This week’s market report provides information on:

LOCALLY

In the last week, the indications of wheat in the CPT Constanța parity have deteriorated to the level of 258-262 EUR/MT, amid the partial easing of the political situation in the Black Sea basin. Thus, the destinations have relaxed and understood that abundance in the pool is a key factor in trading in the near future. The price of feed wheat also decreases, consequently, by about 11-12 EUR/MT compared to the level indicated for the milling specification.

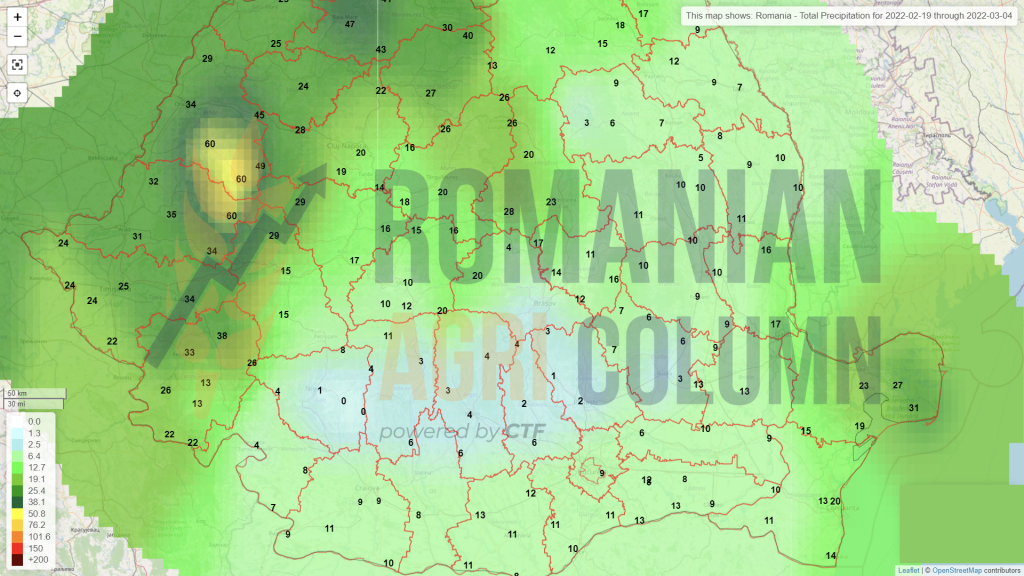

The indicative price levels for the new wheat crop remain at 235 EUR/MT, minus 8 EUR/MT for the feed quality. However, at this moment, Romania is not forecast with abundant rainfall, which could compensate the water deficit. There are certain levels of precipitation in the form of rain and snow in some areas towards the end of February, which would partially create a minimum level of comfort.

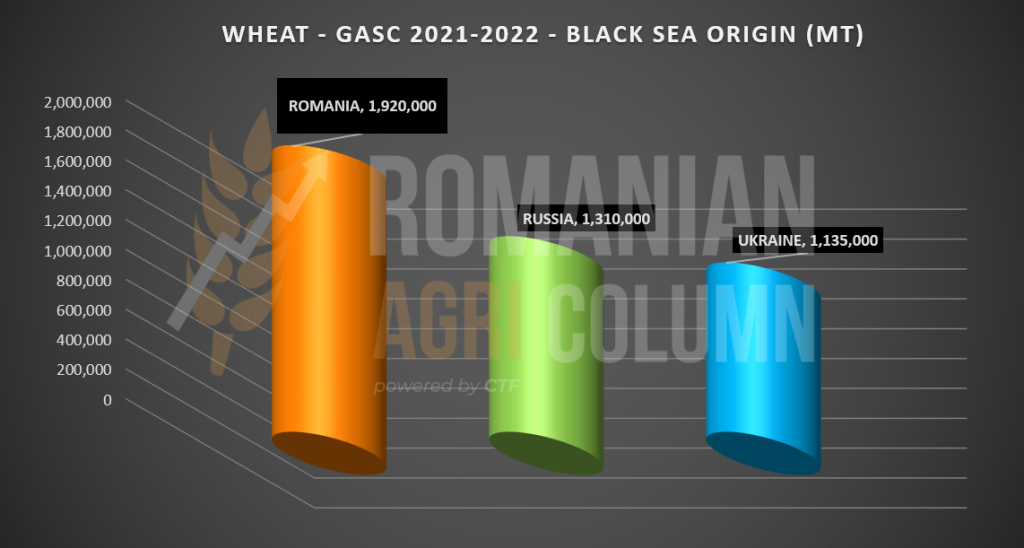

On this background of partial relaxation, we note the GASC Egypt tender, which gives 100% profit to Romanian wheat. Out of a total of 22 participants and a volume of 1.32 million tons displayed, Romania wins all three lots purchased by GASC, i.e., 180,000 tons. The price at which the lot was purchased is 318 USD/MT in the parity of FOB Constanța, equivalent to 338.55 USD/MT C&F. The purchase price is 8.34 USD/MT lower than in the previous auction.

Romania thus becomes the Power Factory in the supply of wheat to the GASC entity, with a total level of 1.92 million tons, leading the sales of wheat to Egypt made through GASC in the Black Sea basin.

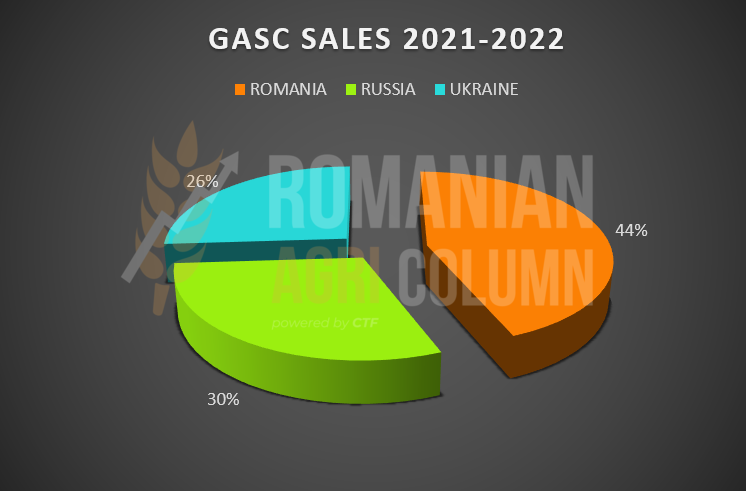

At this moment, counting the three countries, Romania, Russia and Ukraine, we note the level of market share of each in the destination Egypt (sales made through GASC):

- Romania – 44%

- Russia – 30%

- Ukraine 26%

REGIONALLY

At the regional level, we note the state of vegetation of the crops in the Black Sea basin which are in a very good condition at the moment.

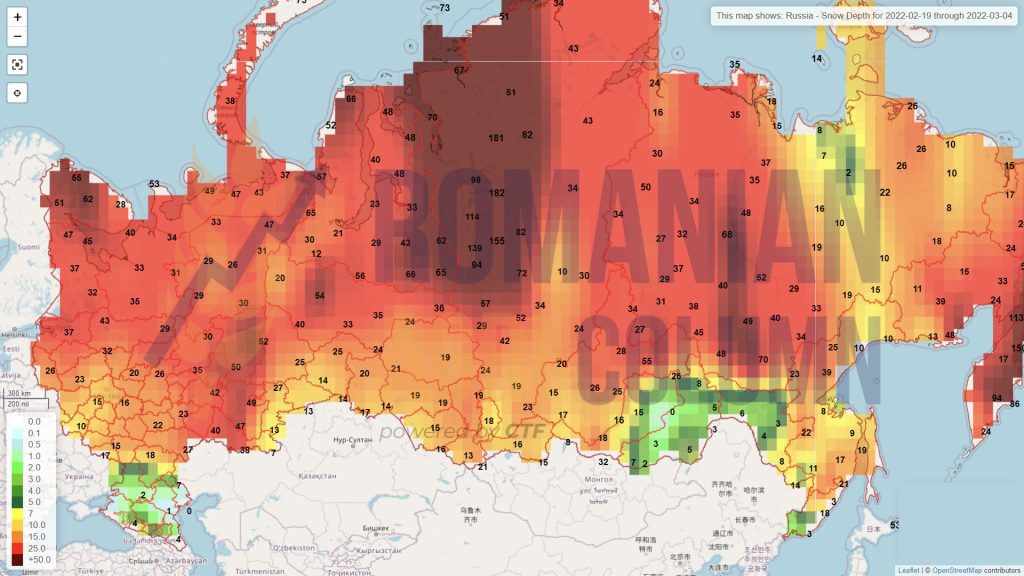

Indications in Russia already show a forecast of 84 million tons of wheat in the 2022-2023 season, with a rainfall regime that has been a water reserve above normal in many areas, such as the Volga region and the Central Plains.

