This week’s market report provides information on:

LOCAL STATUS

Wheat quotations in the Constanța CPT parity reached a level of 205-207 EUR/MT, in the CPT parity. Feed wheat has a difference of minus 7 EUR/MT within the discount term.

The new crop is valued at 197-200 EUR/MT and the feed quality discount is 10 EUR/MT.

CAUSES AND EFFECTS

The extension of the corridor has pushed wheat prices back to where they used to be. The tension generated by the uncertainty fueled the price in the physical market, but the world breathed a sigh of relief after the announcement made by President Erdogan himself, who also stepped into the 2nd round of the Turkish elections.

We understand the challenge of this year, which is composed of two factors: the drop in the price of some crops established at high costs in the fall of 2022 and the Ukrainian tsunami that is also manifesting these days at the level of the port of Constanța. But the Romanian farmers must come to terms with the idea of a balance being restored in the market, namely, the volume of the harvest associated with the strengthening in terms of the flow of the European solidarity lines are factors that balance the global market.

What was will no longer be, the return to normality also means a conscious assumption of some gaps from a financial point of view. But on balance, things are weighted by the previous season, when the establishment of crops in the fall of 2021 was at normal financial levels, and the galloping prices that followed from March 2022 brought incomes that many did not hope for.

In other words, we are approaching a normality marked by volatility and we have to look at the figures that indicate an 80% drop in the price of gas compared to September 2022, a 60% drop in the price of fertilizers compared to the same period and implicitly a cost reduced diesel by 40%. These are the factors we need to look at and indicate our future in terms of pricing vs spending.

Anticipation is also part of the tactical arsenal to secure the business and we indicate once again the large volume of goods that will enter the port of Constanța in the near future. And if we do not secure and deliver, in the campaign, on harvest pressure, the problems will become acute, the logistics and the drop in the price of wheat will then be extremely big problems.

REGIONAL STATUS

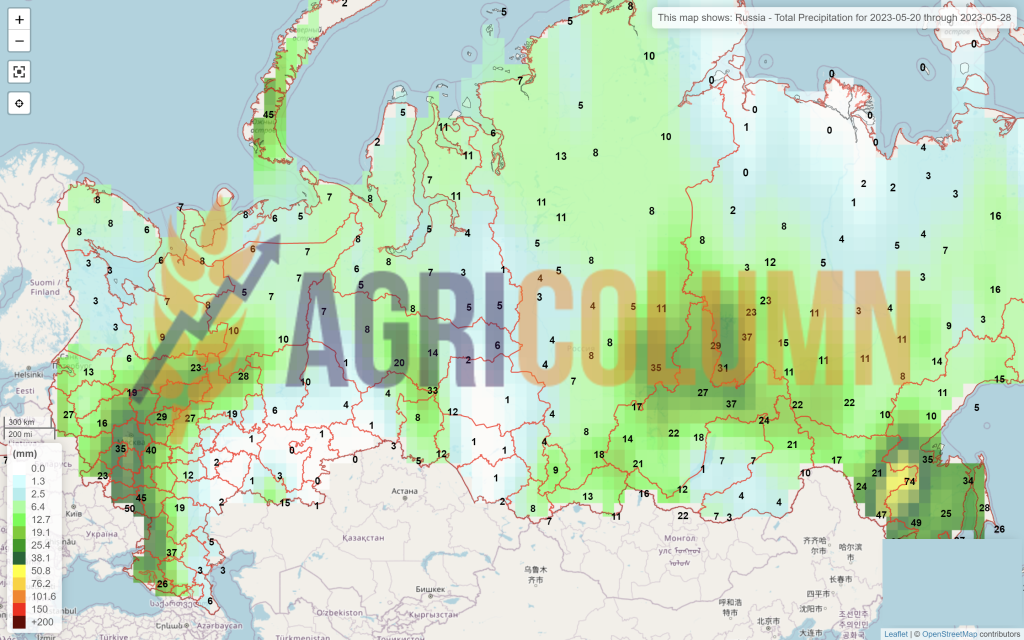

RUSSIA. The wheat problem, however, comes from Russia, which is seeing a revival of crops and has a high degree of satisfaction with spring wheat. Russia will contradict the USDA as they do every year, so they will have much higher production than the USDA estimate and will be left with a lot of unsold wheat from this year, about 20 million tons. Lower production in Russia, lower EU consumption and better export.

However, Russia has problems with the export of wheat; just 0.68 million tons in May so far. 45 million for the 22-23 season is too far a target. 38 maybe 40 million can still be reached. But the domestic stock will exceed 20-21 million tons, which inevitably leads to a drop in the price.

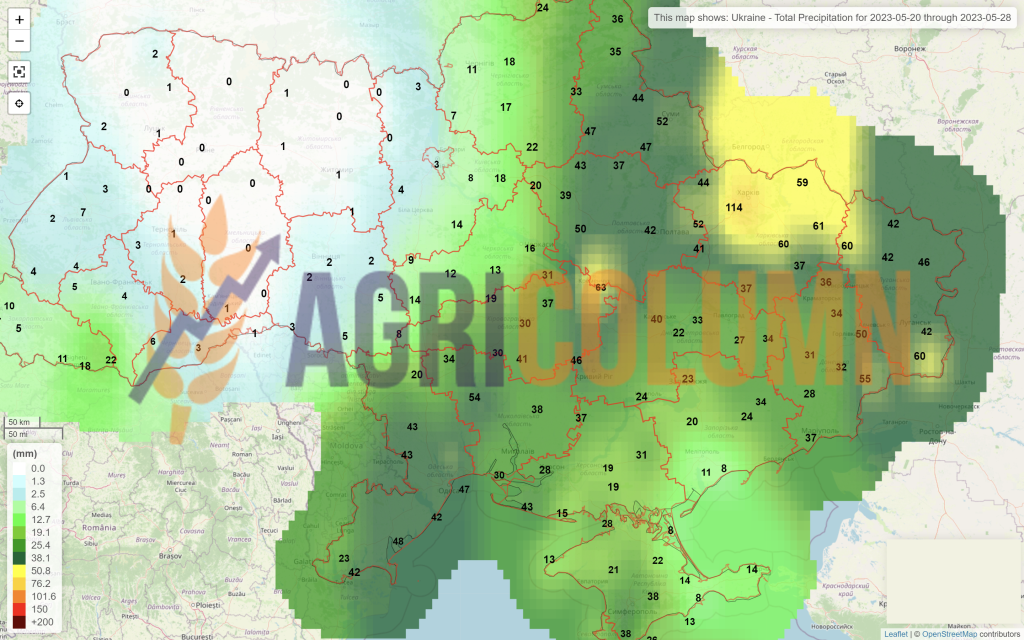

UKRAINE is in the midst of a spring planting campaign and the rainfall regime is helping established crops in autumn 2022. Forecast volumes could be much higher than USDA guidance.

