This week’s market report provides information on:

THIS IS UKRAINE

LOCALLY

We start the wheat road with observations towards the port of Constanța. It will soon be overcrowded due to the diversion of traffic from Ukraine, especially container traffic, as well as other general cargo.

In the context in which the largest container operators in the world have stopped trade relations with Russia (we list here MAERSK, CMS, MSC and others), and merchant ships will no longer enter the port areas of the Black Sea basin due to the dangers (the bombing of the Russian navy, as well as the mines installed in the area), the port of Constanta will take over the weight of maritime traffic in Ukraine.

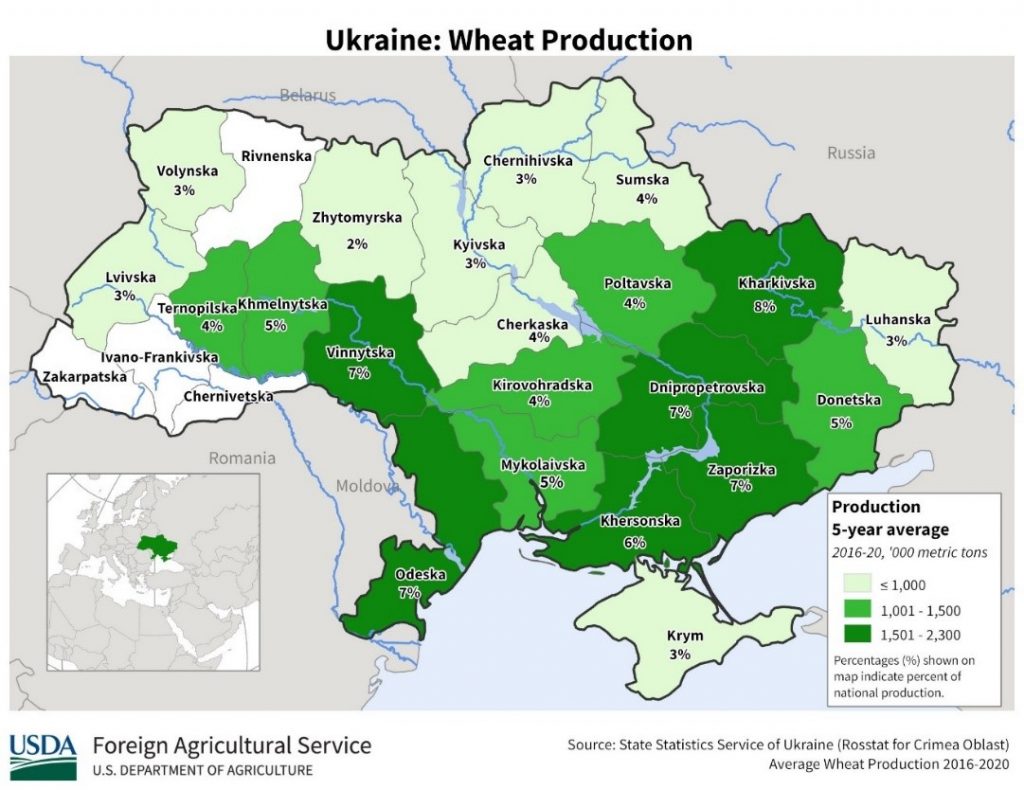

We list Odessa, Chornomorsk, Mykolaiev, Kerson, Ochakiv as main ports, as well as the Bistroe canal. The port of the Sea of Azov, Berdyansk, is already destroyed by Russian bombing and damage is being done to Mykolaiev.

The damage caused by the Russian army will generate operational delays of at least 40-60 days. Thus, we could get very close to the new crop in operation from the Ukrainian side. In the pessimistic scenario, regarding the prolongation of the conflict and its duration more than 30-50 days from now on, we will not have the wheat flow from Ukraine.

Russia has closed ports in the Sea of Azov, Novorossysk, Caucasus, Tuapse, Taman and Kavkaz. The Kerch Strait is blocked and the entire Crimean region is an exclusion zone, meaning no ships can cross it.

But there are other limitations. Constanța and Agigea operate only 2 container terminals each, the rest of the berths being destined for bulk and partially liquid goods. We estimate a finality that will coincide with a similar situation during the summer, when the port is blocked by bulk cargo and trucks, and until the ships succeed each other in operation, these endless queues should not stop. This will definitely happen. Shipowners will no longer enter Ukrainian ports due to the state of war, will no longer enter the Sea of Azov due to the blockade of the Kerch Strait by Russia, and insurance companies will no longer insure ships en route to these destinations.

There is a state of tension in the local market which makes exporters extremely nervous. They cannot afford to pay prices in line with what is happening on the stock exchanges, for the simple reason that the uncertainty regarding potential export restrictions is quite pronounced. The risk of starting a contract and then of not being able to honor it is extremely high.

Thus, what we see as quotations were reduced to 330-340 EUR/MT CPT Constanța, in total disagreement with the indications of Euronext and the status generated by the war that is taking place nearby.

The new wheat crop is not listed. Nobody wants to assume any amount, given that the price on Euronext is constantly rising, given the political factor, i.e., the war in the vicinity of our borders.

Romania is currently the only logically positioned location that can provide fluency to the Middle East, and we will briefly list Egypt, Jordan, other Arab countries, as well as destinations in SE Asia and NE Asia. In comparison, the distance Constanța – NE Asia costs 56.25 USD/MT, while the indication US Gulf – NE Asia costs 63 USD/MT.

If we take the relationship Constanța – Egypt, we have a cost of 25 USD/MT versus 85 USD/MT from US Gulf. With these examples, we highlight the logistical superiority and the geo-strategic potential of Romania, which remains the only predictable and sustainable player in the Black Sea basin.

Romania has an aggregate wheat export level of almost 5 million tons, from the agricultural year 2021-2022. The production of 2021 being 11.2 million tons, with an export level of 5 million tons and a domestic consumption of 3.3 million tons, we estimate an export difference of maximum 2.8 million tons, from this moment.

But Romania’s wheat crop forecast for 2022 is not one of the most optimistic. The autumn drought that delayed the sowing, as well as the lack of precipitation, will generate a deficit of at least 1.2 million tons, reporting everything to a multiannual average of 9.6 million tons.

REGIONALLY

At the regional level, we note the first protectionist actions in Hungary, which completely restrict the export of cereals, and the details will be published in an official document soon. The Republic of Moldova, in turn, has banned the export of wheat and corn, and Serbia has imposed an export tax on wheat.

Bulgaria also restricts exports, but does so in a different way, as follows:

- About 1.5 million tons of wheat will be allocated as an export quota, but it is unclear whether intra-Community trade is also included here.

- About 1.5 million tons of wheat will be purchased by the Bulgarian state as a set of security, if the conflict progresses and intensifies, at indicative prices of 320-330 EUR/MT.

- Corn will be completely restricted to exports.

- Oilseeds will not be impacted, knowing that Bulgaria is a processor of oilseeds due to its infrastructure and runs raw materials mainly from Romania.

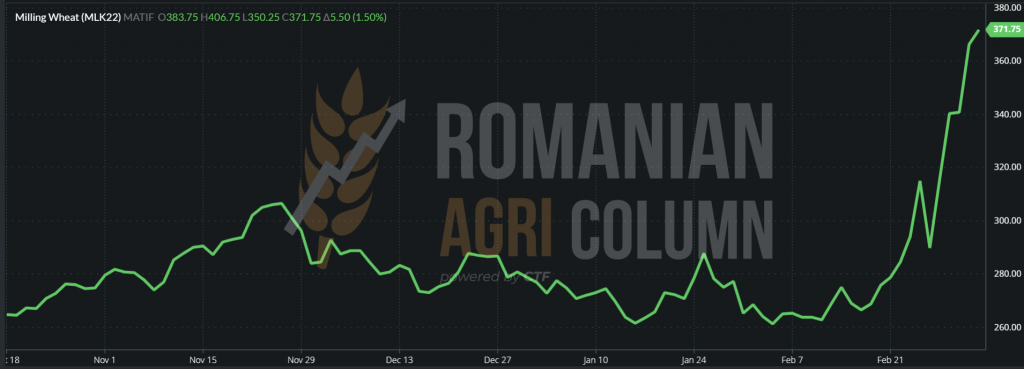

The European stock market is indeed galloping in terms of wheat indications. Quotations exceed levels hard to imagine before the conflict. But what we estimate before the conflict happened with an accuracy of 100%, namely the price of wheat reached a level of 330-340 EUR/MT in the CPT Constanța parity.

EURONEXT MLK22 MAY22 – 371.75 EUR at the close of March 4, 2022

EURONEXT TREND GRAPHIC – MLK22 MAY22 WHEAT. The picture is worth a thousand words.

The first signs of the devastation caused by the conflict will be soon seen. And we’re talking briefly about both the old and the new wheat crop:

THE OLD CROP:

Ukraine and Russia still had to export a cumulative level of 16-17.5 million tons – Russia about 8-9.5 million tons, and the difference on behalf of Ukraine, which was to reach the level of 24.7 million tons export quota, but was stopped at 17.9 million tons.

