This week’s market report provides information on:

|

Wheat market

The rains that covered Romania last week had a beneficial effect on the sown areas. The intake of 40-60 liters of water indicates a very good start in the 2022 campaign.

The wheat has a well-defined route, the indications remaining stable in the Black Sea basin. Last week recorded a plateau phase, a break in the trend and we recorded a level of 263-265 EUR/MT, CPT Constanța indication for milling wheat, while feed wheat has indications of 8-10 EUR/MT lower.

The internal market is in motion all this time. The indications of the processing units are at the level of 247-253 EUR/MT FCA Farms, At the same time, the exporters enter this competition and indicate prices of 250-253 EUR/MT FCA Farms.

But farmers have other expectations on the horizon. They target the level of 263 EUR/MT FCA, which puts extra pressure on the buyers, processors or exporters. And according to the latest USDA report, their expectations are not far from being met in the near future.

EURONEXT indications generate a level of 280 EUR, and this level reflects DEC21 minus Premium of 17 EUR/MT compared to the base, in a normal and calm market. But the turmoil will definitely happen. It will come from the demand for wheat in North Africa and the Middle East, which settles and strengthens the price level with each tender that is generated by destinations. This context of minus 17 compared to the basis will be reversed due to the demand in the Basin and we will see a much lower Premium, possibly up to zero.

Even Jordan, which canceled tenders through MIT due to the price, purchased a batch of 60,000 tons from Romania, set at 365 USD/MT CFR Aqaba, with delivery January 15-31, 2022. At the same time, they canceled the subsequent tender for easy to understand reasons.

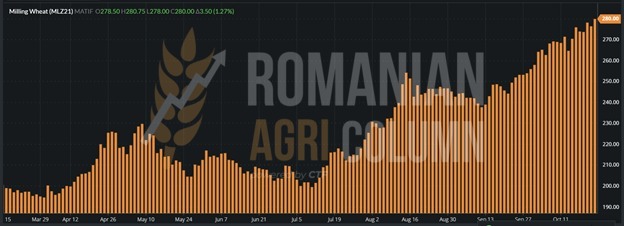

EURONEXT MLZ21 280 EUR +3.5 EUR

EURONEXT: wheat chart MZ21, 30 March 2021 (194 EUR) – 22 October 2021 (280 EUR)

The graphs are suggestive, but farmers need to understand that this year’s production bears the costs of a year ago and was still low compared to this year, fertilizer price levels have reached unbearable proportions, and this will certainly generate price support for the next season as well.

No farmer in the world will sell cheaply, no farmer in the world will invest money in the land to sell at lower prices than the agreement between direct and indirect costs per hectare and production income. In addition to this parameter, a very important factor is taken into account – the weather. We already note the problems in sowing in Russia, which goes on the road in the new season with a minus in the planting of winter wheat of 1.5 million hectares and a lack of water. However, this minus can be recovered in the spring, once the seasonal wheat is planted. Although Russian analysts submit projections for 2022 production of over 80.7 million tons, we believe that they are risky and have no real basis. You really can’t estimate next year’s 2022 production from October 2021. You have no definite basis other than a number of hectares. The weather is uncertain and can play a very important role.

In areas affected by drought last summer on the West Pacific Coast and parts of the Central American Plains, rainfall levels do not meet the requirements for planted wheat. That is why the harvest advance earned on corn is also explained. The weather is dry and allows for full blast harvesting. But as the days go by, the cold makes its presence felt as another risk factor. In South America, in Argentina, the days without precipitation make their presence felt again. BAGE estimates 20.7 million tons of crop forecast, but for now these are only statistical data.

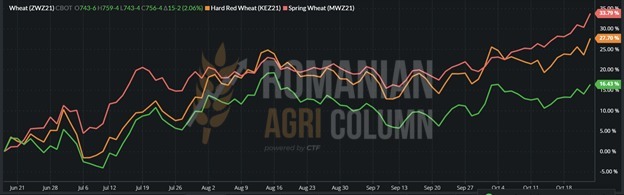

In the American market, wheat suffered a setback. It was generated by the USDA announcement that the estimated 500,000-650,000-ton export schedule for October has not been met. It remained at 362,000 tons. This generated a decrease of -9 c/bu (3.3 USD) in the quotations of American wheat on CBOT and KANSAS on October 21. This also reverberated in EURONEXT, where we recorded a closing of the trading session with a minus of 1.75 EUR/MT MLZ21.

