This week’s market report provides information on:

LOCALLY

The local wheat market is static. The effect of the congestion of the port of Constanța and the need to ship the raw materials generate a lack of demand among buyers. There are also many sellers on this flow, which means that things do not have a growing dynamic in the case of price. We therefore record price levels of 340-345 EUR/MT in the CPT Constanța parity for milling wheat. For feed wheat, the indications are reduced by 20 EUR/MT, which is an extremely large gap.

Looking at the objective, the level of 340-345 EUR/MT is one that covers the investment from 2021, referring strictly to the financial effort of the agricultural cycle per hectare of wheat in Romanian farms. In fact, this level was also given by us as a price base before the beginning of the conflict. The difference from 260 EUR/MT before the problems in the Black Sea basin, to 345 EUR/MT today’s price level in the same parity, represents an increase of about 31.5%.

As regards the price levels offered for the new wheat crop, the levels of 310 EUR/MT for wheat with bakery specifications and 300 EUR/MT for feed wheat have been exceeded.

The European Commissioner for Agriculture has announced some measures in the context of the spectrum of supply shortages caused by the problems in the Black Sea basin. These are realistic measures, viewed through the filter of objectivity. These are generated to support farmers:

- EUR 500 million from the EU budget, of which Romania receives EUR 25 million, with the obligation to supplement the amount with 200% of the state budget, i.e., a total of EUR 75 million.

- The use of areas taken out of production for the cultivation of protein plants.

- Continuation of state aid, as in the pandemic.

The European Parliament also voted in favor of the EU action plan on food security in the wake of the war in Ukraine, which we welcome as an extremely beneficial initiative in the current and future context:

- Agricultural area will not be reduced by 10%, as required by the Green Deal.

- Flexibility for Member States in developing the NSPs (National Strategic Plans), so as to take into account the new reality.

- Reanalyzing the objectives of the Green Deal, based on impact studies.

- Impact assessments for certain regulations, including the Pesticides Directive.

- Flexibility in crops in areas of ecological interest, including the use of plant protection substances.

- Simplifying procedures for farmers’ access to renewable energy.

- Once again, the extreme demand to reduce the number of farm animals in order to switch to a plant-based diet was rejected.

REGIONALLY

Ukraine

Wheat was totally restricted to exports. The country needs food reserves, and the current context makes the need to keep wheat in the country, in the perspective of a lasting war. Regarding the new wheat crop in Ukraine, the first estimates lead to a maximum of 10 million tons that will be exported. But at the moment, these estimates are based on current premises. As things move forward, new estimates will make their way. Everything is extremely variable and volatile.

In this context, the Minister of Agriculture of Ukraine, Roman Leshchenko, resigned and was replaced by Mykola Solskyi.

With regard to Ukraine, we must be extremely realistic and generate a normal and correct analysis in the light of the information we have, as follows:

- Crop estimates will fall by about 55% due to the war in its territory.

- The war has turned into one of attrition and our estimates indicate that it will take 7-9 months until it is finally stopped. News reports of Russian troops intending to destroy all Ukrainian ports on the Black Sea and the Sea of Azov in 2-3 weeks.

- Once peace comes, we will have at least 3-5 years to rebuild, which will come at a huge cost and human effort.

- In this perspective, we will see how absolutely all foreign investment in Ukraine (and we refer to Western capital) will be completely stopped due to uncertainty. Thus, an important agricultural area of the world, an area that annually generates a level of 25 million tons of wheat exports, 33 million tons of corn exports, 7 million tons of exports of crude sunflower oil, disappears from the global radar of origins. The causes are the above: lack of predictability, lack of facilities as they are destroyed, lack of foreign capital to be transferred and time allotted for the reconstruction of the country.

Russia

The Russian Federation is creating a humanitarian corridor, which is a safe lane for ships in the assembly area, located 20 miles southeast of the port of Ilyichevsk. The corridor is open daily from 08:00 until 19:00. (Moscow time), starting March 25, 2022. The length of the humanitarian corridor is 80 nautical miles southwest, and the width of the strip is 3 miles.

We remind you that since the beginning of Russia’s military aggression, at least 5 merchant ships have been damaged, one of which sank. At least two sailors have died, although details are still being confirmed. Two or three ships were captured at sea and escorted to Crimean ports.

