This week’s market report provides information on:

LOCAL STATUS

The local wheat market has contracted quite sharply due to the zonal geopolitical effect, namely Russia’s alleged intention to negotiate a humanitarian corridor to release the approximately 70 cargo ships detained in Ukrainian ports. Thus, we noticed a sharp decline in European and American stock markets, fueled by this geopolitical impact factor.

Prices in the port of Constanța have dropped dramatically, to the level of 365 EUR/MT. After only 24 hours in which the investment funds, through trading algorithms, marked the profit by reducing the net long positions, the indications returned, as this news was only a subject that had to feed the speculative bubble generated by the war. The return was made quickly and we noticed at the end of Friday a level related to the port of Constanța of 385 EUR/MT as the primary indication.

These indications are identical in level, whether we are talking about the new crop or the 2021 season. The only difference is the price level of feed wheat, which for the new crop is set at a negative difference of 20 EUR/MT, while the old crop is penalized with 25 EUR/MT.

CAUSES AND EFFECTS

Panic was sown among farmers, many of them tried to sell goods, frightened by the sudden drop in price. It was a time of confusion and many fell into his trap, but not the farmers who benefit from the protection of the advice we offer, apart from this market report. For more information and details, draw us a line at [email protected] .

However, we have noticed many cases in which intermediary trading companies, not only locally renowned, try to take advantage of the lack of technical knowledge of farmers, proposing contracts that actually grind the potential profit from selling the goods.

We note that we do not have a positive outlook for such an approach that is clearly intended to lower the price by contractual clauses that are not customary in the market, nor do we agree on the way in which commercial and legal clauses are aggregated in such contracts. In short, the penalty clauses inserted and the way in which they are aggregated, including contractual parity, can generate differences of 10-15 EUR/MT.

The problem is one of awareness and farmers need to understand that they have legal rights, as well as obligations, in such contracts. Also, anyone who wants such protection that is subject to the individual consulting service can write to the email address mentioned above.

Another cause that will generate a deficit in the balance of profits and losses of farmers is the logistics. The imprint of the increase in the price level of transport is already evident in road, river and rail quotations. Regarding the most used of them, the road one, we note a 40-50% increase in the transport price. For a route of 18 EUR/MT last season, a minimum of 25 EUR/MT will be paid this season. The availability of means of transport will be another factor of growth in this whole logistics complex.

The effect of increasing the cost of transport is also spreading in the field of operation in the port of Constanța. The costs of electricity and fossils have already left their mark on the level of transbord, which has increased by about 20-25% in the case of Romanian goods. And all this growth complex on the background of logistics will be reversed at the beginning of the chain, to the farmer.

SHORT-TERM VIEW

Farmers need to analyze the market very carefully before generating sales. The market trend and its understanding are an extremely important chapter, which can make the difference between profit and loss for wheat raw material. What we see today is a mix of issues generated by Weather and Politics:

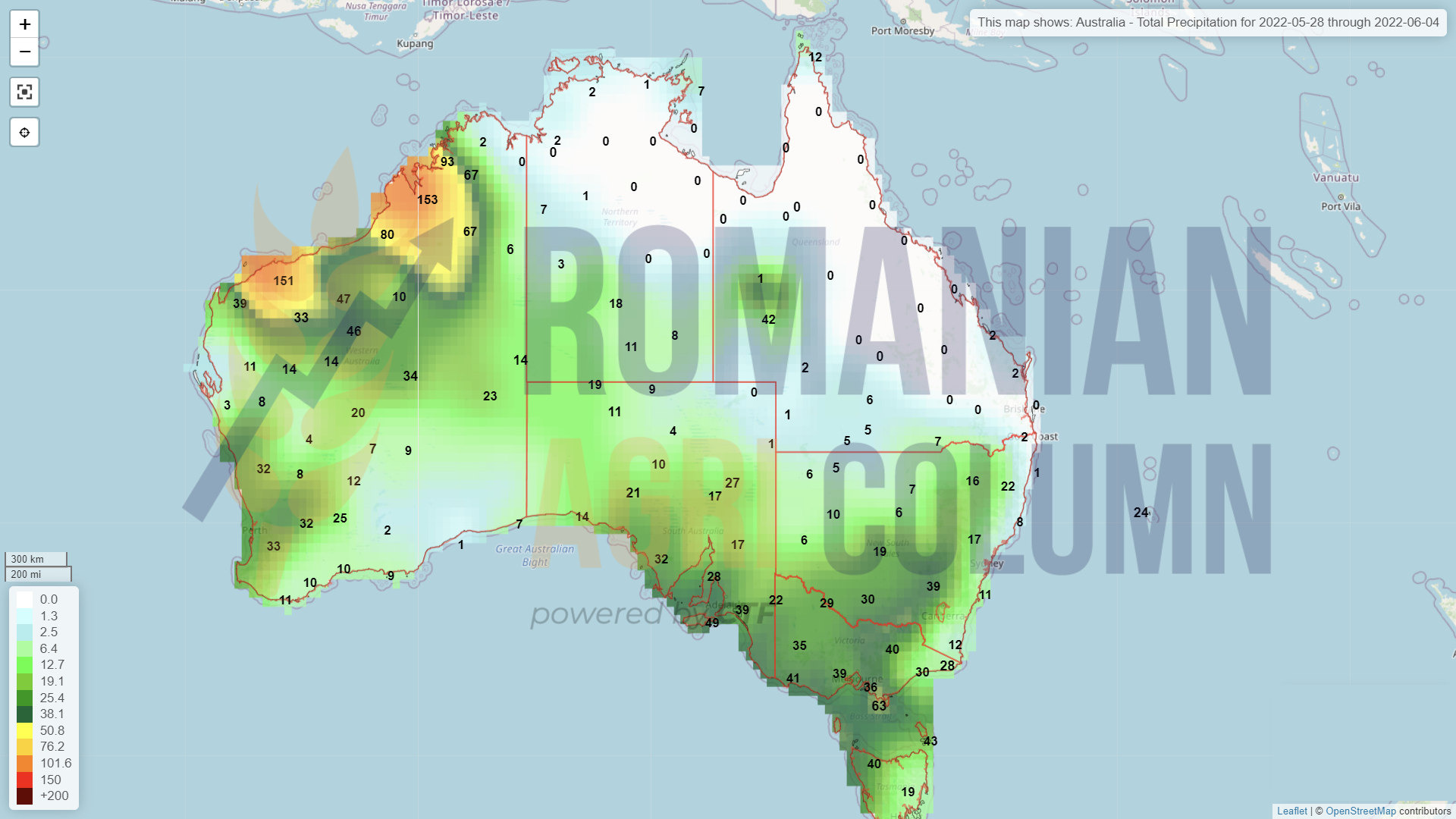

- If the announced rains come, Romania’s production level will exceed 9 million tons, with a maximum potential of 9.3-9.4 million tons. If they do not arrive, we will have a harvest volume of less than 9 million tons, most likely at the level of 8.6-8.8 million tons.

- Regional policy will also create problems through the unpredictable movements it will generate. News of a possible expansion will put pressure on prices. But these will only be fireworks for scholarships, things are already extremely clear.

Russia will not leave the Ukrainian territories unless a defeat is followed by a capitulation. It is the Russian gene and, following the evolution of the war, we can say that they have achieved their main goal. They cut off Ukraine’s access to the Black Sea, simulating interests in the north. It was obvious that they wanted to keep their interest in the north so that they could consolidate in the south. Russia wants to blackmail the world with food, and it does so by blocking Ukraine’s access to its Black Sea ports.

