With the first issue of our report this year, we want to wish you a fabulous 2022 in terms of business as well as personal life!

It will be a year full of challenges, a year that began under the auspices that seem to never end generated by COVID-19, politically tense and that has reserved surprises for us because of Mother Nature since the early days of the year. And of course, we are talking about South American soybean and corn crops. It will be a difficult year to estimate, a year in which the commodity supercycle will not end, in which inflation will not slow down, a year in which weather and politics will mix deeply in agriculture.

As usual, we try to generate the analysis that you filter, so that your business has a lot of predictability and avoids risks, risks that are everywhere and can generate losses in your company’s account.

Starting this year, the report will be structured in well-defined chapters and easier to access thanks to the new template, which allows you to access the desired section with a click. The synthetic content of each category of goods, structured on three levels, Local (Romania), Regional (EU and Black Sea basin) and Global (worldwide), so that it is at your fingertips in a much easier way.

Thank you for the trust you have placed in us and we assure you of our support and accuracy in the years to come, so that your business decisions will be supported by our analysis.

Cezar Gheorghe, author

This week’s market report contains information on:

LOCALLY

The Romanian wheat market is confusing at the beginning of the year. On one hand, farmers are disoriented by the downward trajectory of the price, and on the other hand, buyers who have not yet fully returned from vacation show a reluctance to display slightly firmer prices, amid uncertainty about price traction in the following period.

Thus, from January 3 to January 7, 2022, we see a fluctuation around 270 EUR/MT, with some highlights, up to around 282-283 EUR/MT. However, the precautionary indications are valued at the level of 272 EUR/MT in the CPT Constanța parity.

The caution is generated by the imminent release of the USDA report, which will arrive on January 12, aggregate with the end of the year, which generated the liquidation of positions of investment funds at the end of December 2021, leading to a sharp decline in stock prices.

At the local level, processors want goods to be picked up during January-February, but the quotations offered do not generate much liquidity at this time. We emphasize on this occasion what we have said since the beginning of December of the year just ended, when we urged farmers to sell wheat. There is quite a lot of liquidity in the Romanian market and, with the price degradation, farmers will lose the potential expected at peak times.

But now it’s quite late and no good things are happening in a panic mode. The “profit taking” movement of funds, fueled by a lack of demand in the Black Sea basin, aggregated with the winter holidays that will last for Ukraine and Russia until January 10-12, 2022 are not factors of coagulation of a level higher price, especially since the USDA report will bring new data in this regard.

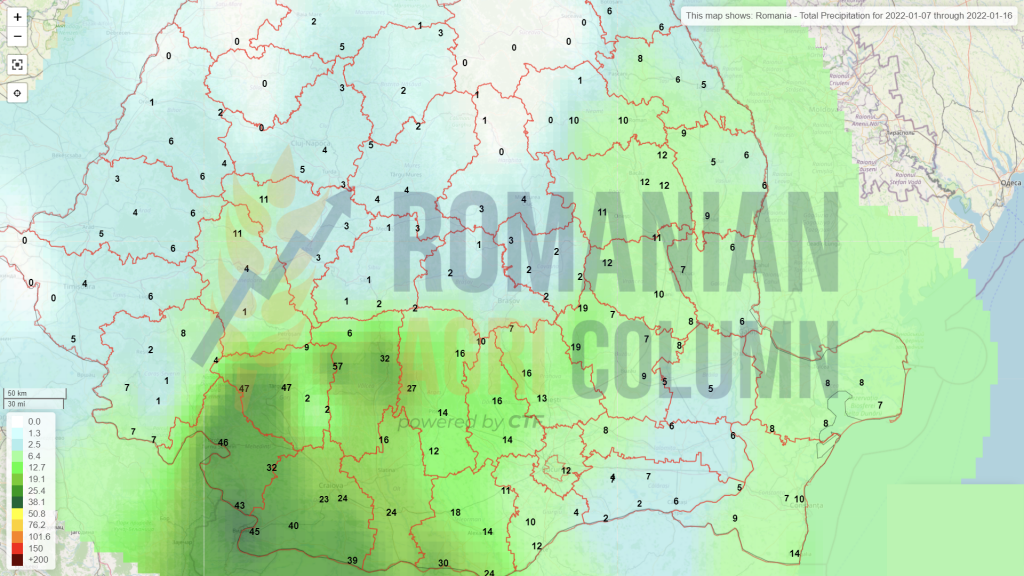

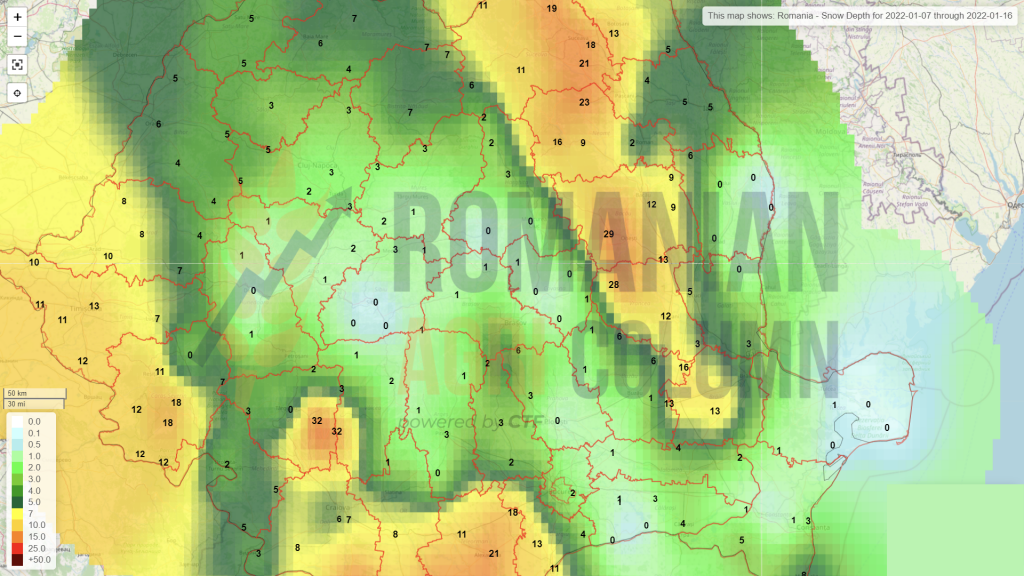

In Romania, the wheat crop is in favorable conditions for this moment. The water supply in the soil is correct, but it is desirable, of course, precipitation to bring accumulations in the upper layer of 15-20 cm to allow leaching the level accumulated so far to the next lower layer of 15-20 cm. The weather forecast at this time is cooling the weather, as 15 degrees during the day is not a beneficial factor for the wheat crop, aggregated with certain rainfall. We see some exceptions to these rules in the northern part of Romania, in the area of Moldova, which will not have rainfall. In this area, more precisely delimited by the Focșani area in the south and up to the border level in the north, the lack of precipitation is visible. Delayed sowing and lack of water affected the wheat crop. Uneven sprouting, partial prouting, as well as premature yellowing are the visible effects at this time of year.

In the year-end report, the European Union degrades Romania as a crop potential up to the level of 8 million tons. Their expression is based on insufficient rainfall and the potential for winter frost, i.e., freezing of plants that will not withstand frost due to the late sowing season.