“On March 25, at 10 o’clock in the morning, no ship in Ukrainian ports took advantage of Russia’s provocative invitation,” added A. Klymenko, editor-in-chief of the Black Sea News.

Russia has built its wheat export network. We see export commitments through jointly owned companies to Egypt. We note the huge flow of goods that will move to China, we see the trade on the Caspian Sea to Iran, as well as the supply that they will make to Syria.

With Kazakhstan and Belarus under its control, Russia will have enormous control over wheat flows and will generate a supply chain to the Middle East, China and Afghanistan through the corridors it will create with China.

In addition, we estimate the creation of a power pole that will be positioned in the context of the Middle East, Southeast Asia (India, Pakistan, Bangladesh, Afghanistan,) composed of Russia and China. They will effectively control this whole area and potentially generate sales to North Africa as well, as the European Union, including Romania, will not have enough production to cover demand.

As for the current wheat price trend, the demand factor remains unchanged, but it will not be higher. Destinations are looking for other sources of supply and are carefully balancing their own reserves, waiting for a lower price level of the new crop. Thus, the demand for the old crop will be in place, but we will no longer witness explosions in terms of prices. April, May and June also separate us from the new crop.

But social problems will not be long in coming to poor countries, especially in Africa and the areas mentioned above, so that a supplement of Russian origin aggregated by Chinese technological support would further fracture the world, as Africa is a huge source of untapped wealth and knowingly kept in poverty. Culture generates progress, and there, underdevelopment is at its peak, starting with the education system, which is essential for any nation.

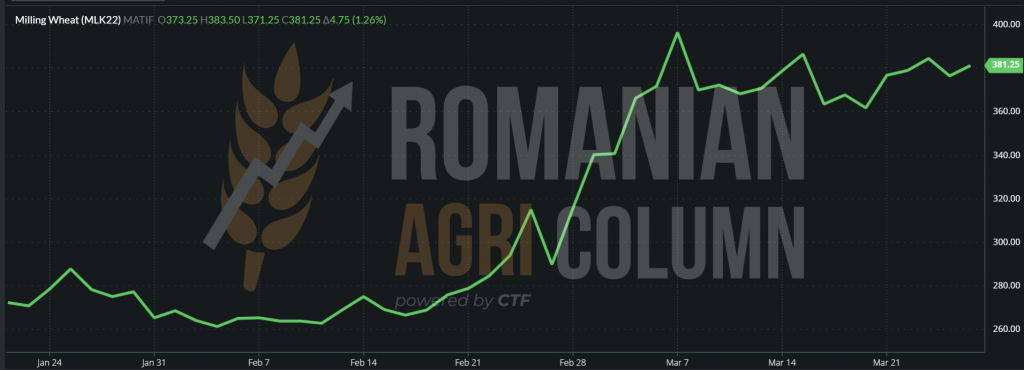

EURONEXT generates decreases and increases caused by political factors and the games played by the investment funds, which enter and exit, generating these sinusoidal curves. Notice how the crop inverse changes, namely MLK22 MAY22 vs. MLU22 SEP22 (33.5 EUR).

EURONEXT MLK22 MAY22 – 381.25 EUR (+4.75 EUR) at the close of March 25, 2022

WHEAT – EURONEXT TREND GRAPHIC – MLK22 MAY22: UP & DOWN on a range from 360 to 380 EUR

TENDERS

In the March 23 tender, TMO Turkey bought 455,000 tons of wheat with delivery on April 1-30. EXW prices ranged from 419.9 USD/MT Bandirma (-0.1 USD/MTn compared to March 2 purchase) to 447.7 USD/MT Izmir (-0.1 USD/MT compared to March 2 purchase) for wheat 12.5% and from 423 USD/MT Bandirma to 427.8 USD/MT Samsun for wheat 13.5%. C&F prices ranged from 429.8 USD/MT Samsun (-15 USD/MT compared to the March 17 purchase) to 445 USD/MT Iskenderun (-4 USD/MT compared to the March 17 purchase) for wheat 12.5 % and 445 USD/MT Iskenderun for wheat 11.5%.

