This week’s market report provides information on:

LOCAL

The indications of wheat in the port of Constanța have had ups and downs lately. We have seen both indications of 265 EUR/MT and indications of 278 EUR/MT in the CPT Constanța parity, all determined by the imminence of Russia’s attack on Ukraine.

The difference for feed wheat is 11 EUR/MT at the moment, and the goods are traded. Romanian farmers understand that there is a lot of wheat in the country, that we have an over-production and thus, the volumes move from one place to another.

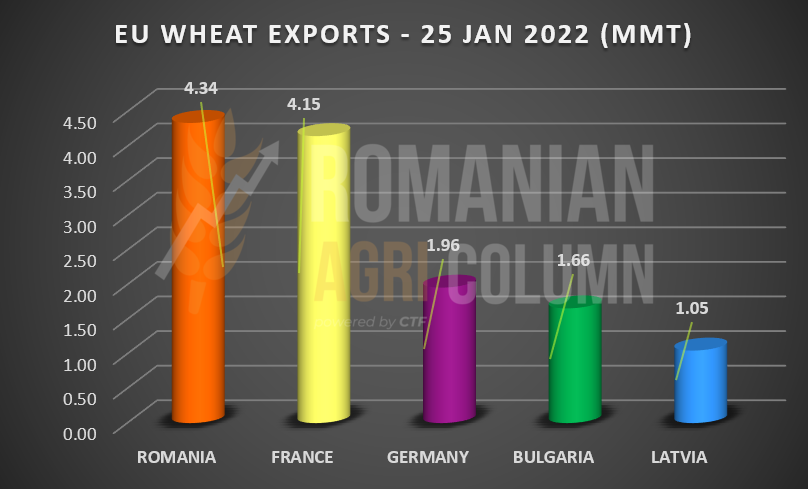

At the moment, the European Union has exported 15.63 million tons of wheat, and Romania takes the 1st place in wheat sales at EU level, with a total of 4.34 million tons, leaving France in 2nd place with 4.15 million tons.

The new wheat crop is capitalized through forward contracts at the level of 236-238 EUR/MT in the CPT Constanța parity, with a discount of 5 or 6 EUR/MT for the quality of feed.

In Romania, we have the same problem landscape in certain areas, highlighted by drought and uneven germination of crops. Hopes for February on the precipitation regime are in vain. The weather forecast does not indicate a rich rainfall regime, but only neutral, according to the multi-annual averages, so a poor one in these conditions.

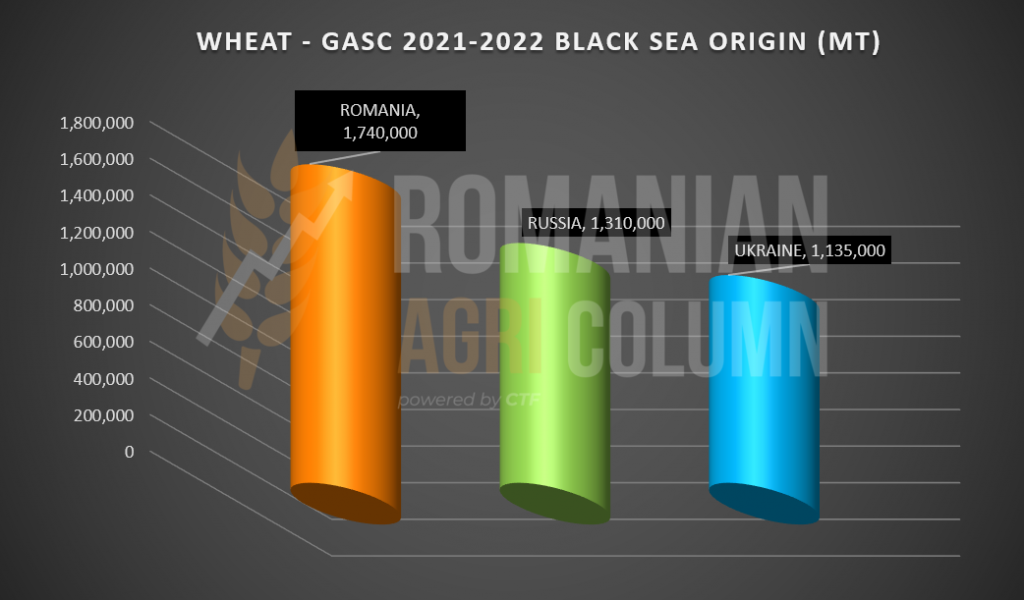

On January 28, 2022, a new GASC tender took place. Egypt has purchased 420,000 tons of wheat from the three sources in the Black Sea basin, namely Romania, Ukraine and Russia. In the top sales for this auction, Ukraine ranks first with a volume of 180,000 tons, followed by Romania with 120,000 tons and Russia with 120,000 tons.

The level at which Romania sold the volume is 329.65 USD/MT in the FOB Constanța parity, which, converted into EUR, indicates 289.2 EUR/MT. If we extract the costs of fobbing, and participation in the auction, as well as the exporters’ margin, we have a maximum level of 273 EUR/MT in the CPT Constanța parity for the March delivery.

In this way, Romania consolidates its leading position in sales in Egypt through the GASC authority and with a total volume of 1.74 million tons, as well as a percentage of over 43% within the Black Sea basin team. However, the difference between Romania and Russia is not very big. Only 430,000 tons separate the two origins, and the wheat road to Egypt is not over yet.

| What we need to keep in mind is that the year 2021 must not be forgotten. We will not meet for a long time with the position of leader of the Black Sea pack. Let us keep in mind and be proud of the Romanian farmers, who made this possible.

To lead 2 countries with a tradition and large volumes of wheat production (Russia with 75.5 million tons and Ukraine with 33 million tons), given that we have a production in 2021 of 11.3 million tons, it is something that shouldn’t be easily forgotten. |

REGIONALLY and GLOBALLY

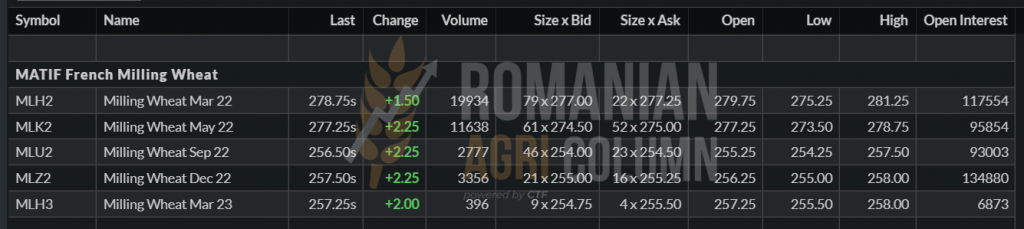

The tension is at a very high level in the Black Sea basin and we are trying to explain the main reasons why the wheat goes up and down on the stock exchanges. But first, let’s look at the indications from the closing of January 28, 2022 on EURONEXT.

