Today’s special market report is dedicated to WASDE (World Agricultural Supply and Demand Estimates), a market report of the United States Department of Agriculture. Below you can find information on global production, consumption and stocks for the following crops:

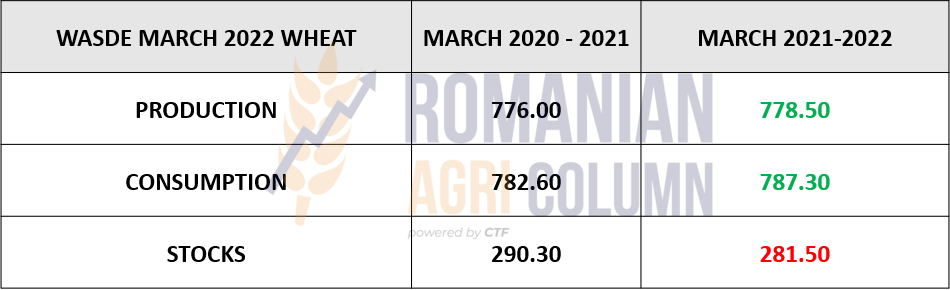

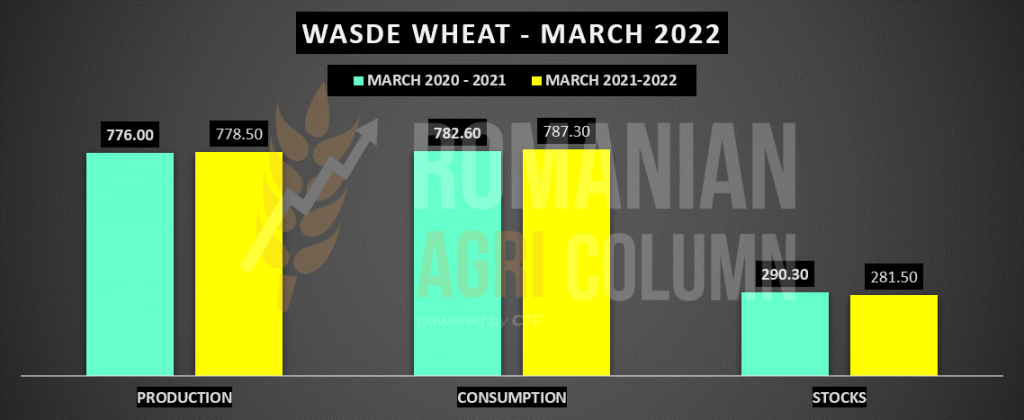

PRODUCTION: WASDE has generated a projection of global production rising from 776.42 million tons to 778.5 million tons. This increase was due to the revaluation of Australian production, which was increased by about 2.3 million tons to 36.3 million. Another marginal increase was recorded in India, of about 0.1 million tons. Marginal decreases were recorded in Russia (0.3 million tons) and the EU (0.1 million tons).

CONSUMPTION: WASDE generated a downward consumption projection of 0.8 million tons from 788.08 million tons to 787.3 million tons. This decrease comes from India and partly from Australia and Ukraine. Therefore, the internal consumption and, implicitly, the residual one decrease. In Ukraine, of course, the decline is due to the war caused by Russia.

STOCKS: WASDE generates a much higher level of stocks than last month, rising from 278.21 to a level of 281.5 million tons, so a level of 3.29 million tons. Stocks are closely linked to global trade and production. Thus, we have seen the production, we are now focusing on trade. We record a decline in global trade, estimated to decrease by 3.6 million tons, to the level of 203.1 million tons. The decline in global trade is driven by reductions in export estimates applied to Ukraine (4 million tons) and Russia (3 million tons). We therefore initially have a decrease of 7 million in global trade, which is offset by a rising level of Australian exports by 2 million tons to 27.5 million tons and India by 1.5 million tons. up to the value of 8.5 million tons. At the same time, destinations are declining due to the crisis in the Black Sea basin and very high prices. We see these declines on account of Turkey, Egypt, the EU, Afghanistan, Algeria, Kenya, Pakistan, Tanzania and Yemen.

