This week’s market report provides information on:

LOCAL STATUS

Indications of wheat in the port of Constanța reside in values of 325-327 EUR/MT, with the usual discount of 20 EUR/MT for the quality of feed wheat. In the local market, processors are offering prices between 318-325 EUR/MT. We therefore have a competitive market from this point of view, where demand and supply create the conditions for free trade.

Goods from the Republic of Moldova and Ukraine are offered at the level of 300 EUR/MT in the country for processors and traders. Naturally, these goods are a competition for the Romanian ones. At this time, we have an import level of over 200,000 tons of wheat from the above-mentioned origins. Especially in the north-eastern area of Romania, major distortions are created in the market, and Romanian farmers are clearly disadvantaged from this point of view.

Wheat sowing has started in Romania and we already have a proportion of at least 10-14% sown from the usual 2.15 million hectares.

CAUSES AND EFFECTS

Holding on goods did not go in the direction that many expected, and the levels actually fell, just as we predicted. Regional volume pressure weighed heavily in the balance.

Another reason to mention is the desire to move into the new fiscal year, in other words to reduce the tax base related to 2022. This is a goal for a large mass of farmers.

At this moment, however, the farmers are busy with the autumn sowing, with the harvesting of the sunflower crop and the corn or what is left of it.

One effect that we reiterate, because it needs to be reminded, is that we cannot have a positive path in terms of the price of wheat. Regional volumes weigh very heavily, demand is extremely low at the moment, and regional competition does not position Romanian wheat in a very comfortable position.

Only one aspect can generate an increase and that would be a possible deterioration of the local geo-political situation. But now this is not on the horizon. The green corridor still has days to cross until it expires, and the recruitments announced by Russia are just beginning.

Also, the mock referendum that will certainly generate a situation of force for Russia will not be recognized by the international community, but will generate a so-called legitimacy to act. But to act you need a regular and trained army, which Russia cannot generate at the moment.

REGIONAL STATUS

RUSSIA once again flaunts its production with a new level that defies logic, namely 100 million tons. Yes, it may be true, but we must take into account the looted wheat from Ukraine, which is included in this number evoked by the Russian analysis houses.

UKRAINE is staying at the same volume level and it’s off season.

The EUROPEAN UNION also receives, as we well know, a surplus of 0.8 million tons. But the Union is also out of season at the moment.

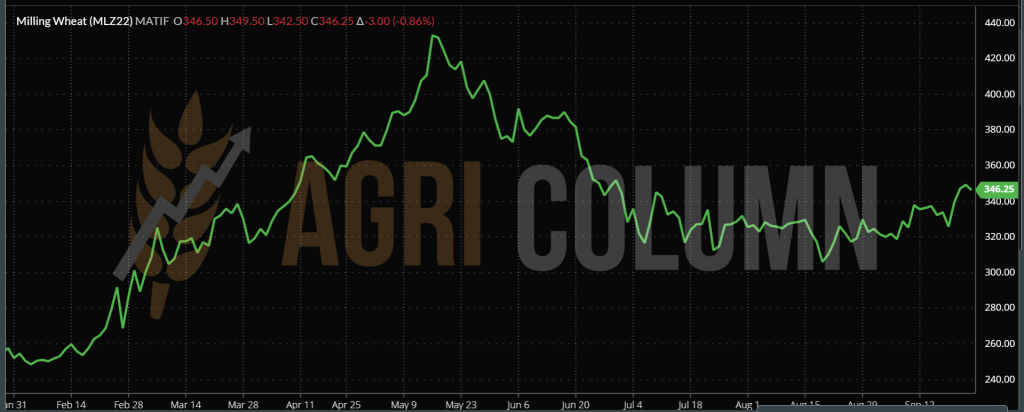

EURONEXT MLZ22 DEC22 –346.25 EUR (-3 EUR)

EURONEXT WHEAT TREND CHART – MLZ22 DEC22

GLOBAL STATUS

In CANADA the wheat harvest is in full swing and the forecast holds. But we have potential there as Hurricane Fiona approaches. It is not possible to assess the direction at this time and how it will enter Canadian territory, but the warnings are there.

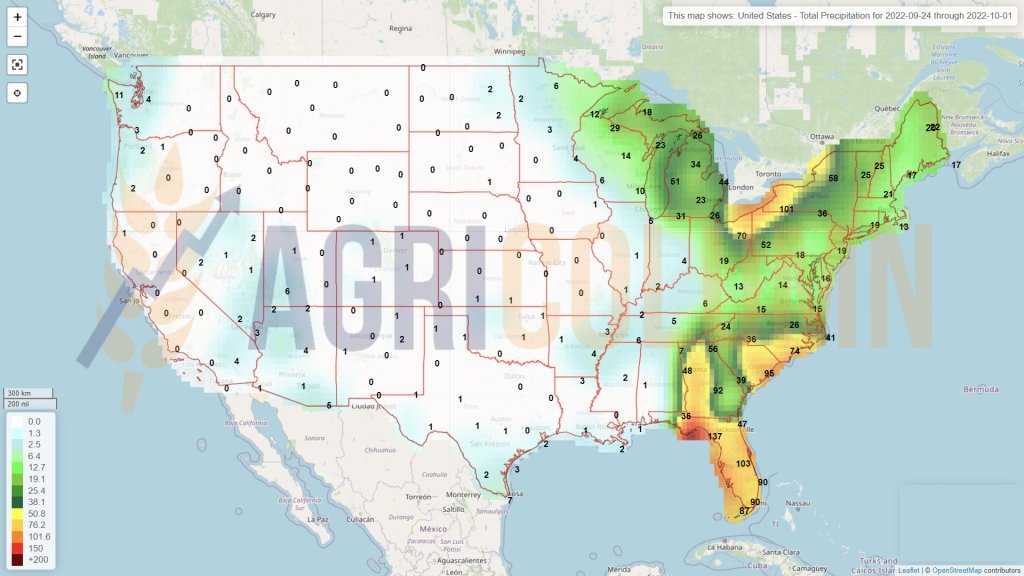

US is fast approaching the end of the spring wheat harvest and no major changes are seen, so the volume forecast remains the same.

