This week’s market report provides information on:

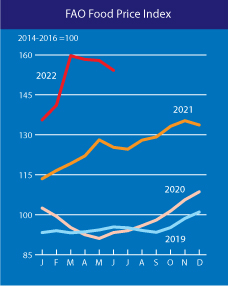

INDEX PRICE OF FOOD AND RAW MATERIALS (July 8, 2022)

SOURCE: https://www.fao.org/worldf or odsituation/foodpricesindex/en/

The FAO FOOD PRICE INDEX * (FFPI) averaged 154.2 points in June 2022, down 3.7 points (2.3%) from May, marking the third consecutive monthly decline, although still by 29.0 points (23.1%) over its value a year ago. The drop in June reflected declines in international prices for vegetable oils and cereals.

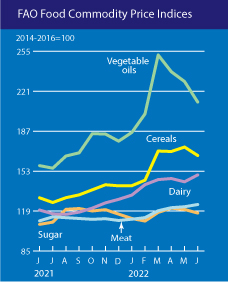

FAO INDEX PRICES FOR VEGETABLE OILS averaged 211.8 points in June, down 17.4 points (7.6%) from the previous month due to lower prices for palm oil, sunflower, soybeans and rapeseed. International palm oil prices fell for the third consecutive month in June as seasonal production growth in the main producing countries coincided with the prospects for increased export deliveries from Indonesia amid large domestic stocks. Meanwhile, global quotations for sunflower and soybeans have also fallen due to reduced global import demand as a result of rising costs in recent months. In the case of rapeseed oil, in addition to streamlining demand, international prices have fallen due to the supply of new crops.

The FAO INDEX OF CEREAL PRICES was on average 166.3 points in June, down 7.2 points (4.1%) from May, but still 36.0 points (27.6%) above since June 2021. After reaching an almost record level in May, international wheat prices fell by 5.7% in June, but rose by 48.5% from last year. The decline in June was due to seasonal availability of new crops in the northern hemisphere, improved crop conditions at some major producers, including Canada, higher production prospects in the Russian Federation and slower global import demand. International coarse grain prices fell 4.1 % in June, but were still 18.4% above the previous year. Declining pressure due to seasonal availability in Argentina and Brazil, where maize harvests have progressed rapidly, and improved crop conditions in the United States supported a 3.5% drop in world corn prices in June. Concerns about the outlook for demand amid signs of an economic slowdown have added to downward pressure. Among other coarse grains, sorghum and barley prices fell by 4.1% and 6.1% in June, respectively, in tandem with lower maize and wheat prices.

LOCAL STATUS

The indications of the port of Constanța are at the level of 350 EUR/MT, with the same consistent discount of minus 25 EUR/MT, if the goods have the quality of feed. Russian pressure is felt in commodity prices, which are in line with the value of the Russians in the FOB Constanța parity. Euronext acts as a marker and the award is made with a Premium level that varies daily between 20 and 14 EUR, according to the FOB level in the Black Sea.

In Romania, wheat is harvested and production variations per hectare are mixed between regions. In the region of Moldova, yields are extremely low, with yields of 2-3 tons per hectare. In other areas that have had constant rainfall, farmers can harvest 7 tons per hectare. It is extremely difficult to calculate, taking into account the degree of fragmentation of the plots and the large number of farmers who own areas in operation.

The logistical nightmare is in full swing. The port of Constanța is the leading exponent of this situation. The queues of trucks waiting to enter the port stretch on the A2 highway, which connects Bucharest and Constanța, for kilometers (between 6-10 kilometers of trucks). At the same time as the occupation of the emergency lane on the highway, the issue of road safety also arises. Seaside tourism is at high altitudes and road flow is extremely high. A potential danger is developing. The tourist flow that goes to the seaside has a narrow path, and the truck drivers who naturally get out of the cabins are extremely exposed.

The origin of the goods is mixed. Romanian and Ukrainian goods are waiting for days for access to the port for unloading.

Communication is also a delay factor. Drivers in Ukraine, not speaking the Romanian language, do not get along with the staff that manages access to the port and thus wastes extremely valuable time. Due to the small width of the access strip in the port, on any gate you would like to enter, the blockage is formed instantly. Any attempt to bypass a blocked truck also results in the blocking of the exit lane from the port.

The waterway is no longer an option. Extreme drought has dried up the Danube and the depth has dropped sharply upstream. The Danube ports will soon be isolated and the transfer terminals will no longer be able to receive or deliver goods to the port of Constanța.

Romanian farmers are extremely dissatisfied with prices. The costs of financing the production cycle have been high and the revenues from the productions made do not cover them. Retention is the phenomenon we mentioned in the last issue. Thus, Romanian farmers take the wheat to their own warehouses, waiting for price increases, financing the stocks through various creditors approved in the Romanian market.

CAUSES AND EFFECTS

The Russian tax lowered the level of wheat sales, penalizing the FOB parity price in the Black Sea basin by 27 USD/MT and adding a pressure in addition to the one generated by the harvest.

August will also generate pressure from Russia in the Black Sea basin. The need to sell is covered by the fact that Russian farmers have to finance themselves. The deadlines arrive without delay and they must be covered by the income generated by the sale of wheat, in order to be able to continue the future production cycle.

However, drought and insecurity will lead to an increase in Euronext and CBOT. The fundamentals win this round in the face of the attempt to stop inflation. Port prices effectively reflect insecurity and low freight.

REGIONAL STATUS

EUROPEAN UNION generates a report of a substantial decrease in the volume level. Thus, for soft wheat, the forecast decreases by over 5 million tons, from 130.4 million to 125 million tons. The most important decreases are generated by Spain, France and Romania. Each of them is thus a direct contributor to this decline. Hungary also has crop volume problems and is also making a negative contribution to this decline in volume.

UKRAINE harvests wheat in the south, but the problems there are extremely high. In the southeast, Ukrainian farmers have the problem of war and harvest among craters and vegetation fires caused by artillery fire. Naturally, the goods enter the warehouses, because there can be no question of shipping.

Also in the southeast, Russia transports Ukrainian goods by truck to their areas, whether they are ports or buffer storage areas. These are daily actions; it is actually a deprivation of goods against Ukrainian farmers. We are talking about the hope of survival, because how else could we call the final thought, that maybe the crop will not be taken by the Russian soldiers? It is an ultimate hope for the survival of farms in southeastern Ukraine.