We do not yet subscribe to these early estimates. We want to observe the development in all phases, but we want to bring to the attention of farmers the subject of fertilizers and we are referring here to the distribution of nitrogen in February-March. Despite the particularly high prices that farmers face globally, the recipe for success is not to rationalize and stop using dosage, but on the contrary.

An optimal dosage will generate a higher level of production, which will cover the resources allocated to the purchase of fertilizers. In other words, a higher yield, with a support for the price of wheat will generate a much higher profit than a low or close to zero use. This is the first effect, because the second will come successively, namely the depletion of soil from nutrients from fertilizers, which will finally affect subsequent crops on the principle of crop rotation.

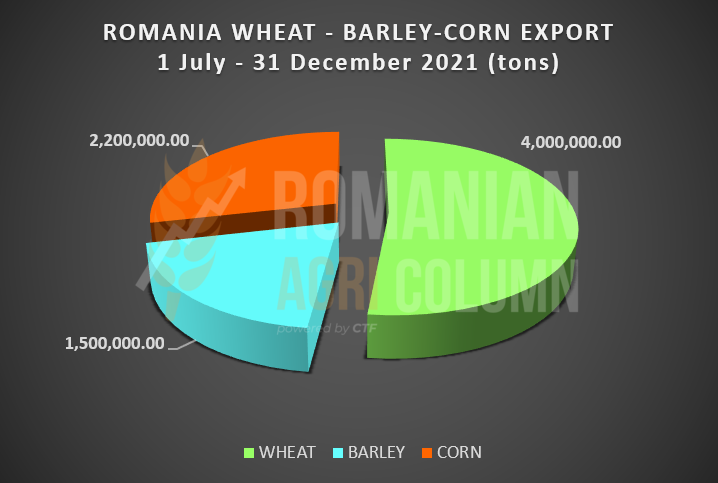

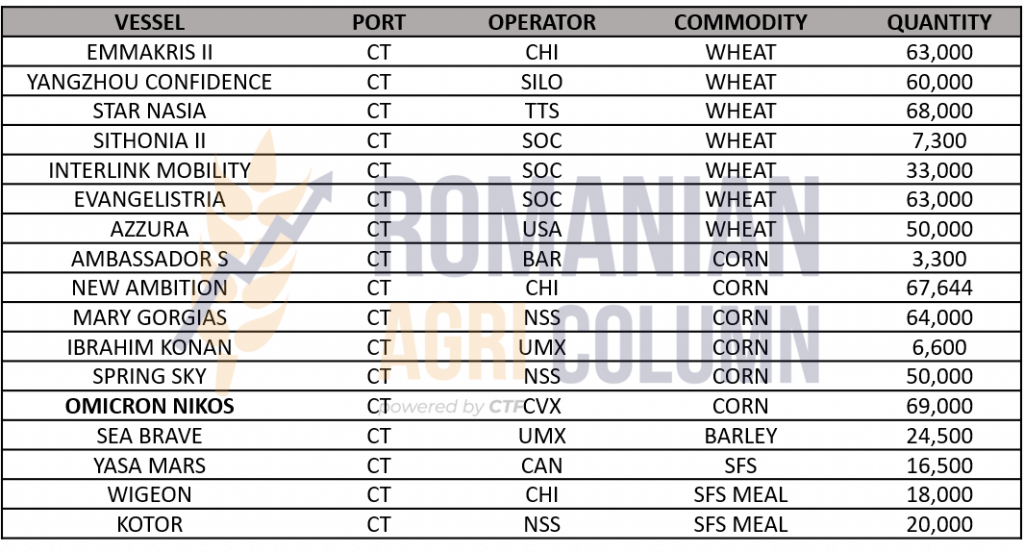

Romanian exports of wheat, barley and maize from the first half of the agricultural year 2021-2022 in the chart below:

REGIONALLY

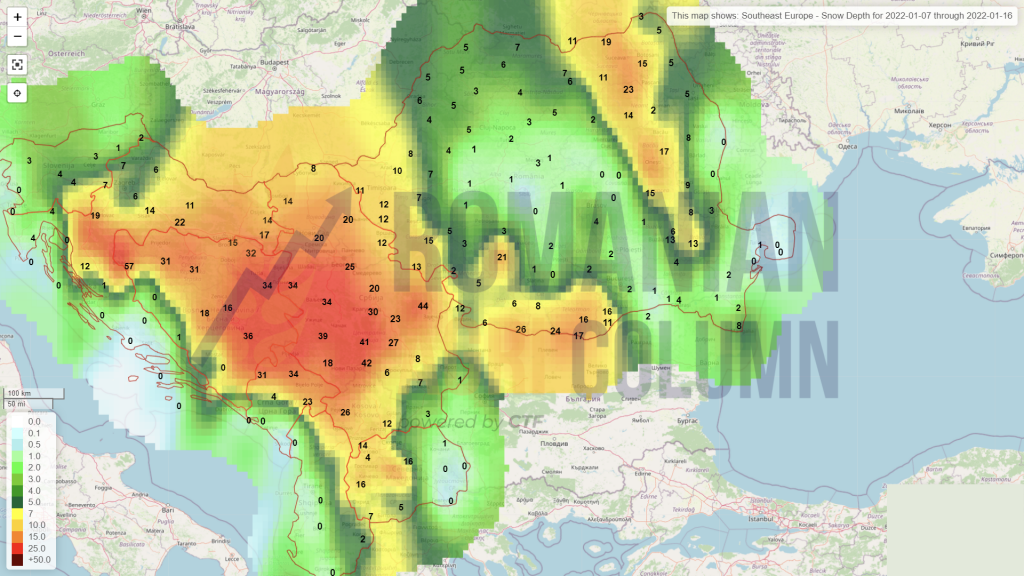

At the regional level, we do not see any particular problems with wheat crops in Russia and Ukraine. The rainfall has favored the development of the plants, and the snow covers the areas that were sown in autumn with wheat. So, at the moment, there are no conditions of concern in the Black Sea basin, on the contrary, the potential crop is higher than in 2021.

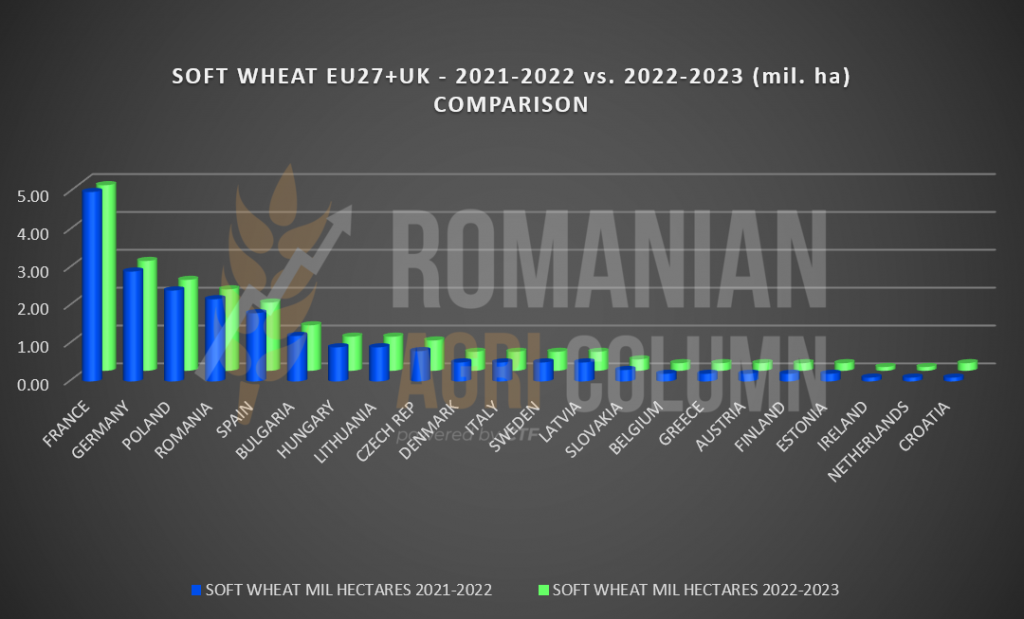

At EU level, things are just as good overall. There are no particular problems from the point of view of the vegetation stage. At the level of sown areas, there are no major discrepancies between the fall of 2021 compared to the fall of 2020 – the EU-27 level is 21,650,000 hectares, compared to 21,670,000 hectares.

