This week’s market report provides information on:

NOTE TO ISSUE 47/2021: Due to the emergence of the potential danger from the discovery of the new South African strain COVID-19 called OMICRON, all quotations have fallen sharply. Fear of global lockdowns and suffocation of the supply chain have caused destinations to fall back on hold. So we also note these effects that have impacted the market. But the panic is not an element that must generate hasty actions, but rather requires a time of estimation and information to make the best decisions in this regard. The fundamentals of the physical market have remained the same as before, except that the effects of the current situation are impacting for an indefinite period. We take note and will return with more information in the next issue. |

Wheat market

The quotations of Romanian wheat in the CPT Constanța parity reached the level of 295-298 EUR/MT, in line with the indications of the Black Sea basin and in accordance with the level of the last Egyptian auction, which brought a lot of 60,000 tons from Romania. Then the discharge of costs generated a price level in FOB of 306.7 EUR/MT, which leads to the indication level valid until mid-November 26, 2021, equivalent to the one mentioned above.

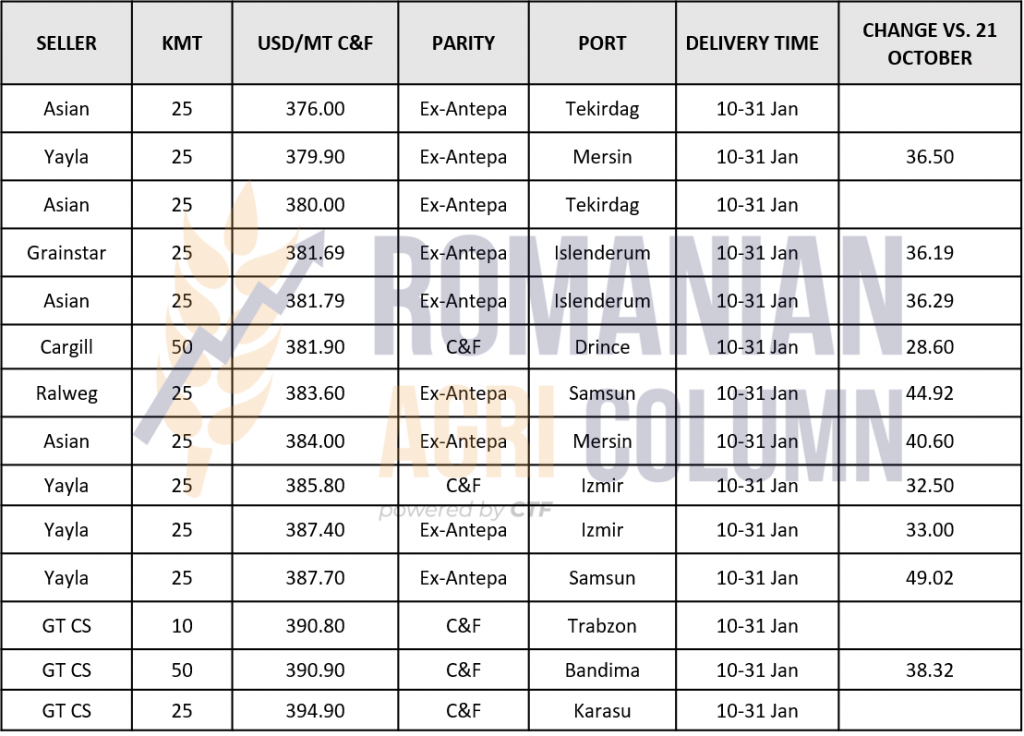

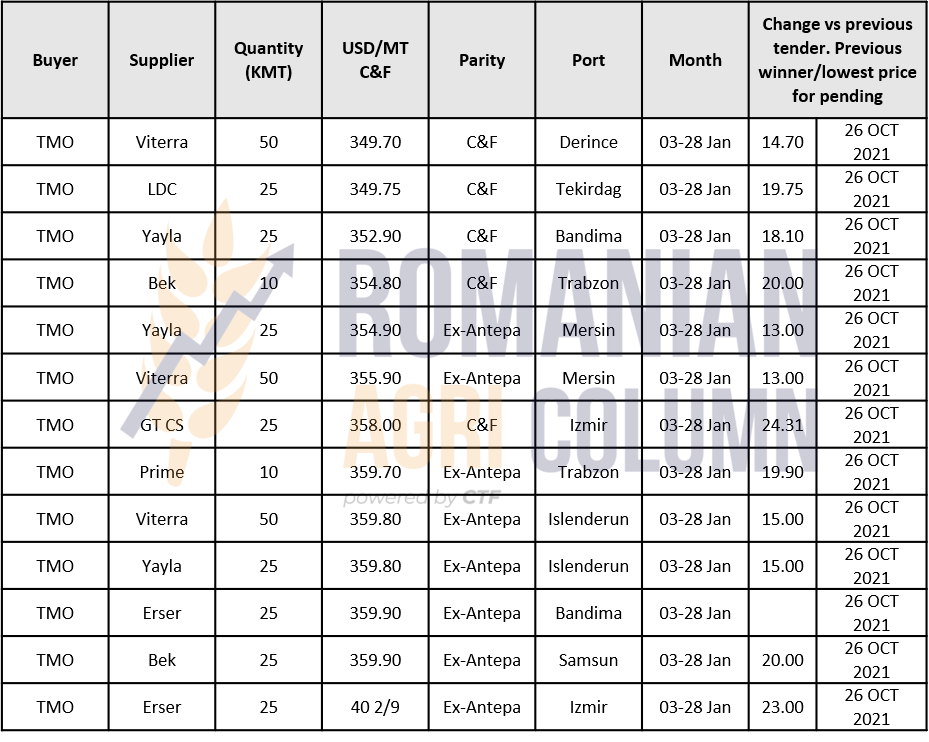

TMO TURKEY completed a tender for the purchase of 385,000 tons of wheat on 25 November 2021. Due to the large number of ports where the delivery will take place, as well as the fact that the transport will take place with small capacity vessels, it is difficult to estimate an average selling price. But what we notice in the last column is the price difference between November 25 and October 21, 2021. It is a significant amount that wheat indications gained in a month.