In the context of the global balance of supply and demand, the existence of these blocked volumes creates a very big problem. The balance had been found, the negative difference in the last WASDE report of about 9 million tons seemed surmountable with the help of the expected increase coming from Australia, which will be adjusted positively by 3-4 million tons, from a level of 34 million at a maximum of 38 million tons. Argentina also contributed to the balance with the 1-1.2 million tons generated in addition as crop level.

At the moment, however, the global balance of Production-Consumption-Stocks is very unbalanced. Such a non-exportable stock of goods in the basin impacts the market in the medium term by unbalancing supply to the detriment of destinations.

Every day without port activity on the Black Sea, about 100,000 tons of wheat and 100,000 tons of corn are NOT loaded. EU stocks are limited, so there is every precondition for wheat prices to rise sharply. Let’s not forget that record levels were reached in the context of 2008, when wheat reached 520 USD/MT.

In the current context, there are very confusing situations from a legal point of view. We refer to the declaration of force majeure by the seller. Given that the seller has sold in CIF Egypt parity, for example, and the transport is provided by the Egyptian National Naval Company (NNC) and the latter cannot send the ships for loading, we are at a standstill. The seller cannot declare force majeure, because he cannot charge not because of himself, but because of the one who sends the ship to the cargo, Charter-Party. The buyer cannot declare force majeure, because he buys in CIF parity. In other words, there is a legal deadlock that only lawyers can resolve in this context.

But the problems continue. Ukraine’s port infrastructure has been damaged to some extent. It takes weeks/months/years to recover, depending on the level of damage. Problems with financing/trade sanctions in Russia, even if they are reduced now, will take weeks to resolve (months/years to regain confidence as a source). Insurance companies no longer cover travel in the area due to the conflict.

If wheat from the Black Sea is not available by July, either because of the ongoing conflict or because of sanctions on Russian wheat exports, prices could rise significantly.

If sanctions were imposed on wheat exports, we could still see governments in some large importing countries, such as Iran or China, ignoring Western sanctions on Russian exports and still procuring grain – as well as countries with food insecurity, especially in the Middle East, East and North Africa.

The demand will have to be rationalized in the short term and will need to be moved geographically to other sources: EU, USA, Argentina, Australia.

But are these origins well enough prepared to take the shock of the missing stock in the Basin? From a logistical point of view, it is a major handicap, which we found in the last attempt to acquire Egypt through GASC, where the highest value was given by American wheat, with a level of 517 USD/MT CIF Egypt. The French wheat present in the auction was quoted at 430-439 USD/MT, also delivered in CIF Egypt parity.

Destinations switched from the “hand to mouth” status to “hold your breath” behaviour. Don’t move, don’t breathe and just wait for a stabilization, maybe a cessation of the conflict, a decent normalization in order to be able to resume transactions at more realistic prices, because what we see today does not really make sense. Today’s prices are based on panic, fear and disorder.

Because we also mentioned tenders, we let you know the latest transactions, as follows:

- GASC tender of March 3, 2022 was canceled. The CIF equivalent is 517-520 USD/MT. Another issue is the declaration of force majeure. If the GASC is charter (NNC) and does not present the vessel when loading, the seller is not obliged to declare force majeure. GASC has to do it, but the process is more difficult.

- ODC Tunisia purchased 100,000 tons of durum wheat from Casillo at a price of USD 634.89/MT C&F. The tender was initially set for the purchase of 75,000 tons.

- TMO purchased, subject to confirmation, 370,000 tons of wheat in its auction on March 4, with delivery on March 10 and April 8, 2022. Prices range from 410 USD/MT to 517 USD/MT, the difference being the customs and unloading port. However, TMO announced the subsequent rejection of about 75,000 tons of the auction due to a very high price.

As a conclusion of the above, the old crop wheat will be expensive no matter what. There is no viable counterweight to goods in the Black Sea basin. Other possible zonal protectionist policies will follow, and there is still a long way to go before the new crop.

The NEW CROP, which we will discuss below, already has a major handicap:

Ukrainian farmers will not be able to work in the field. The chaos caused by the war will cause delays in the spring sowing of sunflower and corn seeds.

Ukrainian farmers will experience operational adjustments in seed volume, crop protection products and fertilizers.

Russian farmers will be acutely affected by the lack of seed and crop protection companies. In other words, they will lack technology, and this will be reflected in yields.

Russian farmers will feel the shock of the exit from the global trade circuit, in terms of prices, coupled with the sharp devaluation of the ruble against the US dollar. Their goods will be disproportionately sanctioned in terms of prices compared to set-up costs. For example, 1 USD = 107 RUB.

We draw preliminary conclusions and we can say that we will have a production deficit in both countries. The current situation makes spring work difficult and production yields could fall due to the lack of application of technology and the siege and the fact that Ukrainian farmers are defending their country. In Russia, agricultural activity will be affected too by sanctions and isolation, which will cause technology companies to disappear from the Russian market.

To make matters worse and more complicated, drought in North Africa and the Middle East will increase demand for wheat. Specialists’ estimates show a 38% increase in demand. Iraq is already setting the tone, announcing a demand for 2 million tons of wheat as a reserve at this time. They are asking for funds to secure this state reserve, which has not been taken into account so far.

GLOBALLY

American wheat indicates weakness in the Central Plains. Although it may seem premature to discuss this, we raise once again the question mark over the American wheat crop. We set aside any USDA statistics on area, productivity per hectare, and production. We are trying to outline the effects of the December weather, we are trying to combine the information about the lack of water supply in the soil and about the volume potential, which will certainly have a decrease in all this context of things that have happened and been recorded.

But we get news from China that worries us. Minister of Agriculture, Tnk Renjian, says the Chinese wheat crop is the weakest in history. The marketing year 2021-2022 brought China almost 137 million tons of wheat. Judging by the seriousness of the statement, we try to understand what the “weakest” harvest in history means. And we reduce last year’s figure by 20% to a level of 109.6 million tons, a decrease of 27 million tons. Who replaces it? And how? On land, the chances are extremely low. Only 27 million tons can be sent by shipping. This is in addition to the annual import requirement of 10-12 million tons, as a surplus over own production.

Moreover, Chinese Premier Li Keqiang said: “We need to work together to secure the food basket and make sure that the population is fed. At the same time, China will stop any attempt to use the arable land for anything other than agriculture and, in particular, intensive grain cultivation.

So we have in front of us a real Gargantua, an insatiable organism. Outside of its own reserve, China must meet its economic model of governance, and we will see it in full pursuit of food, searching and buying everywhere.

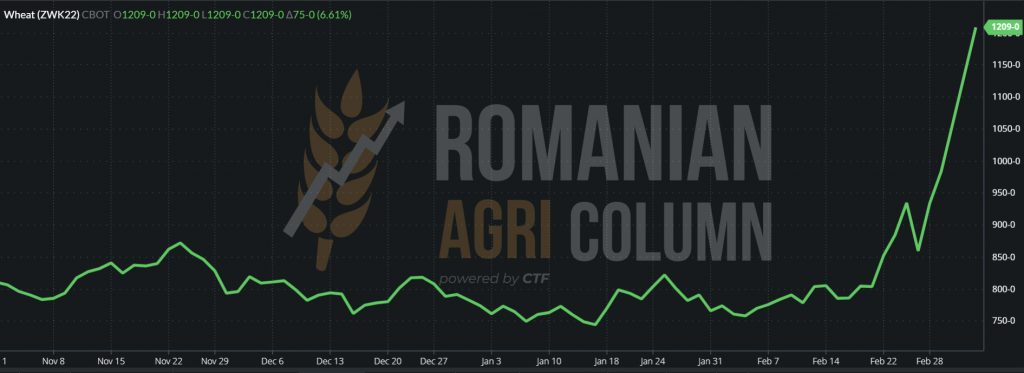

CBOT identically reacts to EURONEXT. Mutual funds are in position and playing money in extremely short terms. We see how net long positions accumulate and how profit scenarios generated by the Black Sea war are constructed as a puzzle based on algorithmic bases.