Ukraine also has a very good status at the moment, which indicates a high potential for the future wheat crop.

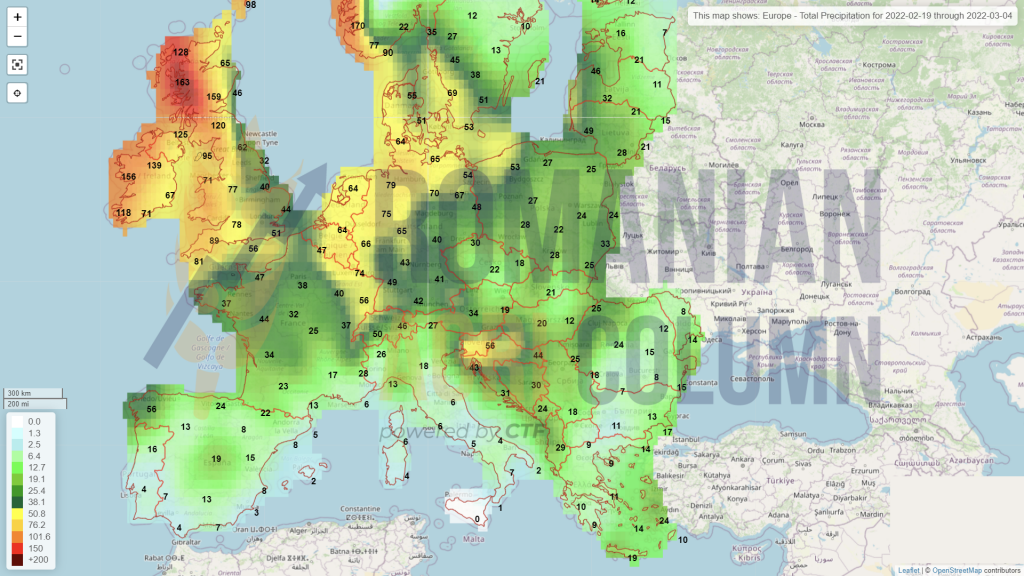

The European Union is keeping its crop forecast status unchanged at this time. Things will become much clearer in terms of potential in the coming weeks. Rainfall problems remain the same as before in the same areas of the EU, but a normal regime in March could put things back on track.

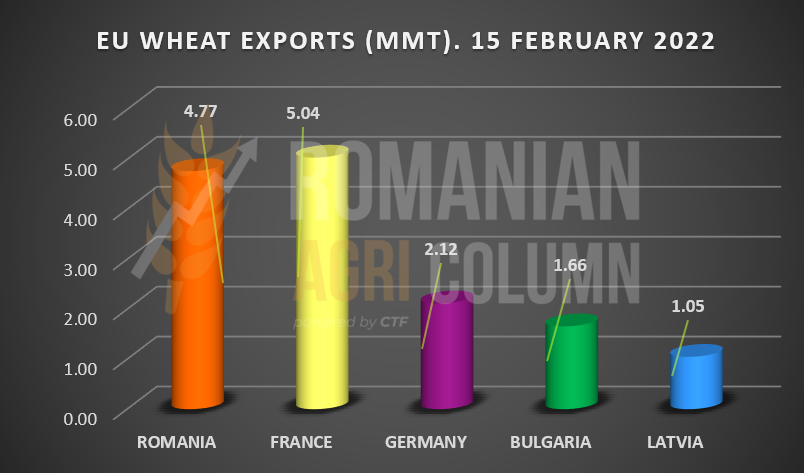

Against this background, we also note the level of exports of Romania, which stood at 4.77 million tons on February 15, 2022. At European level, Romania and France together have a cumulative level of 9.81 million tons, out of a total of 17.27 million tons of wheat exports.

The Algerian state has purchased through OAIC between 300,000-500,000 tons of milling wheat, with optional origin, South America, Australia and the Black Sea basin. The prices engaged in the tender are at the level of 345.5-346.5 USD/MT in the C&F parity. However, the Black Sea basin is expected to be a major supplier in this closed auction.

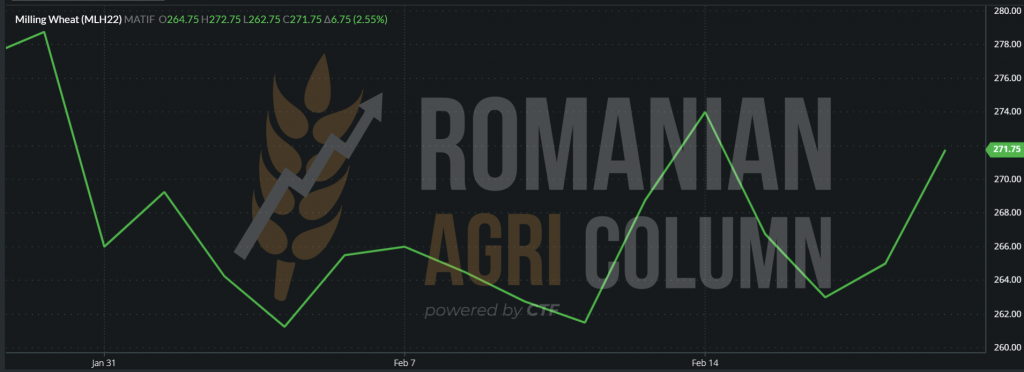

At the stock market level, we are waiting for the start of liquidation of investment fund positions. We are fast approaching the end of February and, implicitly, the downward movements of the stock market indications of MAR22. The correlation with the physical market will exist due to the volumes in the Black Sea basin and thus, the funds will leave the net long positions at the end of February.

And so begins the episode of Profit Taking. EURONEXT – 18 February 2022 – MLH22 MAR22 – 270 EUR

GLOBALLY

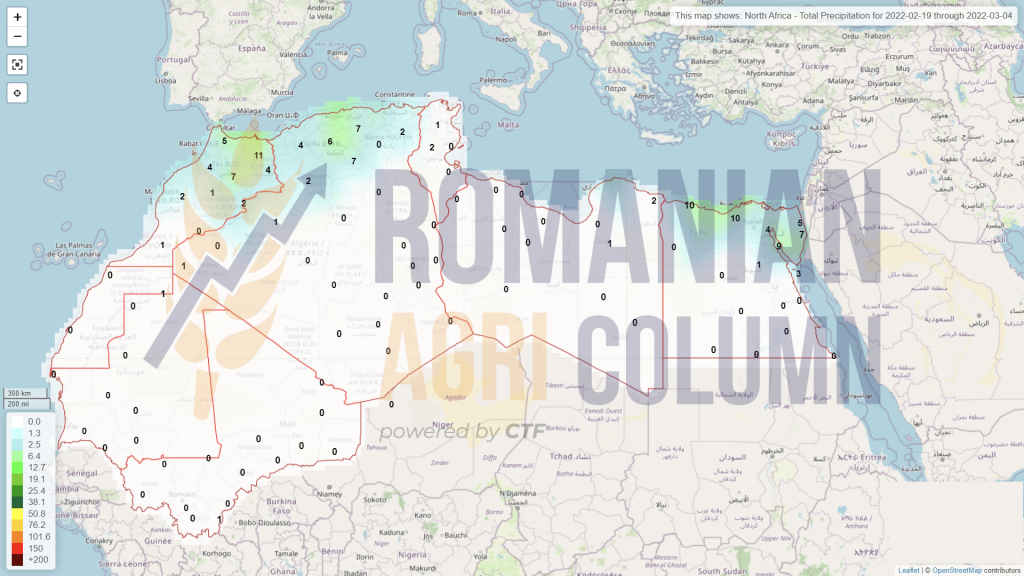

We start with Morocco, which is going through the most severe drought in the last 30 years, and the premises are not the best. There will certainly be a disastrous season for this North African country.