Today, November 29, 2021, there will be a new auction generated by the Egyptian state through GASC, the representative body. A new auction was expected to enter the circuit, after only two days before they had announced in the classic way that they have a 5-month wheat reserve. This classic way is, in fact, the way the announce the market: “get ready, we buy”. Nothing more.

In Romania, most farmers move sales next year. It is a measure that also moves the payment of taxes to a wider horizon. For a sale of goods increases the tax base at the level of a company through the financial record between costs and income called profit. But the effect could become somewhat dangerous due to the potential to flood the commodity market, which could lead to lower purchase prices at the level of buyers due to abundance. If we include in this calculation the potential of an extraction from the Romanian state reserve, generated by the high market price and the processors’ desire of replacement at a lower price in the future crop, we can see a much lower price due to lack of demand from the local market. It is a signal that we give to farmers, a correct and coherent signal, to estimate and not of over-evaluate, to have a balance in the management of the potential and, not in the end, a signal of normality.

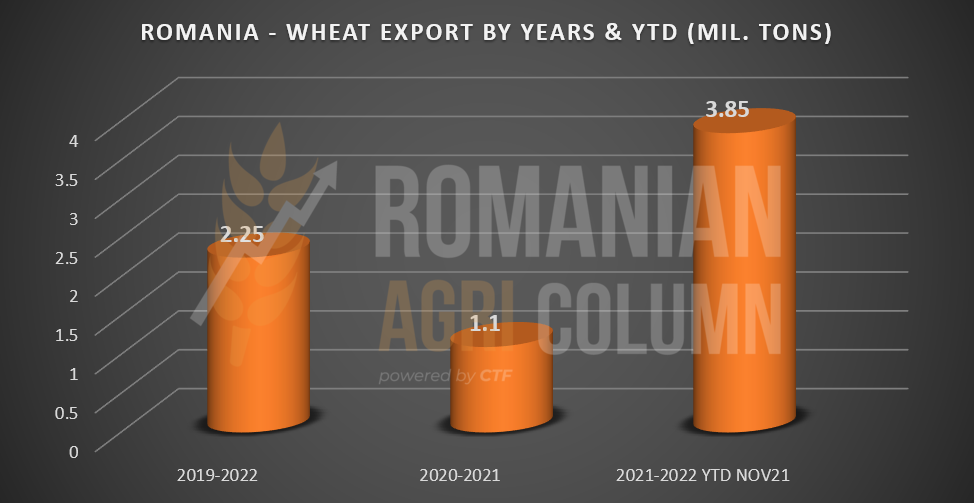

Romania has a very high level of wheat exports compared to other years. More than 3.85 million tons have been exported so far, compared to 2.25 million tons in a normal year, not taking into account the 2020-2021 benchmark due to pedological drought. It is an increase of 58%.

France is finally providing us with information about the cumulative export level of the 2021-2022 season and the figure it displays is 3.42 million tons. We keep in mind that France has a crop level of approximately 36.5-37 million tons and what we notice is the difference between Romania and France: a higher level of export of Romania compared to France, associated with the level of production in Romania of 11.3 million tons, compared to 37 million tons in France.

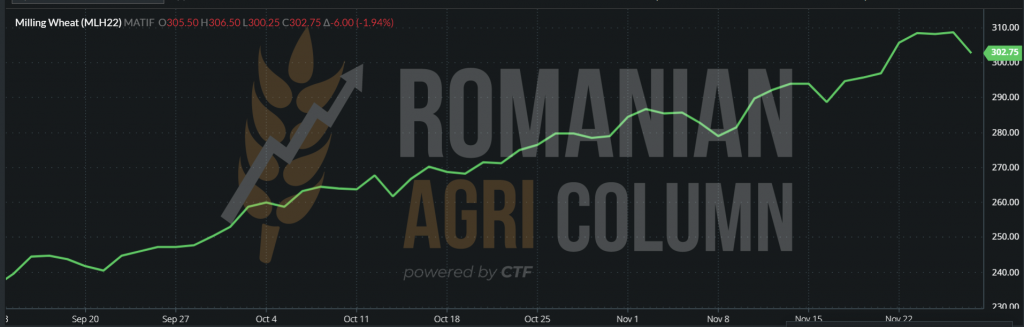

But so far, other events have marked the price of wheat. The excitement of the 300 EUR/MT, a milestone reached on Euronext, had barely dissipated, and another event was perceived at its real value.

We have been reporting floods in Australia since November 15 to our subscribers. The torrential rains actually turned into whirlpools that covered the wheat fields. The effect came a few days at global level. The conclusion was quite disappointing for the Australian crop, namely that there will be losses in volume and quality.

South Wales is actually under water, the state of Victoria as well, and we see this very clearly. The 8-day forecasts indicate significant rainfall in Queensland, New South Wales and partly in Victoria, which will exacerbate Australia’s problems.