In the chart below, you can find the areas that were sown with wheat in the fall of 2021, which will be harvested in the summer of 2022, for the marketing year 2022-2023 (green columns). We also compare with what was sown in the fall of 2020 for the summer 2021 crop and the 2021-2022 marketing year (blue columns).

In the EURONEXT plan, things are deteriorating, as expected. The imminence of the WASDE report, as well as the excessive harvest in Argentina, have meant that the price of wheat has not risen.

To these data from the analysis we also bring the Russian volume exported until the end of December 2021 – 20 million tons in total versus 25.8 million tons last season. These figures clearly indicate the delay of Russia caused by the export tax, which from January 12, 2022 will amount to 98.2 USD/MT.

This indicates a surplus of goods in Russia, which inevitably leads to lower stock prices. Judging by current figures in Russia, we understand that the market will have to be flooded with Russian wheat starting in February, if not earlier. This will be primarily due to the export tax which will force Russian farmers to sell the in stored quantities the hope of an even higher price. Russia’s total export index is currently 35 million tons.

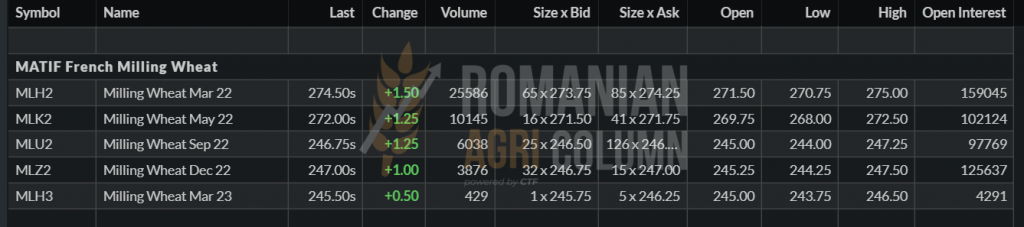

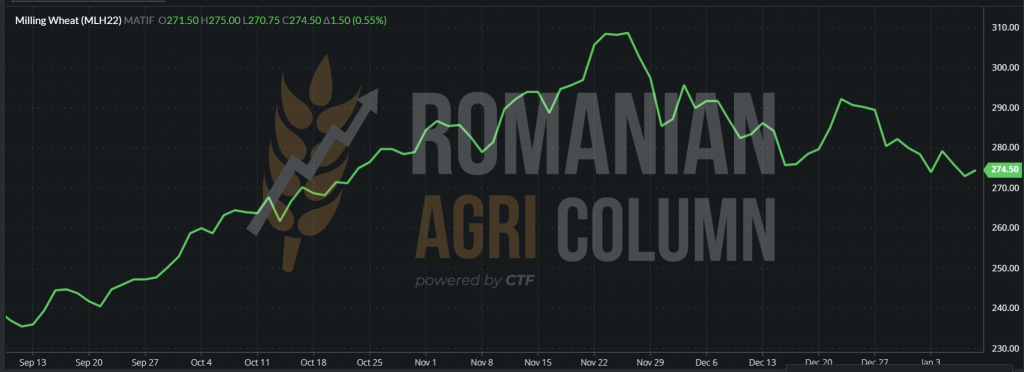

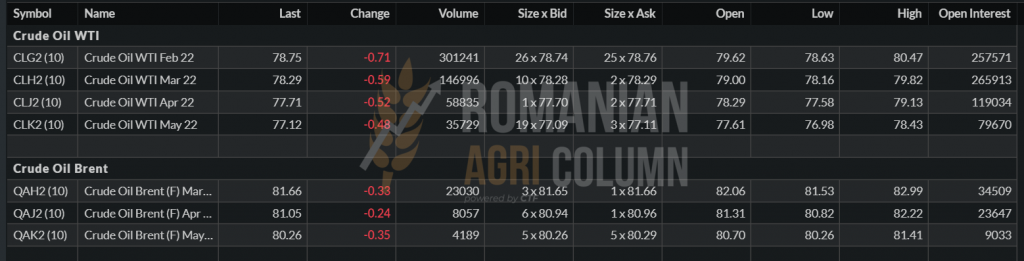

EURONEXT MLH22 – 274.5 EUR at the close of January 7, 2022

Wheat trajectory – MLH22 – SEP21-YTD

The Black Sea Wheat is also declining in quotations: IAN22 – 333.75 USD / FEB22 – 328 USD

GLOBALLY

Leaving the United States, we will cross the two continents from north to south and assess the status of the wheat crop, as well as the related crop levels.

In the United States, as we all know, violent storms of hot dust have affected American winter wheat. The proportion is not exactly known, but some analysts estimate between 25-35% and others 50%. However, this damage cannot be quantified at this time because the snow that fell from the Central Plains to the Atlantic coast, accompanied by violent storms, the so-called blizzard, followed. In other words, the United States is still an unfolded scenario in this regard.

Down in South America, Argentina is about 0.5% of the end of the harvest and local indications place the crop at a level of 21.5 million tons, about 1.2 million tons higher than the initial estimates. Thus, the Argentine surplus will once again lower the price of wheat globally, because if we add Australia, Argentina and Russia (which was raised in the previous report by 1 million tons), there are all the premises we mentioned in previous reports.

We will have a month of January that will be determined by a wave of quantities that will be wanted to be sold by the stock holders, not only locally or regionally, but also globally, to the same extent.