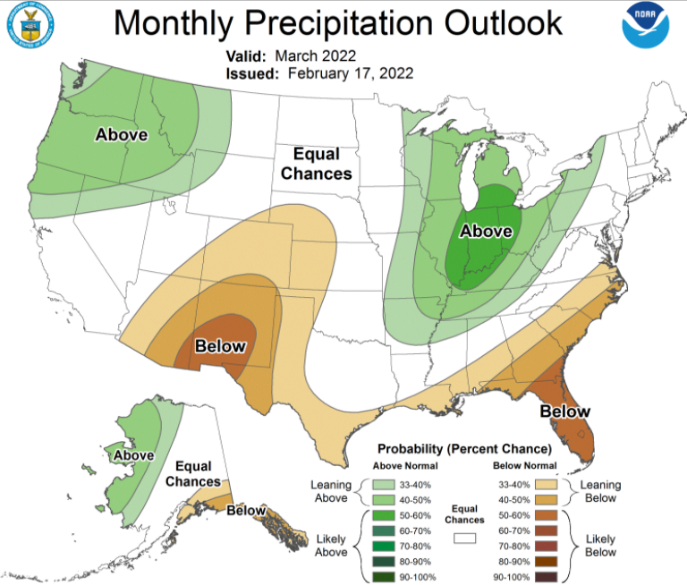

Globally, we are closely monitoring the future wheat crop in the United States, and here we are seeing a shortage of water in the soil in the south of the Central Plains. This will impact future crop yields if continued. The US has a deficit of rainfall and it will continue in the south of the Central Plains in March 2022.

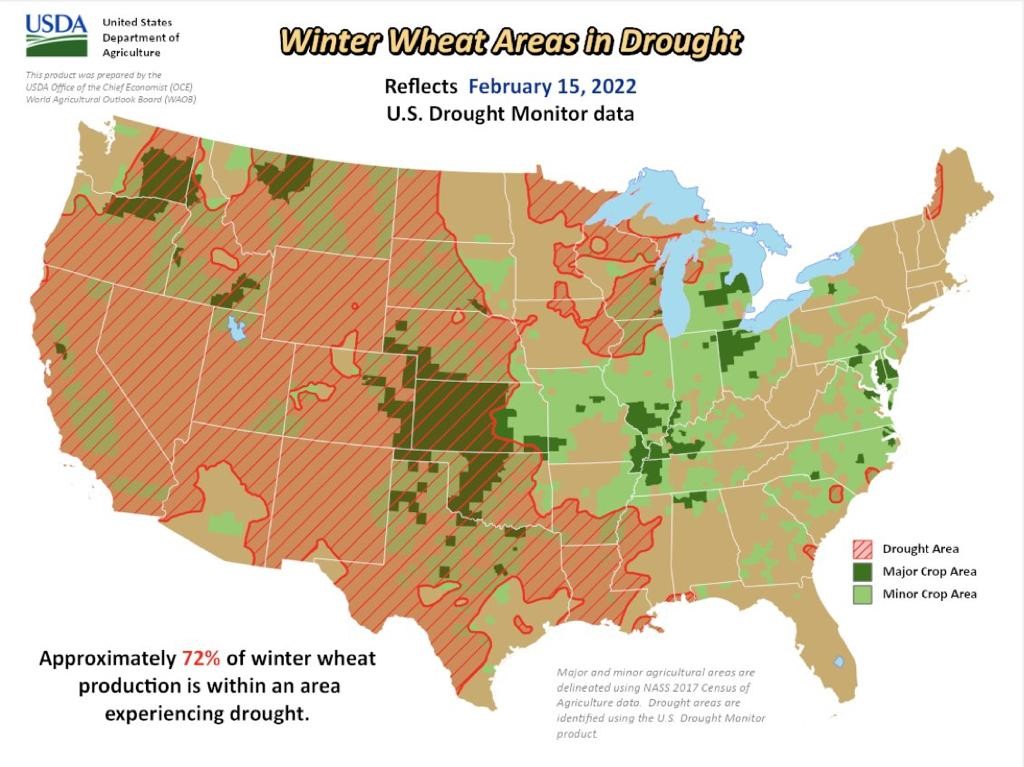

NOAA (North Oceanic Atmospheric Association) indicates a deficit of rainfall in areas cultivated with wheat. Combined with what we noted in the previous issue (reduced number of hectares planted with spring wheat due to the change in favor of soybeans and maize), there is a lower potential than the multiannual average. The USDA also indicates a level of 72% of winter wheat in drought-affected areas.

Australia is reviewing its wheat production from 34 to 39 million tons, and this review will certainly be certified by the forthcoming WASDE report. It is an increase in production (revision) that will impact global trade and, implicitly, reduce the price of wheat. However, at this time, it is only a local estimate, which is not guaranteed by the USDA.

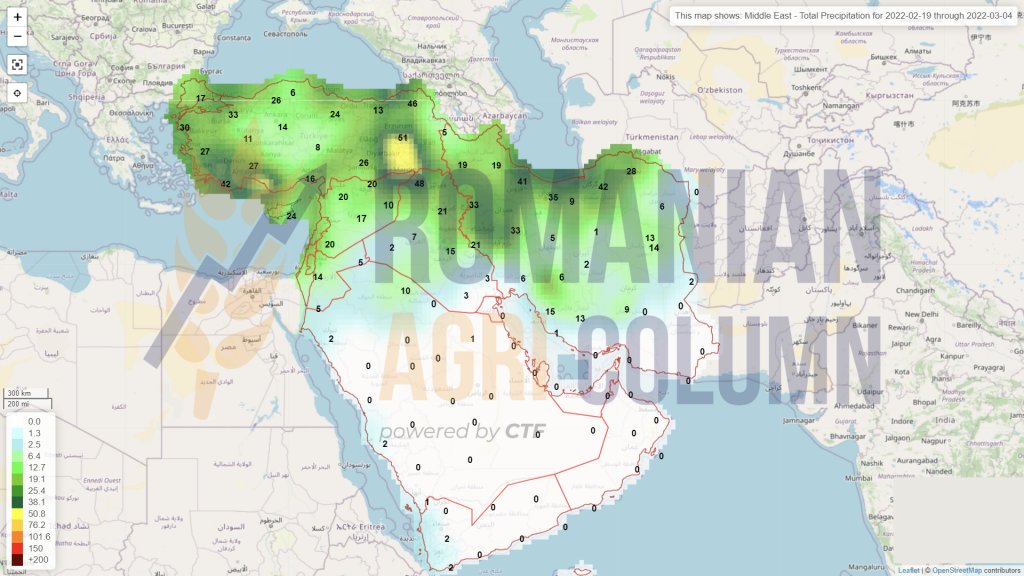

Wheat imports into the Middle East are expected to increase by 38% year-on-year to 4.6 million tons in 2022. At the same time, countries in North Africa, the world’s largest wheat-importing region, will see significantly higher grain imports as droughts reduce domestic production. Any interruption in exports from Ukraine or Russia would increase competition for wheat supply, already at its lowest level in recent years, from other major exporters, including the EU, Australia and North America. Middle Eastern countries rely heavily on wheat imports, especially in years of low production. Wheat comes mainly from the EU, Russia, Ukraine and Kazakhstan. Russia has already capped its wheat exports with an export quota that runs from February 15 to the end of June. Russia has also imposed a variable-rate export tax on wheat, adopted in June last year, which has reduced grain exports from year to year. Iran, the largest wheat producer in the Middle East, expects production to fall by 20% this year to 12 million tons due to the drought, which is 17% below the average for the past 5 years. Meanwhile, wheat fields in neighboring Iraq are also suffering from “severe” drought, while Syrian wheat regions are experiencing “extreme” levels of drought.