CBOT ZWK22 MAY22 – 1,209 c/bu (+75 c/bu) at the closing date of March 4-5, 2022

CBOT WHEAT GRAPH – ZWK22 MAY22

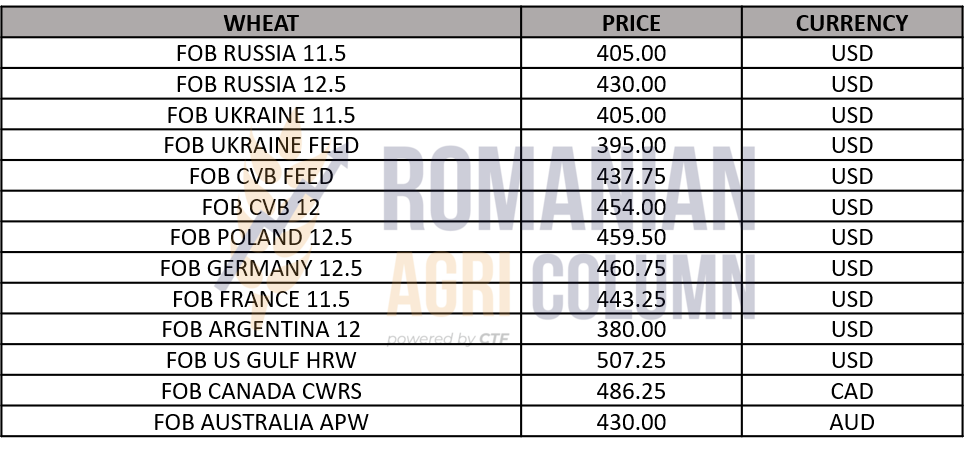

PRICE INDICATIONS IN VARIOUS ORIGINS

ANALYSIS

- The long scenario or the short scenario are the two options to consider. Each of them generates a transition to a new crop. But the short one can generate much more stability.

- Of the two scenarios, whichever is chosen, the impact will come from the new crop.

- The price of old crop wheat has been amplified by political factors, war and protectionism.

- No improvement in current status is expected within 45-60 days, which puts the new crop under pressure today: war, protectionism, weather (see China, see Middle East, North Africa and potentially US) are the three factors that fully govern the moment.

THIS IS UKRAINE

The local market reached the level of 262 EUR/MT for the goods delivered in the CPT Constanța parity. The new crop is no longer listed at this time, as volatility is extremely high and the default can occur instantly. The problems we see are related to the sales made to Jordan and Saudi Arabia, because the goods will certainly be hard to find, and the exporters will suffer losses, even if they bought CALL insurance.

THIS IS UKRAINE

LOCALLY

The indications of maize at CPT Constanța level are 310-320 EUR/MT. In some isolated cases we also noticed higher quotations, at the level of 335 EUR/MT. It makes sense for this to happen. The weight of origin and delivery from Ukraine is moving to Constanța.

Ships in the harbor of the port of Odessa for loading had to retreat to Constanța to make up for the unloaded differences. The financial cost of waiting has tripled all this time, because any day costs money.

In the short and medium term, corn will have a very high support. The war will generate additional demand and Romania will take over part of the demand for destinations in Asia as well as in the EU. In the context in which Bulgaria will ban the export of corn, we can see the origin pressure to which Romania is subjected. And it would not be out of the question to see the price of maize higher than that of wheat, even for a short period of a few days, just out of the need to cover the contracted export.

As for the new maize crop, absolutely no quotation is generated. The risk is extremely high and no one wants to expose themselves unnecessarily, especially since the sowing season will start in about 2-2.5 weeks.

REGIONALLY

Ukraine has generated a fantastic corn crop of about 42 million tons this year, of which exports were forecast at 33 million tons. By the start of the war, Ukraine had managed to export about 19 million tons. At the moment, 14 million tons remain to be exported. The supply will be made from Romania and South America, due to the better logistics compared to the USA.

The Iberian Peninsula will be supplied by the US, but with GMO corn. The situation is volatile. Every day brings new changes, the pressure is extreme and the destinations are looking for cover. China has consumed the first episodes of stock piling and now goes out to buy again, anything, at any price. But the peace in Asia raises big questions.

Why is China stocking up so much? Are there any plans for an assault on Taiwan? But there is an agreement called QUAD, made up of the US, Japan, Australia and India, which will retaliate in the event of a Chinese armed attack on Taiwan.

EURONEXT is extremely turbulent. The quotations of corn have a great amplitude and increase every day, given by the wheat and the lack of the 14 million tons in the Black Sea basin. Bulgaria’s statements on the ban on corn exports will also contribute to Monday’s increases.

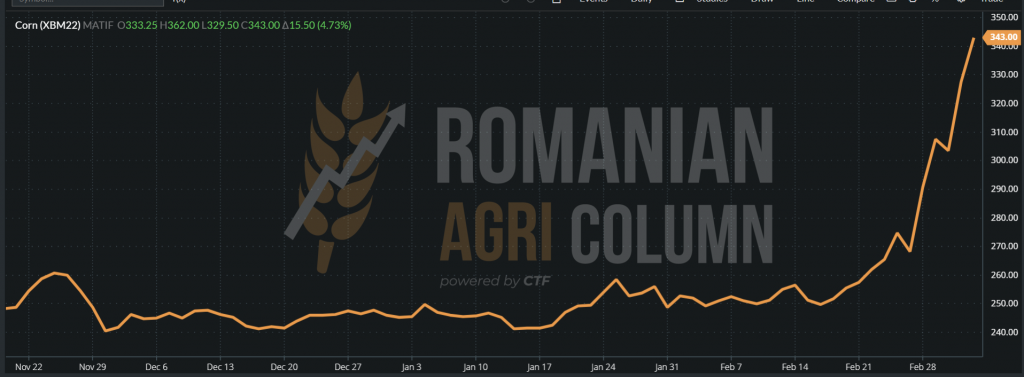

EURONEXT XBM22 JUN22 – 343 EUR (+15.5 EUR)

EURONEXT CORN GRAPHIC – XBM22 JUN22

With regard to the new corn crop, we anticipate a decrease in the potential in Ukraine due to the state of war and the lack of products (supply disruptions). Russia is also exposed. Due to the sanctions, Russian farmers will not have 100% sowing technology.

GLOBALLY

Destinations have an alert supply rate during this period. The life cycle of the corn price is in the progress phase, and the problems generated by the weather in South America have weighed heavily in the decision to move the origin to the Black Sea basin. However, Argentina has a similar cost to the Black Sea basin in terms of logistics, but the harvest will take place later. Asian destinations such as China, Vietnam, South Korea, the Philippines and, last but not least, Indonesia have a logistical appetite for corn in the basin. The European Union buys maize from Romania through Spain due to the fact that it is not genetically modified.

Argentina and Brazil will suffer further production declines. Thus, compared to WASDE in February 2022, when Argentina was quoted at 54 million tons, the preliminary indications of the report go to 52 million tons, while Brazil decreases by 1 million tons, to the level of 113 million tons. Starting from the initial Brazilian forecast of 121 million tons and cumulating the current Argentine depreciation, we have a minus of 10 million tons. This minus would be partially digestible, but that is until the moment when we review the non-exported goods from Ukraine, of 14 million tons. With a minus of 24 million tons, the Production-Consumption-Stocks balance will go into deficit on March 9, 2022, according to the upcoming WASDE report. However, by analyzing things correctly, traders are already working with these figures, so the report will only confirm and no longer influence. Prices are already extremely high and volatility is at its peak.

But one problem is darkening the Brazilian horizon, namely the decoupling of Russia from fertilizer replenishment. It is a spectrum that makes farmers shudder, because the percentage indications of the lack of supply are of the order of 20% of what is needed. But this will mean the disappearance of one billion dollars from the market, an estimated cost of the 20% missing from the fertilization plan. In any case, Brazil aims to reduce fertilizer use by 25% by 2030.

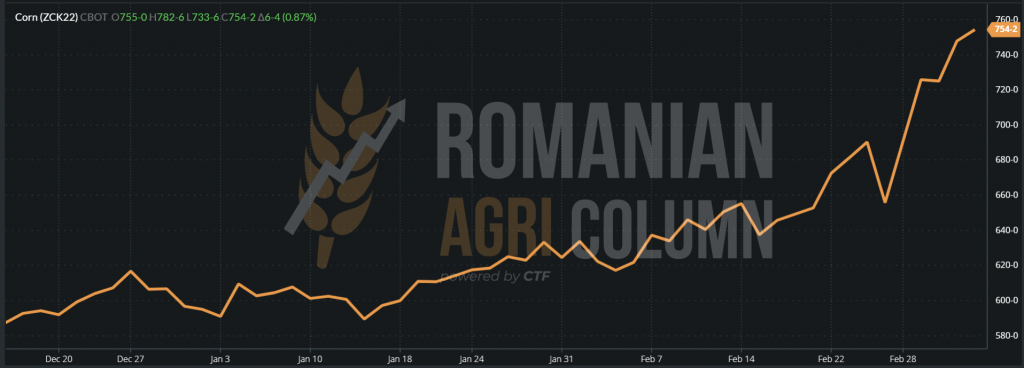

CBOT ZCK22 MAY22 – 754 c/bu

CBOT CORN GRAPHIC – ZCK22 MAY22

CORN INDICATIONS IN MAIN ORIGINS

ANALYSIS

- Extremely high pressure on maize prices in the only remaining Origin, namely Romania.

- Bulgaria will ban corn exports in the coming days.

- South America will lose another 3 million tons of corn in the forecast, 2 million from Argentina and 1 million from Brazil.

- Volatility will continue to generate the inflationary spiral of prices.

