This week’s market report provides information on:

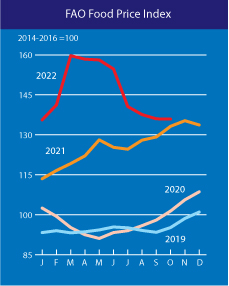

FAO INDEX – OCTOBER 2022

CEREALS

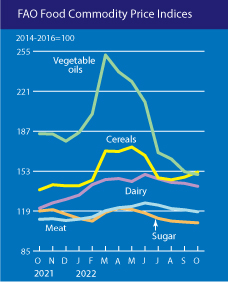

The FAO Cereal Price Index averaged 152.3 points in October, up 4.4 points (3.0%) from September and 15.2 points (11.1%) above its value in a year ago. International benchmark prices of all major grains rose month-on-month.

World wheat prices rose by 3.2%, mainly reflecting continued uncertainties related to the Black Sea Grains Initiative. Tighter supply in the United States, following a downward revision in production, also contributed to the markets’ firmer tone.

International grain prices rose 3.5% month-on-month, driven by a 4.3% increase in world corn prices. The rise in corn prices was supported by lower production prospects in the United States and the European Union, along with dry planting conditions in Argentina and uncertainty over continued exports from Ukraine.

Meanwhile, world barley prices rose only marginally (0.3%), with higher world supplies stemming from better production prospects in the European Union helping to limit price gains.

OILSEEDS AND VEGETABLE OILS

The FAO vegetable oil price index averaged 150.1 points in October, down 2.4 points (1.6%) month-on-month and nearly 20% below the year-on-year level previous. The continued decline in the index was driven by lower global prices of palm, soybean and rapeseed oils, which more than offset higher quotes in sunflower oil.

In October, international palm oil prices fell slightly from the previous month, largely influenced by persistently high stocks in Southeast Asia, despite concerns about the unfavorable weather outlook in some areas of the main oil regions. growth.

Meanwhile, global soybean and rapeseed oil prices fell on the prospect of abundant supplies in the coming months. In contrast, international sunflower oil prices recovered moderately after falling continuously over the past half-year due to uncertainty over the future of the Ukrainian export corridor amid rising geopolitical tensions.

THE CEREAL CORRIDOR

RUSSIA re-entered the game. In a true poker bluff, Russia has re-entered the game, proving once again, if need be, what it really wants, namely, the fertilizer trade. Despite having no sanctions on the fertilizer and wheat trade, Russia cannot move anything in the fertilizer trade area and its hands are tied.

Why? Because the sanctions are applied to the Russian oligarchs who own the industrial giants that produce fertilizers and, implicitly, by excluding Russia from the payment system, they do not have access to the market. On their Asian and Middle Eastern turntables they cannot sell fertilizers because the Middle Eastern countries produce their own fertilizers and do not need the Russian ones. In Europe, they have no way to sell because they have sanctions on oligarchs and payments. Even in Brazil, their partner, they can’t transact, also because of payments. There can be no question of barter. What to bring back from Brazil? Corn? What to do with it? They have it too. Soy? Not even, they have that too. It’s SUM ZERO GAME for Russia.

The same goes for wheat. Because of the payment system, they are restricted to a barter market and that’s about it. But, after having positioned themselves very well in September and October, maybe even November, the circle narrows. It is not enough for their crop to be exported. The circle closes.

Russia began to bleed financially because of these two parameters, sanctions on payments and on oligarchs in the fertilizer industry. And as I’ve argued for a long time, they’re effectively being pushed into the ropes, and they can do nothing but blackmail.

Does anyone think that they suddenly changed their mind after announcing that they were withdrawing from the Istanbul Agreement? It was a good reason to blackmail again. For otherwise how can we look at things fairly? Russia is mercilessly throwing missiles, bombs and drones at Ukraine, and suddenly it is angry that Ukraine has attacked with 10 naval drones some of the military ships stationed in Sevastopol.

The Russian narrative makes us smile, and we might consider ourselves guilty of it, given that Ukraine’s dramas are so vast and complex that guilt turns the potential smile into contempt for Russian propaganda. Their ships were attacked from the grain corridor, they claim. It’s a joke to anyone with an integral complex of neurons on this planet. And what ships? The military, of course, who sat like ducks in the sun in the harbor without a care while they systematically destroy Ukraine’s energy infrastructure and take innocent human lives.

Returning to the narrative thread, Russia re-entered the game after they had emphatically stated and uttered threats against the Grain Corridor. Another absurdity taken to the extreme. How to do such a thing? To attack and destroy, say, a Turkish escort ship? THERE IS NO WAY!!! Turkey is a NATO country and if a single ship is hit, article 5 of the organization is activated. It was also seen that Ukraine and Turkey went about their business, continuing the transfer to the inspection point in Istanbul.

The captain of the Black Sea at the moment is Recep Tayyip Erdogan, the President of Turkey, who is playing an extraordinarily large card at the moment, a card that may shape the commercial and perhaps even military future of the Black Sea. The keys to the Bosphorus are in his hands. The Gate is there and there is where everything will be decided. We are talking about entering and exiting the Black Sea, and the future is in Turkey’s hands.

Today’s positioning will send Russia’s ambitions back to the Sea of Azov, where it really belongs. The Black Sea is not Russia’s as they claim. The Black Sea belongs to the countries that have access to it, according to Maritime Law and the laws of Public International Law, and the countries with access are clearly Ukraine, Romania, Bulgaria, Turkey and Russia, in the north, on the right bank of the Kerch Strait.

After Russia re-entered the game, i.e. active participation from Istanbul, the lobbying moves went into fast forward mode and we noted how the UN, through Mr. Guterres, is lobbying extremely aggressively for Russian fertilizers, claiming that they will help global agriculture. Turkey was also actively involved in drawing up, together with Russia and the UN, lists of countries that could benefit from Russian fertilizers.

It’s just a perpetuation of Russian blackmail taken to another scale. If the world gives in to this blackmail, they will prosper and make fabulous profits that will fuel Putin’s war machine. Europe and the Anglo-Saxon allies must not give in under any circumstances. Russia must understand that it is an aggressor and a terrorist state. Russia is killing innocent people and has invaded a neighboring country. They trampled on the sovereignty of a country, as they have been doing for decades. They tried with Afghanistan and they retreated in disgrace. What were they looking for there? Lithium and uranium resources, of course. Nothing else.

Russia has no options at this point. And giving in would actually mean the escalation of the conflict and the loss of innocent human lives on both sides, because the Russian soldiers are also, in their vast majority, not to blame for being sent into the shredder of human lives.

Russia has said that if it does not agree to extend the Istanbul deal, it will not prevent Turkey from buying Ukrainian goods. And here we clearly see future scenarios. We are certain that they will not bomb the three ports of the corridor, Odessa, Pivnyi and Chornomorsk.

And another scenario may happen, the one in which Turkey will become an intermediary in the global trade in agricultural raw materials. If Russia does not prevent Turkey, this automatically leads to Turkey’s broker role, which will do nothing but strengthen Turkey’s position in the Black Sea basin, with the resulting financial gain attached. Erdogan will become the Master of the Black Sea, undoubtedly.

