This week’s market report provides information on:

LOCALLY

Starting with this issue, following the WASDE report, we are parting with the 2021-2022 season. It was a marvelous year for Romanian farmers, a year in which they took a well-deserved revenge against the disastrous year 2020. It was a year that we will not meet again soon, a superb year materialized by the fact that Romania has so far exported over 6 million tons and continues to lead sales to Egypt through the local GASC authority.

From now on, we will talk about the 2022-2023 crop, as it is, full of uncertainties and full of side effects caused by the weather and the political factor.

The local wheat price indications increased to 385 EUR/MT in the CPT Constanța parity. But the discount for feed quality is extremely high, reaching 20 EUR/MT. We find the old technique in the wheat sales complex. If the Test Weight (TW) falls below 75 kg/hl, the declassification is instantaneous. The same goes for the protein content – what is below 11.5% is downgraded instantly. And the measurements are always governed by the principle of 0.5% uncertainty.

The 20 EUR discount always favors the buyer because he carries out the mix of qualities, so that the average quality indicates the milling parameters. And so it is transferred to a mix of 50% -50% performed at a quantity of 65,000 tons, an amount of 650,000 EUR. This mix is possible in theory, because in practice, the heat, the temperature of the product and the calibration of the equipment are factors that influence the physical measurements. We must recall here the legal conditions. Modern laboratory equipment is not approved in Romania for determining TW. The only instrument permitted by law and approved remains the cylinder. And not infrequently were the cases when the differences between the measurement performed on Granomat, for example, and then with the approved cylinder revealed differences of at least 1% minus in Granomat. 1% can also mean a price discount of 1%, i.e., 3.85 EUR/MT or downgrading to feed quality, which means a minus of 20 EUR/MT on the farmers’ account.

REGIONALLY

FRANCE is facing major problems near the harvest. The indications that we have mentioned in the last two months are taking shape and the degradation of the harvest volume due to the lack of water is a certainty, unfortunately. The initial estimated level of 35 million tons of common wheat or soft wheat, as it is also called, we bring, according to our estimates, to 32 million tons. We will follow closely the evolution of the French wheat crop, but the quality is expected to be good. It is the opposite effect, the smaller the volume generates better quality due to the preservation of nutrients in fewer grains.

RUSSIA, according to the USDA, is indicated at the level of 82 million tons as production. But Russian analysts are claiming 87 million tons at the moment. It is at least a bold statement because we know all too well the Russian way to promote their interests through attempts to manipulate the market.

At the same time, they claim that they will export about 40 million tons, a very high level of exports, judging by the 33 million tons for the 2021-2022 season. Contrary to their claims, we generate questions, as is natural. How will they export, as long as no shipowner sends their large-capacity ships, Panamaxes, to the Sea of Azov, because of the extremely high war premiums, because of the reputation to be maintained (no one will do business with those shipowners sending ships to Azov)?

In the two months since they invaded Ukraine, Russia has been effectively trading in coastal vessels of 20,000-27,000 tons. And we can’t help but wonder – of the 87 million tons, how many are associated with Ukraine? I mean, how many are stolen from Ukraine? And in support of our claim, we are inserting what happened the other day. The satellite images show Matros Pozynich, under the Russian flag, at the dock in Latakia, Syria. After being refused in two ports, this ship with 27,000 tons of wheat landed, in the end, the stolen goods from Ukraine are trafficked through Syria.

We also see the whole planet declaring TV stations in Russia that they will take corn and wheat from Ukraine to sell in China and blackmail and put pressure on the free world to negotiate with them. To negotiate what? The attitude of the supreme predator?

This attitude and this mode of action actually takes us back to the Early Middle Ages.

Let’s recall the article published by the author of this report a long time ago, which clearly indicates that Russia, as the owner of the Black Sea basin, will decide who lives and who dies. The link (in Romanian) here: https://www.zf.ro/companii/retail-agrobusiness/opinie-cezar-gheorghe-analist-expert-si-consultant-pentru-comertul-20551854

UKRAINE estimates a crop of 19 million tons of wheat, down sharply from last year’s 32-33 million tons. This is naturally due to the invasion it is subjected to and the systematic robbery it suffers on a daily basis, starting with the theft of agricultural machinery and ending with the theft of large volumes of goods. However, Ukraine still has an unsold stock of wheat from the last crop, which we still estimate at 4.5-5 million tons.

It now depends, of course, on how much of this commodity has fallen into the hands of the Russians who carry out this systematic large-scale robbery. However, the Ukrainian export projection for the 2022-2023 season is quoted at a maximum of 10 million tons of wheat.