MLH22 MAR22 | EUR 278.75 (+1.5)

EURONEXT TREND GRAPHIC – MLH22 MAR22

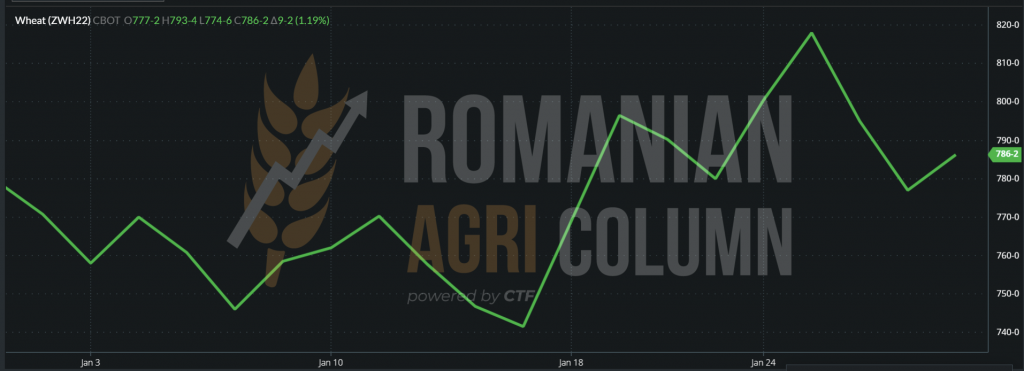

In the same analytical regime, let’s look at the development of CBOT: 786 c/bu (+10)

Looking at the two charts, EURONEXT and CBOT, you can clearly see the identical route of the last few days. We intentionally inserted only January 2022 in order to have a much clearer price route on the two stock exchanges.

Let’s analyze this information:

RUSSIA still has about 11 or 12 million tons to export, out of a total of 34 or 35 million tons (according to USDA). The current level of exports is 24 million tons, and the export tax has dropped to 95 USD/MT.

UKRAINE still has 8 million tons to export. They are now at 16.6 million tons and the export forecast is set at 24.6 million tons.

We therefore have an estimated volume of at least 20 million tons that must leave the basin.

Here we add the Romanian surplus of about 4 million tons (minimum), which must be exported in the coming months and the figure rises to 24 million tons. In other words, in the absence of a conflict, there is a lot of wheat in the Black Sea basin and it has to be sold.

The prerequisites for lowering the price of a potential for flooding the Russian wheat basin are very high. Russian farmers will see the new crop on the horizon after February 20 and will start selling massively. Ukraine will do the same, so we will see the price go down. BSW already indicates prices for February 2022 in red.

But stock trading algorithms can be made to react to news much faster, and so we witnessed a health gallop on EURONEXT and CBOT on 25 January 2022, when wheat reached 291 EUR and 818 c/bu on CBOT, respectively. News of Russian troops crossing Siberia to Belarus, to the Ukrainian border, disturbed (or not) the algorithms, which raised the market to the mentioned levels.

Suddenly, the next day, the “profit taking” operation began and the wheat started to fall on the stock exchanges. No news disturbed the trading algorithms (hmm…) and so the decline continued rapidly until January 27, 2022.

Then, on January 28, 2022, wheat began to grow timidly. From here, things get trickier. The conclusion is very clear to us. Rapid operation of profit taking.

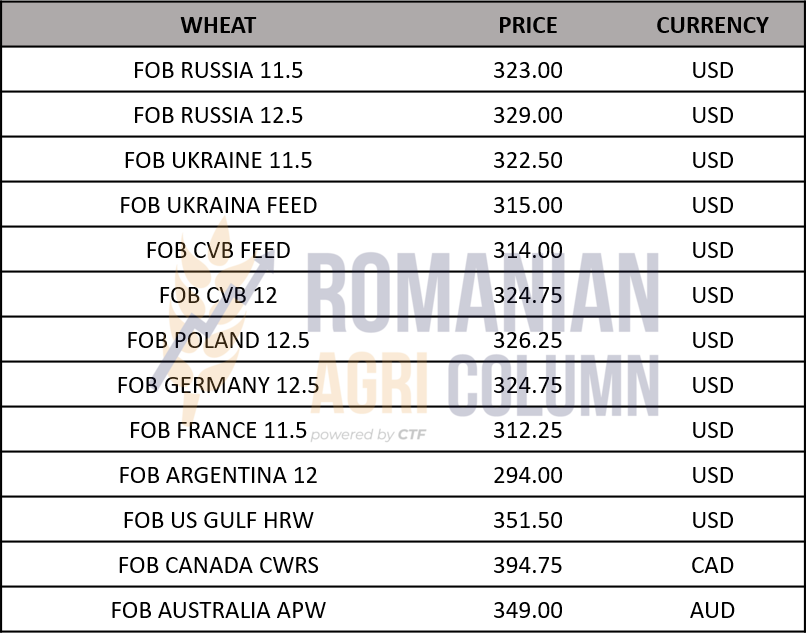

WHEAT PRICES INDICATIONS IN VARIOUS ORIGINS

ANALYSIS

- There is enough wheat in the Black Sea basin. The demonstration of this fact was at GASC, where there were many bidders.

- Wheat will have to come out of the Black Sea basin. The market will continue to be full of wheat.

- Wheat is sufficient globally, so nothing can disturb the supply. Nowhere is it still harvested. That was the global crop.

- The only disturbing fact that could affect the wheat market is Russia’s attack on Ukraine. But here too we see some factors that could defuse this show of strength. The first is American and European diplomacy. The second is the Russian settlement in the device, which is not finished yet. The third is the elapsed time. And if things don’t rush, the ground window closes, Russian blackmail in the winter also comes to a halt as the weather warms up, and as a final note, China’s president Xi urged Putin to refrain during the Olympic Games.

LOCALLY

The indications of the port of Constanța remain unchanged and we see the same level of 243-245 EUR/MT. Liquidity remains unchanged, but we are also seeing indications for a new barley crop. They range from 218-220 EUR/MT to 225 EUR/MT for larger batches.

The first problems that can be seen on the horizon in Romania are in the area of Moldova, where, in Bacău County, there are farmers who will reseed the barley crop (with a spring crop) or at least so they claim at this time. Let’s hope that the number of hectares that will be reseeded is limited, and the negative difference will be recovered in other areas of the country.

REGIONALLY and GLOBALLY

We have an unchanged status compared to last week in terms of hibernating crops at European level and in the Black Sea basin.

Jordan postpones the tender for 120,000 tons of barley for February 2, 2022.

The price of FOB Russia barley remains unchanged at 295 USD/MT. Australia also maintains the same level of 261 USD/MT in FOB parity.

LOCALLY

The price indications for maize increase in the CPT Constanța parity, up to the level of 248 EUR/MT. The increases were dictated by reasons related to bad weather in the Black Sea basin, which conditioned deliveries from Ukrainian ports, as well as rising tensions near Ukraine’s border with Russia.

Romanian farmers feel the level and trade significant quantities of corn during this period. It is a beneficial moment and we mention that the level of Romanian corn export related to the 2021 crop has reached 2.5 million tons.

The indications for maize for the new crop are at the level of 212-215 EUR/MT in the CPT Constanța parity. But it is early and we do not see a desire for forward signing by farmers at this time.