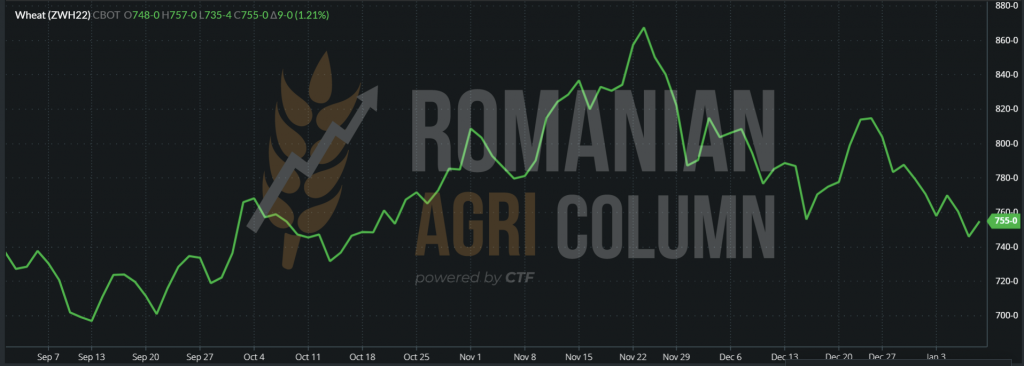

WHEAT – CBOT ZWH22 – 755 c/bu at the closing on January 7, 2022

ZWH22 WHEAT TREND

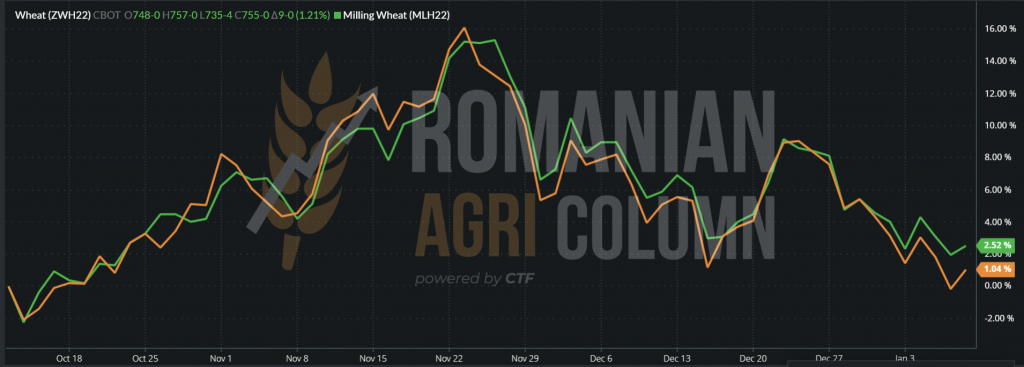

COMPARISON EURONEXT MLH22 (green) – CBOT ZWH22 (orange)

TENDERS

- JORDAN purchased 60,000 tons of wheat of Romanian origin through Agro-Chirnogi, at a price of 326 USD/MT CFR Aqaba, with delivery in August 2022. CHS and Ameropa participated by offering 329.87 USD/MT, respectively 333.9 USD/MT.

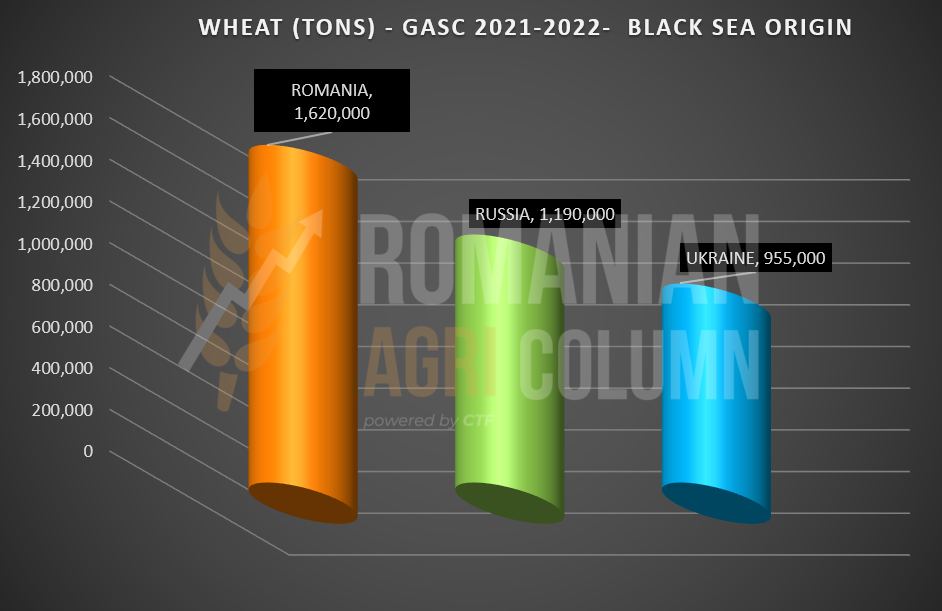

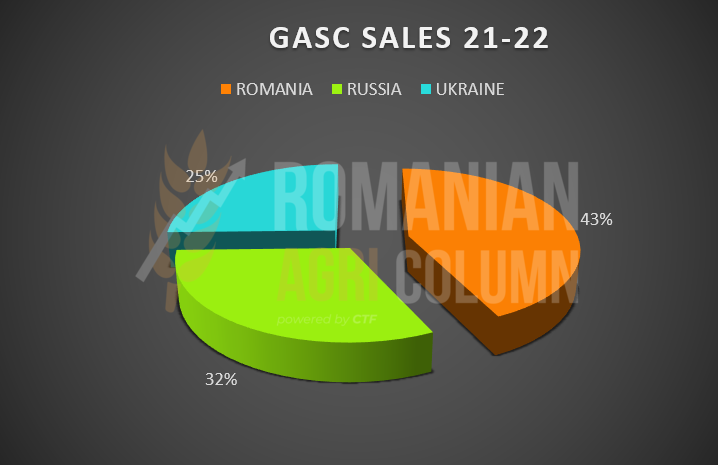

- In the last tender of last year, GASC EGYPT purchased 300,000 tons of wheat, as follows: 3 x 60,000 tons of Ukrainian origin, 1 x 60,000 tons of Romanian origin and 1 x 60,000 tons of French origin. With this auction, Romania consolidates its first position in the Black Sea basin in terms of sales to GASC Egypt and we are in the middle of the 2021-2022 season.

So far, GASC has purchased 3,825,000 tons out of an estimated 5.8 million tons. So there is still a potential of a maximum of 2 million tons in the next 3, maximum 4 months.

But surely the competition will become much fiercer. Despite the Russian tax, the goods in the basin must find their destinations and we are already seeing the competition in the Mediterranean as it takes place in this game.

RATIO BETWEEN THE COUNTRIES IN THE BLACK SEA BASIN:

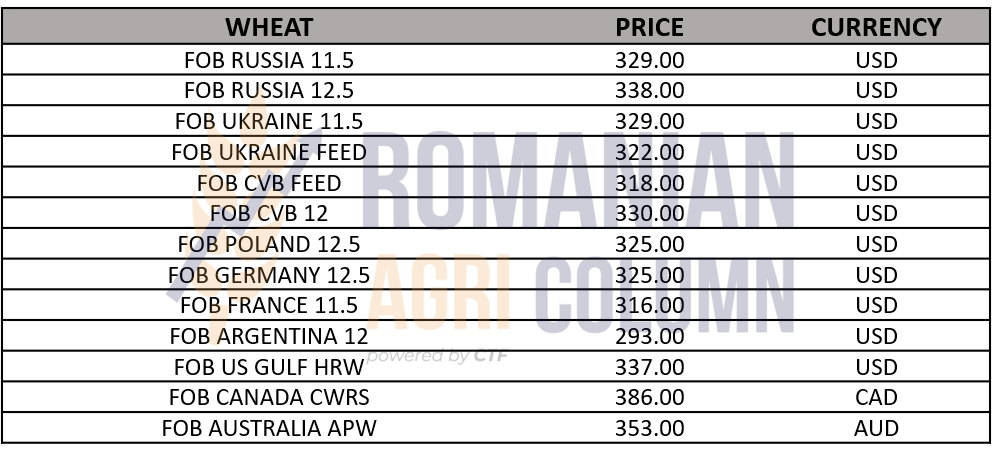

WHEAT PRICES IN VARIOUS ORIGINS:

ANALYSIS

- WHEAT POSITION is starting to become less sustainable.

- Consolidation of stocks comes from Australian and Argentine crops.