However, we see that the regional analysts do not reduce that potential of 32.5 million tons in any form. The discount will come, for sure. They may need much more certainty, but flooded fields as well as water-covered farms are exactly the evidence they need in a preliminary estimate of declining production. And let’s not forget that the time for the WASDE report is approaching again.

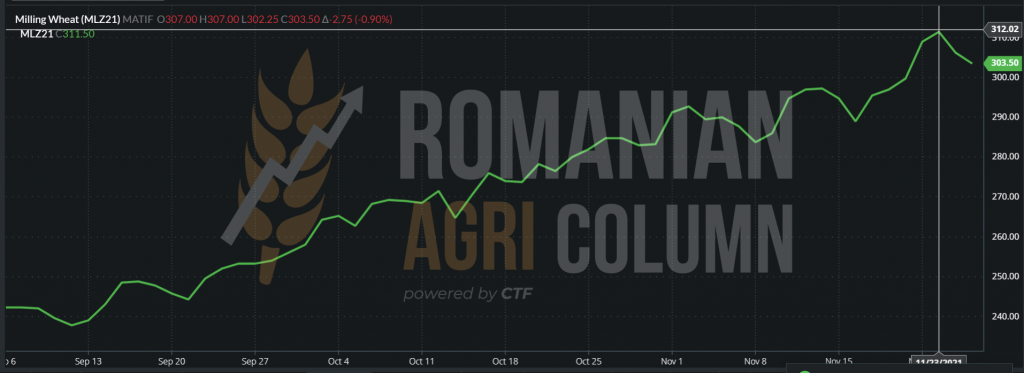

Traders who had fixed export contracts with milling quality suddenly encountered major problems and were forced to look for merchandise to replace the depreciated quality. Thus, the Butterfly effect spread to the other origins, with Euronext posting EUR 312 in absolute terms.

EURONEXT MLZ21: 312 EUR (top right)

AUSTRALIA – VICTORIA

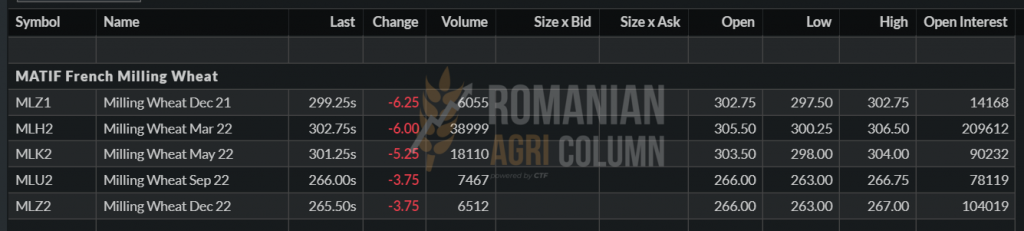

But the indication MLZ21 DEC21 began to degrade compared to MLH22 MAR22, as a natural consequence of the liquidation of positions and roll-over, movements with which investment funds have accustomed us, by the way. However, the news soon arrived that the WHO has begun the meeting to assess the risk potential of the new strain of COVID-19 that has appeared in South Africa, and the trading booths have gone into total risk elimination.

Thus, liquidations of positions were generated instantly and, implicitly, MLH22 quotations decreased. This was followed by the chain reaction of buyers in the physical market, who retreated and stopped purchasing goods until the WHO estimates.

However, this estimate has a very high-risk potential. The virus has the apparent ability to withstand the vaccine and, therefore, measures to counteract its occurrence in Europe and the USA have been taken, until the ban on flights in that area. Indeed, a sanitary barrier was created in an attempt to stop it.

The closure of Euronext on November 26, 2021, as CBOT was closed due to holidays, generated a sharp deterioration to the level of 302.75 EUR, an appreciable decrease.

EURONEXT TREND – MLH22 – March 2022

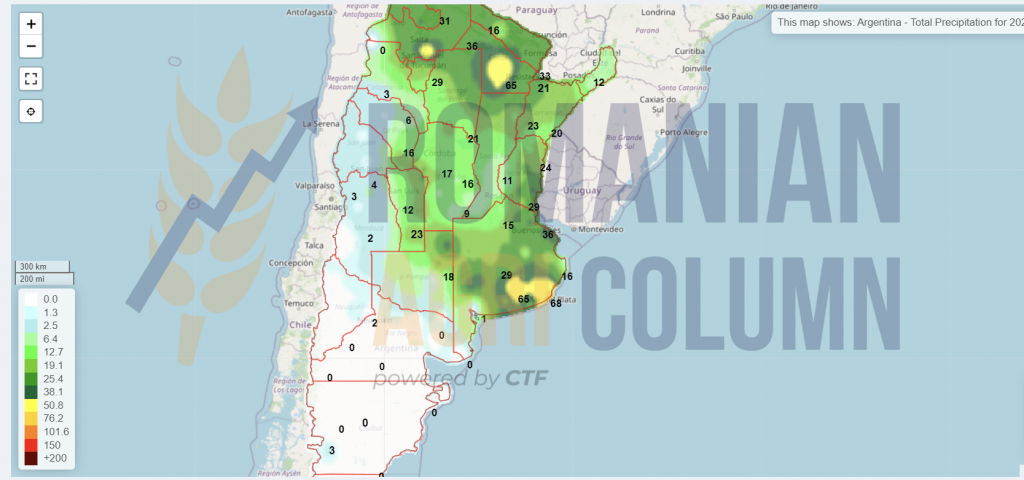

Traveling overseas now, we see a re-evaluation of the Argentine wheat crop, which is boosted to 20.3 million tons, up from 19.5 million tons.