REGIONALLY

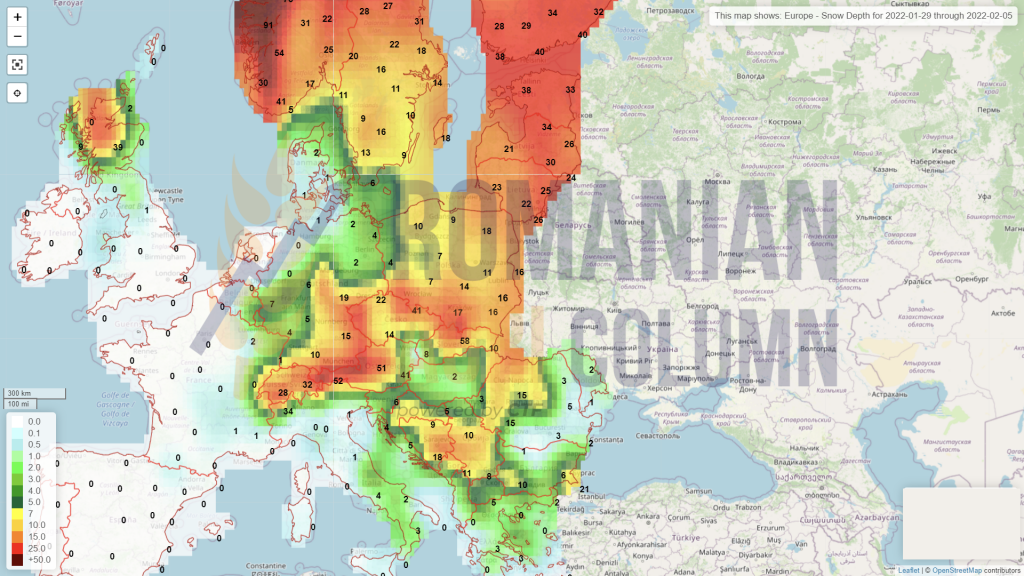

Last week, we recorded a moment when the weather caused the price of corn to rise, namely the cessation of activity in 7 ports in Ukraine. Thus, Chornomorsk, Mariupol, Mikolayiev, Berdyansk and Kerson closed operations due to snowstorms that impeded loading and piloting. Odessa and Pivdenny also halted operations and banned piloting. Bistro channels, Bug and Kherson channels are open. At the time this report is written, the activity has returned to normal, but the episode has created a positive price change due to inability to operate. The focus shifted rapidly to the port of Constanța, where corn evolved in price to the level of 243-245 EUR/MT.

There is still delivery pressure in Ukraine. About 20 million tons have to leave Ukrainian territory through ports, and the specter of war generates a much faster operational pace. Let’s hope that everything will calm down, although, analyzing the latest Russian movements, we have doubts about this.

The positioning of field hospitals and the supply of blood reserves indicate intention. However, Russian press releases received on official channels show for the first time a non-belligerent intention. But as we have learned from history, specifically from the author of “The Art of War”, Sun Tzu, “the whole art of war is based on deception.”

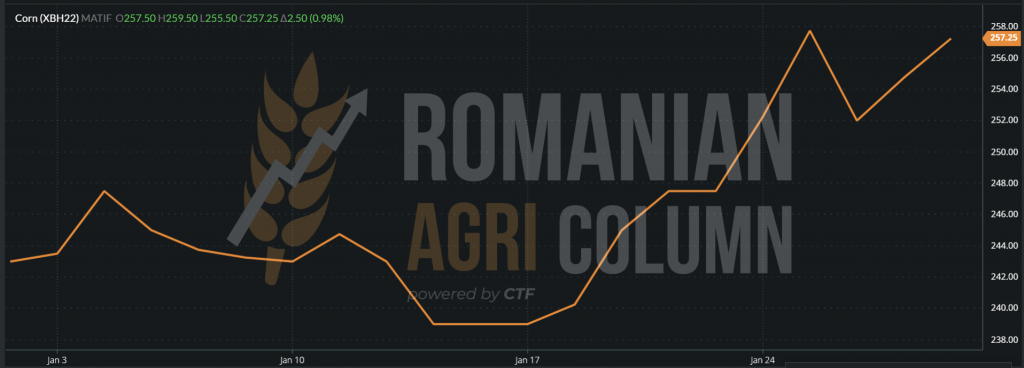

EURONEXT quotes corn up. The trading session of 28 January 2022 set the level with an increase of 2.5 EUR, up to 257.25 EUR. The XBH22 calculation matrix in normal crop condition works in parameters, i.e.: XBH22 – 10 EUR = CPT CONSTANȚA.