RUSSIA has started harvesting and preliminary reports indicate good production. It is true that Russia has had optimal conditions throughout the winter and will generate a very good wheat crop. The question to which we do not yet have an answer is the one related to the final volume. It is certainly not a harvest volume of 80-81 million tons. But compared to the claims of Russian analysts of 89.4 million tons, we still have reserves and we would prefer to position their crop level at 84-84 million tons.

EURONEXT MLU22 SEP22 – 357 EUR (+18.25 EUR) | BSW – USD 375 (FOB indication in Black Sea)

EURONEXT WHEAT TREND GRAPH – Certainly, 325 EUR was not a correct level of wheat.

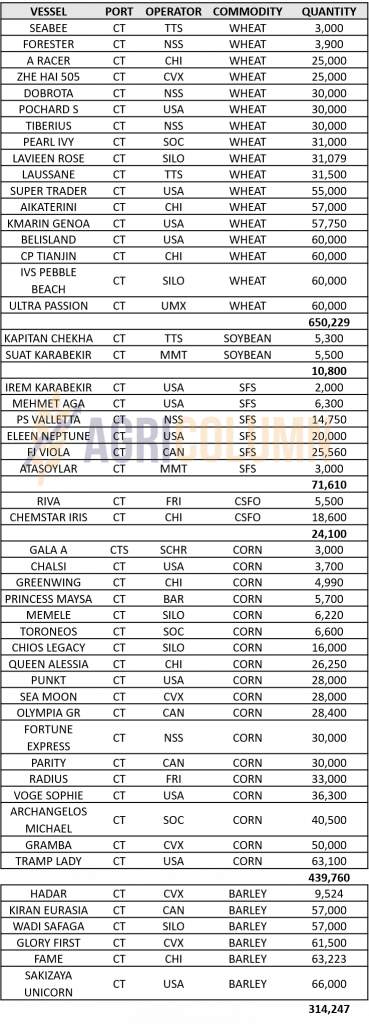

TENDERS

EGYPT acquired through a private procurement organized by GASC a volume of 444,000 tons of wheat in C&F parity, as follows:

- September 1-15, 2022: 77,000 tons from GTCS RUSSIA, at the price of 416 USD/MT

- September 16-30, 2022: 77,000 tons from GTCS RUSSIA at the price of 416 USD/MT | 55,000 tons from Louis Dreyfus FRANCE, at a price of 416 USD/MT | 60,000 from Agro Chirnogi ROMANIA, at the price of 416 USD/MT

- October 1-15, 2022: 60,000 tons from GTCS RUSSIA, at the price of 416 USD/MT

- October 1-20, 2022: 60,000 tons from Viterra FRANCE, at the price of 416 USD/MT

- October 16-31, 2022: 55,000 tons from Louis Dreyfus FRANCE, at the price of 416 USD/MT

EGYPT purchased another 60,000 tons of wheat, with delivery in the second half of July 2022, originating in Germany.

MIT JORDAN purchased 120,000 tons from Ameropa Romania, with delivery in the first and second half of November, 2022 at a price of 427.50 USD/MT in CFR Aqaba parity.

GLOBAL STATUS

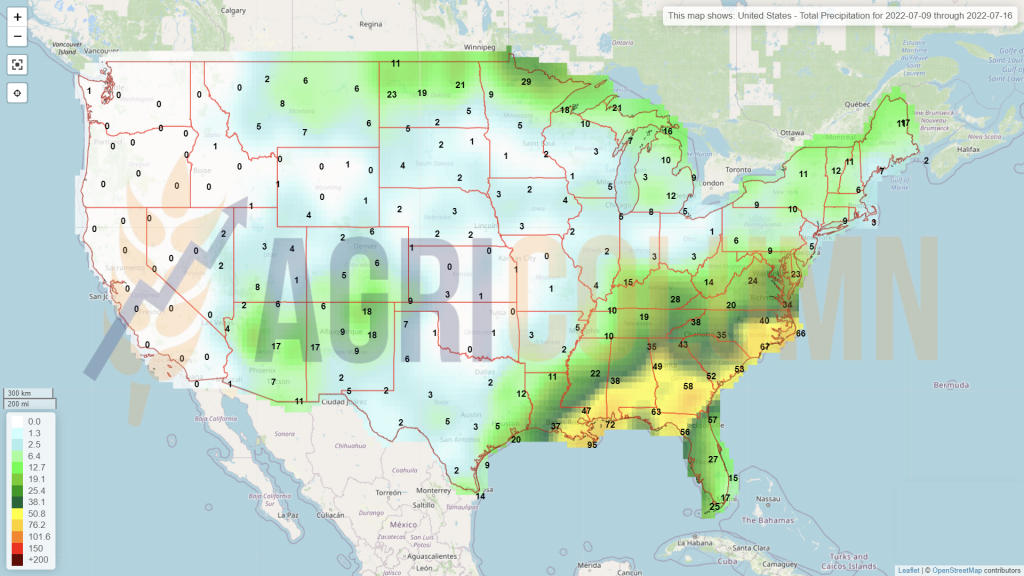

USA. American spring wheat is under good auspices. American winter wheat is in full harvest and has reached a level of 58% above the level of previous years, in terms of progress of harvest.

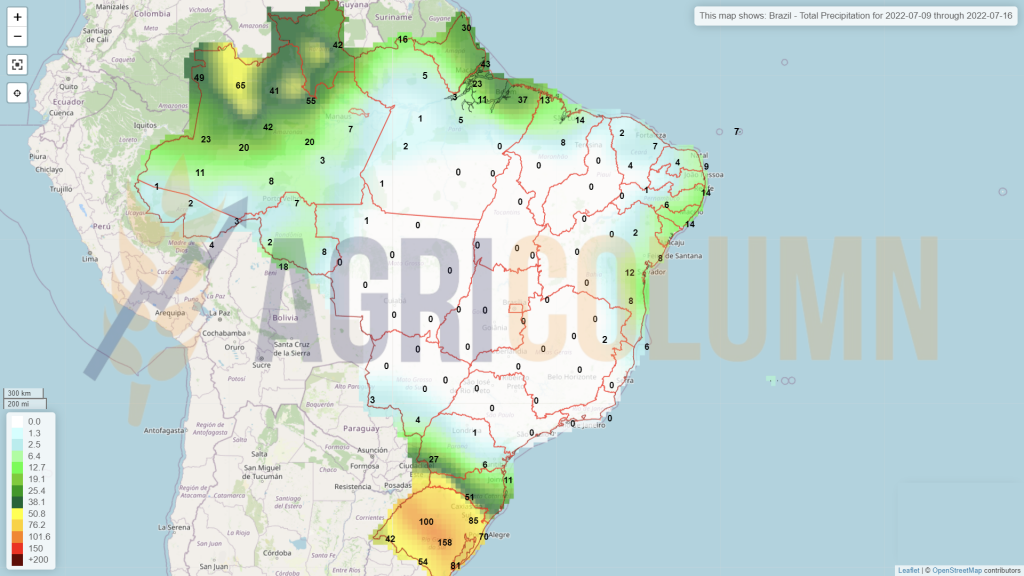

BRAZIL will generate an increase in production by 1.2 million tons, up to the level of 9 million tons.