REGIONAL STATUS

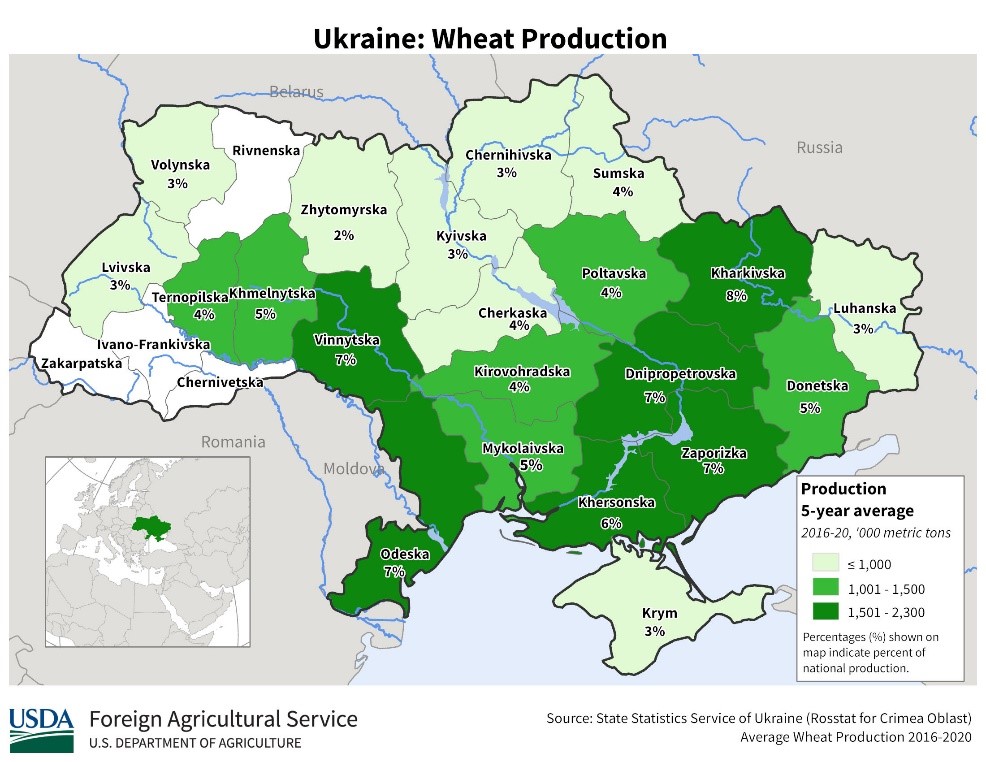

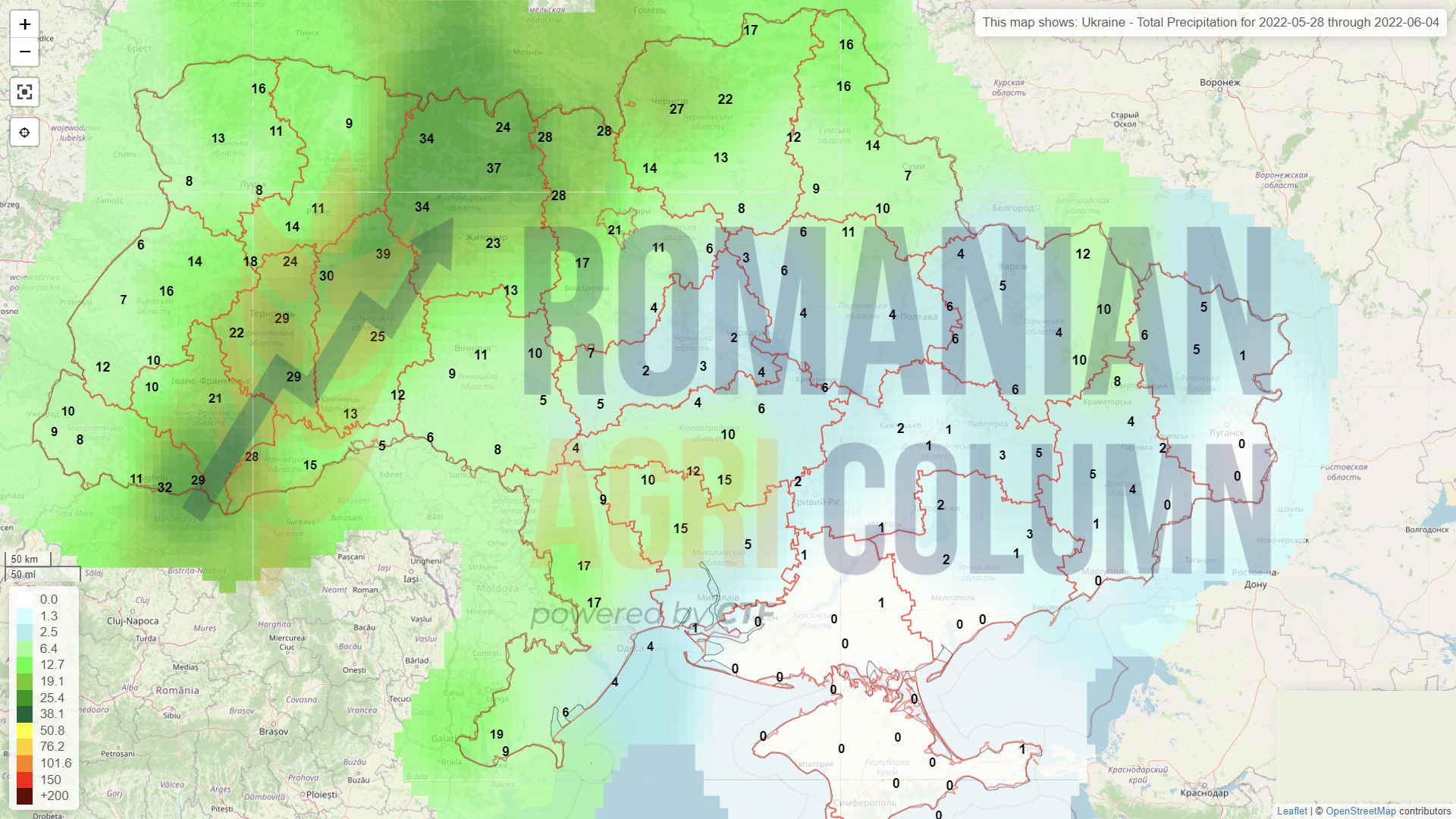

UKRAINE maintains its status, which we have mentioned in recent reports, of about 20 million tons of wheat as harvest volume this season. Ukrainian wheat looks promising, NDVI is up to expectations, and harvesting is expected to begin in early July 2022.

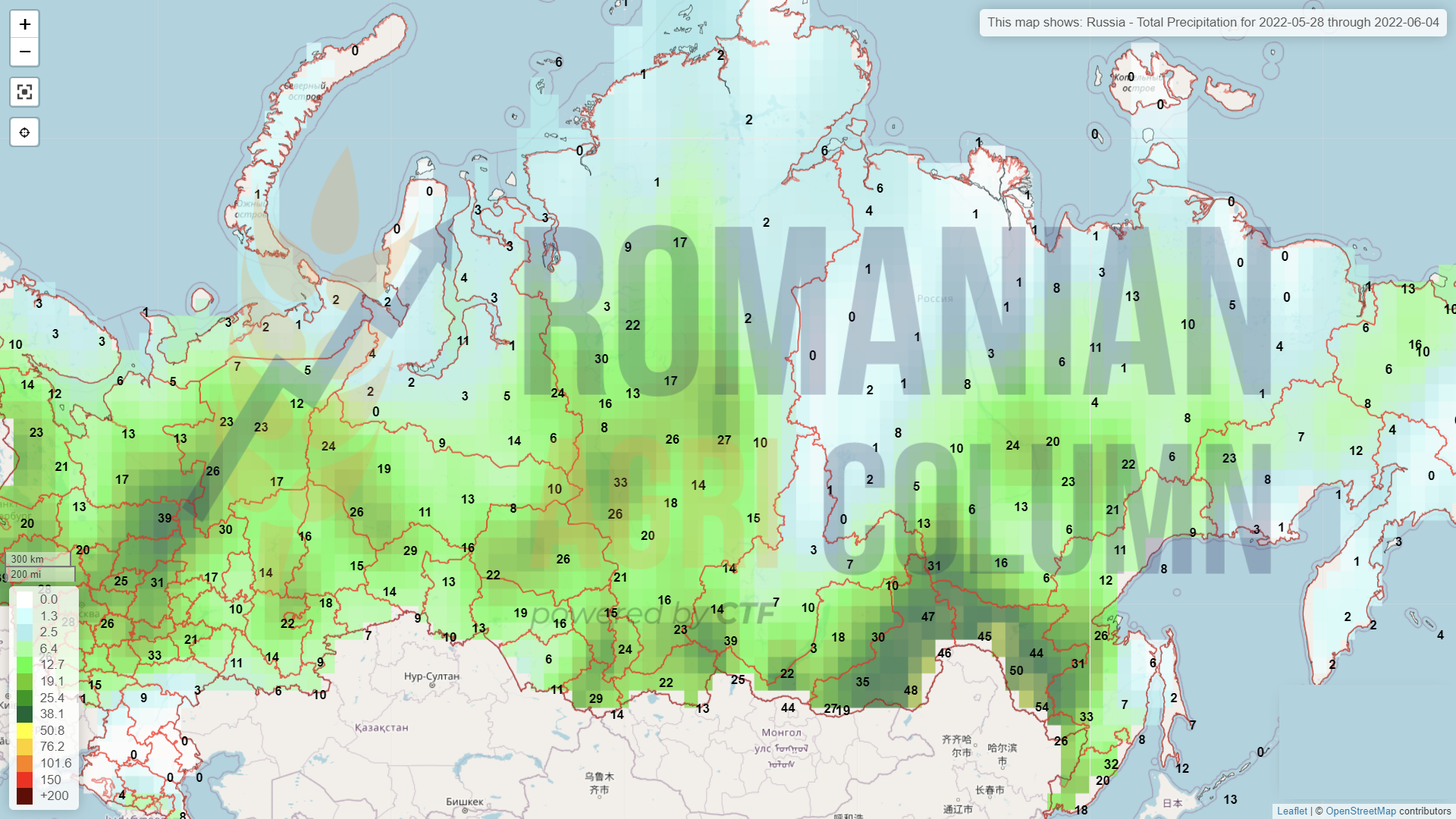

RUSSIA has the same volume norm as expressed in the May 12 USDA report, which is 82 million tons. The local analysis houses generate the same incurable optimism caused by maximizing the future benefits of the sale of goods. The probability that the Russian figures will be higher is partly due to the assumption of Ukrainian volumes on their account.

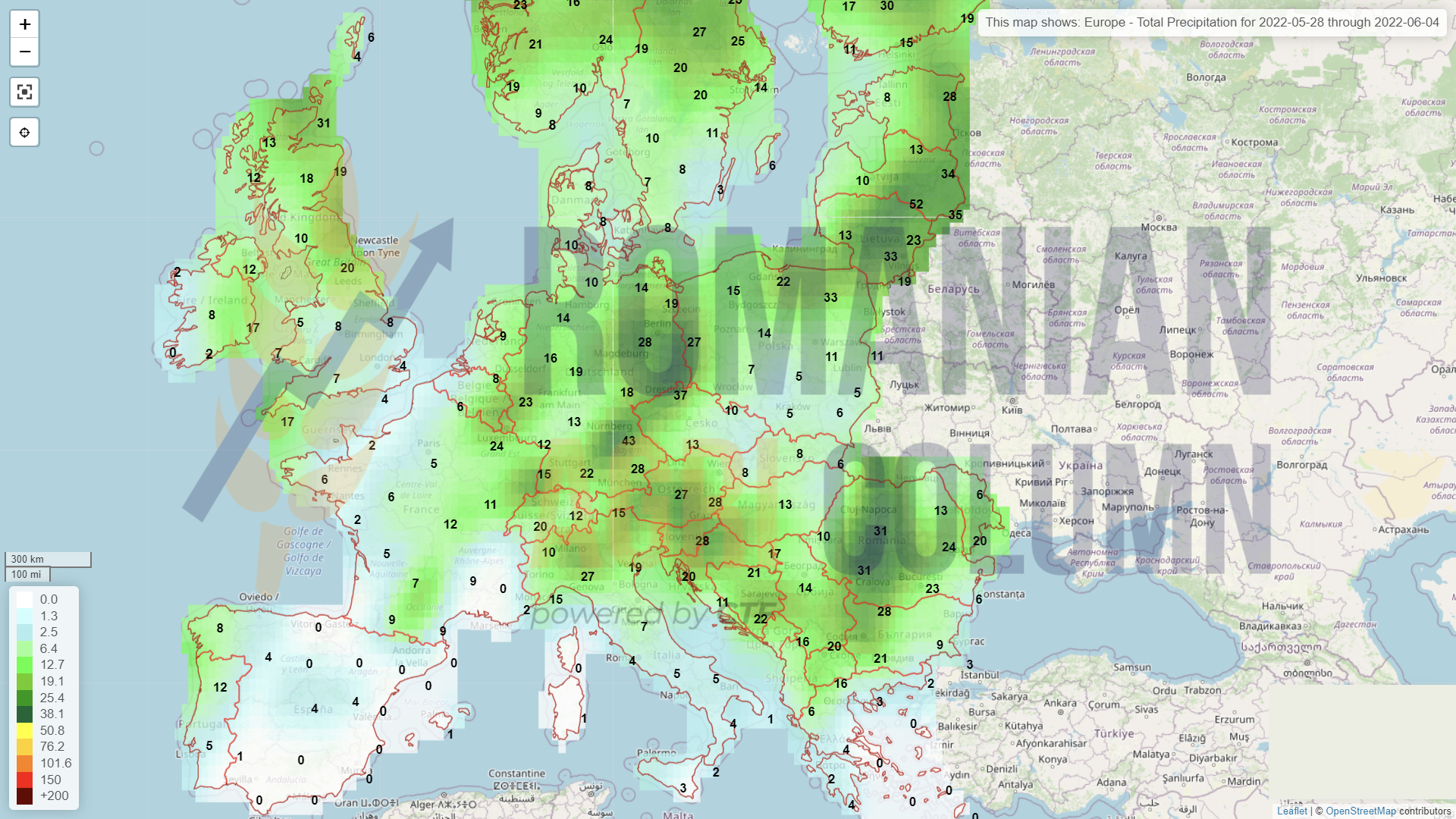

EUROPEAN UNION – the level of productivity per hectare decreases and we find the same status as last week. Moreover, precipitation will be absent in France and Spain until June 4, 2022, which will not bring benefits in terms of volumes, their estimation thus having no point of support, in the sense of recovery.