EURONEXT XBH22 MAR22 – TREND GRAPH FROM THE BEGINNING OF THE YEAR

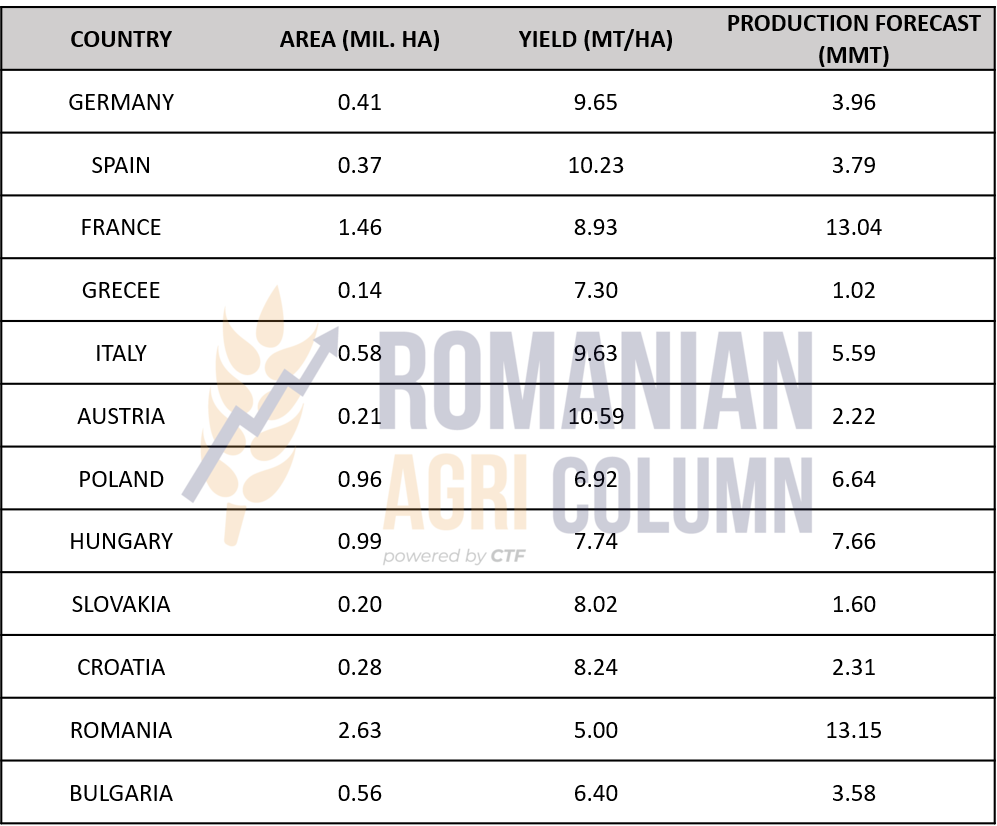

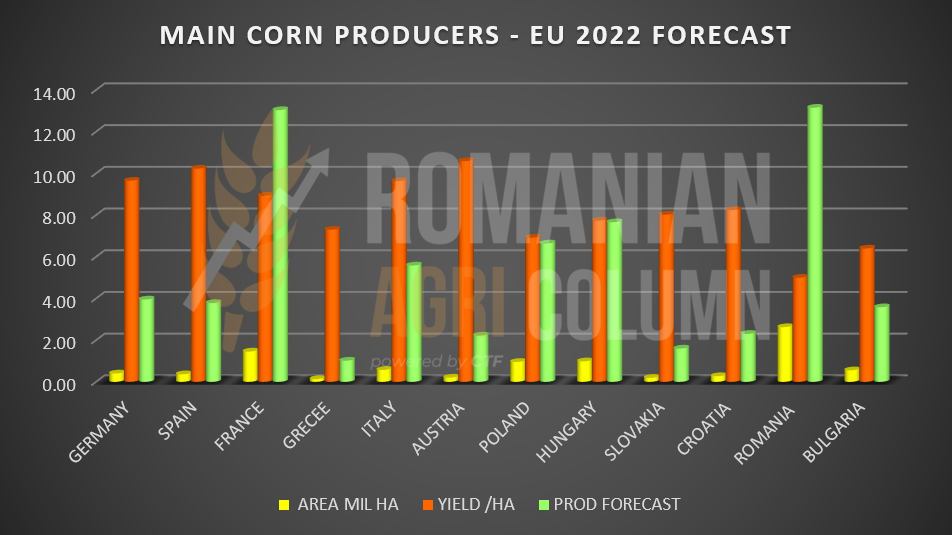

Regarding the forecast for the new maize crop, we have a deficit of about 3 million tons in the EU forecast, from 67 million tons in 2021 to 64 million tons in 2022.

The following are the main EU corn-producing countries, with the forecast for sowing, as well as the estimated yields per hectare:

Forecast Chart – Top EU Corn Producers, 2022

(area, productivity and forecast production)

GLOBALLY

South America continues the sad story of corn. After the sweltering heat wave, combined with a prolonged drought that persisted throughout South America, rains have arrived, but initial estimates of production degradation in Argentina show a 3 million-ton drop in production originally estimated at 54 million tons. We currently have a level of 51 million tons, but no one guarantees that this will remain the case. If we take into account the Brazilian loss, we are at a minus of 8 million tons, which gave support to the corn on the American stock market.

American corn continues to sell in the same strong trend, even though Mexico and Japan have canceled purchases from the 2022 corn crop.

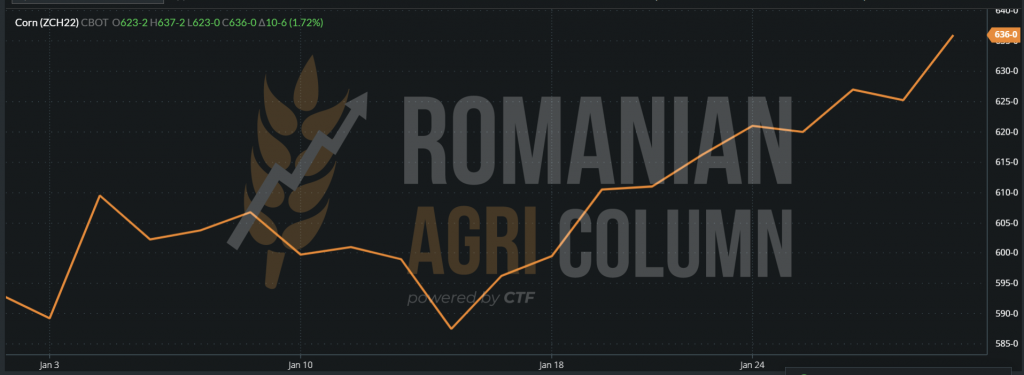

CBOT ZCH22 MAR22 – 636 c/bu (+10 c/bu = +3.94 USD)

CBOT ZCH22 MAR22 – TREND GRAPH JANUARY 2022 (until January 29, 2022)

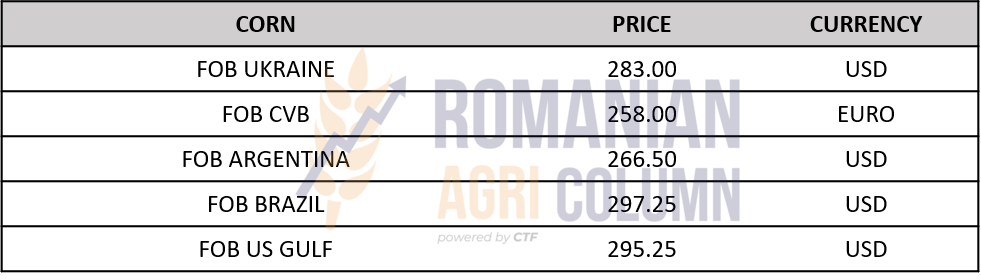

CORN PRICE INDICATIONS IN MAIN ORIGINS

ANALYSIS

- Again, the weather factor raises volume issues.

- The same factor raises the price of corn.

- The Black Sea region, on the one hand, and South America, on the other, support the price of corn.

- The story of the price of corn goes on. There may be more surprises in South America, as well as in the Black Sea Basin – the weather on the South American continent and political issues in the basin.

LOCALLY

The indications generated by the processors are starting to take on a much more obvious outline. AUG22 – 10 EUR (or -5 EUR in some cases) is already a norm in the market, thus leaving the time for farmers to set the final price. The port indicates a level of AUG22 – 15 EURO, but this level can be improved in the near future.

What we all need to understand in this growing rapeseed market for 2022 is that we are still at a level of uncertainty, which means that we are exposed to the Weather Market factor, the most unpredictable element of global agribusiness.

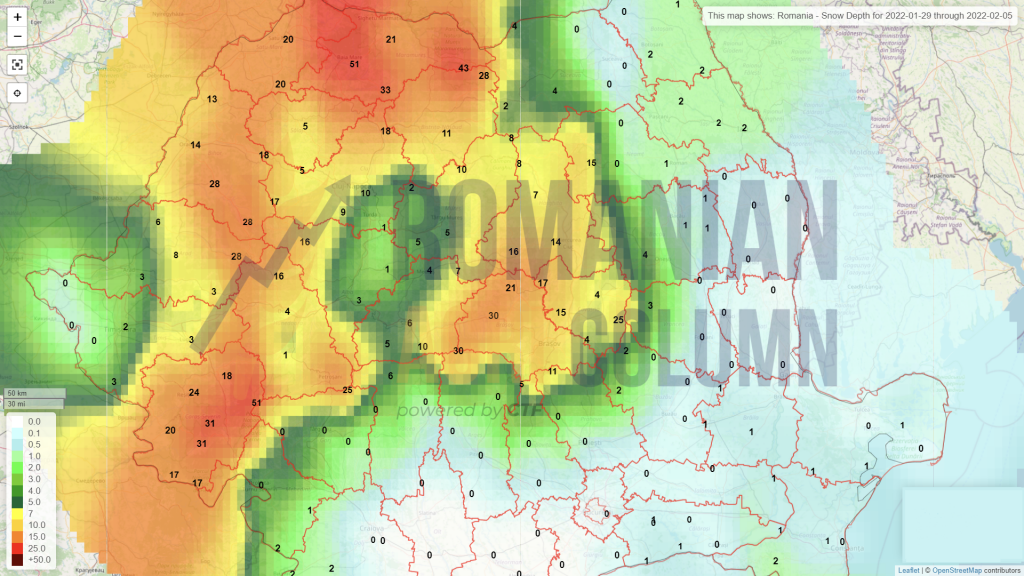

In Romania, at a level of 415,000-417,000 hectares sown in autumn, rapeseed is not in very good shape in some areas of the country. An uneven germination or even a non-emergance is easy to notice, especially in the area of the Carpathian curve and East of that. There, water, the vital element, has been missing for a very long time and we list regions from Vrancea, Galați, Vaslui and Bacău that are affected by this phenomenon of drought and lack of precipitation. Indeed, the curvature of the Carpathians stops rainfall, and if we associate this with negative temperatures of up to minus 15 degrees Celsius during the night, we have a picture with a not very pleasing prospect.

