This week’s market report provides information on:

LOCAL STATUS

Romanian wheat prices fluctuated continuously between 365 and 385 EUR/MT, ending the week at a level of 370 EUR/MT in the CPT Constanța parity. The differences were made by the EURONEXT levels, which fluctuated between political factors that resonate with the price of goods, due to the war in Ukraine. We have the same negative difference for feed quality – minus 20 EUR/MT from the indicated price. The difference is still very large, if we look at the overall balance of wheat.

CAUSES AND EFFECTS

Combined weather and political factors have generated this carousel of increases and decreases for Romanian wheat. The stabilization occurred at the level of 370 EUR/MT, following the GASC auction, which has already given Romania an advance in the 2022-2023 season. Thus, Romania won a volume of 240,000 tons at a price of 442 USD/MT in the parity of FOB Constanța. The transport will be carried out by NNC (National Naval Company) from Egypt, the final price at the destination reaching the value of 480 USD/MT.

Converting EUR to parity of 1.07 indicates a price of 413 EUR/MT in FOB Constanța. However, there are many other costs to be deducted, such as fobbing, bidding, financing (because the payment will be made by the Egyptian state within 180 days on the basis of a letter of credit guaranteed by the government). It is also necessary to reduce the quantity differences, the so-called shrink, as well as the trading margin of the exporter. So the final calculations decrease from the price of 413 EUR/MT in FOB Constanța quite a lot of euros. The final value in CPT parity may not exceed 385-387 EUR/MT.

SHORT-TERM VIEW – ROMANIA MARKET

- Romanian harvest pressure, associated with the offers of Ukrainian wheat which is at the level of 296 EUR/MT DAP northern border Romania.

- The market is waiting for the parameters that will decide the recession. Very soon, on 14 June 2022, the FED will announce an increase in interest rates.

- Between the peak of 415 EUR/MT and 370 EUR/MT we already have a difference of 45 EUR/MT in the negative direction. Farms that have initiated an individual consulting contract with AGRI Column they had the necessary guidance before the seen declines and made timely decisions. [email protected] is the address where you can request the service package.

REGIONAL STATUS

RUSSIA increases the level of domestic production to 87.3 million tons and raises its export level to 42 million tons.

UKRAINE is in the same status as last week, with 20 million tons of production. But the figures we have for the end of May in terms of exports are only 42,000 tons of wheat. They managed to cross the borders and be sent.

FRANCE, despite the precipitation received, does not show signs of recovery, but still relies on a level of 33.6 million tons. Until we have complete figures, we remain conservative and continue to indicate 32 million tons of soft wheat.

CAUSES AND EFFECTS

RUSSIA actually plays chess with the whole world. It has two moves in front of everyone. Indeed, markets in Asia, the Orient and partly in Africa are beginning to be controlled by Russia. And so we have a clear and concise explanation of how the level of Russian crop and export estimates have increased.

It all started with Kazakhstan, which registered Russian-owned companies and transport units under Kazakh tax identity. It effectively created the first conveyor belt and then signed trade agreements with China and India for the delivery of wheat. When India lost in terms of cargo volumes, the heat reduced the Indian crop by 12 million tons. It was a suspension. After announcing a freeze on exports, India returned and said they would supply about 500,000 tons of wheat to surrounding countries and Egypt. At the same time, Indian trading companies received the approval of local banks to open letters of credit for the payment of Russian wheat. And another move is highlighted by insurance companies (excluding London) that will cover the risk for ships entering the Black Sea and loading at Novorossysk, Russia.

Thus, the road was smoothed, as we had predicted for about two weeks, namely that India and Kazakhstan become the turning points of Russian wheat. India will sell its own wheat and receive Russian wheat in return. Moreover, it will supply Bangladesh as well as other surrounding countries. And Bangladesh imports 4 million tons of wheat annually.

Ironically, the UN has called on India to replace Uganda and Ethiopia with wheat. In other words, they sent a clear message: we know that you are receiving Russian wheat, so supply these countries with your wheat, since you will replace it.

Iran will import 5 million tons of grain from Russia via the Caspian Sea and will pay in car parts. We also know that Renault has a presence in Iran, and Russia has taken over the Renault plant from its territory. We could say that it is a happy coincidence: demand meets supply.

Pakistan has said it will import 2 million tons of wheat from Russia to support the low local crop due to the heat, becoming another market that Russia will control, along with India, Bangladesh, Iran, Syria, Egypt, as well as East Africa. If we include here China, which annually imports about 10-12 million tons of wheat, we have the complete picture: South Asia, China and East Africa.

Moreover, the latest developments indicate that African countries are demanding Russian wheat, and we are talking about just one example, Zimbabwe, one of the 24 countries that did not support Russia’s exclusion from the UN Human Rights Council.

Returning a little closer to the Orient, the Ukrainian wheat stolen from Russia is unloaded in Syria and then distributed. Turkey is receiving the same accusations from Ukraine that it is buying Russian-stolen wheat from Ukraine.

Russia uses as a predator the weakness of the West and we take the avoided sanctions as an example (the SWIFT payment system is avoided by paying in barter, rupees and yuan). What the West does not understand is that the world, first of all, must be fed and it does not matter by whom and how, and secondly, it is not composed only of the West. When hunger sets in, you don’t have much choice, but with a full stomach (as we can say about the West and the UN), you can keep your principles. However, the UN knows that there will be Russian wheat in East Africa, and yet it is compromising.

The predator is in the midst of shaping the world, occupying its positions of strength in Asia and the Orient, and creating two worlds. This is exactly how I estimated it would be on February 25, in an article in Ziarul Financiar, namely that Russia will control the wheat and sunflower oil market. And they will not give up, because they know that the world must be fed, the world must be kept calm by food.

On June 8, 2022, an attempt will be made to mediate and create a corridor for the extraction of Ukrainian goods through the port of Odessa. The meeting will be moderated by Turkish President Erdogan and, if successful, will be strengthened by a UN resolution. In principle, the parties agreed. Russia has apparently made concessions but has achieved something, and we believe that what Russia has achieved is the ability to transport large Panamax ships to destinations. In other words, the insurance will give flexibility to shipowners who will send their ships for loading to Novorossysk, Taman or Tuapse in the Sea of Azov. But if this happens, it will put pressure on the price of wheat. A flow of goods entering the market means a coverage of demand and, implicitly, a relaxation of prices. However, we believe that Russia will not leave this corridor open for too long, but will even use the demining of the Odessa port area to try a troop run directly into the port, to occupy a bridgehead and to make the junction with his troops from the southeast.

The map we insert indicates much more than words can make the Russian presence and the occupation of the Black Sea outlets, associated with the presence in the main areas of origin of Ukrainian wheat.