WASDE MARCH 2022

PRODUCTION – CONSUMPTION – STOCKS

2.08 | -0.78 | 3.29

ANALYSIS

- Insufficient cuts in the Black Sea basin in Ukraine and Russia. The two countries were supposed to export about 16-16.5 million tons, but they are low in export potential by only 7 million tons cumulatively. Where is the rest exported? In the current state it is very difficult to tell.

- Compensation from Australian production going directly to exports, along with India, which exports up to 8.5 million tons, make the impact of global trade no more than 3.6 million tons.

- Destinations are still holding their breath and turning to their own stocks. It is logical, considering that there are still 95-105 days until the new crop harvest.

- A report that seeks to delay the situation that has effectively spiraled out of control in the Black Sea basin, where the two major players in terms of wheat exports are brutally leaving the scene, one as a victim and the other as an aggressor.

- The primary indication is bearish, but until when?

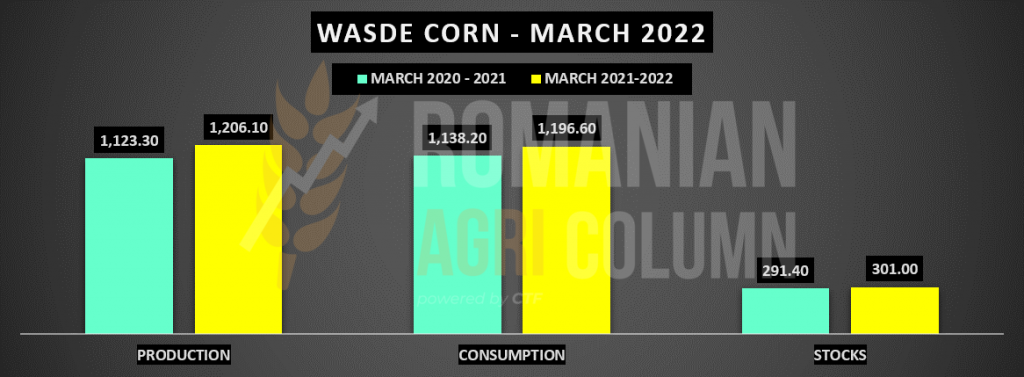

PRODUCTION: WASDE indicates a marginal increase in global production from 1,205.35 million tons to 1,206.1 million tons. Basically, we have an increase of 0.75 million tons. It comes from a compensation exercise that accounts for higher production in India by 2.5 million tons and Russia by 0.2 million tons and decreases the level of production in other regions. The decline comes from Argentina, where the deterioration is not as high as analysts estimated. Only 1 million tons are reduced, from 54 million to 53 million tons. Decreases are also recorded in the EU (0.2 million tons), Ukraine (0.1 million tons) and South Africa (0.7 million tons). At the same time, Brazil is left untouched in the forecast, with 114 million tons.

CONSUMPTION: WASDE indicates an increase in consumption of 1.43 million tons globally, from 1,1195.17 million tons the previous month to a level of 1,196.60 million tons. Consumption is increasing in the FSI complex, i.e., Food, Seed and Industrial. Consumption in US ethanol production increases by 0.635 million tons to 135.9 million tons.

STOCKS: WASDE generates a low level of inventories by 1.22 million tons, from 302.22 million tons to 301 million tons. The level decreases due to trade offsets. Thus, US and Indian exports are up, while Ukrainian exports are down due to the conflict on its territory. Imports to Egypt, Algeria, Turkey, Israel and Bangladesh are falling. Stocks in Ukraine and Russia are rising due to the impossibility of exporting. But they are declining in Argentina and South Africa, as a compensation, due to declining production in these countries.