GLOBALLY

Farmers in Canada could face another drought this year. Dry conditions have reduced last year’s Canadian crop, and wheat crops in the United States and China have major problems.

By 2020, before the drought, Canada’s wheat exports accounted for 13% of wheat traded globally, according to the US Department of Agriculture. Much of Canada’s prairies are still dry, with southern Alberta and central Saskatchewan in “extreme drought” since February 28th.

The US is not doing better either, in the context of the lack of water supply in the soil. 41% of American winter wheat is currently in drought-affected areas. The rains are forecast to wet the US, but we still do not believe that they are enough to restore the water supply and revive the American winter wheat. So, as I said in the past, there will be volume issues in the United States.

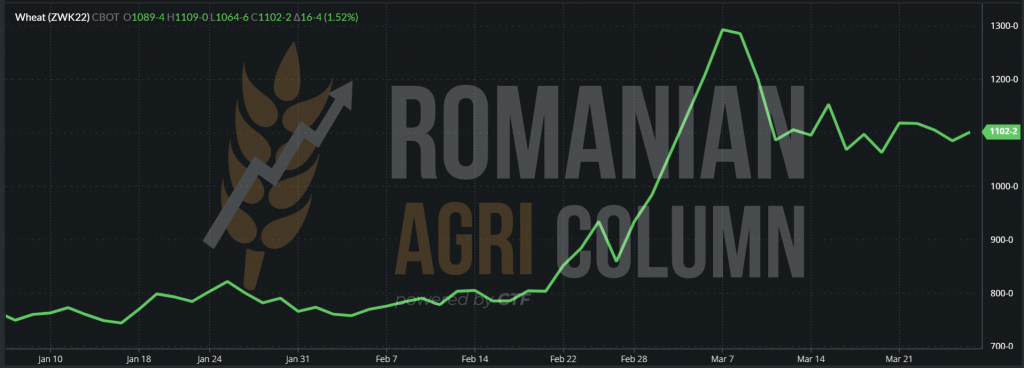

We go into the stock market and notice the same volatility generated by political factors and exploited by investment funds.

CBOT ZWK22 MAY22 – 1,102 c/bu (+16 c/bu) | Crop inverse ZWU22 SEP22 – 1,069 c/bu (-33 c/bu = -12 USD/MT). Compared to EURONEXT, here we have a much lower level of crop inverse.

WHEAT – CBOT TREND GRAPHIC – ZWK22 MAY22

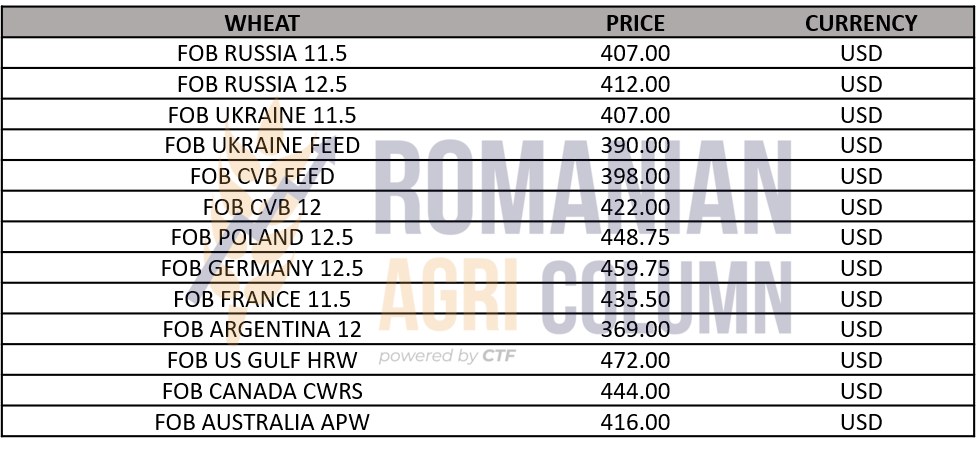

WHEAT PRICE INDICATIONS IN VARIOUS ORIGINS

ANALYSIS

- The global wheat market is reconfiguring around new data.

- Russia will generate a magnitude of power in the Middle East and Southeast Asia.

- The European Union will have its own food safety on the radar, as well as volumes for destinations in North Africa, the Middle East.