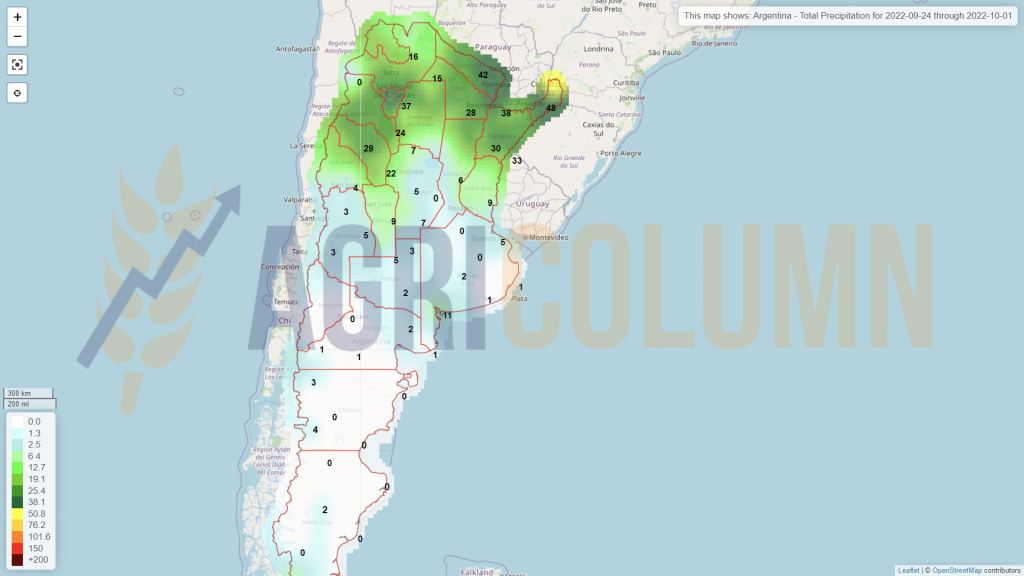

ARGENTINA has special problems. Argentine wheat is not in good condition. The good to very good rating is at 14%, down from 50% a year ago and from 31% as an average over the last 3 years. Certain areas register abandonment, that is, farmers no longer tend the crop. We remind you that Argentina took a wrong turn in the season, sowing only 6 million hectares, compared to the expected 6.5 million. The Rosario Grain Exchange cut its estimate for Argentina’s wheat crop to 16.5 million tons as drought reduced production potential.

BRAZIL it is by far a surprise. With a crop level of 11 million tons, it becomes self-sufficient. Normally, Brazil imported about 6 million tons from Argentina. But this season, Brazil saw this increase in volume, from 7.4 million tons in 2021 to 11 million tons in 2022.

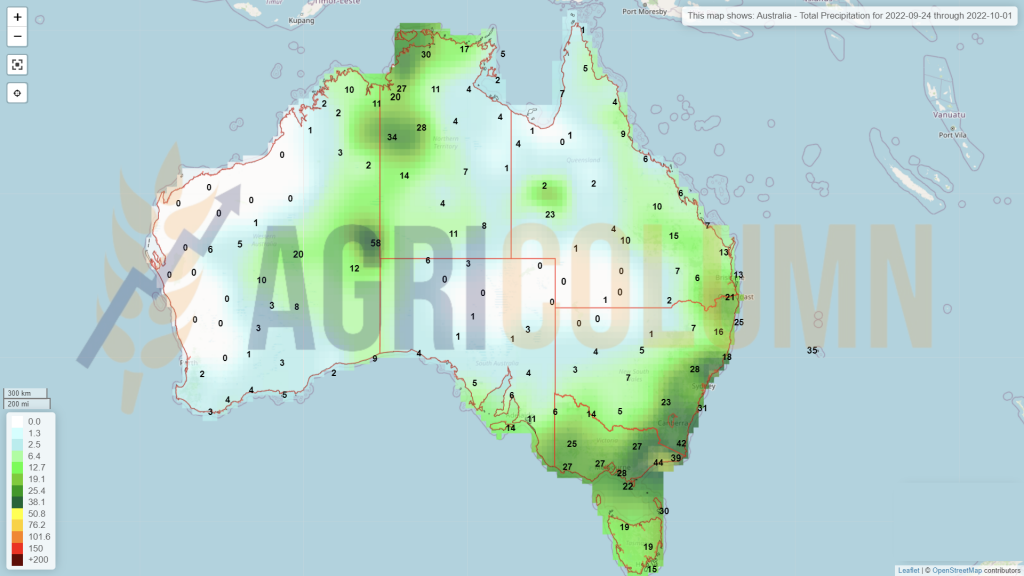

AUSTRALIA remains unchanged and we await the entry into the fields for harvesting and for this area from Antipodes. The forecast volume remains unchanged at the moment, but we could see positive swings due to the recorded rainfall volume.

CBOT ZWZ22 DEC22 – 880 c/bu (-30 c/bu = -11 USD)

CBOT WHEAT TREND CHART – ZWZ22 DEC22

TENDERS

SAGO SAUDI ARABIA purchased a volume of 535,000 tons of milling wheat for delivery November 22, 2022 – February 23, 2023. The protein parameter was set at 12.5%. Port planning, price levels, and vendors below:

Jeddah Port:

- 65,000 tons Cargill at $366.65 C&F (Nov. 10 – Nov. 25)

- 55,000 tons LDC at $368.75 C&F (Nov. 10 – Nov. 25)

- 65,000 tons Cargill at $368.70 C&F (Feb. 10 – Feb. 25)

Yanbu Sea Port:

- 63,000 tons Holbud at $371.68 C&F (Dec. 10 – Dec. 25)

- 63,000 tons Holbud at $372.78 C&F (Jan. 10 – Jan. 25)

- 65,000 tons Cargill at $367.90 C&F (Feb. 10 – Feb. 25)

Dammam Sea Port:

- 60,000 tons Solaris at $375.88 C&F (Nov. 10 – Nov. 25)

- 65,000 tons Cargill at $373.20 C&F (Feb. 10 – Feb. 25)

Jizan Sea Port:

- 55,000 tons Cargill at $380.20 C&F (Jan. 10 – Jan. 25)

TCP PAKISTAN has launched a tender to buy 300,000 tons of milling wheat, delivery October 2022. Deadline for submission of offers is 26 September 2022.