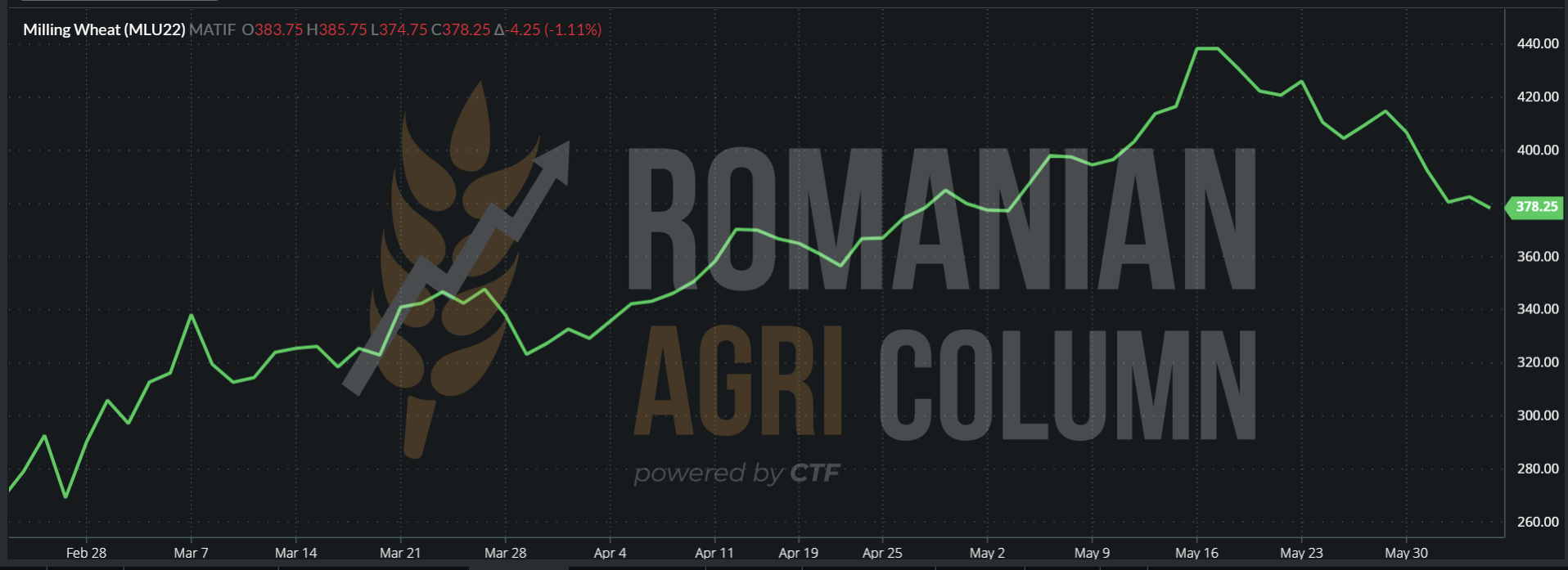

EURONEXT is losing ground every day. The association with the possible initiation of an export corridor through Odessa weakens the tension and thus the wheat decreases.

EURONEXT MLU22 SEP22 – 378.25 EUR (-4.25 EUR) at the end of June 3, 2022

EURONEXT WHEAT TREND GRAPHIC – MLU22 SEP22

GLOBAL STATUS

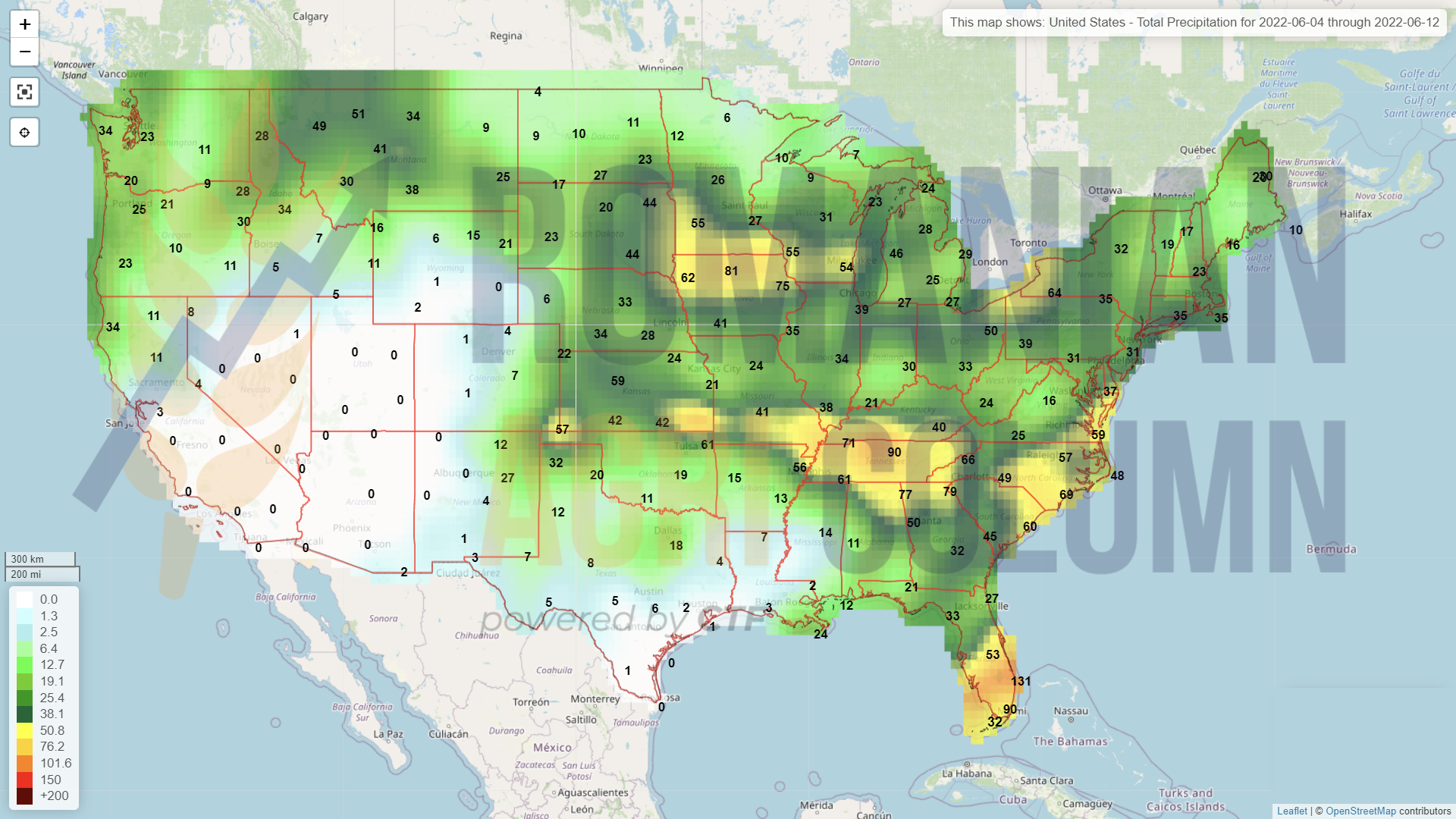

United States is in the same state of play, even though winter wheat has begun to be harvested. Texas and Kansas remain the US states with the biggest problems. Local sources even indicate a 60% wheat field abandonment rate in Texas and about 8% in Kansas. Abandonment means non-harvesting. Unfortunately, all our signals from December 2021 to the present have been correct and we maintain our estimate of only 44 million tons of American wheat crop in winter + spring, compared to 47 million tons, according to USDA data of May 12, 2022.