- Ukraine will generate a volume of only 10 million tons for export in the 2022 crop. But it is also under the sign of uncertainty due to the war taking place on its territory.

- As a coherent explanation, any flow of raw material will eventually find its way. Someone needs it and someone will pay. It is extremely simple, whether we are talking about Russian wheat or oil. Under what conditions? This is another chapter, but the essence remains – someone will buy what someone else will sell.

Feed barley is no longer listed in the CPT Constanța parity. Instead, there are quotations for the new feed barley crop and the primary indications are 280 EUR/MT. The barley has almost disappeared from the radar of the port of Constanța. We also note Jordan, which canceled a barley tender.

LOCALLY

The price indications for maize are in line with the trend for wheat. Due to the congestion in the port of Constanța, the indications go down to the level of 320 EUR/MT. Only one exporter indicates 337 EUR/MT at the moment, but only for a short period of time, of 7 days, a sign that they have a spot need. But farmers sell volumes at this level and this explains the concomitant deliveries with the congestion in the port of Constanța. It’s a busy season, indeed, but the problems are systemic and come to the surface everywhere.

In vain does the port have the capacity to take over the goods, if the logistics infrastructure suffers at national level. And we refer to the railway, where the problems are extremely painful. We are talking about an average freight train speed of 17 km/h, which shows us the seriousness of the problems. Apart from this problem, there is also the triage in the port of Constanța, which makes it extremely difficult to facilitate entry to the unloading. Romanian terminals have an operating capacity of about 60,000 tons/24 hour. In other words, a s panamax can be charged in 24 hours.

In vain, however, if the goods cannot reach the port or cannot penetrate the congestion in the port triage. Romania has an obvious problem that has no solution in the coming years. All successive governments have not carried out any macro-plans or modernization of the rail freight structure. Subsequently and cumulatively, there is also the extremely fragile road transport network. With a highway ending in Bucharest, with a Bucharest ring road that has been frozen for decades in the same state of disrepair and with only one lane on the direction of travel, the problems are already extremely serious.

One question we ask in the form of rhetoric is: what will we do when Romania’s production reaches the level of 48-50 million tons per year? How do we move the goods, the surplus, for export? Sorry, but teleportation hasn’t been invented yet.

REGIONALLY

Ukrainian corn is trying to make its way to the port of Constanta and to the Polish border, but things are not easy at all. We remind you that only a number of 150 wagons are available for Romania and they total only 10,000 tons. A very weak flow we could say. But all hopes are tied to Giurgiulesti, where barges can be loaded that can sail on the Danube to Constanța. There they can be loaded on ships in FAS condition (Free Alongside Vessel) and thus can solve the logistical problem of Ukrainian corn. More than 1 million tonnes of export licenses have been issued for Ukrainian maize. They remain to be executed now. It’s not easy, it’s not easy in any way. First of all, we are talking about the availability of barges and then the time they will spend in Giurgiulesti for loading. Not to mention the parking in the harbor of Constanța port, in the pool, until unloading.

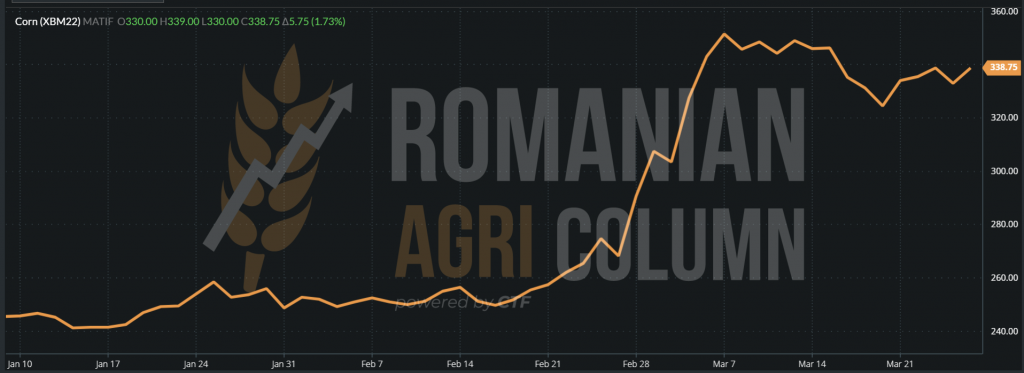

Stock markets are starting to rise, with the effect of funds movements generated by political factors being the main ingredients. The prospect of a long war, associated with the exit and re-entry of funds, will increase the indications of corn to the level of 338 EUR/MT. But we see the new crop with an inverse level of 42.25 EUR/MT. Under normal circumstances, the new corn crop will be pulled up by the wheat, so that this correction will be visible, but in time. EURONEXT XBM22 JUN22 – 338 EUR | XBX22 NOV22 – EUR 295.75

