This week’s market report provides information on:

LOCAL STATUS

The indications of the Port of Constanța hover around the values of 278-280 EUR/MT.

The sales level of the new crop remains granted at the level of 250 EUR/MT for deliveries of new wheat crop in the CPT Constanța parity.

CAUSES AND EFFECTS

We remain in the same outlook as last week, with expectations from farmers and limited export sales. But the premises remain the same. Any regional imbalance would generate growth, but time is running out and the times we don’t want are clearly approaching. Potential supply chain bottlenecks generated by increased ground clampdowns on Ukrainian territory would drive growth in the physical market.

For the new crop, there is also a term and a time of decision. Romanian farmers must be very attentive to the signals and generate cargo flow in the next 3 weeks. Judging by today’s state of crops in Romania, we have no reason to worry about volumes. But Romania must take the first step, farmers must be ahead of others in the market to preserve the potential of the new crop.

REGIONAL STATUS

RUSSIA. Russia is experiencing serious problems in ports. Bad weather plays havoc and stops the export flow at the most important logistics points. The association with the launch of the offensive raises the price of the goods. The Russian government continued to increase grain export taxes for the week of February 22-28, as the impact of the fall in the value of the ruble against other currencies was felt, against the background of relatively stable physical prices, according to official data from the Ministry of Agriculture, published on Friday.

Line-ups for Black Sea deliveries totaled 23.2 million tons since the start of the 2022/23 marketing year in July 2022. Overall, considering all ports and land exports, the volume reached about 27.4 million tons – 22% above last year’s total export figure.

Local analysts raised their estimates of total exports for the marketing year by 100,000 tons amid a weakening ruble and high demand from importers, raising the projection to 44.2 million tons of wheat.

Wheat exports are expected to hit a record high between February and June, which is usually the end of the marketing year. This pace will be supported by the weaker ruble and generally favorable conditions for exporters due to record domestic stocks and strong current demand from importers. The wheat export rate increased to 69.24 USD/MT, or 5.58 USD/MT week-on-week, according to the official exchange rate published by the Central Bank, of 74.7638 RUB to 1 USD.

UKRAINE encounters the same problems in physical inspections and, according to its own estimates, will remain with about 11 million tons from the 2 crops in terms of stocks. This aspect will not generate positive effects because, if we also associate the 8 million tons of export potential from the 2023 crop, we will approach the value of 19 million tons, i.e. similar to what is forecast for this season.

Ukrainian exporters registered 419,440 tons of wheat to go abroad in the reporting period, bringing total wheat exports from the start of the 2022/23 marketing year to 10.7 million tons, up 39.6% little more than at the same stage last year.

Romania, Turkey, and Spain took half the volume during the reporting week to Feb 16 – about 75,000 tons each – along with smaller volumes expected to be shipped to Poland, Bangladesh, Tunisia, Thailand, Lebanon, and Portugal.

THE EUROPEAN UNION. The Bulgarian Ministry of Agriculture published the overview of the grain market on Wednesday, February 15, reporting the level of stocks of the main grains and oilseeds.

The country’s wheat balance currently stands at 3.74 million tons, based on the 6.34 million tons crop for the 2022/23 marketing year, harvested in July, as well as domestic consumption of 1 million tons and of exports of 1.73 million tons in the period July 1-February 10.

As for France, it increased its wheat crop area forecast to 4.76 million hectares. So, we have a new factor of surplus goods in the EU. French wheat status indicates a good to very good vegetative level of 93%, up 1% from the previous week.

SERBIA. Egyptian officials signed an agreement with Serbian officials allowing the import of 1 million tons of Serbian wheat, which will be transported from the Romanian port of Constanța to the Egyptian ports of Alexandria and Damietta. The announcement comes after a meeting of the Egyptian Minister of Supply and Internal Trade, Ali Al- Moselhy, with an official delegation from Serbia.

EURONEXT – MLK2323 MAY23 – 291.5 EUR

EURONEXT WHEAT TREND CHART – MLK2323 MAY23

GLOBAL STATUS

INDIA. India’s wheat output in 2023 is likely to rise 4.1 percent to a record 112.2 million tons, the government said on February 13, as higher prices prompted farmers to expand acreage crop with high-yielding varieties, and the weather remained favorable. Despite the expected production increase, India is considering extending the ban on wheat exports as it seeks to replenish state reserves and reduce domestic prices.

CANADA. The weekly pace of durum wheat exports rose to 166,200 tons, up 71% from the previous week, bringing the total wheat exports for the current marketing year to nearly 3 million tons. This figure is also 109% higher than last year. The weekly pace of wheat exports rose 10% from the previous week to 364,600 tons, bringing the total to 10.6 million tons as of August 1, up 67% from last year.

ARGENTINA. The local USDA office cut Argentina’s wheat and wheat flour export estimates for 2022/23 to 6.2 million tons, 1.3 million tons below official figures released on February 8, due to “lower initial stocks low, of higher domestic consumption and higher final stocks”.

INTERNATIONAL GRAIN COUNCIL IGC. The global wheat production forecast was held steady from the previous report at 796 million tons, a 2% increase on last year’s figures. The forecast for wheat consumption was also maintained at 789 million tons, up 0.8% from last year. The wheat trade forecast was raised by 3 million tons to 197 million tons, which puts it at the same level as last year’s forecast.

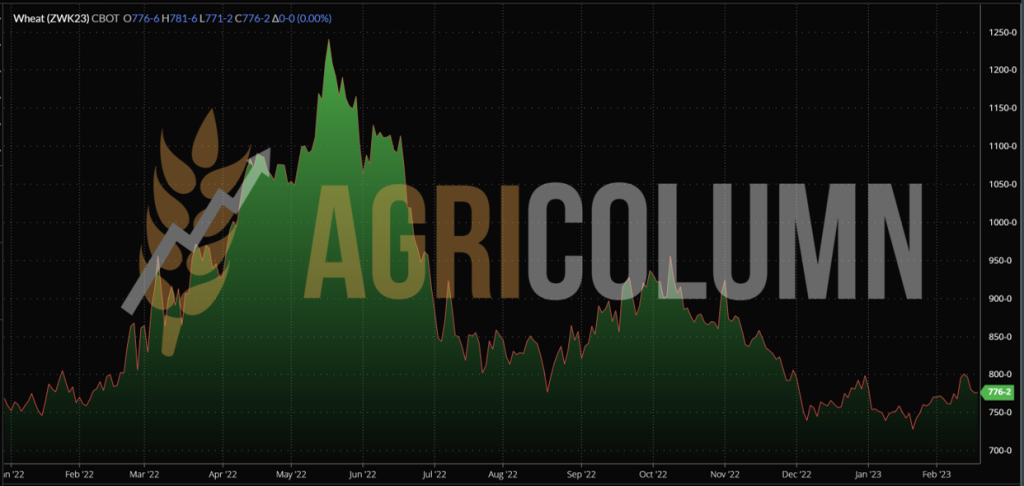

CBOT WHEAT – ZWK23 MAY23 – 776 c/bu

CBOT WHEAT TREND CHART – ZWK23 MAY23

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

TENDERS AND TRANSACTIONS

MIT JORDANIA goes to tender again for 120,000 tons of wheat. The deadline for submitting price offers in the auction is February 21. Possible shipping combinations are June 1-15, June 16-30, July 1-15, and July 16-31. So, we will also have NC – new crop. Jordan made no purchases in its previous tender for 120,000 tons of wheat on February 7, despite unusually high participation from ten trading houses.