The weather is changeable, and what we see in terms of the weather forecast for February is not a positive thing at all. We are referring to the fact that we are still without precipitation and under a weather with positive temperatures, again, an abnormal thing for this time of year.

Thus, at this moment, we estimate that the level of the negative Premium will certainly decrease, and we may see a positive Premium, if things deteriorate in terms of forecasted crop levels. In other words, “AUG22 minus” can easily be transformed into “AUG22 plus”.

REGIONALLY and GLOBALLY

The indications of EURONEXT are closely correlated with the price of fossil energy and, in accordance with the latter, the prices of rapeseed follow the top-down trajectory with which we have become accustomed to. This time, however, the new crop was quoted at over 610 EUR, AUG22. The inverse crop is in favor of the new crop and we see it extracted from the range of 595-605 EUR in which it has been in the last period, a sign of pressure that arises from the weather factor, as well as from the assessment of stocks globally.

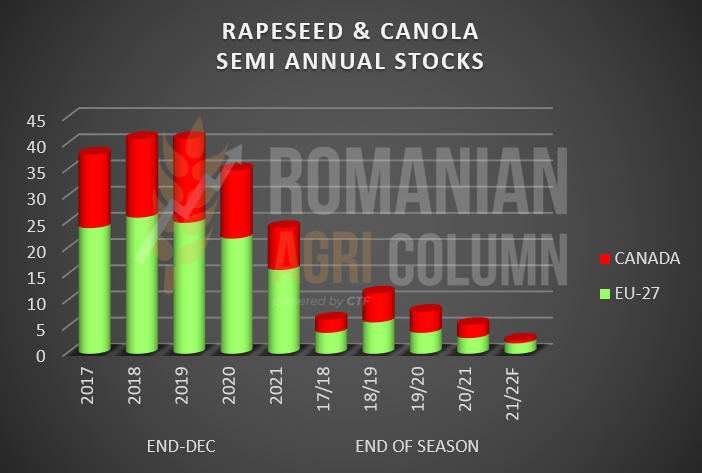

This is the outlook for the global situation in terms of rapeseed and canola stocks expressed per year for the EU and Canada, 2021-2022. F means Forecast and we notice its extremely low level, which indicates from the point of view of prices the perspective of the year in which we are.

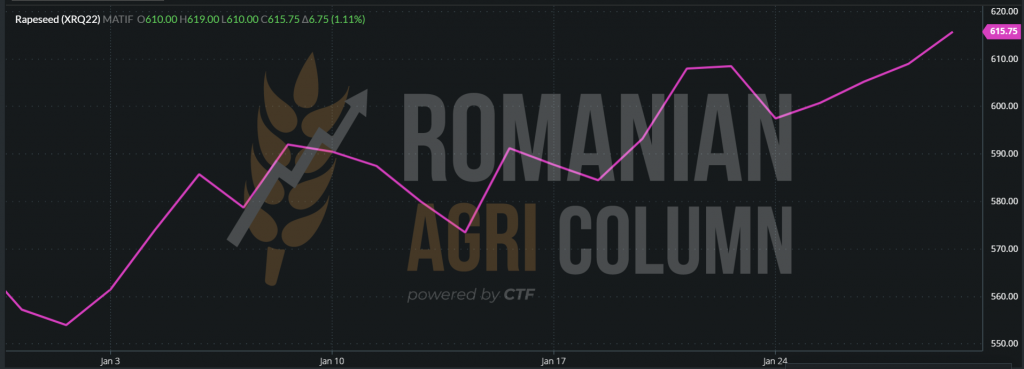

EURONEXT closes its trading session on 28 January 2022 at 615.75 EUR for the indication AUG22 XRQ22.

EURONEXT XRQ22 – AUG22 GRAPHIC | We are seeing sustained growth since the beginning of 2022. The main indicators remain weather and fossil energy.

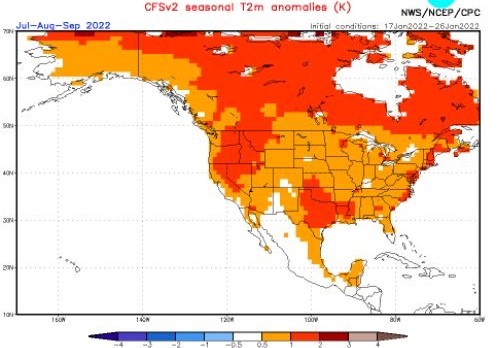

Before the usual analysis, we insert a weather forecast for the summer in Canada and we can already put an exclamation mark, if we consider April 2022 as the time to sow Canadian canola, due to the unusually high temperature forecast.

ANALYSIS

- Rapeseed remains a major source of interest in profit generation.

- The potential is expressed in weather + 2021 stocks + fossil energy.

LOCALLY

The local sunflower seed market is starting to wake up. Quotes are starting to rise, according to our estimates. The indicative levels in the CPT Constanța parity, as well as in the local processors, exceed the level of 680 USD/MT, which, converted at the favorable exchange rate following the strengthening of the American dollar, makes the price particularly attractive.

Demand is growing and we do not rule out the level of 700 USD/MT as an indicator for sunflower seeds in the next period. Summarizing the story of the seeds briefly, we highlight the low coverage of processing at European level, including at local level, as well as the availability of stock at national level.

Tension between sellers and buyers has generated anticipation. The refusal to market the seeds, the capitalization from the sales of wheat and corn generated this situation. But farmers who have waited have reason to believe these days that this wait has not been in vain.

REGIONALLY

Ukraine brings oil levels back to more than 1,400 USD/MT (1,405 USD/MT, to be precise). The demand generated by the lack of coverage of processors at the local level, associated with the growing tensions in the Black Sea basin increases the risk of stifling processing and, implicitly, supply. In this way, the balance is broken in favor of Ukrainian farmers. The factor of regional political instability also played in their favor. The owners of processing plants in Ukraine have decided to start supplying because of fears of conflicts, which are imminent in this period of time, in the context in which Russia threatens the borders of this country.

GLOBALLY

The support we see in the VEGOIL complex comes from two different directions.

The first direction is that of palm oil, which has a high price level, and certain export restrictions generated by Indonesia, which imposed a 20% lower export level on exporters due to lack of production. Production has been limited for some time du to La Nina, which brings storms to the region, thus reducing the operating window in the plantations. Another factor limiting production was the lack of staff due to the effects of the pandemic.