CORN – EURONEXT TREND GRAPHIC – XBM22 JUN22

The demand in the Black Sea basin is holding up very well. The logistical difference between the South American origins and the basin means that the demand is still focused on the origin of the Black Sea. We do not expect future price declines at this source. Spain has to import corn and China is still the strongest candidate when it comes to procurement.

The fervor in the stock piling that China displays should be noticed. They buy from anywhere in the world and stock up. First of all, they want to cover the degradation of the wheat crop, but also to necessarily cover the soybeans. Corn, in turn, is the focus of China. The 26 million ton barrier will certainly be crossed, looking at their pace of acquisition.

GLOBALLY

Brazil estimates a level of 94-95 million tons of Safrinha, the second corn crop, which, combined with a weaker first crop of 5-6 million tons, would lead to 114-115 million tons of total crop. So a good harvest in the end. However, there is still time until the second crop, so the price is still high.

Argentina has started harvesting corn and there is still no substantial deterioration compared to the levels we knew. The USDA forecast is 53 million tons, and according to local analysts, it is 2 million tons lower.

As the Argentine crop generates exports, we will see price pressure. However, the logistics are in favor of the Black Sea basin and we are talking here only about Romania and the weak flows from Ukraine.

In the United States, corn sales have been disappointing in the past week. They failed to come close to the initial estimates and thus the American corn records a non-competitive week.

CBOT, in turn, marks these correlations in the physical market with very slow oscillations and much more frequent outflows and inflows of funds. The oscillations we record on the CBOT indicate the magnitude of the corn volumes and, implicitly, that the global supply stress does not exist. The missing levels in Ukraine can be offset by the two Americas, North and South.

In fact, the group of the two continents together generates 550 million tons. It is an impressive figure, which indicates a health of origins and a predictability preserved over time.

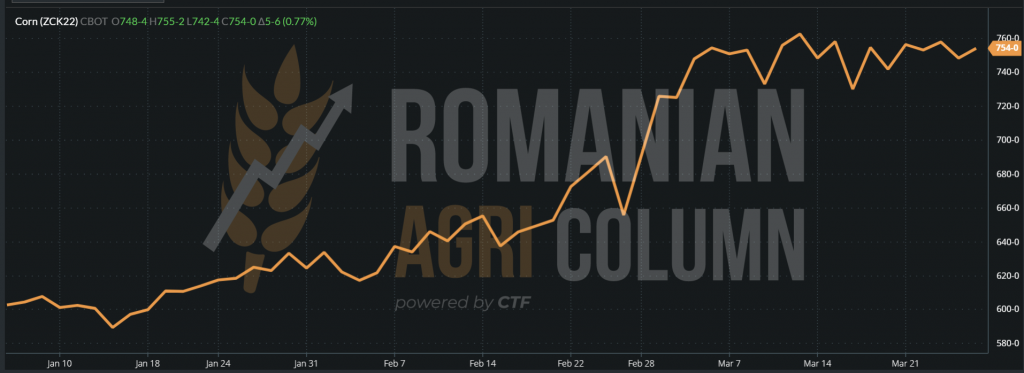

CBOT ZCK22 MAY22 – 754 c/bu (+5 c/bu)

CORN – CBOT TREND GRAPHIC – ZCK22 MAY22

CORN INDICATIONS IN MAIN ORIGINS

ANALYSIS

- The price in the Black Sea basin is corrected due to the volumes to be delivered from the port of Constanța.

- Ukrainian corn is slowly making its way to Constanța.

- South America is starting to ramp up sales. Argentina has started harvesting, and Brazil has a good corn crop (Safrinha).

- US corn sales were not in line with forecasts, leading to price corrections.