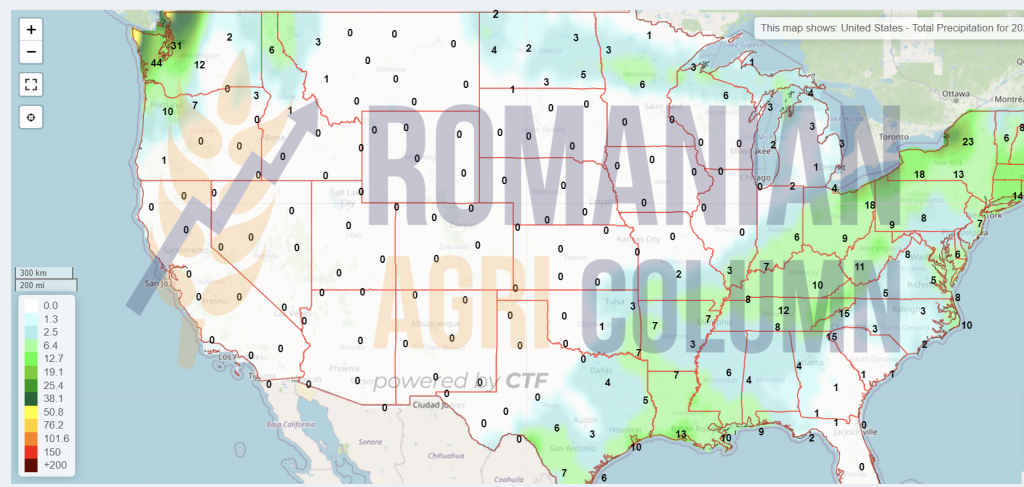

In the north, the US generates a planted crop status of 97%, with a 86% increase in yield and a good to very good status of 44%, down 2% from last week, when it was listed at 46%.

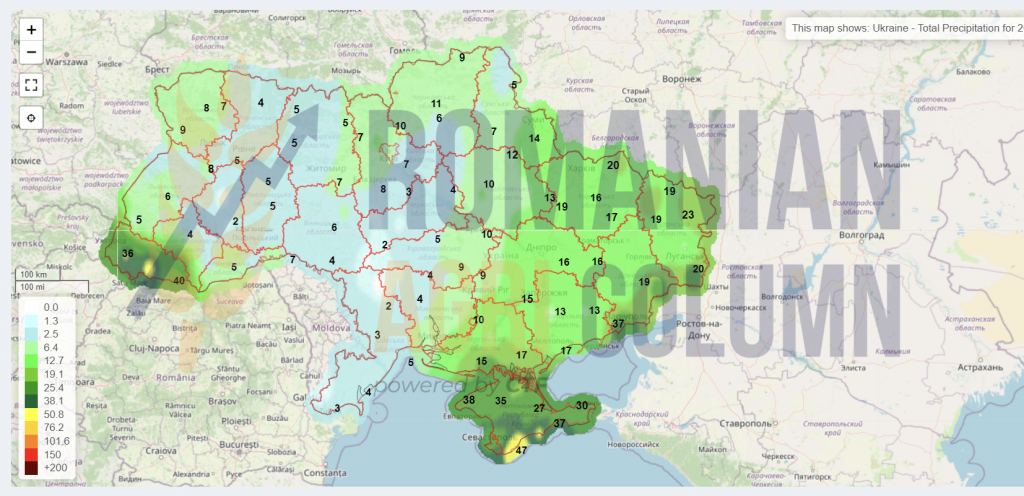

Returning to Europe, we find a good crop status. The rains have potentiated the state of vegetation. In Romania, however, due to the dry weather, the plan to sow wheat had not been completed. 2 million hectares have been completed, out of an estimated 2.15 million. We are at the end of November and the sowing window is closing permanently. But our estimates indicate the completion of the process according to the initial figures. We are also waiting for the official confirmations of the Romanian Ministry of Agriculture to certify the end of the process.

In Russia, things are somewhat uncertain, due to the closure of the sowing window, as well as the level of soil water supply which is not optimal at this time. The snow falls, but if it falls on frozen ground it cannot feed the primary layer of 20-25 cm, so that the roots can feed.

Recent satellite images from NASA have suggested that groundwater in Eastern Europe and western Asia, including western Russia, is very low. Rainfall in early autumn attenuated some of the soil’s drought, but more recent rainfall has become weak again. The short-distance drought in the ground may remain in the winter and could become a “sleeping dog” for Russia in 2022.

Low groundwater does not always create a problem unless rainfall is lighter than usual during the growing season. In this situation, crops that are planted in the spring may have short root systems. If the weather becomes a little dry, the root systems can look for moisture in the deeper soil, only to discover that groundwater is not readily available. If this situation evolves, the crops will be very easily stressed when the weather will be dry, after planting and the spring sprout, when, normally, the development takes place at a sustained pace.

ANALYSIS

- The fundamentals of the physical market have not changed in terms of supply and demand.

- The stagnation of sales and the move in 2022 could have a boomerang effect in the local Romanian market.

- Omicron, the new strain of COVID-19, is holding back the development of wheat prices, with a view to isolating contaminated areas.

- The development will take place after the dissipation of emotion and understanding of the effects in the market.

- Russia passes the duty rate of 80 USD/MT, more precisely 80.3 USD, according to the index calculated by MOEX.

Barley market

The Romanian feed barley market reached a level of 254 EUR/MT in the CPT Constanța parity, which was generated by the imminence of the TMO Turkey auction, which ended. At the same time, we see an increase in the export level of Romanian barley in terms of volume compared to previous years, as you will see in the chart below. What we notice is the very high level of exports so far, a level that has exceeded since November 2021 the export made for a whole season. We remind you that the total production of feed barley in Romania in 2021 was 1.88 million tons.