- 14 million tons blocked in the basin is a lever that can, at some point, recover the market in the sense of lowering the price, but only after the conflict ends and the operational pace can resume.

THIS IS UKRAINE

LOCALLY

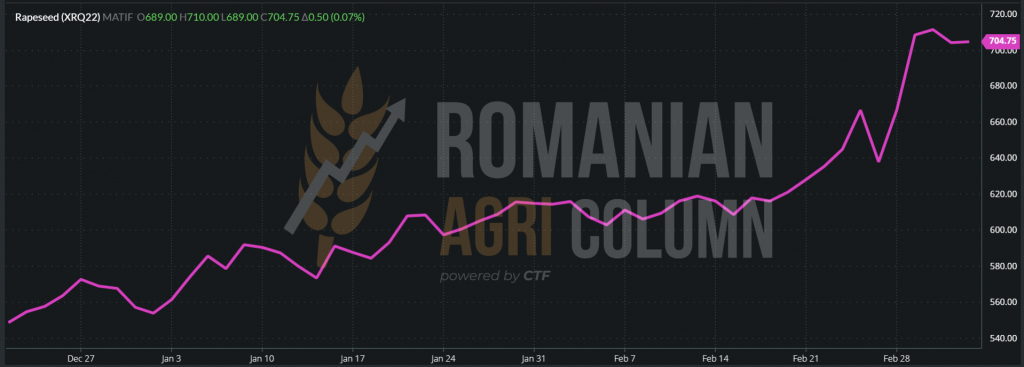

The indications in Romania are conducted after AUG22 minus 10-15 EUR/MT for the goods delivered to the processing units. But the vegetative conditions of rapeseed at this time mean that farmers do not yet have the consistency necessary for forward sales. The political factor also contributes to this state of affairs, which makes the indications of rapeseed on Euronext exceed the level of 700 EUR in the AUG22 indication.

The natural correlation with the price of oil automatically leads to much higher price levels. Our estimates of 660-670 EUR/MT for the new crop have been exceeded for political reasons, i.e., the war waged by the Russian Federation against Ukraine.

So we have 3 unknowns in the equation of the new rapeseed crop, namely:

- How long will the conflict last and what is the price increase?

- How much will the price of oil go up and how much will the price of rapeseed go up?

- How will the weather influence the rapeseed crop in Romania for the balance of supply and demand?

We will certainly find answers in the next period.

REGIONALLY

At the regional level, we see some problems with water scarcity in Europe, specifically in France and Spain. We remind you of the potential problems in Poland and the Baltic States caused by negative temperatures. However, the EU indicates the same forecast level of 17 million tons, including Romania.

In the Black Sea basin, the calculations are changing dramatically. The potential of 6 million tons in the Ukrainian and Russian accounts suffers dramatic distortions, first of all, because the goods will not be able to be taken out of the two countries in any form, neither as raw material, nor processed. The ports will be closed, and the current exclusion zone has shown that it is not working, as the sinking of the Estonian cargo due to a collision with a mine is just the latest example. Ukrainian port facilities are suffering and will suffer.

Secondly, the spring works will not be able to be carried out accordingly. In Russia, the reason is the lack of products, against the background of sanctions imposed and the departure of the local market by global companies, Bayer, Syngenta, etc.

And thirdly, even if we take into account the optimistic scenario of stopping the conflict, it will still take a while for the port operations to resume (minimum 30-55 days).

Thus, with a minus of 25% of European production, we will see a steep rise in the price of rapeseed in the spring, until harvest.

EURONEXT XRQ22 AUG22 – 704.75 EUR at the close of March 4, 2022

EURONEXT GRAPHIC – XRQ22 AUG22 – March 4, 2022

GLOBALLY

Another risk factor is Canada and subsequently Australia. Canada will start sowing in April and estimates for a normal year are 22 million tons. Any problem generated by the weather will put even more weight on global demand and supply. Balancing with the European crop will be a factor in generating volatility, as a whole.

Australia will also start sowing in April. The average volume generated there is close to 5 million tons. Here, too, any weather issue will increase the volatility of S&D (supply & demand).

ANALYSIS

- Extreme uncertainty governs the quotations of rapeseed in the 2022-2023 season.

- The political factor – the war in the Black Sea basin.

- The weather factor – European uncertainties, minor, but there. Uncertainties will arise in North America (Canada) and also in Australia.

- In addition to all of the above, there is increasing processing in Canada, which can narrow the flow of raw materials.

THIS IS UKRAINE

LOCALLY

Things are getting worse when it comes to supplying sunflower seeds to processors. The existing bottleneck in Ukraine generates an acute shortage of crude oil replacement. All indications lead to a lack of raw materials for Romanian processors, in active competition with exporters and EU countries. The demand is particularly high and the ferocity with which prices increase day by day indicates a lack of raw materials.

If last week was trading at the level of 740-760 USD/MT, at this moment, after an almost vertical ramp-up, we see the level at over 1,000 USD/MT. This indication is present in the CPT Constanța parity, in DAP processors and even in FCA Farms for large batches. Although we also see buyers indicating 840 USD/MT, they do nothing but express their disinterest in the goods, in the hope of a future possibility to calm the situation in the Black Sea basin. However, as the constituent elements are presented today, we cannot see a calming, at least apparent, of the war and its effects in the medium and long term. Some exporters buy at prices that are hard to believe to meet EU demand. We are witnessing levels of 1,128 USD/MT, DAP Constanța for batches of 2,000-3,000 tons.

Romanian processors are in obvious difficulty. In a time without war, they could have supplied with crude sunflower oil from Ukraine. This oil would have been brought to Romania and, even if they did not have a processing margin, it would have been refined and thus would have supported the domestic demand in stores. At the moment, this is no longer possible and we must admit that it is only a matter of time before we see two particularly adverse effects:

- Shelf prices in the range of at least 20-25% higher compared to today’s level.

- A decrease in the level of merchandise (sunflower vegetable oil) on the local market.

- Closure of processing facilities due to lack of raw material and lack of imported crude oil as a substitute.

REGIONALLY

The situation is completely hopeless at this time. Odessa is surrounded by Russian warships from the sea, and a naval assault, which includes a bombardment of Ukrainian port facilities, is absolutely inevitable at the time of writing. This assault on the sea will be followed by a landing of Russian troops on Odessa, which leaves no chance for goods stored in port facilities.

And with these mentions, we remind you of the stocks of crude oil blocked in the Odessa – Chornomorsk port region, over 360,000 tons. Subsequently, the companies that own the processing facility in the Mykolaiev area closed the operation. Here we call world giants like Bunge, ADM, Cargill. They stopped the operation because of the specter of the Russian attack, as well as because even if they produced, the crude oil has nowhere to be delivered and stored. The goods are blocked in the above-mentioned port region.

In the region of northern Europe generically called 6 PORTS, indications rose sharply by 440 USD/MT, given that the pre-existing price level for crude oil was 2,000 USD/MT. Following the increase, it formally amounted to 2,400, even 2480 USD/MT.

In the Black Sea basin, there are no more price indications, referring strictly to Ukraine and potentially Russia, which make no sense at this time.

At the same time, in a regional overview, we anticipate other effects that will reverberate intensely in the coming months and that will create a shock wave for the 2022-2023 season. Thus, Ukrainian farmers will no longer have the time and space for spring sowing for sunflower seeds. Even in the event of normal sowing, they will face an acute shortage of fertilizers and crop protection products. The estimates we see are of reduced volume by at least 20% compared to the crop of 2021, around 13.5 million tons, compared to 17.5 million tons in the 2021 season.

Russia will face the same supply problems. Global giants such as Bayer, Corteva and other industry-renowned names will no longer deliver seeds and crop protection products amid sanctions and shut down business relations with the Russian Federation. Here, too, we estimate a low level of seed production of about 20%. The estimated future crop in Russia could generate 12-12.5 million tons.

Europe needs raw materials and is in the same condition as Romania, the lack of raw materials due to the blockade due to the war, as well as a lack of supply of crude oil. Both lead to increases in the above quotations and, implicitly, will lead to an exit price from the processing facilities at a minimum level of 2 EUR/liter, if not even higher.

In a statement, Fediol clearly stated that the European Union was relying on 200,000 tons of CSFO – crude sunflower oil. The level of imports from Ukraine is about 35-45% of what is needed for a year. But at the moment, the EU’s crude oil is at such a low level that it can only be consumed for 4-6 weeks.

GLOBALLY

India is reorienting itself to soybean oil and to palm oil. Its goods contracted in the Black Sea basin are still blocked. However, palm oil prices also reached very high levels, supported by the lack of stocks in Malaysia and the reduction in exports from Indonesia, the two countries being the largest producers of oil.

