This week’s market report contains information on:

LOCAL

Wheat prices in the CPT Constanța parity have dropped dramatically since the publication of the WASDE report. This reflects the availability of the offer in terms of volumes. We noted during December 2021 about the existing volumes in Romania and about the growing expectations of farmers to sell. The feeling that the price was rising was fueled by a long period of time in which wheat was supported by demand.

Throughout this period, we have advised and urged farmers to sell the goods, at least during December. There was no reason to keep waiting. But the desire to see an even higher price meant that the things we repeatedly set out were ignored. It is a tribute paid by those who did not want to sell, based on instinct, not correct and accurate information.

The reflection of the port of Constanța in prices is at the level of 260-263 EUR/MT in the CPT parity, with a discount of 10 EUR for the feed quality, which shows us a decrease of at least 15-20 EUR/MT compared to the days before the report and the days before the December holidays.

So we have a status on the local market that we have been anticipating for 45 days. Many farmers have fiscally motivated the desire to sell, move taxation to 2022 or lack of need for cash flow. These are two extremely wrong reasons that should not be found in the management of a farm’s sales.

The sale is made on the basis of a break-even estimate and on the basis of the correct information which enables the farm to obtain the moments of high percentage potential, so as to reap the so-called price spikes. The motivations for moving in the next year from a fiscal point of view, as well as the motivation related to the lack of cash flow needs are extremely toxic in the management of farm sales.

Panic selling is also an element that only amplifies the loss of potential. In such moments, calm and proper evaluation must prevail. The right information must be analyzed for a good sales decision.

As a benchmark, we can tell you that these days, the price indications in the Black Sea basin, Constanța port, are at the level of 317.5 USD/MT FOB. Converted to EUR, due to a sharp weakening of the US dollar to a ratio of 1:1.1455, we have a level of 278 EUR/MT. Extracting the fobbing costs and handling losses of 0.3-0.36%, we have a CPT price of at least 270 EUR/MT. This price does not include the exporter’s margin, so the difference of up to 260 EUR/MT may mean many other things.

Romania has produced over 11 million tons in 2021, but the local market demand component does not exceed 3.3 million tons. It is an extremely powerful element in the calculation of sales moments, which must raise questions and motivate the percentage sale on spikes, so as to avoid the dramatic decreases that we see these days.

Romanian wheat exports amounted to 4 million tons, until December 31, 2021, and still wheat stocks reside on or off farms, purchased for export. We therefore have a minimum quantity of 3-3.5 million tons that must be transferred (sold) for the 2021-2022 season.

The new wheat crop is priced starting January 5, 2022 and things are getting bigger. The corrections made to the price of the new crop are generated by the indications of EURONEXT SEP22 which have a negative trend in recent days. Thus, we see indications of 228-232 EUR/MT CPT Constanța for new crop goods, with a discount of 5-10 EUR/MT for feed quality.

We were repeating once again that it was a sell signal. It is necessary to sell forward a maximum of 2 tons per hectare to secure a part of the farm’s income and, implicitly, to secure the balance of income and expenditure.

EURONEXT SEP22 MLU22 – 243.25 EUR

REGIONALLY

There is a certain state of panic in the Black Sea basin among Ukrainian farmers. Coming after a long period of winter holidays due to the calendar gap between the two Orthodox rites, New and Old, fueled by uncertainties about the potential conflict with Russia, they are at the forefront of wheat and corn sales these days.

This further strains the existing price potential. The desire to sell is present, creating additional pressure on the price of wheat. This tension also naturally extends to the Port of Constanța, through the level we mentioned above in the local analysis.

Before we note the price levels in the Black Sea basin, we want to note the attitude of a Russian analyst who is already filtering everything through the act of aggression against Ukraine. More precisely, this character evokes 2014 when, I quote, “Russian special forces entered Crimea and the price of wheat increased by 20%.”

We deeply disapprove of this way of thinking and analyzing based on Russia’s aggressor attitude. The exploitation of a conflict in generating a higher price of wheat has no foundation in terms of humanity or fair business. Taking advantage of a potential act of aggression against people who do not have expansionist tendencies to increase a financial dowry impoverished by the level of a politically imposed tax is an example of appalling cynicism, if we may say it.

Russia is still slowing down because of its protectionist policies, and the undisguised joy of a potential future generated by the death of innocent people makes us disapprove of this gentleman’s sharp slippage.

Returning to the business spectrum, BSW indications are declining for February, an extremely strong price trend signal that we anticipate. The actual flooding of the wheat basin, dictated by the level of volumes and the fact that Russia is lagging behind the export program, generates a sharp drop in quotations. As we can see below, FEB22 KFG22 generates a lower level by 9 USD/MT compared to KFF22 IAN22. The equivalence of FEB22 in EUR is according to parity 1:1,145, i.e., 284.6 EUR/MT.

BSW KFF22 JAN22: 335.25 USD (-1) – KFG22 FEB22: 326.25 USD (-2.25)

Quotations for the new wheat crop have indications of 295-300 USD/MT FOB Ukraine, with delivery July-August 2022, which reflects 257.6-262 EUR/MT.

In the EU, wheat is listed at 315 USD/MT in FOB Rouen for 11,5% PRO quality, with delivery in February-March.

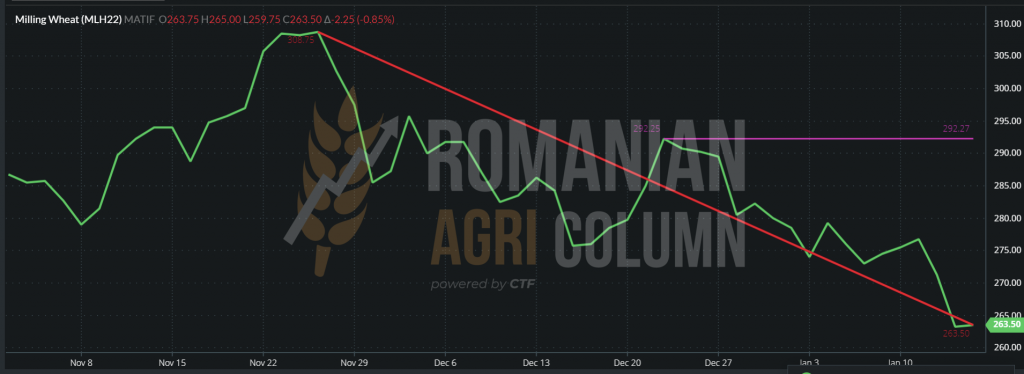

On the stock market, the effects of the WASDE report are effectively crushing European wheat. The results of the report have a negative reflex, expected, by the way. Wheat loses 30 euros from December 22, 2021 to January 14, 2022.