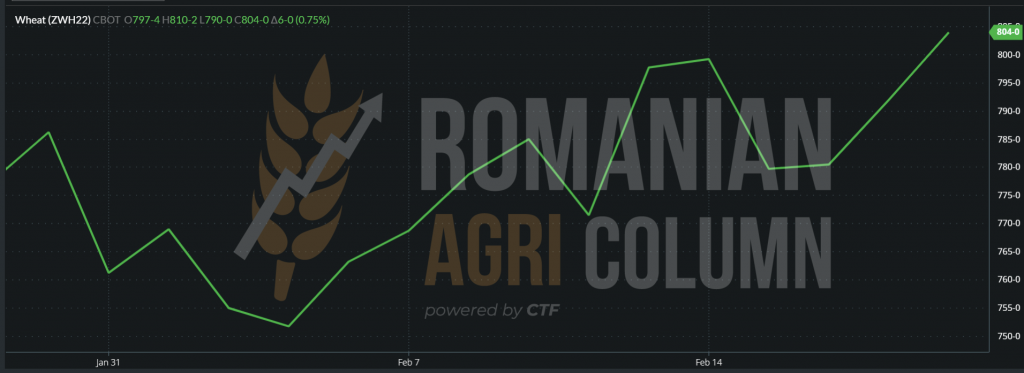

CBOT February 18, 2022. The same Profit Taking action at the CBOT level. ZWH22 MAR22 = 804 c/bu (+6 c/bu)

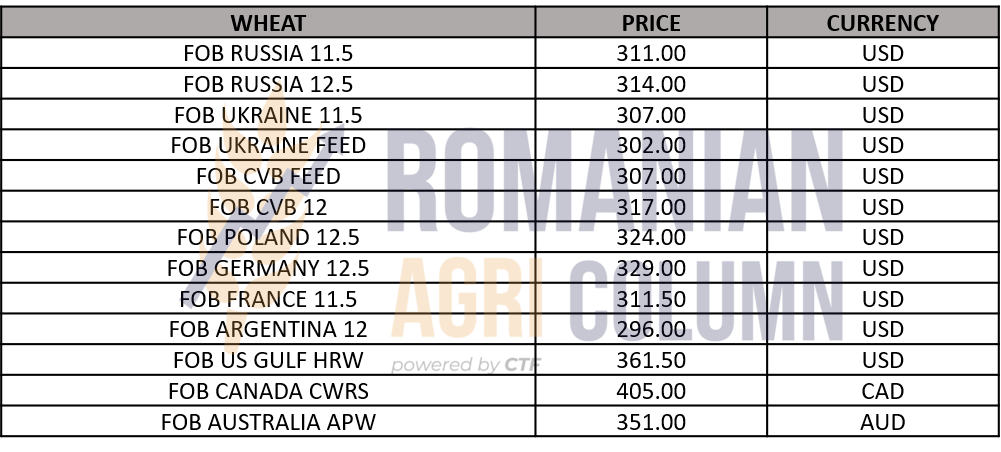

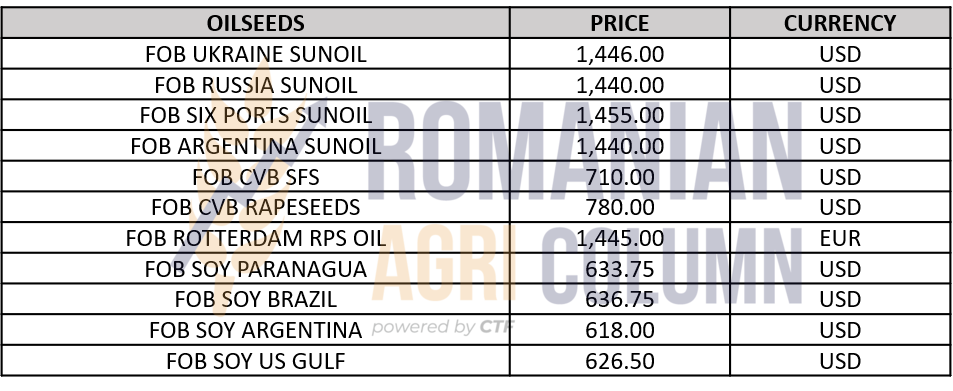

PRICE INDICATIONS IN VARIOUS ORIGINS

ANALYSIS

- The volumes are abundant in the Black Sea basin.

- Tension seems to be at an average level these days, but we do not rule out a military response from Russia after February 20, 2022, a way in which the fundamentals of the market are changing, due to the political factor.

- Australia raises the wheat crop estimate by 5 million tons, but this is not certified. In the March WASDE report we may see an upgrade, but maybe not 5 million tons…

- IGC keeps world wheat production unchanged at 781 million tons.

- Funds perform net long or roll-over positions where they feel there is potential.

LOCALLY

The market is in an unchanged status with the old crop barley. The price indications remain at the level of 250 EUR/MT in the CPT Constanța parity, while the new barley crop is indicated at the levels of 212-218 EUR/MT.

REGIONALLY

Unchanged status of barley crop in the Black Sea basin and in the European Union.

GLOBALLY

Out of season.

LOCALLY

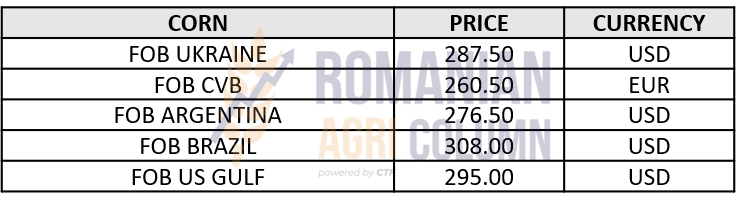

The indications of corn in the CPT Constanța parity are reconsolidating around 250 EUR/MT. The moderation of tensions in the Black Sea basin is increasing trade efforts in the region in the event of a conflict that would disrupt trade in the area.

At this moment, Romania has reached the level of 3 million tons of corn exports in the 2021-2022 season. The sowing forecast for 2022 is 2.63 million hectares.

REGIONALLY

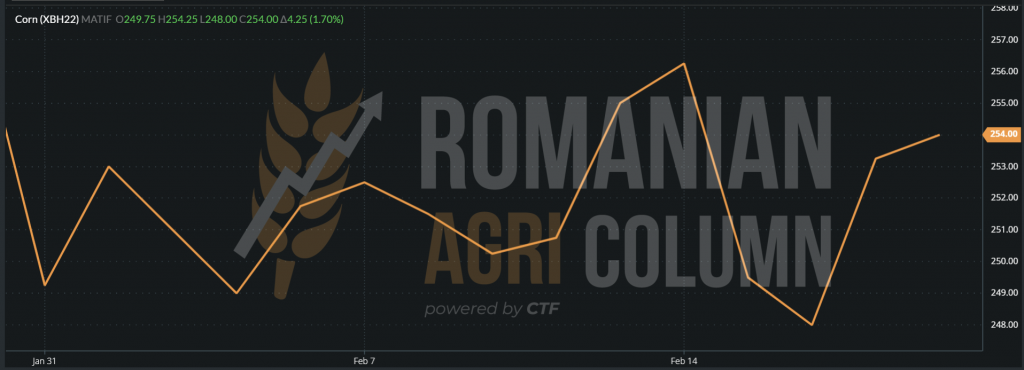

At the regional level, we observe the same context as in the case of wheat. We refer to EURONEXT, which indicates a closing level of 254 EUR XBH22 MAR22. The funds will make a profit taking or roll-over by the end of February 2022.