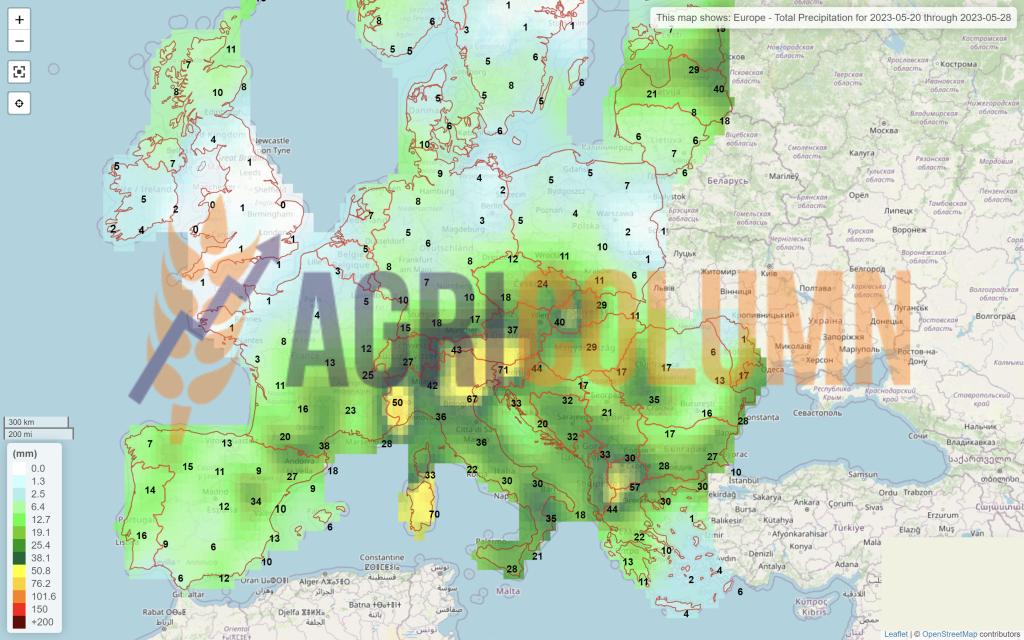

The EUROPEAN UNION is doing well at the moment. Punctual degradations, but not severe, are manifested in France. Crop conditions eased slightly in the week to May 15, with minor reductions noted. But overall, the main grain crops remained in good shape compared to last year. About 93% of the milling wheat crop was rated good to very good, down from 94% last week and compared to 73% in 2022.

BULGARIA: Wheat stocks are around 2-2.3 million tons, of which 500,000-800,000 tons will be exported by the end of June, so exports will reach 3.5 million tons for the whole year. Bulgarian and Romanian government officials have called for more control over imports of goods from Ukraine and requested financial compensation from the European Commission (EC), claiming that the flow prevented local farmers from selling their volumes. The European Commission reported Bulgaria’s current wheat harvest at 6.17 million tons and estimated future production for 2023/24 at 6.43 million tons.

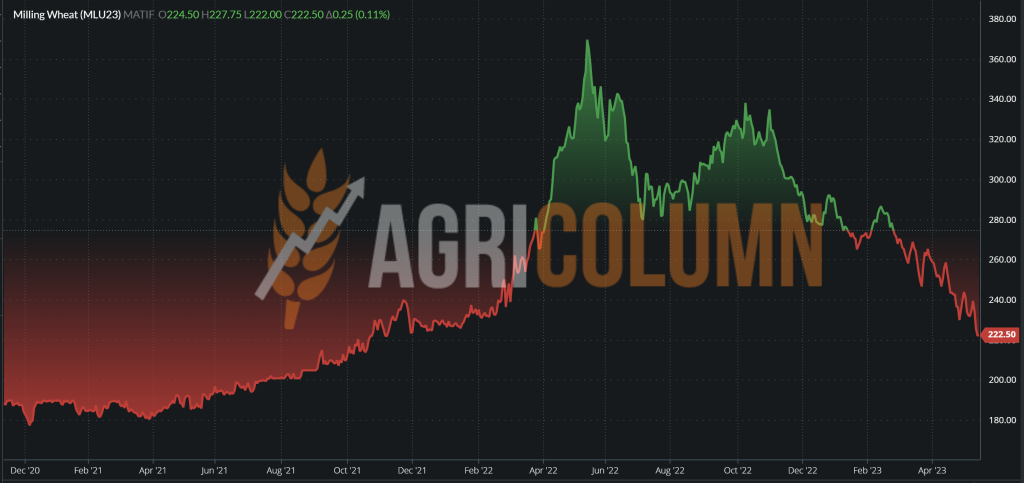

EURONEXT – MLU23 SEP23 – EUR 222.5 (-EUR 12 vs. last week)

EURONEXT WHEAT TREND CHART – MLU23 SEP23

GLOBAL STATUS

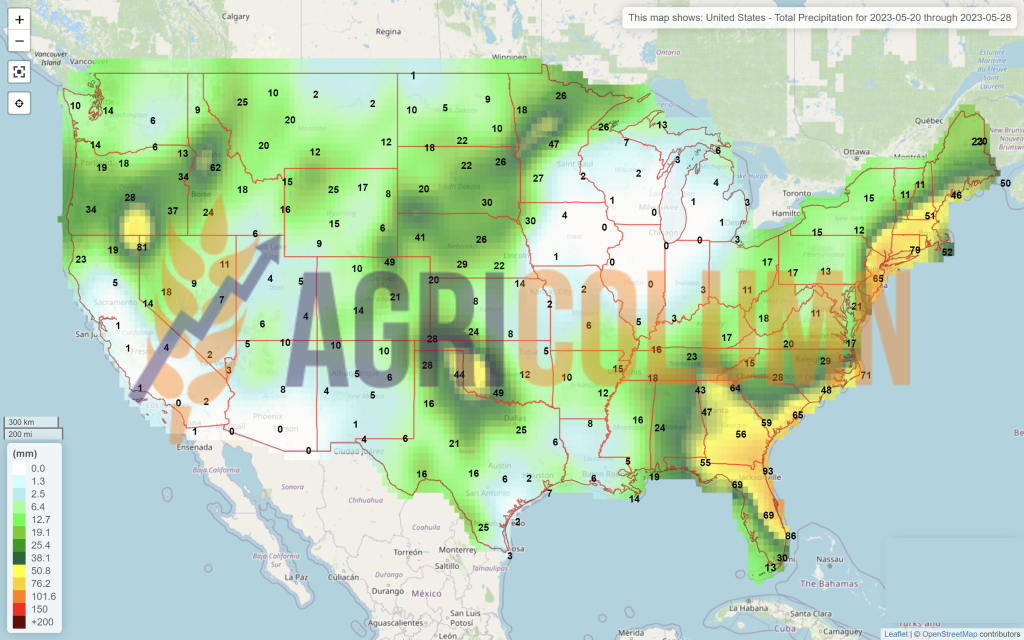

The US remains flat on winter wheat, while seeded spring wheat is gaining vegetative traction. The abandonment rate of wheat seeded land in Kansas is increasing and the overall US winter wheat rate is dropping dramatically from “Best of five years” to “Worst of five years”.