ODC TUNISIA purchased 100,000 tons of milling wheat, 11.5% protein. The delivery period is between March 10-30. Prices in CFR parity (Cost & Freight):

- 25,000 tons from Casillo – 337.68 USD/MT

- 25,000 tons from Viterra – 339.24 USD/MT

- 2 x 25,000 tons from Aston – 339 USD/MT

CAUSES AND EFFECTS

EURONEXT and CBOT have started the liquidations of March 2023, more precisely, from February 15, 2023. What does this mean? We will see funds liquidate positions and/or roll over at the next indication, which is MAY23. Because of this, we see daily swings up and down in the stock markets. But this will increase in the next 8 days. So, we will follow MAY23 EURONEXT and CBOT from now on.

REGIONAL STATUS – CEREALS CORRIDOR

Traders are making every effort to have time to deliver purchased volumes by March 19 and do not plan to load ships after March 15, as they do not count on the continuation of the grain corridor due to the rhetoric from the Russian Federation, which is supposedly withdrawing from the grain agreement.

Meanwhile, Russia is destroying Ukraine’s port infrastructure, creating threats to the security of Ukraine’s southern regions from the Black Sea and disrupting the Black Sea grain corridor, while the Russian Federation will take advantage of free commercial shipping from Russian ports on the Sea Black.

At a press conference in Geneva on February 15, UN Under-Secretary-General for Humanitarian Affairs Martin Griffiths responded to the call by Ukrainian ministers and said the implementation of the grain deal should be extended beyond March 19, when it expires. He expressed confidence that this would be done to ensure international humanitarian security.

The Russian Federation has started its offensive and will advance only in Donbas. According to the Ministry of Defense, the Russian Federation has already started an offensive campaign in the Lugansk region, along the Svatove-Kreminna line, in the west of the Lugansk region. At the same time, the full involvement of Russian forces may lead to a final climax without achieving the goals of fully occupying the Lugansk and Donetsk regions. This climax will likely provide a window of opportunity for Ukrainian forces to launch their counteroffensive. But it won’t be easy, as Russian troops have amassed 1,800 tanks, 3,950 armored vehicles, 2,700 artillery systems, 810 self-propelled guns, 400 fighter jets and 300 helicopters for their new offensive.

Things are getting worse in Ukraine. Russia took the initiative.

NATO Secretary General Jens Stoltenberg warned in a briefing on Monday (February 13) that the West is now locked in a race against Russia to bring ammunition to the front line in support of Ukrainian forces. He specifically stated that NATO countries are in a “logistics race” for ammunition and weapons supplies at a crucial time of escalating fighting. This is because “Russia seems to have already launched a large-scale offensive in Ukraine, sending thousands and thousands of additional troops”, Stoltenberg explained.

“It is clear that we are in the logistics race. Key capabilities, such as ammunition, must reach Ukraine before Russia can take the initiative on the battlefield.” He also dramatically described “a war of attrition becoming a battle of logistics” while admitting that “yes, we have a challenge. Yes, we have a problem, but we have a strategy to solve it.” In some ways, his new words are a belated acknowledgment that Russia has already taken the lead.

FEDERAL RESERVE: “Given stronger growth and firmer inflation news, we are adding another 0.25% to our Fed forecast. We now expect three more hikes of 0.25% in March, May and June, for a maximum funds rate of 5.25-5.5%.”

SUMMARY OF CONCLUSIONS

The narrowing of the window of opportunity for Ukraine in attempting to deliver the goods is obvious. We expected Russia to have the initiative on the battlefields of the occupied territories.

At the same time, we see Russia generating large volumes of wheat in the Black Sea basin, and if things continue in this way, along with repositioning on the ground in Ukraine, we will see total rationing of the market in the basin.

In other words, Russia will decide the price of the goods and the volumes. But we have to keep in mind only one parameter: Russia has to sell wheat, and a blackmail and blockade due to raising the price to much higher levels is not possible. Why? Because volumes must be sold. What Russia is trying now is nothing more than establishing a new territoriality in the global wheat market. But the destinations are not naive either. They want to have healthy partners and thus share their risk. Cheap Russian wheat is good, but its unreliability as a partner forces me to get my supplies from other sources.

We therefore remain in the same expectation, which will last until mid-March, when the markets will enter the spring cycle generated by the forecasts for the new crop, which can be seen very well on the horizon. So, the price evolution will not be positive from this point of view.

THE GRAIN CORRIDOR does not bother Russia. As long as Russian officials systematically block inspections and choke the Ukrainian flow, they have absolutely no reason not to extend it. It really is a beneficial thing for them, one of image and bargaining point. But looking at the Black Sea map, removing the rest of the ships and keeping only Bulk Carrier and Tanker, we see who dictates, namely Russia. Ukraine looks very fragile in the POC (Pivnyi -Odessa- Chornomorsk), but the transit is sharpening towards Romania, at the mouths of the Danube.

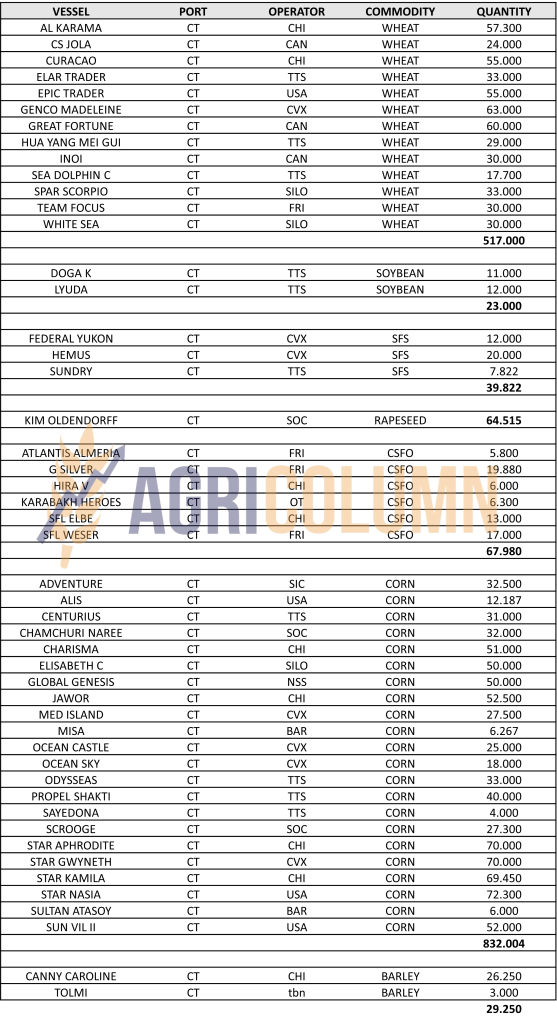

Source: marinetraffic.com

LOCAL STATUS

The feed barley price indications remain in the 240-242 EUR/MT indication area, CPT Constanța parity.