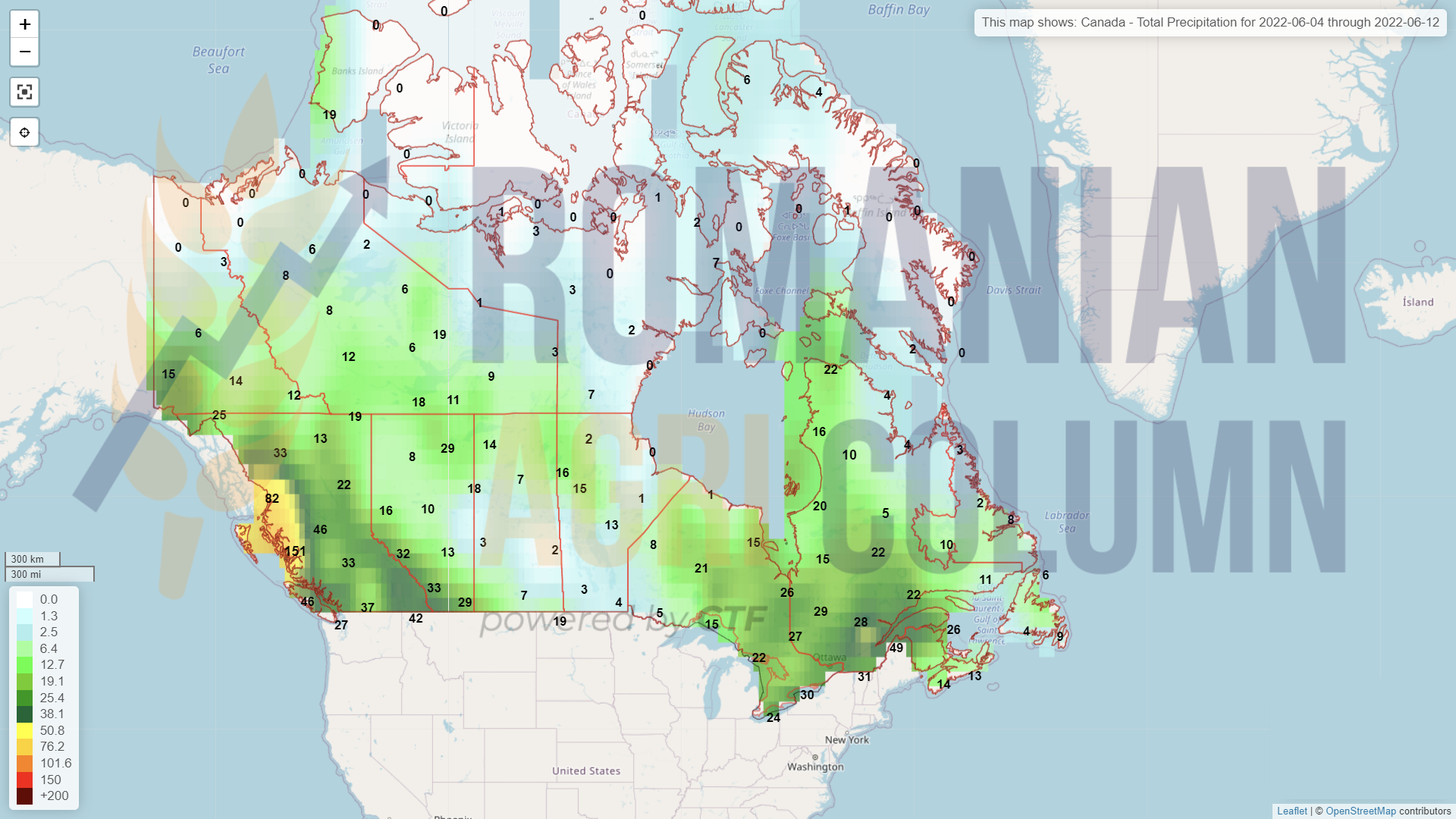

CANADA indicates an increase of 3 million tons compared to previous estimates. Canadian crop yields are 33 million tons, compared to 30 million tons. Precipitation in Canadian prairies has been auspicious for Canadian wheat.

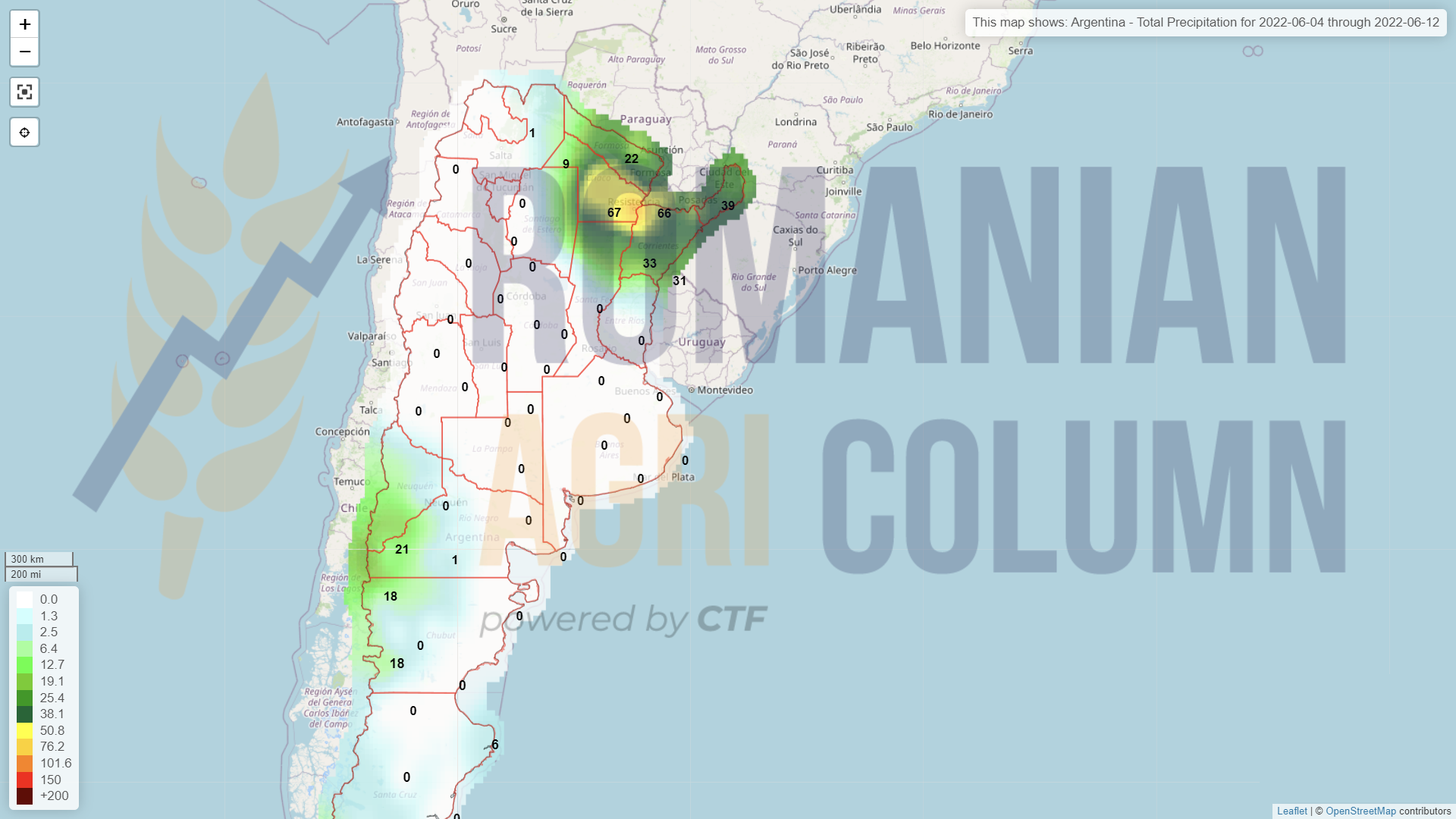

ARGENTINA, as we stated many times, is reducing the area of wheat to only 6.5 million hectares, but compared to the initial forecast of 19.5 million tons, it raises its forecasts by 1 million tons.

AUSTRALIA also raises its harvest forecast by 2 million tons, from 30 million to 32 million tons, which indicates a compensation, albeit partial, compared to last year’s huge harvest volume of 36 million tons.

CAUSES AND EFFECTS

Here we will dissect the whole wheat globally and start with the tendency of some Asian states to enter directly into the behavior of hand-to-mouth (i.e., to buy only what it consumes, not in stock piling, i.e., accumulation due to necessity generated and a harvest pressure that will naturally lower prices). Vietnam is an example of this and we see how they came out of a contract to buy Australian wheat through the wash-out procedure. This example indicates a breakthrough in which local processors can no longer generate sales in domestic markets and prefer to run their business at 50% of its potential, pending price easing.

In all this context, we bring to the fore the three factors that have declined and, if they come together at an end that will be recorded in 10 days from now, will further lower wheat prices globally:

- Mediation meeting under Turkish patronage. If they reach a partial agreement, a significant flow of goods will migrate to the market and we will naturally have a drop in prices. What we need to understand from this is that Turkey is beginning to consolidate and take a dominant position in the Black Sea trade. The Dardanelles and the Bosphorus are effectively the gates to the world from the basin, and Turkey can play this card very cleverly, becoming a factor of stabilization and regional predictability.

- June 10 USDA report. This will lead to changes in global crop volumes and could be the second factor in the deterioration of wheat prices.

- Federal Reserve, which will announce the new interest rate on June 14. All indications point to a 0.5% increase in monetary policy interest rates. At the moment, the USA has been experiencing the highest inflation level for 40 years, and Europe for 20 years.