The next day, October 22, 2021, things returned to normal, with a jump over what had deteriorated the day before. Thus, CBOT SRW ZWZ21 regroups with an increase of 15 c/bu (5.51 USD) and pushes the wheat back on its natural path. KANSAS HRW KEZ21 goes up by 24 c/bu (8.18 USD), and MINNI MWZ21 by 25 c/bu (9.2 USD).

CBOT ZWZ21 – green | KANSAS KZ21 – orange | MINNI MWZ21 – red

In the rest of the world, as a summary, we note the increase in the level of Algerian imports to the level of 8 million tons due to the degradation of their own crop by up to 38%. German wheat will take its place in front of French wheat in this destination due to the lower price, and Russia has penetrated the Algerian market with a batch of 60,000 tons of wheat.

Turkey has provisionally purchased 300,000 tons of wheat until final approval. The price varies between 351.5 USD/MT C&F TEKIRDAG and 354.9 USD/MT C&F BANDIRMA. Logistics makes the difference. From origin to destination, we have a value of 38-41 USD/MT, high cost due to small ships of maximum 25,000 tons.

The Asian wheat market is in a somewhat desperate situation. The level of wheat import calculations exceeds the price of processed flour and this is becoming a major problem for Asian countries.

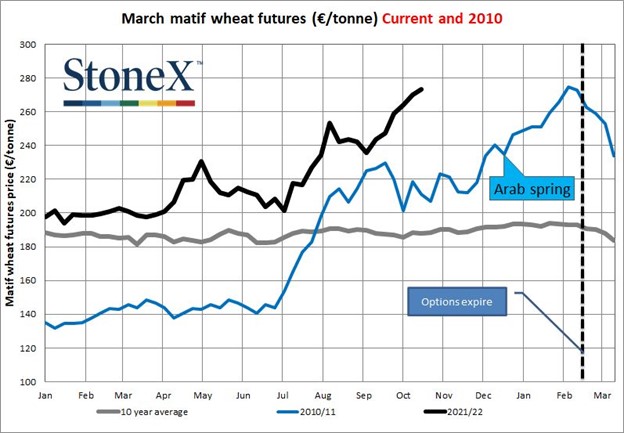

We insert a graph of the EURONEXT wheat price, compared between the 2010-2011 season (blue line), the average of the last 10 years (gray line) and 2021-2022 (black line). Source: STONE X.

BSW – BLACK SEA WHEAT regains its cadence after the decrease of 3.5 USD/MT caused by CBOT on October 21, on October 22, 2021 with the indication FOB NOV21 of 325 USD/MT.

The export tax on Russian wheat is quoted at the level of 67 USD/MT, at an index of 295.8 USD.

ANALYSIS

- Wheat continues its demand-driven march. Production does not cover consumption.

- We estimate a level of 338-343 USD/MT FOB BLACK SEA in January – February 2022.

- Some exporters already offer farmers the option of forward contract for next year’s new crop, at the level of MLU SEP22, minus 21 EUR/MT CPT Constanța, i.e., 222 EUR/MT. But who is willing to sign a fixed basis and a calm market premium in today’s inflationary hurricane? Absolutely nobody, for sure.

- The sales paradigm is changing. The origin will determine the price in the coming years due to the very tight supply and demand, all directly related to the weather and politics.

Barley market

The indications have increased, helped by the feed wheat factor. The port of Constanța has been aligned and for about 3-4 days we have been witnessing a stagnation of the barley price level around 230 EUR/MT.

However, barley does not have such a high productivity in the 2021-2022 season, so we forecast a constant demand. Turkey, through TMO, is organizing a new tender for the purchase of 235,000 tons of barley. Tunisia, through ODC, purchased 2 lots of 25,000 tons each, at the price of 349.22, respectively 346.05 USD/MT CFR.

The demand being constant, the expectation that the barley will be quoted well in the next period is a positive and normal one, Barley lots are also starting to be traded in the country, mainly due to the fact that one of the important players in the pig farming industry has particularly serious problems due to the African swine fever, 6 units being effectively depopulated.

Barley thus follows a quiet and calm path in terms of price and demand at the moment. We forecast this in the next period, without significant decreases or fluctuations.