Until then, the Russian war machine is systematically destroying Ukraine’s energy grid. Hundreds of thousands of people will have nothing to warm themselves with, no electricity and no water. And we don’t want to imagine how they will live. Carrying water with a bucket up to the 7-8th floor, using it sparingly, shivering from the freezing cold in your bed in the dark and not being able to use the toilet are already real scenes in most areas of Ukraine. At the same time, Russia also destroyed crude sunflower oil storage tanks of a Chinese company in Mykolaiev. About 17,000 tons or 17,000,000 liters of oil were destroyed.

VIA REUTERS: “Four sources, who declined to be identified because of the sensitivity of the subject, said Russia is asking Western countries to allow state lender Rosselkhozbank to resume relations with correspondent banks despite Western sanctions. This would allow the bank, which until now has not had a major role in international grain trade, to process payments for Russian grain and other food products, two of the sources added. Before the most recent sanctions, such payments were handled by international banks and subsidiaries of other Russian banks in Switzerland. The sources did not say what response, if any, Russia received to its proposals. “

LOCAL STATUS

The indications of the port of Constanța are at the level of 325-330 EUR/MT in CPT parity. The price of feed wheat is 25 EUR/MT lower than the price of milling wheat.

In the country, at the processing level, the price indications are 320-325 EUR/MT, depending on the quality offered to the processing unit.

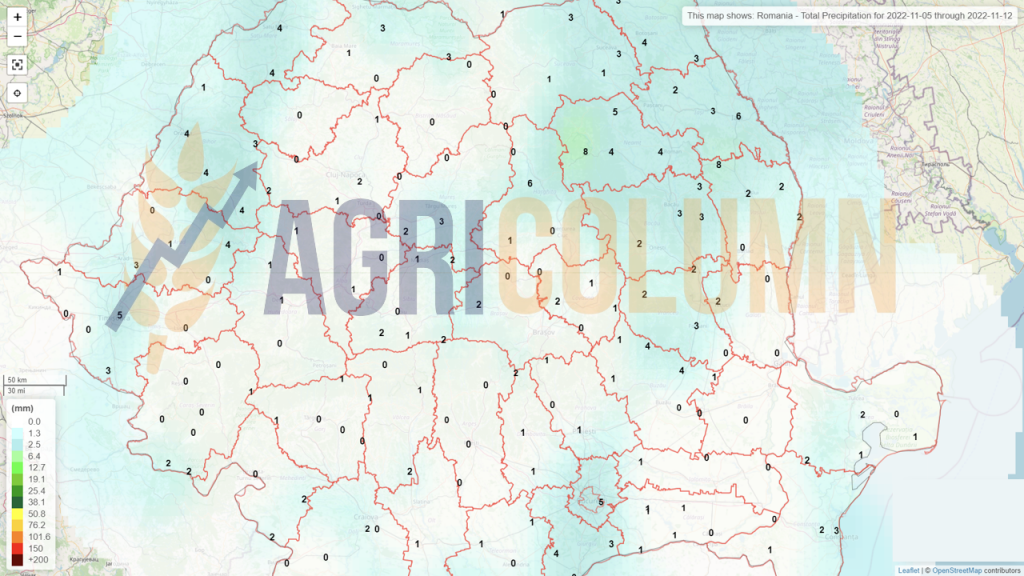

The problems generated by the lack of precipitation are becoming more acute and Constanta county is a prominent exponent of this phenomenon. Non-emergence, uneven emergence, associated with the yellowing of plants are expanding phenomena in the southern part of Romania, as well as in areas prone to drought such as Vrancea, Bacău, Vaslui and Iași. It is already an extremely serious alarm signal, as precipitation is not visible at all on the horizon. 2020, 2022 and 2023? Only the West and North of Romania will receive some rain. Otherwise nothing.

CAUSES AND EFFECTS

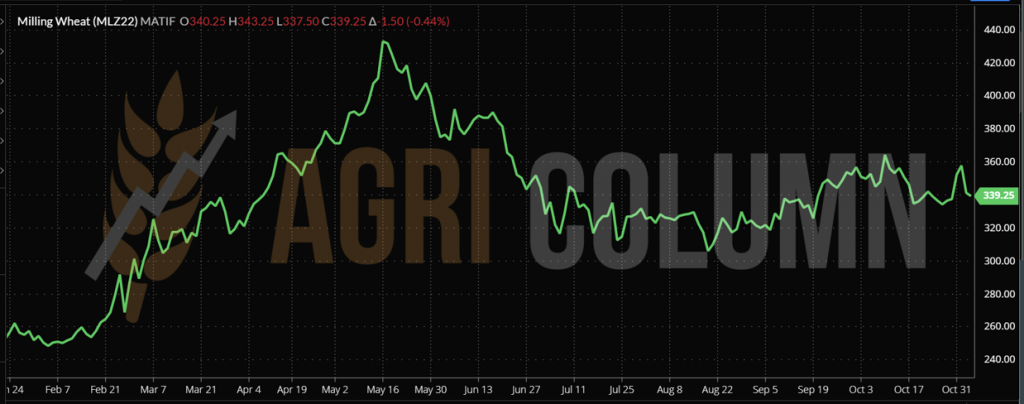

As we have seen, the untimely exit of Russia from the Istanbul agreement generated a momentary panic, which caused the price of wheat to rise to the value of 340 EUR/MT in the CPT parity. But the change in price intervened immediately and led to the initial relaxation of prices. It was an extremely short-lived surge, a surge that benefited only hedge funds. The wheat route in the following period follows the same capped trajectory. Every time it tries to break the pattern, the fundamentals of the physical market bring it back to the correct level of this period.

Until November 18, when the Istanbul Agreement will be extended or not, there is not much time left. Interspersed we will have the USDA report on November 9, 2022, which will not create much suspense with its estimates of global wheat production. Perhaps we will even see a reduction in consumption due to prices and thus the potential shortage in South America will be compensated.

REGIONAL STATUS

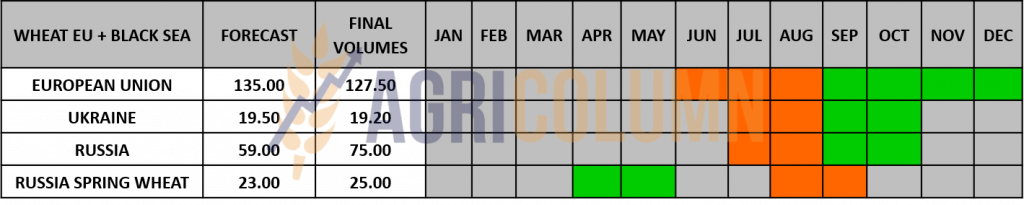

RUSSIA is at the same accelerated rate of wheat export. Southerly winds have caused problems for Russian wheat shipments, but the accelerated pace of exports continues and will generate high volumes in November as well. The United Grain Company (OZK) assures that the export of Russian grain has nothing to do with the agreement. The main buyers, the countries of the Middle East and Africa, have adapted to the sanctions imposed on Russia.