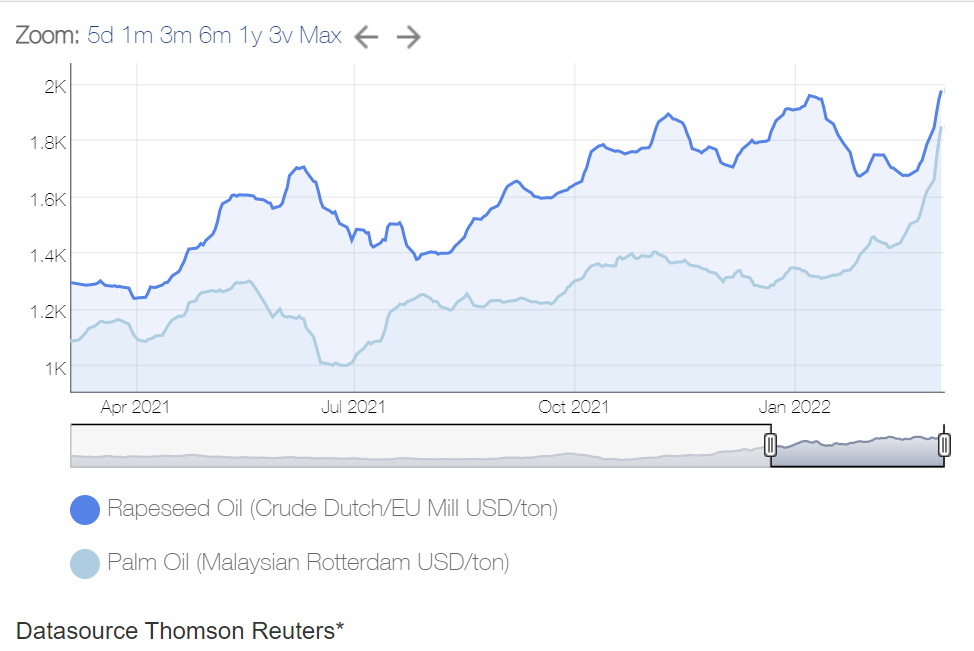

We insert the indicative levels of palm oil, which reached 1,850 USD/MT in Rotterdam. The correlation of the price level between sunflower and palm oil generates this inflationary spiral, everything pivoting on the blockage in the Black Sea basin.

And in order not to be repetitive, in the same graph you will find the price level of rapeseed oil, which in turn reached 1,985 USD/MT. Photo source: Reuters.

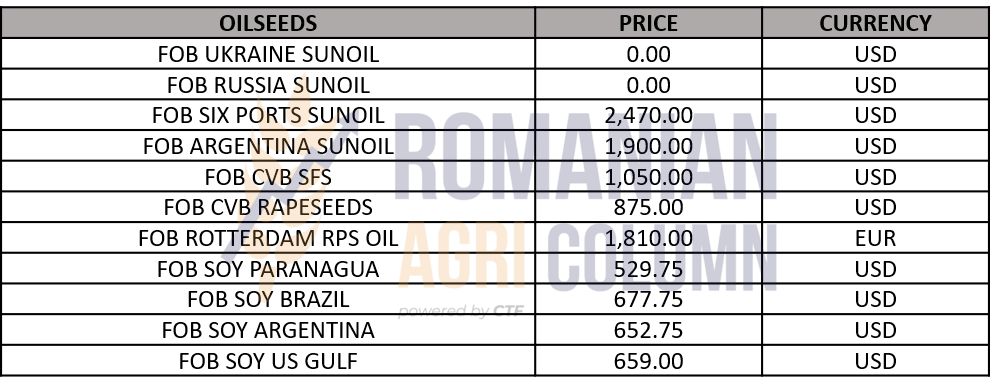

CSFO AND OILSEED PRICES IN VARIOUS ORIGINS

ANALYSIS

- The acute shortage of raw materials generates extremely high prices for sunflower seeds.

- The acute shortage of Ukrainian crude oil on the market subsequently generates supply shortages in the producer-consumer chain.

- Forecasts for future crops are extremely pessimistic due to political factors (war and sanctions).

- Everything rolls in the final price of sunflower vegetable oil.

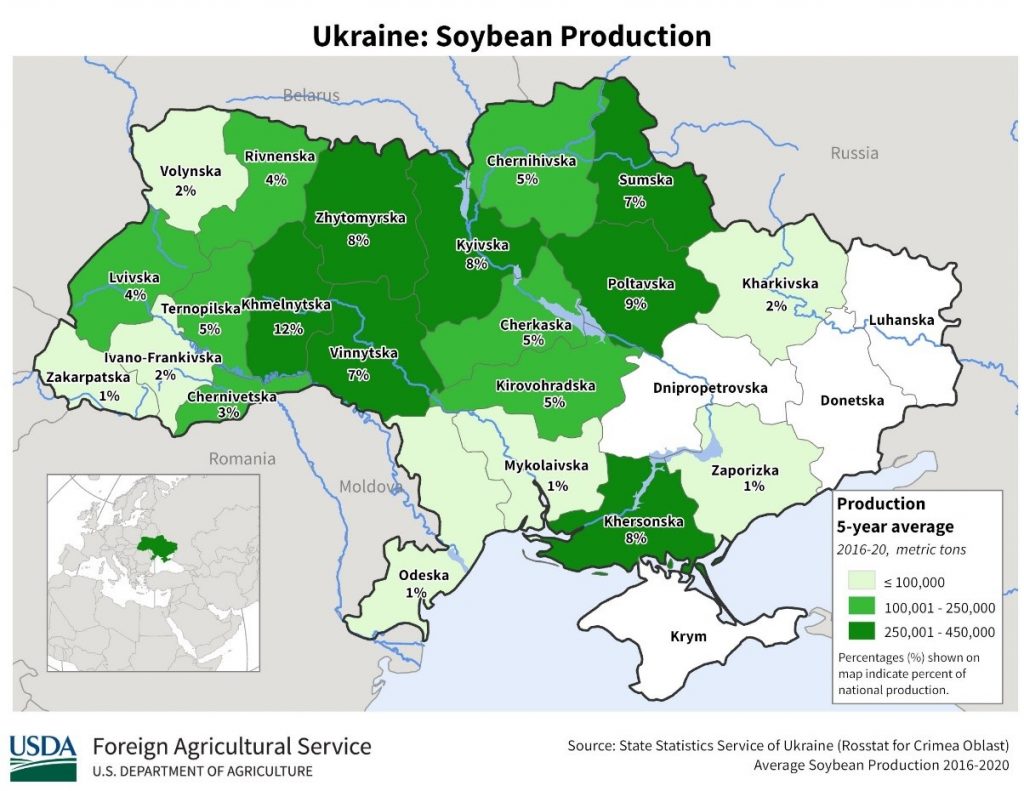

THIS IS UKRAINE

LOCALLY

Processor specifications remain at 660 USD/MT for non-GMO soybeans delivered to Romanian processing units. Cross-border indications in Hungary amount to 625-628 EUR/MT DAP processing units for sustainable goods.

REGIONALLY + GLOBALLY

Forecast changes are already in place in South America and we are seeing a decline in the forecast in Argentina. According to BAGE, soybean production is now at 42 million tons, compared to the initial estimate of 46 million tons.

The Brazilian soybean crop is still degraded. StoneX reports 121.7 million tons, and the latest USDA report shows 134 million tons. It is an impressive drop, which reduces the global potential by 27 million tons, including Brazil, Argentina and Paraguay. This is exactly the level of balance that China is giving up, i.e., 30 million tons.

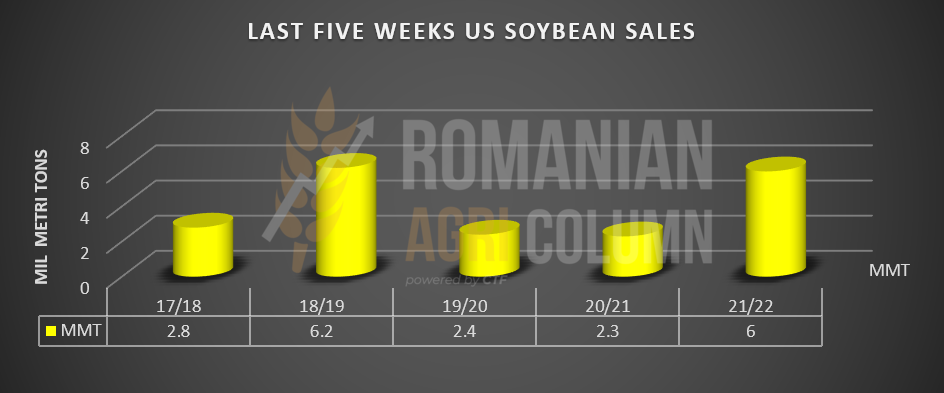

The US indicates impressive soybean sales, exceeding 6 million tons in the last 5 weeks, compared to previous marketing years.

In a few days, more precisely on March 9, 2022, we will have the WASDE report, generated by the USDA, and we will consolidate what has been said above in the current context.