Corn market

The Romanian corn market has indications of 236 EUR/MT in the CPT Constanța parity, the variation being in some days of +/- 2 EUR/MT. We also noted variations of up to EUR 4 in a positive sense dictated by the need for contractual execution of certain exporters, in October, the urgency of dispatching berths being the main source of spot growth.

In the country, large-volume farmers have set benchmarks of at least 222-223 EUR/MT to sell corn. This level is largely granted logistically with the price in the Port of Constanța, noting here the exporters who buy at this inland price level.

Neighbors in Bulgaria have much higher prices than farmers in Romania. The difference is at least 5 EUR/MT and is visible in trading. This is mainly due to the fact that the Romanian state did not sign the phytosanitary agreement with China, and Bulgaria did so, as did Ukraine. A question mark lingers in our thoughts. Why didn’t Romania do it? What factors determined the refusal to sign the agreement, because a delegation of the relevant body from China visited Romania precisely for this purpose. But nothing happened and things remained the same as before.

Harvest pressure in the Black Sea basin is beginning to become apparent. As we note, Ukraine is beginning to harvest massively and is putting sustained harvesting pressure into the Black Sea basin. Days without precipitation facilitate the harvesting process in Ukraine and progress is visible. At the same time, in anticipation of this, we estimated the deterioration of the price of maize. Degradation in the Black Sea basin reached a level of 8 USD/MT for cargo loaded on ships, in FOB parity. From an FOB indication of 280-285 USD/MT dictated by the absence of goods, the delayed harvesting of rains and a delay of 2 weeks of harvests in the pool, today we note 272-274 USD/MT and a flattening of the carry level on the following 3 months, i.e., storage does not induce an increase, as seen today.

Of course, the harvest puts pressure, of course the price degrades given the volume. Let’s not forget Ukraine’s export forecast of 32.5 MMT, from a harvest of 38 MMT. But these things will pass and we must regroup in visualizing the global levels of production and consumption.

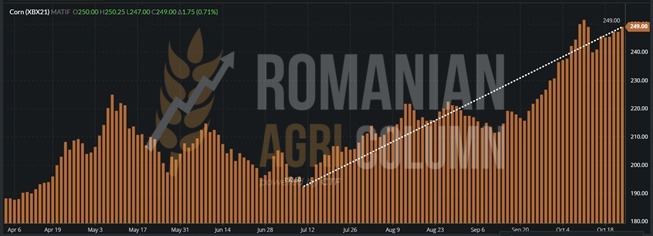

Returning to the CPT Constanța price of 235-236 EUR/MT, we see that the EURONEXT NOV21 ratio is maintained, i.e., the Negative Premium of 10 EUR/MT is applied to the quotation and then the trading margin of the exporter is deducted. If we use this calculation formula, we have the following formula that’s applicable to a normal market, dictated by harvest pressure and volumes that meet forecasts: XBX21 (249 EUR) – PREMIUM (10 EUR) – TRADING MARGIN (3-4 EUR) = 235-236 EUR/MT

XBX21, closing October 22, 2021: +1.75 EUR compared to the previous day

GRAPH XBX21. We note 192.5 EUR (12 July 2021) and 249 EUR (22 October 2021).

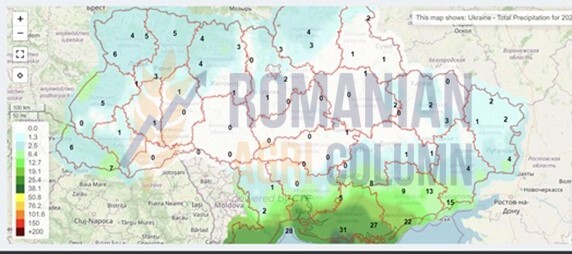

We will stay for a while in the Black Sea basin to analyze two images, one with the forecast of no rainfall in Ukraine, which favors the pace of harvest, and the second with the most productive regions in terms of corn in Ukraine. Source of the second image: USDA

However, we are in the same landscape, with a positive balance, but very close in terms of corn production worldwide, PRODUCTION VS CONSUMPTION/STOCKS. Any anomaly that occurs fuels the fragility of the system.

And with this we are moving to the North American continent, where the USA is at a harvest level of over 55%, above an average of recent years, with a very good production. But the advance in the harvest is generated by the lack of precipitation, which acts in two directions, one positive for the advance of the harvest and the other negative for the winter crops.