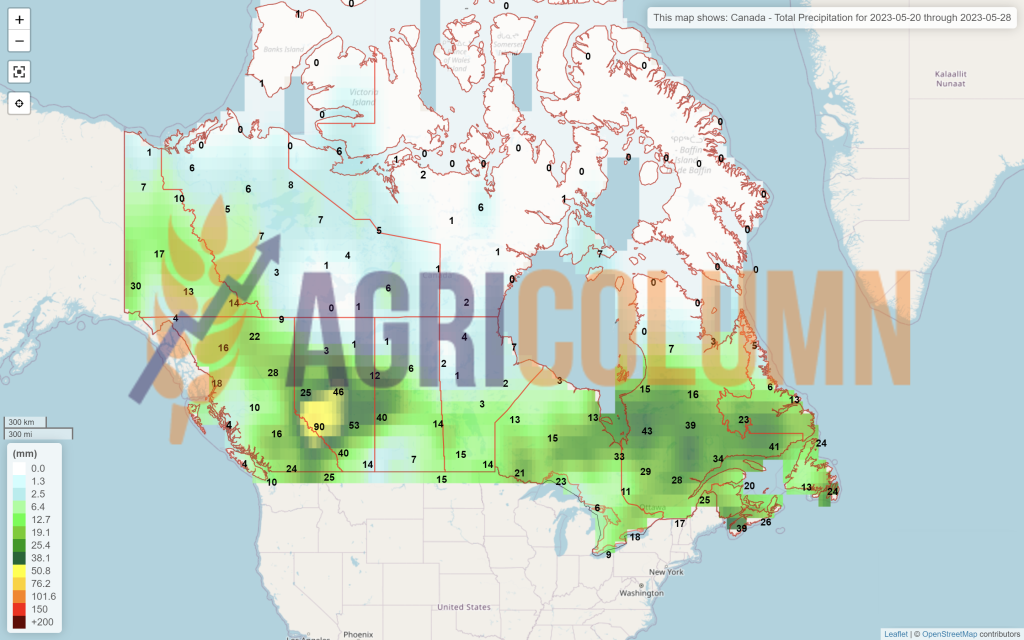

CANADA, despite the wildfires, remains an offset to the US winter wheat crop, 37 million is still in the current forecast.

INDIA remains at 110 million tons as the previous week. A potential delay in the monsoons could keep temperatures high, leading to problems.

CBOT WHEAT – ZWU23 SEP23 – 646 c/bu (-25 c/bu = -9.5 USD/MT vs last week)