MPOC (Malaysian Palm Oil Council) estimates also predict a 5% drop in imports from India to just 8.2 million tons due to high prices and potential for further growth.

The second line of support comes from the soybean crop, which is experiencing a sharp decline in South America. Brazil is actually lowering its forecast daily, reaching now a minus of 14 million tons, associated with Paraguay, which decreases the forecast from 11 to 4.5 million tons and in the near horizon is also seen Argentina, which is already initiating in the region Santa Fe the process of calamity of the new crop.

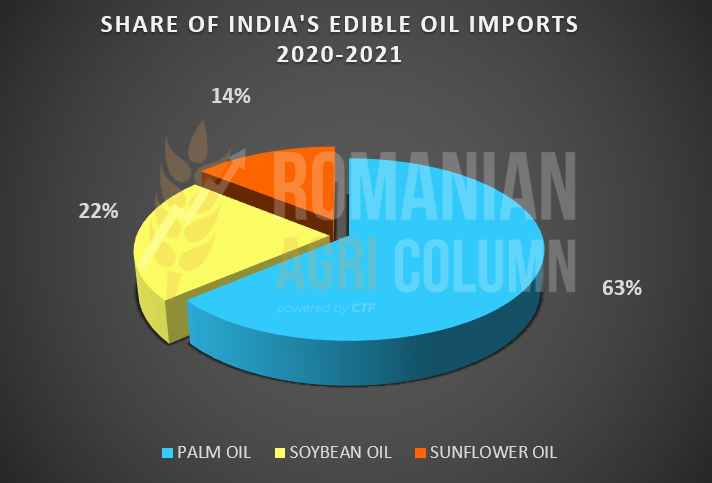

Sunflower oil has a share of 14% in Indian imports, according to the chart we insert below, the data being generated by the association of processors in this country.

SUNFLOWER AND OILSEEDS PRICES INDICATIONS VARIOUS ORIGINS

ANALYSIS

- In summary, the VEGOIL complex gives an expected boost to sunflower seeds.

- There is still liquidity in Romania, but it can dissipate very quickly due to the fact that Romania is the origin.

- We could easily see levels of 700-720 USD/MT for sunflower seeds in the near future.

- The combination of Weather Market (South America) and political (Russia vs. Ukraine) factors generates the much-anticipated rise in the price of sunflower seeds.

LOCALLY

Soybeans are gaining traction in price and we are seeing how levels of 650-670 USD/MT are already being practiced for batches waiting to be traded locally. Farmers are still waiting, boosted by soybean CBOT growth. But at the moment, the great interest is generated by the processing units in the countries West of Romania, and Hungary is an eloquent example in this respect.

GLOBALLY

Things are getting worse in South America, with Brazil being a telling example in this regard. After an extraordinary start in terms of the forecasted soybean crop, valued at around 144 million tons, they actually lose 10% according to the latest estimates, to the level of 130 million tons.

Paraguay loses more than half – from 11 million to 4.5 million tons.

So we have a minus of over 20 million tons of South American production, and things continue to get worse.

Authorities in Argentina, in the Santa Fe region, have begun receiving requests for crop calamities, in this case soybeans, which is an extremely strong indicator of what is to come.

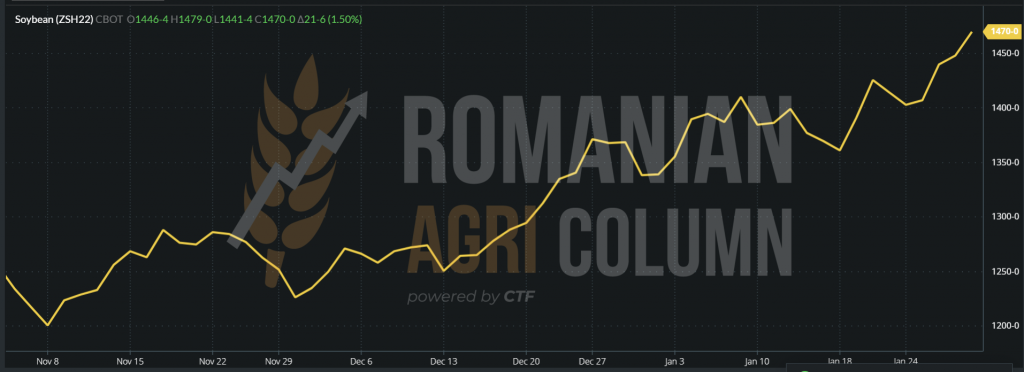

With the help of the weather factor, soybeans therefore return from that unlikely 1,200 c/bu, to the level of 1,470 c/bu for the indication MAR22 and 1,475 c/bu for the indication MAY22. Converted to USD, 542 USD – 441 USD = +101 USD

CBOT ZSH22 TREND GRAPHIC between November 8, 2021 – January 29, 2022

ZSH22 MAR22 GRAPHIC – 1,414 c/bu

Neither soybean oil nor soybean meal is inferior and we record the sequential growth.

ANALYSIS

- Once again, the weather factor influences us, despite the optimistic initial forecasts.

- Soybeans still has potential, depending on Argentine development, which, despite the rains, indicates obvious crop weaknesses.

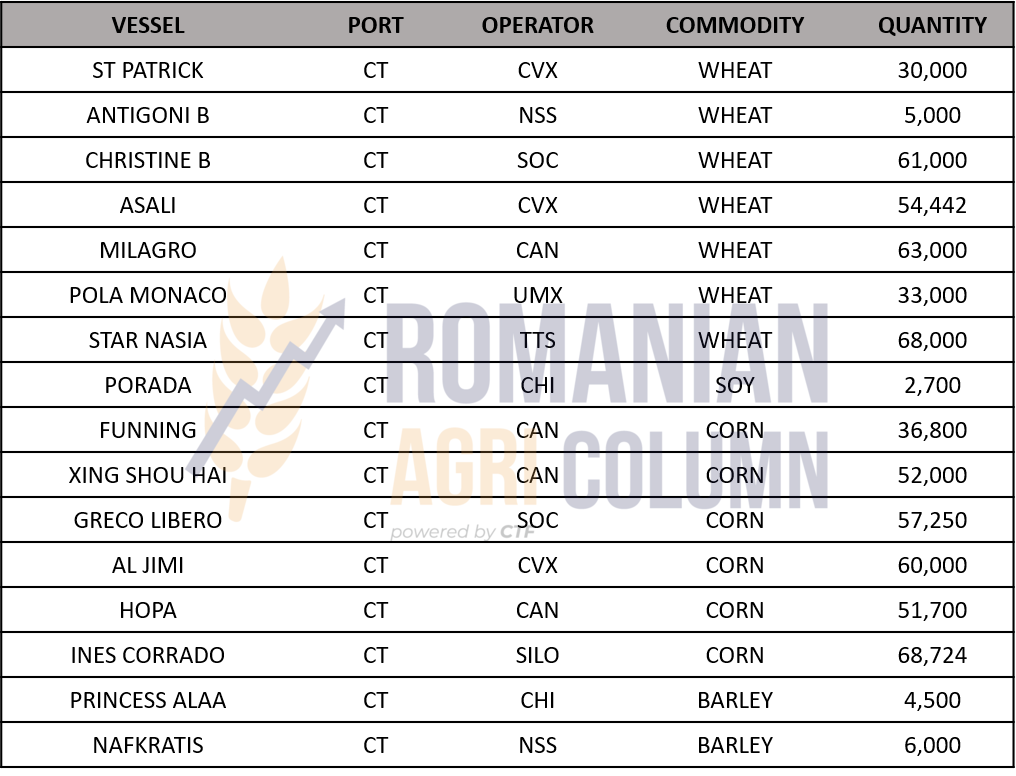

WHEAT = 315,000 TONS | CORN = 325,000 TONS

Who doesn’t love a strong dollar and a weak ruble these days?