- Russian wheat did not reach the export parameters compared to last year (20 million tons DEC21 vs. 25.8 million tons DEC20).

- The WASDE REPORT will generate neutrality at best, although there are chances of bearish.

LOCALLY

The local market remains stabilized at 240 EUR/MT in the CPT Constanta parity, but the liquidity is not so strong. The level of Romanian barley exported until December 31, 2021 exceeded 1.5 million tons, so they are quite rarely found in large quantities.

The condition of the barley crop sown in the fall is good. The humidity in the soil is sufficient at this moment, so apart from the area of Moldova, which we have already mentioned, there are no problems on the horizon in the next 10-15 days.

REGIONALLY

Russian barley is well covered by the fallen snow, so there are no problems at this time. Similarly, the Ukrainian barley is safe from any problems in the next period.

The EU is doing just as well. The barley crop has a good vegetation condition and a sufficient water supply in the soil for the next period. The only area with a water deficit is Spain at the moment, but things do not seem to be degrading, at least in the near future.

GLOBALLY

The prices of Australian barley are at the level of 263 AUD/MT FOB, at least unchanged before the holidays, while the price of Russian barley also remains at the level of 295 USD/MT FOB, stabilized as the price in the port of Constanța.

LOCALLY

The indications for Romanian corn are at the level of 235-237 EUR/MT. This level has been around for some time, supported by demand in the Black Sea basin. During all this time, we still notice areas in Romania where the harvest is not finished, especially in the North of Moldova, as well as in the center of the country, in the Transylvanian plateau and in the areas of the Brașov region.

Corn traded very well before the holidays. Now, after the first week of 2022, we are seeing a low level of transactions due to the fact that farmers are still on well-deserved leave, after a year full of efforts.

REGIONALLY

In terms of harvest and quantities, they remain the same. Ukraine, Russia, Romania and the rest of the EU have finished harvesting.

EURONEXT indications remain stable. The value of 243-244 EUR remains the benchmark in quotations for French ports as well as those in the Black Sea basin.

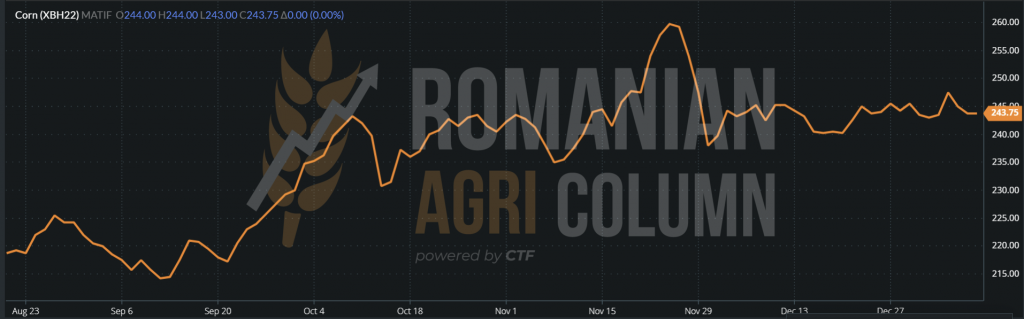

CORN – EURONEXT XBH22:

XBH22 EURONEXT GRAPHIC – notice the almost flat line starting with November 30, 2021

GLOBALLY

We’re going to South America, where the first surprises come from, if we can call them that. Due to the lack of water, heat and the phenomenon of La Nina, which has its expression for the second year in a row, Brazil is also facing problems for the second year in a row.

Namely, Safra, the first corn crop, is degraded in Rio Grande del Sul, as well as in Parana, by about 3 million tons. Thus, aggregate, the Brazilian crop is degraded by 4-5 million tons, since the last WASDE report, which generated the figure of 118 million tons. The new level is 113 million tons.

Argentina faces the same problems and, on the horizon, the estimated 57 million tons of maize could be blurred at the time of harvest. According to satellites that measure the stage of vegetation, Argentine maize is degraded in production to 46-47 million tons, which is about 9-10 million tons at this time.

The two aggregate factors above maintain the price level in the Black Sea basin, as well as the demand from this source.

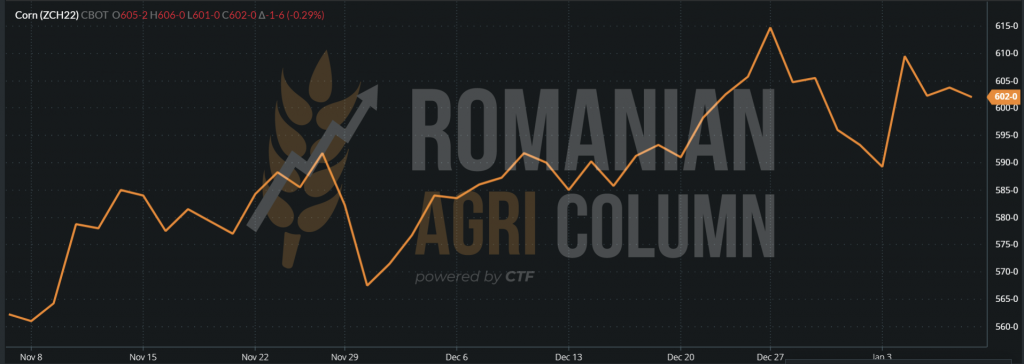

For these reasons, CBOT remains above 600 c/bu.

CORN – CBOT ZCH22 – 602 c/bu

CBOT ZCH22 CORN GRAPH

CORN PRICES IN DIFFERENT ORIGINS:

ANALYSIS

- Corn keeps its price stable in the Black Sea basin due to the accumulation of South American factors.

- The American story is just beginning, new updates will not hesitate to appear.

- Will WASDE fix this issue on January 12? We don’t know, but we hope they will at least partially do so

LOCALLY

Rapeseed is actually marching in search of liquidity, because the quotations we see these days are nothing more than the effect of an uncovered demand, of a drama unfolding some time ago in Canada due to the drought.

Rapeseed sown in autumn is in satisfactory condition locally. The soil water supply supports the current state of hibernation or “dormancy”. Indeed, there are still areas with unseen or uneven emergent rapeseed, but we have become accustomed to this phenomenon and have certified for many years that in February rapeseed emerged and developed accordingly, producing the expected harvest.

REGIONALLY

Russia and Ukraine are doing very well in terms of rapeseed crops. The water supply in the soil, even if not satisfactory in all areas, is ensured by the snow that covered the plains.

The European Union also has a good rapeseed crop. The reserve of water in the soil allows the development that will follow in the spring, and the water that will come from the snows that cover or will cover the plains during the winter will contribute to the volume of the reserve.

GLOBALLY

The levels we observe are not realistic at all, if we compare FEB22 correctly with AUG22. The difference or the inverse crop is 241 EUR, a level that has nothing to do with reality in any form.

Rapeseed has a fairly limited volume, and demand is strong. The European Union produces 17 million tons, and Canada was supposed to produce 21 million tons, but it ended up at 12.7 million tons. Russia produced just over 3 million tons, identical to Ukraine. India exceeded the forecast of 8.8 million tons, reaching a level of 11 million tons. Australia also scored an additional 700,000 tons. So the Canadian deficit was not covered in any way and so we came to the prices that we see displayed.