CBOT WHEAT TREND CHART – ZWU23 SEP23

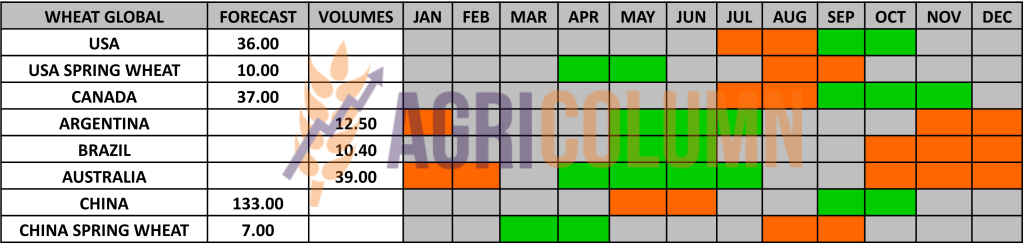

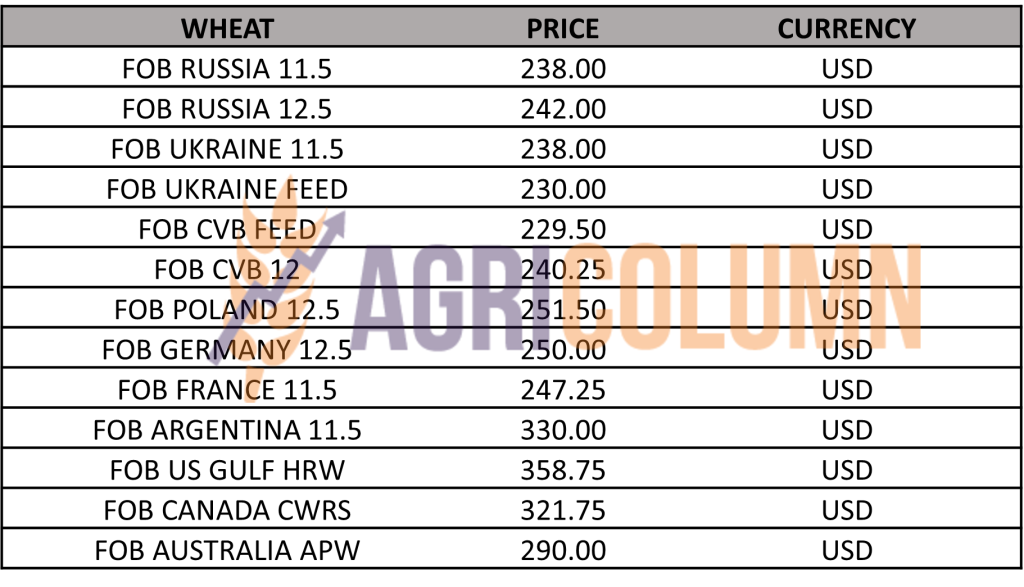

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

CAUSES AND EFFECTS – THE STORY

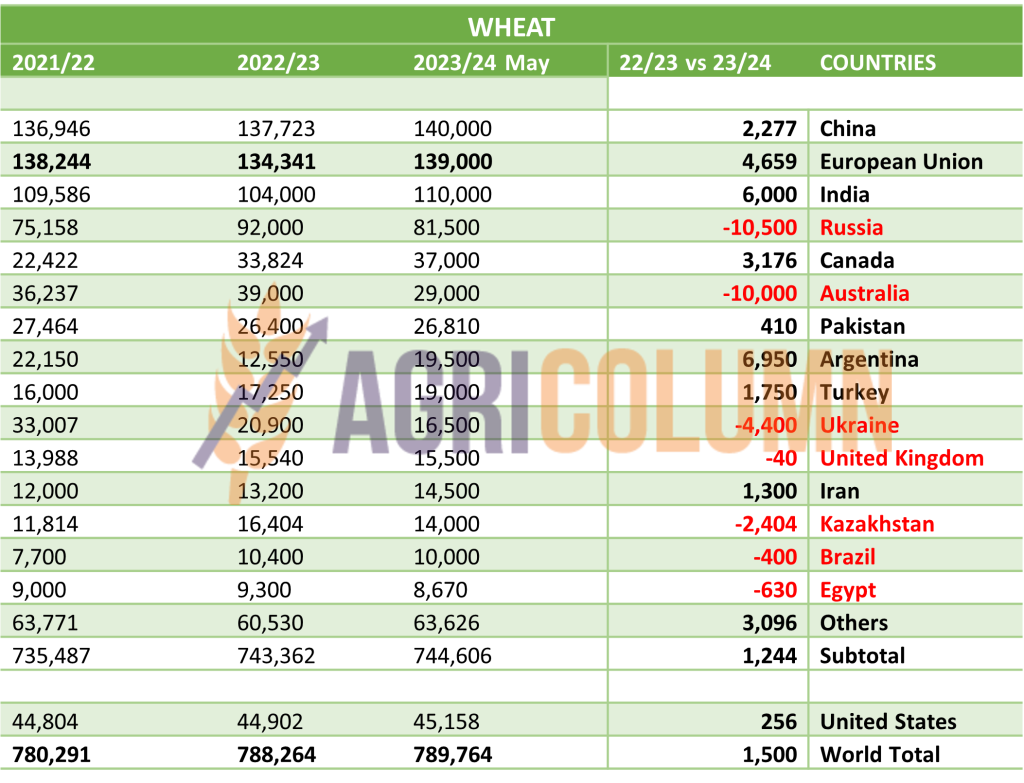

The global wheat production forecast shows us the richest year in the last 6 years. Thus, we have a level of 790 million tons. The numbers speak for themselves and the forecasts are still very conservative. More than 10 million tons fell from Russia and another 10 million tons from Australia.

But, in the overall figures, we have to make some personal notes, as follows:

- Russia will generate more than 81.5 million tons of cargo volume. This is where the specific reluctance of the USDA comes in, not wanting to fuel another downward spiral in wheat prices based on higher volume in Russia.

- Australia is a working hypothesis for now, the disappearance of the La Niña phenomenon from the landscape and the entry into ENSO does not necessarily mean a production that drops steeply by 25%.

- Ukraine is estimated to be extremely reserved, but I am absolutely convinced that they will raise the level and generate a volume close to 18 million tons.

And now, some explanations that will generate a transition to a period that we are all waiting for, namely the wheat harvest in the northern hemisphere:

- Russia will remain with a non-exported volume of about 20 million tons. The extent of unsold stocks is clearly seen in the actions of the federation. The devaluation of the ruble and the lowering of the export tax are the primary elements. The threshold was set at 212.5 USD, and the ruble reached a parity of 80/1 USD. All the noise about the floor price of 250 USD/MT in FOB parity for the new crop has died down and we are already seeing 240 USD/MT FOB becoming real and extremely present in the bids. But buyers don’t want to commit yet.

- Turkey anticipated the large volume of cargo from the Black Sea basin and barricaded itself under the cover of a 130% import tax. This is to enable local farmers to sell their produce first, thus managing the current price potential.

- The corridor remains open as a sample of Erdogan’s craftsmanship. But here things are extremely easy to understand. Putin does not like a regime change in Ankara, the country that has one foot in Europe and one in Asia, a real giant jailer that holds the keys to the passage through the Bosphorus. Erdogan needed this facility to present to Turkish voters, to present this to them in the form of an all-powerful Sultan with growing and developing regional bargaining power. To be fair and give Erdogan credit, he steered Turkey’s interests throughout the conflict so that he became a primary beneficiary of the interests of both parties involved, Ukraine and Russia. He led them along the path of Turkey’s pecuniary benefit with utmost skill.

- The volume problems in the US are compensated by the Canadian neighbors, and these exalted news about the export of Polish wheat to the US have no foundation other than the journalistic one. There was effectively very little arbitrage between origins. We are only talking about two ships and nothing more. How can we believe the bombastic headlines that the US is importing wheat because of the drought? It’s just a matter of supply and demand. In other words, someone local in the US agreed on the price for the quality offered and thus purchased 2 ships of wheat. That is all, for you cannot conceive of a country like the United States not having wheat at this time. If that had indeed been the case, the CBOT would have skyrocketed.

- Also, an attempt was made to create another artificial headline, namely that water is being brought in by tankers in France and that the drought is deep. No way, there we are talking about a small area located in the Loire valley, in a wooded area. French wheat looks very good and I have described it above.

The world needs wheat, the world needs wheat at a reasonable price. Under these conditions that I have described on the wheat route, high crop volume, declining levels of crop establishment inputs, why would there be a need for very high prices? Harvest time will certainly be delayed by 12-15 days in the Northern Hemisphere, Europe, Ukraine and Russia, but when it starts, the harvest pressure will not be late either. Pressure to which logistics is invariably added, which will, in turn, leave deep traces in the sellers’ accounts.

LOCAL STATUS

The price indications of feed barley decrease to the value of 175 EUR/MT in the CPT Constanța parity.

REGIONAL STATUS

THE EUROPEAN UNION. The harvest potential decreases at the Union level from 51.6 million tons to the value of 49.9 million tons, a minus of 0.7 million tons.

UKRAINE has reached 0.76 million hectares of spring barley sowing level. 0.16 million hectares less than in the previous season.

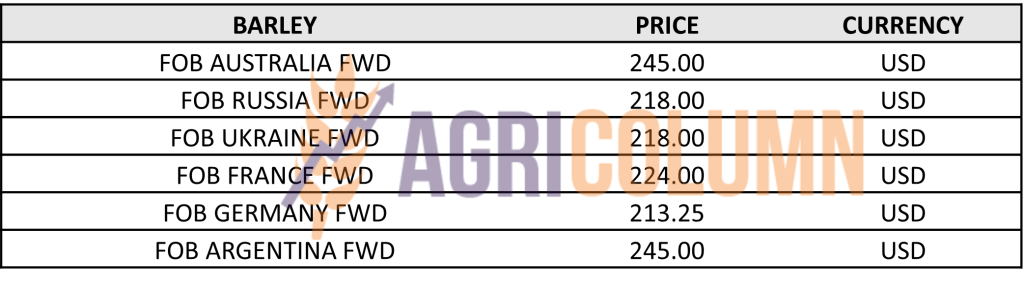

BARLEY PRICE INDICATIONS IN MAIN ORIGINS

GLOBAL STATUS

No essential changes.

LOCAL STATUS

Corn price indications remain at the level of 195-198 EUR/MT for the old crop in the CPT Constanța parity.

The price of the new crop drops to the value of 175-180 EUR/MT in the CPT Constanța parity.

CAUSES AND EFFECTS

Every day that rain falls, the price of corn changes. Because the rains in May are the most beneficial for the Romanian corn crop. And the precipitation conditions continue, associated with a month of June that will not excel in terms of temperatures, which will keep the moisture in the soil at optimal levels for the development of the corn crop.

And this will only potentiate a price future without upward trends. I was arguing that there would be areas where farmers would get 150 EUR/MT FCA. Here we are already there, which means that those who understood our messages have secured 3-4 tons of corn per hectare through forward sales.

REGIONAL STATUS

THE EUROPEAN UNION remains in the same forecast regime, between 63 and 65 million tons, aggregating the indications of reputable analysis houses as well as the data of the European Commission.