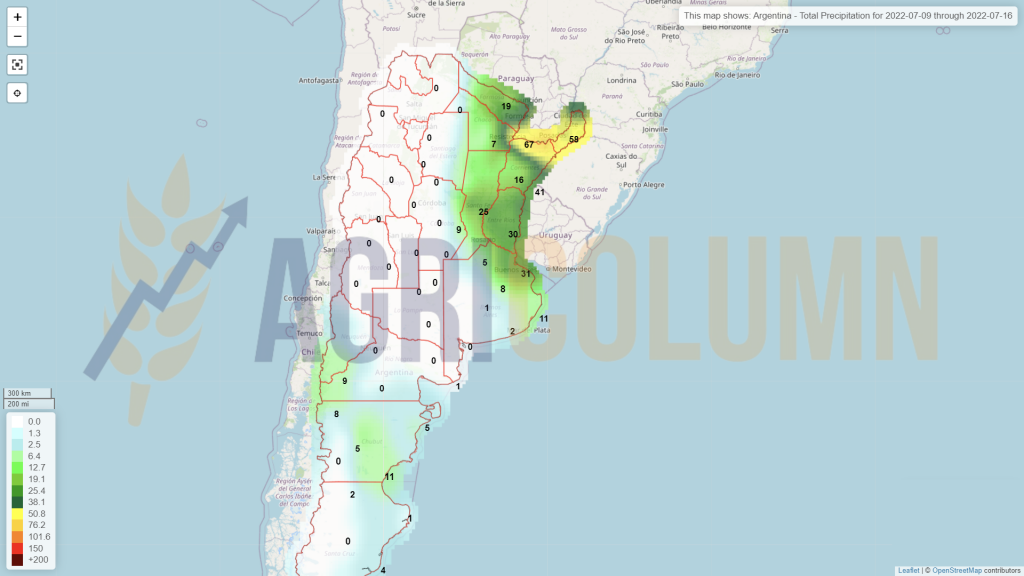

ARGENTINA could reduce the area sown with wheat due to the delays it faces. They are caused by prolonged drought and could lead to a decrease in area from 6.3 million hectares to 6.2 million hectares.

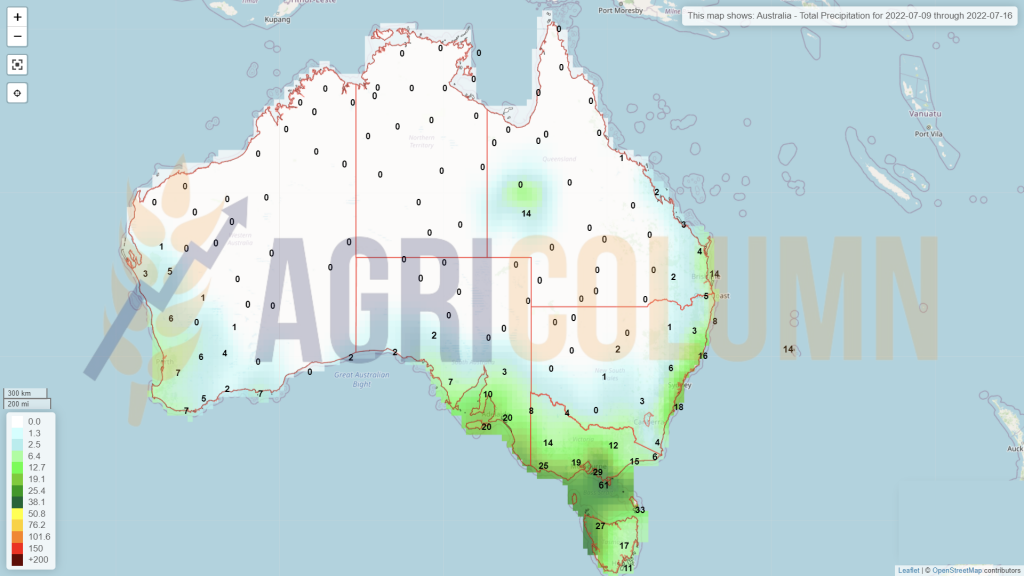

AUSTRALIA is facing marginal wheat problems. The floods are not good, but fortunately, they have not affected large areas sown with wheat.

CBOT ZWU22 SEP22 – 891 c/bu (+55 c/bu = +20.20 USD)

GRAPHIC TREND CBOT – ZWU22 SEP22

CAUSES AND EFFECTS

The wheat market is currently moving between several factors. One factor supports another factor, while another factor contradicts the other two. Let’s analyze and understand the effects. But we set off with the causes.

RUSSIA is lowering the price of wheat globally. Through the level of duty calculated in other parameters, Russia has enough room for maneuver to be able to control the price level and thus become competitive in the wheat trade. Movement to convert the price formation index into rubles and its statutory last week at 15,000 RUB/MT in MOEX (Moscow Stock Exchange) generated a decrease in the export tax, by raising the level where the taxation starts. Through this action, Russia has become competitive and the first effects are already visible in the Black Sea basin, the volumes sold directly to GASC being witnesses to this. From a level of 387 USD/MT FOB Russia, today we have a level of 360 USD/MT FOB Russia for PRO 12.5 wheat.

The fact that FEDERAL RESERVE announced that it will intervene again on July 15, 2022 is another factor. The intention will certainly materialize, but only the number of points will remain in question. Will there be an increase of 0.75% or 0.5%? It remains to be seen, but the liquidation of the positions on CBOT and EURONEXT indicates this certainty. And it’s not just about the liquidation for July 2022 and the transfer to the new crop, naturally. It is about anticipating what will come and impact the Futures market. The value of collateral will no longer be supported by cheap money and thus the balance of risk will shift to skepticism. The only answer that fund managers ask themselves is: Is the potential for margin gain sufficient to cover the costs of financing material guarantees? And if so, what is the risk of it not happening?