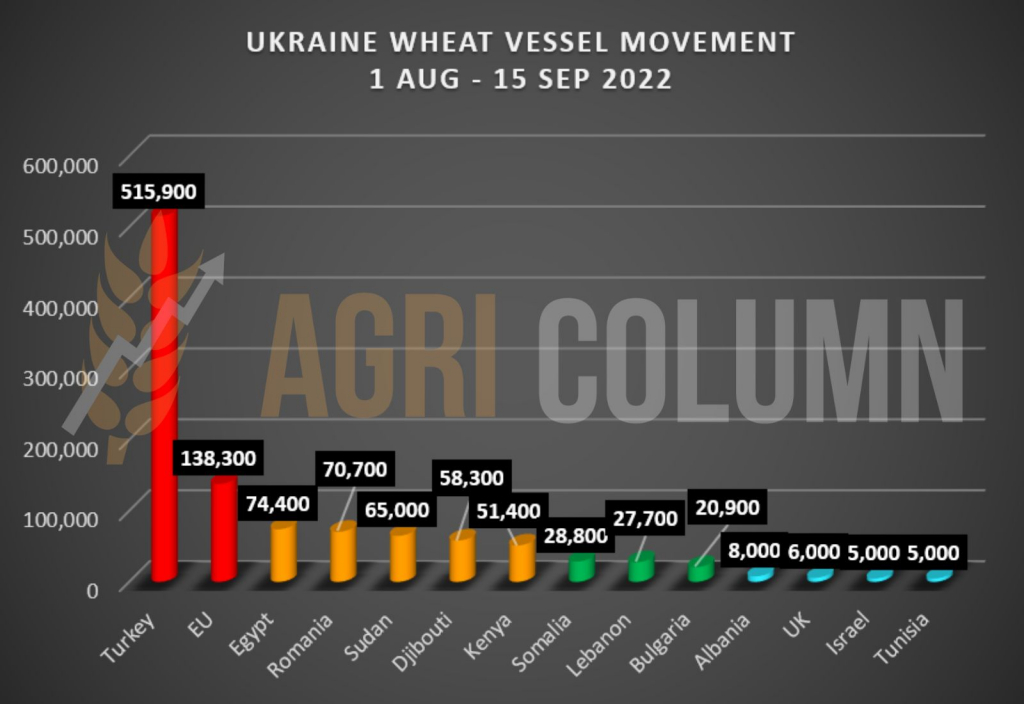

POC GREEN CORRIDOR (PIVNYI, ODESSA, CHORNOMORSK). We have the data on Ukrainian wheat deliveries from August 1 to September 15, 2022. In the transparency we are used to, we will visualize where the Ukrainian cargo went during this period.

CAUSES AND EFFECTS

The first cause of the wheat increase on the stock exchanges, Euronext and CBOT, was Mr. Putin’s announcement of the partial mobilization of 300,000 reservists, in the context of which Ukraine was dominating with a counter-offensive of proportions, managing to push the Russian red tide back from many areas and thus to reconquer territories. This news caused a great deal of excitement and was a “reason” for trading algorithms. Thus, hedge funds bought positions in the commodity wheat and, implicitly, prices went up.

But the physical market remained somewhat unmoved by this emotional wave. It reacted only 8-10 EUR/MT in CPT Constanța parity. Why? For 2 reasons, the first being that Romanian wheat was not competitive anyway, and the second is an operational one par excellence.

Recruiting 300,000 reservists when they don’t want to is an extremely difficult operation. In vain, Russian propaganda presents images of highly motivated citizens who want to go to war. They, in fact, do not want this, and the reality indicates real exodus to the borders and people of a lower condition under the influence of alcoholic beverages. Let’s not forget that winter is coming and I don’t think it’s an easy thing to recruit 300,000 men, equip them, train them and send them to the front. With what? With the same poor and outdated military equipment? Without modern resources missing due to sanctions? It will take longer and we estimate a long time horizon, of at least 3-4 months.

During this time, Russian wheat has nowhere to be stored and must be sold. It is extremely simple. With sanctions also set to apply to Russian oil, the revenue streams must be there to fuel the Russian war machine. I remind you that from December, 2 million barrels of monthly oil will no longer be shipped to the European Union. And what will Russia do with this surplus? Friendly destinations, India and China, have obligations in turn (India to Saudi Arabia in particular). It will be very hard on Russian financial resources, and the wheat must be sold. The Green Corridor will be maintained, otherwise their small ships will no longer have access to other ports to unload wheat.

The Argentine damage is not a cause for concern at the moment. It is so far, if you like, a part of the export to Brazil, which will no longer take place due to the rich Brazilian crop.

After 2 days of stock market excitement, the profit taking episode happens, i.e. the funds extract their profits. And we see that in the CBOT close, down 11 USD on the DEC22 indication. Extremely predictable and not at all new. This is fueled by the FED’s decision to increase the interest rate by 0.75%, in full agreement with the original plan. And we will all see more and more hedge funds moving their interest into areas other than commodities.

It is only a matter of time before the liquidation of the current positions and the realization that money has become more expensive, and the risk of not covering the financial costs is much greater than the risk of making a profit.

Thus, we estimate that in the absence of a reckless decision by Mr. Putin, wheat will continue its flat course in terms of prices for the next period as well.

LOCAL STATUS

The price indications from the port of Constanța are summarized around the value of 270 EUR/MT, without being of particular interest in this period. Some buyers are placing offers at 260 EUR/MT, while others are still offering 270 EUR/MT.

REGIONAL STATUS

MIT JORDAN Jordan did not purchase any quantity of barley during the tender on Wednesday, September 21, 2022. The intention to purchase 120,000 tons did not materialize due to the failure to meet the number of participants. Only Cargill and Viterra participated (and the minimum is 3 participants). A new tender for the same volume is expected to end next week.

CAUSES AND EFFECTS

We still don’t have a very good picture of the barley price path. The demand is there, but the price is penalized and pressured by feed wheat and corn in the Black Sea basin. We do not foresee a return in the next period. Romania imported a volume of 55,000 tons of barley from Ukraine.

LOCAL STATUS

Corn price indications in the port of Constanța remain around 285 EUR/MT. We have no change from the previous days. The market remained exactly at the same levels.

In the local market, we continue to see interest held at 280-285 EUR/MT on the DAP Buyer condition. We have to admit that goods of Ukrainian origin continue to create distortions in the market and this aspect creates a great handicap for Romanian farmers.

CAUSES AND EFFECTS

The rate of harvesting has reached the level of 20-23% locally, and the lack of volume does not categorically influence the price. The proximity and availability of Ukrainian and partly Moldovan goods creates the effect I was talking about above.

Apart from that, the sight of Ukrainian harvest volume, as well as continued 2021 cargo flows from Ukraine, cause the price to remain in the same set as before. Romania has so far imported a volume of 300,000 tons of Ukrainian corn.

REGIONAL STATUS

UKRAINE still sees the corn crop at 31.5 million tons, but we foresee some problems with the rainfall not holding back and making the commodity unable to be harvested. Moreover, they will have to include the cost of drying, which could boost the price of corn by a minimum of 5-10 EUR/MT, estimating an extraction percentage of at least 3-4 percent multiplied by a minimum cost of drying and handling.

RUSSIA remains in the forecast, but it is extremely hot. Not bad at all for ripening and harvesting at this point.