According to IKAR, average prices for Russian Federation wheat with 12.5% protein at the end of last week were around 312 USD/MT (FOB). Rusagrotrans saw a drop in quotations to 305 USD/MT. If no new specific sanctions are introduced, then the export figures will be very high. Shipping growth continues to be negatively impacted by financial logistics and vessel chartering difficulties.

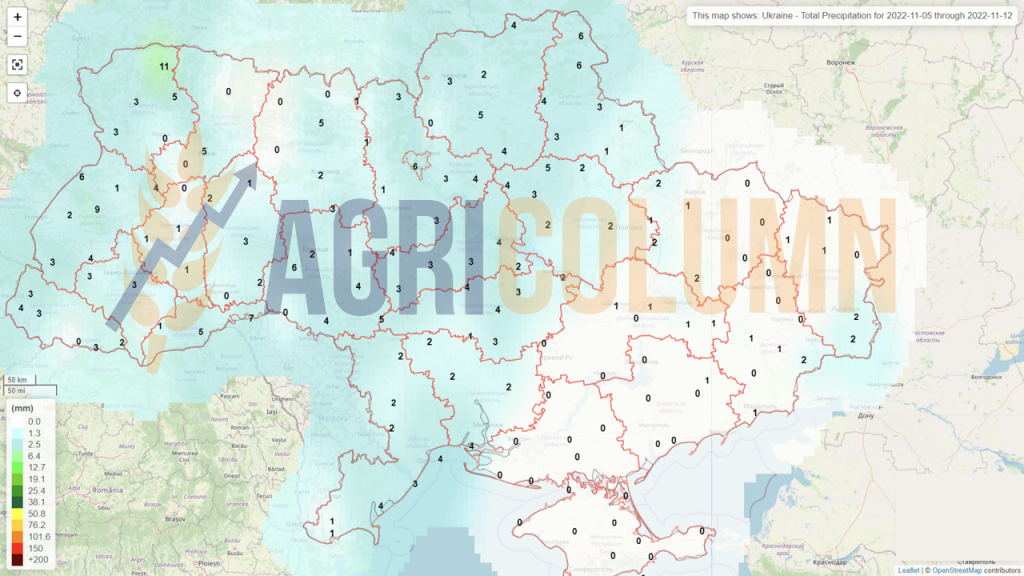

UKRAINE, after having weakened the pace of exports due to Russia’s exit from the agreement, has also recovered thanks to insurers who are showing positive interest in insuring ships entering the Grain Corridor.

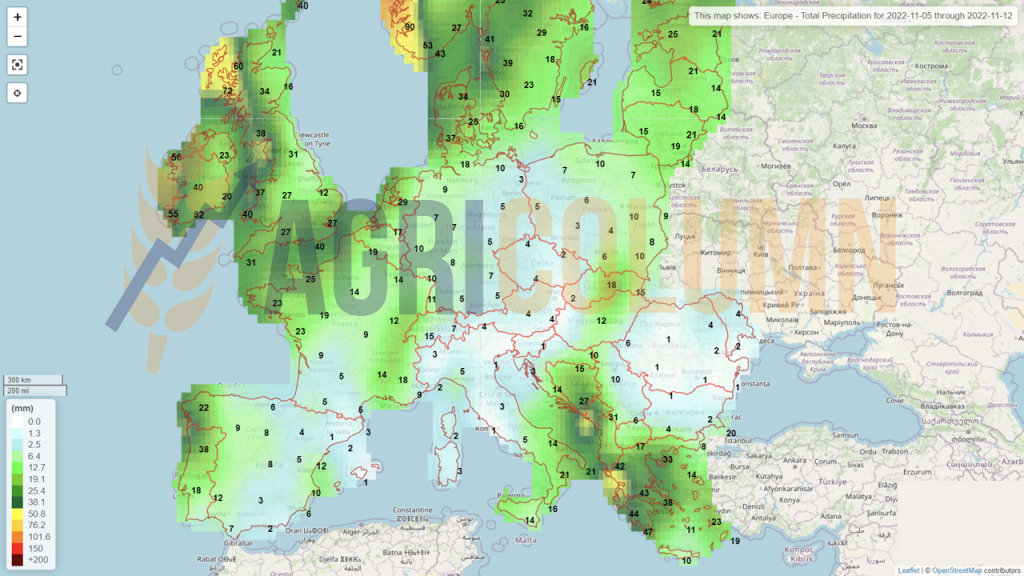

THE EUROPEAN UNION maintains its export pace, in the condition of a dry season, which effectively decreased the export potential. The EU’s strengths are naturally the predictability of trade relations and the origin of goods.

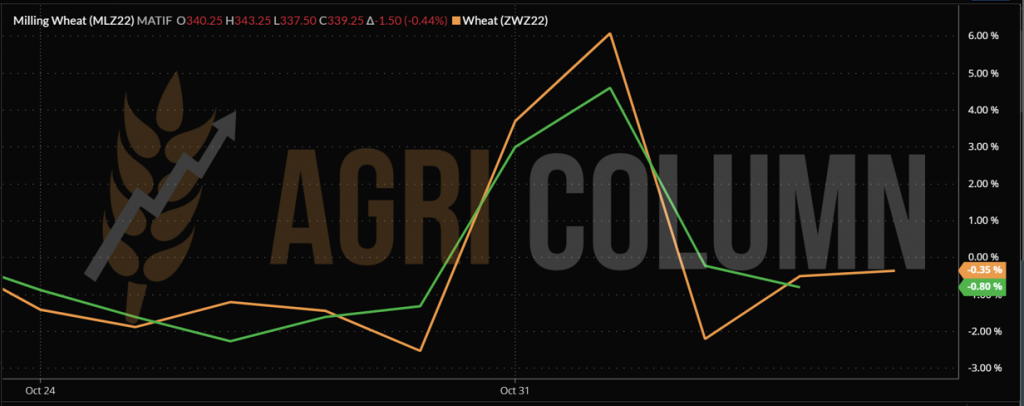

EURONEXT MLZ22 DEC22 –339.25 EUR (-1.50 EUR)

EURONEXT WHEAT TREND CHART – MLZ22 DEC22

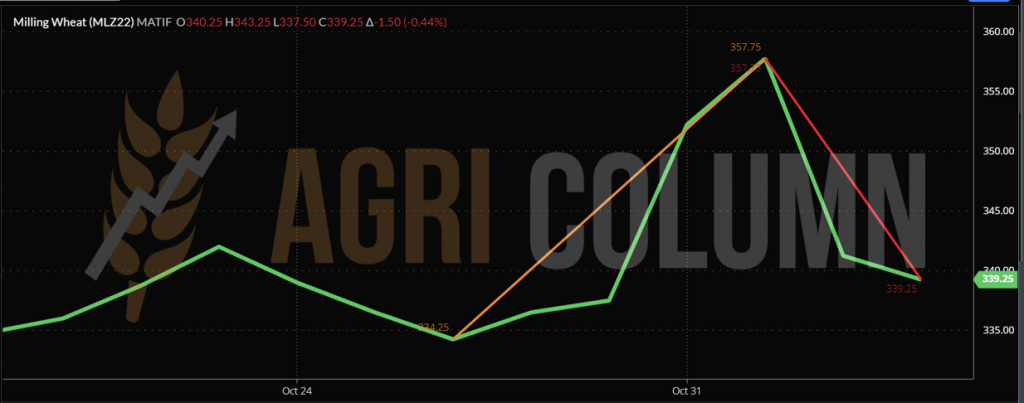

EURONEXT-CBOT WHEAT TREND CHART (October 26 – November 3, 2022)