If this happens and is doubled by a second correction in July, as appearances indicate, we will actually see commodity prices sharply falling, with corrections of 80-100 EUR/MT at least, for the simple reason that stock markets will be effectively devastated. All the wild pursuit of profit generated by the unconscious printing, so to speak, of money to support the effects of the pandemic will end. The guarantees required for the positions on the stock exchanges will no longer be able to be sustained and thus many of the speculative actors will be forced to leave.

The savagery of investment funds that aimed only at generating profit based on global food will be stopped. The world can no longer bear this level, it is simply meaningless. A ton of wheat looks the same if it costs EUR 180, and if it has a value of EUR 400, and the world must be fed, not plundered by financial reserves.

And yes, we say it and we support it, the Investment Funds have increased the price of raw materials (agricultural goods), energy and, implicitly, the associated costs on the chain to our plate. For what? For the crazy rush to make money from the money printed by the EDF and the Central Banks during the COVID-19 pandemic.

THE NEXT 10 DAYS WILL BE DECISIVE FOR THE PRICES OF THE GOODS. THE RECESSION IS COMING SOON AND THE FARMERS HAVE TO KEEP THE CAPITALIZATION OBTAINED FROM THE RECENT VERY HIGH PRICES. IT WILL BE USEFUL FOR FUTURE INVESTMENTS, WHICH WILL FURTHE BRING CAPITAL.

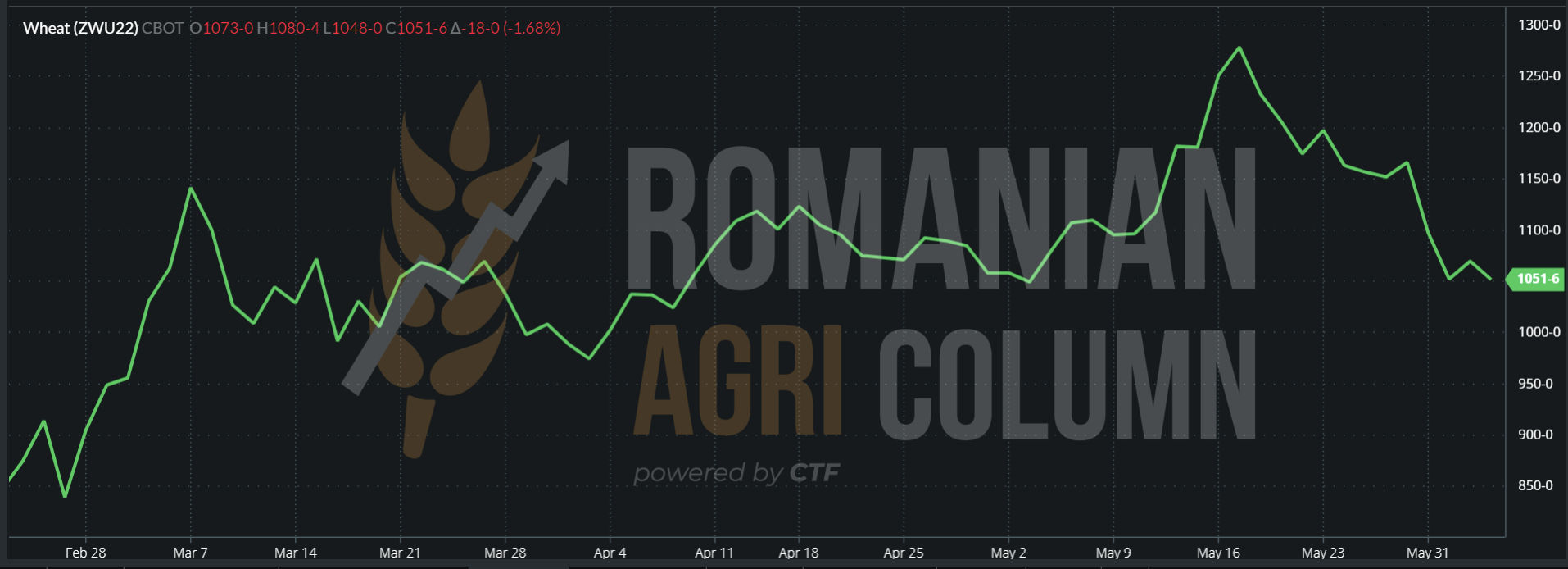

CBOT is in full agreement with what is happening now in the global market. We see successive declines in trading days. Funds feel the recession and liquidate positions daily.

CBOT ZWU22 SEP22 – 1,051 c/bu = 386.18 USD

CBOT WHEAT TREND GRAPHIC – ZWU22 SEP22

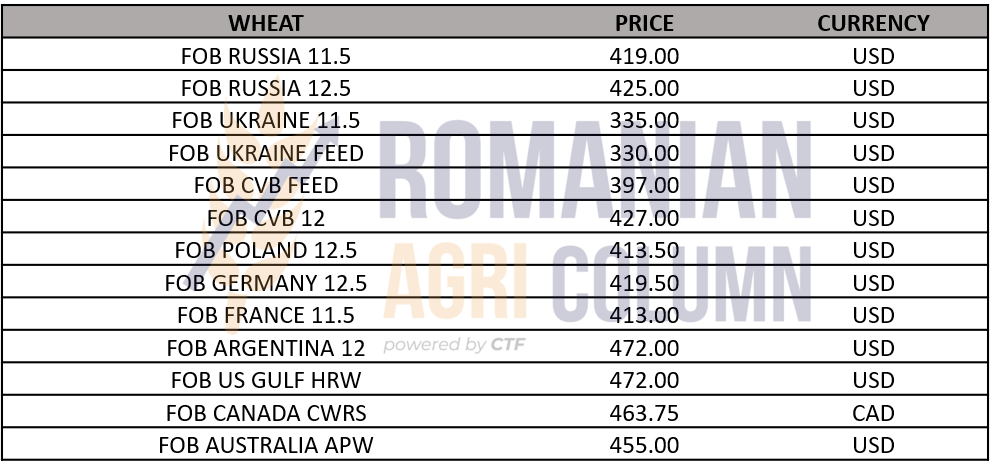

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

LOCAL STATUS

The price indications for feed barley have contracted, being equally affected by the regional and global factors set out above. Barley returned to the level of 342-345 EUR/MT in the CPT Constanța parity near the harvest. Because yes, there are only a few days until the combine harvesters enter the chains for the first cuts, as defined by harvesting the sides of the plot and determining the quality conditions, in this case, the Test Weight for feed barley.

The base is 62 kg/hl (TW Test Weight) and the minimum is set at 58 kg/hl with a 1:1 penalty, in the contractual average between the base and the minimum.

CAUSES AND EFFECTS

Feed barley is, in principle, logistically free. The availability of means of transport should not be a problem.

The quality condition could lead to changes in price behavior. But until the first cuts, we estimate that the Romanian feed barley meets the basic conditions, especially those of Test Weight (TW).

REGIONAL STATUS

FRANCE is experiencing a deterioration in the barley crop. The rains came too late, but from now on we will start harvesting, so we first wait for Romania to set the tone, and then we will follow the evolution of the French barley crop.

The price level of feed barley in Rouen with July delivery was set on Friday, June 3, at 342 EUR/MT, so it was granted 100% with the indication CPT Constanța.

CAUSES AND EFFECTS

Potential problems with feed barley will occur in the cascade, as for the other goods, if June 8 and 14 is confirmed what we announced in the wheat chapter. And so barley is no exception.

LOCAL STATUS

The prices of corn followed the same downward trajectory as that of wheat and we see indications of maximum 307 EUR/MT for the old corn crop and maximum 302-303 EUR/MT for the new crop in the CPT Constanța parity.

The shape of corn in Romania is satisfactory so far. But the level of the crop depends on the volume of rainfall over the next 20 days. What is seen at the moment is not good, but the weather forecasts, as we well know, may change.