90 USD BRENT | almost 87 USD WTI

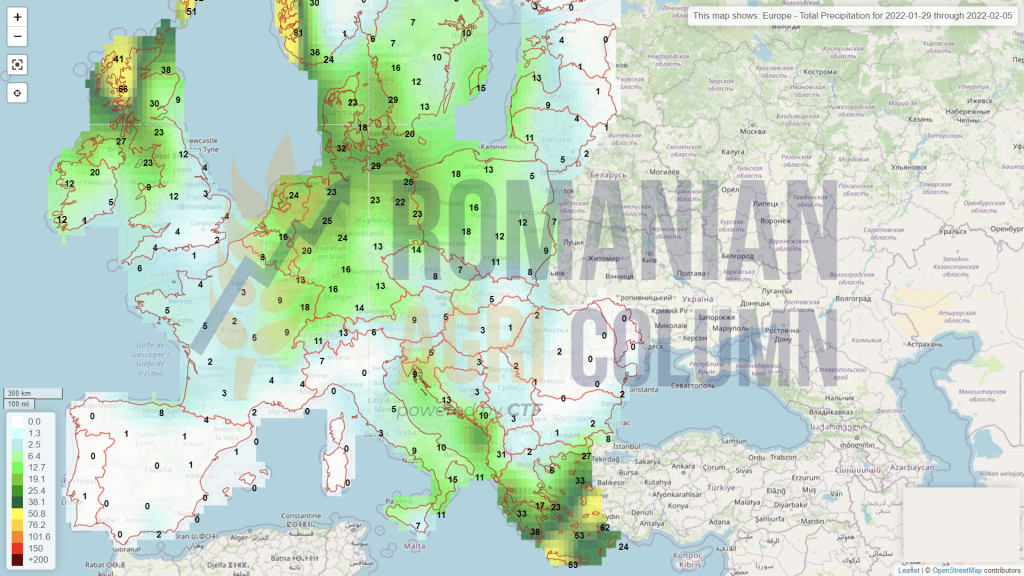

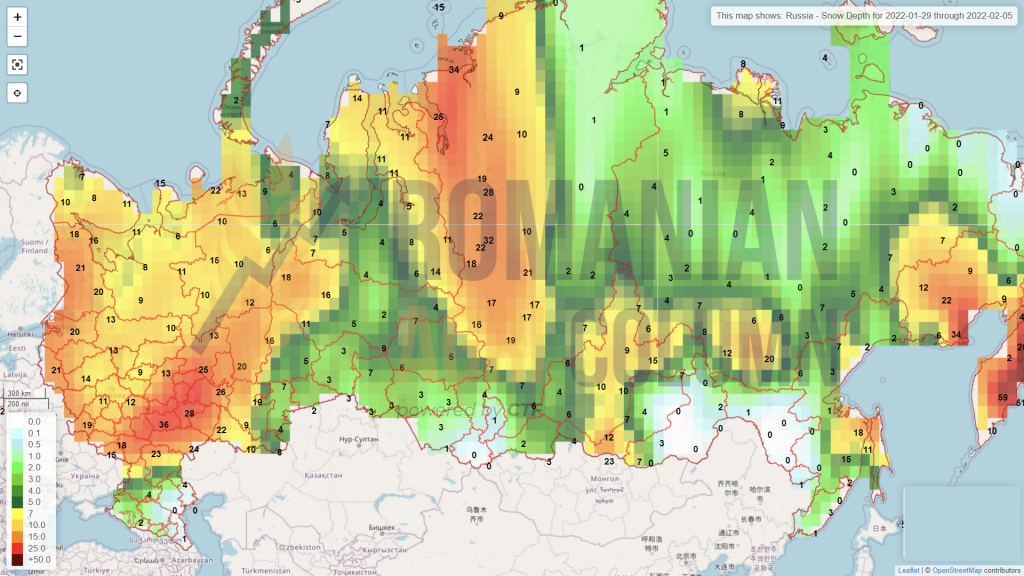

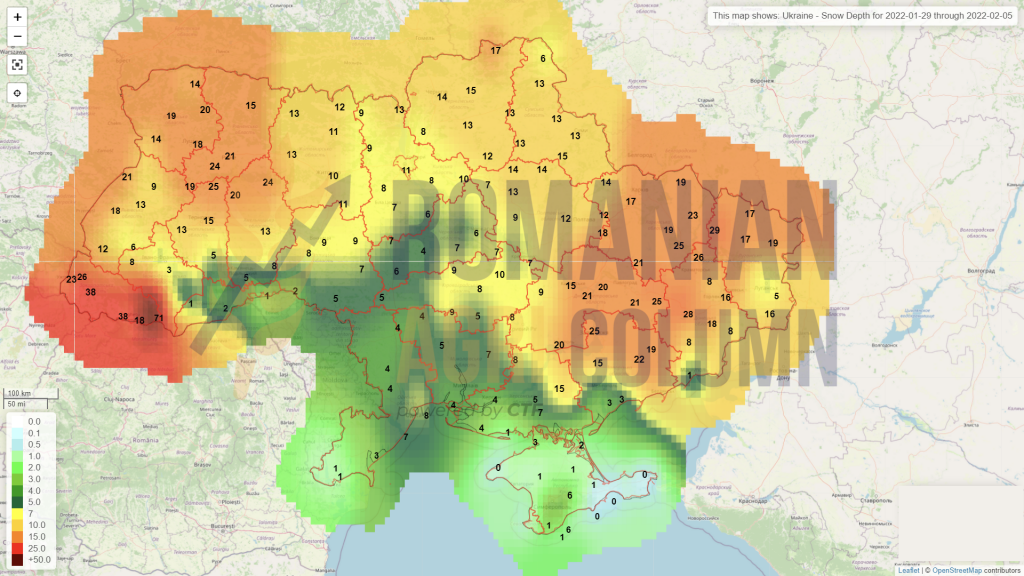

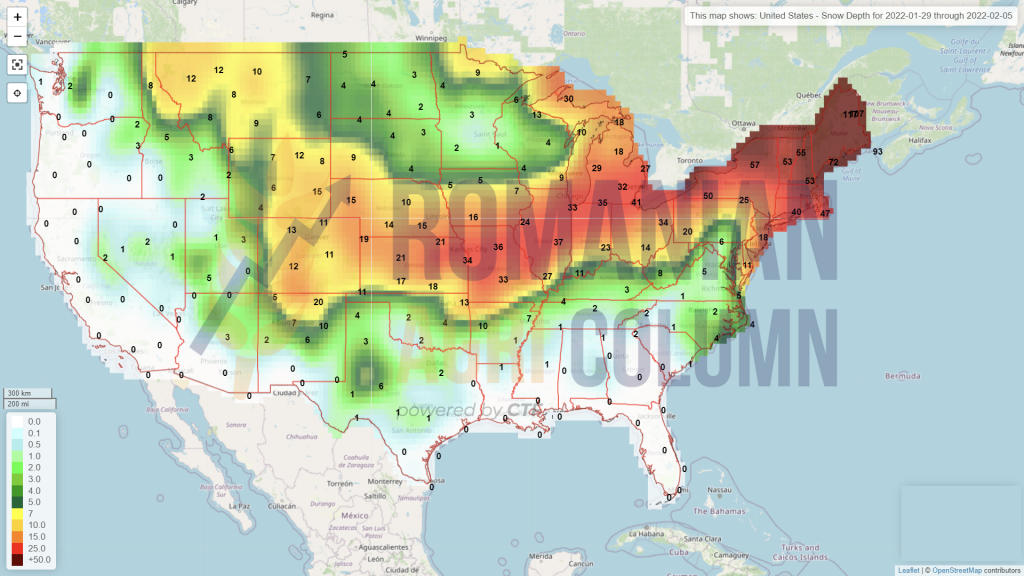

29 January – 5 February 2022

Romania (snow)

Europe (snow)