The engines of the world giant (in the sense of a corn producer) are already set in motion and running fast. We see in the USDA weekly reports a volume of 457,000 tons of corn sold, as well as a volume of 133,000 tons destined for Mexico, the same Mexico ignored by general calculations regarding corn production. Mexico went through a terrible drought in 2021. Let’s not forget its position in Southern California, and note its normal consumption of corn, 20 million tons of own production and 20 million of imports. 10 million used to come from Brazil, a country that was penalized by the weather in the 2021 season and 10 million used to come from the USA. The report is now reversing, with the US taking a significant share of Brazil and meeting Mexico’s consumption needs. Mexico is one of the top two most important US customers in the corn trade, and creating an additional volume for the US does nothing but make up for the possible gap left by China.

China, from a logistical point of view, seems closer to the Black Sea basin than to the USA. Logistics in the Black Sea cost 65 USD/MT, while 83 USD/MT is the cost level in the US GULF. 18 USD advantage can be easily reversed in the price of the goods, so a more expensive origin in the pool. This explains why the pressure to originate in the Black Sea basin was acute until the time of the full blast harvest of Ukraine. And let’s not forget that in NE Asia there is also South Korea, which these days is loading important volumes from the Black Sea basin.

Remaining in terms of production, we advance Brazil’s projection in terms of corn for 2022-2023, which can materialize at the level of 118 million tons, a well-deserved revenge after the disaster of 2021.

However, big questions are beginning to emerge about future American corn crops. The cost of setting up is around 1,000 USD/acre, and the price of corn should also be high to cover expenses. An increasingly common alternative is that corn areas in the US would shrink next season, with farmers migrating to wheat and soybeans. It is a working hypothesis that must be followed, if and how it will happen, in view of the fact that it would unbalance supply globally.