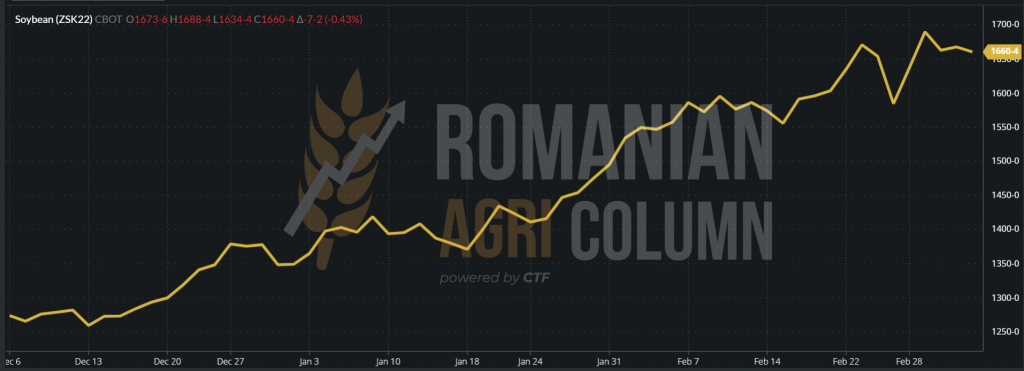

CBOT SOY ZSK22 MAY22 at the closing date of March 4-5, 2022

CBOT SOYBEAN GRAPH – ZSK22 MAY22

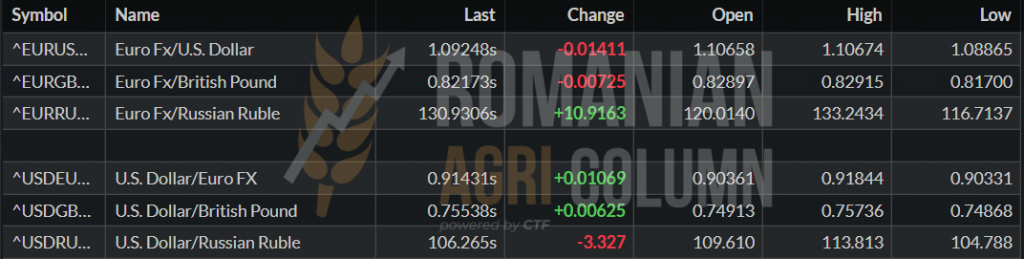

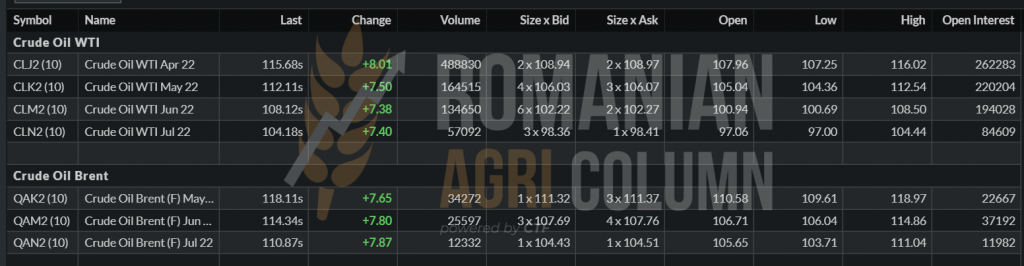

EUR/USD 1:1.09. USD is strengthening. USD/RUB 1:106.26. MOEX (Moscow Stock Exchange) opens on Wednesday. Then you will see the fall.