CAUSES AND EFFECTS

UKRAINE could face serious logistical problems at harvest time due to the areas with the greatest potential for wheat volumes and production, which are located exactly in the south of the country, in the path of conflict. Map with areas described below, USDA source:

RUSSIA. A heat wave will affect Siberia, with temperatures up to 5-6 degrees higher than normal – they will be close to 38-39 degrees Celsius, which, combined with the lack of rainfall in eastern Russia, could diminish wheat potential.

Also in this regard, we see a partnership created by Russia with Iran for wheat supply. The volume of goods that will be generated by Russia will reach the level of 5 million tons. In addition to other raw materials, wheat will be the main component of this primary volume indication. We also note here that Iran has a need of 7 million tons of imported wheat.

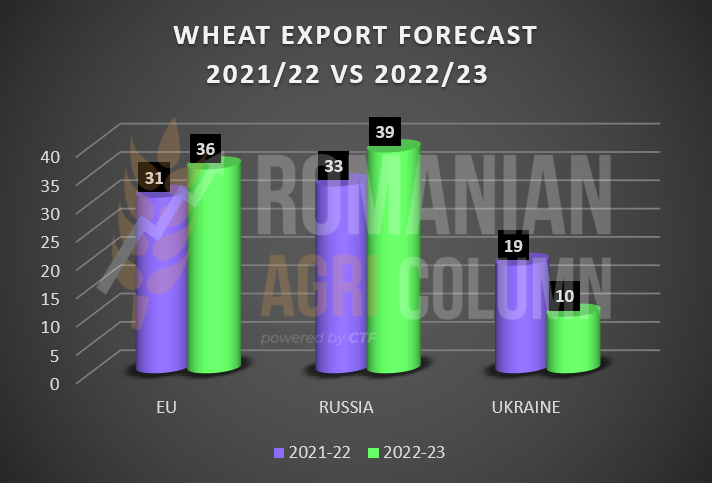

The European Union will generate a higher level of exports than last season. The primary estimate is 36 million tons. For clarity, we insert a regional chart, which estimates the export values 2021-2022 and the forecasts for the season 2022-2023.

North Africa, the Horn of Africa, and the Middle East are facing extreme problems, and Russia’s blackmail is just an attempt to divert attention, while building separate flows of goods and payments from the usual ones, which are blocked today by economic sanctions. Moreover, Russia wants to build large-capacity ships to move goods across the Caspian Sea on the Iranian corridor. Russia is blackmailing food into the world. It provides food and energy by blackmailing, and this will not stop. Don’t be fooled that it ends soon.

In other words, the price of wheat has no reason to decline, unless there is a recession very soon. But the FED is not very determined at the moment and we are very much looking forward to mid-June to see the side effects of FED monetary policy.

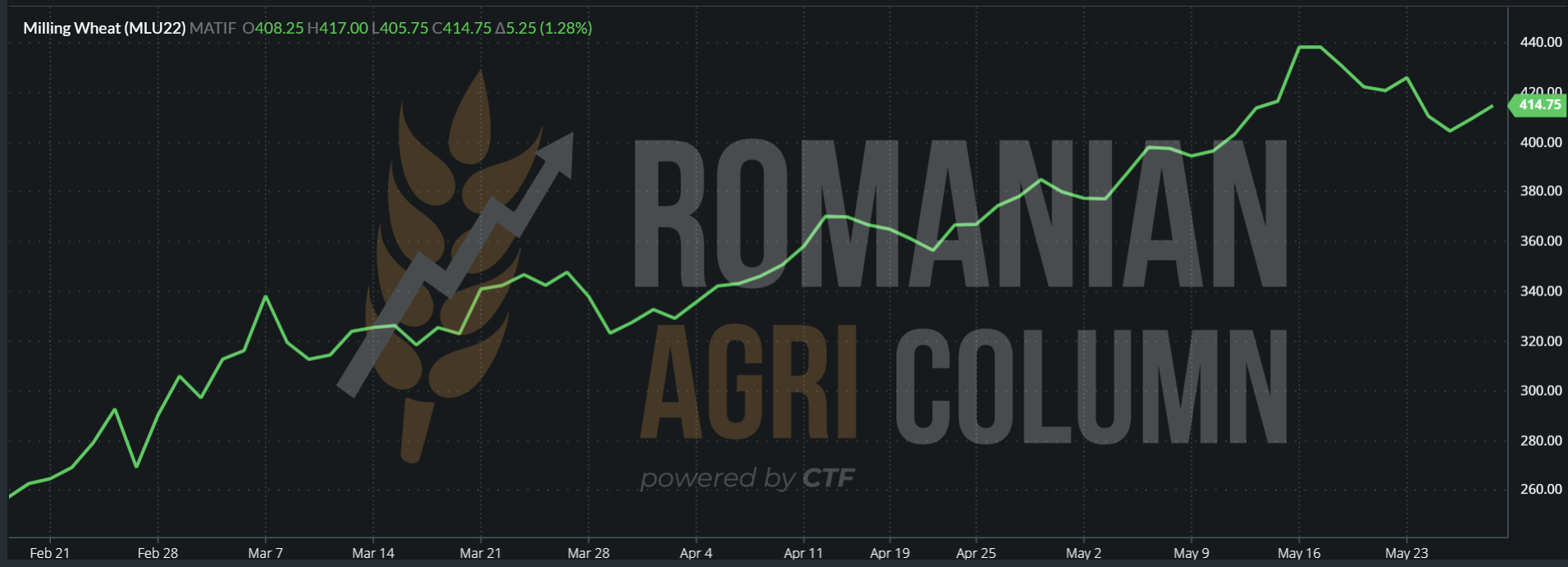

EURONEXT has fluctuated as described above, with investment funds making Profit Taking to return to growth in less than 24 hours.

MLU22 SEP22 at the close of May 27, 2022 – 414.75 EUR

WHEAT TREND GRAPHIC ON EURONEXT – MLU22 SEP22

GLOBAL STATUS

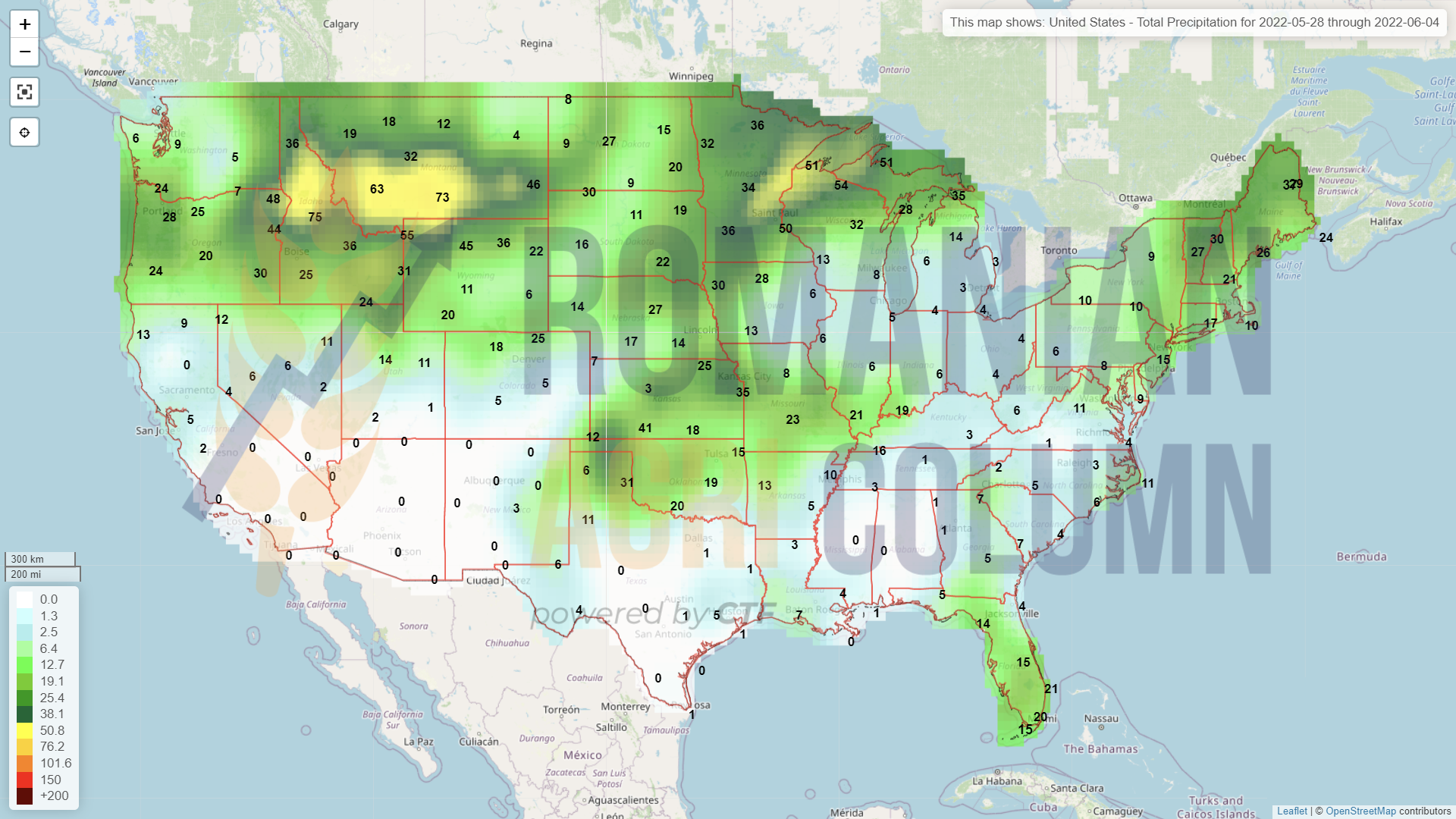

United States, even though it receives certain amounts of rainfall, has no positive note on the rating of winter wheat. The same level of 28% good to very good. The rest of the American wheat is in the same perspective as before.