THE WEATHER that generated the decrease in volumes in the European Union is the compensator of the two factors above. Demand exists, but volumes are projected to be smaller. The only unknown of the volumes is Russia. How much will it generate as production? 82 million tons? 85 million tons? Or 89.4 million tons? For, if we calculate the highest value of the Russian forecast, it compensates for the loss of volume of the European Union.

And now with the factors in place, we were trying to understand how they compensate each other. Clearly, the Russian crop will partially, if not totally, offset the European deficit. In such conditions, we are trying to understand the high degree of competition generated by France in the last sales to the destination Egypt, and this in the condition that they had not started the harvest yet. The decreasing price trend between the two sales of minus 24 USD/MT indicates a potential price degradation and we believe that France has intuited well. Selling what is not yet in the barn, it generated the short position, and will cover (trading companies) in the harvest pressure.

This risk appetite for France also indicates an estimate of close potential (the price of wheat) which will certainly not be very high, taking into account the first two factors. The volume of the Russian crop associated with the tax cut blends perfectly with the FED’s intention to raise interest rates. However, in this mixture we must also take into account the WASDE report that will be released on Tuesday, July 12, 2022.

EURONEXT will make this YO-YO move in agreement with CBOT because the next liquidation of positions will be at parameter SEP22, and the indication of Jerome Powell, President of the FED, was clear. You will leave the positions at liquidation, not at the interest rate increase. Practically, they still have to play until the end of August 2022 and this game will be influenced by the WASDE report of August 12, 2022. And from what is seen now, that ratio will be unfavorable to the global volumes of wheat. But if Russia will be quoted at 89.4 million tons of production, 7.4 million tons will compensate for the shortcomings of the European Union. However, EURONEXT followed the liquidation effect of CBOT without positioning the focus on the physical foundations, which foundations came and repositioned the wheat to the normal level, in a complex that positions the wheat in the Black Sea basin rising from 360 USD/MT at 375 USD/MT in FOB parity.

UKRAINE-MYKOLAIEV. A new rocket attack destroyed a port silo. Hunger games continue. No chance for discussion. CBOT and Euronext will raise for this reason, even if it has become commonplace.

RUSSIA aims to show who decides the price of wheat and through this gesture raises the price in the Black Sea basin. In other words, it indicates who leads the wheat game, at least regionally. With a single rocket, they raised the price of wheat in the basin.

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

LOCAL STATUS

The price of barley is degrading in the CPT Constanța parity and we see how its level is slightly away from 300 EUR/MT. More precisely, 297-298 EUR/MT is the current price level in the port of Constanța.

REGIONAL STATUS

Ukrainian barley is offered in the parity of CIF Constanța at the level of 280 EUR/MT for July deliveries.

Jordan purchased 60,000 tons of barley from Trans Oil International, at a price of 360.5 USD/MT, CFR Aqaba. Delivery will take place in the second half of October 2022.

CAUSES AND EFFECTS

Naturally, the price of feed barley is in line with the price of feed wheat, but the season has just begun. Globally, barley appears to be unbalanced in terms of volumes versus demand, as it was last season. So we do not rule out a price recovery after November 2022, taking into account that the market was marked by the last sales until the mentioned period.

BARLEY PRICE INDICATIONS – RUSSIA AND AUSTRALIA

LOCAL STATUS

The price indications of maize in the CPT Constanța parity are at the level of 280 EUR/MT. The price downgrade subsequently targeted corn as well. However, due to the fact that it is still in the fields, the degradation is not so strong. Overall, if we draw a line between 320 EUR/MT (past levels) and 280 EUR/MT (today’s price), we see a significant difference. 40 EUR/MT is a figure which, if multiplied by a volume, generates a very large deficit from a financial point of view. The old corn crop has the same indication as the new crop, so there is no crop inverse.

Remaining in the area of the word deficit, we must turn our attention to the Romanian corn, which these days suffers extremely due to lack of water. The area of Moldova is completely affected, and Dobrogea and the southern counties of Călărași, Giurgiu, Teleorman and Olt, as well as quite large areas of Timiș have extremely big problems. The western plains also lack water.

We are moving quickly towards a production deficit due to the lack of water supply in the soil. Water was lacking during the winter, and the reserve was not built. We see the year 2020 repeating itself and we see the initial corn production declining dramatically day by day. The rainfall did not mean much, it did not constitute in the areas where a positive balance of the water deficit fell.

We were trying to be realistic and see the stages of this episode, but the ending doesn’t look good at all. At least 22-25% of the expected corn crop will be evaporated in its own way by excessive heat and lack of precipitation. Getting out of the heat wave was beneficial. Plants can breathe and vegetate, but unfortunately, in many areas they are actually lifeless, so implicitly without any hope. Not to mention the fact that a heat wave is coming again.

The momentary intentions of the farmers are directed towards retention. The reduced volumes lead to a higher price potential in the future that will be written after the harvest.

CAUSES AND EFFECTS

The local market is given to the global market, and the latter reacts to the stimulus called drought. The Romanian export market still retains its logistical advantage. The price difference is to the advantage of Romanian and Ukrainian corn transited through the port of Constanța. On the Texas – Asia SE route, the transportation costs of one ton of corn amount to 75 USD/MT, while from Constanța to the same destination, the transport cost is 47.5 USD/MT. The difference in logistical cost can be used in the purchase of goods from farms.

REGIONAL STATUS

HUNGARY has extremely severe drought problems in the eastern part of its territory. Estimates lead to a decrease in the volume level by 25-30%, which seems realistic today, considering the Pannonian desert, ie a flat plain, without landforms.

SERBIA faces the same problems. A decrease in crop volume is expected here as well, due to excessive heat.

FRANCE and SPAIN are also in line with this unwanted trend and will, in turn, record declines in production.

UKRAINE remains at the same volume level, of 27.7 million tons, but the problems faced by Ukrainian farmers are found in the financial complex. In fact, they can’t finance the next harvest if they don’t sell. Thus, they continue to sell at discounted prices. The need for liquidity is very high. They are in a position to manage stocks, sales, storage space and maturities, plus the necessary capital to continue the production cycle. The farthest subject is for them the future crop. In fact, they claim that they are not interested, because they have to sell, harvest and store, as well as to avoid the effects of Russian bombing, artillery attacks and ground assault. Many Ukrainian farmers lose their lives as collateral victims in the war. Many are actually killed by Russian troops targeting combine harvesters and tractors.