European Union, following consultations and discussions, has generated a plan to create a Green Corridor for Ukraine, in the sense that 20 million tons are to leave Ukraine in the next 3 months. It is, in our opinion, a utopian plan, which has no chance of realization. Expressing 20 million tons in 3 months has more of a political connotation of declaring intentions than a realistic basis for realization. And we will explain point by point the 3 chapters of the green corridor that will have to allow the crossing of 20 million tons through the borders of Romania and Poland.

1. ROLLING STOCK AND TRANSBOARD: to transport 20 million tons you need to load 400,000 wagons or 800,000 trucks. The European Union can replace the green corridor with, say, 10,000-20,000 wagons. You don’t need more, because you can’t actually load in a timely manner. The loading time of a 40-car train is 48 hours.

Suppose that the collective effort will generate a level of 24 hours on the loading of a complete train. We open the border points and assign each one a level of 4 loading lines. We note a maximum number of 8-10 border crossing points: Reni, Giurgiulesti, Halmeu, Dornești, Izov-Hrubeszew PL and the other Polish crossing points, as well as the one in Hungary.

Mathematics gives us the following results:

- 10 crossing points x 4 loading lines x 90 days = 3,600 trains, i.e., 144,000 wagons. In short, only 7.2 million tons in the three months. And this in the condition that everything must work with the precision of a Swiss watch.

Let’s not forget that trains have to be maneuvered, so locomotives are needed.

Let’s not forget that the goods must be brought by Ukraine to the border and this means volume of wagons and unloading. You can’t actually unload goods between rails or sideways.

Let’s not forget that we need transboarding and loading equipment. Where, how many, how are they positioned and how will they operate? They will have to be arranged either between trains or separately.

Let’s not forget that the goods must be checked qualitatively and weighed, so the 24-hour deadline for a complete train of 40 wagons is completely out of date and out of reality.

Let’s not forget that in Romania the harvesting of the new season starts from June 10-12. And barley, rapeseed will need logistics.

The railway infrastructure in Romania is extremely precarious and, after the wave of accidents last year, the feeling of lack of resistance is very acute.

Not to mention the car transport, the roads are still crowded. Will they endure an additional influx of 10,000-30,000 trucks, knowing that during hot days oversized transport is prohibited?

Identical to trains. During the summer season, passenger trains to Constanta have priority, and freight trains run with speed restrictions on hot summer days. In Romania, the average speed for rail freight is 20 km/h.

It is clearly an unattainable goal. 20 million in 3 months.

2. BORDER FORMALITIES: Staffing for flexible formalities and integration of goods into the Union without crossing the mandatory requirements as a Union border. Another very difficult thing to do, given that it is very easy to move from one state to another at Union level. Customs workers are almost non-existent and need training to retrain. That takes time, financial and human resources.

3. STORAGE OF GOODS IN THE EU: The accommodation for a period of time of the goods in the locations in Romania is somewhat difficult, given the fact that Romania starts harvesting in a maximum of 30 days. And we wonder what owner of a silo or storage base will occupy its storage space with goods from Ukraine when the harvest volumes arrive in waves in Romania, i.e., barley, rapeseed, wheat, sunflower and corn? Who will block the space while waiting for their own crop? It’s a two-way question. One is about the time of harvest, because everyone wants to preserve a potential future, in the conditions dictated by the weather globally. The second meaning is that costs, electricity and fossil fuels have reached very high levels and prices for services have reached a level of 70% compared to last year.

BUT

Something discussed and agreed is missing. An essential element with profound implications for Romanian farmers and for national food security. The protection that must be granted to Romanian farmers is missing, an element that has been discussed and agreed but is completely missing.

At the moment, the goods from Ukraine are offered with a discount of 30-35 EUR/MT compared to the Romanian goods. I explained this whole complex in the previous article in Ziarul Financiar. Ukrainian goods that will enter and transit will be practically in the absence of customs regulations. Thus, the Romanian goods will be pressed with a discount of 30-35 EUR/MT.

Regardless of the destination, export market, intra-community or domestic, Romanian goods must align, in terms of much higher production costs than in Ukraine and in terms of more expensive logistics. The cost of a barge from Galați to Constanța has already doubled.

The relationship is very simple, if we judge only the Romanian wheat and corn. 9.3 million tons of wheat and 14 million tons of maize, with a discount of EUR 30/MT means a gap in the pockets of farmers and, implicitly, of the state, due to the lack of 700,000,000 EUR in the tax base. Instead of returning to the commercial circuit, this amount is lost. Or, at an average production of 5 tons per hectare, multiplied by 30 EUR discount, the Romanian farmer and Romania implicitly lose the value of the subsidy.

Farmers need to be protected. They have other costs of producing goods within the EU. In addition, they must be compensated for the side effects that exist, despite the good intentions of the Union to help Ukraine. Farmers already support the logistical factor generated by this wave. The costs of barges in Galați/Brăila have doubled and we will see road transport biting deeply from the price of goods in the FCA parity, not to mention their availability.