GLOBAL STATUS

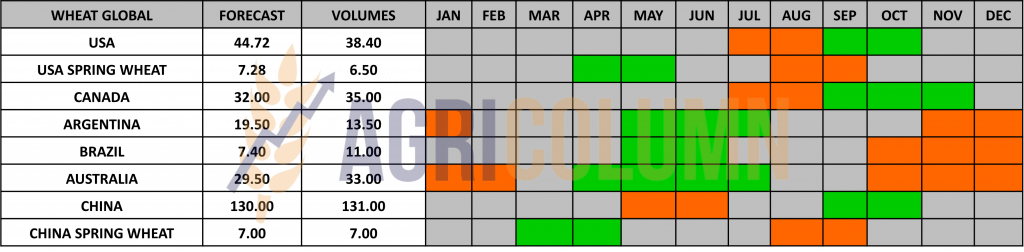

The US remains in the same dramatic drought scenario in the central plains. Low US winter wheat conditions (only 28% good/excellent condition out of 87% seeded) add to the anxiety. Instead, it accelerates exports very strongly, with over 3 million tons sold and shipped in September.

ARGENTINA drops production forecast dramatically. Subsequently, Argentina lowered the forecast from 19.5 million tons to 16.5 million tons. But this weekend, degradation has risen to very high levels, and according to local analysts, Argentina’s wheat production will be 12.5 million tons, a maximum of 13.5 million tons.

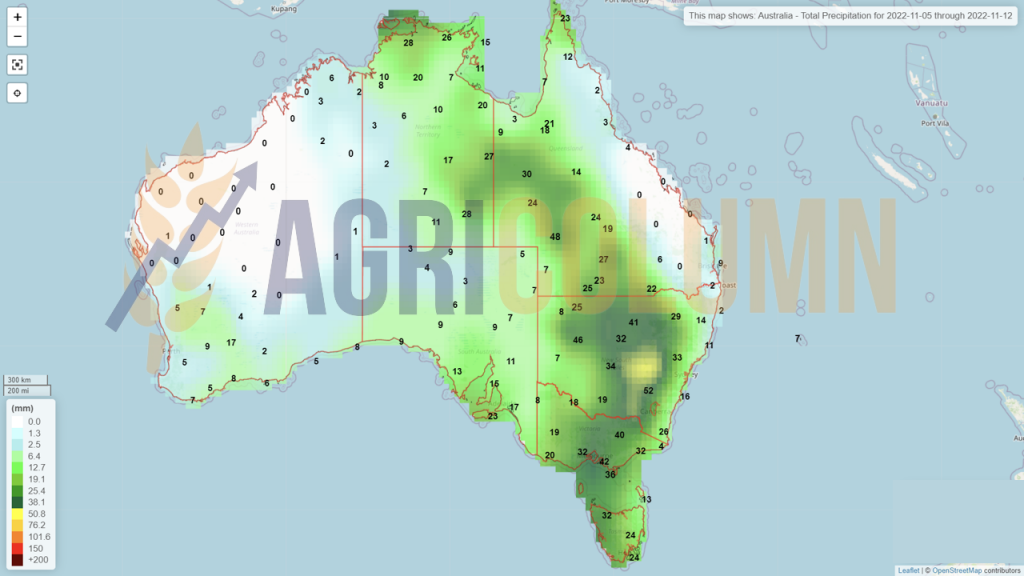

AUSTRALIA literally dives into the water. Nothing new, uninterrupted rainfall comes to outline a potential imbalance in the wheat market.

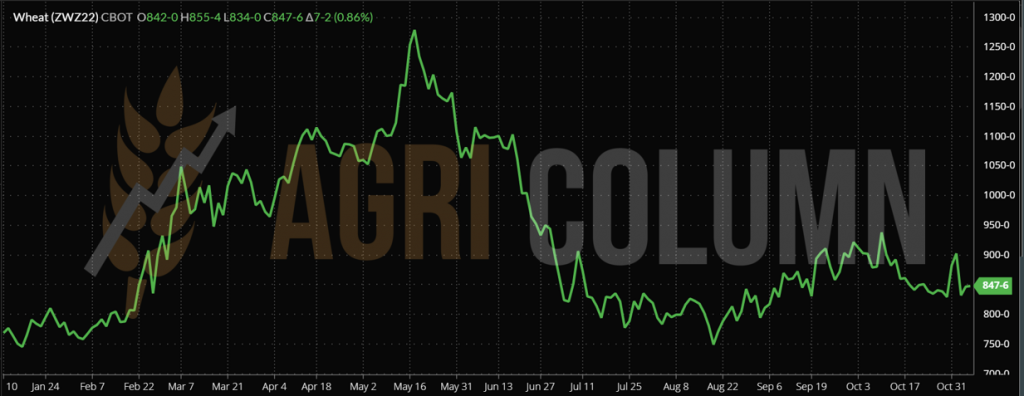

CBOT WHEAT – ZWZ22 DEC22 (847 c/bu (+7 c/bu = +3.3 USD)

CBOT WHEAT TREND CHART – ZWZ22 DEC22

CBOT-EURONEXT WHEAT TREND CHART (October 28 – November 4, 2022)

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

TENDERS AND TRANSACTIONS

IRAQ. Iraq bought 150,000 tons of wheat in an auction: 3 origins: Australian at 480 USD/MT, Canadian at 489 USD/MT and Lithuanian at 499 USD/MT (CFR Qasr port).

PAKISTAN. In addition to the 385,000 tons, the ECC (Economic Coordination Committee) also approved the purchase of 300,000 tons of milling wheat at 372 USD/MT CIFFO for delivery between November 2022 and January 15, 2023.

JORDAN. Wheat tender cancelled. No purchases were made in last week’s auction for the purchase of 120,000 tons of wheat. Participants: CHS, Cargill, Ameropa and Buildcom. A new tender will take place on November 15.

CAUSES AND EFFECTS

Wheat reacted purely emotionally on the North American and European stock markets. The tension generated by Russia’s announcement to withdraw from the grain deal sent wheat prices 20 USD above on the CBOT and plus 17-18 EUR on the Euroenxt.

The return came immediately after Russia’s announcement that it would return under the agreement. The market relaxed and the indications fell to the previous values.

The FED increased the monetary policy rate by 0.75%, but this had already been calculated by the hedge funds and had no impact.

In the final hours of trading on Friday, the North American market reacted on the back of the USDA’s announcement of high export values for September.

In the immediate period ahead, the wheat price level will not fluctuate. Everyone is keeping an eye on the extension of the Istanbul Agreement and this will depend on the price of wheat in non-Russian origins, as many destinations do not want to buy from Russian origin due to sanctions on the payment system.

So an apparent lull will follow, but behind the curtain, the Russian propaganda machine aided by the UN and Turkey will try to lift certain sanctions imposed on the payment system and on the owners of the fertilizer companies.