EUROPEAN UNION. According to COCERAL, the Association of European Traders, the EU-27 maize crop for 2022 is now seen at just 51.9 million tons – well below the previous forecast of 66 million tons and down from 70.2 million in 2021 – due to significant downward revisions for a number of countries due to hot and dry weather during the pollination period, notably Hungary, Romania, France, Italy and Germany. Instead, Poland will deliver 7 million tons of corn (the third producer in Europe, after France and Romania).

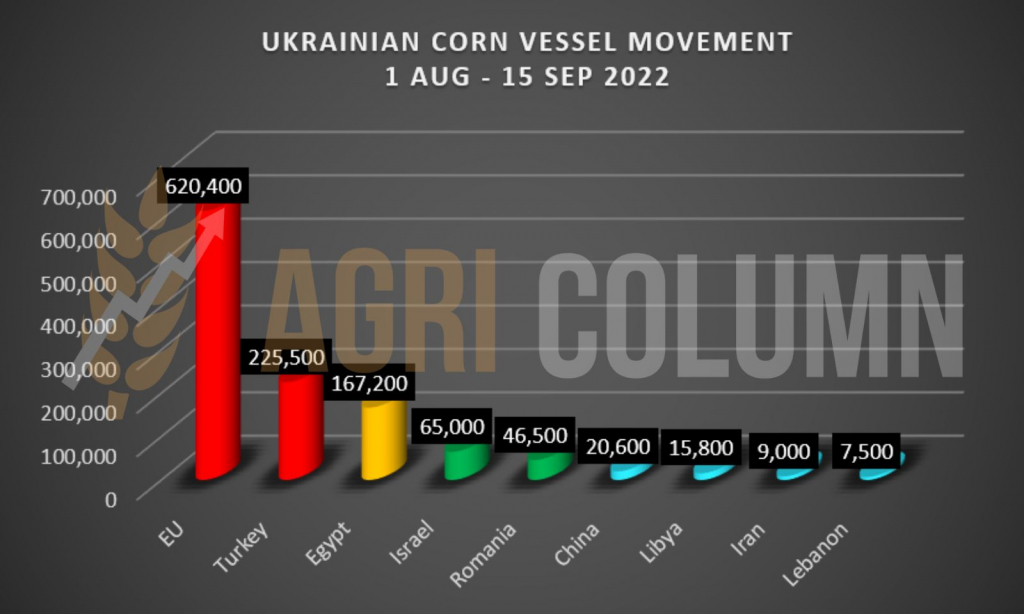

THE GREEN CORRIDOR. We also have here the transparent data about the volumes and their destinations:

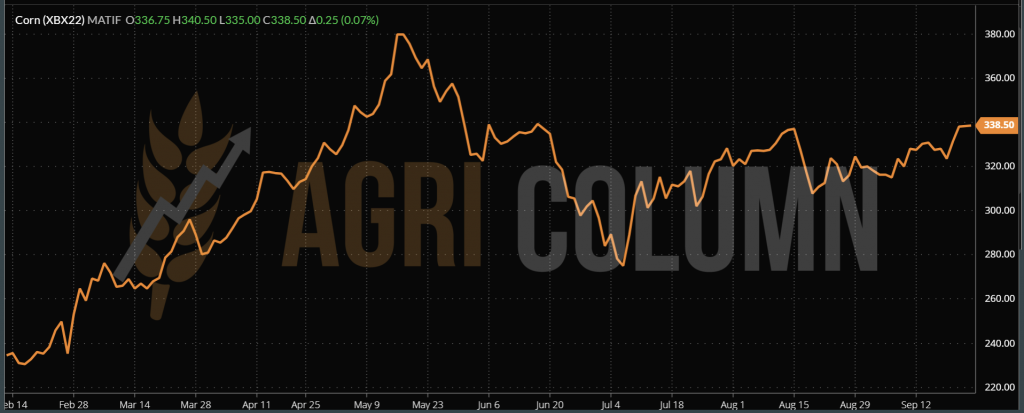

EURONEXT CORN – XBX22 NOV22 –338.5 EUR

EURONEXT CORN TREND CHART – XBX22 NOV22

GLOBAL STATUS

The US harvest corn and have reached 8-10% harvest level. By some measurements in Kansas, production is not good, in some places even disappointing.

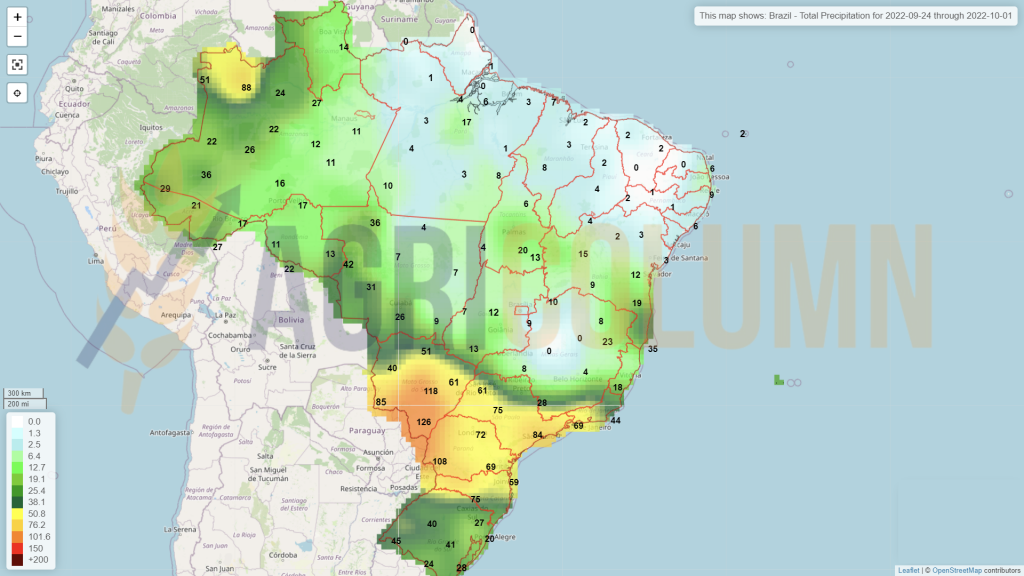

BRAZIL and ARGENTINA have no changes in substance as far as the corn crops are concerned. They are practically out of season.

