Romanian Agri Trade Summit, one of the largest events addressed to International Agribusiness, will take place on February 22, 2023 in Bucharest.

The initiative aims to reconfirm Romania’s strategic role in global agribusiness and to bring together the most important players in the dynamic grain market – top Farmers, Traders, Processors and Distributors.

This week’s market report provides information on:

LOCAL STATUS

The Port of Constanța indications remain at the same level 275-278 EUR/MT minus 15-20 EUR/MT for feed quality. New crop quotations remain at the same parameters, i.e., a level of 242-245 EUR/MT.

CAUSES AND EFFECTS

Romanian wheat is starting to move towards an end, and we see this expressed in the increase in exports over the last week. We are already up by 120,000 tons since the last report and are now around 2.1 million tons. The domestic market is in no rush to supply the new crop. Precipitation falling in the form of snow indicates a revival of the potential of the new wheat crop, and by implication, this induces relaxation among the Buyers. As I pointed out, production must be at high levels to cover the level of cost per hectare. Globally, the trend cannot be upward, inflation under control is a parameter that governs the markets, along with the state of crops. And they are already seeing each other. We have one month left and we will see much better the state of crops at the Romanian level.

REGIONAL STATUS

RUSSIA is at a time when their narrative is receiving definite opposition from the USDA. More precisely, this body says with subject and predicate that 102 million tons of wheat is a story and that’s it. There is no way Russia has a 102-million-ton crop level. Maybe only with the 11 million tons stolen from Ukraine. That’s what the USDA suggests. But Russia is in an obvious hurry to ship the wheat. Excerpt from marinetraffic.com:

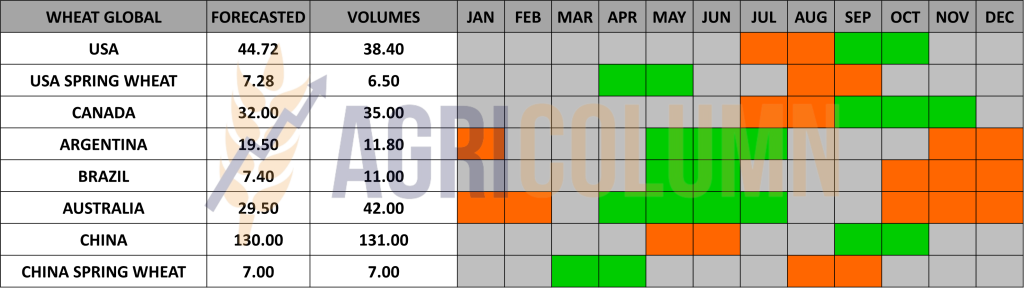

UKRAINE will generate a level of 16 million tons of wheat for the summer crop of 2023. The status of crops is in a favorable period and the figure stated above will be the closest to reality. A minus 5 million tons from the 2022-2023 season and at ½ the level of the 2021 crop, when they had a harvest volume level of 32 million tons.

THE EUROPEAN UNION reached 18.15 million tons of common wheat export level. The barrier of 18 million tons has been overcome and we will certainly reach volumes of 23-24 million tons exported in the Union. Imports are at the level of 4.75 million tons at the moment. The main source of import is Ukraine, as we well know.

EURONEXT – MLH23 MAR23 –286 EUR

EURONEXT WHEAT TREND CHART – MLH23 MAR23

GLOBAL STATUS

The USA, in turn, started to sell wheat, and the previous week, we also recorded 500,000 tons of volume sold in a single day.

ARGENTINA is out of season.

AUSTRALIA is out of season, but the local USDA attaché has started to accept Australia’s high harvest volume, which it has rewarded with an extra 0.4 million tons. Of course, there is still a long way to go until 41-42 million tons, but we fully understand USDA’s role in the global price outlook.

CBOT WHEAT – ZWH23 MAR23 – 750 c/bu

CBOT WHEAT TREND CHART – ZWH23 MAR23

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

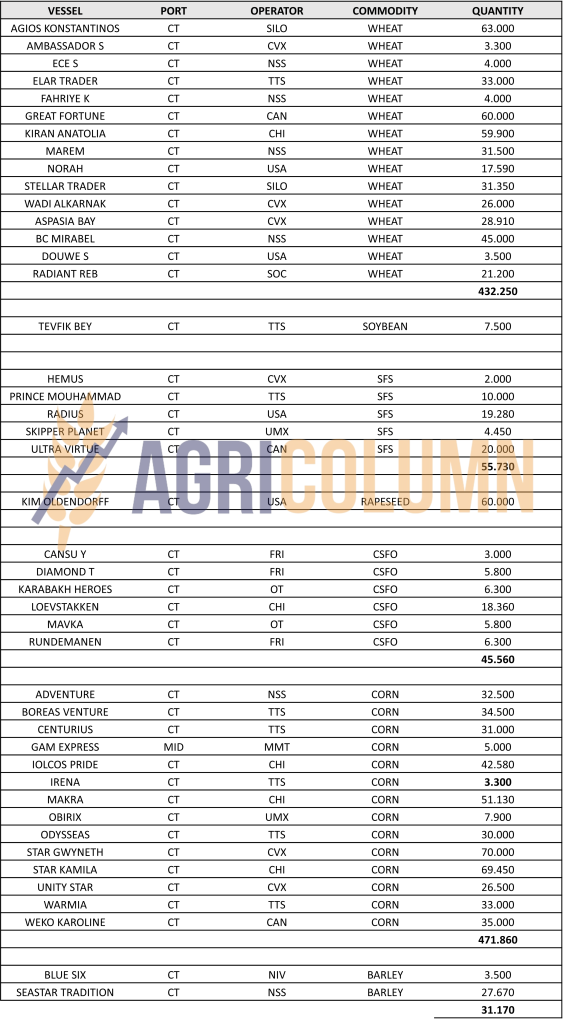

TENDERS AND TRANSACTIONS

Jordan. Milling wheat tender. 120,000 tons, optional origins. Delivery May and June 2023. Deadline for submission of offers: 31 January.

Iraq bought 150,000 tons of wheat from Australia, according to the Ministry of Trade. Viterra was the seller at 445 USD/MT, CIFFO Umm Qasr. Delivery is made within 75 days from the opening of the Letter of Credit.