REGIONAL STATUS

RUSSIA. The Russian government continued to raise grain export taxes for the week of February 22-28. Barley export duty also rose to 49.72 USD/MT with the core index unchanged at 261.1 USD/MT.

UKRAINE. Weekly barley exports stood at 46,552 tons, while the total volume exported since the start of the 2022/2023 season stood at 1.98 million tons, which is still 67% below last year’s pace. It is estimated that 2.5 million tons will be included in the volume of the new 2023 barley crop.

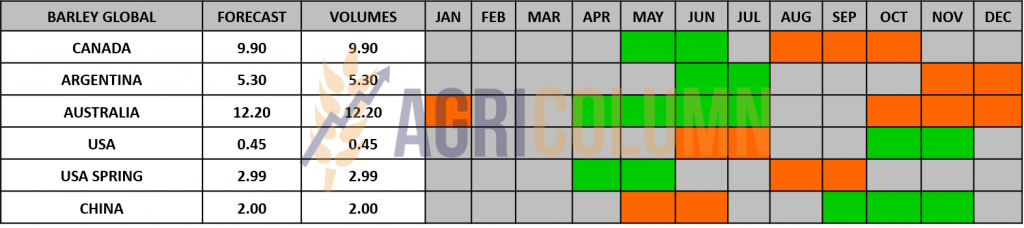

BARLEY PRICE INDICATIONS IN MAIN ORIGINS

GLOBAL STATUS

CANADA. Weekly barley exports posted the biggest increase at 122,800 tons, up 159% from last week, bringing total exports since the start of the season to 1.9 million tons, up 13% compared to last year.

LOCAL STATUS

Corn indications in the port of Constanța are at the level of 265 EUR/MT.

CAUSES AND EFFECTS

Corn remains at the same level as the previous week. It has not degraded in terms of price or demand because demand exists regionally and is clearly a seasonal commodity. The European Union is still asking for corn, Ukraine is trying all transit channels to move goods within the European Union, and the conclusions of the latest global reports indicate a marginal decrease in global production. If we judge from the lens of prices, wheat has declined, but corn has remained stable. And taking this benchmark, we see a difference of 10-12 EUR/MT in the physical market between the two commodities, compared to 40-50 days ago, when we had a difference of 30-35 EUR/MT in favor of wheat. In stock market terms, we can put the equal sign between the two commodities. The conclusion is simple. Wheat, which is the driver, declined, but corn remained stable. The global volumes of the two commodity categories make the difference.

REGIONAL STATUS

UKRAINE. The weekly volume of maize declared for export stood at 647,080 tons, a 26% delay from the previous week’s pace, bringing the total of corn exported since July 1 to 17.2 million tons (or 6% less than the annual rate).

In the week to February 16, Romania and Spain were the main destinations for Ukrainian corn, taking about 135,000 tons each, although Romania is mainly a transit destination, from which the grain is re-exported.

Ukraine claims that it will remain with a stock of 21 million tons of corn, accumulated from previous crops. But even if it will be included in the new crop, the question of the quality condition arises.

The EUROPEAN UNION is clearly favored in terms of logistic level related to Brazilian and North American Origins. Shipping quotes have dropped a lot and both mentioned origins are quoting a maximum of 12 USD/MT from loading ports to the Iberian peninsula. Spain is favored from this point of view, as China’s demand to replenish pork stocks generates demand for feed for processing and shipping the meat to its destination. In other words, Spain will process and therefore needs feed, and South and North American corn, is valued through the prism of logistics.

EURONEXT CORN – XBM23 JUN23 – 290.75 EUR

EURONEXT CORN TREND CHART – XBH23 MAR23

GLOBAL STATUS

ARGENTINA. Corn planting ended in Argentina after a weekly advance of 0.9 percentage points, the Buenos Aires Grain Exchange (BAGE) said in its weekly report published on Thursday. Argentina is expected to harvest 44.5 million tons in 2022/23 on a projected area of 7.1 million hectares. In the previous agricultural year, the country harvested 52 million tons from 7.9 million ha.

“Harvest of early crops is progressing at a good pace in the provinces of Santa Fe and Entre Ríos, with yields below initial expectations,” said BAGE. Maize rated as good to excellent fell 9 points on the week to 11%, while area considered in good condition fell 2 points to 44%.

That said, acreage in poor condition now accounts for 45% of the crop, a weekly increase of 11 percentage points. Moisture is considered favorable in 45% of the area, down 10 points from the previous week, while 55% of the area remains dry.

The U.S. Department of Agriculture (USDA) field office in Argentina has cut estimates for the country’s grain production and exports, with corn production estimates cut below the latest official USDA figures to 45 million tons, it said. -a report from February 10.

BRAZIL. Safrinha corn planting reached a completion rate of 20.4% as of February 11, up from 10.7% the previous week, though still below the 35.1% level recorded a year ago.

The second crop of Safrinha corn is being planted rather slowly in the state of Parana in southern Brazil. Only 12% was planted, compared to 28% last year and 23% on average. The indicators are not good at the moment. The closing window is fast approaching, and the difficulties are intensifying. Too much precipitation is damaging.

Safra corn harvest reached an 11% completion rate on February 11, just 1.9 percentage points higher than the previous week. The harvest of Safra corn is also delayed compared to the previous year, when at this time 17.5% of the planted area had been harvested.

Brazil, which is poised to HARVEST more than 300 million tons of soybeans and corn in the 2022/2023 season, faces a grain storage deficit of 117 million tons this cycle. Brazil should invest 2.90 billion USD per year to avoid expanding the grain storage gap.

INTERNATIONAL GRAIN COUNCIL IGC.

- World maize production was reduced by 8 million tons from the previous forecast to 1.153 billion tons, which translates into a 0.7% year-on-year decline.

- The corn consumption forecast was also cut by 8 million tons to 1.180 billion tons, down 3% year-on-year.

CBOT CORN ZCK23 MAY23 – 677 c/bu

CBOT CORN TREND CHART – ZCK23 MAY23

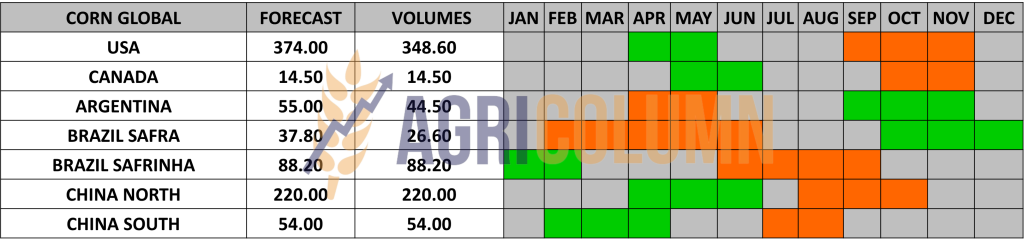

CORN PRICE INDICATIONS IN MAIN ORIGINS

CAUSES AND EFFECTS

We remain in the same general picture as in the previous week. The control parameters are identical, and we recall them for good measure. First, the crop level in Argentina cements the corn platform and supports it. Second, the rainfall in Brazil does not make room for the sowing of Safrinha. However, in the European Union, it is observed how the commodity has cursive and generates volumes from Ukrainian origins.