EURONEXT – 18 February 2022 – XBH22 MAR22 (+4.25 EUR)

The correlation in the physical market is due to the life cycle of the price of corn, fueled by the state of South American crops and the support from Asian demand for corn.

We estimate for Monday, February 21, 2022, a level of 252-253 EUR/MT CPT Constanța.

GRAPHIC EURONEXT XBH22 MAR22

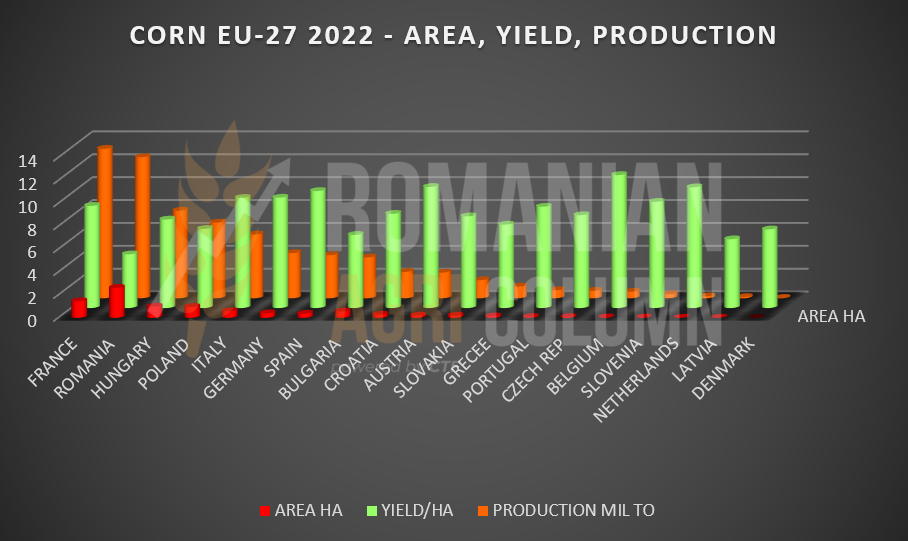

In the 2022 crop plan, we have a planting forecast at European Union level that contains the areas projected to be sown, productivity per hectare, as well as the estimated production level for each European Union country.

As can be seen, there are large discrepancies in the level of production per hectare between EU countries and the most obvious is between France and Romania. France has a yield per hectare of 8.93 tons, while Romania has only 4.7 tons/ha, given that France sows 1.46 million ha, and Romania 2.63 million ha.

GLOBALLY

The problems persist in South America in Brazil, and now Argentina follows. Crop rating agencies are already showing a drop of 2-3 million tons, so things seem to be certain regarding the degradation of the Argentine crop. This decrease actually supports the global price level of maize, with Brazil forecasting a total of 113 million tons, compared to an initial estimate of 120 million tons, and Argentina with a downgraded level of 51 million tons, compared to of 54 million initial tons, to which we also add Paraguay, which in turn suffers from depreciation, we have a clear picture of the support in the life cycle of corn.

In Argentina, no rain is expected next week, which can only further damage the corn crop. Thus, the support can continue in terms of price level.

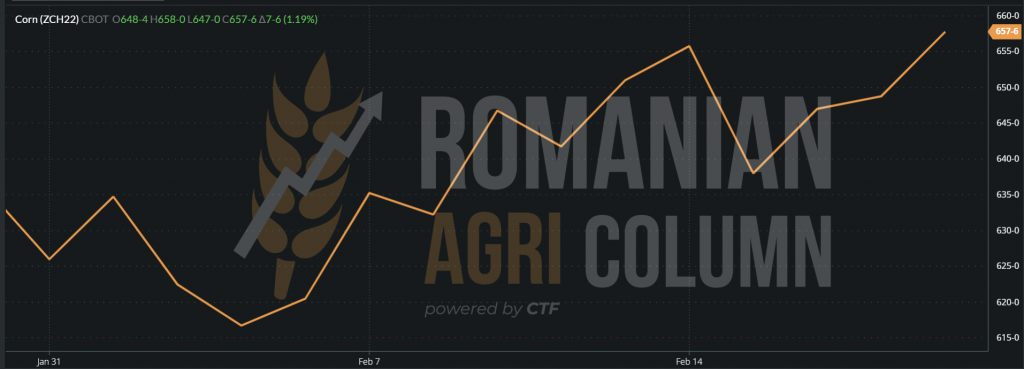

But we expect, as in the case of wheat, a massive sell-off of funds in the coming days, as the level of trading and net long positions of investment funds indicate this. The indications of American corn have increased, as we forecast, their level currently indicating 657 c/bu.

CBOT ZCH22 MAR22 – 657 c/bu (+7 c/bu)

ZCH22 MAR22 CORN GRAPHIC

CORN INDICATIONS IN MAIN ORIGINS

ANALYSIS

- The Black Sea basin is generating short-term support due to local political uncertainty.

- South America generates the same support, due to the weather factor.

- Funds generate large movements in order to make a profit taking or roll-over.

LOCALLY

The Romanian rapeseed crop is under good auspices at the moment. Production forecasts are at a normal level during this period and the 417,000 hectares are expected to come out of winter under normal conditions.

Quotations for the new crop have not changed. The indication AUG22 minus 5 or 10 EUR/MT, depending on the place of delivery, Processor or CPT Constanța, remains unchanged for this period of time.

REGIONALLY

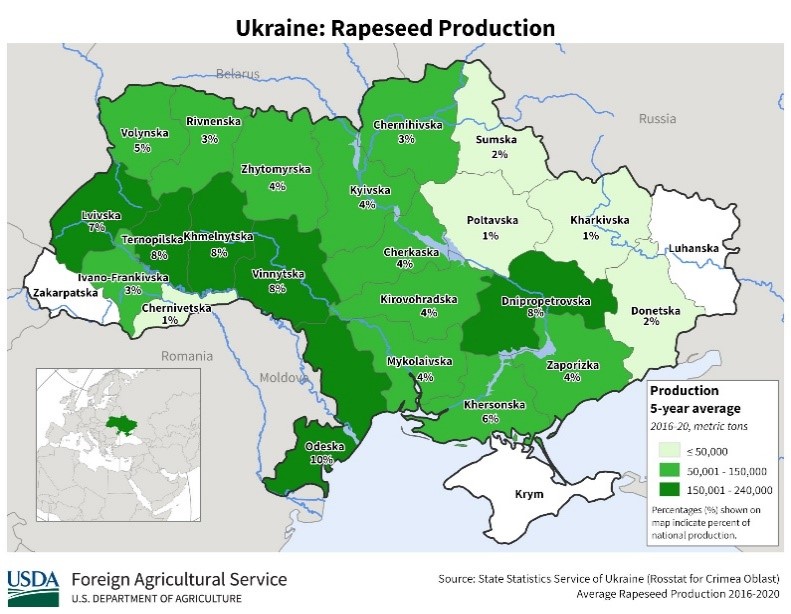

The estimated crop forecasts for Ukraine indicate a productivity level per hectare of 3 tons, which would lead to a production level of 3 million tons, taking into account the 1 million hectares sown with rapeseed in autumn.