- However, China buys goods in an attempt to store them. What effect will it have on the market in the next period? Normally, it should support the price of corn.

LOCALLY

The status is unchanged these days, with a focus of farmers on the maintenance of winter crops. The old rapeseed crop no longer exists, but, as parameters, the quotation is MAY22 minus 50 EUR/MT. The new crop is maintained at the same levels AUG22 minus 10-15 EUR/MT delivery CPT Constanța or DAP Processors.

We already see problems in execution at the level of contracts signed very early, due to the possibility of default. The initial price was lower and thus we could face an intention of non-execution of the contracts at the time of harvest.

We want to clarify the fact that it is essential to execute in their entirety the signed and assumed contracts. It is a legal norm and we encourage the execution of the contract. Over time, we have approved the signing of only 1 ton per hectare, so that the potential can be traced along the entire route of rapeseed vegetation, from January to summer harvest.

REGIONALLY

The same status as for the European rapeseed harvest, so no news means good news.

EURONEXT continues to fluctuate with the price of oil (120 USD/barrel Brent), as follows:

EURONEXT XRQ22 AUG22 – 779.25 EUR at the close of March 25, 2022

RAPESEED – EURONEXT TREND GRAPHIC – XRQ22 AUG22

ANALYSIS

Rapeseed should be tracked by the following factors that may influence it:

- The price of oil

- Volumes in Ukraine

- Canadian crop

- Australian crop

The local indications of sunflower seeds remain at the same levels as last week – 880-900 USD/MT, but very small lots are being traded at the moment. It is an area of calm generated by the internal reserves of sunflower oil, which have brought calm to prices. Inflation remains, however, and expensive goods will be seen in the next quarter of processor sales.

Ukraine is trying to resume oil exports, in this case honoring contracts. It is very difficult, however, from a logistical point of view. Russia has taken Ukraine’s place in India and exports crude sunflower oil to this destination. However, we are confident that Ukraine will also find an easier way to export crude oil in the end, especially in view of the fact that it is not banned for export. However, spring sowing of sunflower seeds in Ukraine will decrease by about 44-48% of the initial potential. Due to this, we expect that of the 7 million hectares sown last year with sunflower seeds, Ukraine will sow only 4 million hectares.

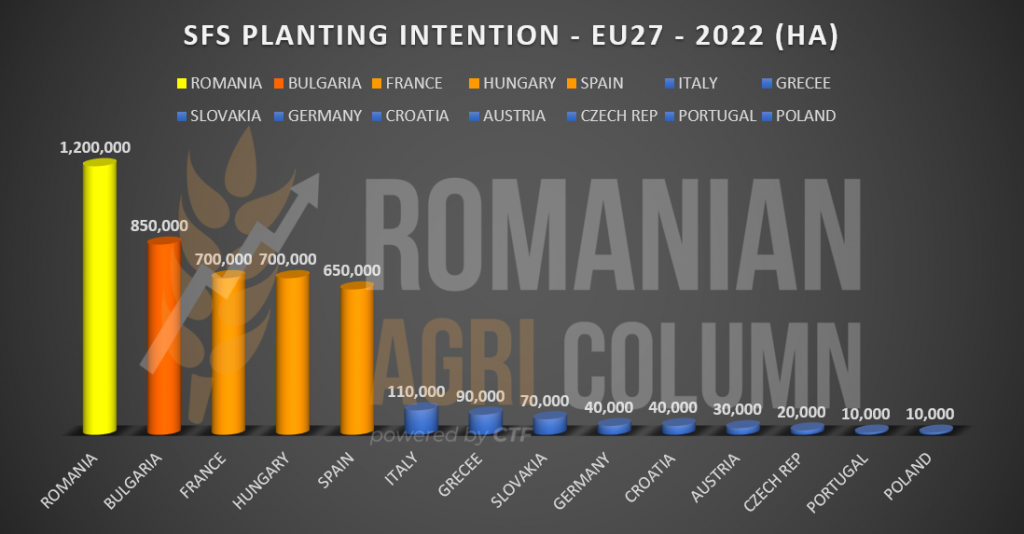

Let us now review the European sowing forecast for 2022-2023, not before mentioning that Romania could reach a level of 1.3 million hectares, compared to the 1.2 million forecasted at this time.