As with wheat, the trading month is changing in EURONEXT and CBOT, and we will in turn move to MAY23 CBOT and JUN23 EURONEXT. The transition is happening these very days and it will take another 8 days for the funds to liquidate the positions and perform the roll -over.

But we must be aware that this price platform will not remain at this level indefinitely. With each passing week, it erodes you. Why? It is extremely simple. South American volumes will be known, and at this moment, we do not think they will be able to decrease, so the premises could reverse, and we could see corn at the level of 245-250 EUR/MT in the CPT Constanța parity.

LOCAL STATUS

Rapeseed quotations in the port of Constanța were granted with the increase on EURONEXT. We thus have a level of 535-540 EUR/MT for the goods delivered in the CPT Constanța parity. Processors remain at the same levels as MAY23 minus 25 EUR, i.e., 540 EUR/MT.

CAUSES AND EFFECTS

Rapeseed has acquired new valences. The demand for rapeseed meal, so the protein market, caused rapeseed to return to 564 EUR on EURONEXT. But apart from this parameter, there is absolutely nothing on the horizon for rapeseed. Even the intensification of the conflict cannot generate spectacular increases. Ukraine’s crops are already sold, and the European Union has two sources of supply to rely on: Canada and Australia.

EURONEXT RAPESEED – XRK23 MAY23 – 550.5 EUR

EURONEXT RAPESEED TREND CHART – XRK23 MAY23

REGIONAL STATUS

EUROPEAN UNION. The low supply of protein meal in the EU has led to an increase in rapeseed meal prices. The shortage was exacerbated by the delay in sunflower meal deliveries.

The year-on-year upward trend continued for EU rapeseed. Rapeseed processing continued in January, primarily in northwestern Europe. Supplies are currently insufficient to meet demand, despite the EU’s recent transformation into a net importer of rapeseed meal (c. 50,000 tons in October-December 2022, compared to net exports of 40,000 tons a year earlier). Russia and Belarus have been by far the biggest suppliers of rapeseed meal to the EU so far this season, trying to make up for the significant drop from Ukraine, where exports have been reduced. Imports rose sharply to around 230,000 tons, up nearly 70% year-on-year.

FRANCE. Rapeseed areas in France increased for the 2023 crop to the level of 1.34 million hectares. The increase is above last year’s levels and above the average of the last 5 years.

GLOBAL STATUS

INDIA. India’s rapeseed production in 2023 could rise 7.1 percent from a year earlier to a record 12.8 million tons, the government said. An increase in production could help the world’s largest edible oil importer reduce overseas purchases of palm oil, soybean oil and sunflower oil.

AUSTRALIA. Canola exports hit a new monthly high of 0.88 million tons in December, up 16% from the previous month and well above the 0.29 million tons recorded a year earlier.

ICE CANOLA RSK23 MAY23 –820.3 CAD

ICE CANOLA TREND CHART – RSK23 MAY23

COMPARATIVE GRAPH. PETROL-RAPESEED-CANOLA CORRELATION

CAUSES AND EFFECTS

The demand for protein helps rapeseed these days. And we have an effective jump of 15 EUR in one week. Delivery delays in the Black Sea basin area are driving up prices.

But overall, the high areas in the European Union, the high areas in India, the rich crops in Canada and Australia, to which we add Germany’s intentions regarding the use of rapeseed oil in biofuel, lead us to one conclusion: the price of rapeseed does not will experience spectacular growth. Brent and WTI quotes are not helping either.

The Canadian-Australian ensemble won’t start seeding until April 2023, so we have a long window of time.

We think it is a good time for a forward sale. Under the condition of a production of at least 2.5 tons per hectare, an operational margin of 25-30% of the investment value per hectare can be captured.

LOCAL STATUS

Constanța port quotes sunflower seeds at values between 540-550 USD/MT.

Processors are correlating and indicating a trading base of 540-550 USD/MT at DAP Processing Units parity.

CAUSES AND EFFECTS

Waiting for the possible impact generated by Russia in Ukraine leaves the seed market free for this period. The price drop of around 5-10 USD/MT is only generated by the recovery of the USD. So basically, no other factor accounts for the 5-10 USD/MT discount. The month of March will be extremely interesting and decisive in the overall price of sunflower seeds.

REGIONAL STATUS

UKRAINE. Ukraine’s sunflower oil exports doubled in the week ended Feb. 16 from the previous week as low prices spurred strong buying interest from end users, data from the Agriculture Ministry showed on Friday. the country.

BULGARIA. Sunflower oil stocks were reported at 1.6 million tons, with total production at 2 million tons, consumption at 1.14 million tons and exports at just 126,825 tons.

According to market sources, Bulgarian sunflower seed processors imported about 1 million tons of sunflower seeds of Ukrainian origin, while logistics operators and traders also supported the transboarding of Ukrainian goods through the ports Bulgarian sea, as well as by land transport.

GLOBAL STATUS

PAKISTAN is starting to generate higher demand for raw material. It’s a start for palm oil-fueled Asia.

PRICE INDICATIONS FOR OILSEEDS AND CSFO IN MAIN ORIGINS

CAUSES AND EFFECTS

As for the old crop, the status has not changed in any way. March will be the one that will absolutely decide whether the Ukrainian flow will be choked and, implicitly, will generate an increase in the price level.

But the 5-10 USD/MT drop in local indications is due to the strengthening USD. As for the new crop, we must have no illusions. Much larger areas will be sown at the level of the European Union, and if the weather does not intervene, we will see a settlement of the price of the new crop at the level of 440-450 USD/MT DAP Processors and 460-470 USD/MT CPT Constanța.

The price of oil in SIX Ports also fell, in line with the calm and timing of Ukrainian cargo flows. 1,137.5 USD/MT is down 17.5 USD/MT from last quotes. Let’s not forget that Russia exports oil duty-free, and in the European Union, Russia and Belarus are major exporters of rapeseed and sunflower protein meal.

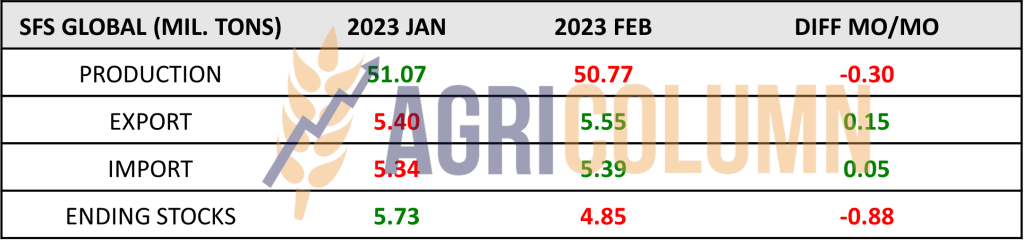

The table below clearly describes in numbers the global status of seed production and stocks. It will be the Geopolitical factor that will boost the market in the next 2-3 weeks.