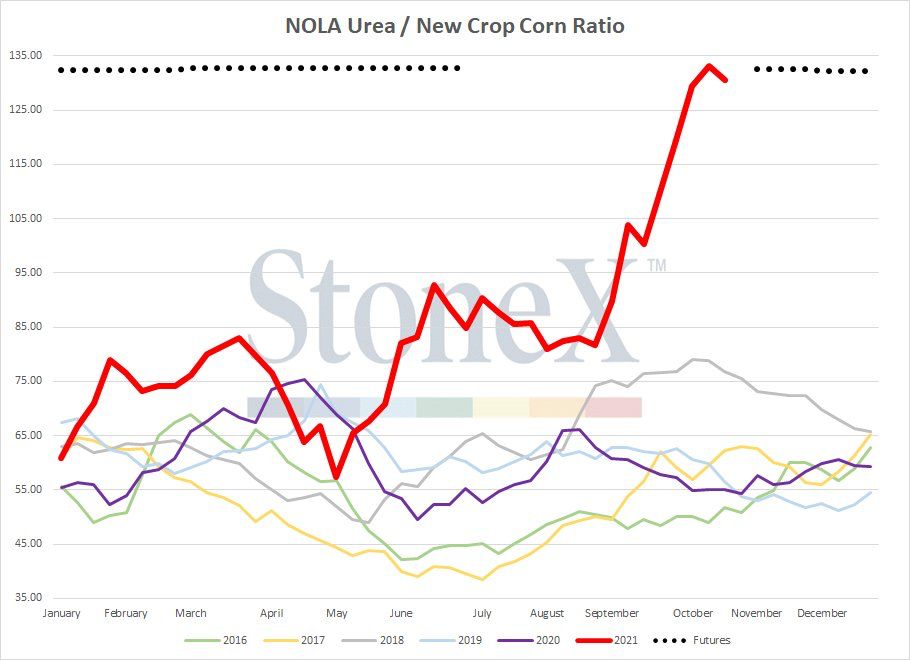

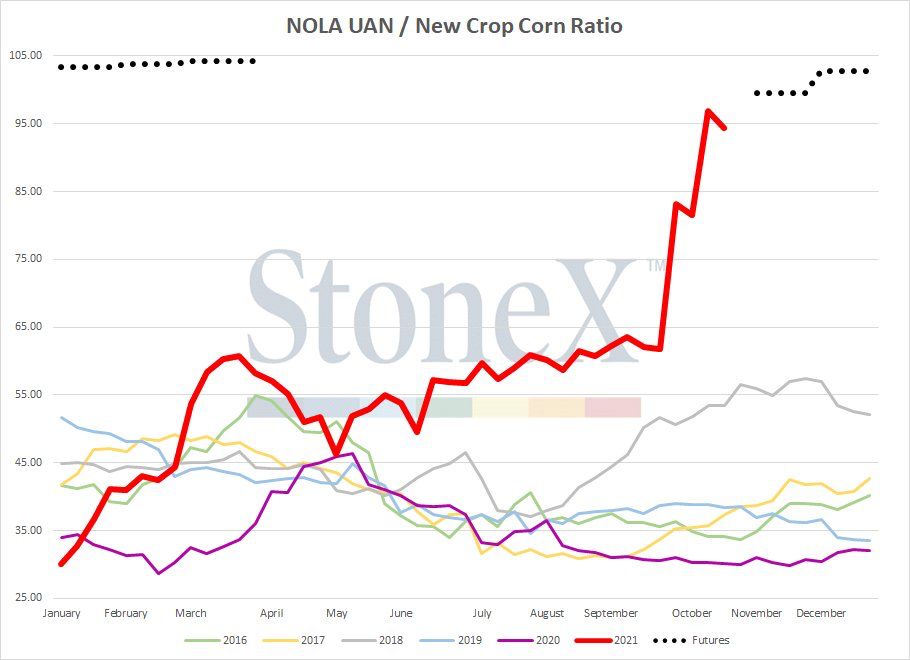

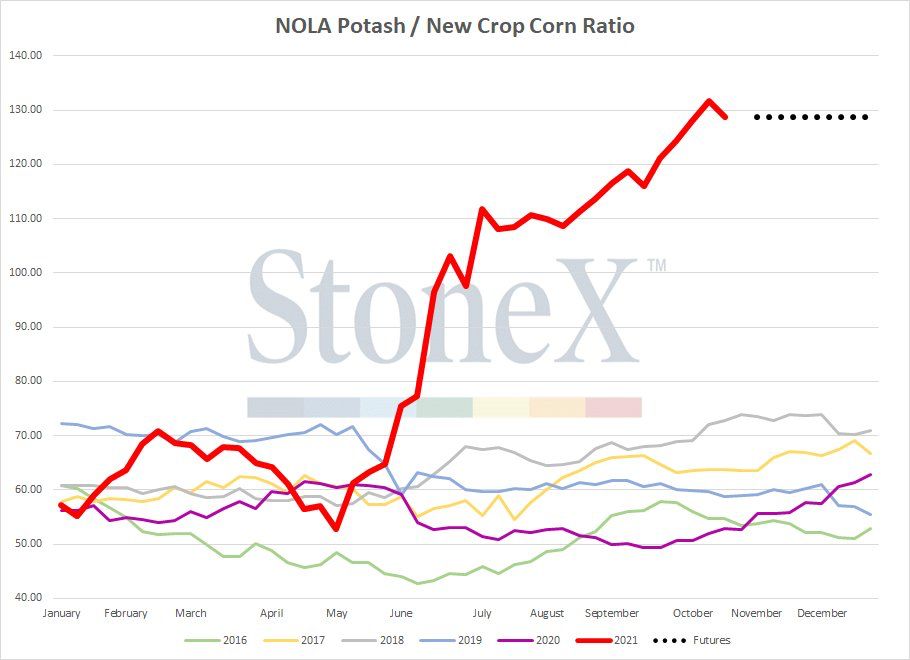

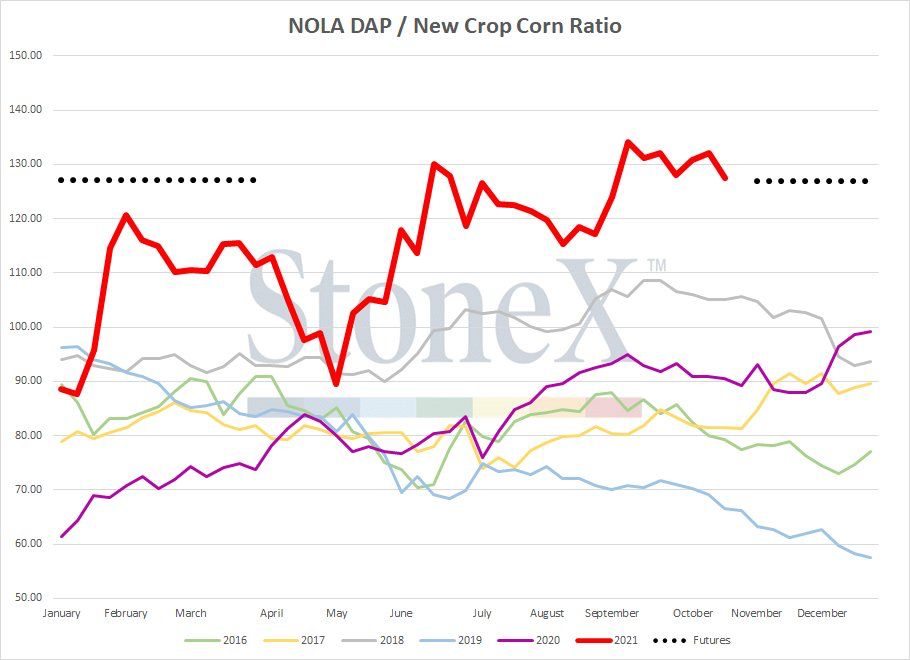

Because we are in the production costs chapter, we insert a group of graphs (source: STONE X) to view the prices of fertilizers. Urea, Liquid Urea – UAN, DAP (18-46-0) and potassium fertilizers, reported as use costs in maize production.

Looking at the graphs above we can conclude that we are in a status from which the primary conclusion we draw is that prices remain and will remain supported by production costs.

Moreover, we are globally in a status called STAGFLATION, a persistently high inflation, combined with high unemployment and stagnant demand in a country’s economy.

American quotes are starting to grow. CBOT: +5 c/bu at the closing of October 22, 2021

CBOT ZCZ21 recovered 26 c/bu from October 13 to October 22 (10.23 USD).

ANALYSIS

- Maize in the Black Sea basin is under obvious harvest pressure. The indications are maintained around 235-236 EUR/MT CPT Constanta subject to a logistical advantage over Nikolayev Ukraine.

- FOB Ukraine is degraded by about 8 USD/MT, to the level of 272 USD/MT. Due to the level of harvest, the volume effect is felt in the price. A total export volume of 32.5 million tons in the 2021-2022 season is starting to put pressure on prices.

- The logistical advantage of the Black Sea remains in place. The 18 USD advantage over the US GULF is a figure that can fuel the original price.

- China DALIAN corn exchange: NOV21 2,542 CNY/MT = 397.41 USD/MT; IAN22 2,580 CNY/MT = 403.35 USD/MT (CNY = Chinese yuan). This perspective shows us the demand and potential in the price of corn.

- As a cumulation, corn has a slow development and will go through the classic stages of the formation of the price life cycle. However, it will be increased by the price of wheat, which will be a traction factor in the 2021-2022 season.

Rapeseed market