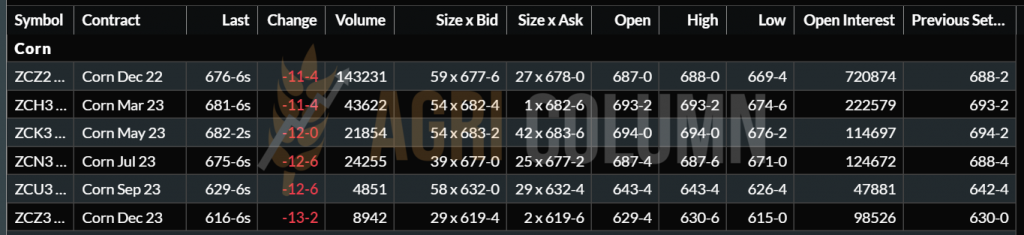

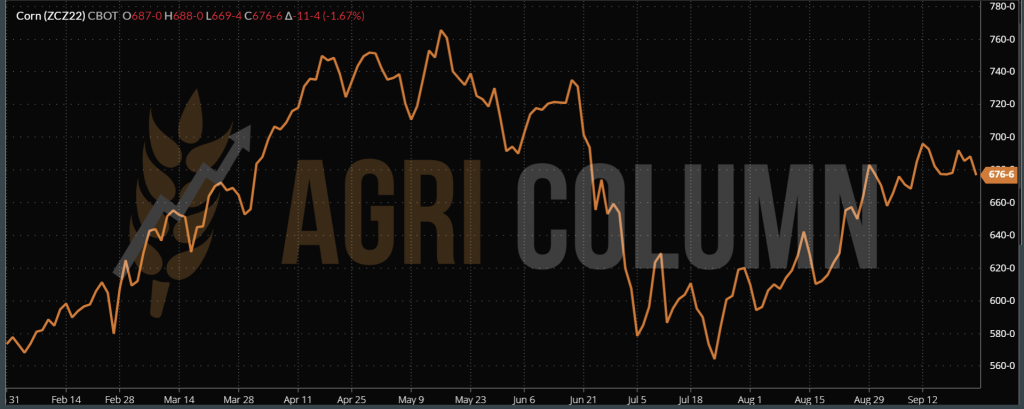

CBOT CORN – ZCZ22 DEC22 – 676 c/bu (-11 c/bu = -4.3 USD)

CORN TREND CHART – ZCZ22 DEC22

CAUSES AND EFFECTS

First of all, I want to say that we are in a period of calmness in the price of corn. It is generated by the harvest started in the US, on the one hand, and the expectation that Ukraine will start harvesting corn, on the other hand.

What is seen early on is a smaller harvest perhaps in the US, but offset by Ukraine. At the level of the European Union, a lack of production is clearly visible, but it will also be compensated by Ukraine and by replacing it with feed wheat through imports at discounted prices.

To all that the decrease in consumption comes, which maintains the current corn price level. China will also buy part of this discounted crop from Ukraine in the coming period. So the demand will be covered and we mean the major demand.

The FED, in turn, moderated speculative temptations by correcting the monetary policy interest rate. In this way, it has cut the momentum of the funds, but we can have the following events that can bring positive corrections in the price of corn, provided that they come to pass. Cumulatively or one by one, they will generate price-increasing effects, as follows:

- The Ukrainian harvest will receive an increase in cost due to the rains that do not seem to stop in the coming period. By default, there will be drying costs that will be added to the price.

- The delay of the Ukrainian harvest will not create problems, the deliveries from old stocks are maintained and therefore it is not a parameter of price increase, but of maintenance.

- The hurricane forming off NOLA, Louisiana, near the Caribbean, which may affect, as it has done before, US port facilities. For now, this hurricane is in the formation phase and we will keep an eye on the situation in that area.

- CBOT versus EURONEXT. We note that Euronext is extremely high relative to CBOT, and the physical market is attuned to CBOT, as it should be, by the way. It makes absolutely no sense in the Euronext matrix-10(12)EUR = Constanta. It is a misleading effect generated by the Russian invasion and perpetuated by algorithms, together with the disappearance from European production of 18 million tons, a fact that benefits French farmers, but creates extremely big problems in Romania, Poland, because of the discounted flows that cross these two countries.

LOCAL STATUS

The price indications related to the port of Constanța remain in the usual working regime, namely NOV22 minus 20-30 EUR/MT. In the local market, processors indicate NOV22 minus 15-20 EUR/MT.

But in European statistics, Romania appears with a rapeseed import level of 280,000 tons, an extremely high figure, if we consider the local production of 1.56 million tons. Naturally, we are talking about Ukrainian goods intended for the processing and production of bio-diesel.

REGIONAL STATUS

Here we have no obvious changes, in the context where rapeseed is out of season. The situation is identical for Ukraine, which is, in turn, off-season, and cargo volumes have gone the way of the EU.

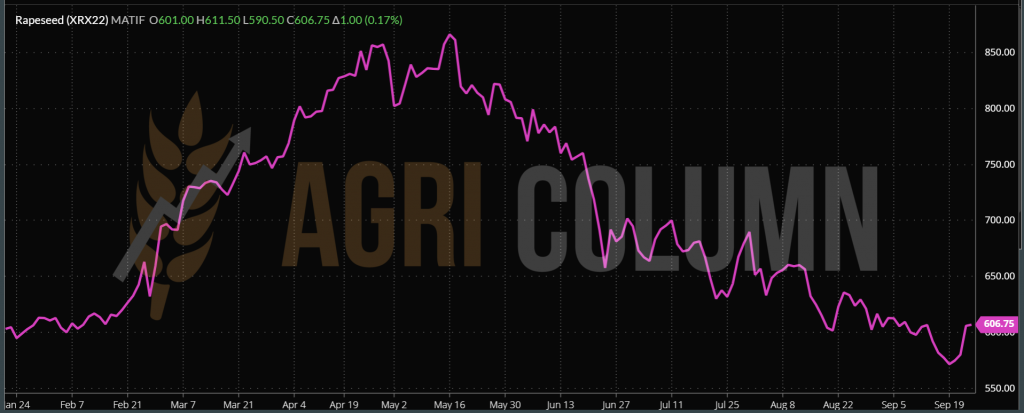

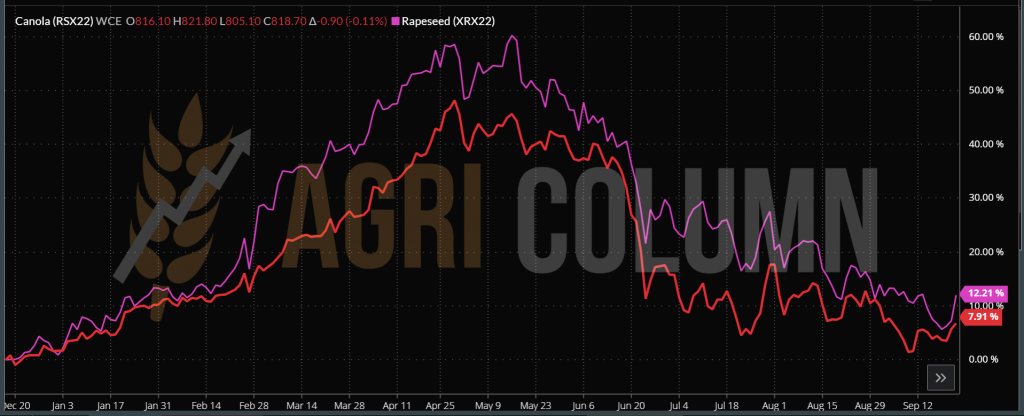

EURONEXT XRX22 NOV22 –606.75 EUR (+1 EUR)