LOCAL STATUS

In Romania, the price indications for soybeans are at the level of 560 USD/MT DAP processing units for non-GMO soybeans.

REGIONAL STATUS

UKRAINE. According to the data provided by the Ukrainian customs authorities, in the week ending on February 16, soybean exports reached 99,250 tons. About 30,000 tons were delivered to the Netherlands. The total volume of soybeans exported since September 1 reached 1.98 million tons.

GLOBAL STATUS

USA. Weekly US soybean export inspections were reported at 1.5 million tons. These were below analysts’ expectations of between 1.6 and 1.9 million tons, according to data provided by the US Department of Agriculture (USDA). The main destination was again China with 998,660 million tons, and other relevant destinations were the Netherlands (131,874 tons), Mexico (82,444 tons), Italy (72,404 tons), the Republic of Korea (60,131 tons) and Peru (32,999 tons). Total inspections since the beginning of the 2022/2023 marketing year reached 39.5 million tons.

USDA’s weekly data on 2022/2023 soybean net sales shows a level of 512,800 tons in the week ended February 9.

Exported volumes totaled 1.9 million tons. China was the main destination (1.1 million tons) and other relevant destinations were Germany (153,500 tons), the Netherlands (131,900 tons), Spain (130,000 tons) and Mexico (114,000 tons).

BRAZIL. Soybean harvesting has a dynamic pace and has reached 15.4% of the area, according to the Conab agency. However, it is a much lower percentage than last year at this time, when 25% of the area was harvested. In Mato Grosso, harvesting was done on 40.1% of the surface, and in Parana, according to the state agricultural agency Deral, it reached 7%.

Soybean production in Parana is estimated at 20.7 million tons, compared to 12.3 million tons last year, on an area of 5.7 million hectares. Soybean crop conditions improved due to the rains and the area assessed in good condition reached 84% of the total area. Those rated as average dropped to 13%, and those rated as poor dropped to 3%. In Rio Grande do Sul, sowing is completed, and harvesting has not yet begun.

According to official customs data, Brazil exported 1.3 million tons in the first two weeks of February. They exceeded the volume exported throughout January of 851,878 tons. The National Association of Cereal Exporters of Brazil expects the February figure to exceed 9.3 million tons.

ARGENTINA. The outlook is worrisome for soybean crops, as crops rated normal to poor have reached 60%, and forecasts point to a drop in temperatures and rainfall volumes that are insufficient for crop needs.

According to Argentina’s Ministry of Agriculture, sales of new crop soybeans fell to 215,000 tons during the week and total sales of the 2022/2023 crop reached 3.4 million tons, compared to the same time last year when sales was 7.5 million tons.

There is a possibility that the decrease in sales is generated by the fact that Argentine farmers want to keep stocks in case the price will be higher as a result of the reduced harvest. The incentive to hold stocks is also supported by expectations of the government’s relaunch of the dollar-soybean program in May-June.

Argentina is the world’s largest exporter of soybean meal and oil, and the outlook for tight domestic soybean supply is expected to have significant consequences for global soybean oil and soybean meal prices in the 2022/2023 marketing year.

CHINA. Soybean processed volumes reached 2.06 million tons last week, according to data from the National Grains and Oil Information Center (CNGOIC). A recovery from the lows around the New Year period is being seen, but the recovery is not expected to continue and volumes are expected to fall back below 2 million tons. As of February 11, CNGOIC reported soybean stocks at 4.65 million tons, down about 12 percent from last week.

Soybean meal stocks rose slightly to 610,000 tons on 10 February. Stock levels rose by 150,000 tons week-on-week and by 290,000 tons to nearly 90% from the same time last year.

Soybean oil stocks were slightly lower this week by 10,000 from last week, reaching 680,000 tons on February 14, down 1.45% from the previous week. With processing activities fully resuming, soybean processing is expected to increase strongly, which will lead to higher soybean oil stocks.

CBOT SOYBEAN ZSK23 MAY23 – 1,522 c/bu

SOY GRAPH TREND – ZSK23 MAY23

EXTRA

UKRAINE BYSTRE – BASTROE

A deepening of a canal linking the Danube to the Black Sea could improve logistics for Ukraine’s shallow-water ports and improve outflows if the grain corridor deal is scrapped.

The draft of the Ukrainian Bystre Canal has been increased by 2.5 meters, reaching 6.5 meters from the beginning to kilometer 77, and seven meters from kilometer 77 to kilometer 166, where the canal meets the Kiliysky Estuary, according to the Ukrainian Ministry of Infrastructure. The changes could allow part of the cargo fleet to go directly to the Black Sea through the Bystre Canal, on the Ukrainian side, and reduce pressure on the Sulina Canal, which is controlled by the Romanian authorities. This canal was used before the war as the entrance to the port of Reni – a small port, which can handle sea exports without going through the controls in Istanbul, which caused major delays for exports from Pivdennyi, Odesa and Chornomorsk.