The statement for rapeseeds might sound something like this: “all quiet on the Western Front“, according to the title of Erich Maria Remarque’s book. The same daily carousel, generated by the agreement with fossil energy and physical contractual coverage in Rotterdam.

Thus, the other day we had peaks and sharp falls, this being the correct expression for the evolution and involution of the rapeseed quotations. The sinusoids of the charts are expressive in this sense and actually represent the transactionality of a month-end, when positions are liquidated, others move to FEB22 and so on.

In Romania, the demand for rapeseed is expressed by a single process, which has thus provided a desolate land, without competition and could run quietly without being disturbed in any way. The results were seen, the origin bringing very good volumes.

The purchase indications materialized at the level of XRX21 minus 25-30 EUR/MT. This very high premium could be manifested due to the lack of competitiveness of other market players.

But we turn our attention to 2022 and see the same support that we forecast for rapeseed, namely indications of 669.75 EUR, with a much smaller decrease than XRX21, where, as mentioned above, positions are liquidated or moved.

However, we also notice AUG 22 XRQ2, with a harvest reversal of 105 EUR (565 vs 670 EUR/MT). But the road is long until the rapeseed harvest in 2022 and many things or events can influence the price. But let’s look with optimism, to conclude the price potential we see today and to calculate very carefully the production costs of rapeseed, so that we have the accuracy of future profit.

Sunflower seed market

The price march continues unabated and we have reached the level we have been estimating for some time much earlier. We have been estimating this level for a long time, but not now. We are at 700 USD/MT for sunflower seeds, a threshold that has been reached due to the following factors:

- The origin moved only to Romania.

- Crops in Russia and Ukraine were degraded by 0.5 million tons.