CAUSES AND EFFECTS

As of Monday, January 23, 2023, the stock markets began to bleed. Funds went into technical sessions and liquidated position after position, literally crashing the US wheat market in the first place. This generated a drop in quotes in the US physical market, which led to a boost in sales in the physical market. Lots of merchandise and a weak dollar are the ingredients that make up the perfect motivation for a sale.

In the chart, it is clear that European Wheat (red area) is still above the US Wheat price trend (green area). And from the trend of American wheat, it is clear how its position in relation to European wheat does not meet the conditions of geo-political influence. As for the Weather factor, the recent snowfalls in the North American territories support the premise of good crops in the summer of 2023. Of course, we will have induction from the Weather during the summer, but the same is true for European wheat. With one amendment. Russian end stocks will have a say in European new crop prices.

The conclusions are, at this point, extremely simple:

We expect the escalation of the conflict in Ukraine, this has a very high certainty. The winter season will pass, Ukraine is stocked with offensive weaponry, and Russia will generate a blockade through an extremely high level of recruitment.

The offensive will generate excitement, and this will clearly transfer to the markets. Maybe not at the levels of the previous season, but, for sure, the emotion will exist and create emulation on the stock markets, because these funds are waiting deadlines to be able to speculate technically. The USDA’s simple statement that Russia cannot possibly have a level of 102 million tons, but a maximum of 91 million tons, made the reaction after the technicality that generated the decrease positive (by 4-5 USD/MT). And then, after the decrease dissipation, it was 2 USD/MT.

But the old crop has some well-established parameters, and one of them is its availability. Australia, Russia and partly the European Union will be able to generate sufficient volumes to cover the demand.

So, there is no higher foundation in this direction. Maybe only Geopolitics. But even there, Russia’s need to export is obvious. In other words, war is war, but we need resources to maintain the cyclicality of cultures. And this cyclicality is somewhat penalized in Russia, because of genetics, which is missing. The origin of genetics has so far been western, Russia failing to have the R&D parameter (research and development) at a high level, so as to avoid dependence on western genetics. And today, Russia only manages to maintain at the level of 60% domestic genetics. 40% is a lot and the difference will be difficult to cover.

And the downward trend in global inflation continues. Don’t be under the illusion that it’s over. The FED forecasts a 0.25-0.50% increase in the monetary policy interest at the end of January. And the plan for a period of 7-8 months is 100 percentage points. This element will keep money expensive, and the consequence will normally be a decrease in the number and activity of exchange funds.

LOCAL STATUS

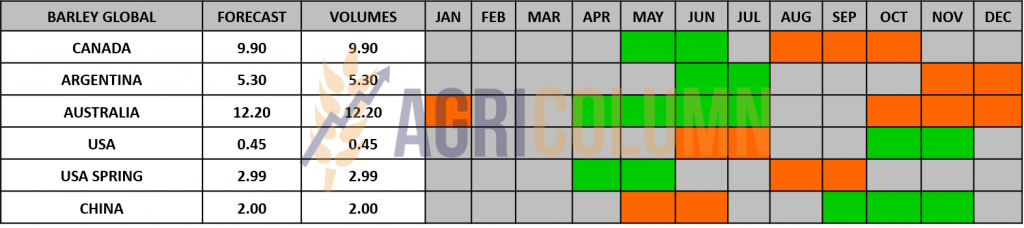

The price indications of feed barley in CPT Constanța parity decreased to the level of 240 EUR/MT.

BARLEY PRICE INDICATIONS IN MAIN ORIGINS

GLOBAL STATUS

CAUSES AND EFFECTS

No news on the barley market at national or regional level. Next, the premises for a decrease in the price level are in place.

LOCAL STATUS

Corn indications in the port of Constanța are at the level of 260-265 EUR/MT.

CAUSES AND EFFECTS

This step back by corn in the price level reflects the CBOT exchange, which fell extremely low at the beginning of the previous week and correspondingly dragged corn lower. Correlation has been mentioned for a long time, as has the fact that wheat will be a factor dragging down corn. And future conditions are mixed. In other words, corn has enough vigor to generate higher price levels than today.

REGIONAL STATUS

UKRAINE only gives us scraps of news in which it mentions that it has harvested further, but we all know what corn harvested in such conditions means. A corn that has been wet since the harvest season began, a corn that may now be frozen, but which certainly retains high levels of aflatoxin and mycotoxins in it. The forecast for the next season is also quite pessimistic due to financial reasons, first of all, and then because of the war. It is seen at a level of 18-19 million tons, compared to 27 million this season and 42 million tons in the 2021 season.

RUSSIA indicates extremely serious quality problems. Russian goods have a major handicap due to ragweed and thus, they cannot compete in exports. The inferior quality downgrades it in front of other competitors in the Black Sea basin.