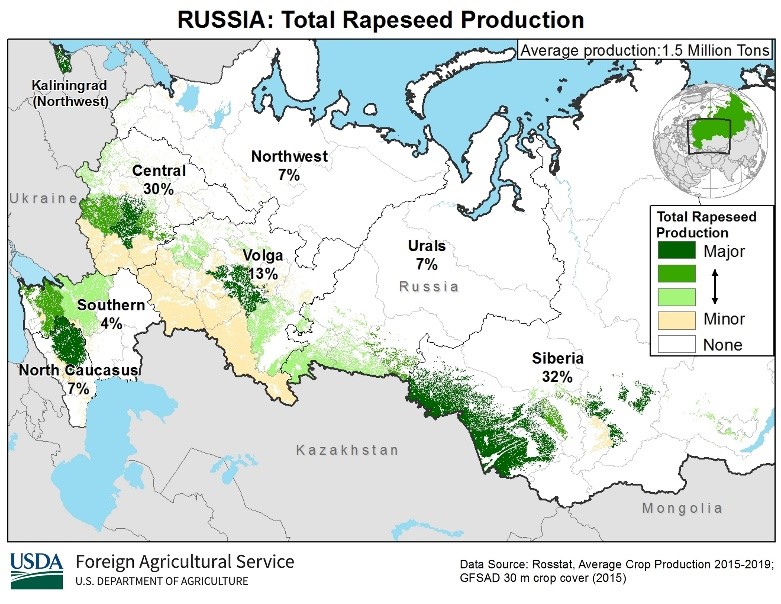

Russia, with 1.6 million hectares, is approaching the production level of 2.8 million tons. The crop is under favorable auspices at this time, and the winter outing will be beneficial, with water reserves in the soil. Productivity is at the level of 1.75 tons/hectare.

Graphic source: USDA

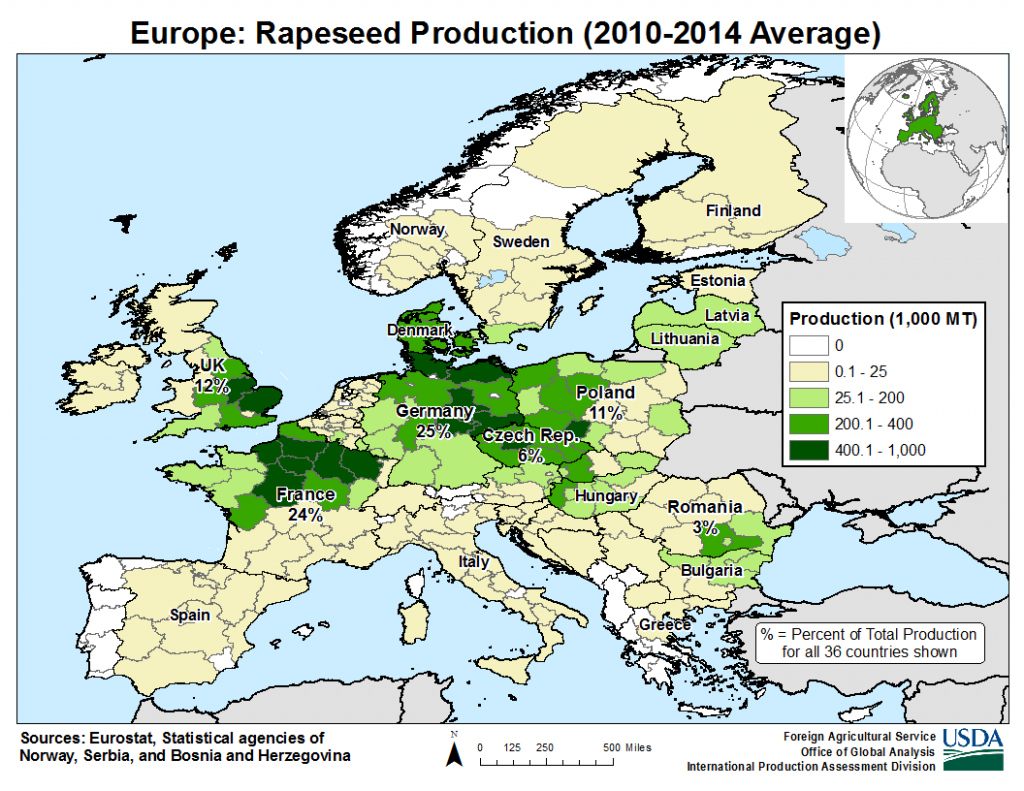

EU27 rapeseed production will reach 17 million tons during 2021-2022, up just 1.8% from the 2020-2021 crop, which was severely affected by dry autumn weather and heavy rains and floods. lightning during spring. This year’s increase is, first of all, the result of the anticipated production increases in Romania. Bulgaria, Denmark, Lithuania and Poland, which are expected to offset the reductions in other Member States.

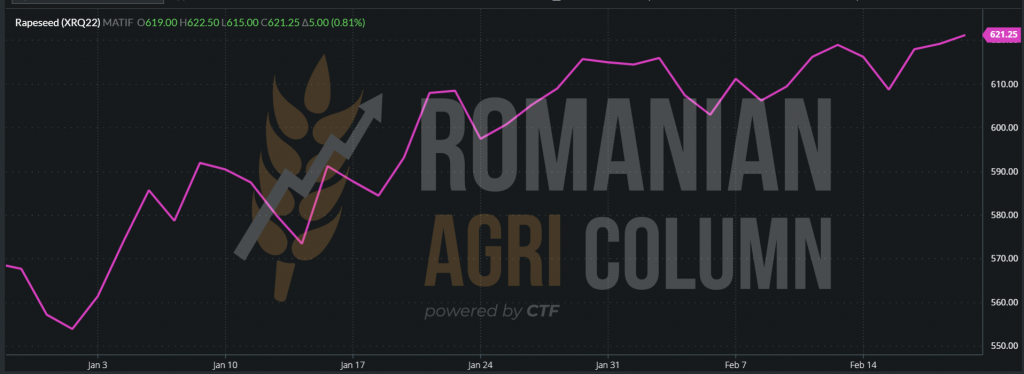

EURONEXT quotes rapeseed at the close of 18 February 2022 at 621 EUR, a clear signal of demand for the new crop. Our previous estimates led to a level of 625-630 EUR/MT, but it is only a matter of time. Rapeseed has support. Even though the price of oil fell initially, it returned to 93.39 USD/barrel in Brent.

EURONEXT XRQ22 AUG22 – 621.25 EUR (+5 EUR)

EURONEXT XRQ22 AUG22 RAPESEED GRAPHIC

GLOBALLY

Canada and Australia are out of season. The sowing season begins in April.

RSK22 MAY22 CANOLA INDICATIONS (+6.2 CAD)

ANALYSIS

- The rapeseed crop is under good auspices in the Black Sea basin.

- The Romanian rapeseed crop is promising.

- The European rapeseed crop is in very good condition.

- Support remains for the new crop, with the 620 EUR level exceeded, as we estimated. The next threshold is 625-630 EUR.

LOCALLY

The local market of sunflower seeds has experienced an increase in terms of indications in the parities of CPT Constanța or DAP Processor. Thus, the level of 280-285 USD/MT is a daily indicator for sellers. The demand is constant, and the price indications in the FOB Constanța parity remain at the level of 707 USD/MT.

REGIONALLY

Odessa crude oil prices rise to 1,445 USD/MT. Ukraine exported 2.65 million tons of sunflower oil between September and January 2021-2022, which almost equaled the volume delivered for the same period last season. In addition, it was 5% higher than the same period in 2019-2020, which was the record season for the export of sunflower oil (6.63 million tons).

Russia, on the other hand, did not reach the forecast level of 4.08 million tons of crude oil exports, currently reaching only 1.2 million tons. The logistics infrastructure does not allow this deficit to be recovered, even if the processing power is normal, as the port facilities in Taman and Tuapse are not designed for transboarding and loading of crude oil at high speed.

Today’s price level is the combined result of farmers in Russia, Ukraine and Romania, who have only sold sunflower seeds in very small lots, preferring to sell wheat and corn due to very good crops. The lots of sunflower seeds sold, even in small volumes, generated the cash flow needed on farms to support current expenses and maturities.

The price level also increases in Hungary around 720 USD/MT, goods delivered to factories near the Romanian-Hungarian border.

OILSEEDS PRICE INDICATIONS IN VARIOUS ORIGINS

ANALYSIS

- Price dynamics are maintained for sunflower seeds.

- The correlation between the refusal to sell by farmers in the Black Sea basin has led to an increase in the price level, even in the condition of a rich crop.