EURONEXT MLH22 MAR22 GRAPHIC

EURONEXT MLH22 MAR22 – 263.5 EUR at the close of 14 January 2022:

GLOBALLY

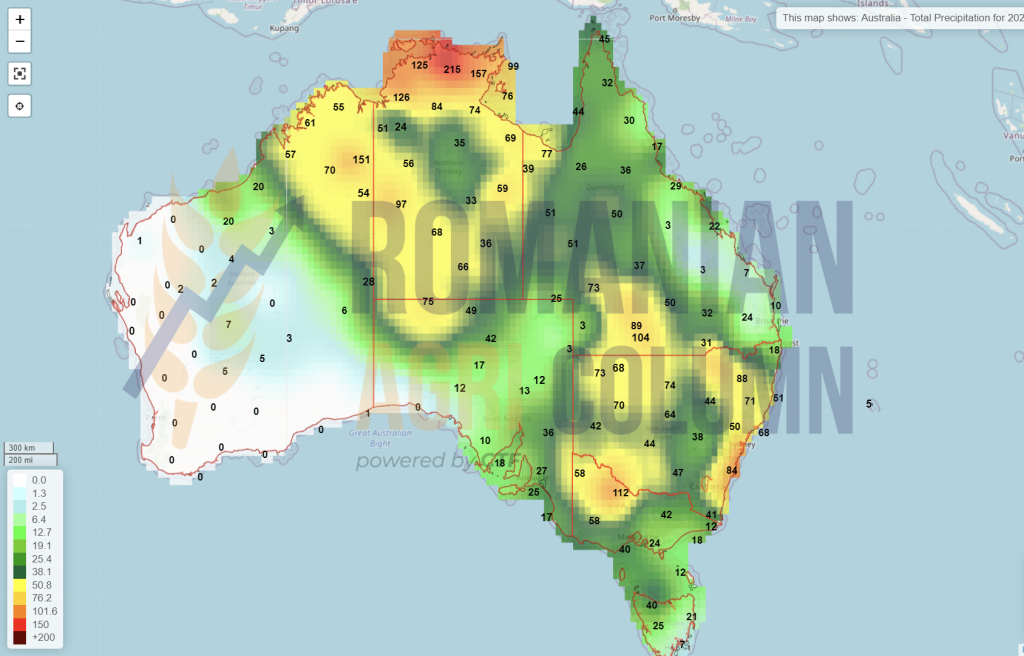

WASDE had a negative reaction to the price of wheat. This was expected by Romanian AGRI Column and forecast in December. A surplus of wheat from the Argentine crop, combined with an Australian surplus, effectively calmed the wheat market. The second period of the 2021-2022 season is definitely becoming a hand to mouth behavior of destinations. Their coverage is sufficient at this time and they will no longer compete as in the first part of the season. We refer here to the traditional destinations of the Middle East, North Africa, Sub-Saharan Africa, as well as Asia as a whole. The recent example of China taking out of its own reserve about 500,000 tons of wheat to sell in the domestic market indicates the relaxed state of destinations.

As time goes on and we get closer to the middle of February 2022, we will see the future crop levels more accurately and we will be able to have more clarity in this regard.

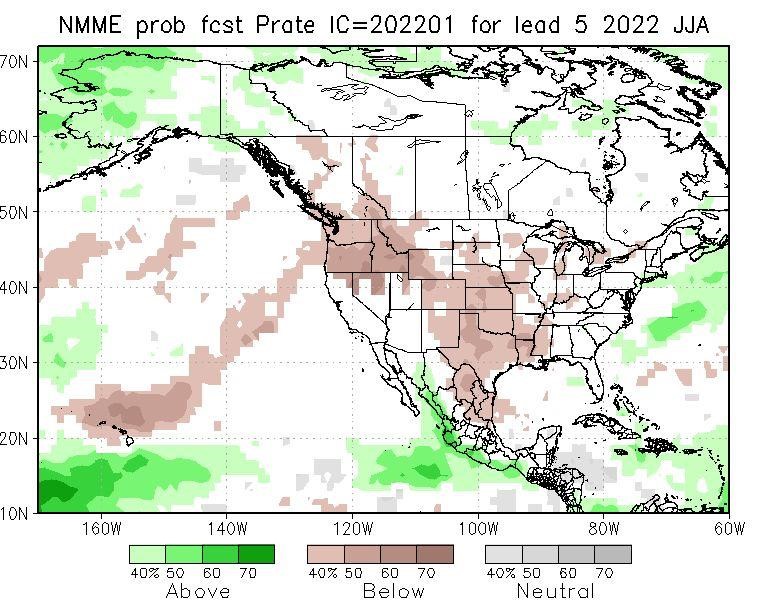

In the US, drought problems persist in the southern Central Plains, which will certainly impact the level of wheat volumes to be harvested in 2022. For now, however, the area of US wheat sown in the fall has not notably differed compared to initial estimates. Thus, the USA accounts for an area of 13.3 million ha, increasing by 100,000 ha compared to the initial forecasts.

Preliminary indications on the price of wheat generate a working hypothesis that nuances a growth effect in the second half of the season, more precisely starting with July, then a tempering and regrouping at the levels we see today in the North American markets. Reducing feed utilization could be the key to stabilizing and lowering wheat prices by the end of 2022.

This working hypothesis is generated by a weather forecast that indicates the months of June, July and August as being extremely dry and hot in the USA. This forecast model could have the effects of last season and it would not be surprising to see Canada operating according to the same predictive model.

Thus, after a month that will bring rainfall on the North American continent, drought and heat will make a definite mark on crops, i.e., wheat, corn and soybeans. As we can see and repeat for the sake of understanding, Canada is no exception.

US stock markets are closed on Monday, January 17, 2022. It’s Martin Luther King’s Remembrance Day, so the closing levels of the night of January 14-15, 2022 are the main landmarks.

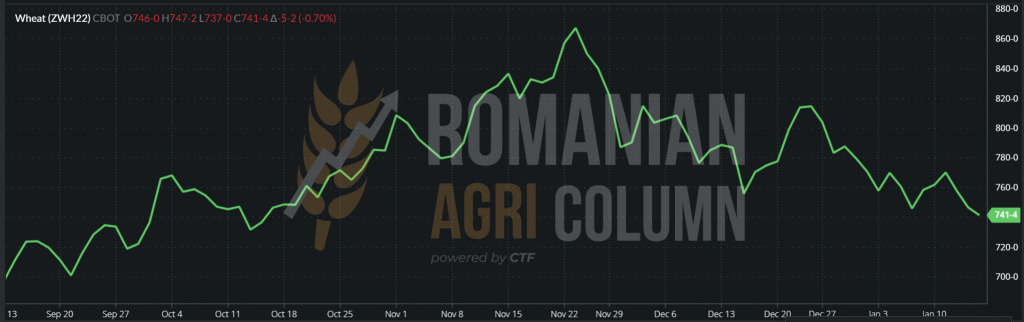

January 14, 2022: CBOT ZWH22 MAR22 – 741 c/bu (-5c) | KANSAS KEH22 – 745 c/bu (-14c)