In France, corn planting continued to progress slowly, somewhat behind previous years. As of May 15, planting was 88 percent complete, up from 79 percent last week and well below the 97 percent completion rate seen last year and the five-year average of 93 percent for this time of the season. Spring planting has been delayed in many regions of France due to persistent rain, leaving many farmers with much of the crop yet to be sown.

UKRAINE reached a sowing level of 3.3 million hectares, down 0.58 million hectares compared to the same period last year. But the delay is caused by precipitation and recovery is possible.

EURONEXT CORN – XBX23 NOV23 –216 EUR (-6 EUR vs. previous week)

EURONEXT CORN TREND CHART – XBX23 NOV23

GLOBAL STATUS

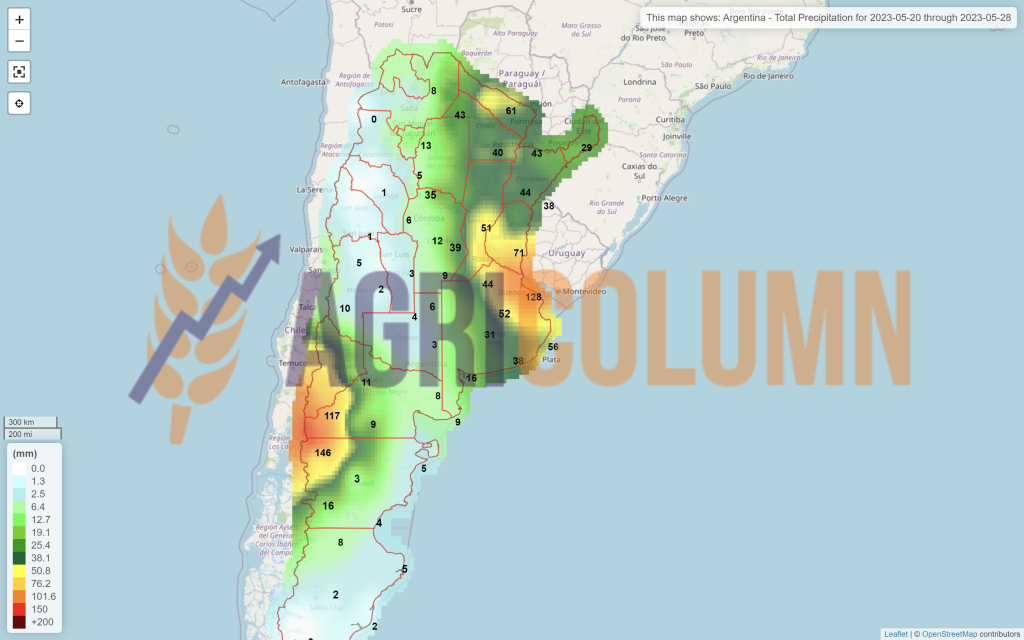

ARGENTINA is harvesting, and BAGE (Buenos Aires Grain Exchange) indicates 36 million tons, a volume very close to the USDA estimate.

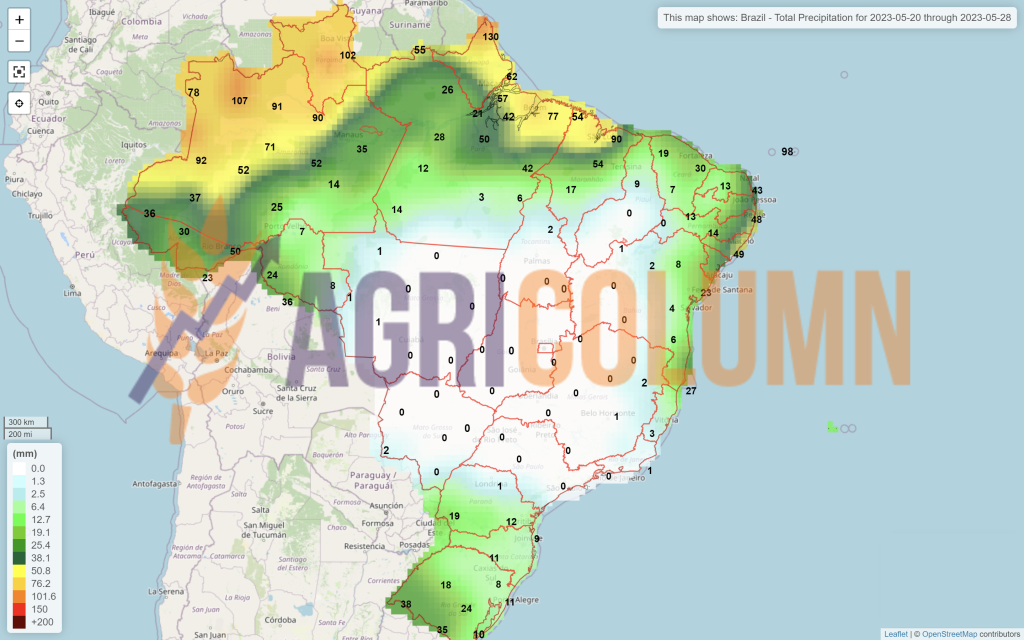

BRAZIL remains unchanged at this time, 130 million tons, Safra + Safrinha aggregate volume.

The US is still seeding, and the projection of 388 million tons remains unchanged.

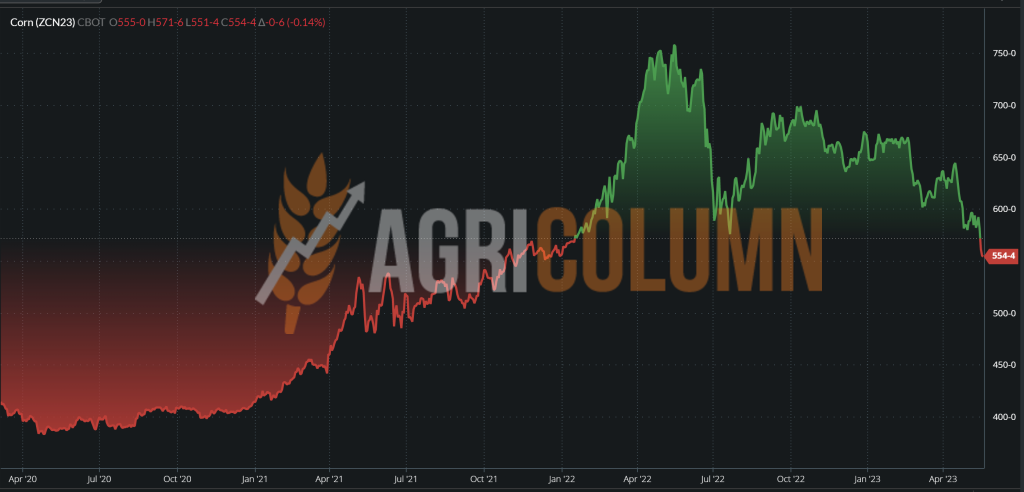

CBOT CORN ZCN23 JUL23 – 554 c/bu (-30 c/bu = -11.80 USD/MT vs. last week)