- The price level of CSFO oil in FOB Odessa/Chornomorsk reached the level of 1,440 USD/MT, with a potential of 1,450 USD/MT soon.

All processors have understood this and want their seeds. But they can only originate in Romania. The direct comparison with 2020 is obvious, with two differences:

2020: Local production in Romania was only 2,080,000 tons and the entire European spectrum, as well as the Black Sea basin were affected by drought. So the lack of volumes fueled the price of raw materials to the level of 720 USD/MT.

2021: Good production in the EU and the Black Sea basin (with an aggregate degradation of 1 million tonnes RU + UKR), but with a global commodity price inflation. In addition, we have Turkey with a persistent drought, high demand from Asia, very tight vegetable oil stocks and demand from China.

The general level of 720 USD/MT will be the next stage. Locally, we recorded a transaction of 10,000 tons concluded at the level of 725 USD/MT DAP processing unit, with the option of delivery until April 2022, which brings a storage cost of 3 USD/month to the seller’s account.

The two processing units in Hungary located in the vicinity of the border with Romania post prices of 710 USD/MT DAP, in German Terms conditions, i.e., with oil bonuses. We must mention that in the rest of the country, Tale Quale is the working method, i.e., without oil bonuses included in the contracts.

What do we have around us? Ukraine is harvesting and has reached an estimated level of 80-82%, behind last year due to the postponement of harvests. However, Ukrainian farmers do not want to sell the goods yet. The CPT price level in Ukraine today is around 20,000 hryvnia/MT, i.e., 762 USD/MT including 20% VAT.

Ukrainian exports to the Chinese market increased to 74%, compared directly to Russia. The latter sold out of the Chinese market, reaching the level of 23%. But Russia is seriously considering raising the level of export tax on sunflower oil. According to TASS, the agriculture minister said on October 21 that they will increase this tax if prices rise, in an attempt to protect the internal market.

ANALYSIS

- The demand is very strong for sunflower oil.

- The level of 6 PORTS or ARAG reached 1,475 USD/MT.

- The raw material is depleted and the processors want to have the goods.

- Shelf oil prices will continue to rise, in line with the inflationary level of commodities.

- Next stop for seed prices? 720 USD? 730 USD?

The soybean market

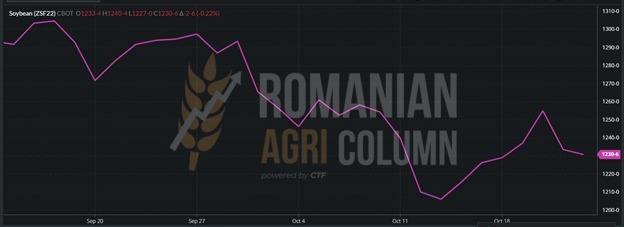

The CBOT indications gained consistency, starting from the day of the release of the WASDE report, October 12, when the soybean actually collapsed below the level of 1,200 c/bu, more precisely 1,194 c/bu. Meanwhile, with the support of exports, soybeans began to return to positive prices. And so we see the closing on October 22, 2021 at a level of 1,230 c/bu, a return of 30 c/bu, i.e., 11.02 USD. For compliance, we look at ZSF22, because in a few days we will exceed ZSX21, which expires on October 30 and is no longer relevant. At this point, positions are liquidated and contracts are transferred on the following indication.

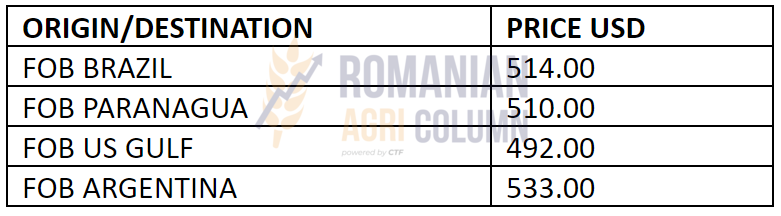

The indications of the main origins are presented according to the table below. The difference between the origins is the logistical cost to the destinations.

The United States sold 2.9 MMT of soybeans last week, the highest weekly volume in more than a year. Total sales of 29.3 MMT as of October 14 cover 51% of the USDA forecast for 2021/22. Non-Chinese sales are not special at all, China’s import level still remains at over 100 million tons.

The American soybean harvest rate reached 65%, a much better rate than in the last 5 years, due to the rainless window, which generated intensity in the gathering of soybeans in the field.