CAUSES AND EFFECTS

The negative traction exerted by wheat is also reversed on maize, but for the time being, at a low level, due to the volatility created by the weather at national and regional level. If, however, the weather will count in the sense of precipitation and implicitly the harvest forecasts will be combined, we will be able to see depreciation.

Also, let’s not forget the Ukrainian flow of goods, which is offered at discounted prices at the Romanian border, as well as in the port of Constanța, despite the logistically terrible congestion, created in Sulina, Reni, Dornești and Halmeu. Ukrainian corn is currently trading at 240 EUR/MT in DAP Reni parity.

REGIONAL STATUS

THE EUROPEAN UNION remains at the same level as in the previous report. We have no changes in terms of volume forecasts, i.e., we remain at a potential of 67-68 million tons.

UKRAINE is about to close the corn sowing season and all data leads to a level of 22-23 million tons of corn as a harvest level. But we also have a residual crop from last season, of about 5 million tons, which would lead to a total level of 27 million tons.

RUSSIA will generate 14.5 million tons, with an estimated export of a maximum of 5 million tons, but in the general plan given to exports, Russia is not an important exponent.

CAUSES AND EFFECTS

Right now, we are seeing a migration of China towards Brazilian corn, as I said in the last issue. However, the demand remains constant in the port of Constanța, the main factor remaining the price indication which, even if decreased, generates liquidity in the sense of traded volumes. We are in June and the barns must be emptied to make way for new crops.

The global association with the predicted volumes of maize could imply a better traction of the price, but at the moment, on the European continent, we are only talking about forecasts that will be confirmed only with the help of precipitation.

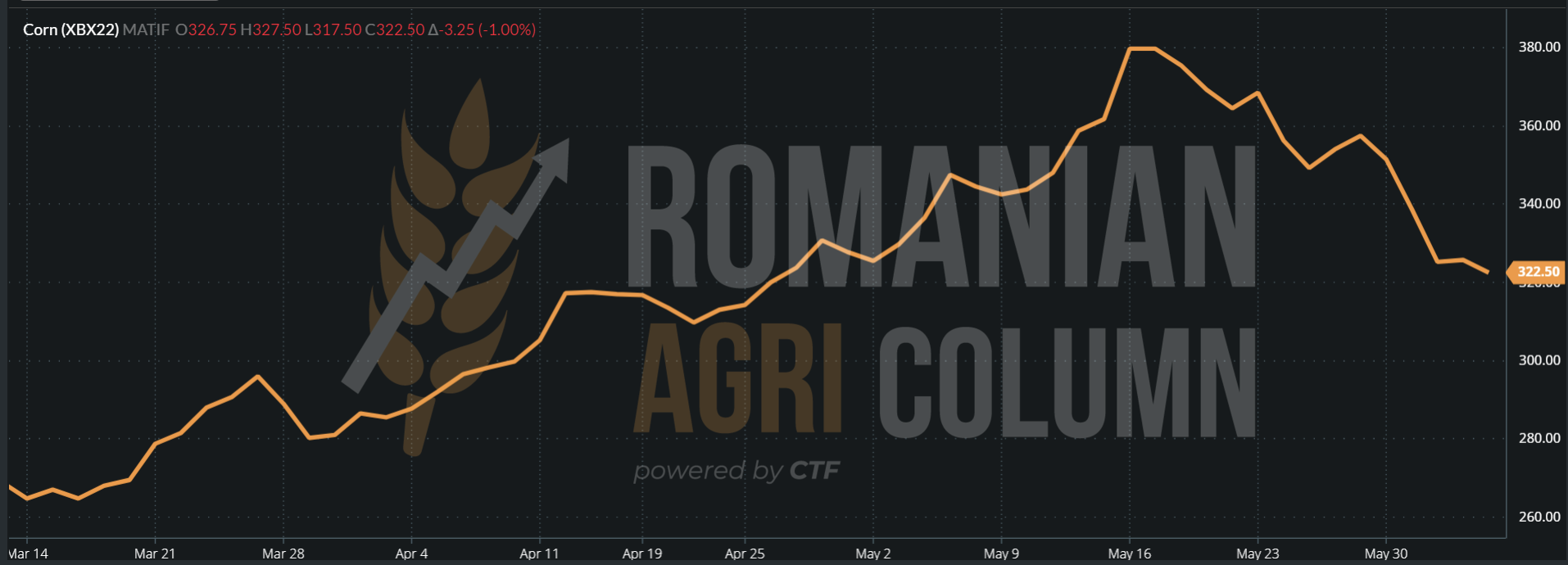

EURONEXT indicates a decrease to NOV22, i.e., the new crop. Let’s remember that we started from a peak of 379 EUR and today we have an indication of 322 EUR, so a 57 EUR negative difference.

EURONEXT CORN XBX22 NOV22 – 322.5 EUR (-3.25 EUR) at the close of June 3, 2022

EURONEXT CORN TREND GRAPHIC – XBX22 NOV22

GLOBAL STATUS

The US closes its corn sowing window around June 10, and estimates indicate delays only in North Dakota. All forecasts lead to 367 million tons of production, which has been receiving support lately, due to rainfall falling in the American Corn Belt.