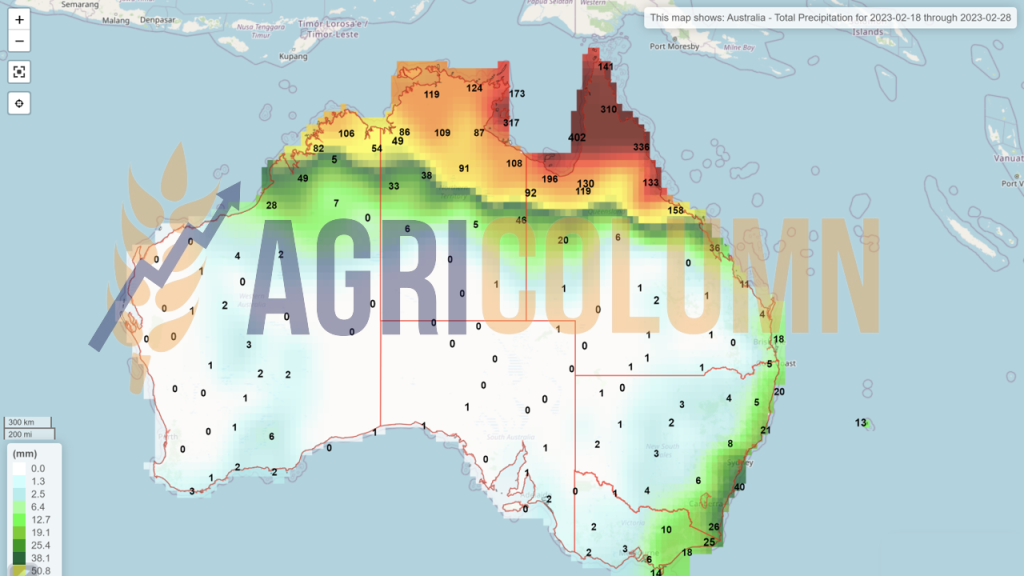

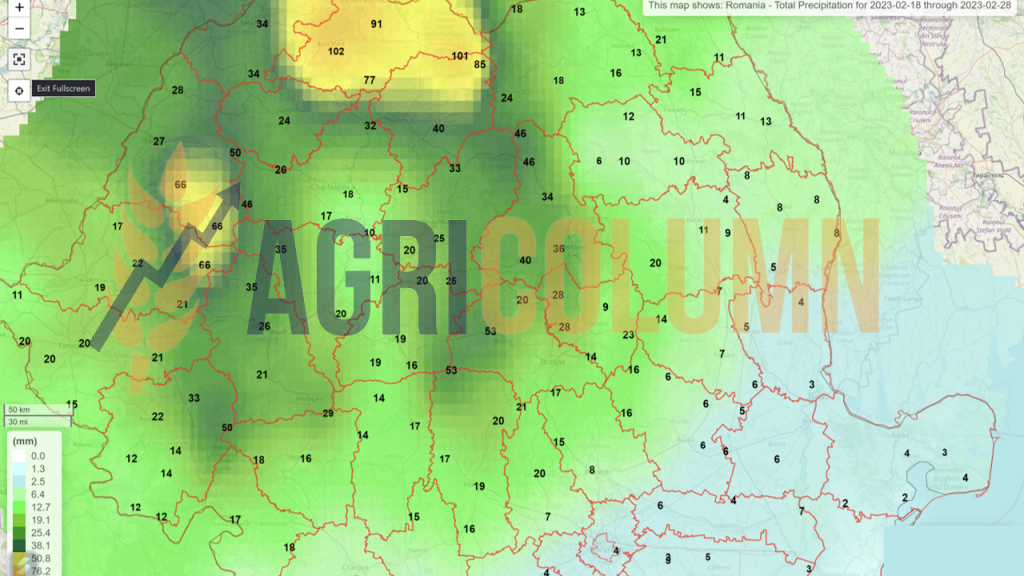

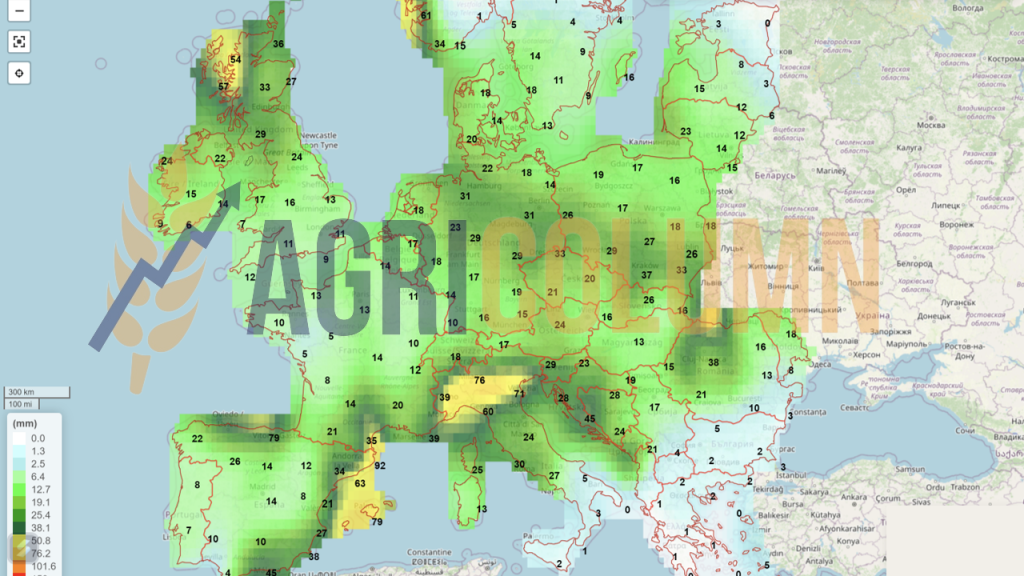

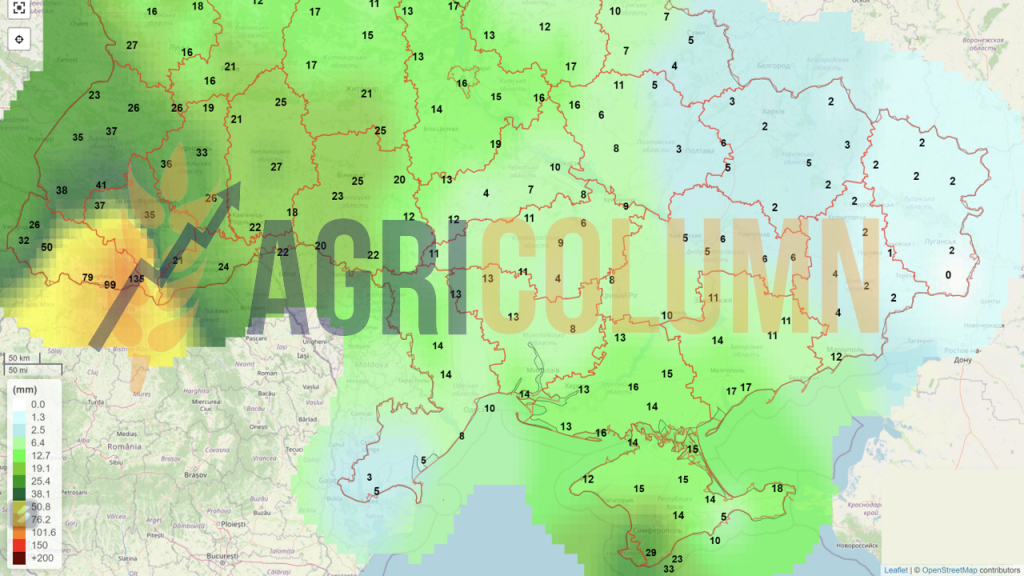

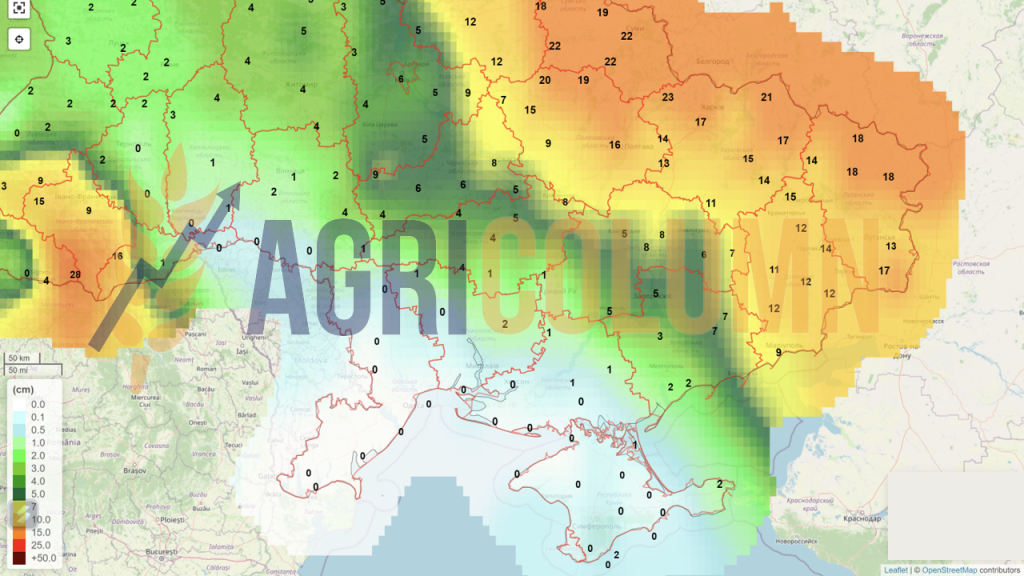

18-28 February 2023

Romania (rain)