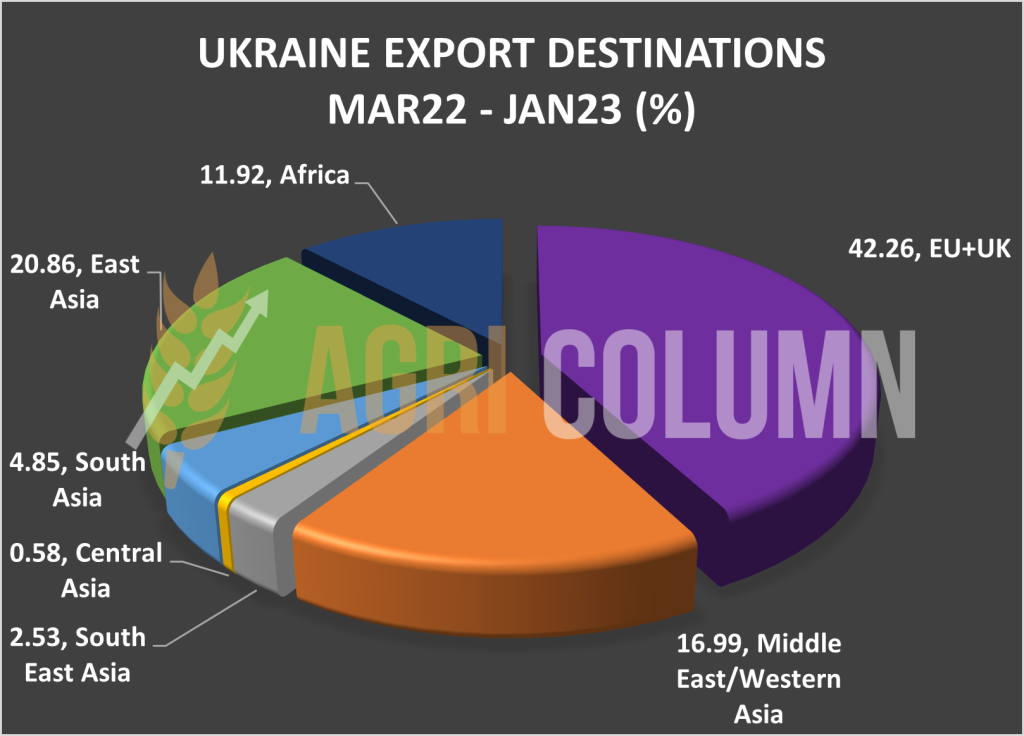

THE EUROPEAN UNION exceeded the level of 16 million tons in terms of corn imports. But here, for your information, we must also insert a graph that clearly indicates the distribution of Ukrainian goods. Leaving aside any emotion and narrative about poor African peoples, the numbers speak for themselves, namely that the European Union received 42.26% of all Ukrainian goods exported from March 2022 to today, January 2023. Africa received only 11.92%.

EURONEXT CORN – XBH23 MAR23 –278.75 EUR

EURONEXT CORN TREND CHART – XBH23 MAR23

GLOBAL STATUS

GLOBAL STATUS

ARGENTINA receives rainfall and improves corn crop ratings from previous days. 12% good/excellent (up from 5%), and 39% poor (up from 47% last week). The precipitation will continue until the middle of this week.

BRAZIL. Delay in starting Safra harvest. Rainfall is the main reason. Safra goes on the road with a handicap of at least 1.5 million tons. It is not much and can be recovered from Safrinha, which in turn is delayed in sowing, due to soybeans that cannot be harvested, again, due to rainfall.

CHINA. The entire component of global trade is waiting for February 1, 2023, when they will finish celebrating the New Year and, implicitly, create demand. It’s not long until we get there, only a few days separate us.

CBOT CORN ZCH23 MAR23 – 683 c/bu

CBOT CORN TREND CHART – ZCH23 MAR23

CORN PRICE INDICATIONS IN MAIN ORIGINS

CAUSES AND EFFECTS

Corn is proving to be a commodity in demand and its resilience in CBOT technical sessions is proof of that. Regarding the goods from the Black Sea basin, there are a few things that are worth explaining, namely:

- Russia can’t really compete because of the quality of the corn. This explains why they did not win the GASC corn tender.

- Ukraine has expensive merchandise, although appearances indicate that it is cheap. Adjacent and associated costs and the somewhat penalized quality of conditioning and harvest times are elements that downgrade it from the point of view of competition in the basin. At its origins, the commodity is cheap, but the associated costs make it expensive. Corridor waiting times in Istanbul for inspection only add to costs. A one-day wait costs a minimum of $15,000 and the wait time ranges from 10-40 days. By relating the waiting cost to the tonnage, we deduce an important contribution to the price.

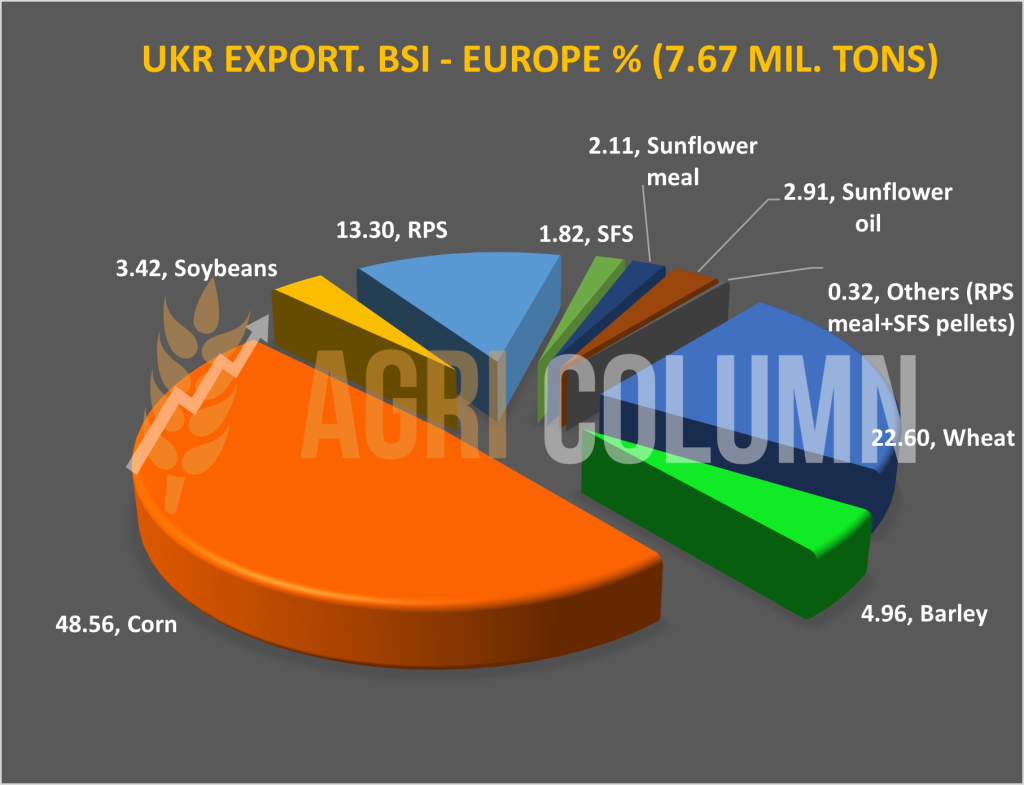

We justify what we said by inserting a graph of the goods that left via BSI (Black Sea Initiatives – the grain corridor) and their component by commodity category. 48.6% of the 7.67 million tons shipped via BSI to the EU is nothing but Maize.

Romania clearly has a very important competitive advantage. Corn of Romanian origin is of very good quality and has no attached costs. From Constanța it is free to go anywhere, without any additional control. But availability of volumes is a parameter that makes it low in volume and availability.

Please observe the situation of the ships that want to enter Romania via Sulina and the state of Constanța port, by comparison with the ships from the Corridor, which depart from Odessa – Pivnyi – Chornomorsk. The image generates the answer. The corridor is extremely expensive and requires quality certifications, compared to Romania, which, being a EU Member State, obeys the rules of not asking for quality certification through sanitary-veterinary certificates.