GRAPHIC CBOT ZWH22 MAR22

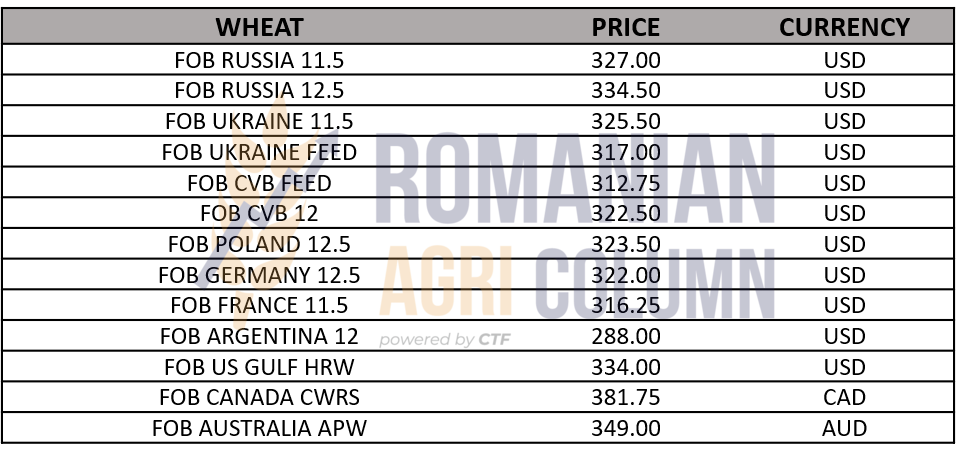

Indications of wheat price of various origins:

ANALYSIS

- Destinations change consumption behavior in the remaining period until the new crop.

- The surplus generated by Argentina and Australia is tempering global demand.

- The Black Sea Basin remains under pressure from Ukrainian farmers’ rush to sell wheat stocks.

- The wheat market will stabilize in the near future. Only a conflict in the Black Sea basin could generate price trend changes, but no one wants a conflict in the area of origin of many destinations.

LOCALLY

The indications for feed barley in the CPT Constanța parity amount to 242-245 EUR/MT. The demand is still in place and supports the price. TMO Turkey indicates a new tender for the purchase of 345,000 tons of feed barley with completion on 20 January 2022. This confirms the lack of liquidity in the balance of supply and demand for barley, which is approaching the price of wheat at this time. The difference is only 7-10 EUR/MT in favor of feed wheat.

Romanian barley sown in autumn is under good auspices so far and we can generate information on surface and volume levels, as follows:

At the moment, the forecasts are quite reserved due to the lack of water and the sowing in water deficit, but things can improve substantially as we get out of the winter.

The European Union has a sowing level of 4.6 million ha in autumn, with a forecast of 5.8 million ha in spring, as follows:

ANALYSIS

- The price of barley is supported by lower global production.

- Auctions certify this, as well as the logistical advantage over Australian barley.

- Sowing and production forecasts are similar to those of the previous year.

LOCALLY

The local price indications do not suffer big depreciations at the level of CPT Constanța, as in the case of wheat. They are maintained as primary indications at 237-239 EUR/MT. Inland farms show levels of 222-228 EUR/MT, depending on the region. Depending on the quantities, levels are generated that can reach up to 235 EUR/MT FCA Farms.

In the case of Romania, we see a final crop attested by the European analysis houses, which places it at the level of 15 million tons, in line with our initial forecast.

Romanian farmers trade corn at the beginning of this year. The thrills of a potential price drop encourage sales during this period. The WASDE report, which generated a lower level of global production, as well as a lower level of global stocks, should have generated a neutral attitude towards maize, but it was attracted by the “bearish” movement of wheat on a descending slope. However, the decline in the EURONEXT plan is not particularly large, and transactions in the Black Sea basin still have potential for expression.

The port of Constanța still has the logistical advantage and we remind you that Romania does not have a phytosanitary agreement with China, which penalizes Romanian farmers for the benefits of this energy-consuming destination in terms of volume and price. A simple comparison with Bulgaria indicates a minus of 5 EUR/MT in the price of Romanian goods.

REGIONALLY

Ukraine continues to position itself as a driving force behind zonal corn sales. The holiday break and the fear of a conflict with Russia are driving the sales of Ukrainian farmers. Indicative prices in FOB Ukraine parity are between 274-279 USD/MT. Conversion to EUR indicates a Black Sea FOB level of 239-243.5 EUR/MT.

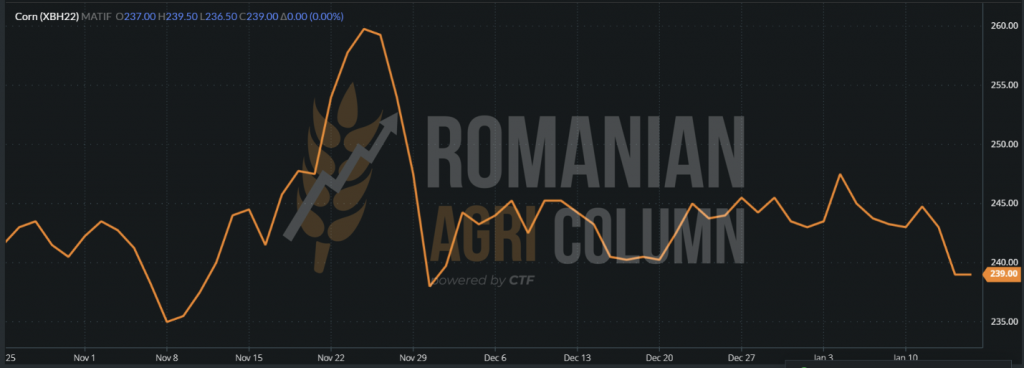

EURONEXT indicates a closing level on 14 January 2022 of 239 EUR, which correctly marks the market these days.

But we suggest you pay attention to the indication XBX22 NOV22, which gives us the first feeling about the 2022 corn crop. Here we have a level of 223 EUR, which should lead to a level of 213-215 EUR/MT in the CPT Constanța parity.

Early estimates of a new maize crop indicate a downward trend in the European Union of around 3 million tons, from 67 to 64 million tons.

EURONEXT XBH22 MAR22 – 239 EUR

We insert the trend chart of the Euronext corn indication to see the decrease of 5 EUR generated by the WASDE report and we repeat the information about PRODUCTION, CONSUMPTION and STOCKS.

GLOBALLY

The outlook is not good for the South American maize crop, and we are talking about Brazil, in particular, which is losing about 5 million tons in the Safra crop, which has raised concerns about WASDE figures. But things could take another turn. The rains will return to South America next week and the compensation could also come from Brazil, as a preview of Safrinha, the second corn crop. Cloud clusters are seen over Brazilian territory, but Rio Grande del Sul and Mato Grosso del Sul are not covered at this time.