LOCAL STATUS

The price indications of feed barley in the CPT Constanța parity did not experience any essential changes. They remain anchored around 280-285 EUR/MT.

As in the case of wheat, the barley crop presents problems that will become more acute, exactly in the areas mentioned for wheat: Constanța, Vrancea, Bacău, Vaslui and Iași.

REGIONAL STATUS

No change in regional status for the period from the previous report to today.

MIT JORDAN closes new tender with no purchase.

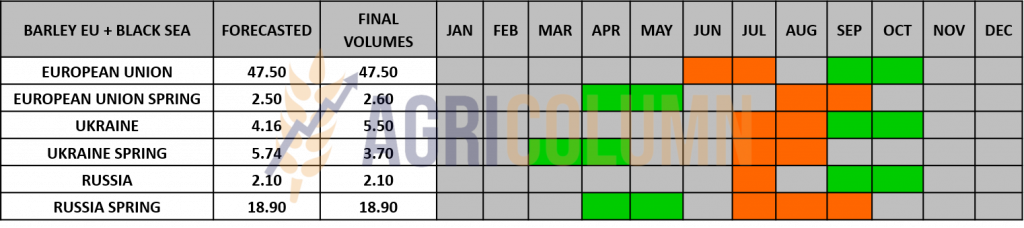

EUROPEAN UNION has a sowing figure of 10.37 million ha, in line with last season. Romania occupies the 6th position, according to the areas sown this autumn.

We insert the composition by country of the areas sown with barley.

BARLEY PRICE INDICATIONS IN MAIN ORIGINS

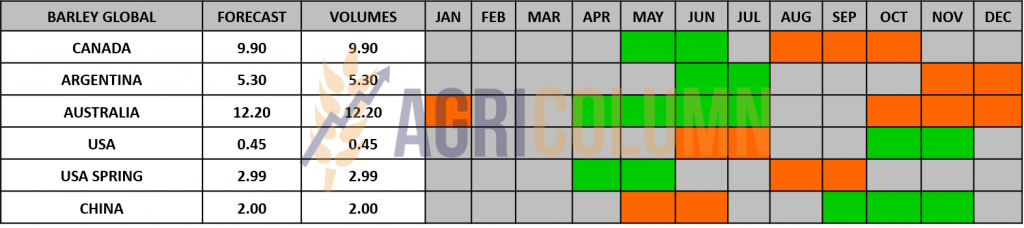

GLOBAL STATUS

AUSTRALIA is in same scenario that week past. The problems generated by the extremely generous rainfall that seems to not be ending.

LOCAL STATUS

Corn indications in the port of Constanța remain on the same platform of 295-300 EUR/MT. The port of Constanța, however, is quite crowded and storage spaces are less and less available.

CAUSES AND EFFECTS

Romanian corn maintains its price level. In the country, farmers prefer to sell their stored wheat to cover their due debts. The corn price level remains within the same parameters for now.

REGIONAL STATUS

UKRAINE continued its corn exports through the Cereal Corridor. The process was stopped by Russia, but continued by Turkey alongside the UN. Similarly, cross-border transit is also carried out. Today, Romania is a real turning point for corn from Ukraine on river routes, railways, and roads.

The EUROPEAN UNION is in the same status. With a disastrous crop of 50.4 million tons, it is relying on Ukrainian corn in the attempt to supply for feed use.

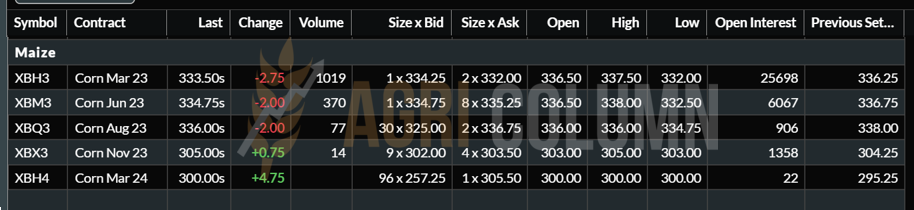

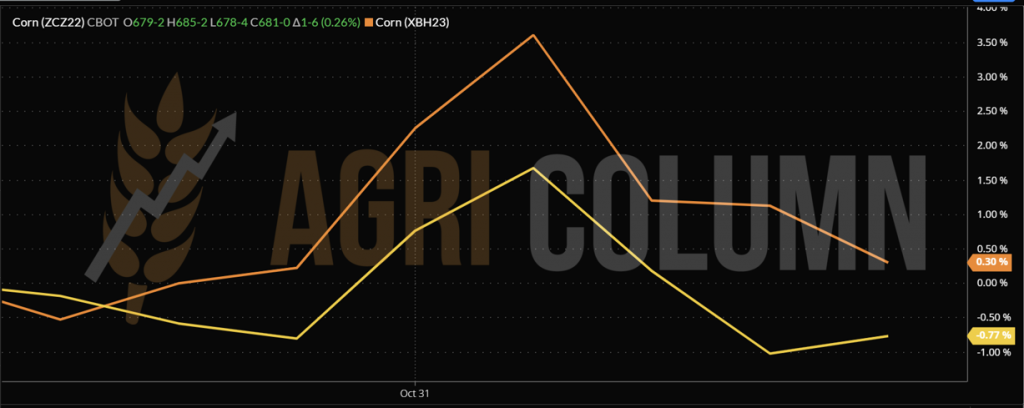

EURONEXT CORN – XBH23 MAR23 –333.50 EUR (-2.75 EUR)

EURONEXT CORN TREND CHART – XBH23 MAR23

GLOBAL STATUS

The US has reached the 80% corn harvest level. Dry weather helps the harvesting process. Further, the low water level on the inland logistics routes creates major problems for the transportation of corn from the Corn Belt to NOLA (New Orleans Louisiana).

ARGENTINA. BAGE (Buenos Aires Grain Exchange) reports a 23% corn seeding level. Lack of water in the soil is the main cause, and the rains that have passed have not succeeded in bringing the lands to the optimum mode for sowing. However, BAGE maintains its seeding forecast at 7.3 million hectares.