LOCALLY + REGIONALLY

Domestic processors have an indication of 630 USD/MT for soybeans, plus coupled support per hectare. Thus, the level can reach 680 USD/MT.

Processors in Hungary are covered for March, and the indicative price level is similar to that in Romania (coupled support included).

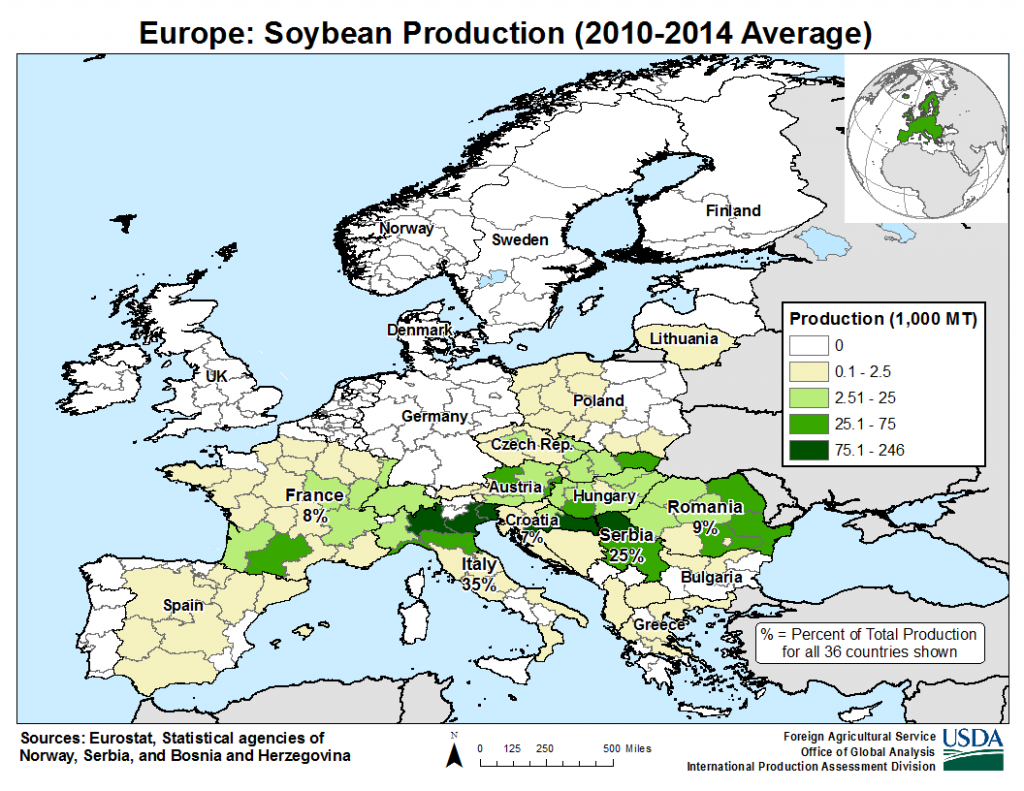

At European level, 2.75 million tons were produced, Romania having a share of 9% of the total, i.e., around 247,500 tons.

Chart source: USDA

GLOBALLY

We are now going overseas and assessing the problems of South America. Brazil is degraded to 133 million tons, as we all know. But Brazil Agroconsult further degrades the crop, to the level of 125 million tons, which means a gap of 17 million tons compared to the initial estimate of 142 million.

But, like a ghost, follows Argentina, a country that has also suffered from a lack of rainfall, and is now eagerly awaiting the degradation of the soybean crop. Estimates say a minimum of 2 million tons, which would lead to a crop level of 45-46 million tons. Moreover, the two countries will have to supply Paraguay with soybeans to meet the need for processing.

China, on the other hand, announces the possibility of giving up an important level of imports, namely 30 million tons of soybeans. This volume is extremely important, given that China imports 100-102 million tons annually. We are talking here about a reduced level of imports by 33%. China also announces that it has increased the level of pork production by 15%, which could lead to a certain reduction in imports. However, let us not neglect the Chinese trade commitments, Trade Deal, which have not been fulfilled in relation to the USA. This needs to be strengthened in the coming period by imports from North America.

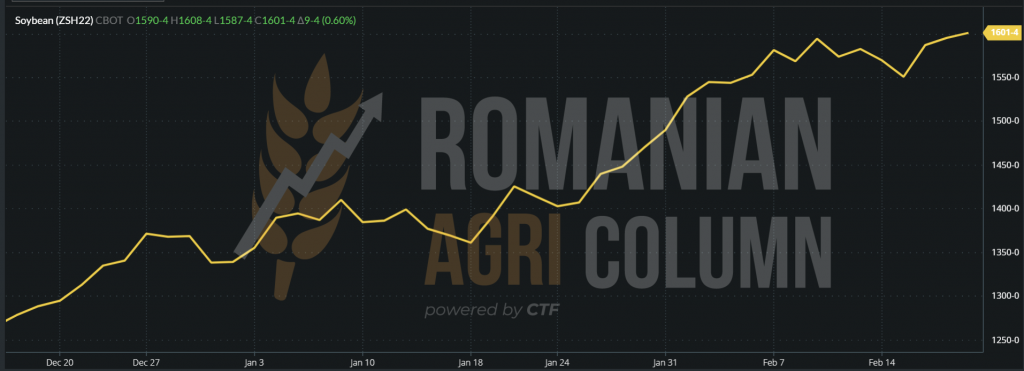

CBOT – 18-19 February 2022 – ZSH22 MAR22 – 1,601 c/bu (+9 c/bu). We are waiting for a sell-off for soybeans.

CBOT SOY GRAPHIC – ZSH22 MAR22

ANALYSIS

- The weather factor conditions the price of soybeans.

- The deterioration of South American crops could be offset by a reduction in Chinese imports.

- We are waiting for the profit taking action of the funds in the week of February 21-25, 2022.

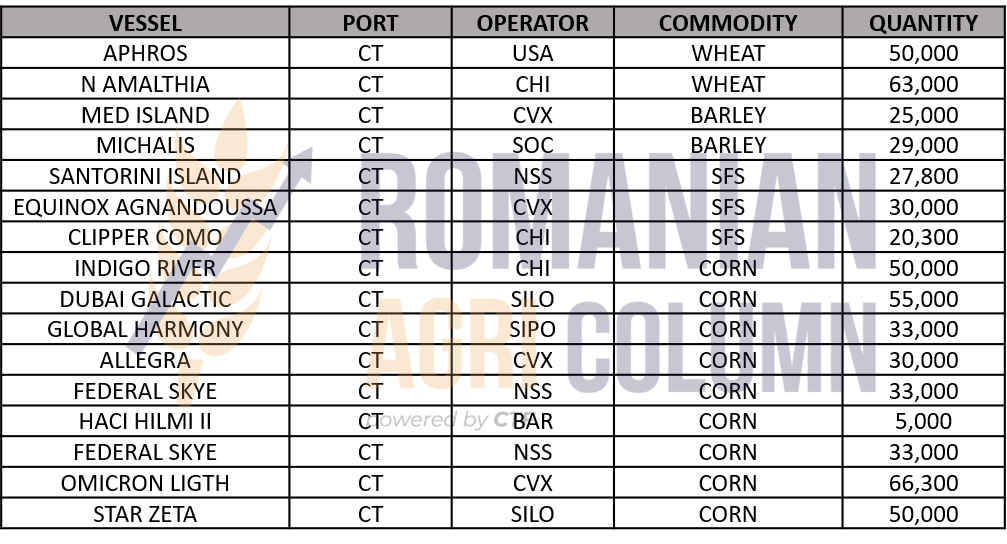

355,000 tons of corn | 113,000 tons of wheat | 78,000 tons of sunflower seeds | 54,000 tons of barley

USD strengthens against EUR (1:1.132)

BRENT is maintained at 93 USD/barrel.