OILSEEDS PRICE INDICATIONS IN VARIOUS ORIGINS

ANALYSIS

- Stocks are not enough, and after May 10-15, 2022, we will see a further increase in sunflower seed prices.

- June 2022 will be the final month for all processors that will enter the process of reassembly, i.e., overhaul for the next season.

- In mid-May, the seed road will stop this season.

- The upcoming season is already announced to be extremely competitive.

LOCALLY

We do not see transactions and, implicitly, certain volumes as liquidity in the market. We believe that there are still local goods in the order of 2,000-5,000 tons.

GLOBALLY

The price of soybeans has risen, a sign that demand for American soybeans is strong, despite the fresh harvest in South America. Private exporters have reported the sale of 132,000 soybeans to China for delivery in 2021-2022.

Argentina’s central area is at risk of severe storms and heavy rainfall, which could lead to flooding. We remind you that at the moment, the Argentine soybean harvest is credited with 42 million tons, down from 46 million tons the initial forecast.

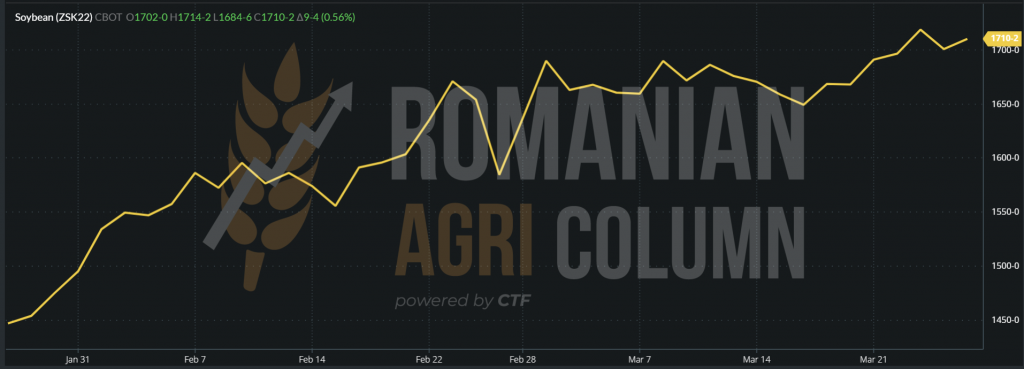

CBOT reflects the success of US soybean sales. CBOT ZSK22 MAY22 – 1,710 c/bu (+9 c/bu)

SOYBEANS – CBOT TREND GRAPHIC – ZSK22 MAY22

ANALYSIS

- China remains the strongest buyer of soybeans.

- With a deeply degraded crop, the need for protein will push it to exceed 100 million tons of soybeans this season.

- The dice are also thrown in Argentina. 41-42 million tons will be soybean grain production vs. 46 million tons initial forecast.

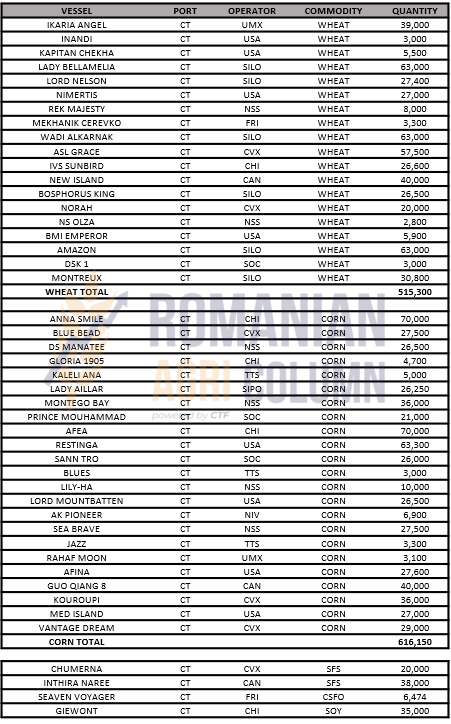

WHEAT: 513,300 TONS | PORUMB: 616,150 TONS

WTI – 111.76 USD | BRENT – 120.65 USD

March 26 – April 9, 2022

Romania

Europe

Ukraine

USA

Brazil

Argentina

China

Australia