Thus, the second crop will compensate the deficit from the first crop, generating the figures of 119-120 million tons initially expected. The diminutive of Safrinha no longer fits well with the size of the second Brazilian crop, surpassing in volume Safra. Safra normally generates 25-26 million tons, and Safrinha 93-94 million tons of corn. Safra being downgraded by 5 million tons, will generate only 20 million tons and Safrinha will compensate the deficit by going up by 3-4 million as a surplus.

Argentina, the second most important player in South America, is suffering from a long-standing drought these days, and is now facing an extreme heat wave of over 40 degrees Celsius. The comfort given by the precipitation is expected to appear the following week and the improvement to occur subsequently. At this time, the corn crop estimate remains intact at 57 million tons, according to Argentine analysts.

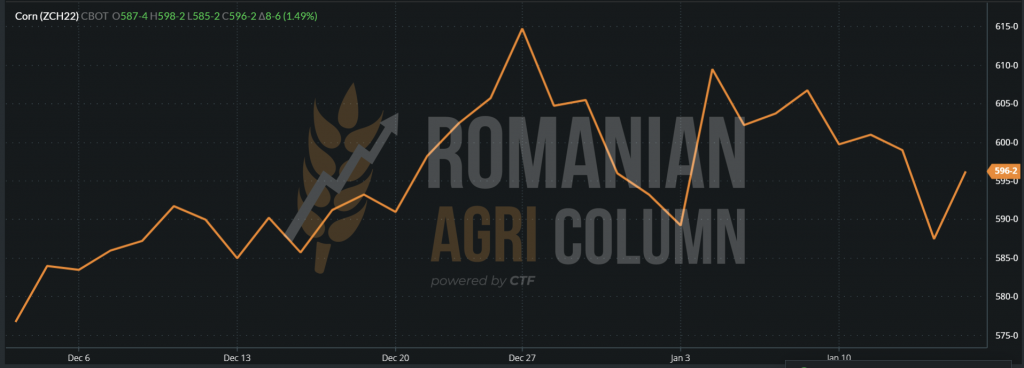

CBOT indicates the return of maize quotations. In the closing session during the night of January 14 to 15, we noted the return to the threshold of 600 c/bu. Corn gained no less than 8 c/bu, closing at 596 c/bu.

CBOT ZCH22 MAR22 – 596 c/bu (+8 c)

Price indications of various origins

ANALYSIS

- Corn has fuel and returns to the neutral zone after being harvested by wheat following the WASDE report.

- The Black Sea basin is effervescent in terms of sales of Ukrainian and Romanian farmers.

- But caution must remain the watchword. Any rainfall in South America will compensate for the lack of 5 million tons in the Brazilian harvest. The balance is somewhat stable, with the Ukrainian surplus partially offsetting the lack of Brazilian volume.

- The competition between origins will begin soon. Brazil and Argentina will compete very closely with the Black Sea basin once the harvest begins.

- One signal that catches our eye is China’s announcement that it will reduce corn imports by 3 million tons. If this happens, it will result in a lower price of corn. Or it’s just a sign that origins are competing to generate a lower price of goods, knowing that China’s destination wants (like everyone else) a lower price.

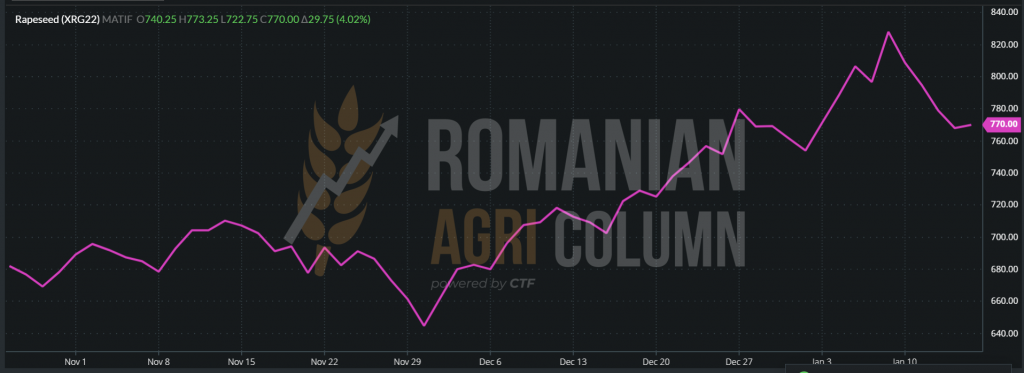

The old rapeseed crop has an obvious setback and we notice a noticeable decrease from 825 EUR to the level of 770 EUR indication XRG22 FEB22. It all has to do with the level of coverage of the positions of rapeseed oil traders, correlated with fossil energy. When liquidity is no longer present, the processing units form the market. The demand is present, and the need for rapeseed oil for biodiesel is evident every day we drive with engines burning fossil fuels. This is the main effect of Canada’s lack of liquidity. We are talking about a snowball that rolled continuously, uncovered by any crop surplus, no matter how small, except for a few small positive adjustments from Australia and, more recently, India.

German biodiesel processors have huge problems supplying raw materials. Liquidity is not present, and everything they had predicted they would process is sold out. In other words, they are short of raw materials to cover sales. Certainly, in these conditions, profitability is no longer a factor to be taken into account, but only the fulfillment of contracts for the sale of oil, an oil that has an average indication of 1,630-1,635 EUR/MT FOB Rotterdam.

EURONEXT XRG22 – FEB22 at the closing date of 14 January 2022 – 770 EUR

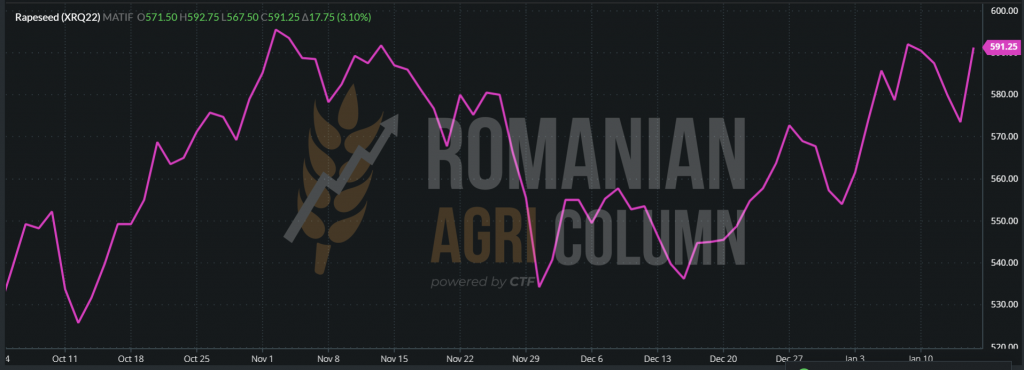

Looking at the new rapeseed crop, we notice the return. We had no emotions that this will not happen, up to the level of 591.25 EUR – XRQ22. Rapeseed has support in demand and, even if we see an exaggerated inverse crop (XRG22 FEB22 770 EUR vs. XRQ22 AUG22 591.25 EUR) of 178.75 EUR, we still consider that XRQ22 AUG22 will exceed your threshold of 600 EUR, it will even go up to the level of 620-625 EUR.