Europe (rain)

Ukraine (rain)

Ukraine (snow)

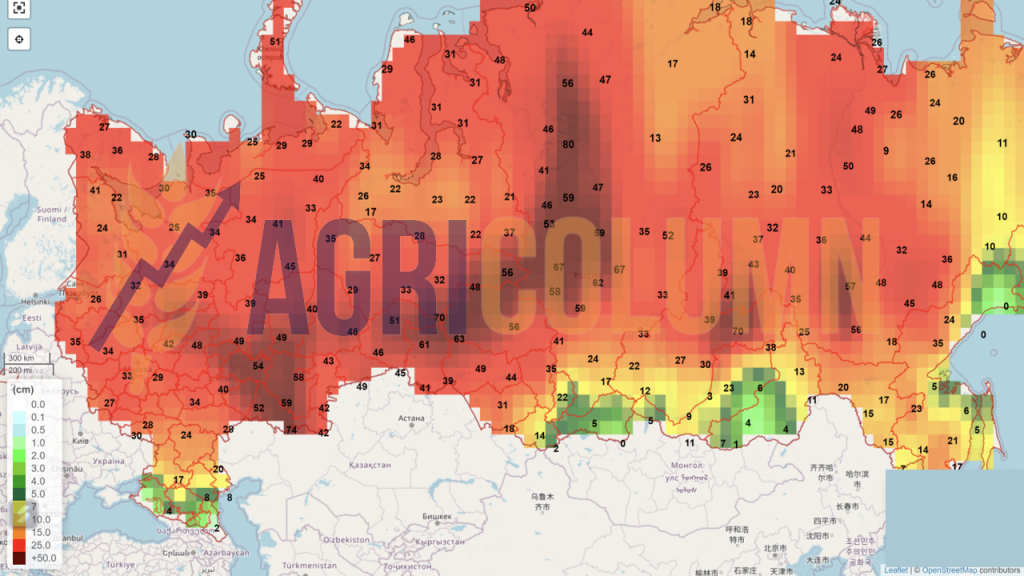

Russia (snow)

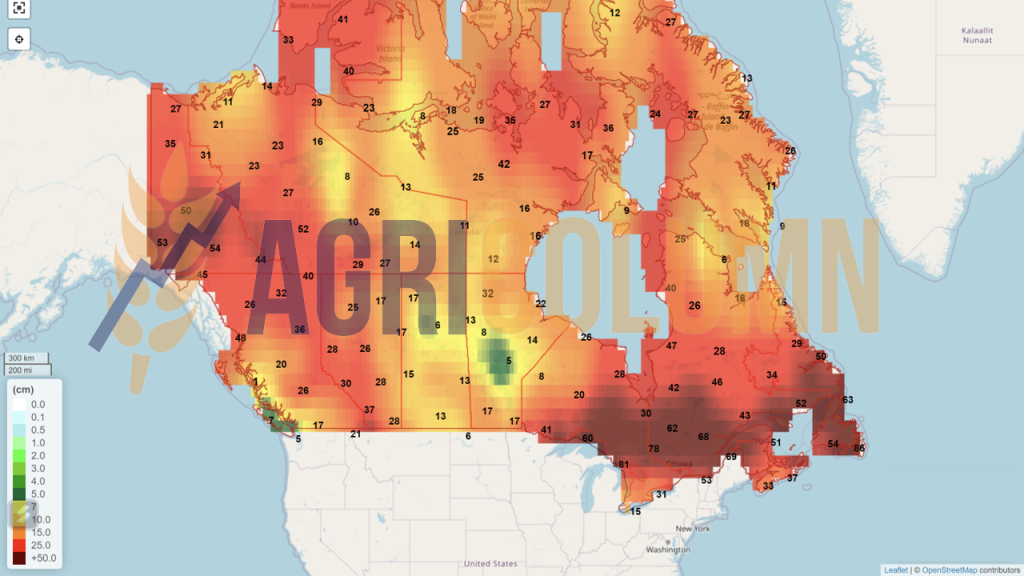

Canada (snow)

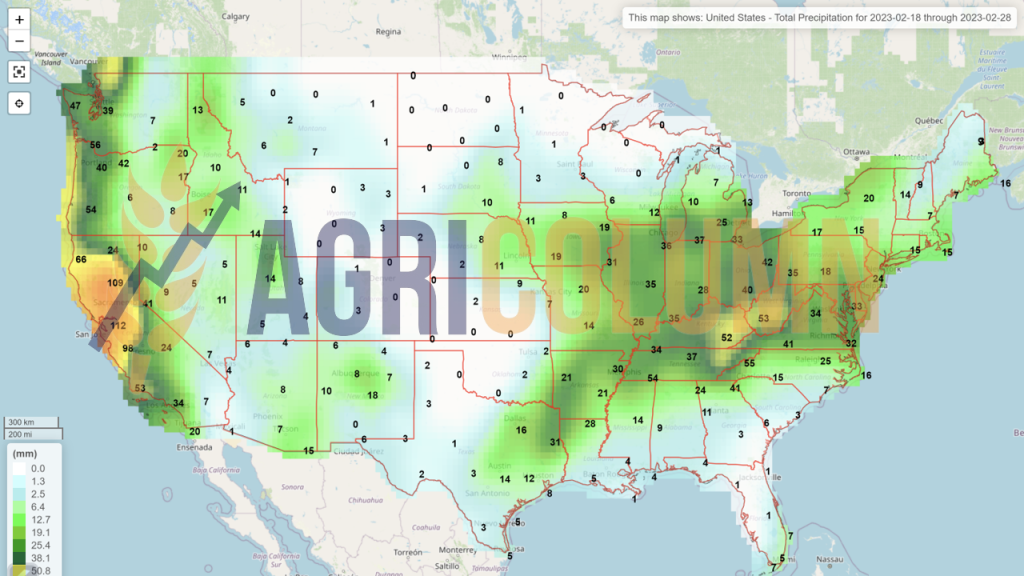

USA (rain)