EURONEXT RAPESEED TREND CHART – XRX22 NOV22

ICE CANOLA RSX22 NOV22 – 818.8 CAD

CANOLA TREND CHART – RSX22 NOV22

EURONEXT RAPESEED VS. ICE CANOLA (NOV22)

CAUSES AND EFFECTS

Our estimate of the increase in the price of rapeseed came in earlier than we expected. And things tend to be weather-related:

- The Canadian crop is penalized by 0.4 million tons.

- The imminent passage of Hurricane Fiona, particularly over the Manitoba region, creates risks and thus ICE Canola is reacting, also fueled by the shortage seen.

- Looking at the indications of NOV22 and MAR23, MAY23 respectively, we see a potential of 10-12 EUR more if we stay at the current status. But things can change.

LOCAL STATUS

The price indications in the CPT Constanța parity are between 530-535 USD/MT, in total agreement with what is also paid at the level of the processing units. But the queen of the ball every day is the commodity called “high oleic sunflower seeds”. The related bonus has increased to over 100 USD/MT.

However, the proximity of the plains of western Romania presents a visible advantage over this category of goods. Bonuses of 130 USD/MT can also be paid there.

The explanation is extremely simple and I have been predicting it for at least a year. The pandemic has restricted HoReCa activity. Consumption was extremely low, and as a direct consequence, the bonus for this item became very low.

Now, after the pandemic, the HoReCa activity generates extremely active demand, and the raw material is not enough to feed the demand. The companies that produce this oil, HOSO, have multi-year contracts, and the pricing is obviously based on market conditions.

In Romania, the harvest is coming to an end, and we estimate well that the end of the month will not reach us and we will finish harvesting sunflowers. The final estimate will not exceed 2.2-2.3 million tons. We are thus in the official figures and once again agreeing on the crop forecasts and proving accuracy in the forecasts from start to finish.

REGIONAL STATUS

UKRAINE has quite serious problems related to the delay in harvesting. The consistent rains of the last 10 days leave no window to harvest and the harvested goods so far do not exceed 1 million tons. Stocks are lower by up to 2 million tons and the new crop harvest is late: 924,000 tons harvested on 15 September 2022 (10%) versus 2.38 million tons (17%) on 16 September 2021. Only 18 units of processing are in operation at this time.

These days, there is even a question of a temporary stoppage of the export of raw material, but not necessarily because of the volume, but because the Ukrainian authorities have lost control of the cargo flows and can no longer account for who paid the tax and if 8% export on sunflower seeds.

Sunflower seeds for the 2021 crop are no longer available. They were exhausted through domestic processing and exports to Romania, Bulgaria, Poland, as well as to other European countries.

RUSSIA will generate that gigantic volume of harvest, but will be hit by the processing and operational inability of the ports to ship the crude oil. We will all see how the raw material will literally start flowing out of Russia due to the inability to support processing and delivery through the ports. And so Russia has problems delivering oil through its ports, let alone crude sunflower oil. But 17.5 million tons is a figure that will put pressure on the price of sunflower seeds in the future.

CSFO (crude sunflower oil) shows on the OND band (October-November-December) a decrease, not dramatic, but still a decrease. The 6 Ports quote on Friday afternoon indicated 1,250 USD/MT OCT, 1,240 USD/MT NOV and 1,230 USD/MT DEC22. FOB Chornomorsk had an indication of 1,060 USD/MT OCT, 1,050 USD/MT NOV and 1,040 USD/MT DEC22. So, it has a downward trend, as we can see.

CAUSES AND EFFECTS

- The Ukrainian harvest is delayed due to rainfall and this aspect is keeping the sunflower seed prices level. But, when they come into force at harvest (full blast), the harvest pressure will generate a degradation at the level of the raw material. But if the rainfall will cause damage to the crop, we will see a support, that is, an increase in the price of the raw material.

- The Russian crop will be harvested in good conditions. We see excessive heat in Russia, which will lead to drying and a harvest in the best conditions. But they will be hit very quickly, at the end of January 2023 at the latest, by the lack of processing capacity and the lack of operational capacity in their ports.

- Argentina will have a good place on the price stage in the sunflower seed arena. Argentine farmers are sowing these days and a harvest of 4.25 million tons is estimated. But in Argentina there are extremely big problems because of the lack of precipitation and the cold. If the degradation will also include the SFS chapter in Argentina, we will see the instant positive correction in the whole VEGOIL complex, but especially in the price of sunflower seeds.

LOCAL STATUS

The purchase indications of those who process soybeans originating in Romania are at the level of 580 USD/MT. Those who transfer these non-GMO goods across the intra-Community border pay an additional level of price because they cannot provide certification for coupled support.

In Romania, up to this moment, we have harvested a level of 15% of the allocation to this raw material. And from the beginning of the season until today, we are at a level of 30,000 imported tons.

GLOBAL STATUS

Soybean harvest is at 3% and a little behind average, but planting was a little late this year as well. But the American harvest level remains at 123 million tons.

Weekly export data indicated that 446,364 tons of soybeans were sold, and total soybean contracts reached 25.73 million tons. This value increased by 11% compared to last season. China holds 13% more contracts than last year. USDA confirms sale of 136,000 tons of soybeans for delivery to China in 2022/23.

ARGENTINA. Following the launch of the soybean export stimulus program, soybean purchases in Argentina are already above the three-year average. Since the dollar-soybean program came into effect, 8.5 million tons have been traded on the local market in Argentina.

Argentine farmers continued to sell soybean stocks and reached the level of 62% sales of the 2021/2022 crop. At the same time, Argentina raised its forecast for soybean production in 2022/2023 to 48 million tons, from 47 million tons previously forecast.

BRAZIL. In the 2022/23 season, the central-west region of Brazil is expected to account for 46% of production, and the southern part of the country still has 30.5% of Brazilian production, but the share has been steadily decreasing. Attention is on southern Brazil to see if there will be a repeat of the drought this year, which reduced Brazil’s soybean crop by 20 million tons last year.

Brazil’s soybean exports are forecast to reach 4.152 million tons in September, according to ANEC, up from 4.471 million tons forecast last week, and Brazil’s soybean meal exports could reach 2.225 million tons this month, up from 2.114 million tons.