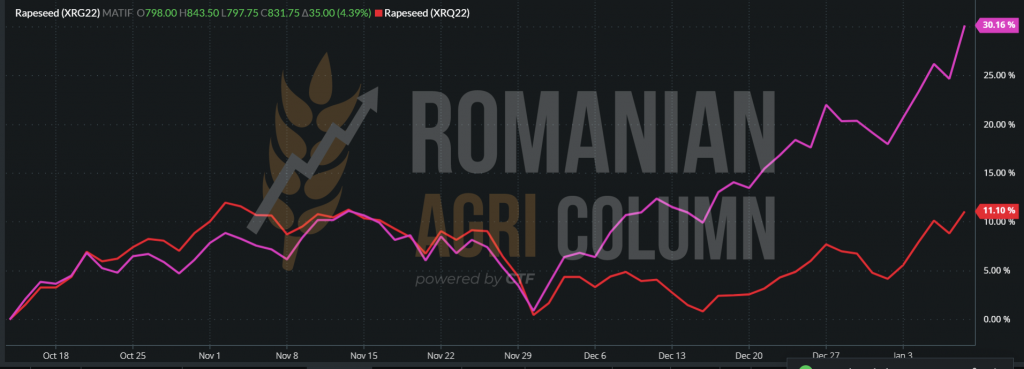

EURONEXT XRG22 831.75 EUR vs. XRQ22 590 EUR = 241 EUR DIFFERENCE

FEB22 vs. XRQ22 AUG 22 XRG22 COMPARISON. XRG22 increases by 30%, while XRQ22 increases by 11%:

CANOLA subsequently reacts identically: +14 CAD RSH22

ANALYSIS

- The new rapeseed crop must be carefully engaged in forward contracts.

- The production potential and, in particular, the pricing method must be taken into account.

- There are several working methods in setting the price of rapeseed crop and Romanian farmers can call on our advice in this regard.

Indications of sunflower seeds have revived immediately after the holidays. Their price reached the level of 630-640 USD/MT in the CPT Constanța parity, with an elasticity of 10 USD/MT in the case of a buyer who wants lots in a more aggressive way.

Romanian processors display the same purchase prices as the port of Constanța. The commodity is starting to disappear and it will certainly be a competition between exports and the domestic market.

Odessa crude oil prices are high in these first days of the year due to the level of coverage of processors. The latter have January covered in terms of processing, but Ukrainian farmers do not want to sell at these levels. Thus, the processors increase the price quotations of crude oil in ASK to the level of 1,400 USD/MT FOB Odessa, while the buyers are positioned at 1,350 USD/MT.

Subsequently, the FEB22 indications also increased by 20 USD/MT at ASK, up to 1,390 USD/MT, while the BID of the buyers is located at 1,330 USD/MT.

Turkey is currently in terms of raw material prices at 710-720 USD/MT CIF Marmara. If we estimate a transport cost from Constanța at the maximum level of 35-40 USD/MT (although it can be a little lower), we reach a FOB Constanța level of 670-680 USD/MT, with the exporter’s margin included.

From Monday, January 10, 2022, we will see Ukraine in the market. They will end the holiday season and thus begin the formation of the sunflower oil market and, implicitly, the seed market at regional level. However, we notice the increase in the price of raw materials or the purchase attempt by about 200-400 UAH/MT, equivalent to 7-15 USD/MT.

Unexpectedly, a support for the price of oil comes from a colleague from the complex called soy, who, due to the problems encountered in South America and which we will see in the chapter dedicated to soybeans, supports the raw material from which the oil is made.

Let us not neglect also the European Union, which through its cultural tradition consumes sunflower oil and which will intensely seek to originate goods from Romania. And we are not only referring to the traditional partners in France, the Netherlands, Spain, but also to the neighbors with processing units very close to the Romanian border, in this case Hungary and Bulgaria.

PRICES INDICATIONS OF ORIGIN OF OILSEEDS:

Soybean indications in Romania are extremely low in value. Buyers are beginning to estimate their sales potential locally and there are no signs of agreement between the local market and what is happening on the mainland, of course talking about South America. Romanian processors have no interest in buying soybeans and the estimate is that they are covered for their processing needs. We understand from this that the destinations (buyers) relied heavily on the South American crop, as did everyone else.

But, unfortunately, things are not going well in Brazil. Brazilian soybeans lose their potential almost daily due to lack of water in the south of the country. Thus, we have an estimate of 133-131 million tons as harvest volume, compared to the initial 142-144 million tons, according to USDA and CONAB.

So soybeans have support because of these events generated by La Nina, the second consecutive year with problems in South America. And the story is not over yet. Next is the freshly finished Argentine soybean.

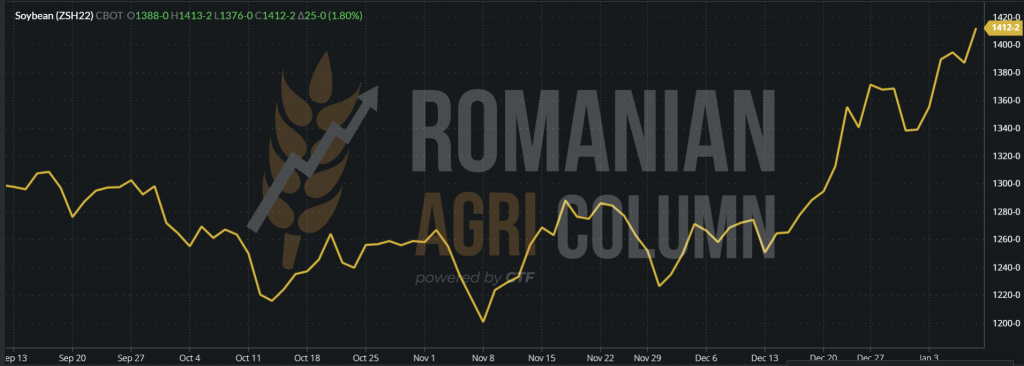

CBOT ZSH22 exceeds the threshold of 1,400 c/bu (1412 c/bu + 24 c/bu)

ZSH22 SOYBEAN CBOT GRAPH

ANALYSIS

- WEATHER MARKET or Mother Nature shows us who decides. If some time ago everyone was relaxed and soy had very low quotations, within 2 weeks, things changed radically.

- SOY also supports the rest of the oilseeds in the complex. Let’s not forget that Malaysia has losses in production due to rains and lack of staff on the plantations, generated by COVID restrictions. As a result, workers in Pakistan, Bangladesh and India are no longer arriving in Malaysia.