CBOT CORN TREND CHART – ZCN23 JUL23

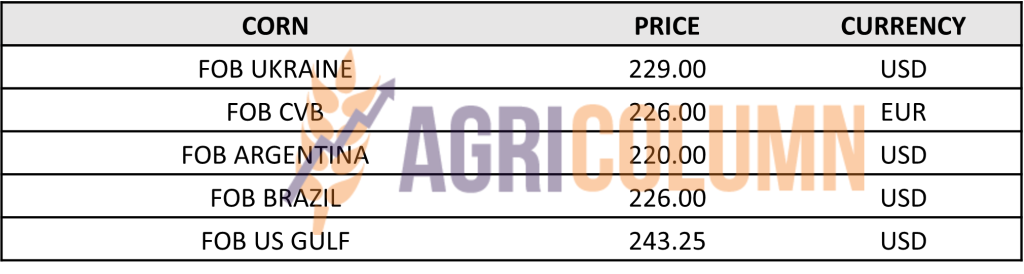

CORN PRICE INDICATIONS IN MAIN ORIGINS

CAUSES AND EFFECTS – THE STORY

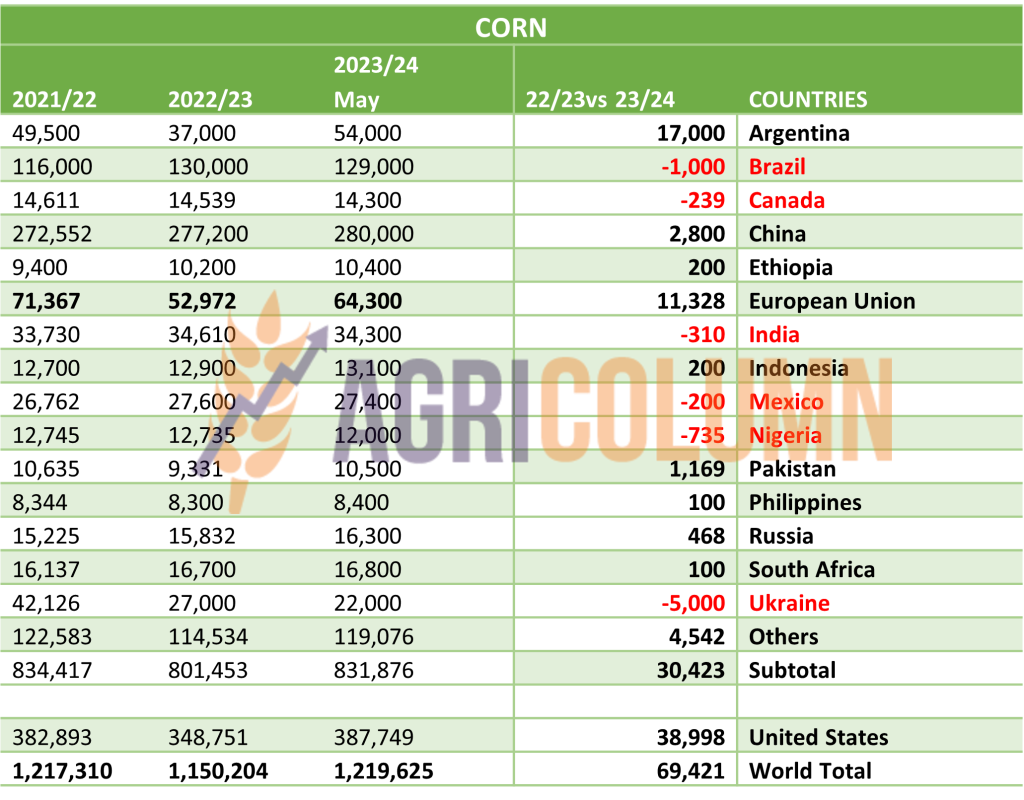

The global corn production forecast is one that indicates volumes that have not been reached in previous years. More precisely, we are talking about volumes of 1,220 million tons globally, with a return of the maize crop in terms of volume in the Northern Hemisphere and very good forecasts for the Southern Hemisphere.

Of course, there is still a long way to harvest, but an additional 70 million tons in the global basket (global basket), of which 39 million more are forecast in the US alone, represent figures that give consistency to the forecasts.

And as the numbers speak for themselves, the table below is representative of the 2023-2024 season:

- The European Union will no longer be a rock due to drought this season, rainfall and a cool June are prerequisites for a rebound harvest.

- Ukraine is credited with only 22 million tons, but this forecast is sure to improve.

- Argentina will return to the area of 54 million tons of production volume, this fall precipitation is forecast in this country that crosses the southern hemisphere.

- Russia is also certain to rise to over 17 million tons, with an export potential of 6-7 million tons.

- The USA, with its 388 million tons, has a surplus of 39 million tons.

- Brazil has a decrease of 1 million tons, but there is still time to confirm or deny.

After crunching the numbers, keeping in mind the weather factor as well as supply and demand, let’s try to forecast a corn price path.

- The European Union will still need corn and Ukraine will still be on the books. The extension of the regulation 870/2022 stemming from the association agreement will make the transit of Ukrainian goods to be mainly towards the Union.

- The US will experience a cool June, forecasts indicate, which is beneficial for maintaining soil moisture in the corn crop. And precipitation is estimated in the next period in the American Corn Belt (The Corn Belt).

- Brazil is an extremely serious competitor for the US, and this competition in sales gives buyers a real win.

- The most powerful buyer is China, which has up to this moment, a volume of over 8 million tons purchased. The road to 28 million tons is long, but China has well anticipated global volume forecasts by canceling many US purchases.

We therefore have in front of us a scenario governed only by the weather at the moment, as the cargo flows are well defined. China will focus on Brazilian corn, after which it will change its logistics channel to Ukraine. This is an extremely clear sign that Putin will not be able to have room to maneuver with the grain corridor. It will suffocate, but it won’t be able to close it. But when it comes to corn, Ukraine will also have the option of China, apart from the European Union, which will try to capture the cheap goods for its own supply.

The US will have to find its own export and consumption formula. And in the recipe we see only one option, i.e. a competitive price.

The weather will be the arbiter of the corn price in the next period, but for now it has not come out in the field. It’s raining outside and the crops are growing, June will be cool, so the Weather doesn’t want to get involved at the moment. Chances of hellish heat in mid-July and then August are there, but we’re not in a close enough area yet to draw any conclusions.

LOCAL STATUS

The indications are maintained on the same calculation formula for the goods delivered in CPT Constanța parity, namely AUG23 minus 40-45 EUR/MT. Processors guidance remains at the level of AUG23 minus 50-55 EUR/MT, DAP processing units.