EURONEXT XRQ22 AUG22 – 591.25 EUR at the close of January 14, 2022

As we said in the previous issue, we recommend the sale related to a mechanism for the subsequent fixation of the indication XRQ22 AUG22, which will leave the potential market participant intact and in solidarity with the subsequent price movements of EURONEXT. Regarding the volume level, we recommend a maximum of 1-1.5 tons per hectare to be sold forward in order to manage the possible risks generated by the weather or unforeseen factors. These days, the processor options are at the level of XRQ22 AUG22 minus 10 EUR/MT.

TREND XRQ22 GRAPHIC. There has been a collateral decline since the January 12 WASDE report.

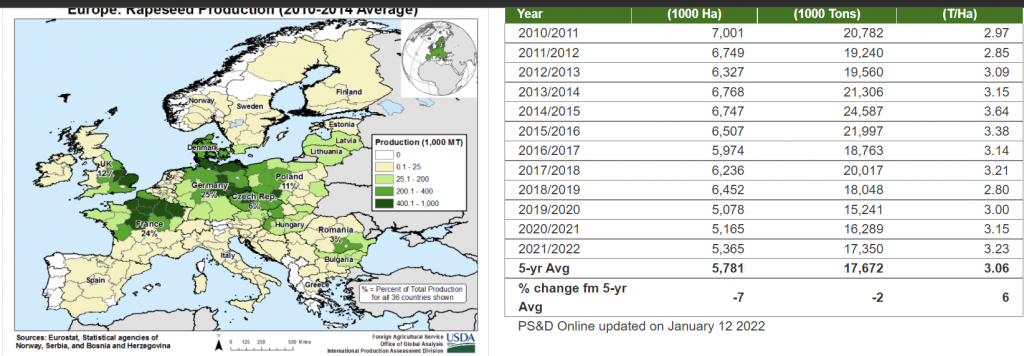

In the image below, we find an average of rapeseed production in Europe in the last 10 years. In 2022, the forecast is 17 million tons, in line with last year and with an average of the last 5 years, which leads us to a support of the price level. The use of rapeseed has become much more common in the vegetable oil market, not only in the industrial (biodiesel) market. Source: USDA

ANALYSIS

- Old crop rapeseed oil still has obvious support due to a lack of liquidity, but this is exactly what penalizes German processors who do not have the raw material coverage for sales already made.

- The new rapeseed crop has the same level of sowing in Europe and the Black Sea basin. Unknown remains Canada once again, with dry weather forecast from June-July-August.

- We recommend maximum caution in forward rapeseed sales. In other words, to be carried out at the fixing mechanism and maximum 1-1.5 tons/ha.

The indications of the port of Constanța and of the processors have seen an increase of about 10 USD/MT, but they are quite weak and do not build around the desire to sell of the farmers. Small quantities move from one place to another and we note prices of 645-650 USD/MT in the southern regions of Romania for quantities of 100-200 tons in the FCA Farm parity.

As for the new sunflower seed crop, it has started to be priced locally at 525 USD/MT. It’s a good start compared to last season, when we had a price of 485 USD/MT in February 2021. But the sunflower seeds that will become the next crop are not sown yet, so a long road awaits us, with many stages.

We note the CVB price level which increased by 15 USD/MT in the FOB parity, reaching 678 USD/MT. On the Ukrainian side, we note the level of 21,000 UAH/MT, up from 19,800 UAH/MT displayed after January 3. This price reflects a level of 751 USD/MT for the goods delivered to the processing units, but the VAT level included in the price of the goods, which is 20%, must be taken into account. If we extract VAT, we reach 630 USD/MT DAP Processors.

As for the quotations of sunflower oil in Ukraine, they are between 1,370 USD/MT ASK compared to 1,350 USD/MT BID. The market is relatively calm and quiet. There are not many buyers at this time because Ukraine has a holiday period lagging behind the rest of Europe, and Ukrainian farmers behave in the same way and do not sell raw materials, preferring to sell corn and wheat. We mention that the processing units in Ukraine have coverage only until the end of January 2022.

This is despite the fact that the overall estimate of the global crop is 6.7 million tons more than last season. However, the difference is that last season, i.e., in 2020, the drought was widespread in Europe and in the Black Sea basin. So there are differences in volume, but also in weather conditions, which entails the need to compare with the 2019-2020 season, as we insert below.

It is observed in comparison with a normal season that the difference in production is only 1.8 million tons. Surprises can also come from Argentina. Also, global sunflower oil reserves are very tight and stocks are not recovering from the 2020-2021 season.

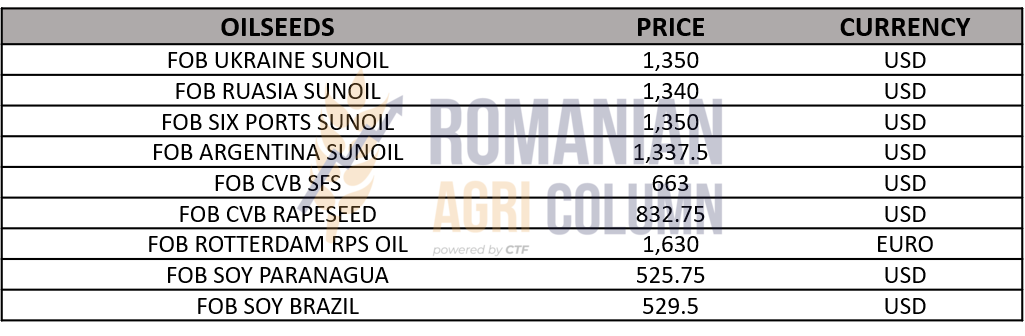

Indications of oil and oilseeds in various origins:

ANALYSIS

- Farmers’ expectations are beginning to take shape. Only time and demand will decide whether the level will rise by 20 USD/MT.

- Surprises could come from Argentina, the last country that can still influence the price of sunflower seeds.

- The new crop is listed, but the seeds still have a long way to go.

At the local level, soybeans are not of particular interest at this time. The price of 555 USD/MT offered by the processors is quite far from the market level and does not constitute a serious level that is currently offered (1,369 c/bu = 503 USD), given that Brazilian soy is offered at the level of 525 USD/MT FOB and the American at 545 USD/MT FOB US Gulf. If we calculate the price of transport at the level of replacement, i.e., ocean transport to Constanța, the logistics of unloading and delivery to the processor, the cost of financing and handling losses, we would reach a level of over 600 USD/MT. And if we think that Romanian soy is non-GMO, we have a different perspective on the price level.

The WASDE report revealed anticipated problems in South American soybean crops. With substantial reductions in production in Brazil (minus 5 million tons), Argentina (minus 3 million tons) and Paraguay (minus 1.5 million tons), the global production deficit reached 9.22 million tons. A 0.3-million-ton compensation comes from a positive but insufficient US review.