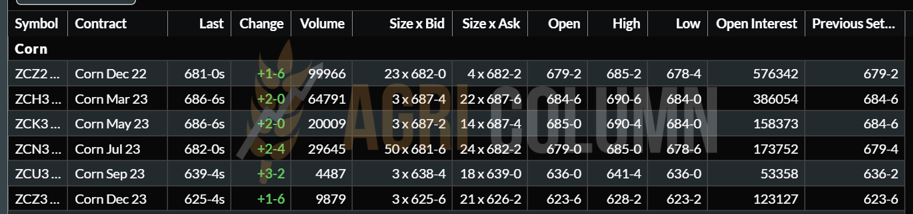

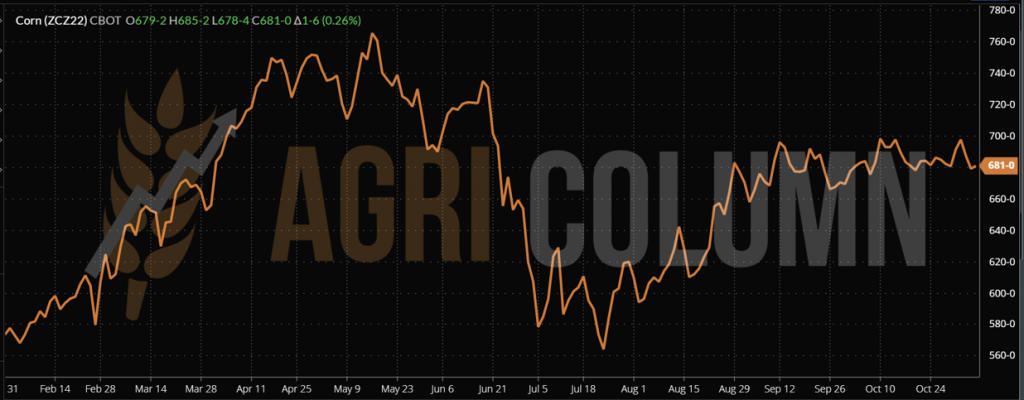

CBOT CORN – ZCZ22 DEC22 – 681 c/bu (+1 c/bu)

CBOT CORN TREND CHART – ZCZ22 DEC22

CBOT-EURONEXT CORN TREND CHART (October 28 – November 4, 2022)

CORN PRICE INDICATIONS IN MAIN ORIGINS

CAUSES AND EFFECTS

Corn will be on hold until November 9, 2022, when the USDA will release the WASDE report that will bring certainty about North American production, which will be much higher than the October 12, 2022 estimate. And sources indicate numbers both so different that we prefer to be reserved. For example, Barchart indicates a 20 million ton increase in US corn production, from 353 million to 373 million tons. Stone X is much more reserved and indicates only 5 million tons of growth, that is, to the level of 358 million tons.

In essence, the result could be one that will penalize the price of corn, relying on much higher productivity per hectare in the US. The higher the forecast, the lower the corn price will drop.

LOCAL STATUS

Rapeseed indications appear in the same mold as in the last period, i.e. FEB23 minus 20-25 EUR/MT for the goods delivered in the CPT Constanța parity and with FEB23 minus 15-20 EUR/MT for the goods delivered to the processing units.

In Romania, rapeseed suffers from lack of water. At the national level, this is already being felt, even if not in an extreme way. But there is no precipitation on the horizon, which raises the first alarm signals for rapeseed crop at the local level. In the Constanța area and crossing Bărăgan, this is extremely visible. We see damaged, stunted, yellowed and troubled crops. Rain is the only thing that can solve the problem of rapeseed and, implicitly, wheat in the next 10-12 days. But until November 20 nothing is visible on the horizon.

CAUSES AND EFFECTS

In the coming period, rapeseed will correlate only with the price of fossil energy. Standardizing the price of fossil energy will drive rapeseed to supply and demand fundamentals. The bullish effect of the last few days was nothing more than the traction generated by Russia’s exit from the Istanbul accord.

We have no change at the regional level, but the main focus remains tracking the vegetation stage of rapeseed, which can be influenced by the weather. The European Union received precipitation in most of the territory, the exception being Romania.

EURONEXT RAPID – XRG23 FEB23 – 664.75 EUR (+4.75 EUR)

EURONEXT RAPESEED TREND CHART – XRG23 FEB23

GLOBAL STATUS

CANADA. Out of season.

AUSTRALIA is under the same harvest pressure under rainfall.

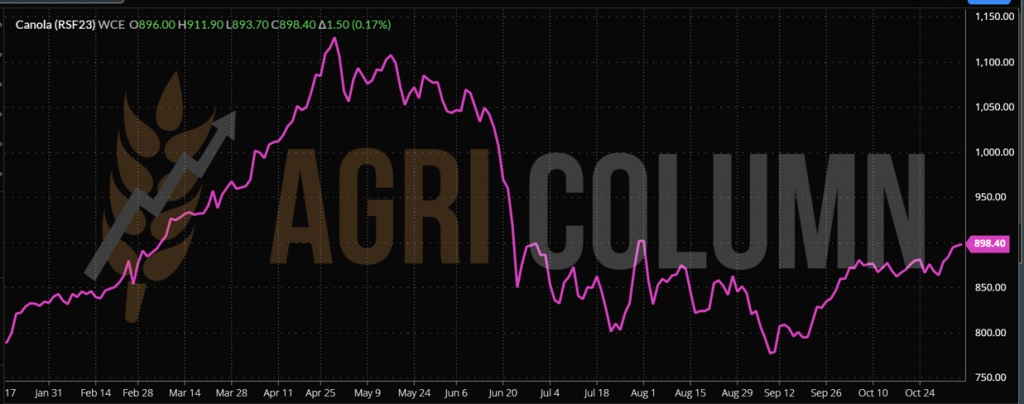

ICE CANOLA RSF23 JAN23 –898.40 CAD (+1.50 CAD)

ICE CANOLA TREND GRAPH – RSF23 JAN23

COMPARATIVE GRAPH. PETROL-RAPESEED-CANOLA CORRELATION

CAUSES AND EFFECTS

Rapeseed receives support from correlation with fossil energy and this is evident in JAN23 Brent Oil quotes, which reached the level of 98.57 USD/barrel.

The state of rapeseed vegetation in Australia is also a concern. We will see the Australian crop fall in volume due to rainfall, which will mean support for the price.

The European rapeseed crop is experiencing problems in Romania and several other areas. This will also strengthen the price in the period ahead.

With the above factors, we note that the rapeseed price trend will continue to have support in the coming week. Matching supply and demand, as well as looking to the future, are fundamental things that support the price of rapeseed.

LOCAL STATUS

Primary indications for sunflower seeds are 565-570 USD/MT in CPT Constanța parity. Processors display the same price levels at processing units, but they also have the same commodity storage space problem.

CAUSES AND EFFECTS

The local market is starting to receive goods from Ukraine, and they are making their way in as usual. Romanian farmers, however, maintain the retention of goods and do not trade until they need financial liquidity to pay dues to input distributors.

The price level offered by processors could be 10 USD/MT higher, but at the moment, farmers are unwilling to sell large quantities, so demand is not matched by supply.

Uncertainty in Ukraine is fueling the rumor mill and we are seeing price levels of 585 USD/MT for cargo delivered to Bulgarian processing facilities in the Ruse area. But logistics is also expensive in this complex. Equivalence with 570-575 USD/MT DAP processing units in Romania is also kept in the logistics complex.

REGIONAL STATUS

UKRAINE is trying through domestic processors to create buffer stocks of raw material to generate domestic processing. Ukrainian farmers, however, do not want to sell the seeds cheaply, they are focusing these days on the sale of corn. During this time, Russia launched a missile in Mykolaiev at a terminal leased by a Chinese company, destroying 17,000 tons of crude oil. Mr. XI’s reply came promptly. He warned Russia that it does not tolerate blackmail with the use of nuclear weapons. The textbook triangulation of Henri Kissinger, former US Secretary of State, near the G20 summit is taking shape.

RUSSIA maintains the same status. No difference from the previous week.

The EUROPEAN UNION finds itself in the same status as last week.