WASDE MARCH 2022

PRODUCTION – CONSUMPTION – STOCKS

0.75 | 1.43 | -1.22

ANALYSIS

- A report that is intended to be neutral in all respects. Argentina is not degraded, according to estimates (only 1 million tons, compared to the estimated 3 million tons). Brazil is also left unchanged at this time. The assessment is correct, as about 90% of Safra is already harvested from the fields.

- In terms of stocks, here we see how the Ukrainian surplus is actually ignored, in the form that it is blocked and therefore cannot be exported at this time. The level to be exported from Ukraine is about 17 million tons and these figures would have had a much greater impact on the price route for maize, if it had been highlighted in WASDE.

- Neutral is synonymous with the reluctance of the USDA, which maintains still robust production figures in Argentina and does not synthesize Ukrainian exports on the grounds that it is 100% blocked.

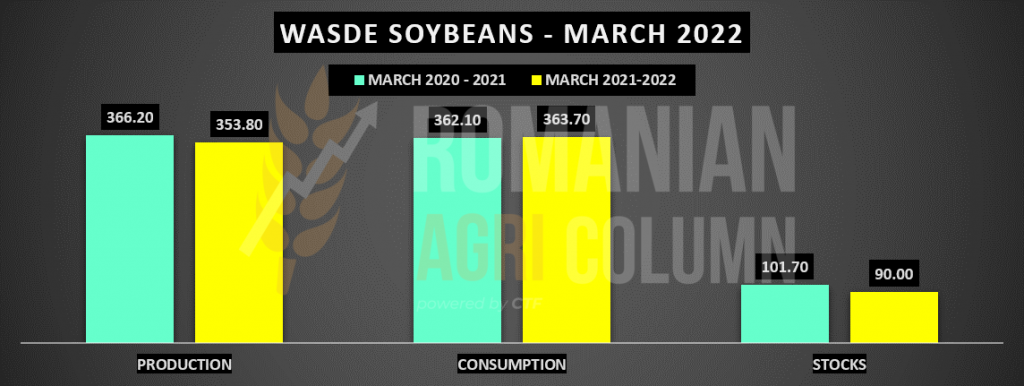

PRODUCTION: WASDE generates a decrease in soybean production by more than 10 million tons, from a level of 363.86 last month to a current level of 353.8 million tons. The declines are, of course, as we all expect in South America – effectively devastated in terms of soybean production. Thus, we note the degradation of 7 million tons in Brazil, from a level of 134 million to one of 127 million tons. Argentina follows with a decrease in production potential to the level of 43.5 million tons, starting from 45 million tons forecast (a decrease of 1.5 million tons). Paraguay is down 1 million tons from production to 5.3 million tons. We therefore have a very significant decrease in global production, which will lead to movements in the market for oilseeds and, implicitly, meal and vegetable oils.

CONSUMPTION: WASDE indicates a decrease in global consumption, driven by the exit from global trade of about 6.4 million tons of soybeans. But trade compensation will come from the United States, which will increase exports due to its decline in South America. However, global consumption decreased by 5.47 million tons, from 369.17 million tons to 363.7 million tons.

STOCKS: WASDE indicates a decrease in global stocks of 2.83 million tons, from 92.83 million tons last month to a level of 90 million tons. Declining stocks have a direct link to global production and consumption.

WASDE MARCH 2022

PRODUCTION – CONSUMPTION – STOCKS

-10.06 | -5.47 | -2.83

ANALYSIS

- Soybeans suffer from predictable degradation due to weather conditions in South America. La Nina once again takes her share of the South American crops.

- 10 million tons is a lot, but the US is trying to compensate and everything has to do with China’s claims that they are reducing imports by 30 million tons?!?!.

- Global trade is also suffering, but the largest share will go to the VEGOIL complex, where soy is a participant.

- A 100% bullish report for soy, but traders have known this for a long time.