The protection of Romanian farmers, discussed and agreed, is missing from the list of measures. And in the short and medium term, this aspect will create irrecoverable damage to the Romanian food chain. There will be objections to my analysis, however:

“What if I’m right and you’re wrong?”

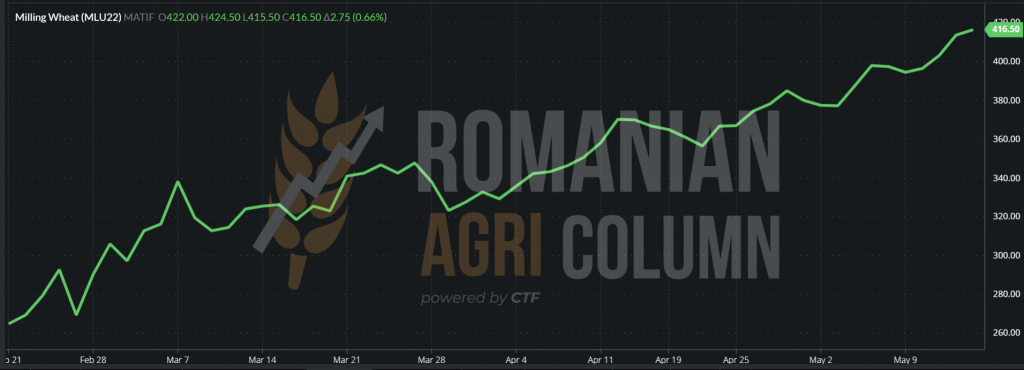

EURONEXT closes post-WASDE report

WHEAT MLU22 SEP22 – 416.5 EUR (+2.75 EUR)

WHEAT TREND GRAPHIC – MLU22 SEP22

GLOBALLY

In the US, the signal I generated many months ago is finally coming true through WASDE in May 2022. “Houston, we have a problem” is acknowledged. The American winter wheat crop is severely penalized, up to the level of 47 million tons. But it is only the beginning. We see it at a maximum of 44-45 million tons. Time is running out and the problems are getting worse in the South Central Plains, Texas is effectively devastated, Kansas is in trouble, and American winter wheat is not improving.

ARGENTINA will generate a production of only 19 million tons, compared to 21.5 million tons this season. The reduction of the surface is the main factor of the decrease of the production volume.

MOROCCO is suffering from a terrible drought and can no longer keep up. The estimated wheat crop is down 5.3 million tons, which is huge. Normally, Morocco generates about 7.5 million tons of wheat on an area of 2.85 million ha. We expect a major impact on the market in terms of demand, which will come from North Africa. Algeria and Tunisia are neighbors of Morocco.

INDIA is restricting wheat exports, a sign that the decline is not just 6 million tons in the 111 million ton forecast. We may be surprised that India imports wheat. Where from? From Russia, of course. Where? We know, but we’d rather keep quiet for now.

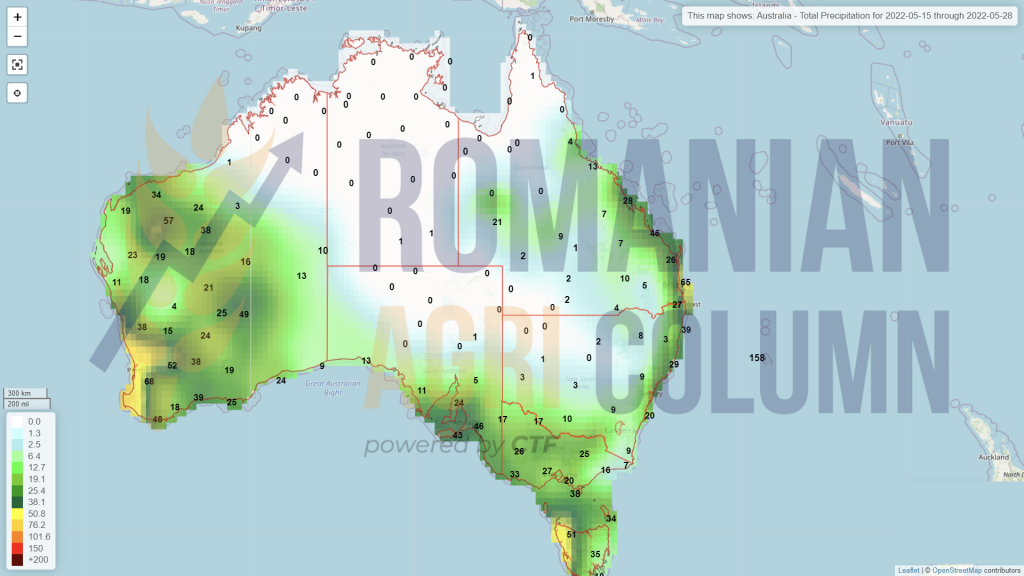

AUSTRALIA reduces the 2022-2023 crop forecast by 6 million tons from 36 million tons to 30 million tons. There is another lack of volume that needs to be addressed in the global context of supply and demand.