Global stocks are also deteriorating by 6.8 million tons due to production cuts, but are offset by a decline in global soybean consumption of 2.1 million tons. This decrease in consumption comes mainly from Argentina, as a sum of the forecast cut in production. Argentina mainly processes soybeans and thus, as it does not have a larger processing base, due to the decrease in production, consumption decreases as a consequence.

However, the fluctuations in the price of soybeans did not stop. After a recovery generated by the emotion of the report, the levels before the report returned. This is due to weak US soybean sales to China. Their numbers expressed in bushels have an impact, as they are at the level of millions. However, when converted into tons, they are substantially reduced to 100,000 tons.

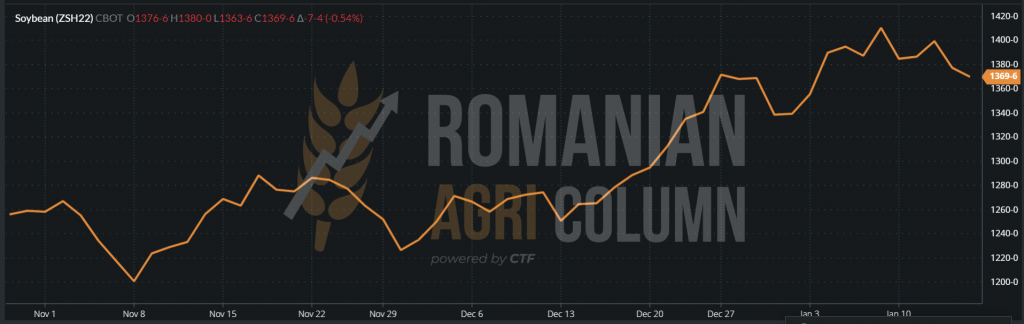

CBOT ZSH22 MAR22 1369 c/bu (-8 c)

CBOT ZSH22 MAR22 GRAPHIC

EUR:USD = 1:1.41

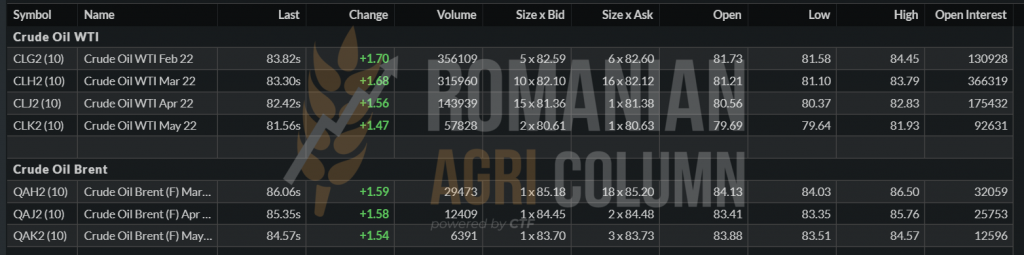

BRENT exceeds 86 USD/barrel | WTI is close to 84 USD/barrel

15-22 January 2022

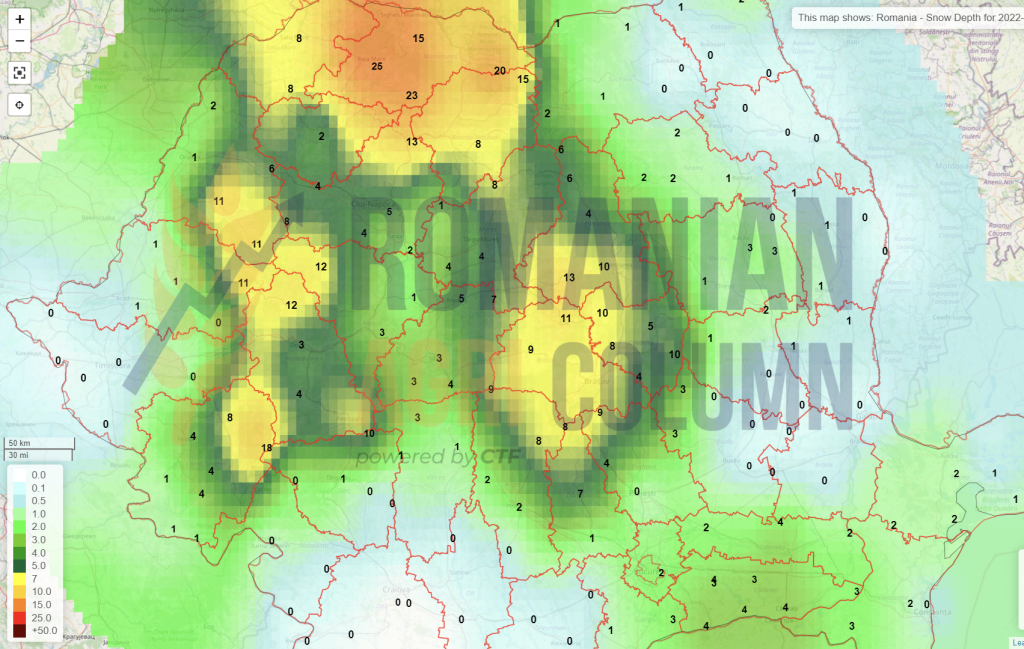

Romania (snow)

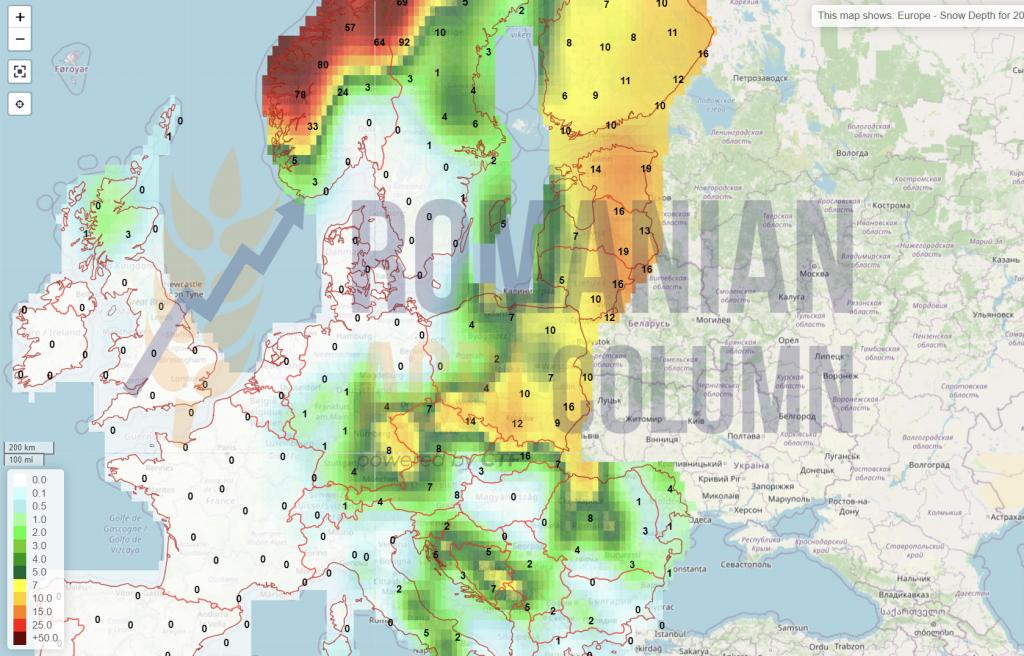

Europe (snow)