In the support of corn, one more thing must be highlighted, namely the demand, which will come from China. They will clearly be out shopping soon, and we know well that this country demands a lot of corn. They are with purchases at a level of around 20.6 million tons and have a requirement of at least 26-27 million tons, otherwise this threshold will be exceeded. The population of China has enough savings from the lockdown and will want to travel, so the demand for ethanol made from corn will absolutely increase.

Conclusion: the corn price trend must be stable in the coming period and demand will have to increase from the China factor. Argentina, through precipitation, would reduce the pressure, but nothing is played. But in general, what starts badly, ends badly.

LOCAL STATUS

Rapeseed quotations in the port of Constanța are at the level of MAY23 minus 25 EUR/MT. This indication calculates a level of 515 EUR/MT. At the processing level, the quotations are MAY23 minus 35 EUR/MT, a fact due to the logistics cost (the difference between Constanța and the Processing Units), i.e., a level of 505-510 EUR/MT. The new crop is also prized. Primary indications are AUG23 minus 30 EUR/MT. It is an initial indication that provides support in estimating farmers’ incomes.

CAUSES AND EFFECTS

European rapeseed imports forecasts increase by 0.6 million tons and thus, rapeseed receives a price support, even if it is not yet substantial. This is the motivation behind the increase in Euronext indications. Already in the port of Constanța, rapeseed is located at a higher price level in terms of FOB values, namely an indication of 606 USD/MT, so 557.5 EUR/MT, according to the parity of 1:1.087.

EURONEXT RAPESEED – XRK23 MAY23 – 536.25 EUR

EURONEXT RAPESEED TREND CHART – XRG23 FEB23

REGIONAL STATUS

No change from last week in the European outlook, nor in Ukraine and Russia for rapeseed. The state of vegetation is in the same normal regime for this period. The coverage request is executed at a normal rate, referring to the processing units. Various estimates for Ukrainian rapeseed are ventilated, but it is not a good time to count, because of the period we are in.

GLOBAL STATUS

CANADA, off season

AUSTRALIA, off season.

ICE CANOLA RSH23 MAR23 –840 CAD

ICE CANOLA TREND GRAPH – RSH23 MAR23

COMPARATIVE GRAPH. PETROL-RAPESEED-CANOLA CORRELATION

CAUSES AND EFFECTS

Rapeseed is waiting. This is self-expression. Support can come from two places:

- A higher level of EU imports, which was partially fulfilled. In June-July an import level of 6.5 million tons will be reached (an increase of 0.6 million tons per year), which means that the Demand for rapeseed in Europe is increasing.

- China, which will go out for purchases and divert Australian freight flows, which will no longer arrive in Europe, but will be shipped to this Destination.

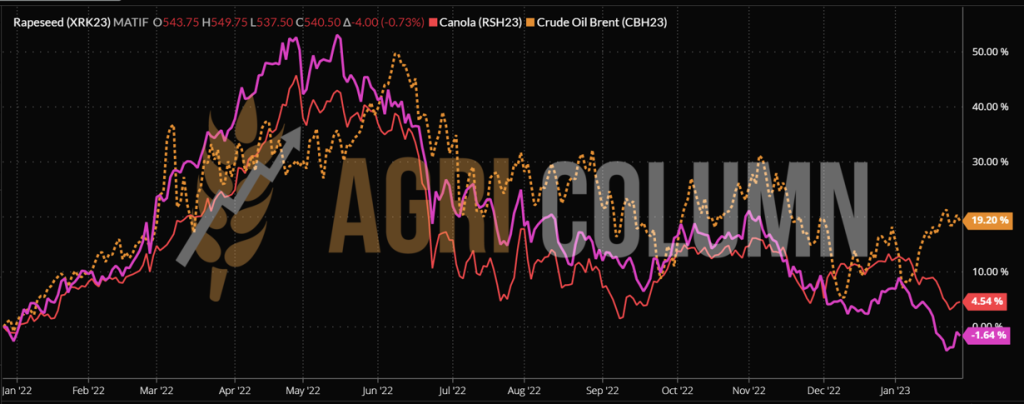

The third supporting factor is the price itself. Even Australia can’t afford to sell below a certain level, so discounting and competitiveness have a limit. And the port of Rotterdam indicates an increase of 26 EUR/MT of rapeseed oil to 1063.5 EUR/MT. Of course, Petroleum and Palm Oil also have their place in the rapeseed price equation.

LOCAL STATUS

Port Constanța remains in the 555 USD/MT area for sunflower seeds for now.

HIGH OLEIC sunflower seeds are quoted at a base level of 565-570 USD/MT.

Processors are correlating and indicating a trading base of 545-550 USD/MT in DAP parity Processing Units.

CAUSES AND EFFECTS

The pressure of the lack of demand is felt. The European Union is not so active in the demand for sunflower oil at the moment. Prices are under temporary pressure at 10 USD/MT lower, but 6PORTS is pointing us up 7.5 USD/MT, which is positive from the temporary dip. It’s barely the end of January, and a potential escalation of the conflict coupled with reduced processing in Ukraine would mean support for sunflower seed prices.

REGIONAL STATUS

UKRAINE remains in the same landscape of poor crude oil exports, intermittent processing and markets that once belonged to Russia are now within reach.

RUSSIA maintains zero duty on crude oil exports and registers new sales in Turkey, their traditional partner. The flower scrap, on the other hand, is taxed on export.

EU is very slowly shaping its demand, fueled by the glut produced by cheap Ukrainian goods.

GLOBAL STATUS

ARGENTINA and its particularities: sunflowers are sown from north to south as soil temperatures rise. Sowing starts towards the end of July in the northern region and extends until mid-December (or even later) in the southern region. The harvest is from mid-October, for the north, and from mid-April for the south.