EURONEXT XBX22 NOV22 – 306.75 EUR (+17.75) | EUROENXT REACTS TO DROUGHT

EURONEXT CORN TREND GRAPHIC – XBX22 NOV22

GLOBAL STATUS

US increases the area sown with corn compared to the intentions of March 1, 2022. Barchart releases an update on the American corn and soybean crop. The first estimate was released on June 21, 2022, and this update arrived on July 5. In summary, the data indicate: plus 5.1 million tons, up to the level of 373.53 million tons.

Productivity increases from 176.4 bu/acre to 178.4 bu/acre, ie 11.19 tons per hectare. But the fields in Indiana and southeastern Illinois are at a critical juncture: they desperately need rain, but good yields are still possible. This week will be decisive, especially for corn. But the conditions for drought in CORN BELT are extremely high.

BRAZIL has the same status as in the previous report, with an increasing volume of up to 119 million tons, consisting of the two crops, Safra and Safrinha.

ARGENTINA is out of the corn crop, but let’s keep in mind in the future the persistent drought that prevents the accumulation of water in the soil.

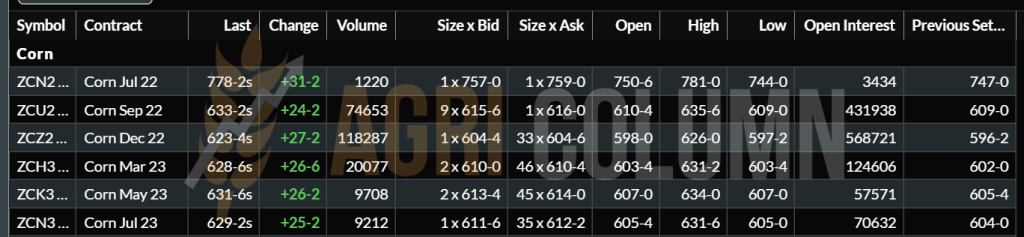

CBOT ZCZ22 DEC22 – 623 c/bu (+27 c/bu = +10.6 USD) | DROUGHT URGES FUNDS TO RETURN

CORN TREND GRAPHIC – ZCZ22 DEC22

CAUSES AND EFFECTS

The European Union’s crops are being called into question. Volumes will be degraded and corn imports will increase. Ukraine will be the main element of origin, along with Romania.

The northern hemisphere of the American continent represented by the USA generates a much larger volume projection. It is a partially offset effect with Europe. At this point, nothing is certain. The American Corn Belt is in good condition. Precipitation has helped this status, but August is coming, a month that is 100% critical for the United States. Then the direction of the corn will be decided.

In numbers, what is declining in the European Union is offset by Ukraine and the US, but Brazil and Argentina will re-enter the game much later and so the price trend is totally unpredictable.

In addition, political and financial factors will also play a key role. The effects of the future EDF increase could overshadow a potential rise in maize prices. Let’s not forget that everything has risen in the price spiral due to the EDF printing press. It is her turn to act in the opposite direction, because it has certainly generated a positive margin in the printed money supply to counteract the effects of the pandemic.

The corn will therefore be marked by WASDE on 12 July and 12 August, by the FED announcement on 15 July and by the weather in August. It is a route that cannot be foreseen, but can be assimilated with that of wheat. But let’s not forget the drought of 2020, which drove the price of corn higher than that of wheat.

CORN INDICATIONS IN MAIN ORIGINS (old crop)

LOCAL STATUS

The rapeseed experienced a boost that propelled it to a level of 700 EUR, granting EURONEXT AUG22. However, many traders kept the initial discounts between minus 15 and minus 40 EUR/MT compared to AUG22. However, there are two traders who do not have coverage at the moment and quote the equivalent of AUG22 in CPT Constanța. The harvest being in progress, the logistics is still extremely expensive and we see a very wide plateau of prices and indications offered in the FCA FARM parity.

At regional level, the European Union indicates a drop in harvest volume below 18 million tons, more precisely by 17.9 million tons, which subsequently raises rapeseed prices.

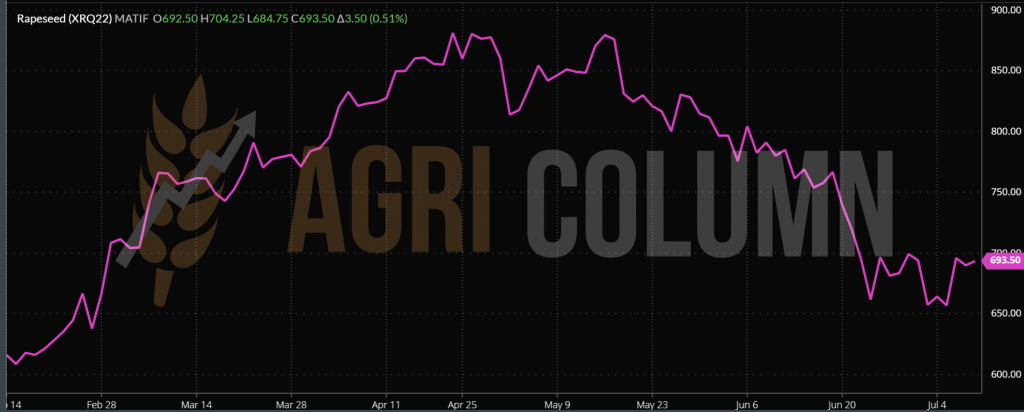

EURONEXT XRQ22 AUG22 – 693.5 EUR (+3.5 EUR)

EURONEXT RAPESEED TREND GRAPHIC – XRQ22 AUG22

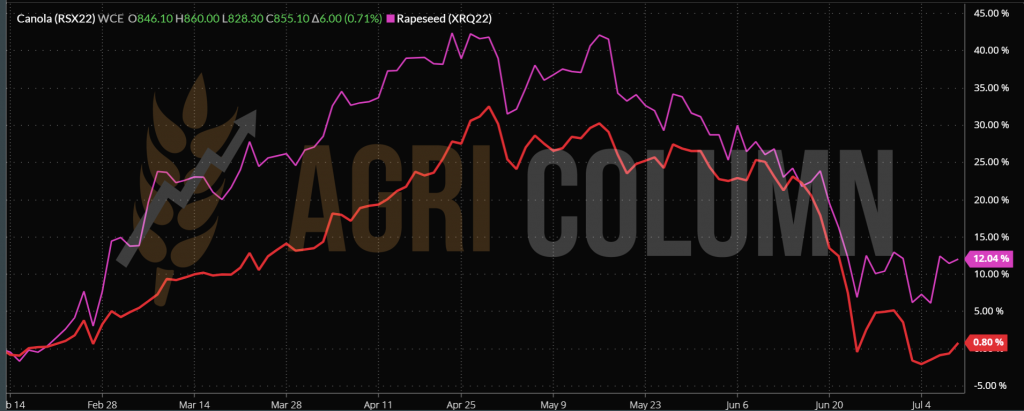

CANOLA, in turn, indicates a sustained increase, after viewing it, below 800 CAD/MT. Moving funds from profit taking and returning to positions generated support.