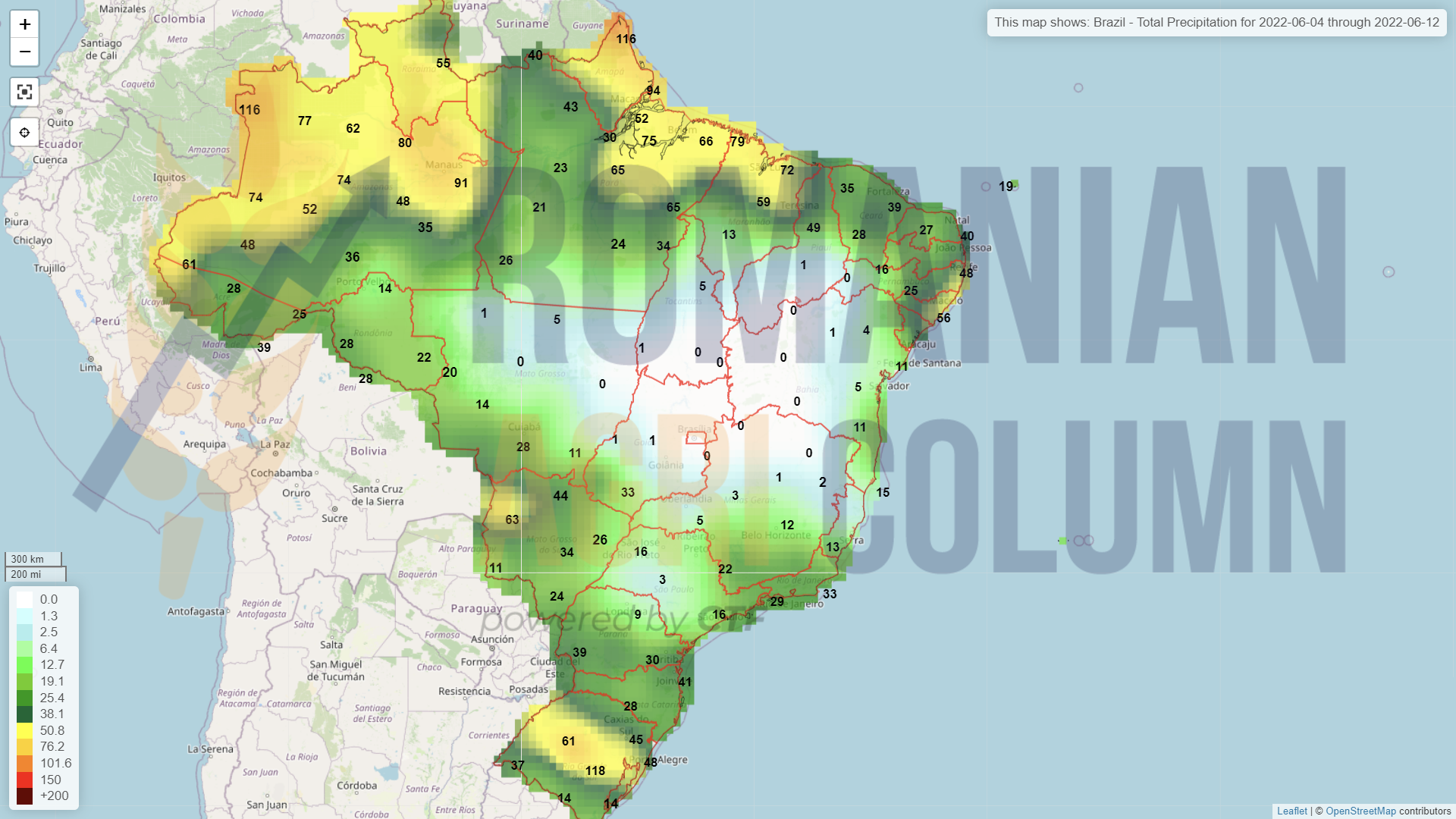

BRAZIL receives an upgrade to Safrinha due to better productivity outside the dry zone. StoneX raises the total forecast again to 116 million tons and thus the 5 million tons forecast to be lost are brought back into the complex of the total Brazilian harvest volumes. The forecast for the new Brazilian crop is set as a general forecast at a level of 126 million tons, 10 million higher than the aggregate one for this season, 2021-22.

ARGENTINA forecasts a level of 55 million tons for the next crop, 2 million tons more than in the 2021-2022 season, when it reached a volume of 53 million tons.

CAUSES AND EFFECTS

Brazil and Argentina partially offset the decline in US crop volume (from 383 million tons to 367 million tons). At the moment, the risk factors for the price of maize lie only in the FED’s actions, which will be on June 14, as an attempt to curb inflation. Investment funds are already leaving corn positions, a sign that they understand the coming recession and want to keep their profits, before the decline that will be generated by rising interest rates and, implicitly, by the rising financial cost of guarantees for stock market speculative stocks.

A UN-sponsored Russian-Ukrainian deal with a resolution would put a lot of pressure on the price of corn, due to the volumes not being exported, due to Russia’s occupation of the Black Sea. We are therefore waiting for June 8 for a possible confirmation, but also the subsequent June 10 (USDA report) and June 14 (EDF announcement).

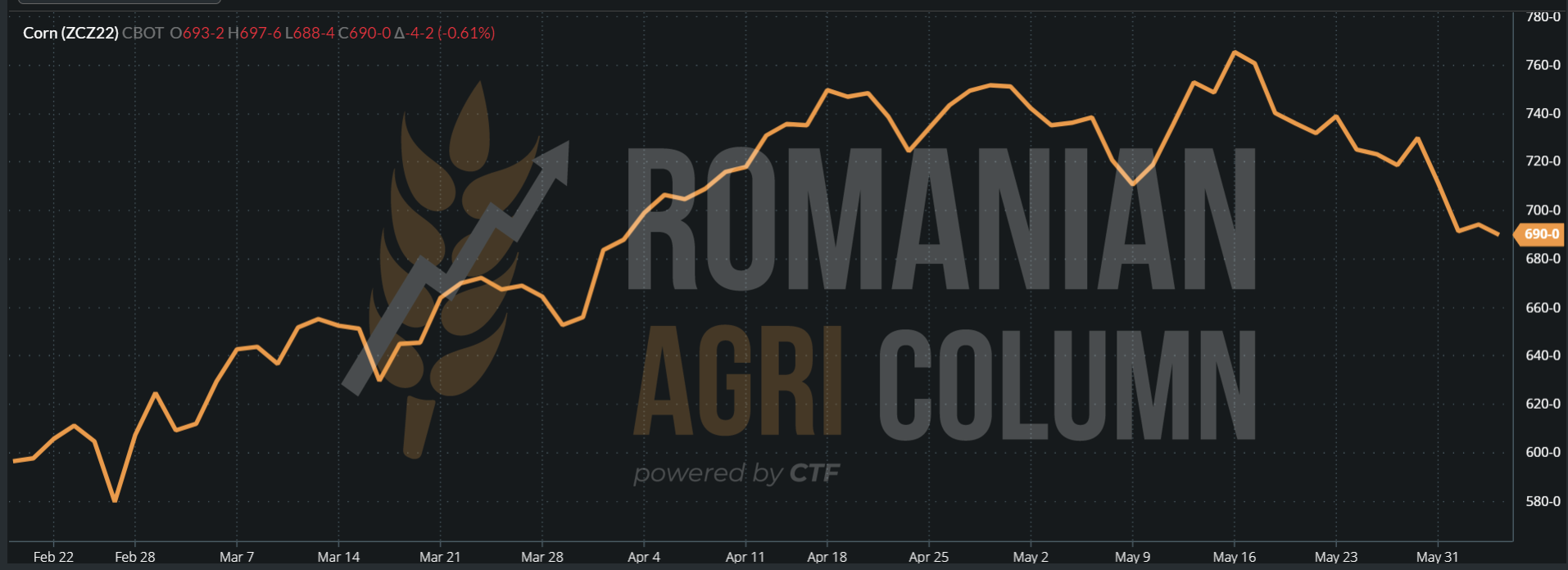

CBOT remains more temperate in the trading session of June 3, 2022, although below 700 c/bu. The trajectory of the last days has been obvious, from a peak of 760 c/bu (299.2 USD) to 690 c/bu (271.64 USD).

CBOT CORN – ZCZ22 DEC22 690 c/bu = 271.64 USD

CBOT CORN TREND GRAPHIC – ZCZ22 DEC22

CORN INDICATIONS IN MAIN ORIGINS

LOCAL STATUS

Rapeseed fell sharply on the last trading day of the week, June 3, 2022, after a few days in a row hovered around the 800 EUR AUG22 EURONEXT indication. The quotations of the port of Constanța and, implicitly, of the processors registered an increase of the negative premium up to -10 EUR/MT. Thus, all buyers positioned themselves at the level of AUG22 – 10 EUR/MT.

The Romanian rapeseed crop has gained more consistency and we see it raised by about 200,000 tons compared to the potential of 1.36 million tons. Today, the forecast is raised to 1.56 million tons. We are waiting for the harvest in order to align ourselves with this harvest forecast, keeping in mind the regions with extreme and moderate pedological drought in Romania.

CAUSES AND EFFECTS

The forecast increase relaxes processors and buyers for the export market to the same extent, on the simple principle that governs the market, that of supply and demand. Thus, the extra volumes begin to be traded with later delivery.

Following the decline in Germany’s announcement that it wants to replace rapeseed oil in the biodiesel manufacturing process with used cooking oil, the increase in the volume forecast makes the indications for rapeseed fall even further.

The beneficiaries are, of course, the buyers, who include in the price the cost of storage and of the qualitative and quantitative deductions related to the storage of the goods for a period of time.

But rapeseed remains a solid element in the structure of culture in Romania. The cost of setting up one hectare is largely covered by income, provided that a harvest of 3 tons/hectare is achieved.

REGIONAL STATUS

THE EUROPEAN UNION indicates, in the light of the latest analyzes, an increase in production from 17.6 million tons to 18.3 million tons, representing a substantial increase of 700,000 tons, of which we remind you that 200,000 tons are allocated to Romania.

UKRAINE will generate the same level of harvest of about 2.8 million tons, but it remains unknown if and how they will be able to bring this volume across borders.

RUSSIA will generate a harvest volume of about 2.65 million tons of rapeseed.