But Brazil is already forecasting production that could reach 140 million tons next season, which puts additional pressure on soybeans.

Moreover, China is facing extremely serious problems with the supply of electricity, which has led to the restriction of processing units in agriculture and thus the processing of soybeans. China is also restricting fertilizer deliveries, creating an overcrowding chain effect on other suppliers globally.

In Romania, soybean indications amount to 650 USD/MT DAP processing units for non-GMO soybeans.

The not-too-distant horizon shows us very good yields in South America, combined with a very good American harvest, which could lead to a stagnation in the price of soybeans, all fueled, of course, by China’s production bottlenecks caused by the restriction of the use of electricity.

EUR-USD parity

Energy

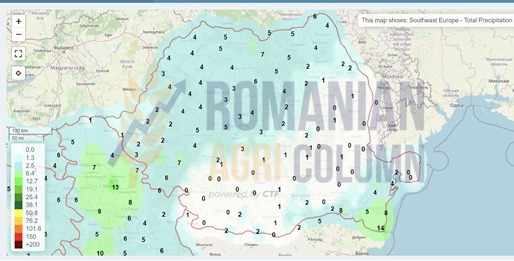

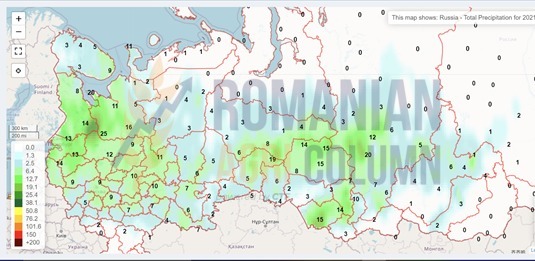

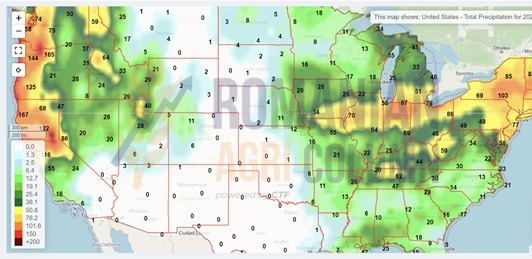

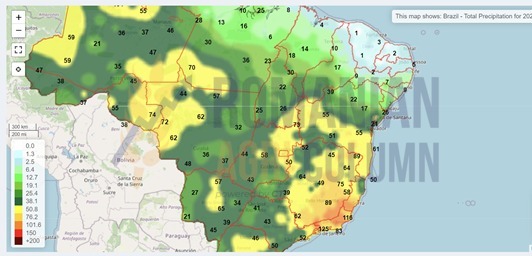

Weather forecast

22 October – 1 November 2021

Romania

Europe

Russia

Ukraine

USA

Brazil

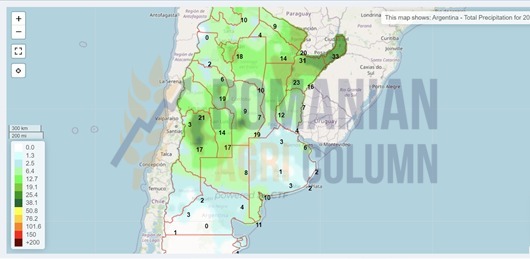

Argentina

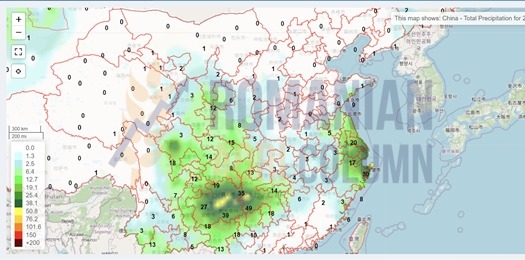

China

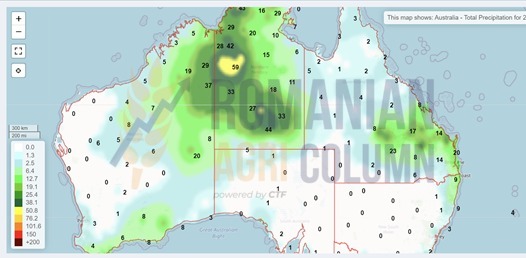

Australia

© Romanian AGRI Column, 2021, all rights reserved