RSX22 NOV22 – 855 CAD (+6 CAD)

GRAPHIC TREND RSX22 NOV22 – CANOLA CANADA

COMPARISON: EURONEXT RAPESEED – ICE CANOLA CANADA

CAUSES AND EFFECTS

The rapeseed finds its lost breath. The increase is not significant, but indicates the reaction after the funds leave the positions and update them after profit taking. The decrease of 200,000 tons of European Union production also contributed to this.

Palm oil also returned to growth. Even if it is not extraordinary, it indicates a positive trend, it indicates the demand, as it ultimately decides the price of physical goods.

In a normal context, unaltered by the FED, we could see a 4-5% return in the price of rapeseed in November 2022. But we repeat, in an unaltered context of the FED. We’ll see the effect in a few days.

LOCAL STATUS

The price indications experienced a revival generated by the lack of appetite of farmers in contracting and we indicate 560 USD/MT DAP processors and subsequently 570 USD/MT CPT Constanța. Moreover, the USD-RON parity makes the price in RON particularly attractive, due to the exchange rate. The indications of the bonus for sunflower seeds with high oleic acid content amount to 40 USD/MT. This confirms the statement in the last issue in which we forecast demand from the European Union.

However, the state of the crop does not show positive signs. The drought is causing obvious concerns across the country. We already estimate a potential degradation of at least 10-12% at this time. The areas with the biggest problems remain those in Moldova, which also include the counties of Galați, Brăila, as well as Dobrogea. No parts of southern Romania are bypassed by problems. Therefore, we need to lower the initial crop estimate from 3.6 million tons to a level of 3.2 million tons. And things, we are inclined to believe, will not stop here. Excessive heat will damage plants decisively, as it has done so far.

REGIONAL STATUS

In all this context, we see indications of goods from Ukraine that penalize the Romanian seed market. We see October delivery a lot that is quoted at 460 USD/MT DAP Bulgaria, which is very unlikely to happen, but there are indications generated by the lack of clear information.

To consolidate the information, it should be known that in CIF Marmara, the price of sunflower seeds at this time, ie the old crop, is 700-710 USD/MT. If we calculate a transport cost of 40 USD/MT on the Constanța-Marmara relationship, we get 660-670 USD/MT FOB Constanța.

UKRAINE is doing well in terms of vegetation and there are no concerns at this time.

However, the European Union will shrink in volume due to the persistent drought that is creating huge problems at European level.

CAUSES AND EFFECTS

The drought will penalize the volume of sunflower seeds, not only in Romania, but also in the European Union. Ukraine will try to compensate with raw materials, but things are not going the way everyone wants.

We thus see an increasing level of the price of raw materials, driven by the effects of drought, the decrease in the volume of goods and implicitly perhaps the logistical cost. Because in the end, the farmer does not have to bear the logistical cost. It should be segmented on the supply chain between the components. Each segment of the chain must be part of the gain and loss.

CSFO AND OILSEEDS INDICATIONS IN MAIN ORIGINS

LOCAL STATUS

The local indications of the new soybean crop are at the level of 550-560 USD/MT for the goods delivered in parity DAP processor. To this level is added, according to the local market, a coupled support per hectare, after obtaining the proof of commercialization to the Romanian processors.

The crop is irrigated during this period in order to generate the estimated harvest volume. This is visible in the regions that mainly cultivate this culture, in the areas of Călărași, Giurgiu, Brăila and Galați. Beneficial areas for soybean cultivation are also in Timiș County, in western Romania.

REGIONAL AND GLOBAL STATUS

The United States recorded a sales volume of 240,000 tons of soybeans last week, up from the previous week. Sales are supported by the dramatic decline in soybean grain prices. At this time, there are no major concerns about soybean cultivation in the United States, but drought forecasts indicate problems on the horizon. Statistically, August is the one that creates problems for American soybean cultivation. But the problems caused by the drought could come much earlier, more precisely after mid-July 2022.

Amid concerns about a potential drought, CBOT is on an upward trend, helped by the return of funds after the massive exodus generated by the EDF effect.

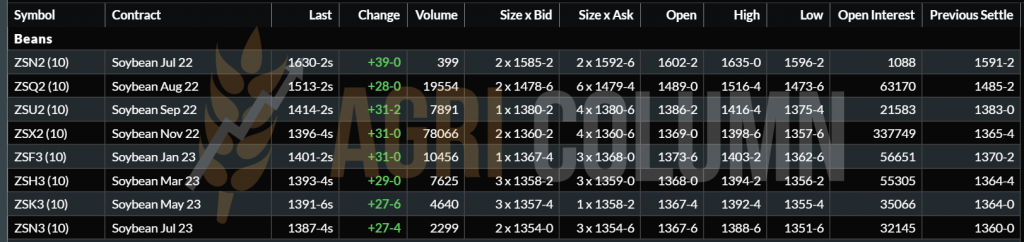

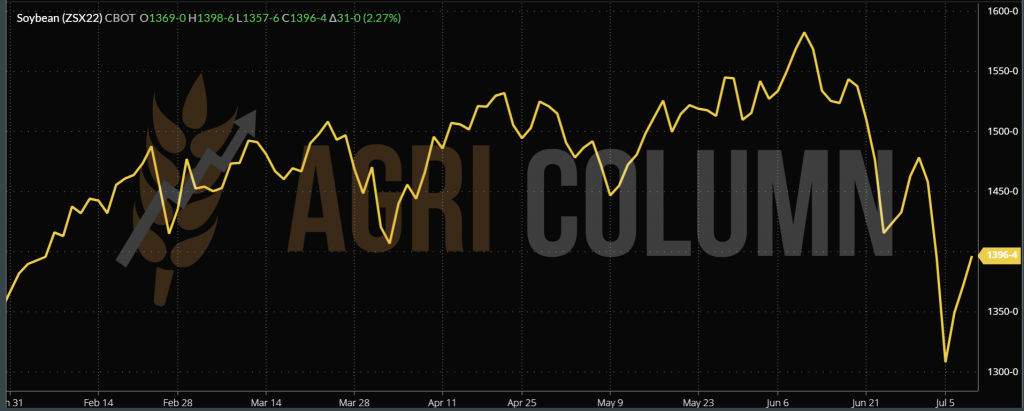

CBOT SOY ZSX22 NOV22 – 1,396 c/bu (+31 c/bu = +11.4 USD)

GRAPHIC TREND SOYBEAN CBOT – ZSX22 NOV22

CAUSES AND EFFECTS

The decrease in soybean grain prices was generated by volume forecasts: USA 123 million tons, Brazil 149 million tons, Argentina 55 million tons, Paraguay 10 million tons. In addition, the FED has taken on the role of correcting inflation and, in turn, adjusting stock prices, raising interest rates.