WTI 115.68 USD | BRENT $ 118.11

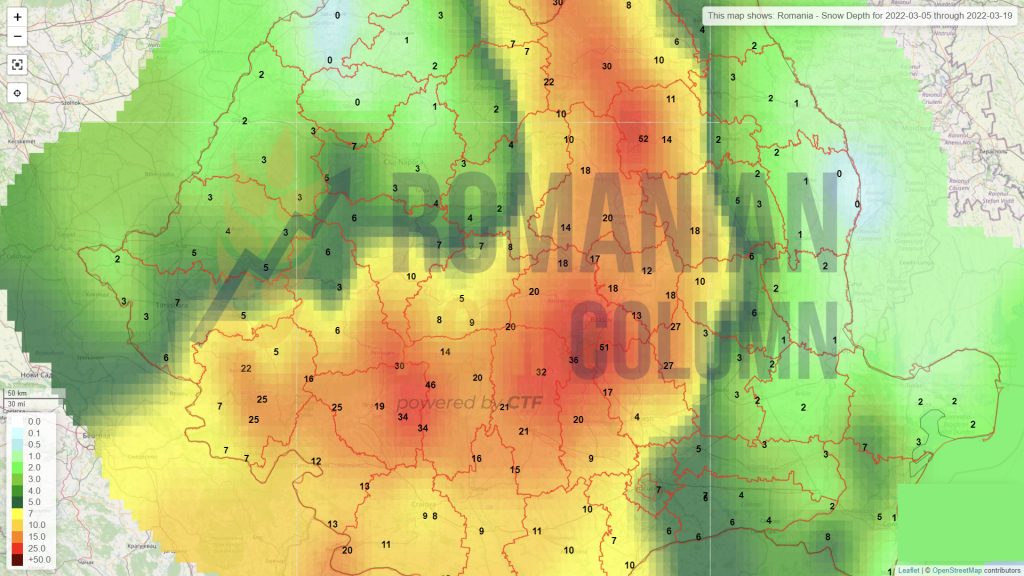

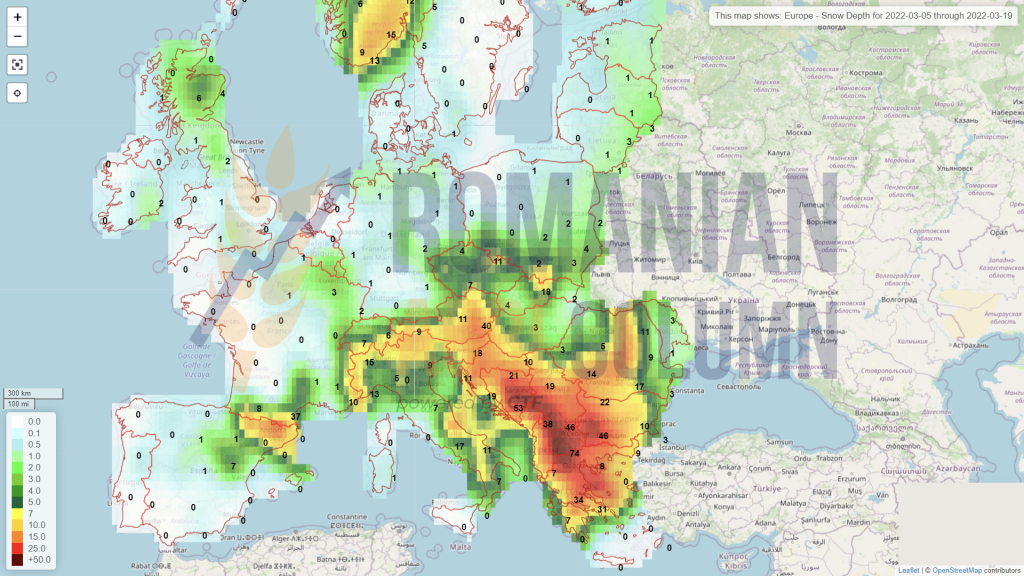

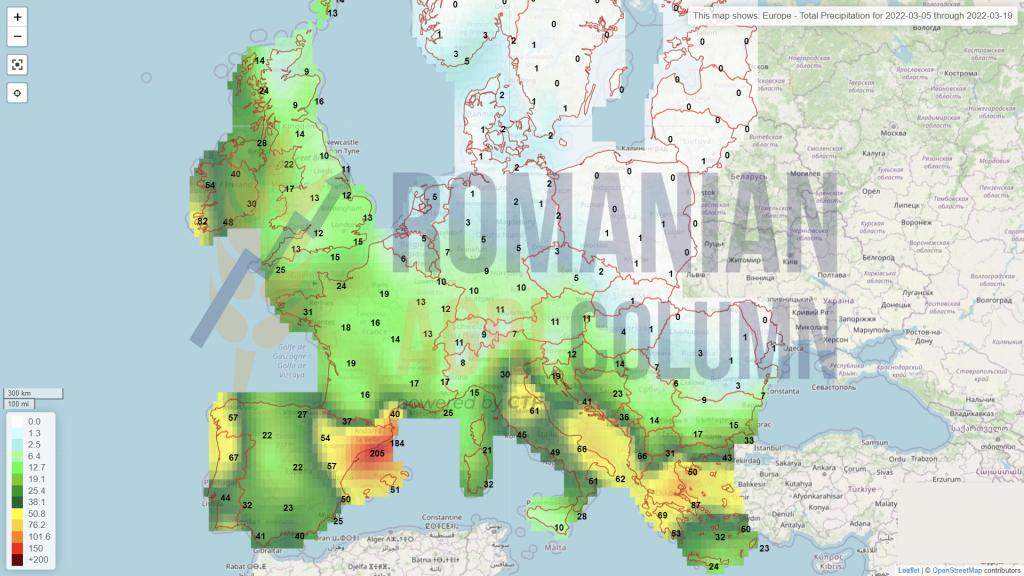

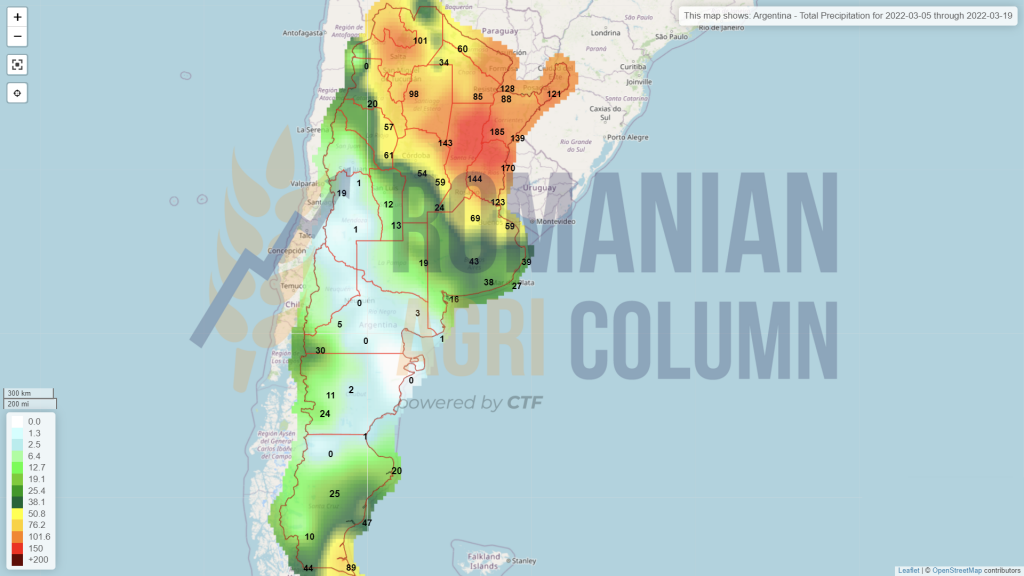

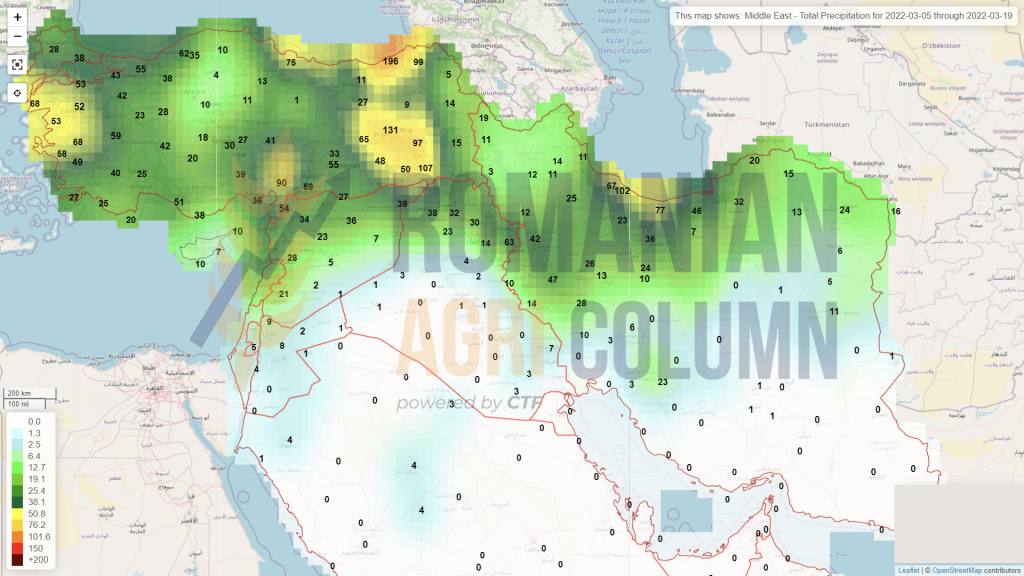

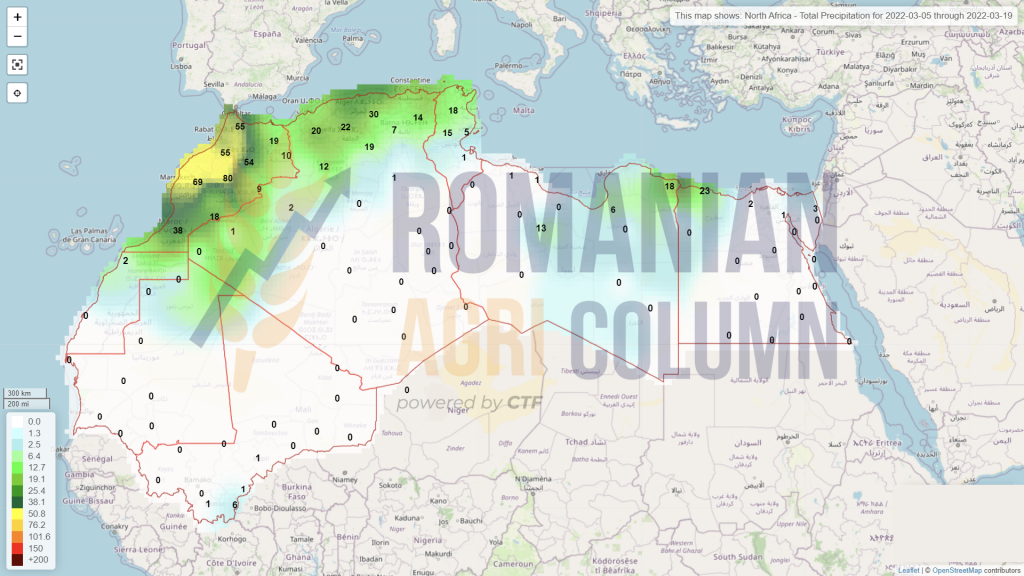

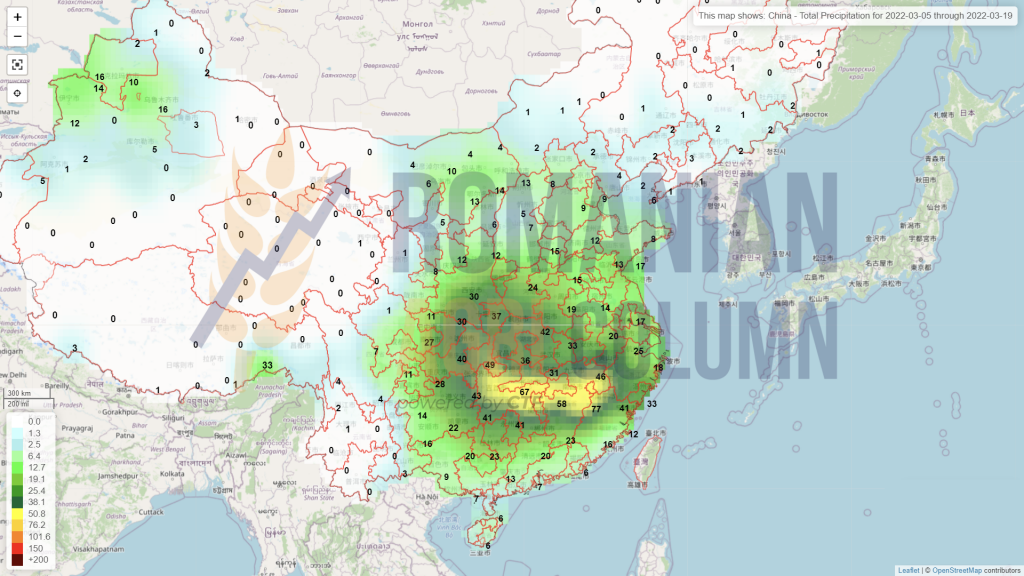

March 5-19, 2022

Romania (snow)

Europe (snow)

Europe (rain)