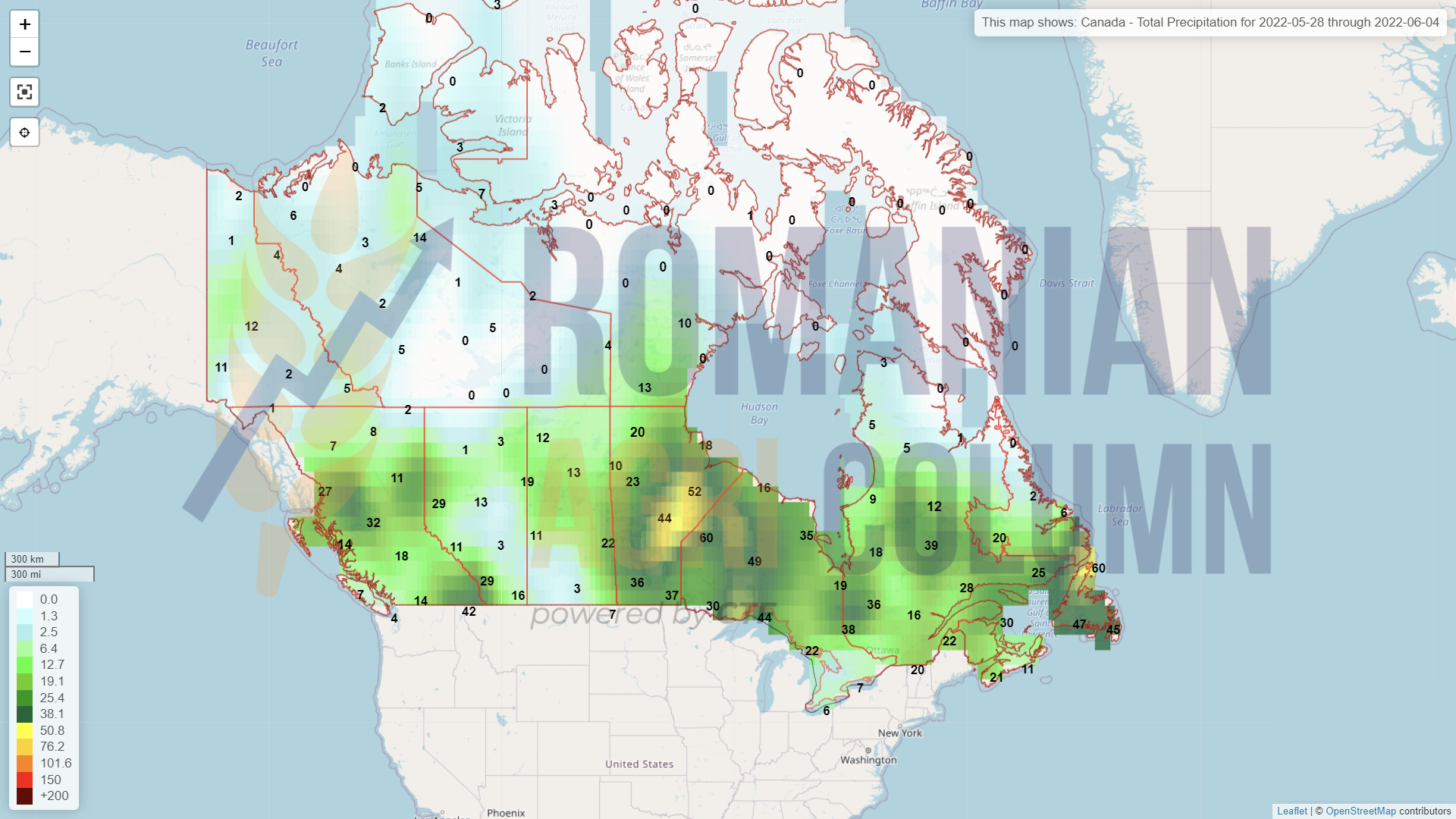

CANADA. Falling rainfall has a beneficial effect on Canadian wheat. The Canadian wheat crop promises a level of 32 million tons.

INDIA confirms the USDA wheat crop forecast below 100 million tons. Nothing unexpected, after the intense heat wave, the country was subjected to. But from 106 million tons, according to the USDA of May 12, 2022, to 99 million tons means another minus of 7 million tons, to which, if we add the difference from 111 million tons, the initial forecast, we reach minus 12 million tons.

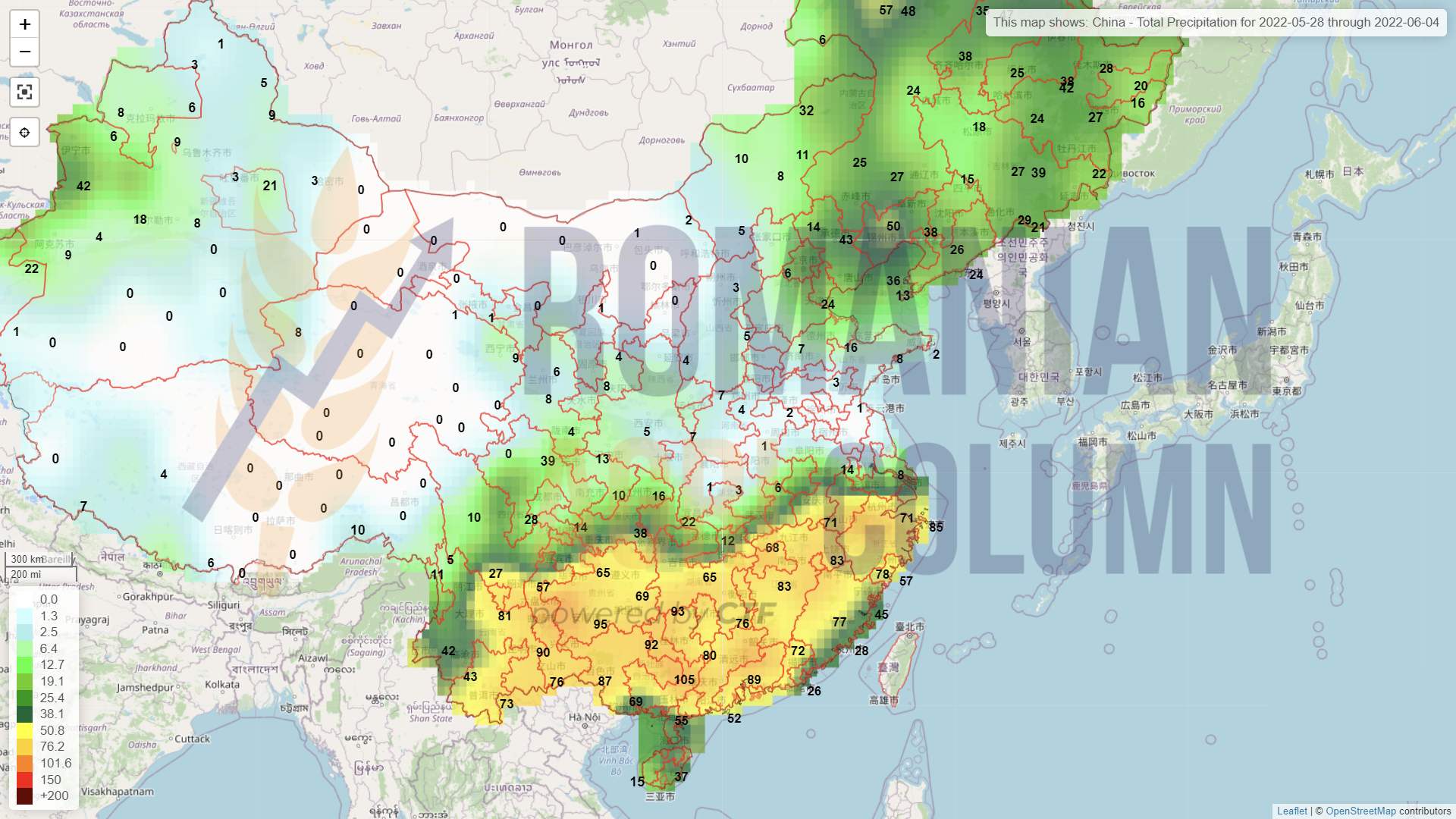

CHINA claims that the wheat crop has miraculously returned and predicts about 137 million tons of crop yields. At the same time, Chinese field analysts are unable to leave the cities due to the lock-down, so there is no official confirmation of these forecasts.

CAUSES AND EFFECTS

INDIA thus confirms the disaster it has suffered. The USDA’s bailout notes what we knew had happened, according to our sources. On the other hand, here we can find support for the price of wheat. India will have to resort to imports, which will come from Russia. At the same time, India says it will sell wheat to surrounding countries and Egypt. These statements sound like a confirmation that they, in turn, will also become a regional distribution market for Russian wheat. Nothing new from this perspective, only now things are becoming much clearer.

CANADA will supply the global wheat market. The initial estimate shows a level of 24 million tons, compared to only 15 million tons last season (the drought generated a low level of crop). This 9 million tons is a counterweight to India, but does not cover the difference of minus 12 million tons.

CHINA could be both cause and effect in the near future. The opacity of the regime does not allow for estimates and a clear view of the Chinese wheat crop, even if there are satellite systems that measure the NDVI of the crop.

SHORT-TERM VIEW | ANALYSIS

Russia will build a new wheat distribution hub in Iran. Many trade companies in Iran are ready to take Russian wheat and distribute it to the surrounding countries. As stated in previous reports, new distribution flows are taking shape in the Middle East and South Asia.

India confirms that it is a new distribution market for Russian wheat, and this will set up a Russian wheat route that will be distributed through Kazakhstan, India and Iran. After India, it is Iran’s turn to become a wheat distributor for Russia, which is thus trying to circumvent the imposed economic sanctions, especially those related to payments. Iran has already announced a barter payment system with Russia, which considers car parts as payment for wheat. Let’s not forget that Russia has car factories built by Renault on its territory, and as a big coincidence, Renault has very big interests in Iran.