But the lack of water globally is very visible. Drought is already a spectrum that will be perpetuated from year to year and this supports the price of soybeans, as well as other categories of raw materials.

In a very short time, we will see the trend, but we must keep one thing in mind. The population must be fed and from this point of view, raw materials must be affordable.

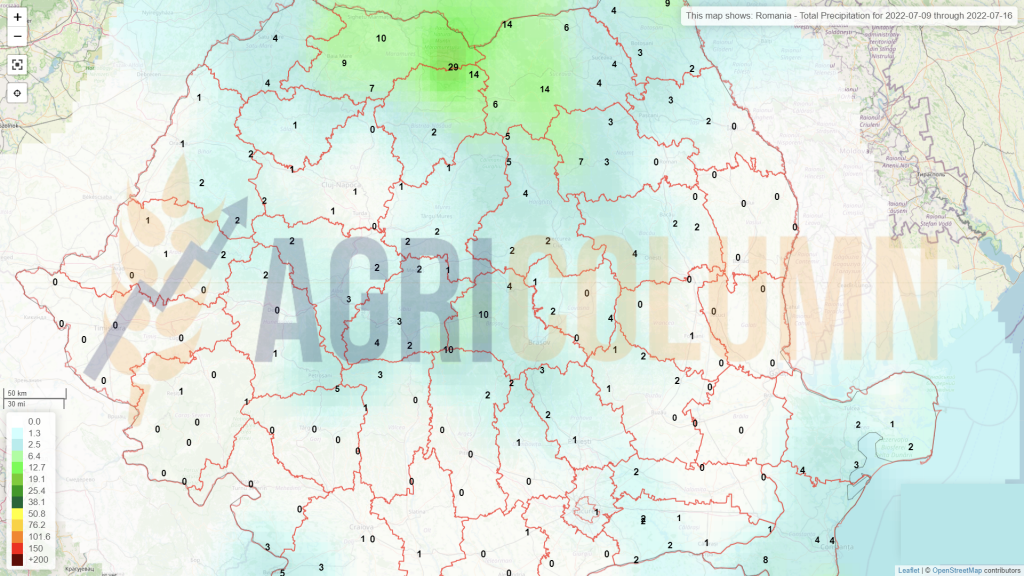

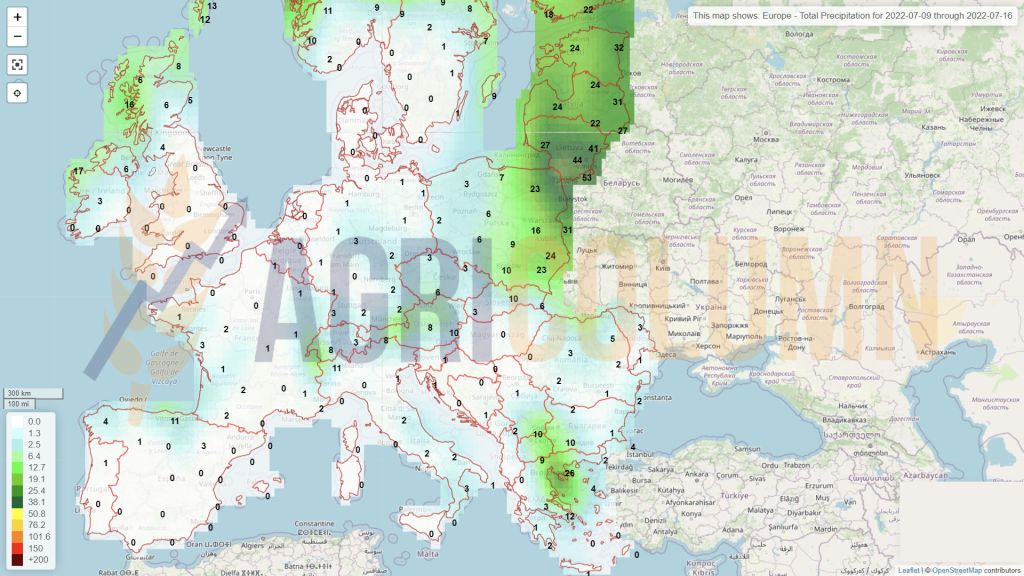

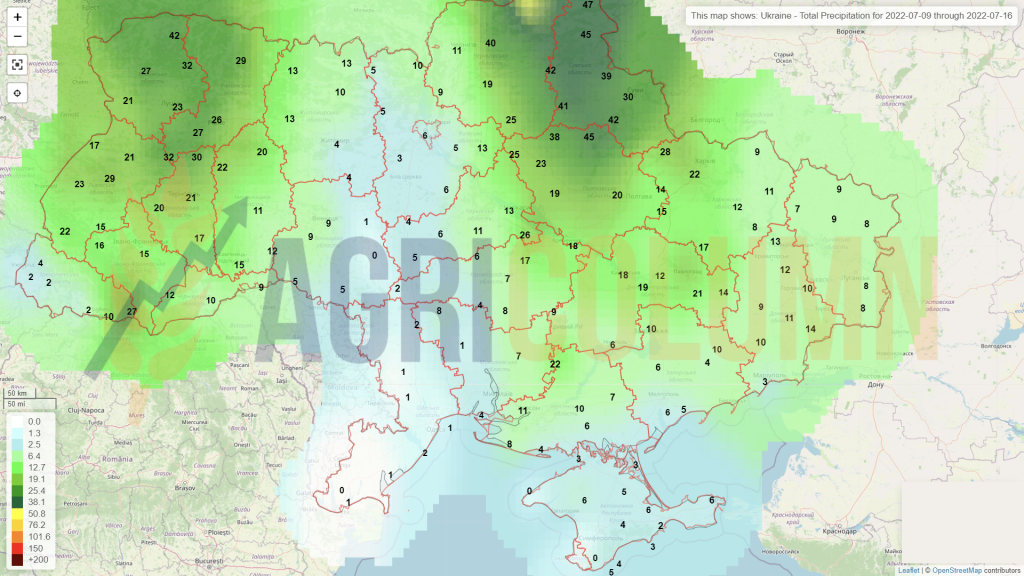

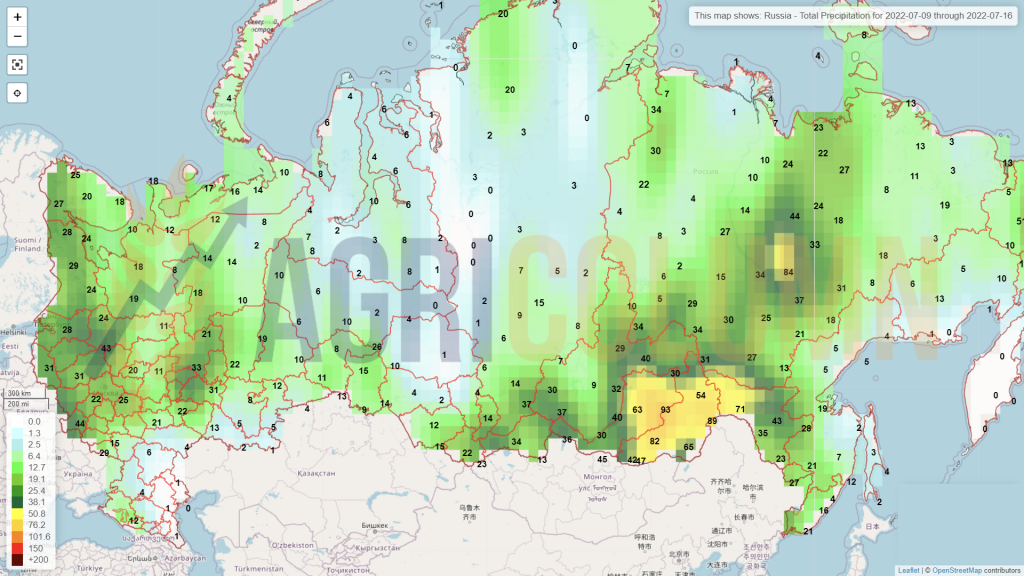

9-16 July 2022

Romania

Europe

Ukraine

Russia

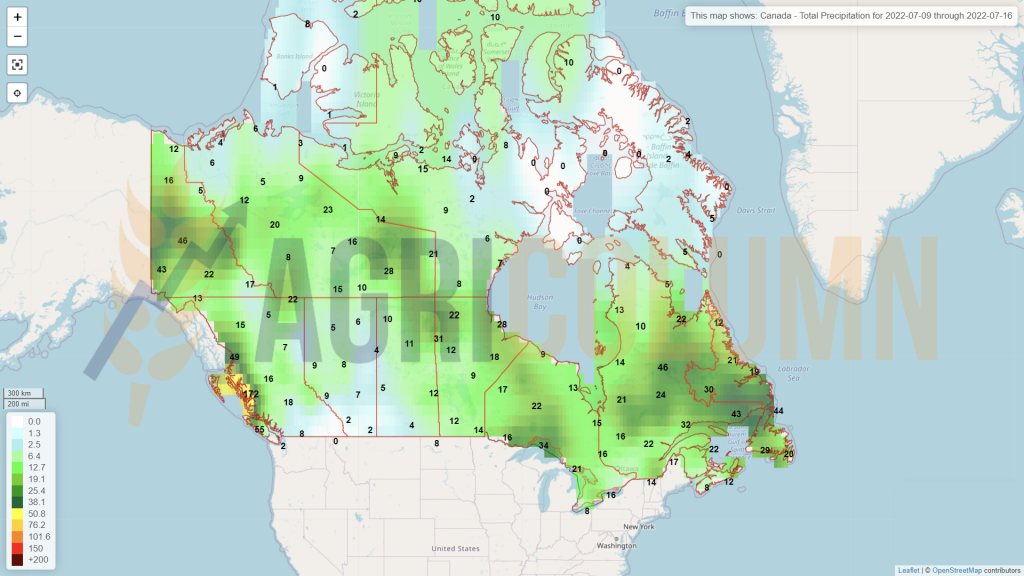

Canada

USA

Brazil

Argentina

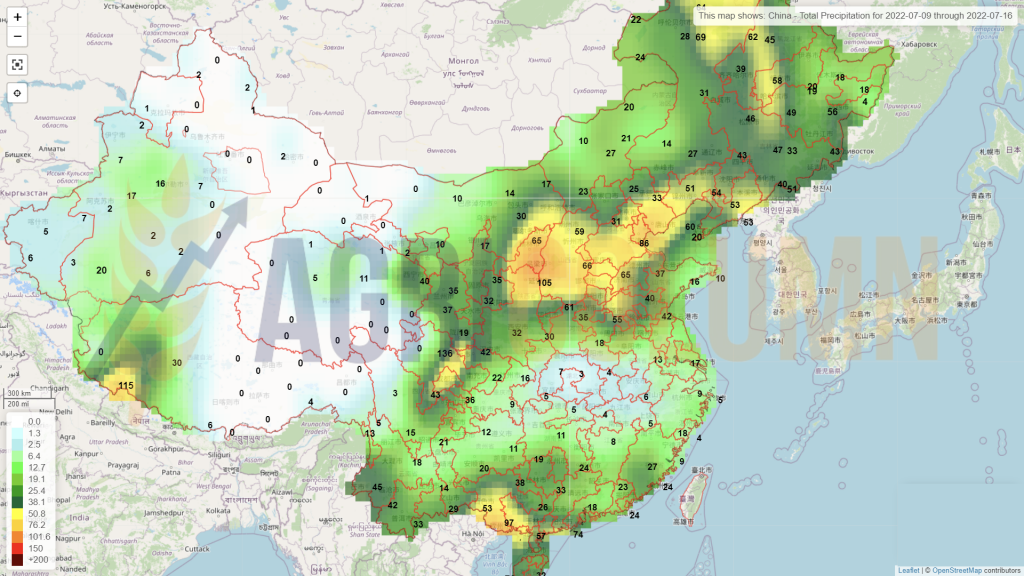

China

Australia