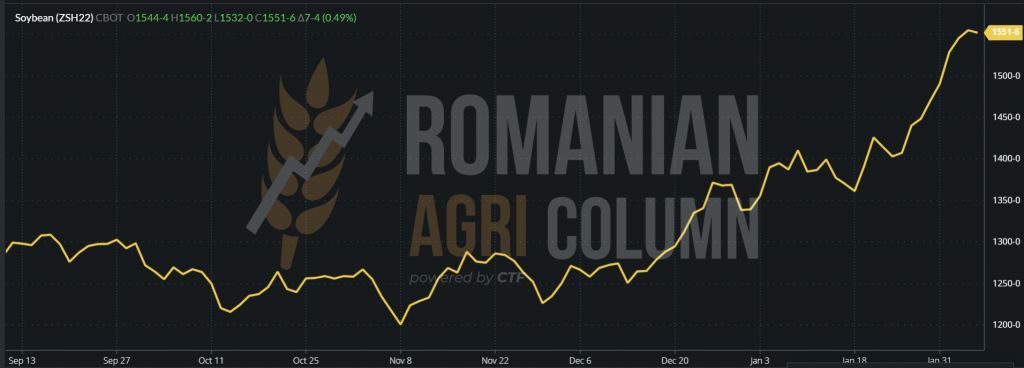

The investment funds have noticed this moment and are actually piled on this commodity on CBOT through net long positions. Our opinion is that the interest is one that exceeds the condition of the goods in the physical market and we could see a dramatic decrease around February 20, 2022, with the expiration of the ZSH22 MAR22 indication. Already in the morning of February 3 we see a correction in the night session of 8 c/bu, which shows us the fragility compared to the status in the physical market. Soybean indications for March are at a record high. This increase is directly comparable to the 2008 level.

On the ground, things remain the same, with Brazil at over 15% and the same estimated loss of 8-9 million tons. As the harvest progresses, the reality will be seen. Part of the loss may or may not be recovered. Argentina is currently downgraded by about 2 million tons. However, what is seen in the physical market is the orientation of buyers for American soybeans, against the background of the slow pace of harvesting in Brazil, the rains that delay the harvest and the harvest levels below the initial anticipation. The competition between origins is obvious in this case as well.

Analyzing agencies indicate different levels, as follows:

- STONE X – 126.5 compared to 134 million tons

- AgRural -128.5 compared to 133.4 million tons

- Datagro -130 front 142 million tons

- COGO – 125 compared to 131 million tons

By averaging, we reach a level of decline around the value we estimate.

CBOT ZSH22 | CURRENT INDICATION = 550c/bu (+ 6c/bu)

CBOT ZSH22 MAR22 TREND GRAPH

FAO-AMIS – Report 4 February 2022

Soybean production fell in 2021/22, mainly due to lower forecasts for Brazil, Argentina and Paraguay due to adverse weather conditions.

Use in 2021/22 has declined due to lower processing in China and several South American countries.

Trade in 2021/22 (Oct./Sept.) was revised downwards, based on lower import forecasts for China and other Asian countries, while export forecasts were lowered mainly for Brazil.

Stocks (execution 2021/22) have fallen significantly, compared to lower forecasts for Brazil, Argentina and China, now indicating a contraction in global stocks to levels well below average.