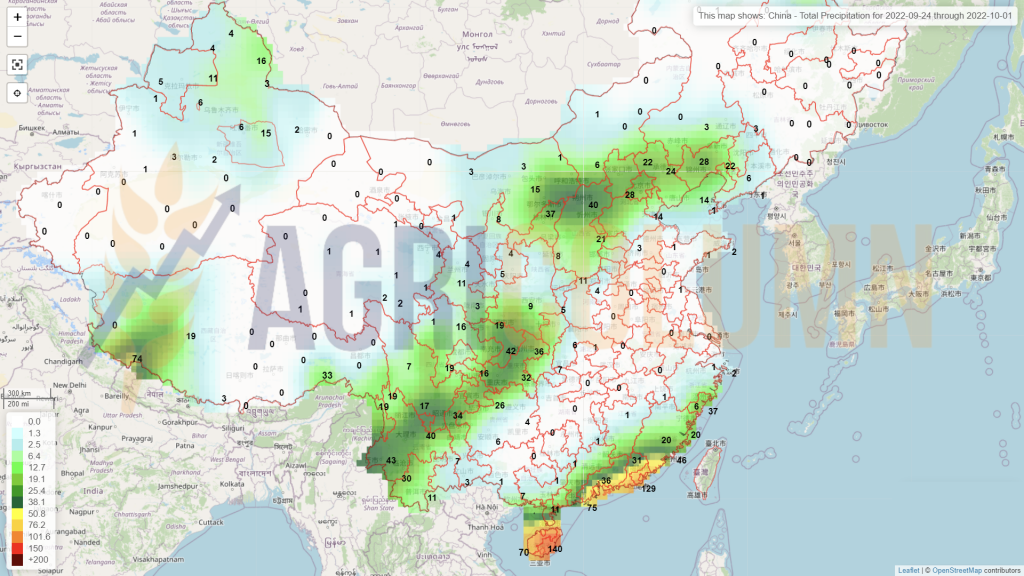

CHINA, the world’s biggest soybean buyer, imported 6.25 million tons from Brazil in August, down from 9.04 million tons last year, according to customs data.

China has purchased up to 3 million tons of Argentine soybeans in recent weeks for delivery in the coming months. That amount is nearly equivalent to the roughly 3.75 million tons the country imported from Argentina throughout last year, and there is a risk of reduced demand for the US crop just as US producers have started harvesting.

This buying campaign will ensure China’s supply in the coming months, but the Chinese government has announced plans to reduce the amount of soybean meal used in feed products as part of a plan to strengthen food security. Thus, even a small change in soybean consumption can be cause for concern for countries that rely on Chinese demand.

CBOT ZSX22 NOV22 – 1,425 c/bu (-31 c/bu = -11.4 USD)

SOYBEAN TREND CHART – ZSX22 NOV22

CAUSES AND EFFECTS

- Argentina is literally dancing the tango with the soybean crop, fooling the competition and making consistent sales to China.

- American farmers will be caught on the wrong foot right at the soybean harvest. But their protection is the financial risk product called Hedging. They secured their price level long in advance.

- What the CBOT is indicating is nothing more than a mix of profit taking with an acknowledgment of China’s waning interest in North American commodities, at least temporarily.

- As the harvest progresses, we will see negative price corrections in the commodity