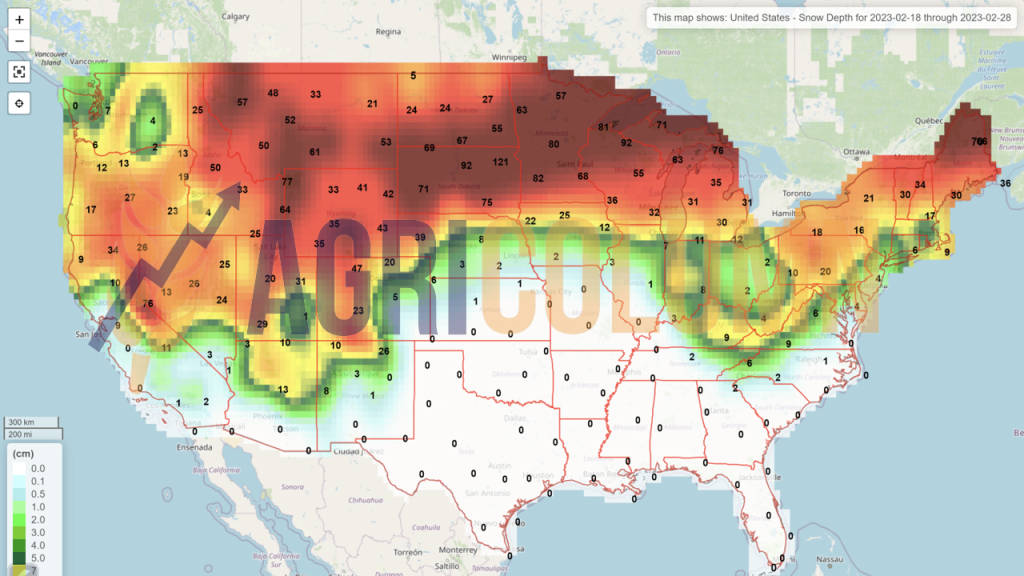

USA (snow)

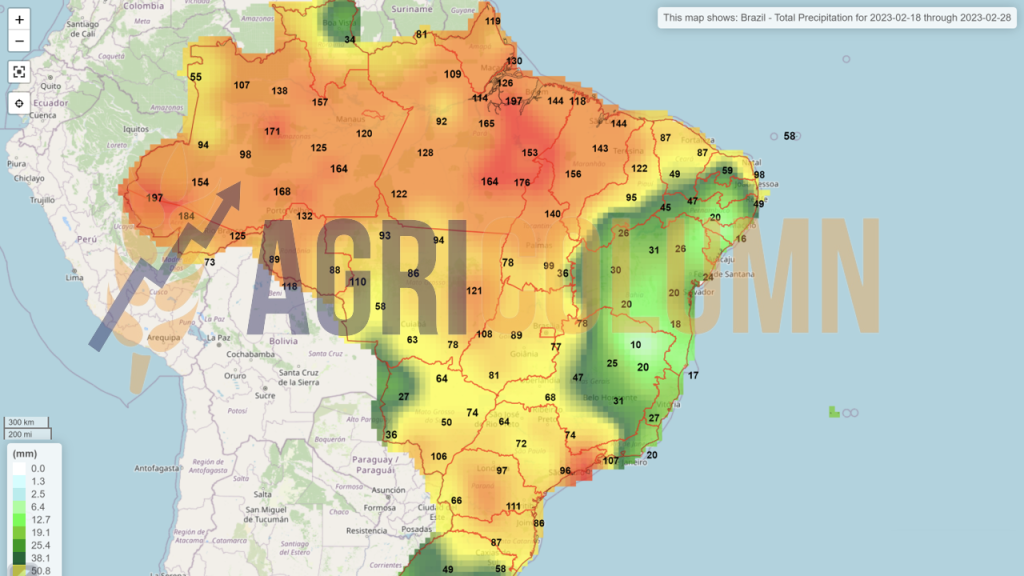

Brazil

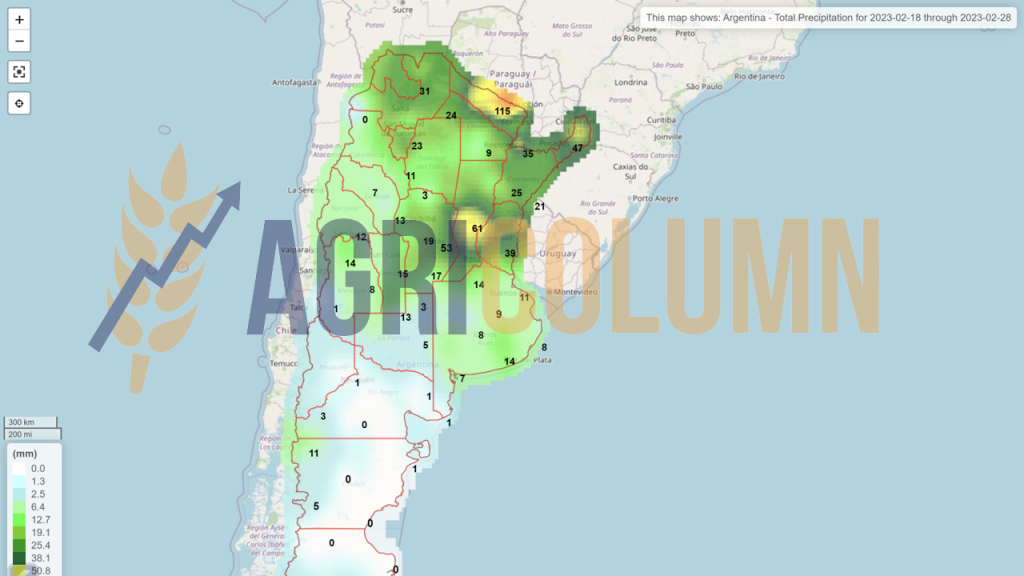

Argentina

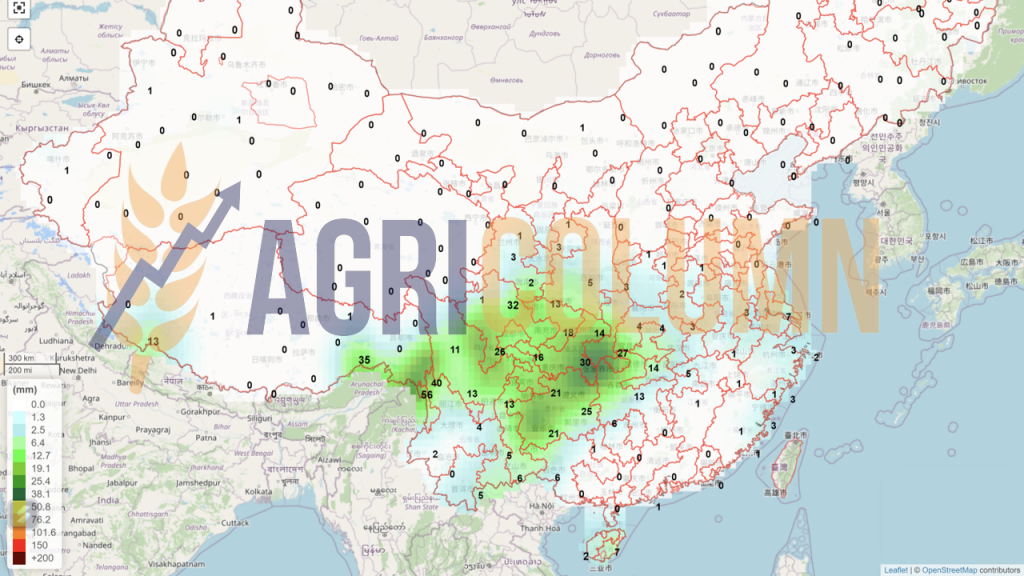

China (rain)

Australia