Russia is also bluffing to release a statement saying it agrees to the creation of a humanitarian corridor for the release of captive cargo ships from Ukrainian ports. However, as we know the Russian strategy in such cases, we only kept the political statement waiting for Russia’s requests, which did not take long to appear. Russian status has called for the lifting of economic sanctions.

Of course, we were expecting something like this, and in the normal state of the European Union granted by the Anglo-Saxon Alliance, these demands were not considered, because they are nothing but blackmail. As a short-term effect, this has only exalted a part of the world, in the hope that the disadvantaged countries of Africa will be able to receive the long-awaited food. The situation there is extremely dramatic. Ethiopia, Somalia, Sudan are just a few areas where hunger is already a reality these days.

Russian blackmail and extreme problems in Africa, as well as in the Middle East, will have to be resolved by the European Alliance and the United States, joined by the United Kingdom. However, if Russia solves the supply problems in Southeast Asia and the Far East, it means that it will govern a very large market, to which we will add, without error, China. Indeed, the world will be divided into two spheres of influence. Russia and China will take Asia as a whole.

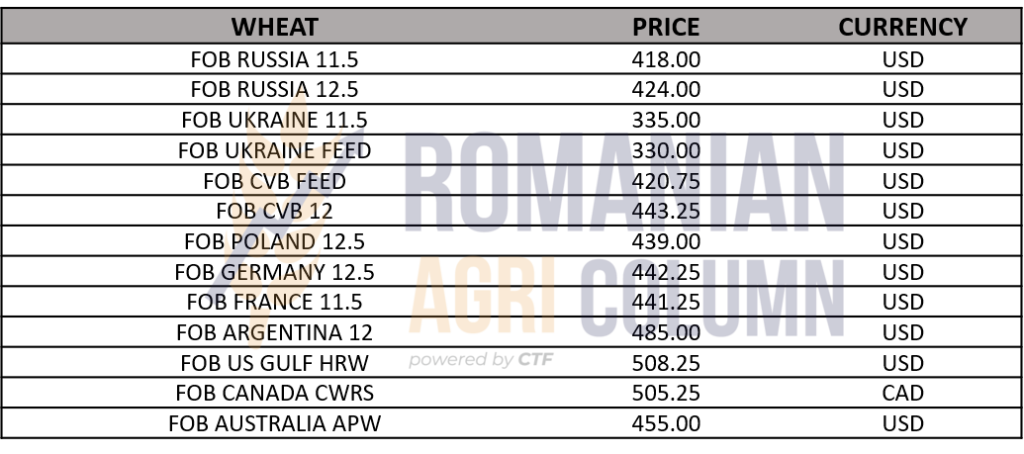

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

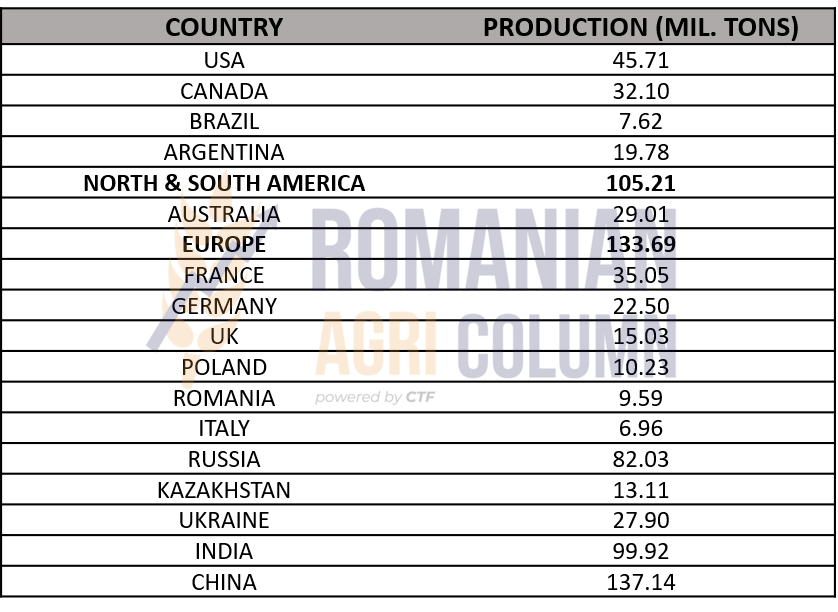

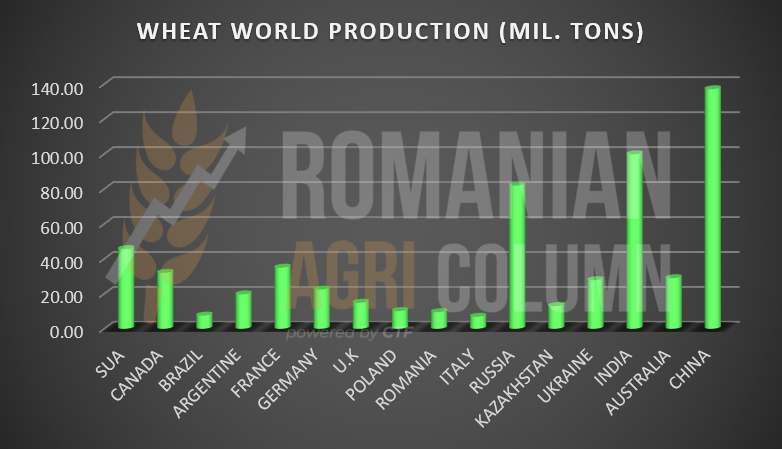

WHEAT PRODUCTION GLOBALLY – MAIN PRODUCING COUNTRIES

LOCAL STATUS

The connection between feed wheat and barley has been detrimental to barley in recent days. The price level displayed in the port of Constanța has deteriorated, according to the decrease in other raw materials, amid the news that Russia will allow maritime corridors for captive ships in Ukrainian ports. But no ship captain assumes the passage through areas mined by Russian naval forces, especially since Russia’s attempt was, in fact, an attempt to lift economic sanctions against it.

Thus, the new crop barley has an indication of 355 EUR/MT in the CPT Constanța parity. And time is running out and we will soon be in the second half of June, when the quantities sold will have to be exported 6-7 months in advance.

CAUSES AND EFFECTS

The market may be delayed in delivering the goods due to the weather. If it rains, there will be delays and the effect would be to spiral up the price level.

REGIONAL STATUS

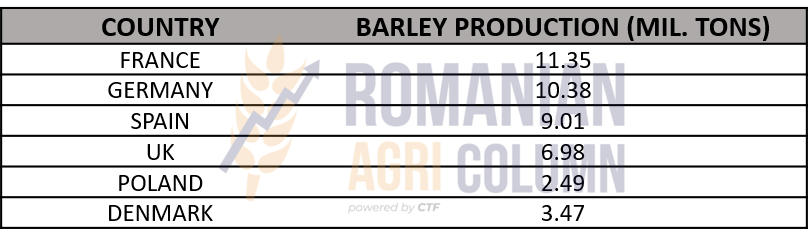

European feed barley projections are shrinking due to declining production per hectare. France, in particular, is lowering the forecast due to a lack of rainfall.

The European Union will therefore generate a projected level of 51.5 million tons of feed barley, and the table and graph show the main barley producers and their crop forecast at EU level.

GLOBAL STATUS

AUSTRALIA promises a level of 11.7 million tons of barley, so it will be a very important player in the market, along with Canada.

CAUSES AND EFFECTS | ANALYSIS

The correlation with feed wheat should generate an increase in the price of barley in the next period, given that the effect of the Russian announcement was short-lived but conclusive due to the impact on investment fund activity.

In general, the difference between Constanța and Rouen is set as a discount. 20 EUR/MT in the negative direction is the positioning of the price in the Port of Constanța. So this equivalence is still maintained – 375 EUR/MT Rouen vs. 355 EUR/MT Constanța, delivery July 2022.

LOCAL STATUS

The price indications generated by the buyers in the port of Constanța are at the level of 320 EUR/MT for the old crop and 310 EUR/MT for the new corn crop. What we notice compared to the previous days is the decrease of the price by 15 EUR/MT for the old crop, from 335 to 320 EUR/MT.

It is, as I wrote about wheat, the effect of Russian political games, namely the announcement that it approves humanitarian corridors for the release of ships loaded with corn, wheat and sunflower oil.

Rainfall is expected to arrive in Romania this weekend and we hope it will not be late, as it is crucial for corn cultivation.

The port of Constanta is still very crowded due to Ukrainian goods and it is very difficult to keep up. But the problems will soon intensify. Romanian barley and rapeseed are harvested in the first half of June, and flows from Ukraine do not stop.

As regards the import or transit procedure for goods from Ukraine, it has been amended by the European Commission. In short, the Commission says that Union law does not require any veterinary or phytosanitary certificates for goods originating in Ukraine and leaves it up to EU countries to take samples to verify that the goods comply with the Union’s food safety requirements. The recommendation also comes with the suggestion that these controls be proportionate and non-discriminatory.

CAUSES AND EFFECTS

The weather will be the main generator of causes in the next period. The precipitation that is forecast to arrive will be able to determine if the Romanian crop will be good or not. The effect will certainly be beneficial for Romanian farmers.

We remind you not to sign forward contracts unless you are sure that you can deliver these goods. Due to an unfulfilled contract, Romanian farmers will suffer financial losses that should not be found in the farm balance sheets this season.

Logistics will bite large sums, as in the case of wheat, from the price of the goods at the origin, i.e., on the farm. It is a cause that ends financially. Therefore, those who can transport the goods with their own means are advised to do so for cost efficiency.

Another cause with an effect on price pressure is the selling value of Ukrainian goods. The indications for sale in DAP Reni were quoted at 240 USD/MT. The equivalent in EUR is about 224.3 EUR/MT. Reni is Romania’s border point with Ukraine. More precisely, it is about the Galati area, Romania.

SHORT-TERM VIEW

The weather will be the arbiter of the price in the next period. The price of corn will only be sustained for a long time. Ukraine will increase and calibrate the volume of corn that will leave the country over time. Already despite the blockages, we see much larger tonnages finding their way to Europe.

The current support will also come from the consolidation of European and American markets. Whatever happens across the ocean impacts Europe and the Black Sea basin. But within 2-3 weeks, there will be a price difference between the old and the new crop. As the outline of the new crop clears, the price difference between the two crops will merge, in a positive or negative sense, against the background of the calibration of the new crop and the start of the Brazilian harvest in mid-June.

