Today’s special market report is dedicated to WASDE (World Agricultural Supply and Demand Estimates), a market report of the United States Department of Agriculture. Below you can find information on global production, consumption and stocks for the following crops:

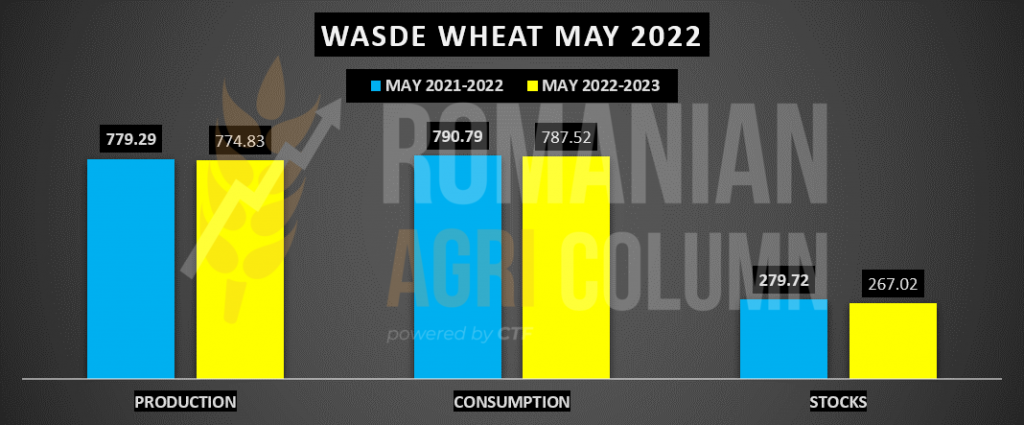

PRODUCTION: WASDE has generated a declining projection globally, which was to be expected, after all the development of winter and spring 2022. We see decreases in the US to the level of 47 million tons (our note is somewhat different and a you will find in the market report on Monday) and decreases in forecasts in North Africa through Morocco, where production decreases by 5.3 million tons (it is a very steep decrease). Australia, in turn, will no longer generate the famous 36 million tons, but only 30 million tons. India is down 6 million tons to 105 million tons due to the sweltering heat wave that has swept across the country. The European Union will also suffer a contraction, but it is not yet quantified. Also, a very significant reduction is found in the case of Ukraine, which drops to a level of 21.5 million tons, compared to 33 million tons last season. In Russia, we can note 82 million tons, far from the 87 million tons they estimate. With all the calculations made, we note an estimate of 774.85 million tons globally, decreasing by about 4.45 million tons compared to last year in the same period.

CONSUMPTION: WASDE generated a consumption projection of 787.52 million tons, down 3.27 million tons compared to the same period last year. Estimates take into account lower feed consumption from China, the EU and Australia, and a decrease in human consumption in India. But if we look at it from the perspective of PRODUCTION vs. CONSUMPTION, we have a clear imbalance. In figures, we have an overall production of 774.85 million tons vs. consumption of 787.85 million tons = minus 13 million tons.

However, global trade is growing to a level of 205 million tons, an increase of 5 million tons compared to last year in the same period. Russia raises its export level to 39 million tons and here we can add with the minus of Ukraine 9 million tons as an export level. In other words, Russia is taking over the market share from Ukraine under the current conditions. The European Union increases its export level by 5 million tons, while at Antipodes, Australia decreases its export forecast by 3.5 million tons.

STOCKS: WASDE generates a declining stock level over the same period last year. Thus, the level of global stocks is 267 million tons, compared to 278.4 million tons last year, in May. With the same note – China holds about ½ of these stocks. It’s like a preheat of the next season. We are on the road with a global production deficit, augmented by a low level of stocks and boosted by higher demand, by increasing global trade.

WASDE MAY 2022

PRODUCTION – CONSUMPTION – STOCKS

-4.46 | -3.27 | -12.7

ANALYSIS

- Production is declining globally due to weather and political factors.

- Consumption is declining, but we must point out that it is May and the transition to the new crop is already taking place, so the decline is somewhat artificial, dictated by the end of the life cycle of the old crop and the expectation of the new crop.

- Stocks are declining, fueled by the war in Ukraine and the country’s lack of export capacity. We see, by comparison, a minus of 12.25 million tons with which we will set off in the new season.