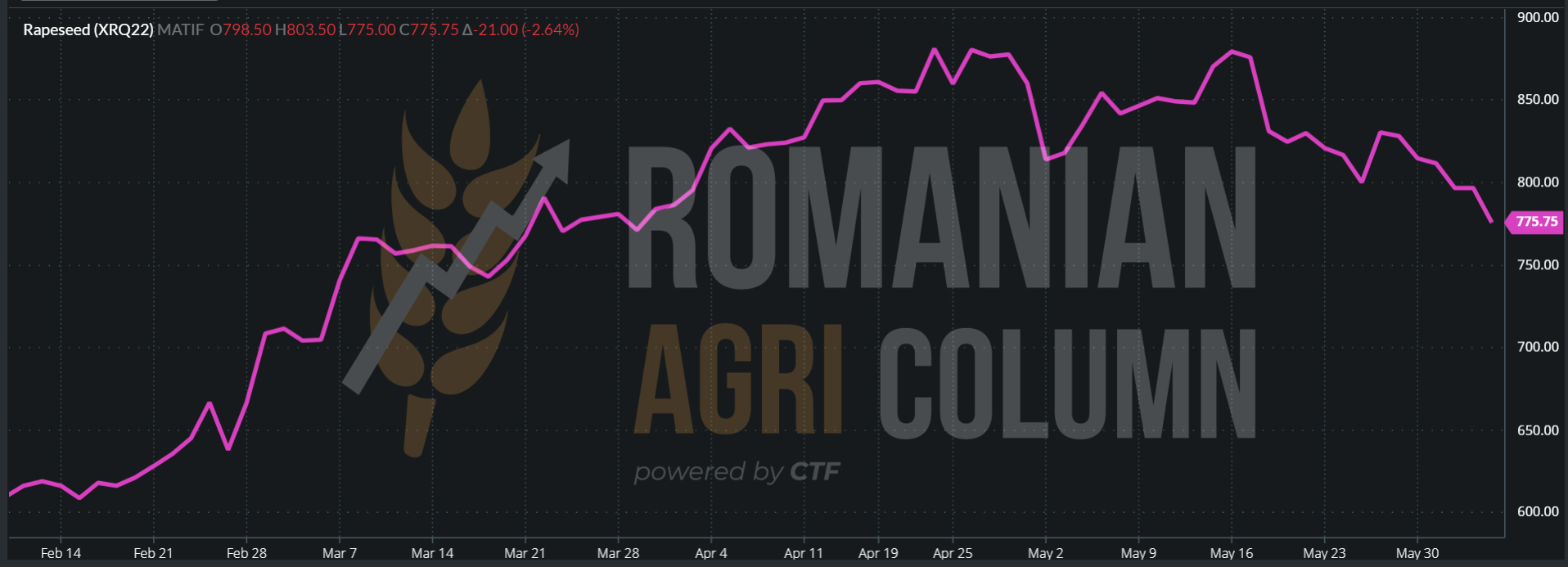

EURONEXT drastically corrects the price level of rapeseed. Last week, the indication AUG22 was at the level of 828 EUR, and on June 3, at the close of the trading session, the same indication AUG22 is set at 775.75EUR. The difference from one week to the next is 52.25 EUR, which already means a lot.

EURONEXT RAPESEED- XRQ22 AUG22 – EUR 775.75

EURONEXT RAPESEED TREND GRAPHIC – XRQ22 AUG22

GLOBAL STATUS

CANADA indicates a very healthy forecast of canola, rising by about 2 million tons, from 19.5 million tons to a potential close to 22 million tons. Humidity and precipitation did their job well.

AUSTRALIA will also generate a surplus of volume. From 4.85 million tons, it raises the forecast to 5 million tons.

ICE CANOLA EXTREMELY CORRECTED – RSN22 JUL22 – minus 33 CAD

CAUSES AND EFFECTS

The first cause of the sharp decline in rapeseed indications is due to the increased volume forecast in the European Union. This was then doubled by the Canadian and Australian forecasts. So on the line we have much larger volumes of rapeseed available and sellers are in a hurry to offer rapeseed to processors in the European Union, even with late delivery, just to secure prices and volumes.

The second cause of the rapid decline in rapeseed is OPEC’s announcement that in July they will supplement production by 648,000 barrels per day to make up for the lack of economic oil on the market subject to economic sanctions. Only here we have an amendment. Russia is making its way, using Indian tankerede (shipping) and processing crude oil in Indian and Chinese refineries. African countries are demanding a supply of grain and oil products from Russia in unison.

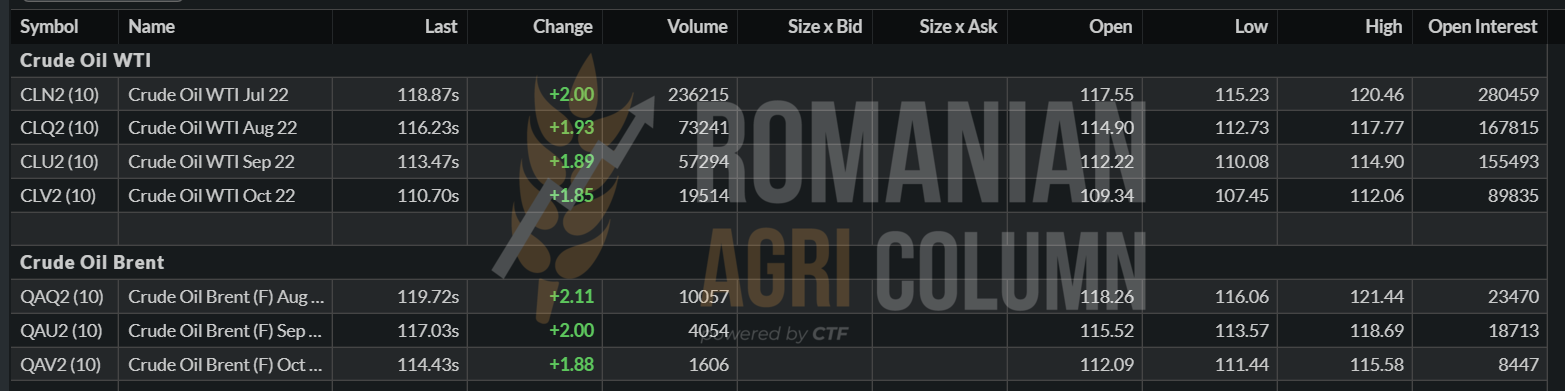

The third cause will naturally stem from the FED announcement, which is already making its mark. Funds are liquidating positions in Euronext, leading to a sharp drop on Friday, June 3rd. Fear of a recession has led to a downturn in funds, as oil prices in Brent have risen from $ 114 a barrel to $ 119 a barrel, despite OPEC’s announcement.

LOCAL STATUS

Price indications vary greatly from one buyer to another. We have a range of between 680, 690 and 700 USD/MT for the new crop, depending on the logistical factor. The differences in price are generated by the proximity of the processing units to the port of Constanța and to the farmers in the areas of origin. Naturally, the port of Constanța has the highest indication at the moment, namely 700 USD/MT.

The Romanian sunflower crop looks very promising. The rainfall in the last 8-10 days has generated a uniform development, so we are positive so far on the potential of 3.65-3.7 million tons.

CAUSES AND EFFECTS

The rich crop level can lead to a price degradation of up to around 650 USD/MT. The proximity and lack of storage space will make it difficult for farmers to sell at harvest. Logistics will put a heavy pressure on the price of goods and will also be, due to the lack of availability as well as the high cost, a factor in decreasing the income from the sale of production.

The pressure of Ukrainian volumes is felt in Romania. In May, about 375,000 tons of old crop sunflower seeds were transited to the EU. Ukrainian goods are offered with a discount of at least 30 USD/MT, compared to the level of 710 USD/MT related to the old crop, the port of Constanța.

REGIONAL + GLOBAL STATUS

THE EUROPEAN UNION raises the volume to 10.9 million tons of sunflower seeds. The state of vegetation in the Union is very promising at the moment and we are seeing an increase in crop yields.

UKRAINE is at the end of the sowing period and we note, according to the forecast, a level of 9.5 million tons, as was, moreover, predicted and mentioned.

RUSSIA raises the level of export tax on crude oil to 520 USD/MT. Apparently, Russian exports would be penalized, but we will see the causes and effects of the explanation.