REGIONAL STATUS

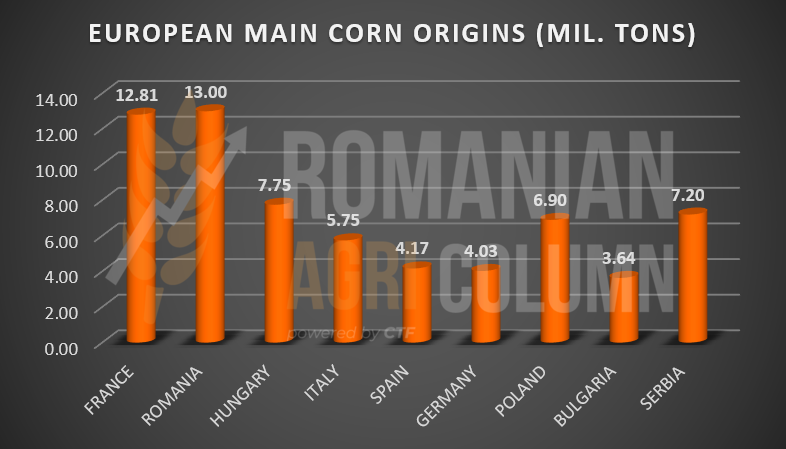

THE EUROPEAN UNION is stationary in terms of crop levels, remaining at a level of 66-67 million tons (68 million tons – estimates by European analysis houses). However, in these estimates, Romania is already downgraded by 2 million tons, due to the weather. If some time ago, 15 million tons were standardized, today the estimates go to 13 million tons. And all just because of the lack of rainfall and water supply in the soil. France is also degraded, as you can see in the table and graph below:

UKRAINE, in the light of the latest developments, could generate a crop of 23 million tons of corn, but the pace of exports is what will ultimately dictate the success of Ukrainian corn, taking into account the volumes not exported.

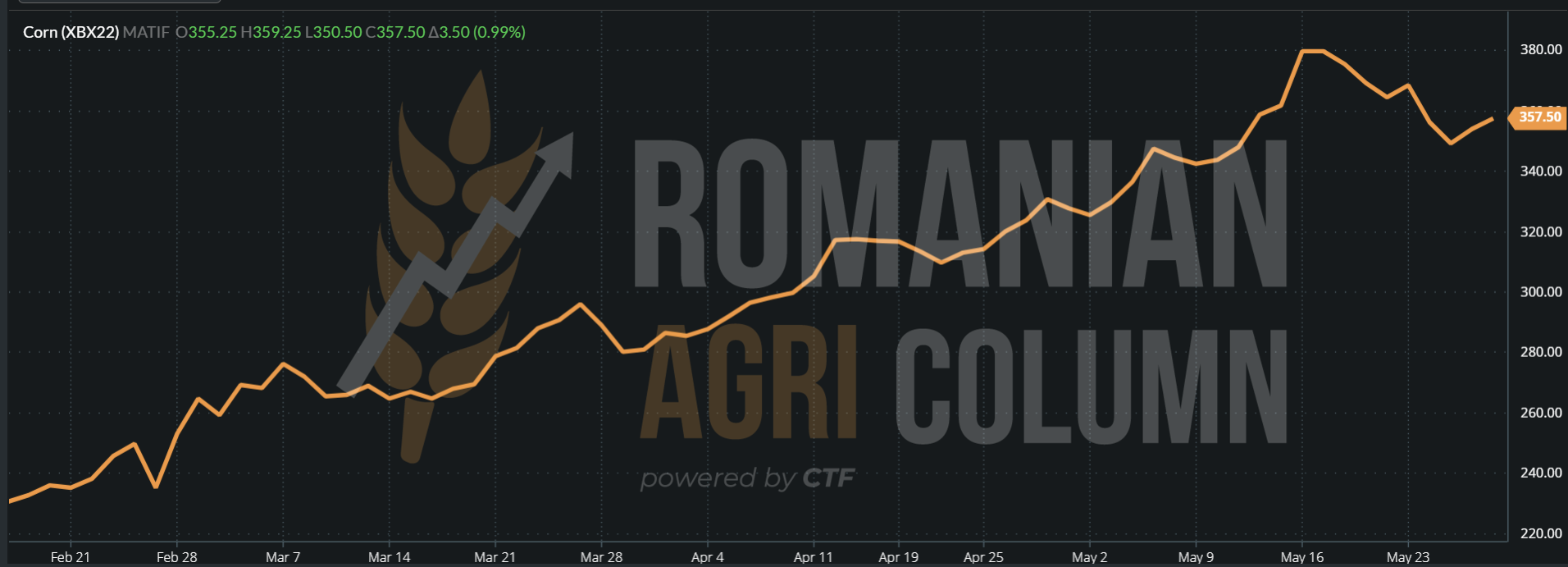

EURONEXT received the setback initiated by the news of the humanitarian corridor evoked by Russia and lowered the initial price level for NOV22, but identical as in the case of wheat, resumed the climb, after proving that it was nothing but a Russian staging to lift sanctions, which has not been discussed in any form by the US and the European Union.

EURONEXT XBX22 NOV22 – 357.5 EUR

CORN TREND GRAPHIC ON EURONEXT – XBX22 NOV22

GLOBAL STATUS

The US is still in the sowing season. Their rate reached an estimated level of 75-78% of the estimated area. Only North Dakota will not be able to sow the surface, but even so, things are not bad at all for American corn, given the rainfall that has fallen and will come to Corn Belt.

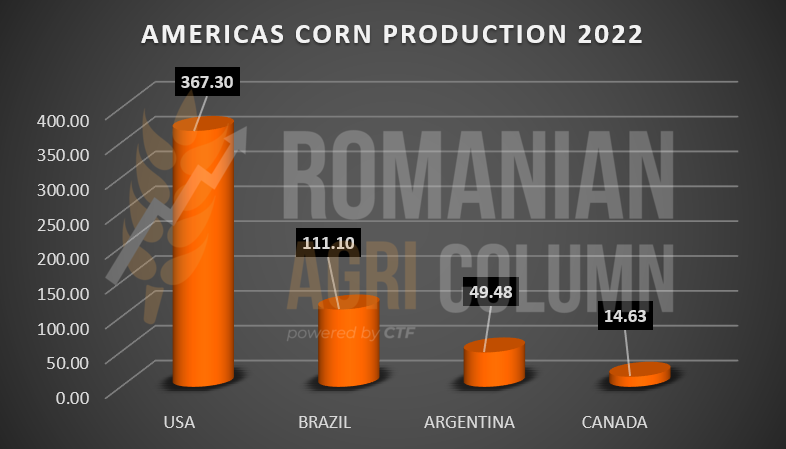

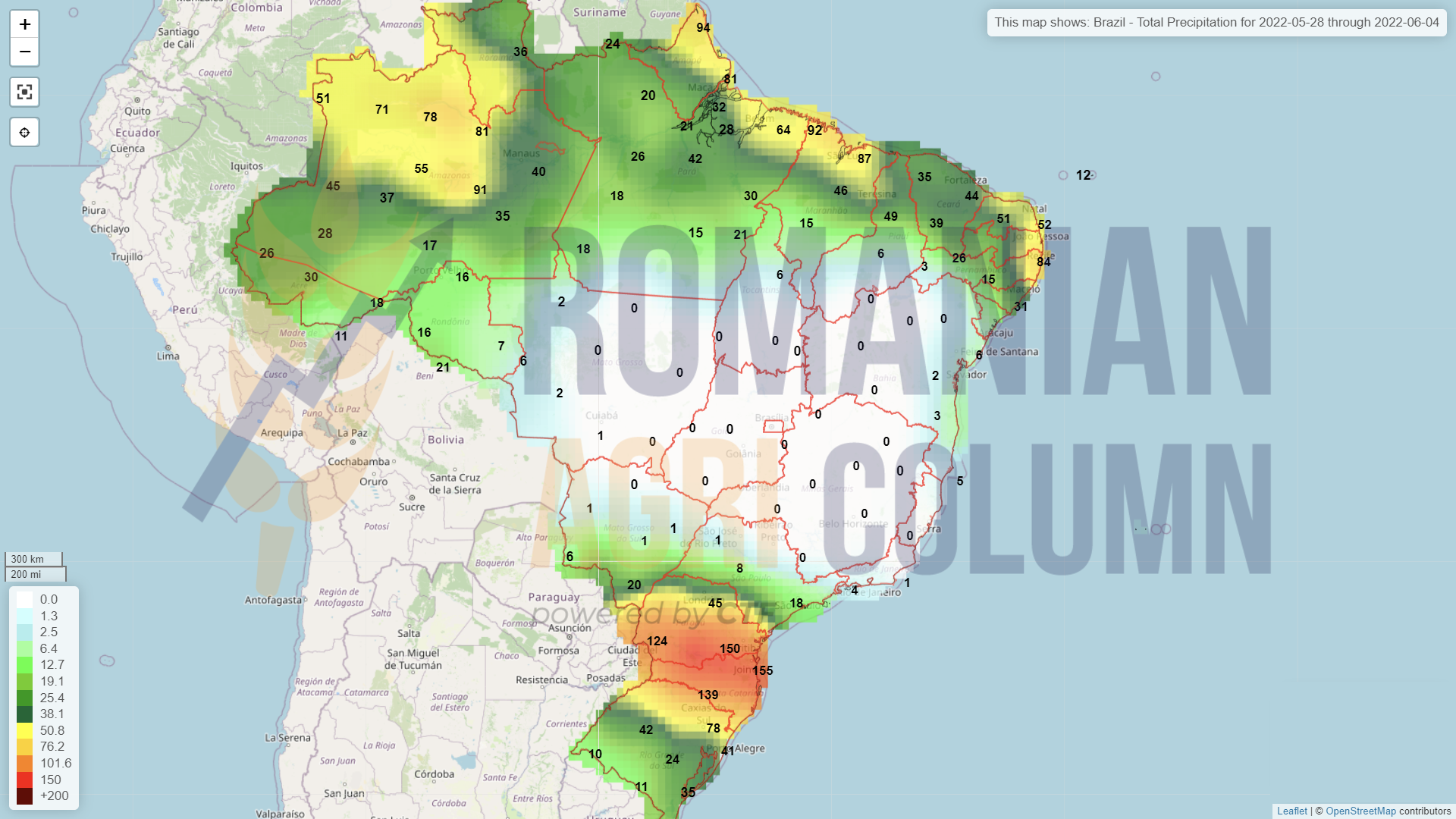

BRAZIL has the same problems caused by the lack of rainfall for Safrinha and the level of harvest volume is reduced by 5 million tons, from 116 million to 111 million tons, the two crops combined.