The TMO auction generated the following results and we notice how the purchase level increased on average by 15-17 USD compared to the previous auction on October 26, which confirms the demand for goods generated by destinations that understand the overall negative balance. Looking back at the CPT indications some time ago, we see an increase of 25-30 EUR/MT for feed barley.

Corn market

The indications of corn in the CPT Constanța parity on November 26, 2021 gravitated around 252-254 EUR/MT. The price support comes, as we said in the last issue, from the aggregation of 4 factors:

- US industrial demand (ethanol);

- Drying costs generated by goods with higher humidity;

- China, which supplies itself from Ukraine;

- Wheat, which supports traction in corn.

In Romania, corn harvesting continues, but the humidity is particularly high. We note problems with humidity in all areas of the country where it is still harvested (and we refer to central and northern Romania). The harvested lots have a humidity of 18-27%, which requires drying costs. These drying costs are starting to increase significantly and we already have a range of 3-4 EUR/1% extraction.

However, this price must be borne by someone and the costs are divided between the seller and the buyer in different ways.

- The first option is the one in which the seller has no option and settles the entire service invoice generated by the service provider (in many cases the buyer of the goods) from the contractual price.

- The second case is the one in which the seller has the option to dry the goods on his own premises and thus can generate the goods at the quality standard of 14% in terms of humidity. At that time, he is the one who includes the drying costs in the price of the goods. The increase in the selling price is practically borne by the buyer, who, however, has the advantage of receiving goods at a humidity standard.

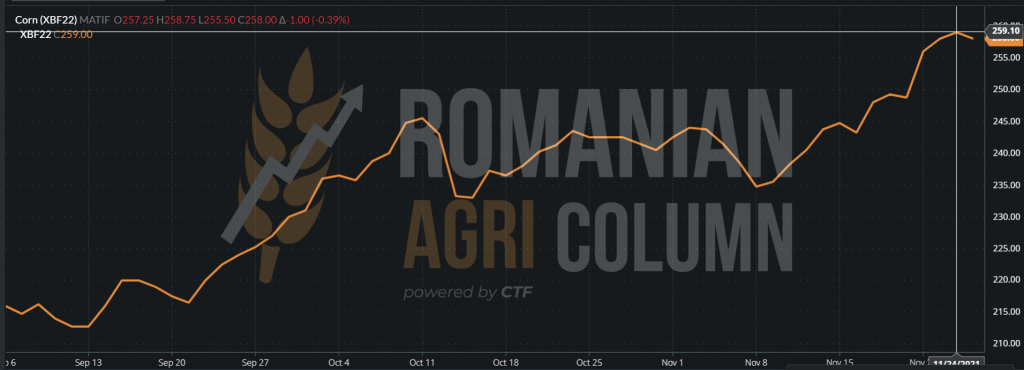

The indications of EURONEXT experienced a rebound generated by the imminent impact with the new strain COVID-19, after reaching a level of 259 EUR on 25 November 2021.

EURONEXT XBF22 CORN (November 25, 2021)

We noted the decrease and decline generated by this factor which impacted the global market, up to 254 EUR, a decrease of 5 EUR. The buyers from the Port of Constanța have effectively closed the transactions until the clarifications that will surely come in the following days, counting in this sense also on the weekends of November 27-28, 2021.

CORN – EURONEXT XBF22 IAN22 – 254,25 EUR

Until November 26, 2021, the corn market in the Black Sea basin was extremely dynamic, taking advantage of the closed American market due to the celebration of Thanksgiving and we record quotations of 253-254 EUR/MT in the FOB CVB parity.

Ukraine is at a harvest level of 87% for maize, which leads to a total of 35 million tons so far, a final estimate of 39.5 million tons. However, this quantity will normally be penalized by the excess humidity present in the goods. Our conclusion is a total of 37 million tons of goods at the humidity standard of 14%.

Russia has reached the level of 14.6 million tons of corn harvested so far, on an area of 2.7 million hectares. The export duty attached to maize is 54.3 USD/MT for the following week.

The European Union reached the level of 4.8 million tons of imports and intra-community trade from the general estimate of 15 million tons for the 2021-2022 season. The total import estimate is based on an EU production of 67.6 million tons and an import level of 15 million tons last season. Spain is a detached leader in imports, and their current level is 2.17 million tons. Last season, Spain imported only 5.63 million tons, after reaching and exceeding levels of 7.35 and 7.65 million tons, respectively.