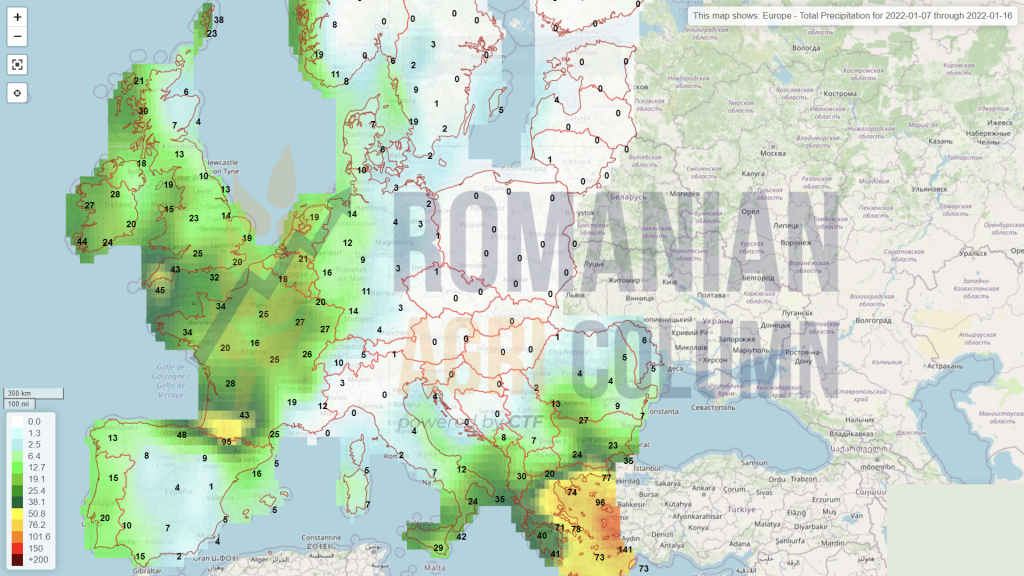

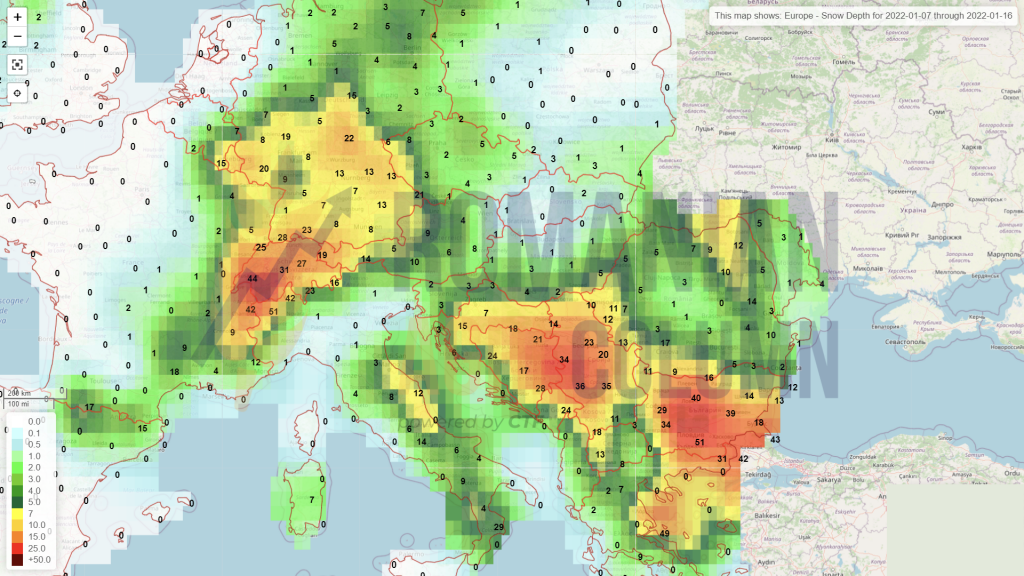

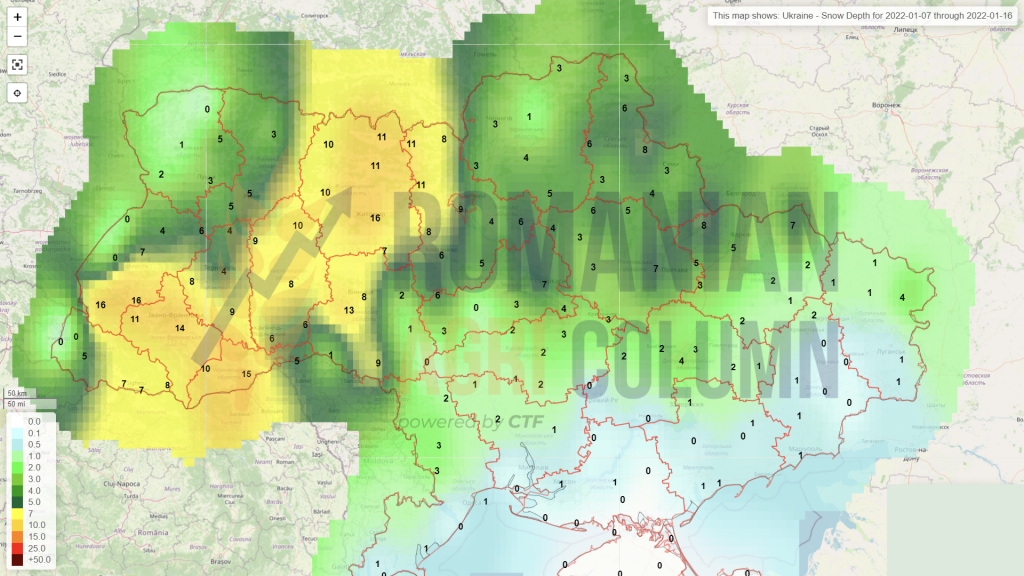

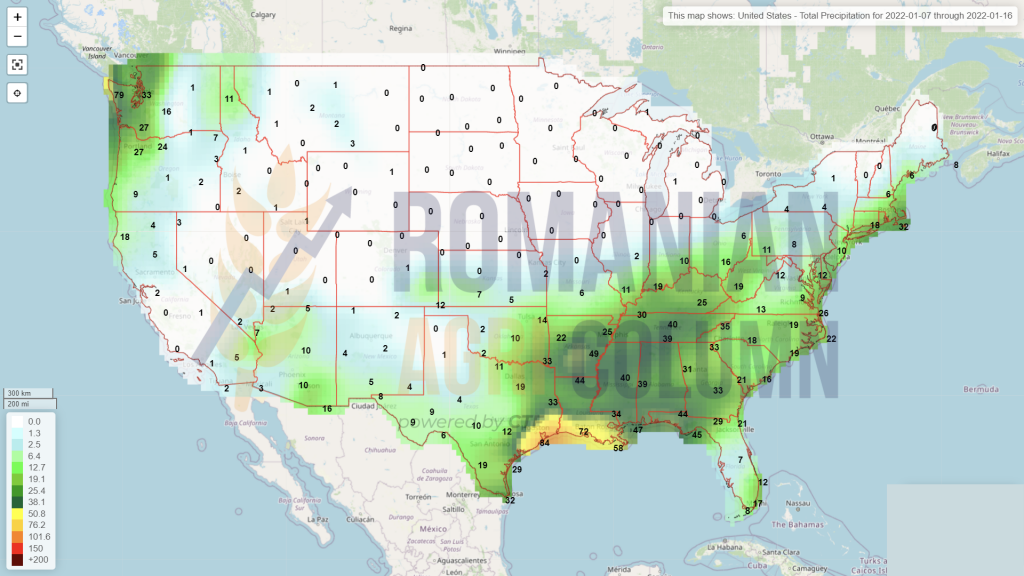

7-16 January 2022

Romania (rain)

Romania (snow)

Serbia (snow)

Europe (rain)

Europe (snow)

Russia (snow)

Ukraine (snow)