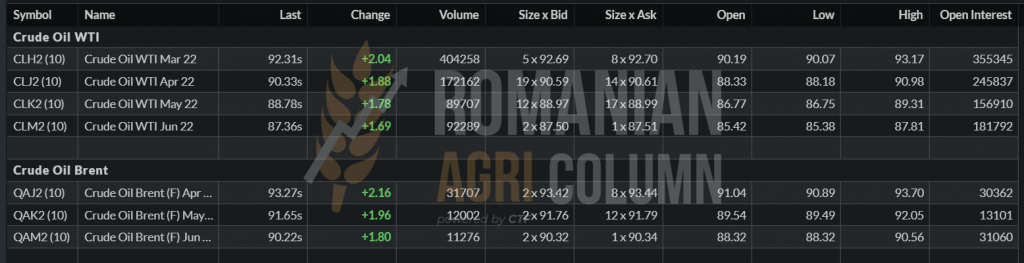

The US dollar weakened against the euro: 1.1448 vs 1.125

Increase in BRENT 93.27 USD | WTI 92.31 USD

5-18 February 2022

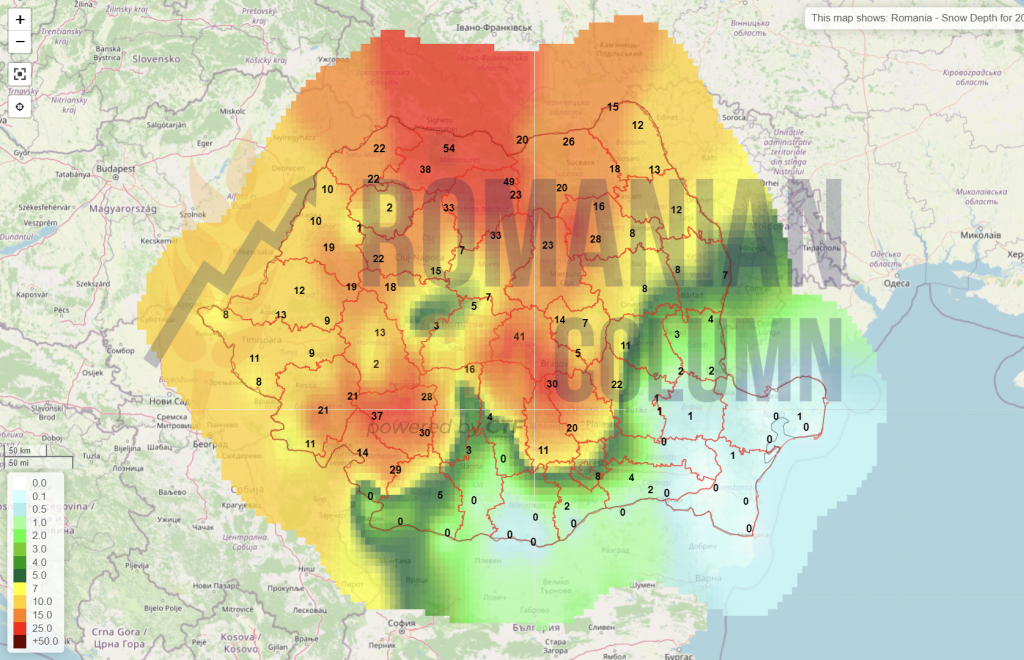

Romania (snow)

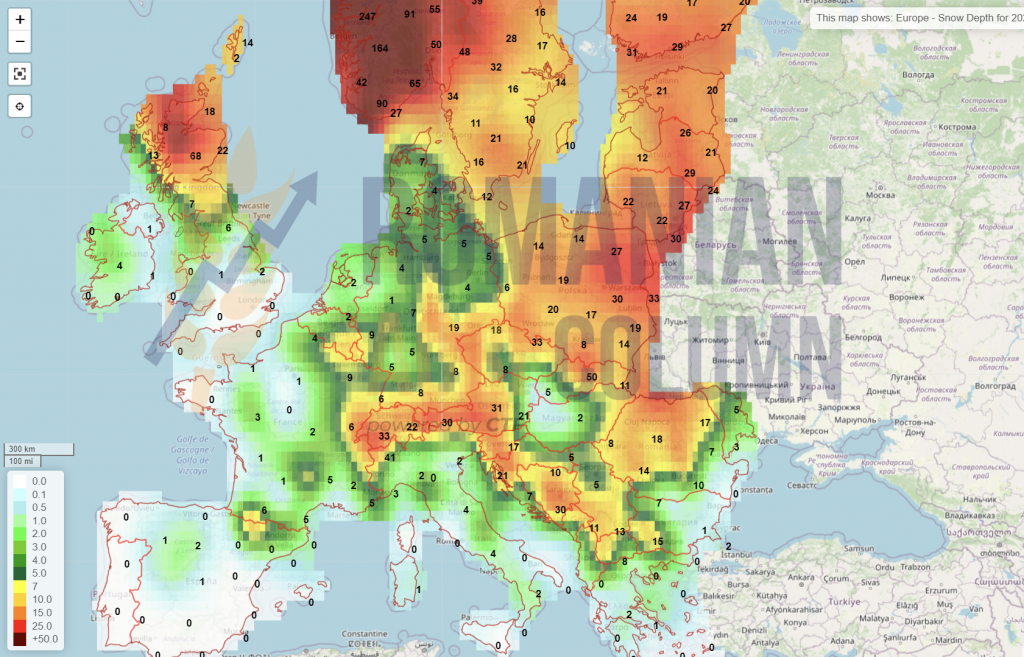

Europe (snow)