CAUSES AND EFFECTS

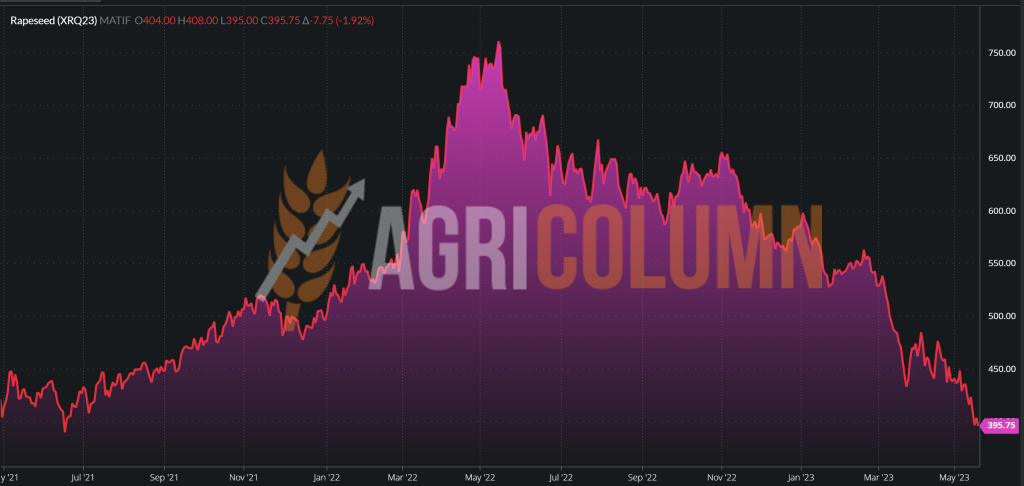

The crop prospects in the Black Sea basin and the European ones are continuously putting pressure on the rapeseed price. Thus, the premise of the AUG23 indication has already been created, which is at the level of EUR 400 and below this threshold. Nothing can generate any change in the rapeseed price trend, price compression comes exclusively from the volume ratio associated with global supply and demand factors, as well as rapeseed partners Vegoil and the natural correlation with oil.

EURONEXT RAPESEED – XRQ23 AUG23 – 395.75 EUR (-20 EUR vs. previous week)

EURONEXT RAPESEED TREND CHART – XRQ23 AUG23

REGIONAL STATUS

The EU remains in the same volume forecast of 20.5 million tons, to which we must add the impact of unsold stocks.

RUSSIA remains at the forecast level of 3.8 million tons.

UKRAINE will generate a volume of 3.3-3.4 million tons, but things could change in a positive direction, towards the figure of 3.5 million tons.

GLOBAL STATUS

CANADA remains at the forecast level of 20.3 million tons for now.

AUSTRALIA. Identical, it is in the forecast, 5.7 million tons.

ICE CANOLA RSX23 NOV23 – 676 CAD (-26 CAD vs. previous week)

ICE CANOLA TREND CHART – RSX23 NOV23

CAUSES AND EFFECTS – THE STORY

From the previous report: “The turnip reaches a dead end. The month of MAY is repeated as in the previous season. We’ve got a number of factors here that we’ve listed repeatedly, and at this point, they’ve lined up. We resume their enumeration and describe the course further:

- Record production in the European Union, over 20.5 million tons;

- Rapeseed production of Ukraine;

- Export record to the European Union of Ukraine;

- Australia’s EU export record,

- Production record in Canada;

- Production record in the US too;

- The price of palm oil, which falls on the increase in production in Indonesia;

- The price of oil, which falls below 74 USD/barrel after climbing extremely high, at the level of

Based on the above, we bring new arguments:

- August canola futures on Euronext fell.

- On the Winnipeg exchange, July canola futures rose slightly earlier in the week amid delays in canola planting, but then fell again.

- In Ukraine, rapeseed forward prices remain at a low level of USD 320-330/MT.

- On the Rotterdam Stock Exchange, rapeseed oil prices continue to fall due to reduced demand from the biofuel industry.

In all of the above we also see an involvement of the environmental political factor:

- Under revised rules for the transport sector, EU countries must force fuel companies to reduce greenhouse gas emissions from spent fuels by at least 14.5% by 2030. Alternatively, they can opt for a 29% renewable energy target for all energy used in the transport sector.

- For Germany, the 14.5% target could be reached as early as 2028, according to a scenario developed by the German biofuels association VDB. This builds on the currently planned roll-out of alternative fuels such as biofuels and synthetic fuels, as well as electric mobility.

So we have the ingredients all combined, plus the environmental and political one above:

- CPO palm oil price drop.

- Soybean quotes down.

- Drop in sunflower oil prices.

- Soybean oil prices fall.

- Decrease in oil indications.

LOCAL STATUS

The port of Constanța is quoting old crop sunflower seeds at the level of 400 USD/MT. Local processors indicate 400 USD/MT.

The quotation level of the new crop is set at 380 USD/MT in CPT Constanța parity, which leads to a level of USD 370/MT for the goods delivered to the processing units.

CAUSES AND EFFECTS

Volume forecasts from the Northern Hemisphere and implicitly from the Nordic production core of sunflower seeds are extremely positive. The signals are clear and the reasoning we repeat in the form of advice is identical to that of the previous week.

We recommend the forward sale of at least 1 ton of sunflower seeds per hectare, because in the event that the import restriction of Ukrainian goods in the 5 neighboring countries is lifted, we could see further price degradation.

REGIONAL STATUS

UKRAINE has reached a seeding level of over 2.3 million hectares.

RUSSIA has no change; it is also at the time of sowing. We maintain the volume forecast at 16.5 million tons.

The EUROPEAN UNION sows, for its part, and volume forecasts will rise to levels that will reach 11.5 million tons. For comparison, in the previous season, the Union generated 9.3 million tons, but let’s not forget the drought. But in the 2020/21 season, the European Union generated 10.3 million tons, against the background of a balanced in terms of weather and production.

GLOBAL STATUS

Out of season.

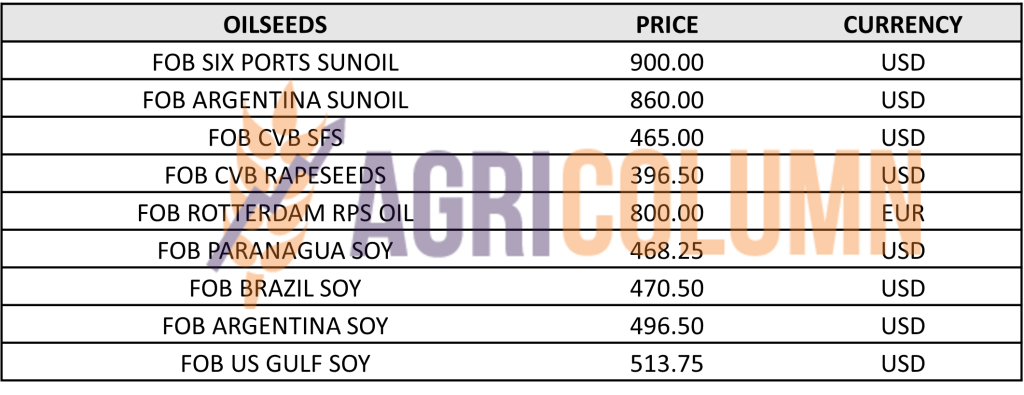

PRICE INDICATIONS FOR OILSEEDS AND CSFO IN MAIN ORIGINS

CAUSES AND EFFECTS – THE STORY

The sunflower seed crop has a potential of 54.5 million tons forecast at this time. To which we must add stocks not sold by farmers from the 2022 harvest.