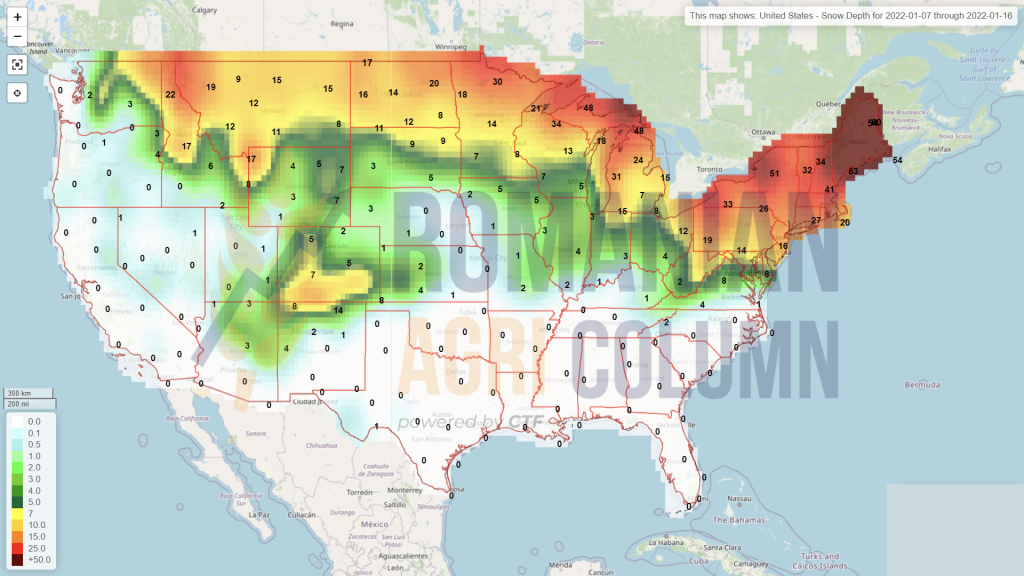

USA (rain)

USA (snow)

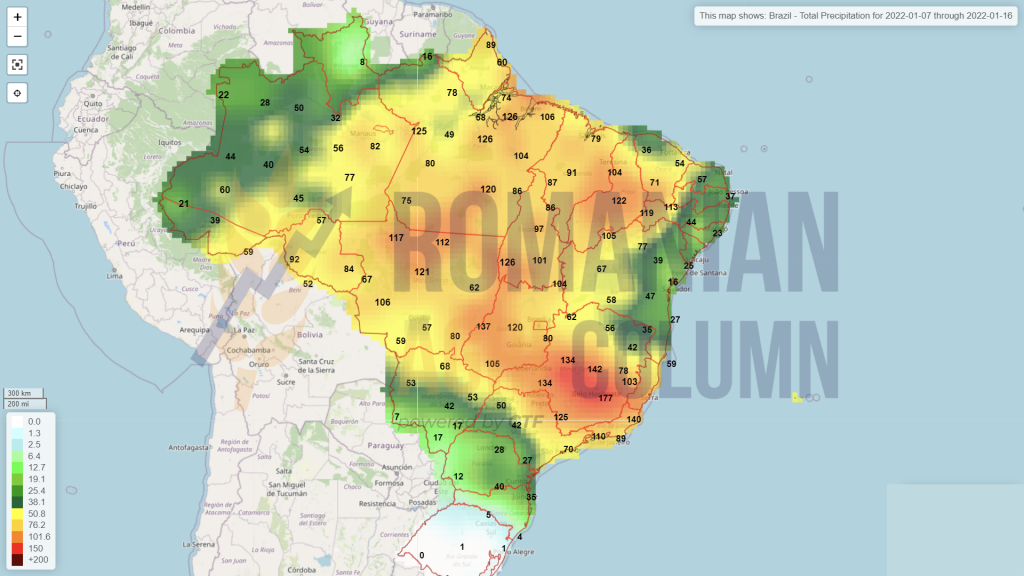

Brazil

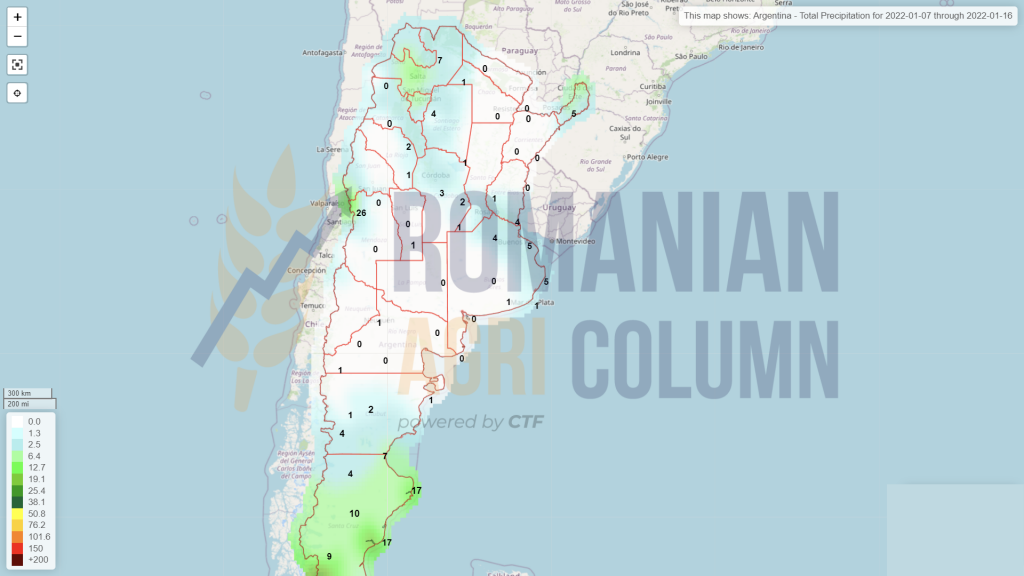

Argentina (lack of precipitaions)

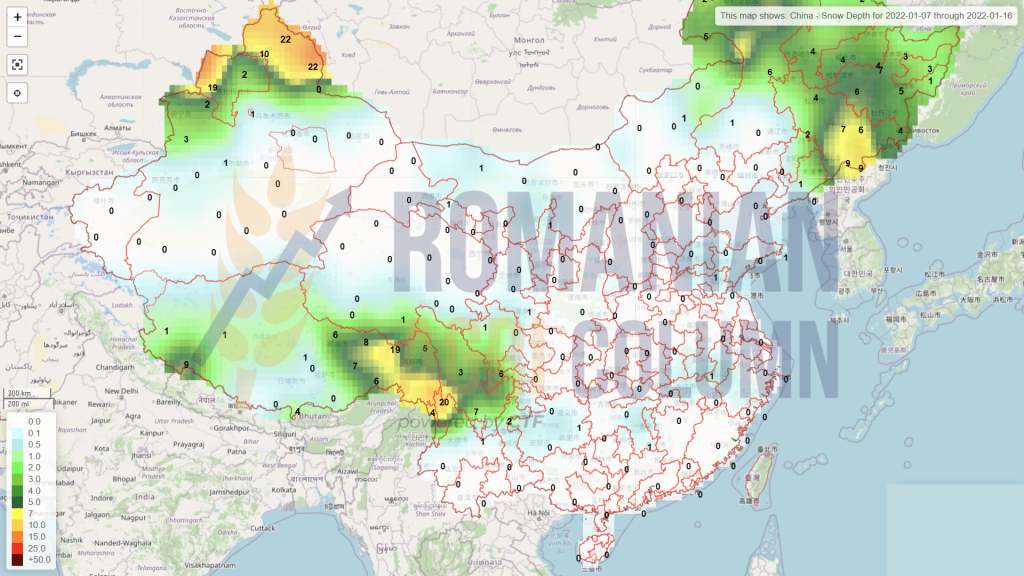

China (snow)