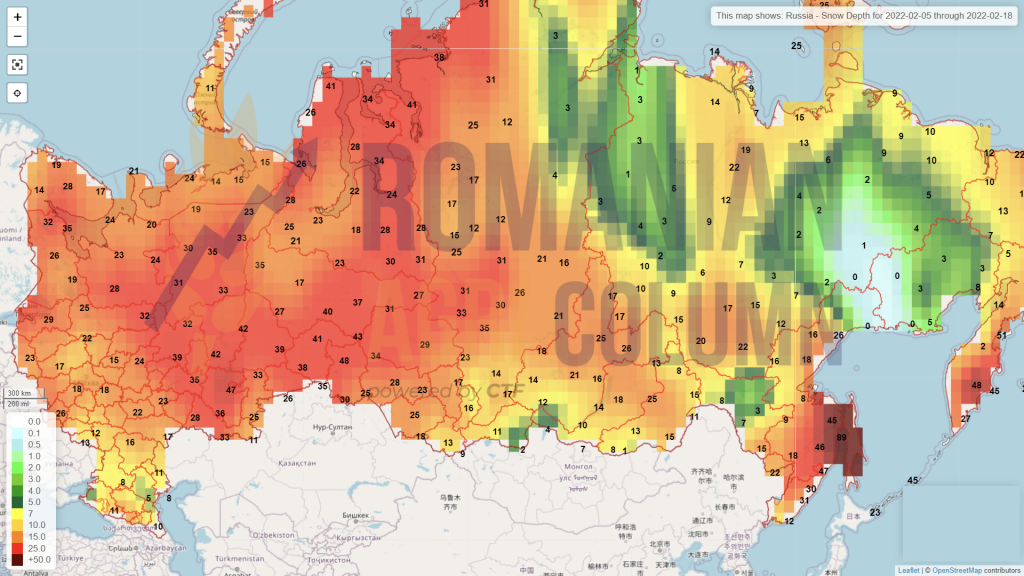

Russia (snow)

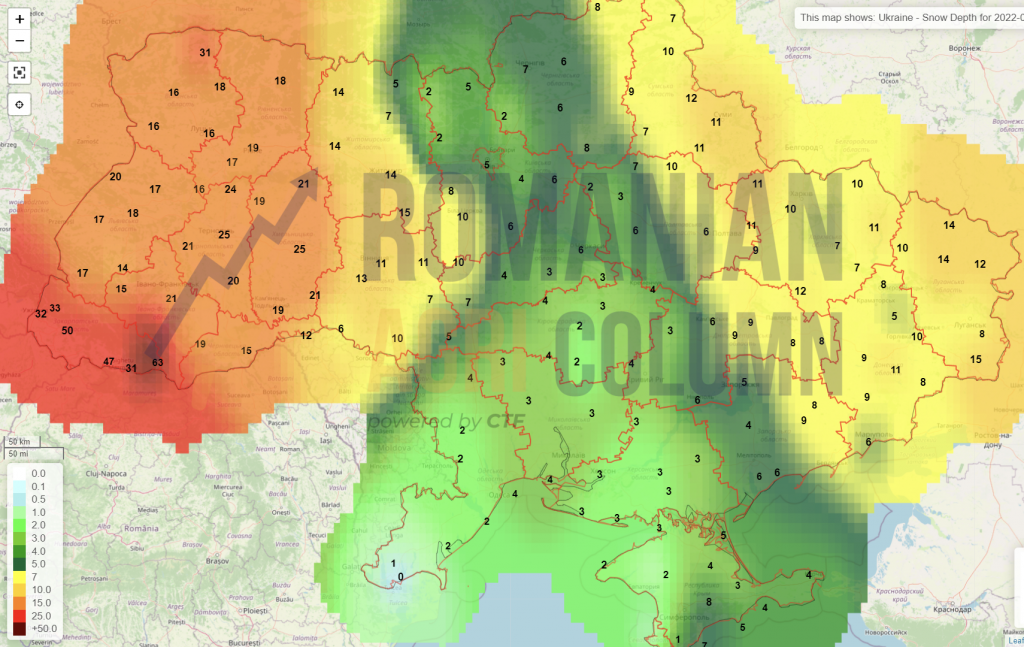

Ukraine (snow)

USA (snow)