This will not make life easy for the price of sunflower seeds. The trend will be downward. With an extended grain corridor and a possible entry of Mykolaiev into the landscape (they are tentative, nothing certain or formal), we could see a very close competition between Ukraine and Russia. Everyone will want to sell sunflower oil in traditional Asian destinations.

But Indian and Chinese stocks of vegetable oils (palm and soybean oil) are high, which does not favor any near-term price or volume potential. The palm oil producing countries, Indonesia and Malaysia, have very good production potential in May and thus put even more pressure on the price of sunflower oil.

The European Union will generate at least 2 million tons higher production in 2023 and the weather forecasts are very good at the moment, so the weather cannot be a factor to be taken into account in the coming period either.

In other words, there is no viable argument today for an eventual increase in the price level of sunflower seeds.

LOCAL STATUS

In Romania, the price indications for soybeans are at the level of 480 USD/MT, DAP processing units for non-GMO soybeans.

REGIONAL STATUS

THE EUROPEAN UNION. Total imports of soybeans this trading season reached 11,000,000 tons, and soybean meal reached 13.7 million tons.

GLOBAL STATUS

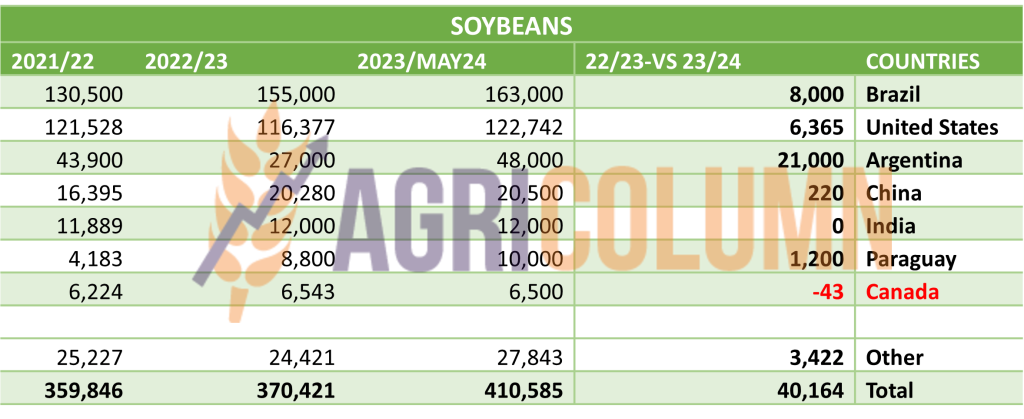

ARGENTINA. WASDE keeps Argentina at 27m tons production, despite BAGE estimates of 21.5m tons.

BRAZIL is maintained at the level of 155 million tons production forecast.

The US has a volume forecast of 122.7 million tons. If we compare with the previous season, we have an increase of 6.5 million tons.

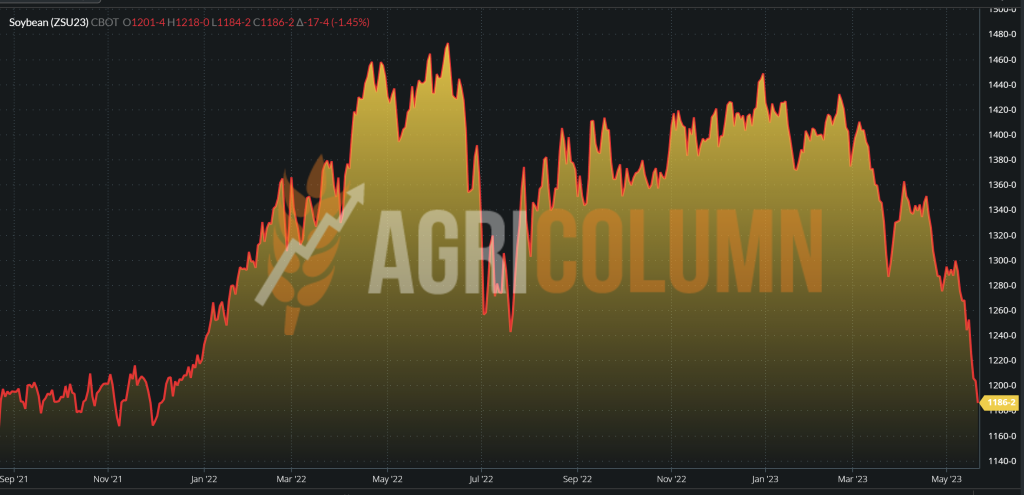

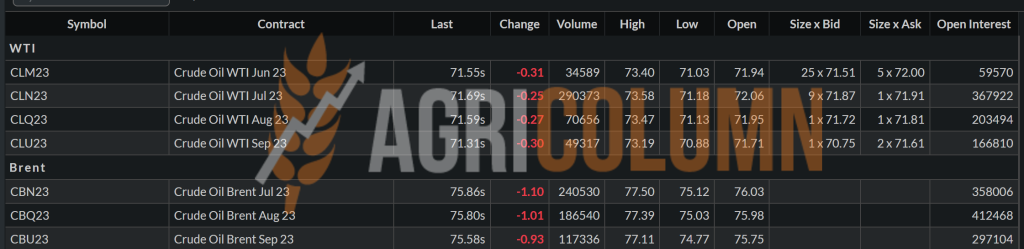

CBOT SOYBEAN ZSU23 SEP23 – 1,186 c/bu (-58 c/bu = 21 USD/MT vs. last week)

SOYBEAN CHART TREND – ZSU23 SEP23

CAUSES AND EFFECTS – THE STORY

The USDA is putting numbers on the production potential for the 2023-2024 season, and it looks fabulous.

With global production increasing by more than 40 million tons, compared to an average index of 365 million tons, we have a positive percentage of 11%, which is indeed a parameter.

The USA will generate 123 million tons, Brazil 163 million tons (+8 million compared to the current season, which is also sensational with 155 million tons), Argentina will return with an extra 21 million tons, being drastically affected of drought, and China has generated purchases of over 30 million tons so far.

China alone buys 25% of the world’s soybean production annually, with the European Union only credited with a maximum of 11 million tons so far. The value of Union imports does not exceed the figure of 12-13 million tons.

Under these conditions, only the Weather factor can generate potential spikes in the price of soybeans, otherwise it will have a downward trend, as I estimated in previous reports by indicating the reverse of the harvest.

20-28 May 2023

Romania

Europe

Ukraine

Russia

Canada

USA

Brazil

Argentina

China

Australia