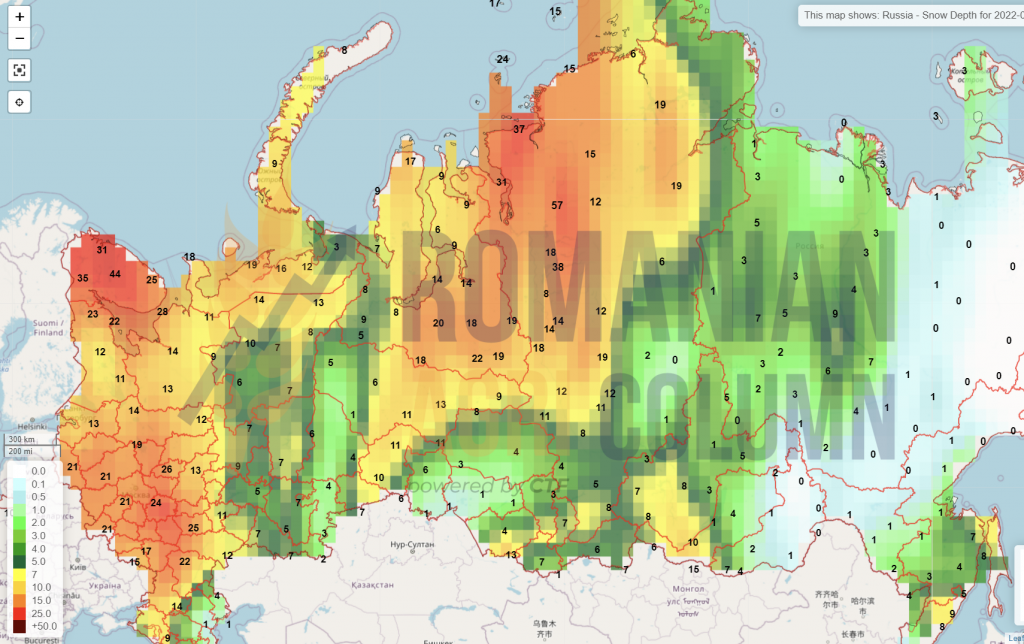

Russia (snow)

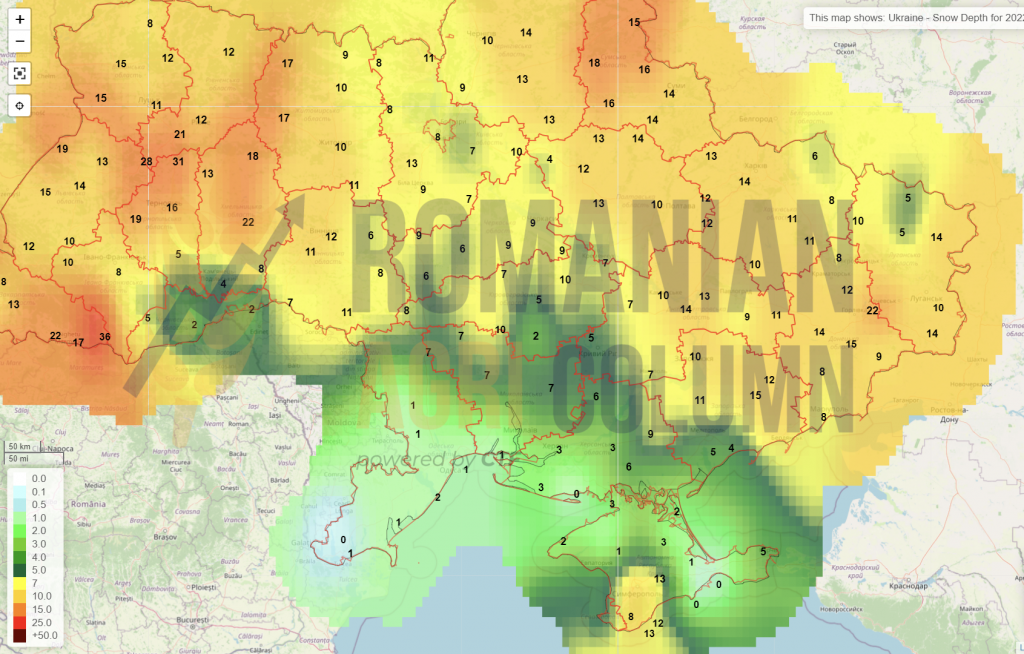

Ukraine (snow)

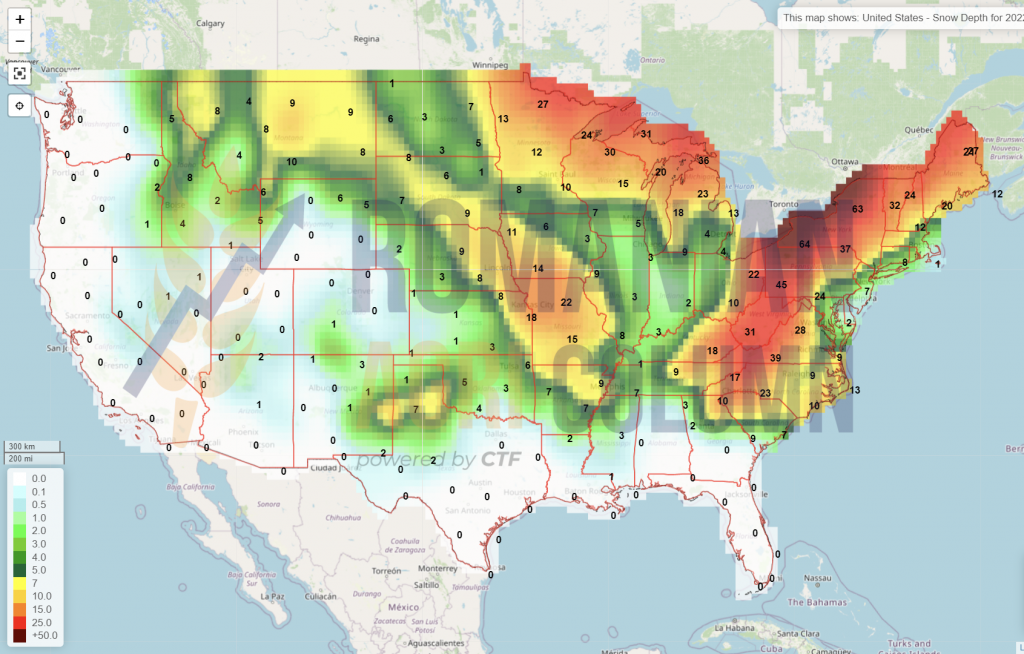

USA (snow)