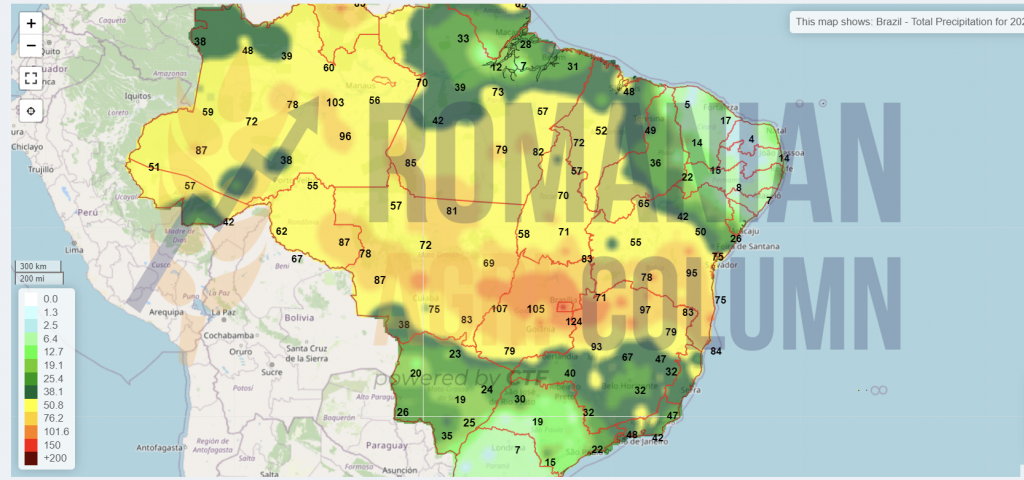

Crossing the Atlantic Ocean, we make the first stop on the South American continent, where the premises of a very good corn crop are in place. Brazil is watered by rains and the benefits are seen in the estimated potential of 124 million tons.

In the USA, the corn harvest is at the level of 96-97% and we can say that in a few days the process will end. Last week’s US corn sales totaled 1.43 million tons. Reported YOY, it is 7% less. Last week’s top buyers in the US are Mexico and Canada, with China buying only soybeans.

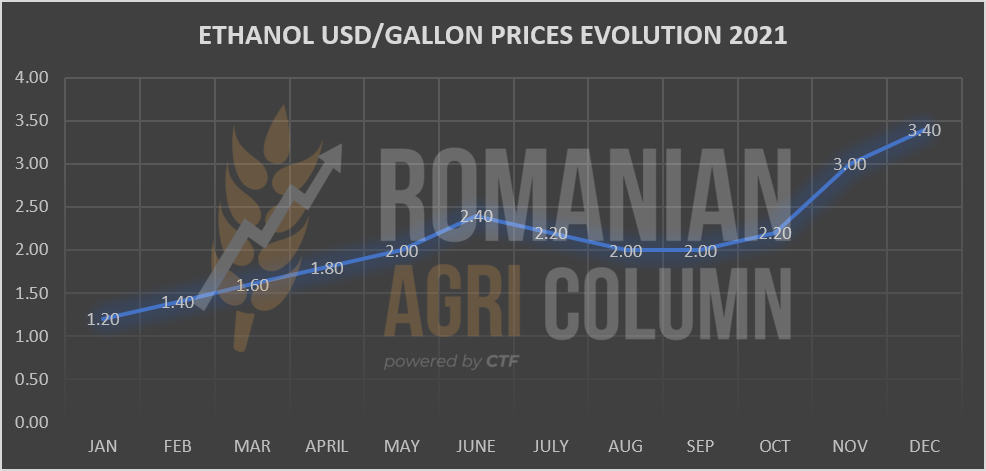

The price of ethanol in the US is rising rapidly, driven by the price of fossil energy and demand for the transportation sector. Iowa, Nebraska, South Dakota and Kansas, representative states of Corn Belt, reported price variation from January to date, according to the chart below:

ANALYSIS

- The foundations of the corn market are in place.

- Demand for corn in the industrial sector is being met by US ethanol.

- The Black Sea basin remains the driving force in the area for the time being.

- Drying costs fuel the price of corn.

- Wheat remains a factor in the price of corn.

Rapeseed market

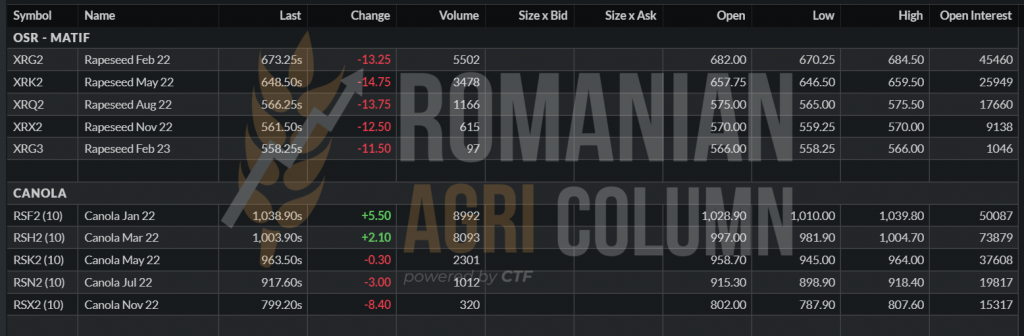

The indications of rapeseed have decreased due to the correlation with fossil energy. We noticed the drop below the level of 700 EUR in Euronext, which automatically led to a price level of about 685-687 EUR/MT in the parity of FOB CVB (Constanta-Varna-Burgas). The availability of rapeseed decreases as time goes on. Small lots are traded, but the order of magnitude does not exceed 1,000-2,000 tons yet.

Processors still have an interest in rapeseed. They will exchange from processing sunflower seeds to rapeseed to honor their biodiesel contracts. Coverage is sufficient at this time, but any batch is welcome, as the demand for biodiesel is adequate. Another report that generated a decrease in Euronext quotes is the announcement of a lockdown in several European countries, which restricted consumption in the next period and we refer to the demand for fossil fuels. As I said, there is a correlation in the energy market that provides support or degrades rapeseed as an element in this complex.

Closing indications from November 24, 2021 are increasing. Oil is on the rise, despite the US announcement of the release of reserves from its own stocks to support the price of fossil fuels. However, these stocks are actually too small to support the attempt to maintain the price level. To this aspect we add the differences of opinion within OPEC, Russia and Saudi Arabia being the main actors.