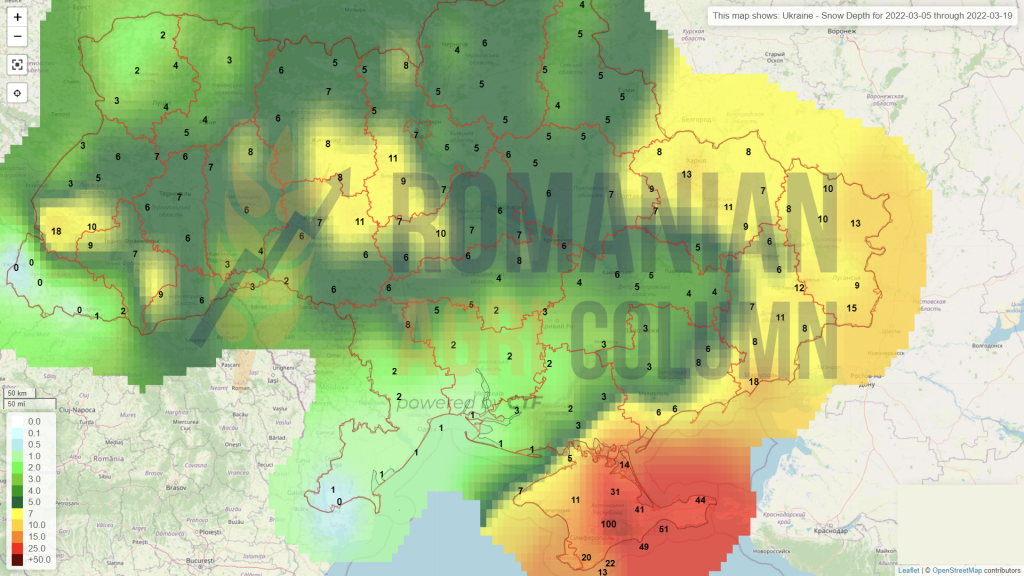

Ukraine (snow)

Russia

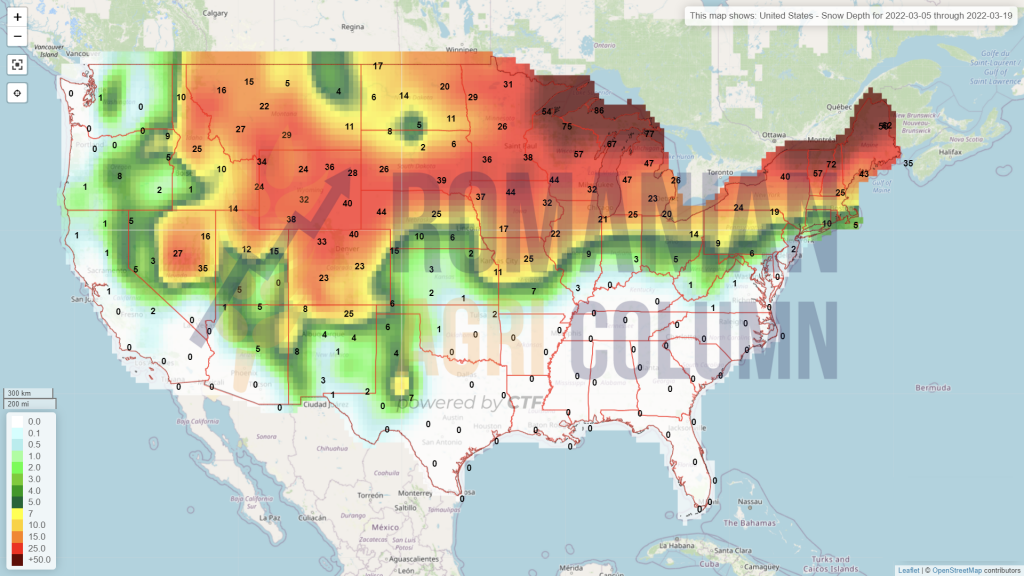

USA (snow)

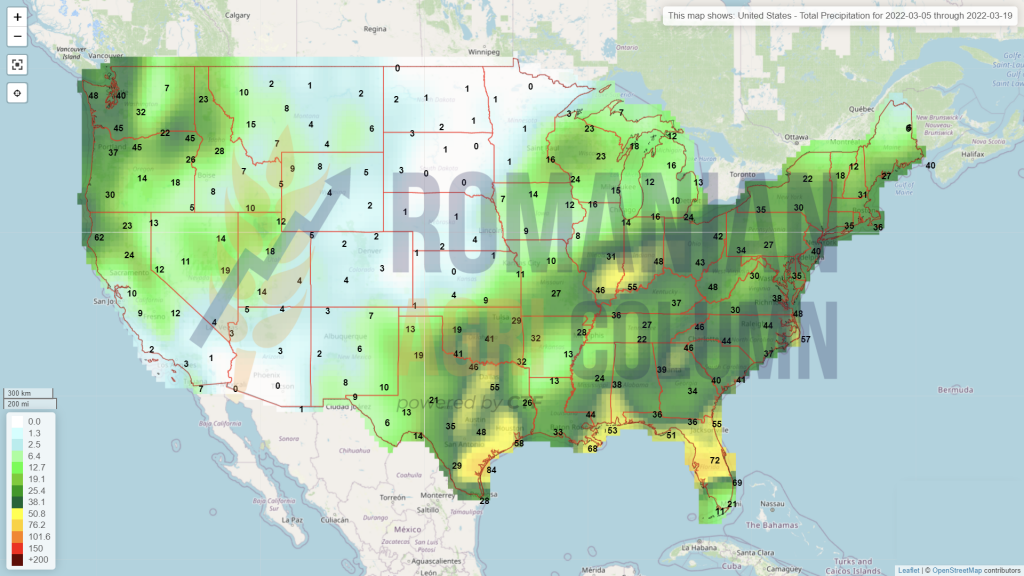

USA (rain)

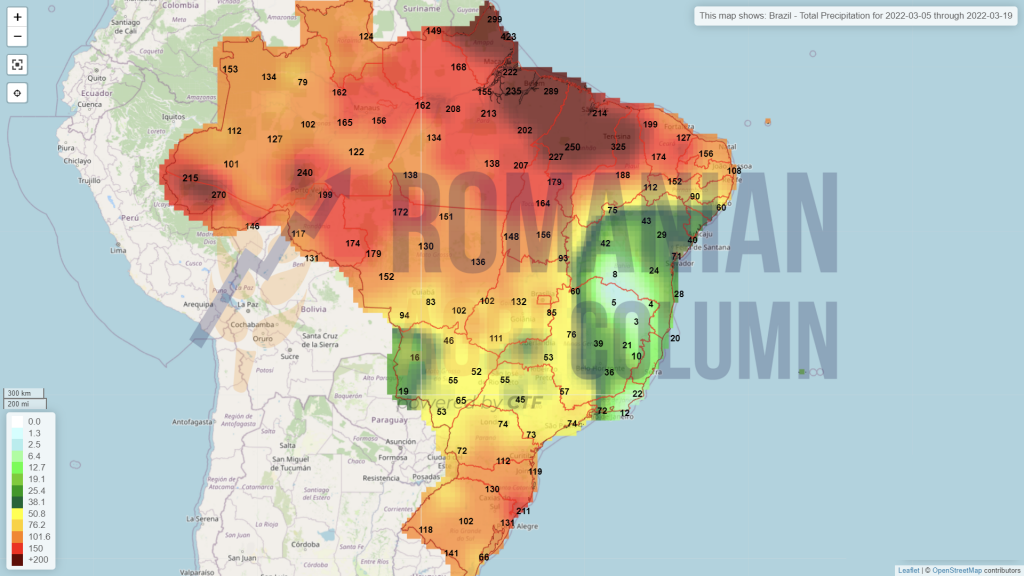

Brazil (rains)

Argentina (rains)

Middle East (rains)

Northern Africa (rains)

China (rains)

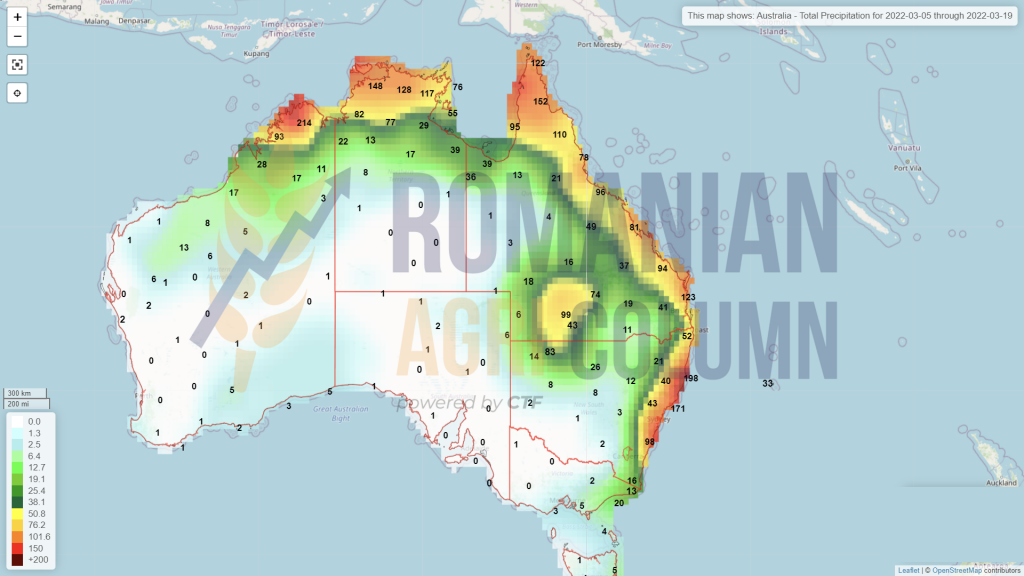

Australia (rains)