CAUSES AND EFFECTS

The European Union has very good harvesting potential, but it needs to find a way to extract crude oil or sunflower seeds from Ukraine, bearing in mind that 200,000 tons of crude oil are needed every month as an import for consumption in the EU.

Russia has concluded trade agreements with India to supply crude oil with sunflower oil and it is very clear what oil it is thinking about. As I said a long time ago, Russia will actually take the Ukrainian production and sell it in India and other destinations.

Despite the very good production forecast in the Union, let’s not ignore that globally it will be a production with 6 million tons less. This difference comes from Ukraine.

Malaysia is restricting the access of Indonesian workers to local palm plantations for bureaucratic reasons (non-compliant work visas) and we expect a disruptive trend in terms of prices, which will spread to the VEGOIL complex. The turmoil could end in the 3rd or 4th quarter of the current year, but until then events may occur.

Sunflower seeds will also be shocked by FED decisions and the potential agreement to create the Odessa export corridor. It is not long and we will see and feel the propagated effect.

The dry weather could be a supporting factor, but this is difficult to predict, especially during the summer, June-August 2022.

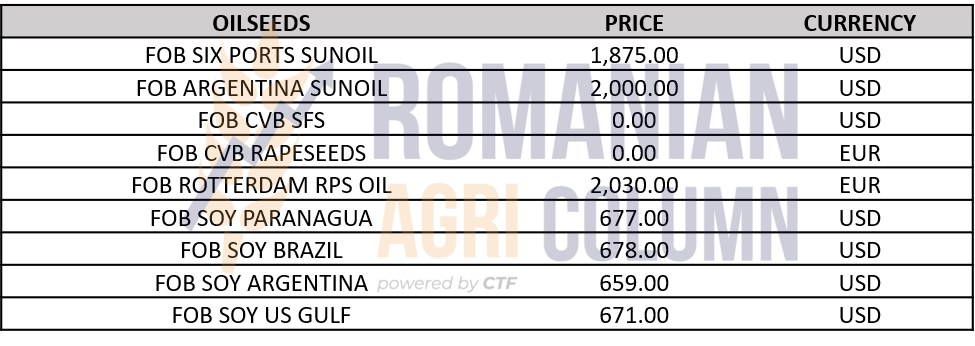

CSFO AND OILSEEDS INDICATIONS IN MAIN ORIGINS

LOCAL STATUS

The first price indications for the soybean crop of 2022 amount to 640 USD/MT DAP Processor. This is a first milestone, and certainly other buyers will agree and point to the new crop.

REGIONAL + GLOBAL STATUS

Future crop forecasts in the world are extremely generous compared to last season:

- US will generate 127 million tons of soybeans, 7 million tons more than last season, due to the increase in the area allocated for soybeans, to the detriment of corn.

- BRAZIL will generate a level of 149 million tons, increasing by 24 million tons compared to the last crop. And here we have an extremely generous forecast.

- ARGENTINA will deliver, according to forecasts, a volume of 51 million tons, increasing by 9 million tons compared to the previous season.

- PARAGUAY will return to 10 million tons after the disaster, when it recorded a harvest level of only 4.2 million tons, due to drought.

CAUSES AND EFFECTS

The price trajectory of soybeans will be impacted by volume. The supply will balance the demand and thus, the price of the new crop will decrease considerably. All the above mentioned areas of origin are in positive volume forecasts and the price difference can already be seen in the CBOT quotations.

Subsequently, the FED factor is seen closely, which aims to reduce inflation and therefore drastic corrections could follow.

The weather could be the only compensator, but La Nina will disappear by the end of 2022, so there is not much chance in this regard.

Cumulatively, the volumes and the expected action of the FED indicate a downward trajectory of soybean prices.

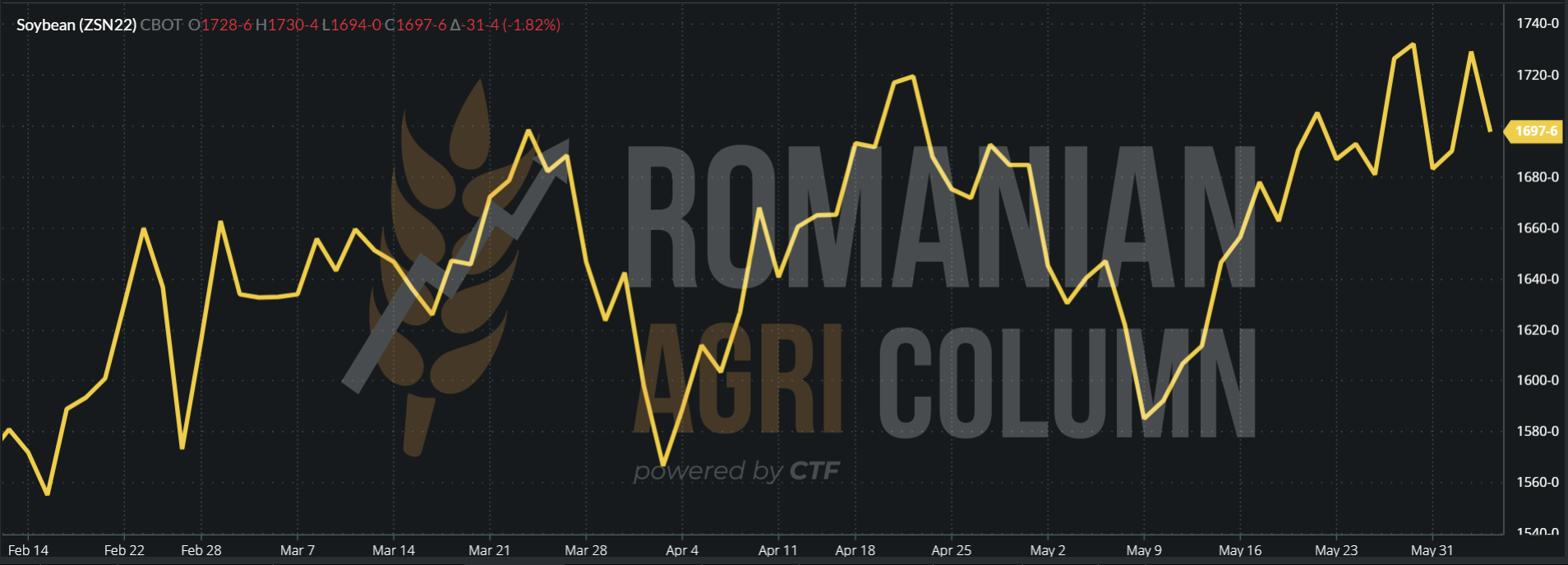

CBOT shows us how the funds are coming out of positions en masse. The world needs cheap food and their movements show us the imminence of the recession.

Comparison between JUL22 and NOV22: -62 USD

CBOT SOYBEAN TREND GRAPHIC

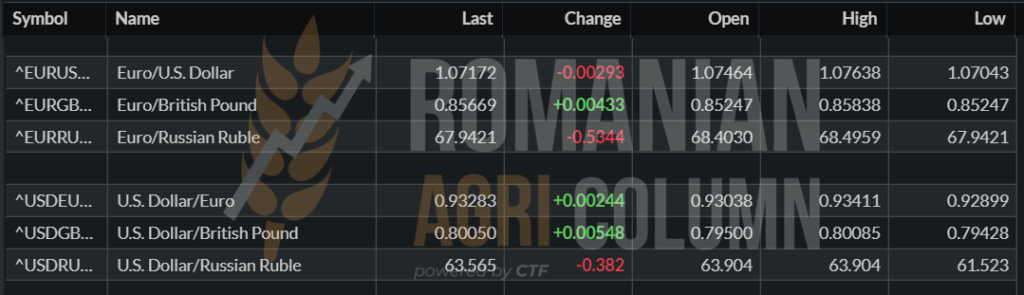

USD weakens against EUR; RUB is strengthening against the USD.

BRENT closes at 119.72 USD/barrel.

4-12 June 2022

Romania

Europe

Ukraine

Russia

Canada

USA

Brazil

Argentina

China

Australia