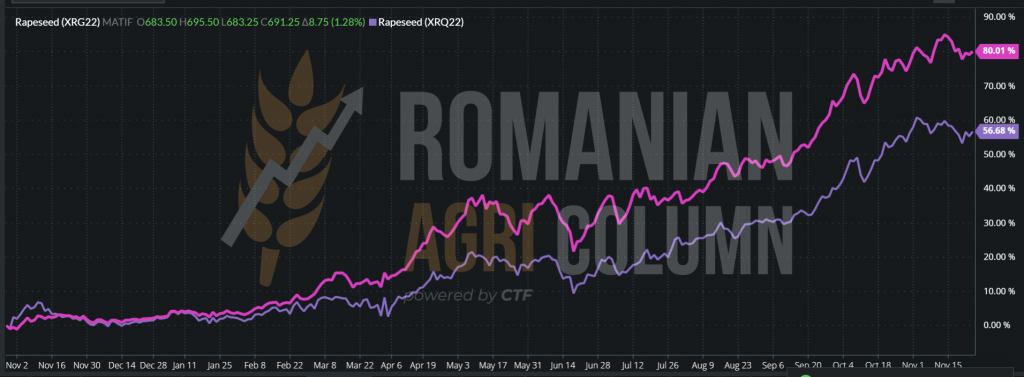

XRG22 + 8.75 EUR | 691.25 EUR. XRQ22 AUG22 – 580 EUR (crop inverse of 110 EUR is maintained).

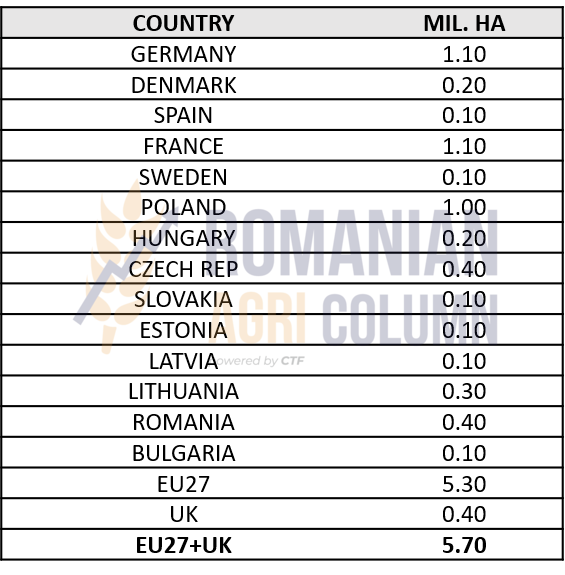

The new crop, that of 2022, is announced to be one within normal limits at this time. We have a positive note generated by a growing number of hectares at European level and, if we add the growth in Great Britain, we get a number of 300,000 hectares more than last year, 5.7 million hectares, compared to 5, 4 million hectares.

A calculation made on the European average of rapeseed production indicates through these 300 thousand hectares a production potential of about 1.1 million tons. And so we can have a rough estimate of European production for next year of 20.75 million tons, calculating the European average at 3.64 tons/ha.

Productivity leaders per hectare remain countries such as Germany, Denmark, Poland and France. Romania registered a significant jump during 2021, the average productivity per hectare increasing from 2.6 tons in 2019-2020, to a level of 2.9 tons in 2020-2021, despite the drought and ending the 2021-2022 season with a production of 3.42 tons per hectare obtained from 390,000 hectares.

COMPARISON EURONEXT XRG22 FEB22 – XRQ22 AUG22. We observe the percentage increase of the XRG22 indication due to the uncovered demand and the XRQ22 cadence generated by an extra hectare at EU + UK level.

But the rapeseed road must go through another winter and a spring, time that will generate changes. Whether they are positive or negative, we will all be their witnesses on the journey to the 2022 crop.

What we need to remember in the current context are the fundamental elements of supply and demand, the support of the price of rapeseed generated by fossil fuels, inflation and the costs of setting up the crop, associated, of course, with the weather.

EURONEXT XRG22 – closing November 26, 2021, effect of the announcement about COVID19

Sunflower seed market

Price indications in the parity of CPT Constanța or DAP Processor are around 650-660 USD/MT. The only exception is an exporter who has a ship of 40,000 tons to ship and his offer is more consistent with 10-20 USD/MT. In the country, batches of sunflower seeds do not move. We note only very small quantities, of the order of hundreds of tons, traded zonally, with prices in the area of 660 USD/MT.

However, farmers must also see the RON/USD parity, which, due to the strengthening of the American currency, already has another result in conversion. Having a past benchmark of 4.15 RON/1 USD, a price of 660 USD has another value now. At the level of RON 4.15, a ton was valued at RON 2,739 in conversion, and today, at the same price level of USD 660, we have a converted price of RON 2,910.

From the point of view of availability, the transaction estimates of the Romanian sunflower seed harvest reached the level of 72-74%, out of a crop of 3.3 million tons. This means an availability of about 825,000-850,000 tons remaining to be traded. Processors need these resources and will compete for retention in the country. However, as we have pointed out in previous issues, support mechanisms need to be set up in this action. Food safety is a priority and not something else. Compliant actions, support actions from the Romanian state are desirable in ensuring food security. Romanian processors have high manufacturing standards, respecting HACCP norms and product traceability. Thus, manufacturing costs are also perhaps higher compared to other processing units outside Romania. There are solutions, but they only need to be applied and we only refer to two of them, subsidizing storage within a network of locations, which apply the same standards and where there can be traceability on the product and attached coupled support for farmers selling to processors in Romania, so that the added value is attached to the production of sunflower seeds and, implicitly, the Romanian state can reach two targets: food security and primary and related taxation. It is, if you will, a kind of balance that marks a normality.