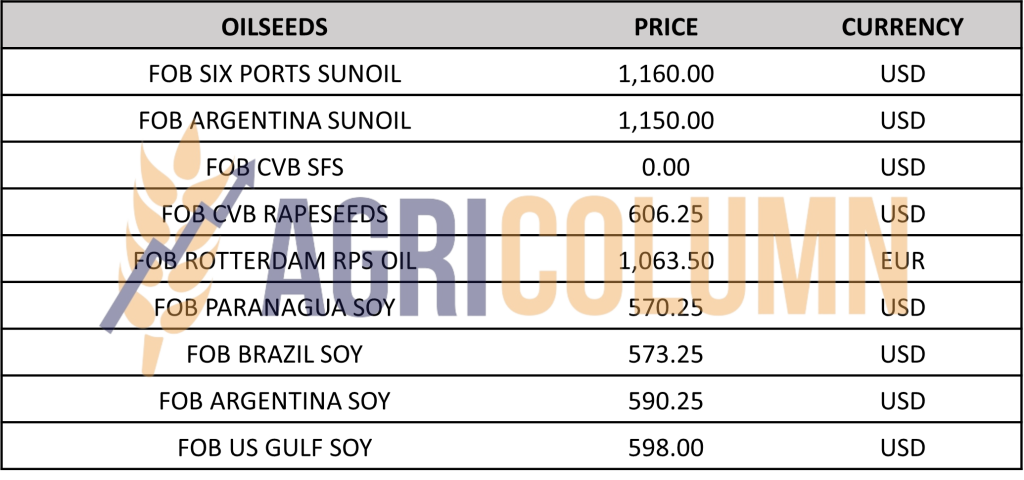

PRICE INDICATIONS FOR OILSEEDS AND CSFO IN MAIN ORIGINS

CAUSES AND EFFECTS

- The story of the import of Ukrainian oil into the European Union meets some quality-generated hops. Thus, the European Union no longer shows the initial appetite for Ukrainian goods. Quality is a parameter that becomes somewhat questionable.

The competition generated by cheap oil is obvious and the markets are saturated. But several details are lost sight of (or do not want to be noticed), namely:

- EU operating costs of processing facilities;

- The costs of European Farmers to produce raw material;

- There is no tariff or sanitary-veterinary barrier.

So Ukrainian commodities are putting a lot of pressure and we are talking about crude oil. Their discounts generate extreme pressure on the commodity market.

- Another country indicates the fragility of raw material volumes. Kazakhstan has introduced an export tax on sunflower seeds of 20%, but not less than 100 EUR/MT.

The tax will take effect in February. It is indicated that the sunflower seed export tax has been permanently introduced. We know that the production of this country is low, about 1.1 million tons from 1.1 million hectares, but it is a signal.

- However, support could come from Indonesia, but for now it is at the testing level. Namely, an obligation for buyers of palm oil for export to pass these volumes through the Exchange.

“Indonesia, the largest supplier of palm oil, is studying rules that would require exporters to trade at least some of their oil on local exchanges before shipping it abroad, to improve data control and transparency.

The aim is to have a benchmark price for a specific palm oil product on the exchanges that can be used to calculate export duties and taxes, Didid said Noordiatmoko, acting head of the Commodity Futures Trading Regulatory Agency, known as Bappebti. It would also provide more clarity on supply and demand, helping efforts to ensure a good supply of the local market, it said.

We have seen many companies that have sold palm oil to their sister companies, which most likely includes transactions involving so-called special prices,” said Noordiatmoko, justifying the plan. This means that government tax revenues from oil palm trees are probably not as big as they should be,” he said.

It’s only the end of January and things are about to take another turn. Already the Farmers in Poland, Romania and Bulgaria have reached a very low level of the way they accept and bear the competition generated by the discounts, the quality of the Ukrainian goods. Decisions at the European level must be taken. European farmers are constrained by regulations and this Green Deal, the Road to Hunger, as they clearly call it, while Ukrainian goods have no tariff or technical (sanitary-veterinary) restrictions.

LOCAL STATUS

In Romania, the price indications for soybeans are at the level of 530-540 USD/MT DAP processing units for non-GMO soybeans, with delivery after February 1, 2023. Between July 1 and January 22, 2023, approximately 147,000 tons of soybeans and 243,000 tons of soybean meal were imported.

REGIONAL STATUS

THE EUROPEAN UNION. Weekly soybean imports to EU countries were 101,522 tons, down 48% from last week. Total soybean imports increased to 6.07 million tons, but this is 18.61% less than last year in the same period.

Imports of soybean meal in the EU in the week of January 15-22 were 228,661 tons. Thus, total imports reached 8.9 million tons, which means a decrease of 2.5% compared to last year.

GLOBAL STATUS

USA. Weekly soybean export inspections from the US reached 1.8 million tons, being reported at the maximum value of market expectations, which ranged between 1.4 and 1.8 million tons, according to data provided by the US Department of Agriculture (USDA).

Total inspections since the start of the 2022/23 marketing year have reached 34.1 million tons, down 2.7% on last year.

China was the main destination, obtaining 1.2 million tons of US soybeans, with other relevant destinations being Germany (168,890 tons), Mexico (123,860 tons), Italy (71,602 tons), Taiwan (62,476 tons) and Bangladesh (57,678 tons).

USDA’s weekly data on net sales came in at 1.1 million tons for the week ended Jan. 19, up 16 percent from last week’s level.

BRAZIL. Brazil’s 2022/23 soybean harvest has started and reached 2% of the planted area of 43.4 million hectares, compared to 5.5% of the area at the same time in 2022, according to Conab. The country’s main soybean producer, Mato Grosso, has so far harvested 7% of the planted area, while last year at this time it was at 15.6% of the area. Conab estimates that the soybean harvest in the country will be 152.7 million tons.

Crop conditions in the Brazilian state of Parana have improved and those considered good have reached 81%, those considered average have remained stable at 15%, while those considered poor have now dropped to 4% of the total sown area. Soybean production in Parana is estimated at 21.4 million tons. Planted area remained stable at 5.7 million hectares, up 1.3% from last year’s 5.6 million hectares. In the 2021/22 agricultural year, the state planted 5.6 million ha and produced 12.2 million tons.

ARGENTINA. Sowing progressed to 98.8% of the expected area of 16.2 million hectares. Less than 200,000 ha remain to be planted, concentrated in the north of the area.

Recent rains in Argentina prevented further damage to soybean crops, according to the report issued by BAGE (Buenos Aires Grains Exchange). As a result, the crops assessed as good-excellent increased to 7%, 54% are assessed as being in poor condition, and the areas classified as average are now at 39%. Areas considered dry have decreased to 63%, and areas considered optimal and adequate are now 37%.

However, significant losses of the sown crop are expected due to high temperatures and lack of moisture in November, December and most of January.

Argentine farmers’ sales of new-crop soybeans climbed 230% during the week to 271,000 tons, a different trajectory than the 2021/22 crop, which fell 14.2% to 42,000 tons. Thus, the total sales of the 2022/23 harvest reached 3 million tons, compared to last year’s level of 6 million tons.