GLOBAL STATUS

ARGENTINA is still in the growing season with no further information on the sunflower seed crop. But we don’t think they will be able to extract the forecasted 4.2 million tons.

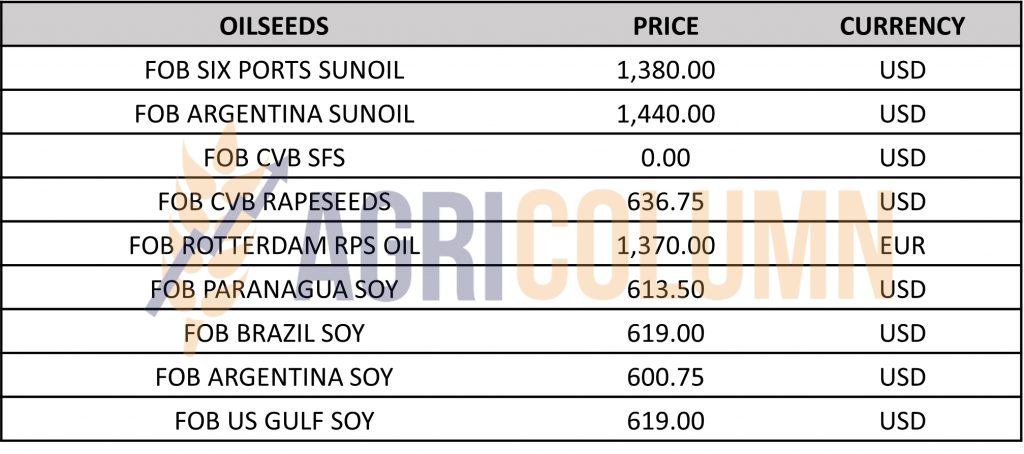

PRICE INDICATIONS FOR OILSEEDS AND CSFO IN MAIN ORIGINS

CAUSES AND EFFECTS

The status remains the same this week. The demand is manifesting itself, and the supply is coming at a very slow pace. We note these things from the acquisition activity of these days in the Constanța port regime, as well as in the processing units.

Sunflower seeds have a much higher price potential than today. Everything will be resolved in January 2023. Until then, the processing units are covered. The JFM Stripe is very close and the supply will start after December 1st 2022.

And let’s not forget the Argentinian crop that is not in good shape, and a minus 2 million tons would matter a lot in the price equation, all aggregated with the level of palm oil production that seems to be in question, from the cause of the floods in Indonesia.

In the VEGOIL complex, the demand for sunflower oil started to increase, also supported by its fellow complex, soybean, which recorded increases in indications.

LOCAL STATUS

In Romania, the price indications for soybeans are at the level of 570 USD/MT DAP processing units for non-GMO soybeans. Between July 1 and October 23, 2022, approximately 84,000 tons of soybeans were imported.

REGIONAL STATUS

GLOBAL STATUS

USA. The pace of the US soybean harvest was dynamic, with the harvest level reaching 88%. Forecasts generated by Barchart prior to the release of the USDA report are on the rise: on October 12, 2022, they were 117 million tons, with a yield of 3.35 tons/hectare, and on November 1, 2022, they were 130.64 million tons, with a yield of 3.55 tons/hectare.

USDA’s weekly export data showed 830,000 tons of soybeans sold in the week ending Oct. 27, 2022.

BRAZIL. Brazil’s soybean production could fall below 150 million tons in the 2022-2023 crop year because of the La Nina weather phenomenon in South America, according to analysts at HedgePoint. This analysis slightly reduces initial projections of a record harvest.

Soybean crops in Brazil are 48% planted, compared to 52% at the same time last year. More rain is forecast in western Parana. Excessive moisture and low temperatures slowed soybean development. Last week was critical for soybean sowing in Parana. The pace was slowed by the rains, but the farmers caught up and did not allow any further delays, so that 67% is now sown.

There were difficulties in delivering soybean meal to the port of Paranagua due to blocked roads, although the impact was considered minimal. However, operations in the Port of Paranagua have returned to normal, as the protesters are no longer blocking the trucks.

ARGENTINA. The delay in sowing soybeans in the central area of Argentina is 45% and represents an alarm signal of a drastic decrease in investment in this crop. There will probably also be farmers who will reduce fertilizers or not fertilize at all. Soybean sales in Argentina reached 71% of the 2021-2022 crop.

CHINA. Soybean supplies are arriving at Chinese ports and processing margins are positive. However, this week’s processing was 15% below the weekly level of 2021 as questions remain about the strength of demand.

China’s soybean processing volume recovered slightly, while soybean stocks continued to trend lower, according to data from the National Grains and Oil Information Center (CNGOIC).

Because of the low level of the Mississippi River, Chinese buyers of soybeans are changing the origin from the US to Brazil. These changes are made on the contracts already concluded with the North American partners through the origin option clause in the contract. Enable that clause and washout.

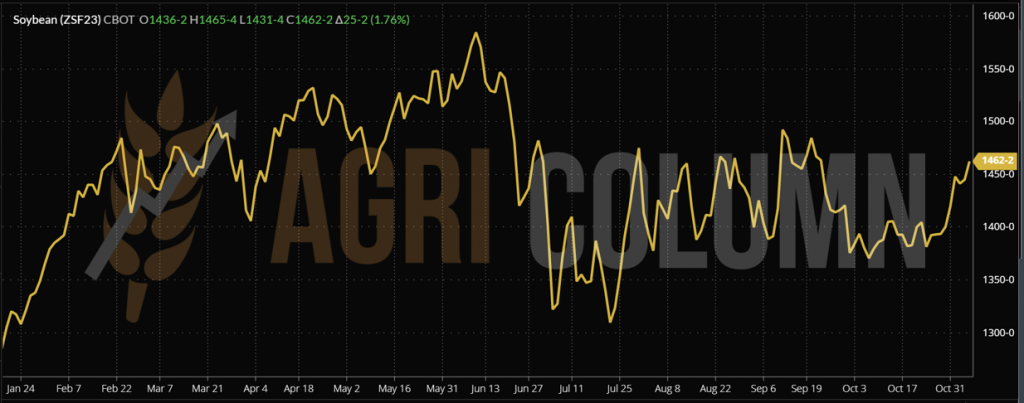

CBOT ZSF23 JAN23 – 1,462 c/bu (+25 c/bu = +9.20 USD)