CBOT – the decline generated by the Russian statements was a beneficial one for the funds, which extracted the profit and then returned, due to the fundamentals of the physical market.

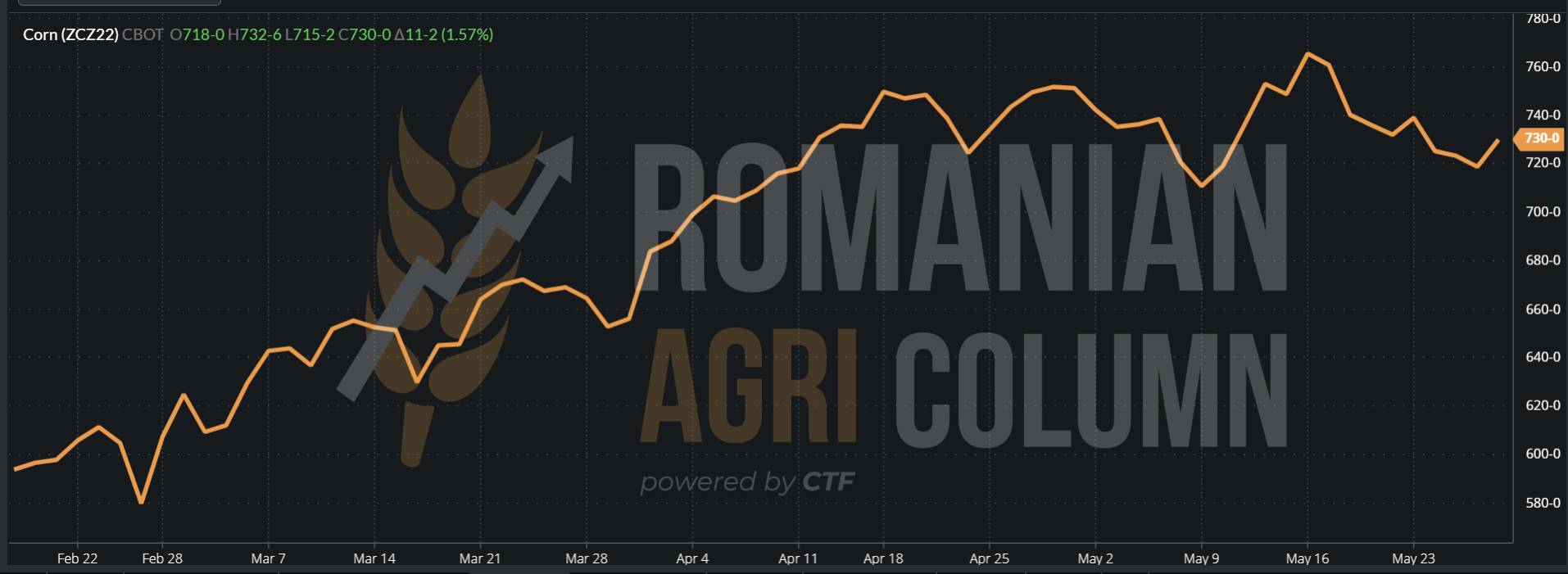

CORN – CBOT ZCS22 DEC22 – 730 c/bu (+11 c/bu)

CORN TREND GRAPHIC ON CBOT – ZCZ22 DEC22

CAUSES AND EFFECTS | ANALYSIS

FERTILIZERS. Many are noticing a drop in fertilizer prices in the US and are happy. But one thing is utterly forgotten – in the northern hemisphere, necessities have long since been bought, and the decline we are ingesting today is nothing more than de-stocking. When it comes time to buy, we will see the same complex increase in price. Does anyone think that American farmers have changed from corn to soy in vain?

BRAZIL, due to the lack of rainfall and the fact that it will generate a reduced by 5 million tons Safrinha crop, supports the price for the corn that will come to the market after mid-June.

EU is under the influence of the weather. Precipitation is the main cause that will determine the degree of fulfillment of the crop forecast. Uncertainty will soon be dispelled.

CHINA has shifted its focus from Ukraine to Brazil. This reconfigures a freight route and, implicitly, a price route in the Black Sea basin.

UKRAINE desperately trying to move corn to export. Blockages of barges and ships are recorded at Sulina, and prices have actually exploded. It also stays for 2 weeks at the entrance to the canal. In vain the shipowners have increased the tariffs, the wait is penalized and they will make only 2 flights per month, instead of 8-10, let’s say. The terminals in Constanța are crowded with Ukrainian goods and there are no longer any rules. There are accusations that Romania is slowing down the extraction of goods, which is totally unfounded. There is, if we talk about Sulina, a small number of pilots for the canal, and a pilot is not trained overnight.

We will have, if all the above are supported, a trend of stagnation in the price of old crop corn. Regardless of the USA and Brazil, the Ukrainian flow keeps the price stagnant, due to the discount it offers to export the goods.

CORN INDICATIONS IN MAIN ORIGINS

LOCAL STATUS

Rapeseed prices have depreciated. In addition to the problems they encountered in EURONEXT, buyers have traditionally increased the level of the negative premium, i.e., the discount compared to the indication XRQ22 AUG22, from minus 5 to minus 10 EUR/MT. The latest estimates put the Romanian rapeseed at 1.56 million tons crop level, increasing by 0.2 million tons.

CAUSES AND EFFECTS

Increasing the projected crop level causes buyers to relax. They know that rapeseed is a cash commodity and must be sold to cover cash needs on farms, as well as maturity coverage. We also know that rapeseed is very difficult to store, it is very technical to store it and not all farmers have adequate storage facilities.

Thus, against the background of the depreciation in Euronext, the premium increases, i.e., the value of the discount compared to AUG22. This is a primary effect of the increased crop pressure and harvested volume.

REGIONAL STATUS

The European rapeseed crop is declining in productivity and this is evident in France. European houses of analysis generate a decrease, but not significant, in rapeseed production at European level, but still do not position 17 million tons as a total harvest volume. The regional status is currently 17.67 million tons.

EURONEXT made the first positive corrections, fueled by the correlation with oil and palm oil, which still has trouble understanding the export restriction in Indonesia. We saw quotes of 832 EUR on Friday, May 27, 2022 and so things are starting to balance.

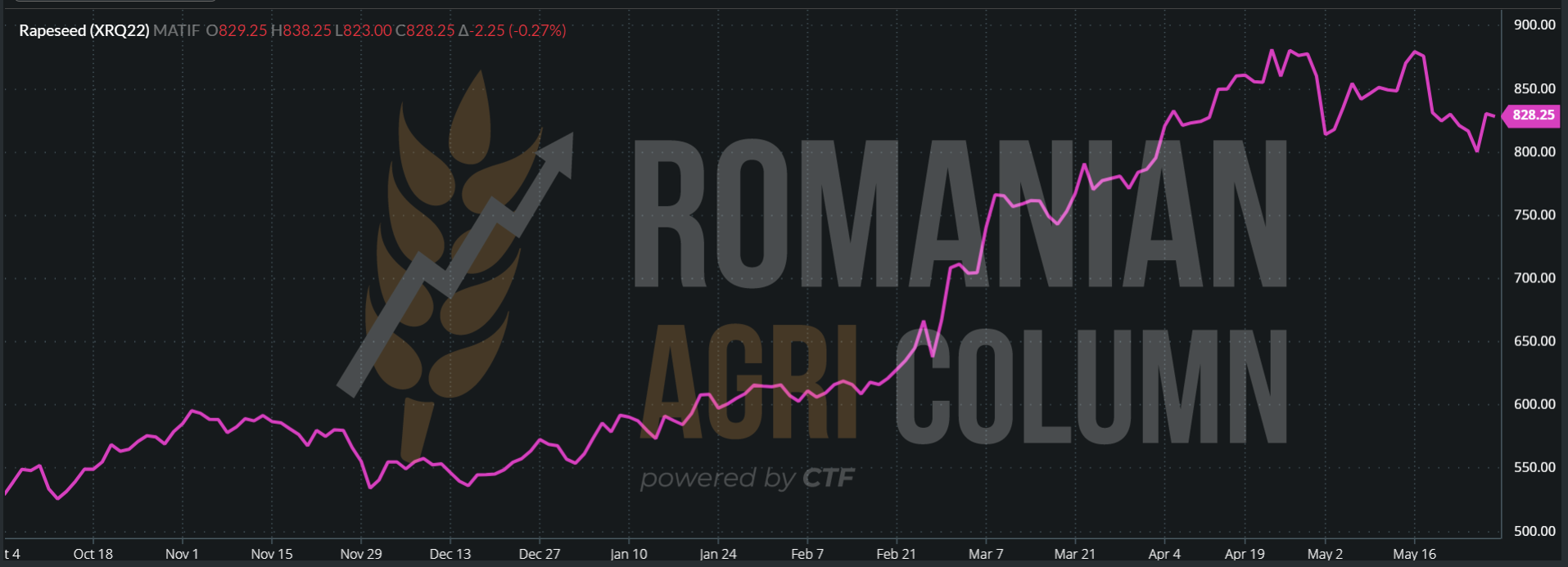

EURONEXT RAPESEED XRQ22 AUG22 – 828.25 EUR

RAPESEED TREND GRAPHIC ON EURONEXT – XRQ22 AUG22

GLOBAL STATUS

CANADA is the beneficiary of rainfall and the canola crop looks good for this period. The generation of volumes of 19.5 million tons is realistic at the moment.

ICE CANOLA also corrected in a positive way the decrease generated in the past days.

CAUSES AND EFFECTS | ANALYSIS

The sharp decline in European rapeseed has been triggered by the feeling that rapeseed oil will be replaced by biodiesel production. But, from word to deed, there are many stages and it takes time. Apart from political statements, many other things are needed.