CHINA. Chinese imports of soybeans from Brazil fell in 2022 for the second consecutive year, according to data from the General Administration of Customs of China. Brazil soybean volume reached 54.39 million tons in 2022, down 6.45% from the previous year. Imports from other key suppliers, the US and Argentina, also fell as weaker demand amid a year of Covid-related disruptions and higher domestic production weighed on imports.

In 2022, China bought 29.5 million tons of soybeans from the US, down 8.48% from the previous year, while imports from Argentina fell 2.08% to 3.65 million tons.

Weak processing margins for most of the year kept demand from Chinese processors limited, and feed demand from pig farmers was also subdued amid weak farm margins.

In the January report Oil USDA’s Crops Outlook, China’s 2022/23 soybean crop is forecast to be nearly 2 million tons higher than last month at 20.3 million tons. The change reflects official data showing an increase in the area planted to soybeans in China – by almost 10% compared to the previous estimate. Increasing domestic soybean production is expected to reduce reliance on foreign soybean supplies to meet current domestic demand projections. Therefore, the forecast for soybean imports is reduced from 98 million tons to 96 million tons.

CBOT SOYBEAN ZSH23 MAR23 – 1,505 c/bu

SOYBEAN TREND GRAPHIC– ZSH23 MAR23

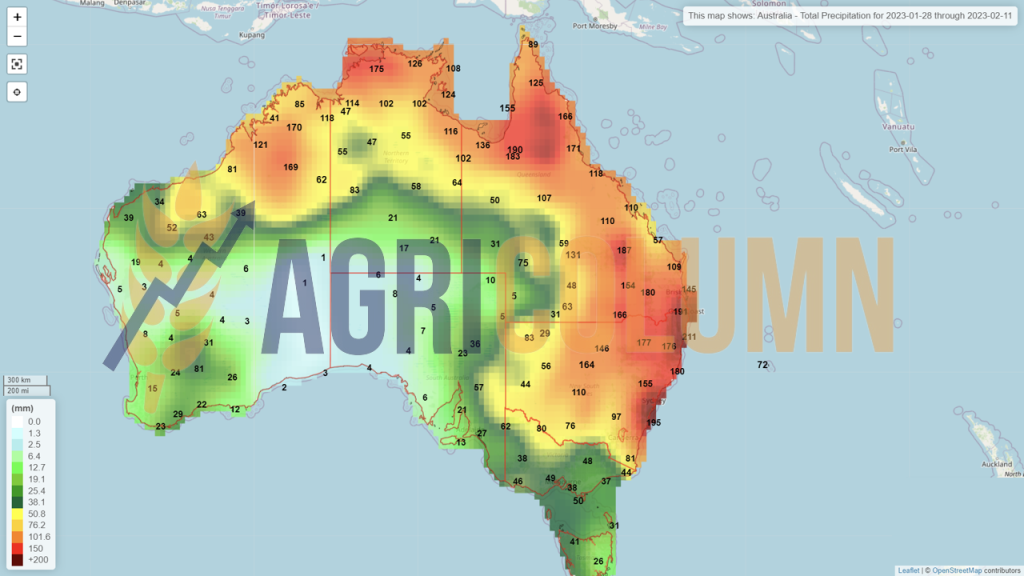

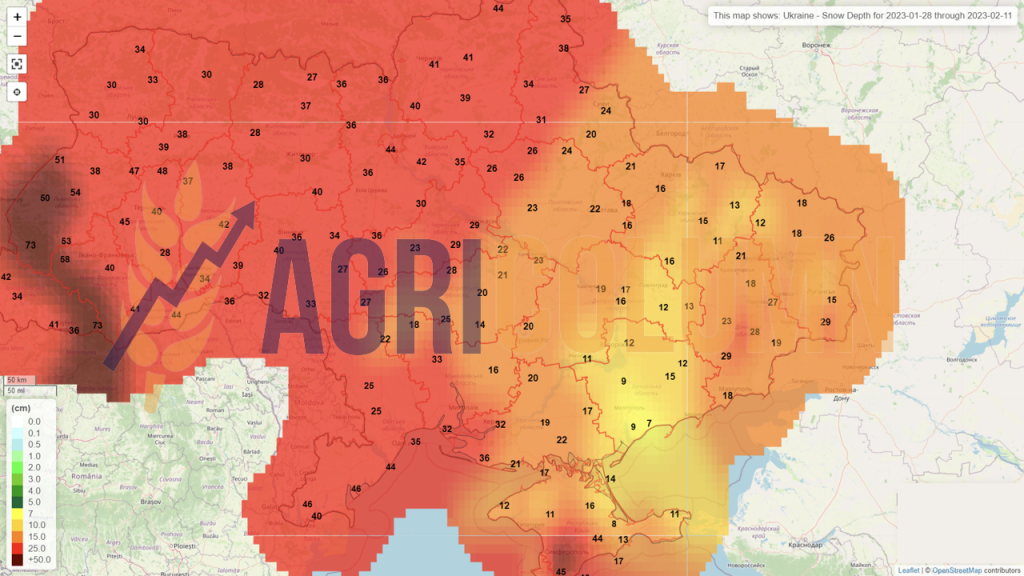

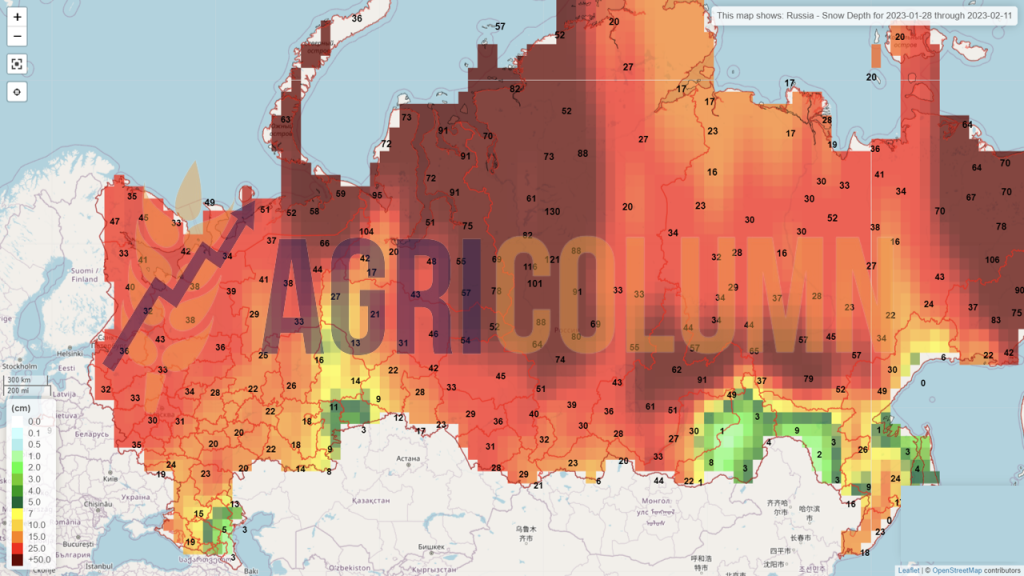

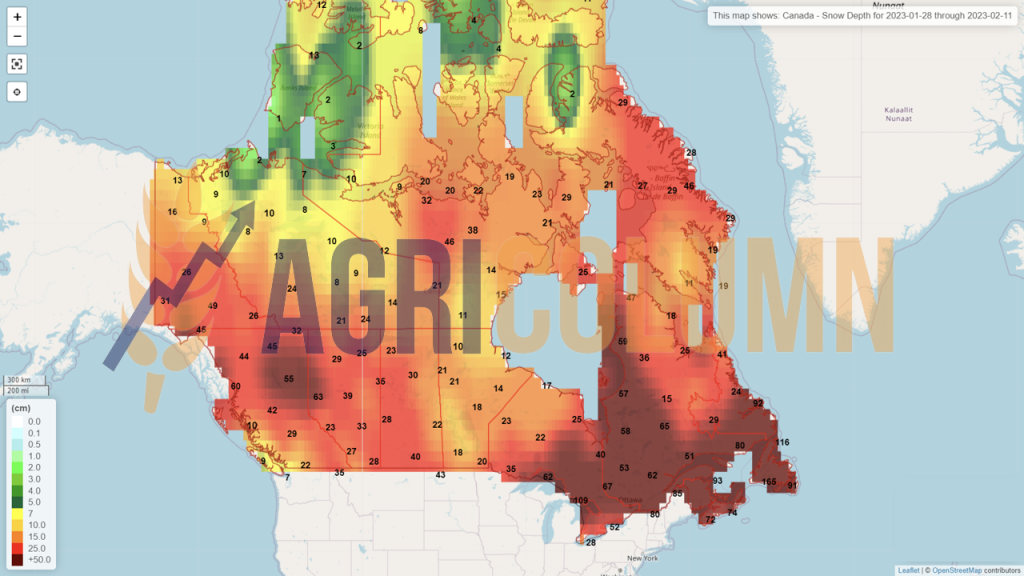

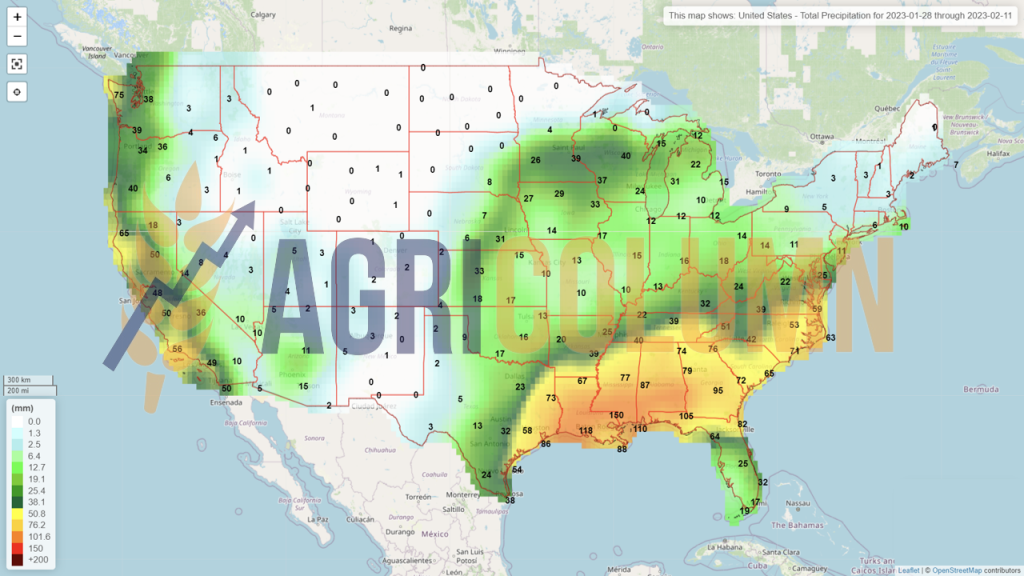

28 January – 11 February 2023

Romania (snow)

Europe (snow)

Ukraine (snow)

Russia (snow)

Canada (snow)

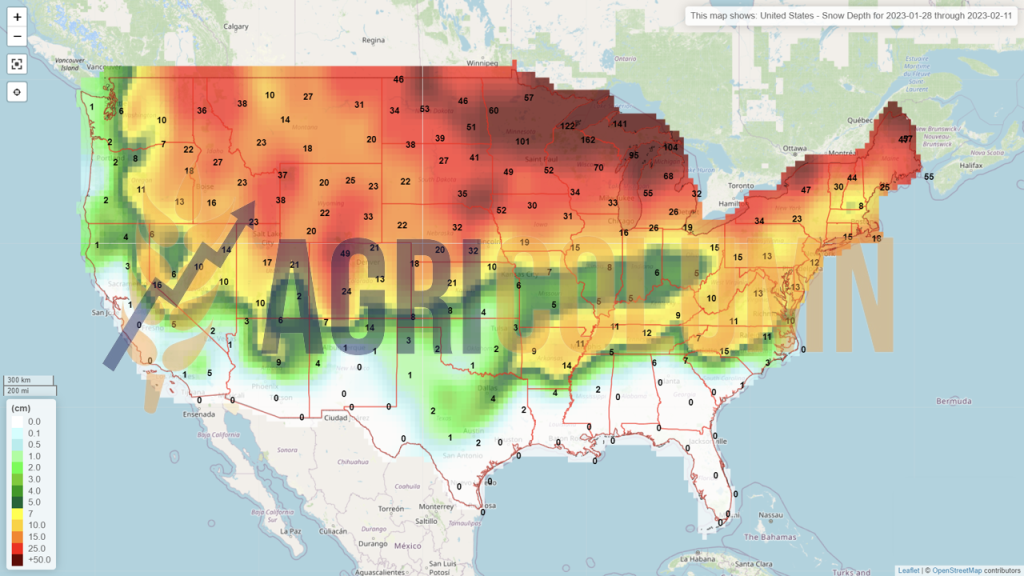

USA (rain)