CBOT SOYBEAN TREND CHART – ZSF23 JAN23

5-12 November 2022

Romania

Europe

Ukraine

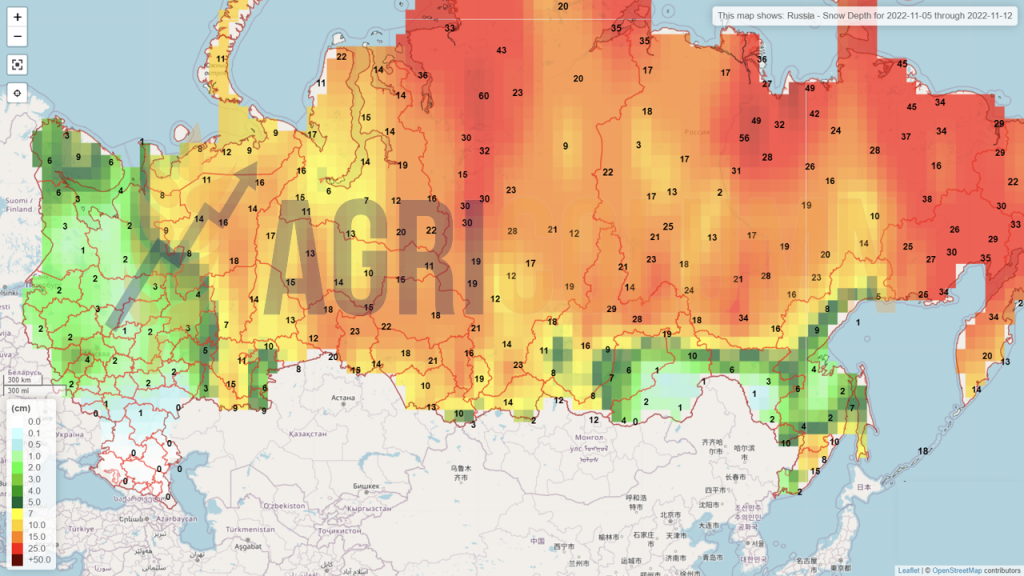

Russia (snow)

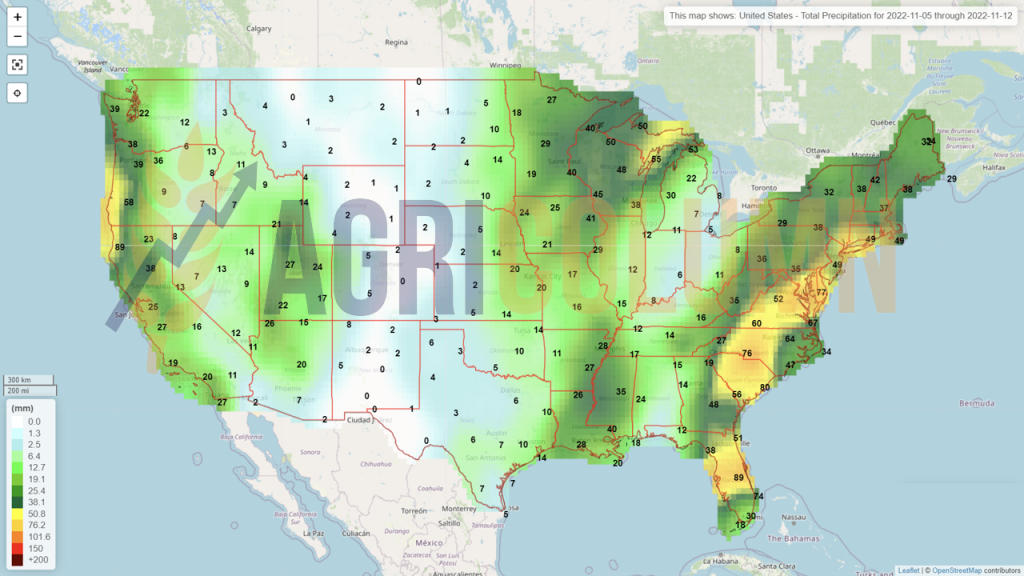

USA

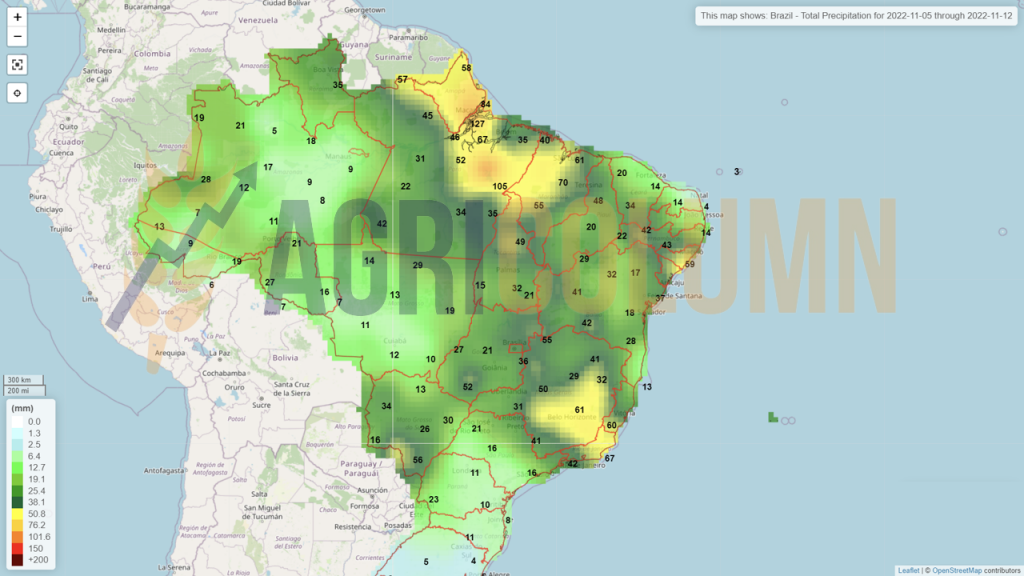

Brazil

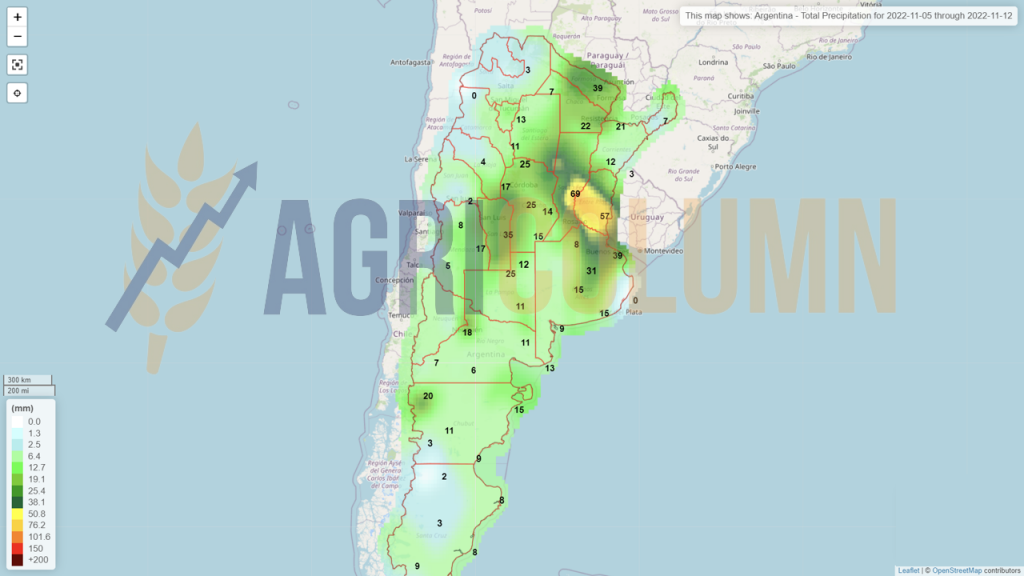

Argentina

Australia