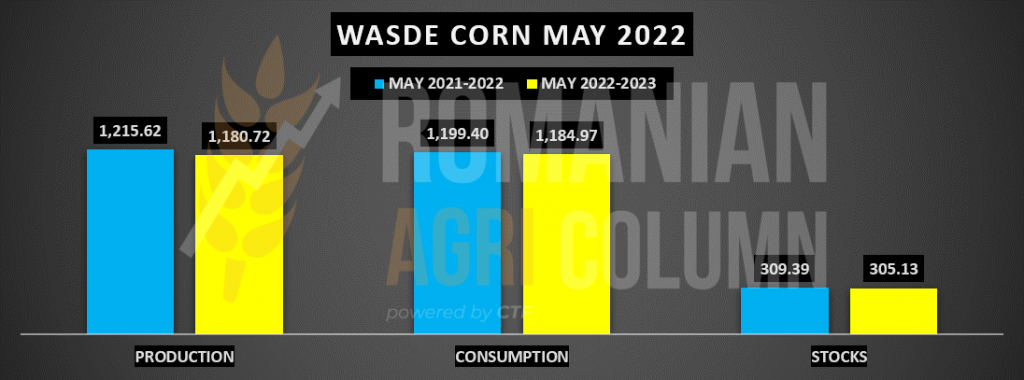

PRODUCTION: WASDE is generating a sharp drop in production for the 2022-2023 season for May. Compared to the same month last year, we have a minus of 34.9 million tons, from an estimate of 1,215.6 million tons last season (May 2021), to a level of 1,180.72 million tons in this season (May 2022). The world is deprived of corn, and as we wrote in our previous reports, the United States will generate most of the shortfall in this production due to reduced corn acreage and productivity per hectare. In short, almost ½ of the decrease in production is in the US account, about 16.5 million tons. Ukraine is effectively deprived of potential due to the war generated by Russia and the production forecast for the 2022-2023 season is reduced by at least 20 million tons, from a potential of 40 million to only 20 million tons. The increases in the 2022-2023 forecasts come from South America, where Brazil, with a projection of 126 million tons and Argentina of 55 million tons, compensate with 10 million and 2 million tons, respectively, the gap left by the USA and Ukraine.

CONSUMPTION: WASDE is now showing a decline of about 14.43 million tons when comparing between the two crops. Last year, in the same period, we had an indication of 1,199.4 million tons, while the current projection indicates 1,185 million tons. The decrease in consumption is generated by China, by reducing imports by 5 million tons. The European Union also adjusts its imports by 1 million tons less to 15 million tons. As a direct consequence, as Ukraine is no longer able to supply exports, this value is also reduced by global consumption. However, we find increases in Iran with 1 million tons and in Vietnam with 2.3 million tons.

STOCKS: WASDE generates a declining level of stocks, but not dramatically. Compared to 309.4 million tons in May 2021, we now have a global stock level of 305.13 million tons of corn. The decline in stocks is due to their lower level in China.

WASDE MAY 2022

PRODUCTION – CONSUMPTION – STOCKS

-34.9 | -14.43 | -4.26

ANALYSIS

- Compared to May 2021, we have a serious production deficit. The USA and Ukraine are the two countries that, consolidated, decrease production. The US is affected by reduced acreage and productivity per hectare, and Ukraine by the inability to reach last year’s production figures.

- Consumption is declining globally compared to May last year. This decline comes from reduced imports into China and collateral in other areas. Reducing feed and industrial use is a temporary premise. The world is moving and consuming.

- Stocks show a marginal decline due to the decline in China’s own stock, but do not overestimate the market. But they too must be put back in place at some point, from where they were taken.

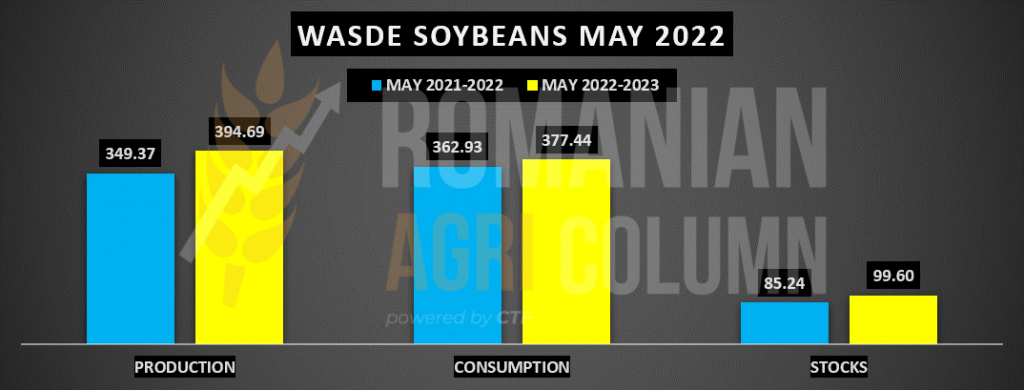

PRODUCTION: WASDE generates a growing soybean production for the 2022-2023 season. And we have in comparison May 2021, with a level of 349.37 million tons, compared to the current forecast of 394.7 million tons. The ending season was largely driven by the drought factor. The new season looks optimistic and so we have an increased forecast of 45.32 million tons this season. Forecasts are estimates, of course, but we note here Brazil, with an increase of 24 million tons, up to 149 million tons; Argentina with 9 million tons, up to 51 million tons of production; and Paraguay with an increase of 5.8 million tons, up to 10 million tons of production. The US will add 5.6 million tons and reach a level of 126.3 million tons.

CONSUMPTION: WASDE indicates an increase in consumption forecast by 14.5 million tons compared to May 2021, which is not a special value, if we compare with the production potential 2022-2023. China is already at a level of 99 million tons, compared to 92 million tons this season.

STOCKS: WASDE indicates a higher level of stocks than a year ago in the same period, when we had 85.24 million tons, and now the figure is 14.36 million tons higher, up to 99.6 million tons. The increase in stocks stems from a lower level of use in China in the 2021-2022 season (100 million tons of import forecast and only 92 million tons achieved so far) and, implicitly, of imports, so that countries of origin have more unsold volumes yet.

WASDE MAY 2022

PRODUCTION – CONSUMPTION – STOCKS

+45.32 | +14.51 | +14.36

ANALYSIS

- The 2022-2023 forecast is already very optimistic in terms of production. Hopes are, as always, related to the weather and we will see how it evolves in the next period for South American production.

- China has a higher consumption compared to 2021-2022, from 92 to 99 million tons.

- The stocks are decent, we could say, if we look at the severity of the drought that has affected South America. The increase compared to last season comes from the low level of Chinese imports.