USA (snow)

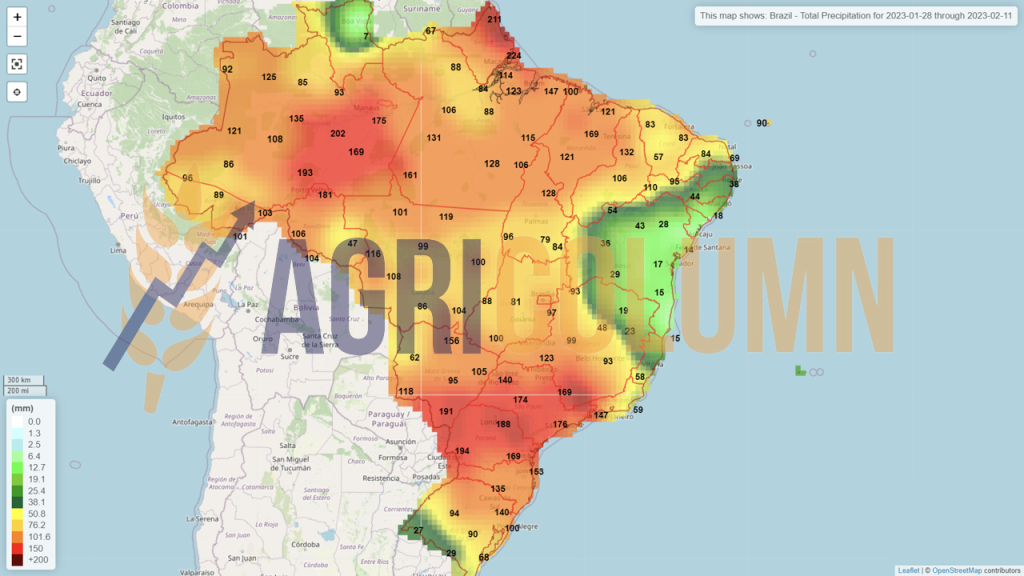

Brazil

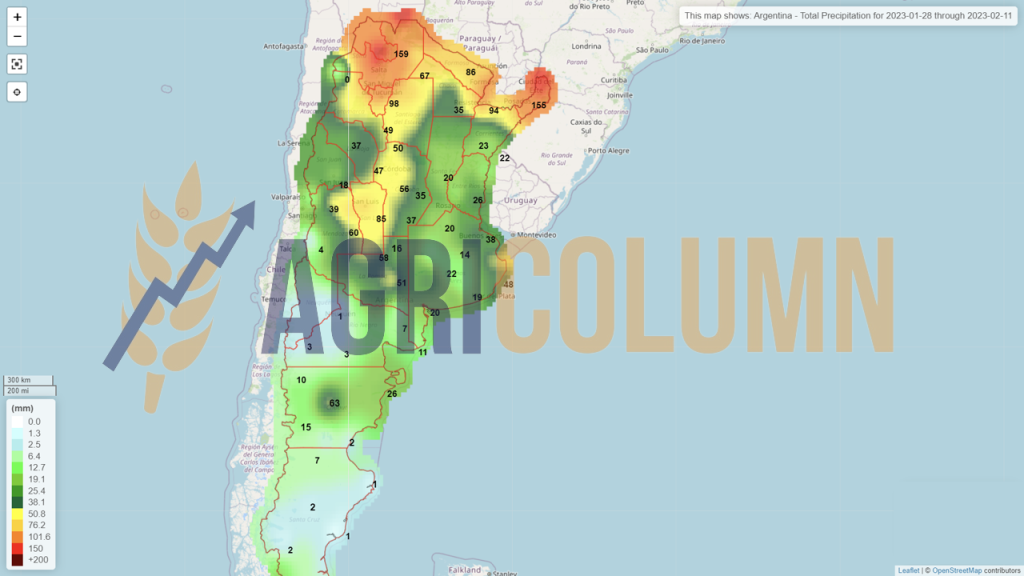

Argentina

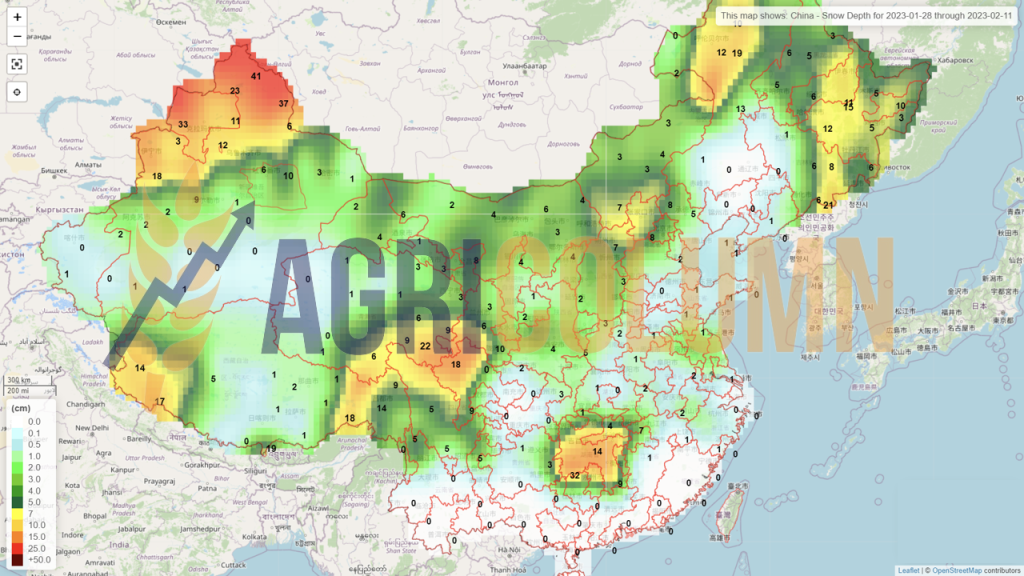

China (snow)

Australia