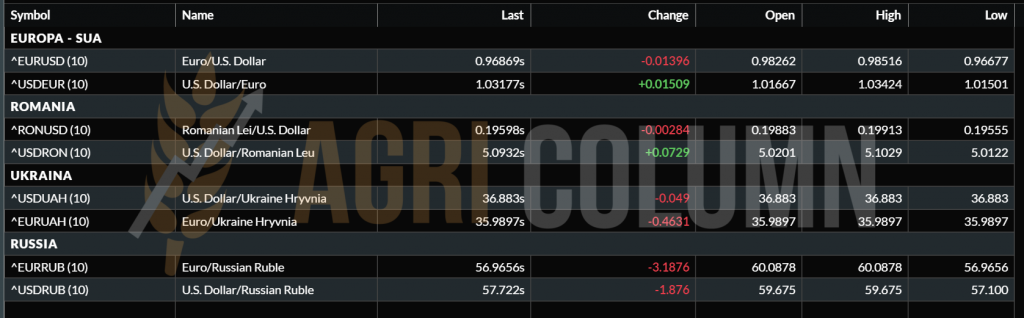

EUR:USD – 0.968:1

EUR/USD TREND CHART

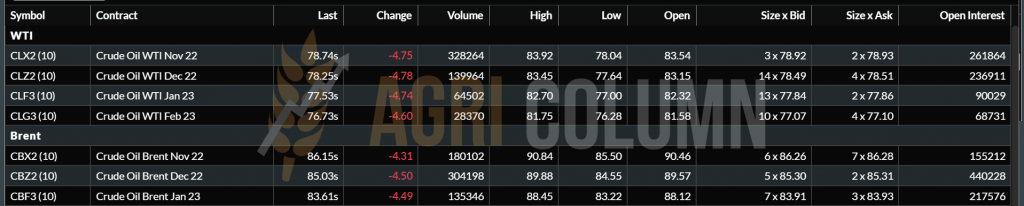

OIL. WTI = 78.74 USD/barrel | BRENT = 86.15 USD/barrel

WTI & BRENT PRICE TREND CHART

24 September – 1 October 2022

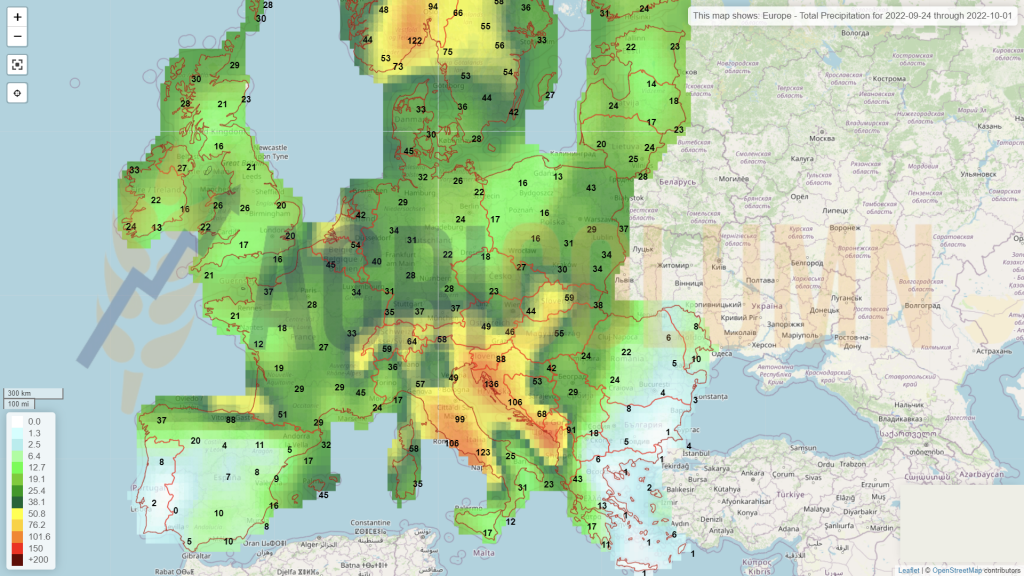

Romania

Europe

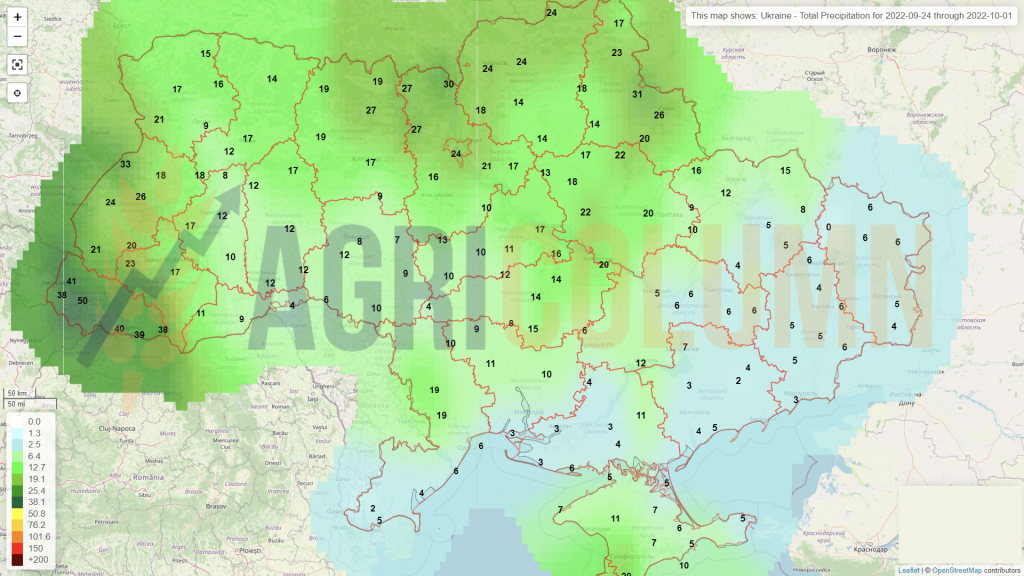

Ukraine

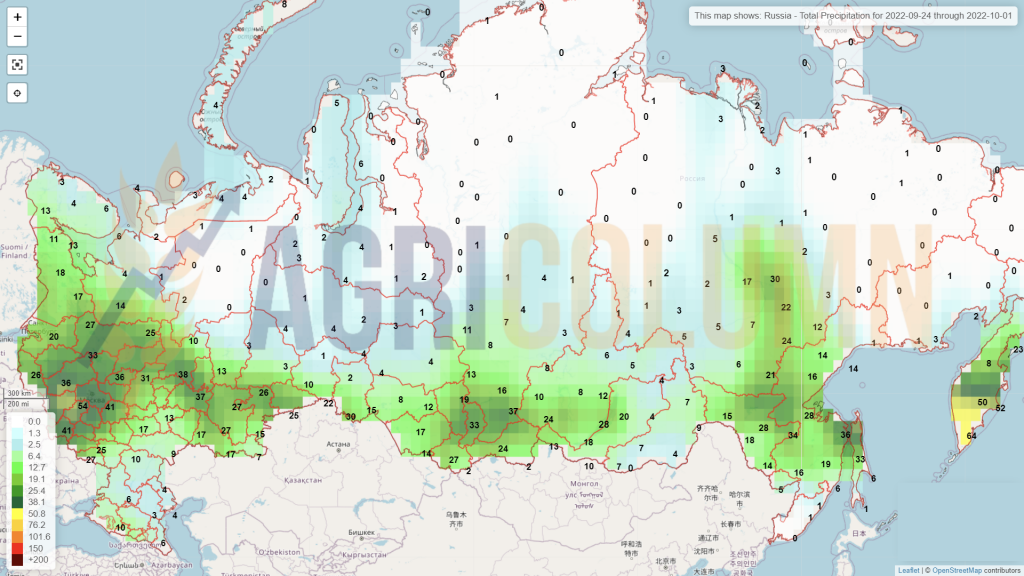

Russia

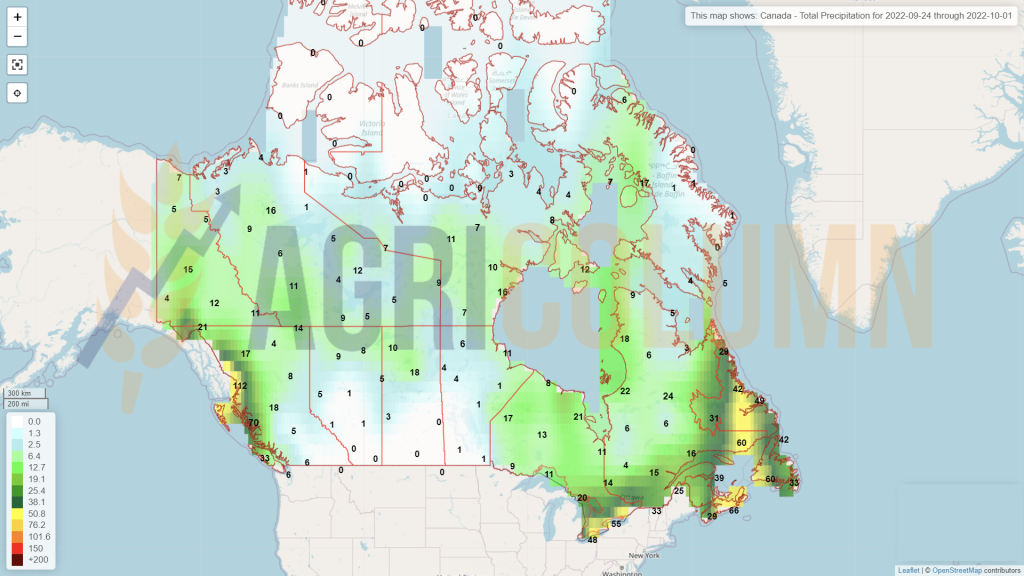

Canada

USA

Brazil

Argentina

China

Australia