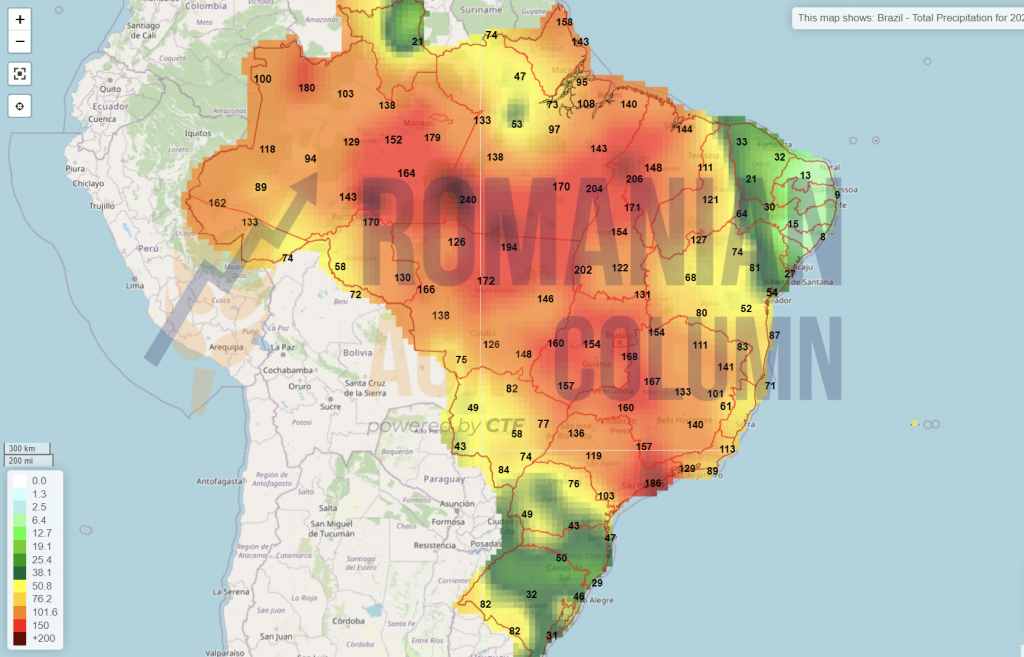

Brazil (rains)

Argentina (rains)

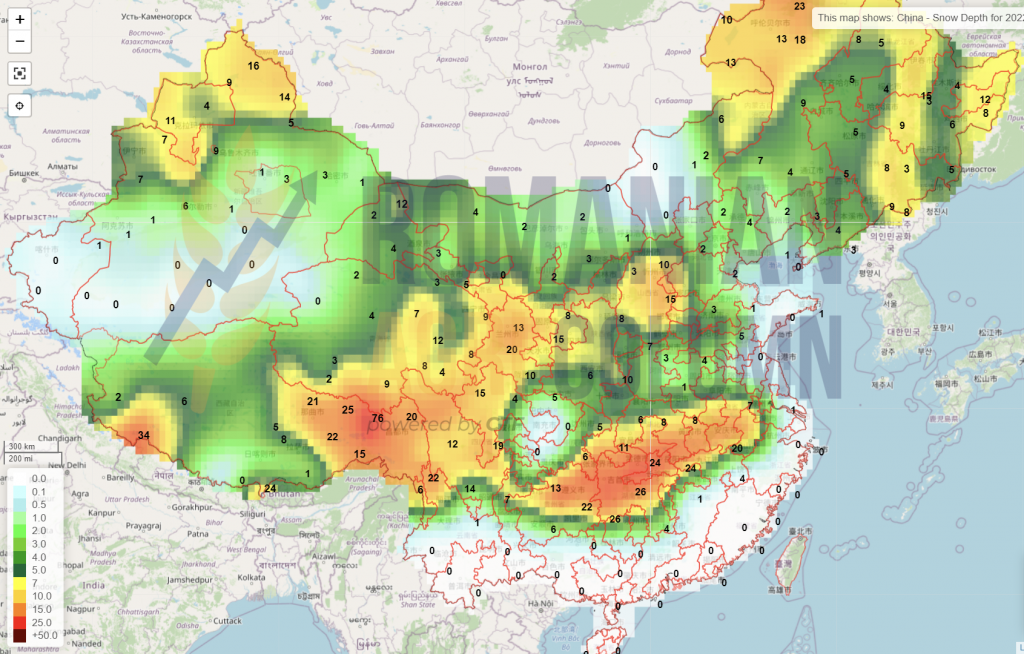

China (snow)