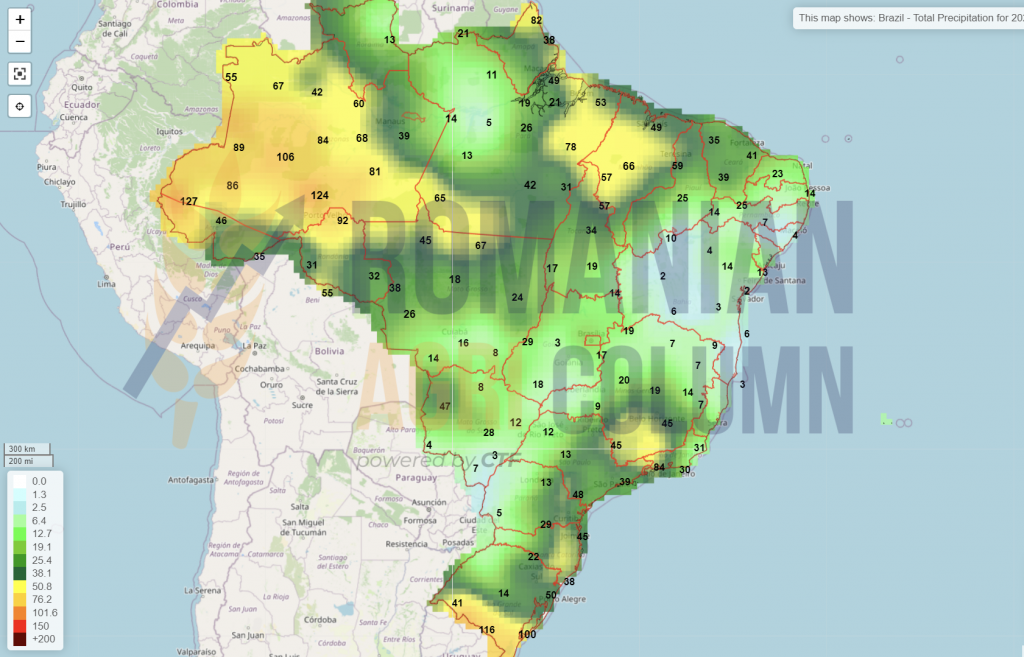

Brazil

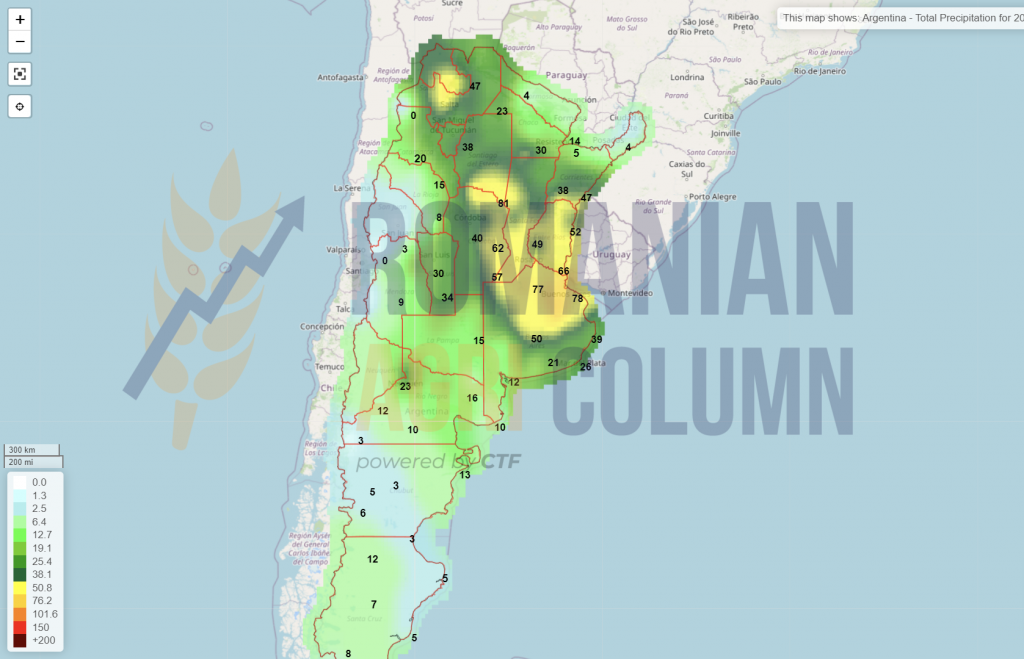

Argentina

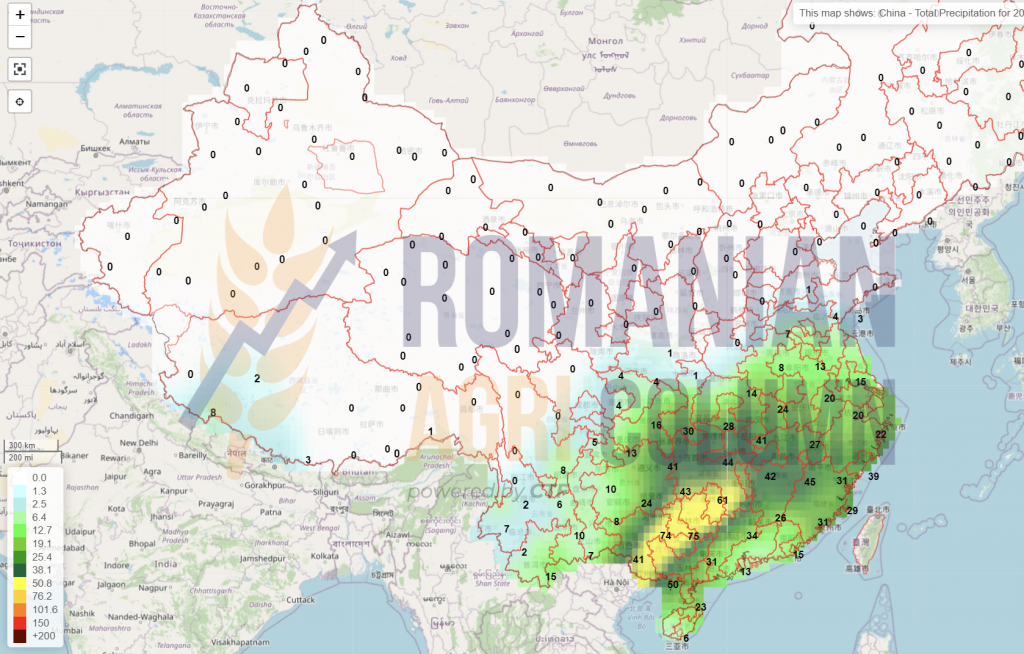

China

Australia