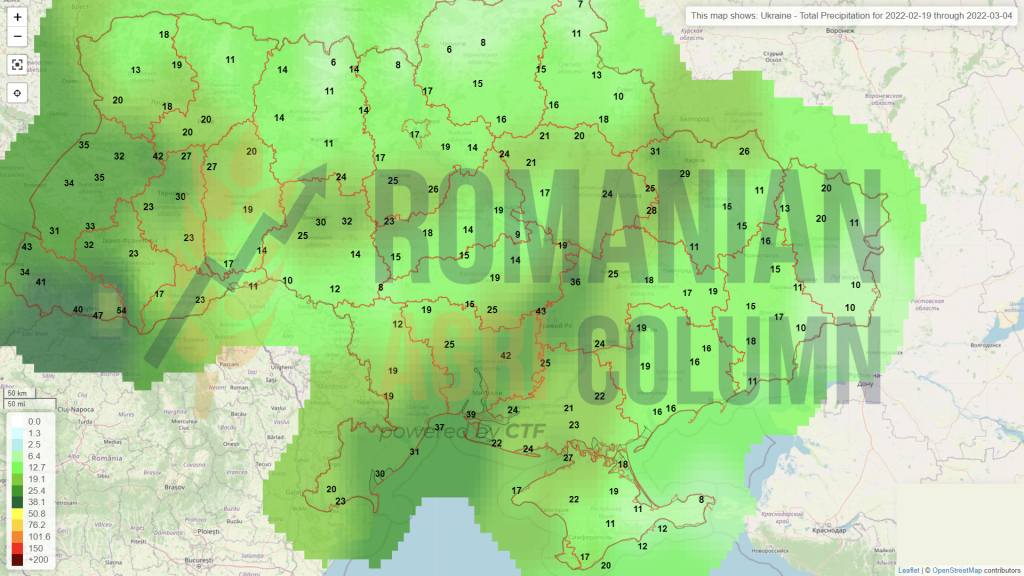

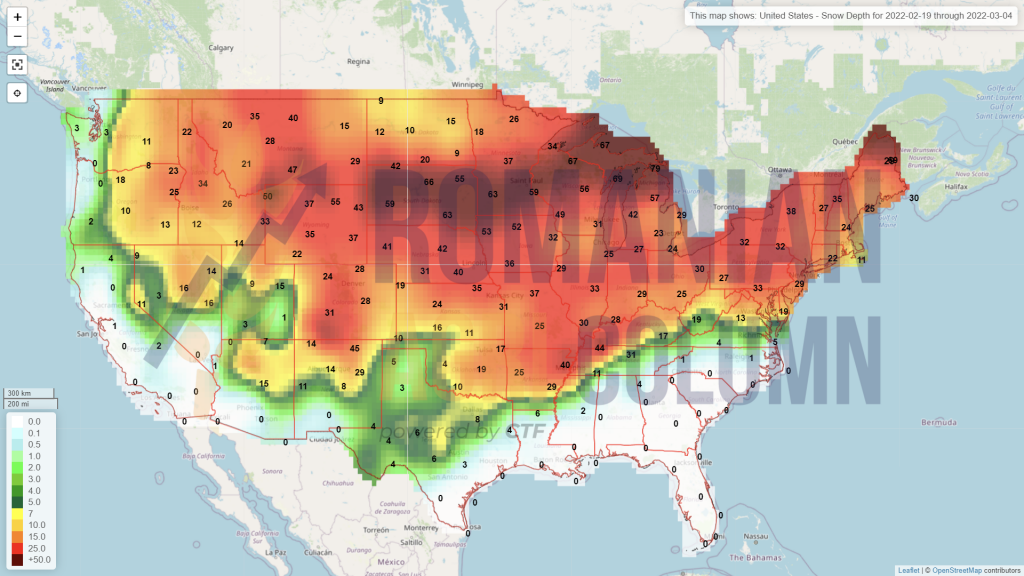

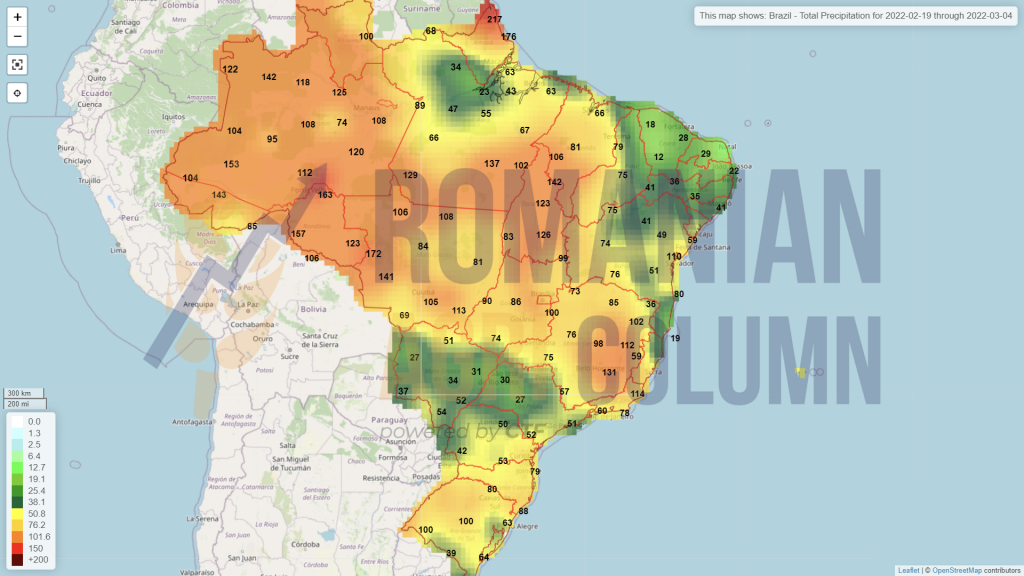

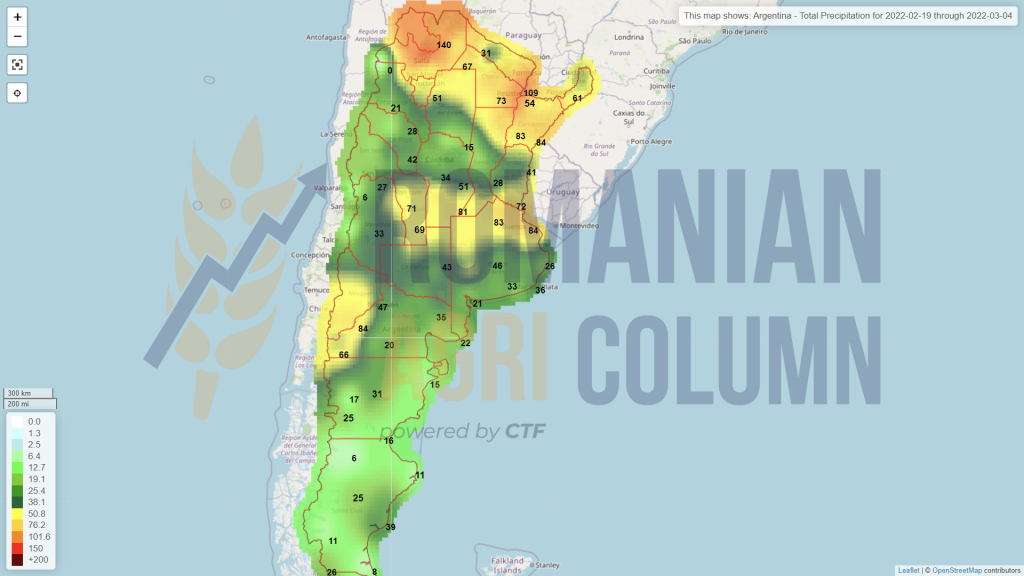

21 February – 4 March 2022

Romania (rain)

Europe (rain)

Russia (snow)

Ukraine (rain)

USA (snow)

Brazil (rains)

Argentina (rains)

Middle East (rains)

Northern Africa (rains)

China (rains)