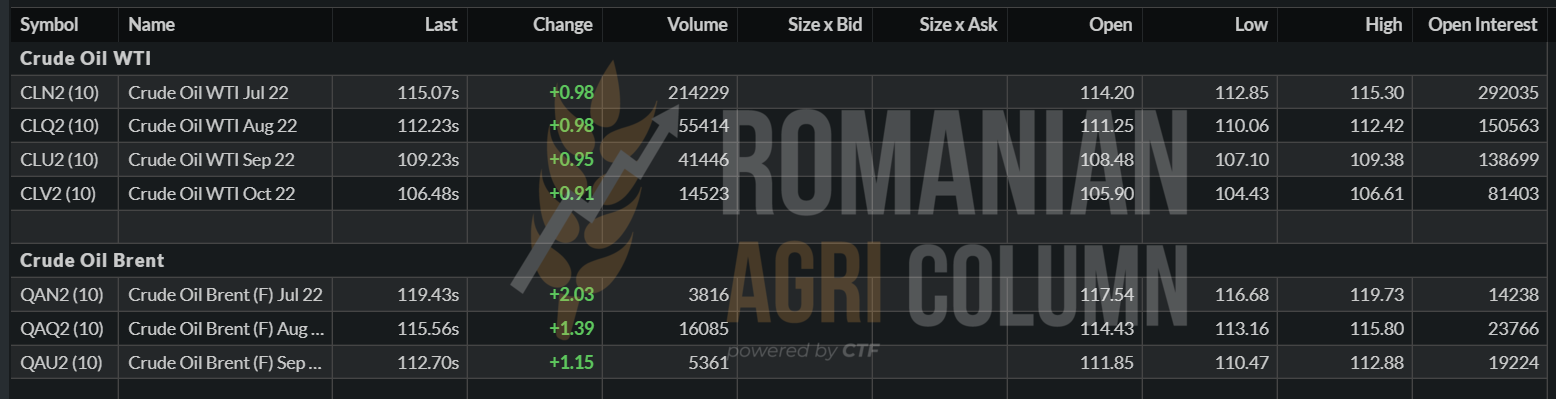

The correlation with oil added strength to rapeseed, the level of 119 USD/barrel in Brent being registered on Friday, May 27, 2022.

Rapeseed was also influenced by the lack of decision in Indonesia, which does not know how and in what way restricts the export of palm oil. Initially, they had declared that the export barriers would be lifted, and then they would return and claim that they would still retain the 10 million ton restriction option, which means a lot if we look at the total global production of palm oil, valued at 75 million tons. million tons.

The replacement of rapeseed in the manufacturing process of biodiesel, soybean oil, has also increased, being the beneficiary of the increase in the price level of soybeans on CBOT, so that a support for rapeseed came from this direction as well.

LOCAL STATUS

Indications of sunflower seeds naturally followed the broadly drawn trajectory of Russia’s attempts to lift sanctions. Naturally, the buyers decreased the market by 40 USD/MT, up to 710 USD/MT in the CPT Constanța parity. The mirage of an easy supply, of access to goods in Ukraine generated this state of comfort was predictable, by the way.

The Romanian sunflower crop is in full development and the sufficiency of some precipitations could offer an extremely high support to the forecasted volume of 3.65-3.7 million tons.

CAUSES AND EFFECTS

A first cause of diminishing effect of the crop could come in time. Although today we do not have forecasts of excessive heat waves for the months of June and July, such an event would cause a decrease in the volume of the harvest. That is why the recommendation to farmers is not to sell forward more than 1 ton per hectare. It is a mature exercise, because the market can be engaged differently in the months after the harvest and the benefits come smoothly and naturally.

REGIONAL STATUS

Ukraine reduces the price of raw materials by 5%. The reduction is due to the existing coverage in Turkey and Bulgaria and thus the Ukrainian goods do not have the same number of pre-existing buyers. In addition, there is already a record for the sale of raw materials against the market premises that we know, namely that Ukraine exports only crude oil.

Logistics is and remains tense in the area, with logistical costs exceeding any barrier to normalcy. For example, before the price reduction, the Ukrainian raw material (sunflower seeds) was quoted at the level of 880 USD/MT CIF Marmara, and the logistic cost is 150 USD/MT.

CAUSES AND EFFECTS

Sunflower seeds are making their way into Ukraine right now. In small batches, but in rhythm. The cause is obviously war. With a Russia that will not give in, only an optimist will still hope that Ukrainian ports will be unblocked. This is excluded.

Russia has played the card of suffocation and destruction and will do so at all costs. Thus, after consolidating its presence in the southeast, it will move further west. In this context, Ukrainian goods will not be able to leave the country, as everyone wants. We are simply talking about the laws of physics. The rest are good intentions and political statements.

Does anyone think the US has approved the $ 40 billion Land & Lease program in vain? There will be a long war, maybe years, until the most drought will give way and we hope to be Russia, in its capacity as aggressor and potential Master of Food at regional and Asian level.

As a direct consequence, this price decrease is only due to the fact that, at this moment, the processing units are covered and in a maximum of 2-3 weeks they will enter the annual revisions. After that, the chase for goods will follow again. Of course, there will be the traditional harvest pressure, but farmers are capitalized and have this element at hand.

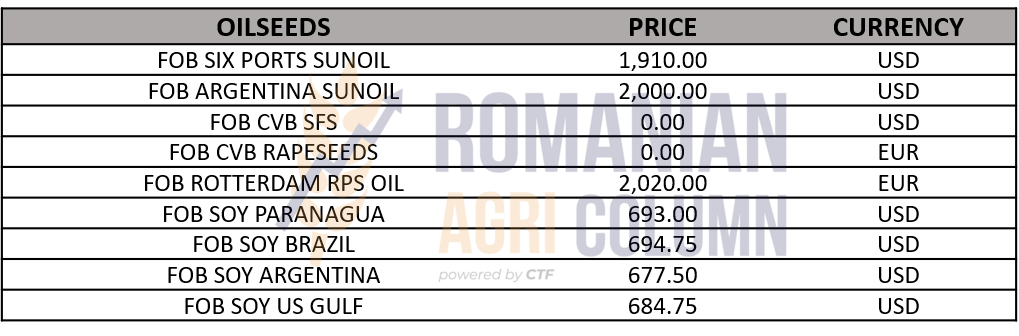

CSFO AND OILSEEDS INDICATIONS IN MAIN ORIGINS

LOCAL STATUS

At the local level, the demand does not exist anymore and the lack of interest of the buyers is manifested by the non-offer of certain lots offered for sale. The same is true at the level of the Danube region – processors do not show interest in soybean.

CAUSES AND EFFECTS

What was raised yesterday as a price, is not interesting anymore today. We see the cause on the horizon of the new crop, with a similar number of hectares and a gear in the global market, where the replacement level for the new crop is much more convenient than the potential price that could be offered today.

GLOBAL STATUS

The US is lagging behind in sowing soybeans and this is compounded by CBOT indications. The South American sisters are at the level of potential for next season, but there is still a long way to go.

CBOT is growing due to a lack of goods, demand from China and the pace of US sowing.

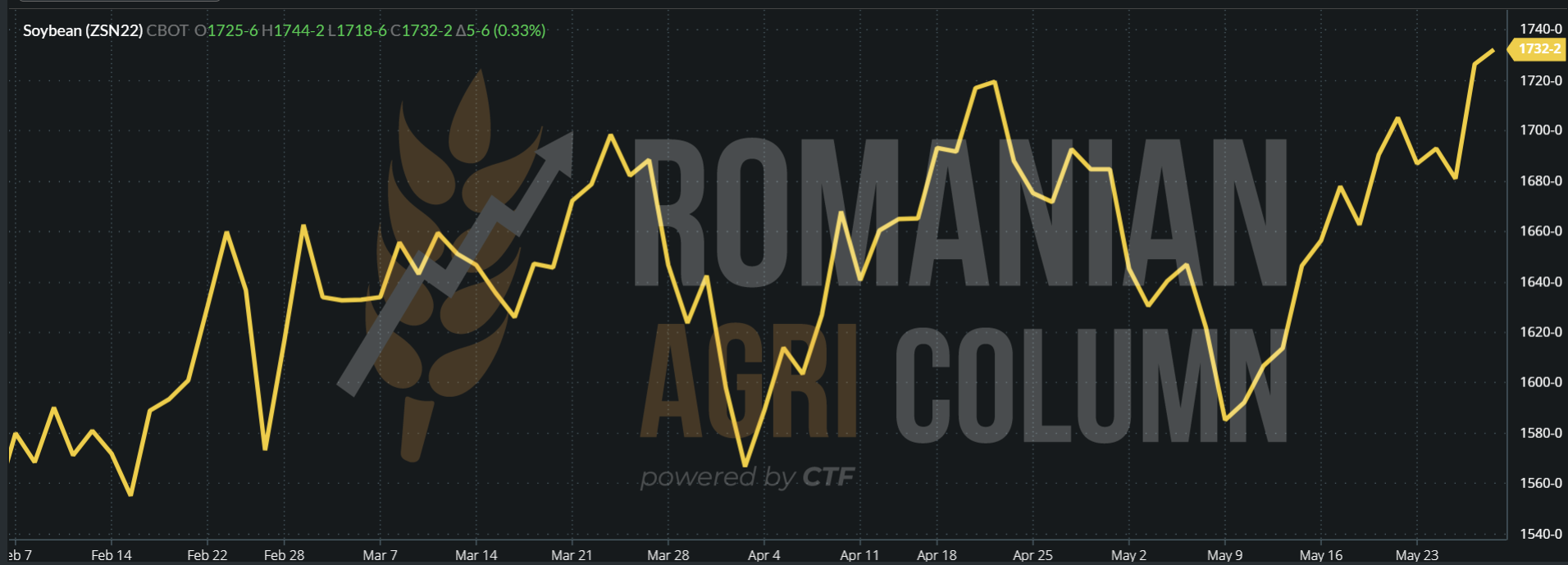

CBOT SOYBEANS – ZSN22 JUL22 – 1,732 c/bu = 636 USD

SOYBEAN TREND GRAPHIC – ZSN22 JUL22

CAUSES AND EFFECTS

The new crop looks great in terms of volume and forecast. This is the cause we need to focus on and analyze. And the first effect is found in the quotations of the new soybean crop, which decrease dramatically compared to those of July 2022. Specifically, the indication ZSX22 NOV22 shows a difference of 188 c/bu, which, translated into USD shows 69 USD/MT.

Specifically, the new crop is priced at USD 567/MT. This is an extremely strong signal for the future crop. We have a very high volume indication that only the weather can change. But La Nina is about to end at the end of autumn 2022, after a cycle of two consecutive years and ENSO is entering a state of stabilization.

EURO/USD 1: 1.07 | USD/RUB 1: 66.84

USD weakens against EUR.

BRENT 119.43 USD/barrel after falling to 104 USD/barrel

28 May – 4 June 2022

Romania

Europe

Ukraine

Russia

Canada

USA

Brazil

Argentina

China

Australia