Europe (rain)

Russia (snow)

Ukraine (snow)

USA (snow)

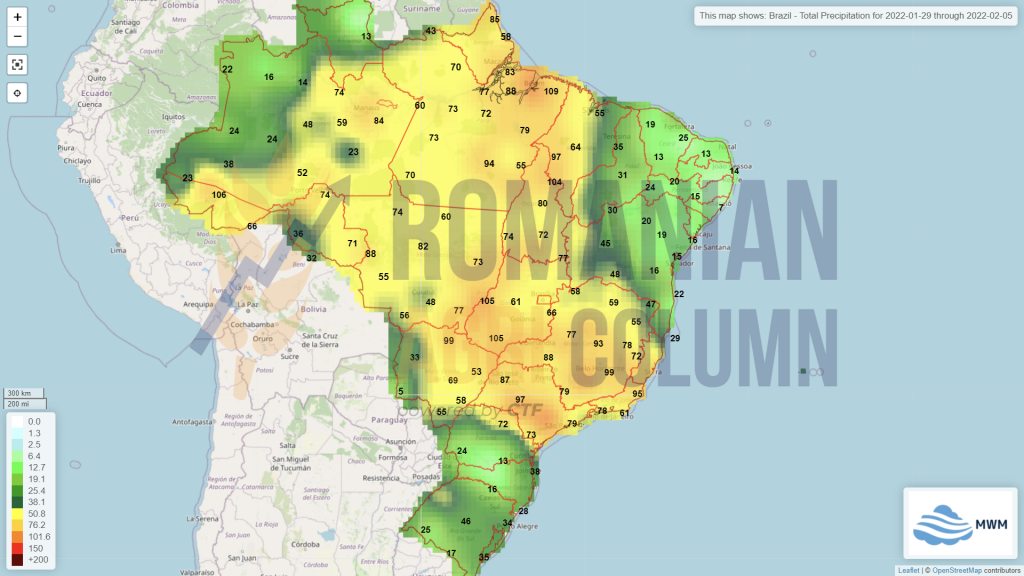

Brazil (rains)

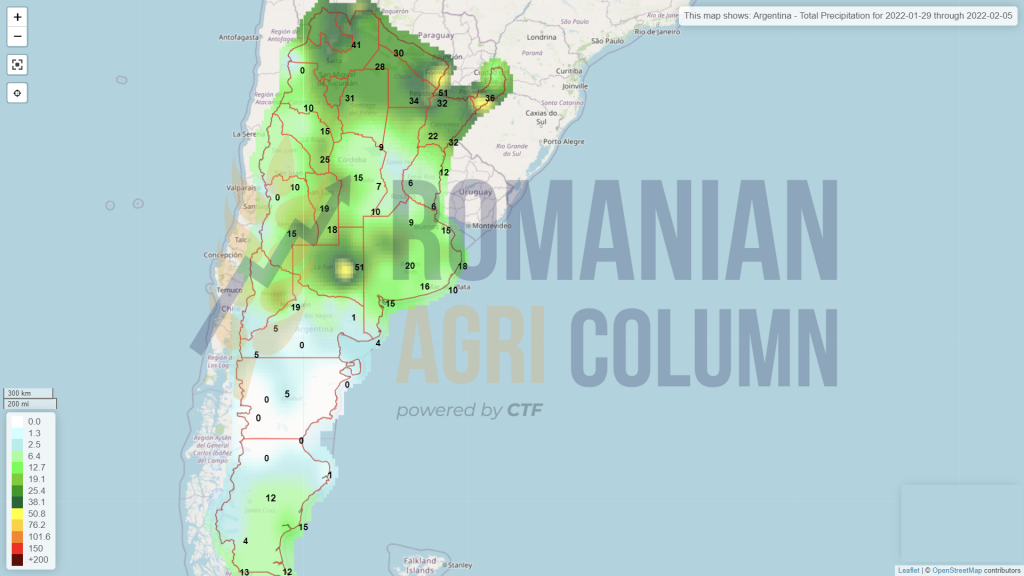

Argentina (rains)

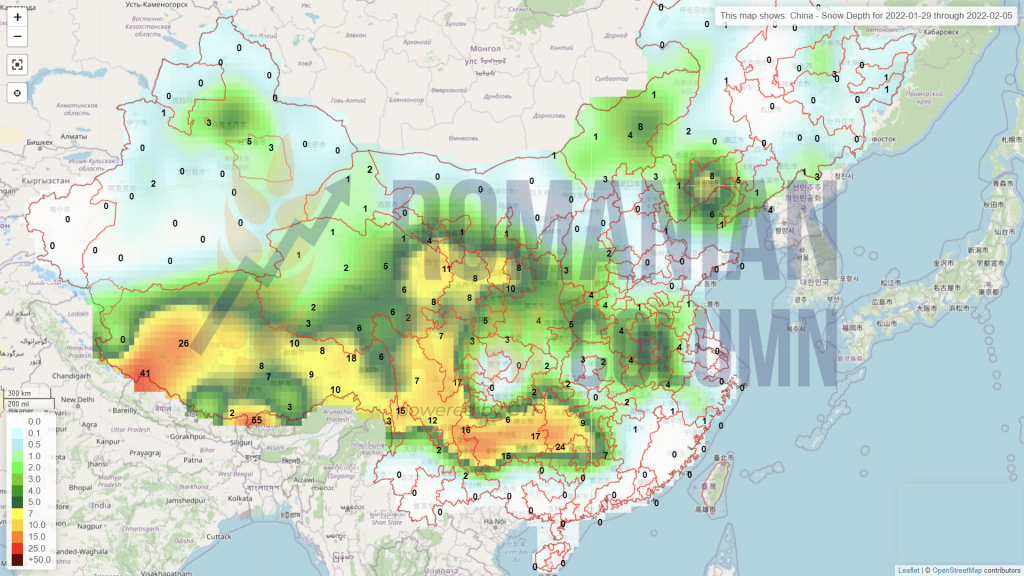

China (snow)

Australia (rains)