Turning to the situation of stocks and production at EU level and the Black Sea basin, we can generate a calculation that tells us that things are not as balanced as they are thought to be. We start from the working premise that sunflower oil has no substitute in the European diet and the Black Sea basin. It is practically non-existent due to decades of food culture and the EU’s tendency to restrict access to palm oil as much as possible, which has deforestation as its main basis and is therefore contrary to European rules.

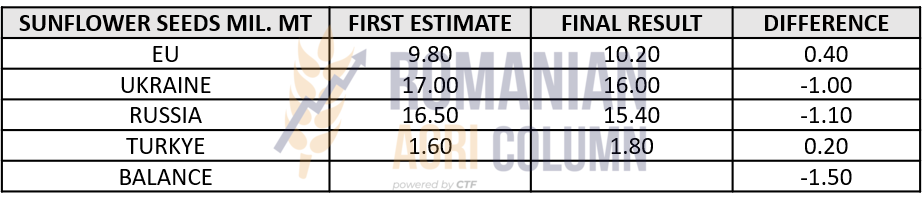

Ukraine had a crop target of 17 million tons and all conclusions lead to a crop level of about 15.8-16 million tons, so a deficit of about 1 million tons. In this context, the reluctance of Ukrainian farmers to sell plots is noticeable, as they are today at a sales level of about 32% compared to 54%, the average of the last 5 years. This creates additional pressure on processors who only have stocks to process for 30-45 days, given that demand is high and the 276 USD Russian tax pressure that will take effect on December 1, 2021 will generate higher levels.

Russia had a crop target of 16.5 million tons and the indices show a maximum level of 15.4 million tons, a deficit of 1.1 million tons. To this deficit are added the political factors of withholding of the raw material materialized by the export tax of ½ in the amount of one tone and attached to a level of taxation of the export of crude oil of 276 USD/MT.

The EU indicates a higher-than-initial crop, with values of 10.2 million tons, about 0.4 million tons in addition to the primary crop indication. To these figures we add the fact that the EU has at this time a much lower level of raw material imports than the average of previous years, which is caused by the sufficiency in production at European level.

Turkey harvests 0.2 million tons more than last year, from 1.6 million tons to 1.8 million tons. Turkey is currently importing crude oil at zero import duties, but after January, they will traditionally start looking for raw materials.

ANALYSIS

- The demand for sunflower seeds still exists and is sustained.

- Local stocks still exist and are available amid farmers’ reluctance to sell.

- At regional level, the European surplus is balanced by the production deficit in the Black Sea basin.

- The price trend for December and January 2021 shows to be stable.

- CVB FOB indications are at the level of 700 USD/MT.

- Black Sea quotations indicate 1,400-1,410 USD/MT.

- Raw material price indications in Ukraine increased to the level of 20,500 UAH/MT, equivalent to 758.5 USD/MT, VAT 20% included.

The soybean market

On the Romanian market, soybeans are traded at the level of 620-630 USD/MT, but in small batches of hundreds of tons.

The quotations of soybeans have gained some consistency in the period from November 15 to today. CBOT has shown traction in this regard and we see recovery after the USDA report of November 9, 2021.

US export inspections showed a sales level to China of 1.2 million tons. These quantities do not include sales of about 330,000 tons from the previous week, but with an unknown destination. In absolute terms, China’s imports of soybeans from its origins are 41% behind the same period last year. Now they are at a level of 5.15 million tons.

Brazil reported soybean sales of 3.3 million tons in October, 22% less than the previous year in the same period (4.23 million tons). Adding to total sales, there are a total of 5.11 million tons of soybeans sold to China, 41% less than last year.

These days, business in the US is closed due to Thanksgiving, so any potential for sales moves is pending.

Brazil has reached the level of 90% in soybean planting, and the rains that will not be long in coming will boost the future crop in the already existing premises of 142 million tons.

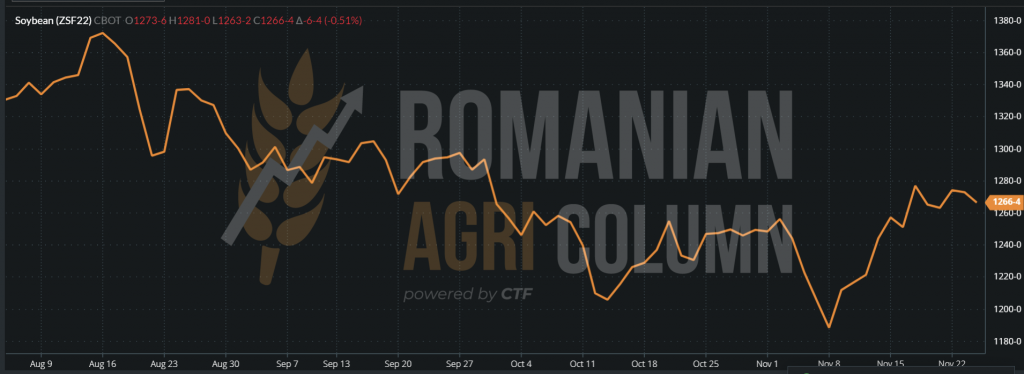

CBOT – soybean trend at the closing of November 24, 2021

CBOT ZSF22 – effect of the COVID-19 announcement

Fossil energy

EUR-USD parity

Weather forecast

28 November – 5 December 2021

Romania

Europe

Russia (snow)

Ukraine

USA

Brazil

Argentina

China

Australia

© Romanian AGRI Column, 2021, all rights reserved