With all the calculations performed, we note an estimate of 774.85 million tons globally, decreasing by about 4.45 million tons compared to last year in the same period in production. If we look at it from the perspective of PRODUCTION vs CONSUMPTION, we have a clear imbalance. In figures, we have an overall production of 774.85 million tons vs. consumption of 787.85 million tons = minus 13 million tons.

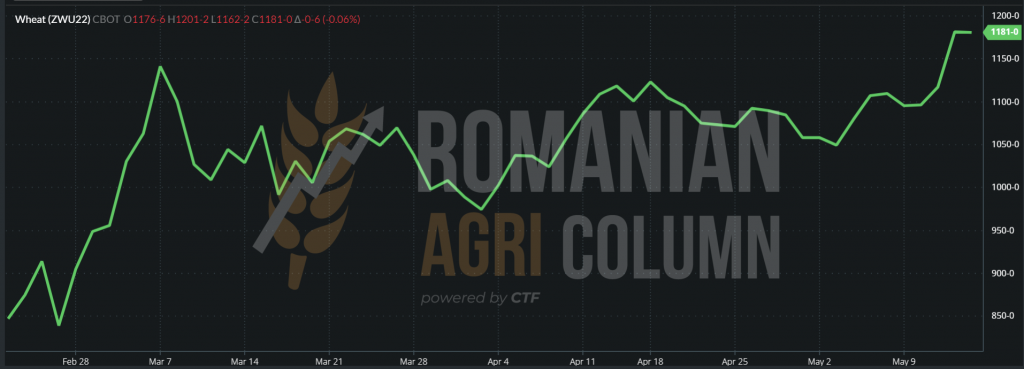

CBOT at May 13-14, 2022. ZWU22 Remains Stable – 1,181 c/bu (434 USD)

WHEAT TREND GRAPHIC – ZWU22 SEP22

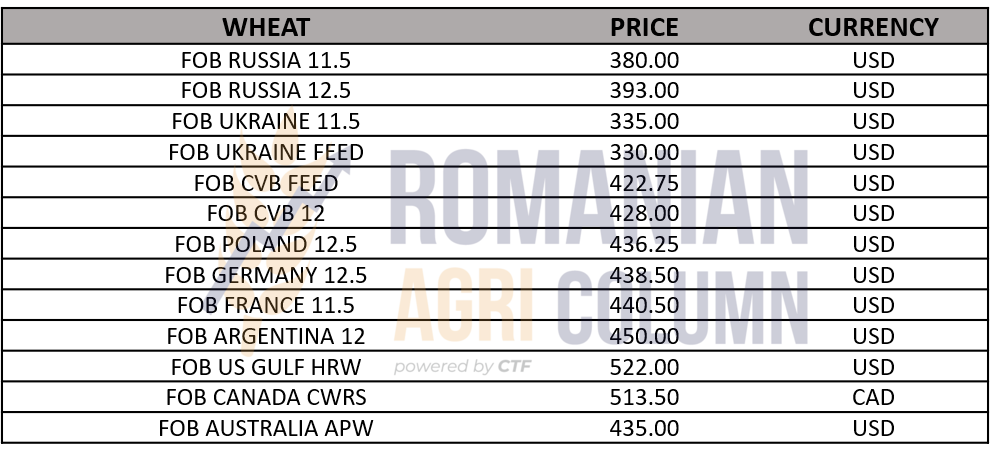

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

ANALYSIS

- We are going through a very delicate year. In terms of supply and demand, things are unbalanced before they start.

- The original offer loses ground due to the weather factor.

- The demand in destinations is becoming more consistent, also due to the weather factor.

- Freight flows from Ukraine are routed through Europe, with Constanta being the main module of all new routes.

- Constanța receives practically the place of the most important geo-strategic point in the Black Sea basin, in all this context.

- But farmers along the entire trajectory of transfer routes need to be protected.

LOCALLY

Barley indications have intensified as June approaches, which is the shipping month for many short exporters. Thus, we note a range of 330-340 EUR/MT and we estimate that the level will increase further. Delivery in the second half of June 2022 will be possible only if the weather does not cool down and will become very hot. However, if the thermal regime returns to lower levels, the harvest will certainly be delayed.

REGIONALLY

The problems are obvious in the European Union and we see the effect of the lack of water that has accompanied us throughout the winter in France and Spain, as well as in some areas of Germany. The forecasted volumes will be reduced and we note the Rouen feed barley with delivery July 2022 at the level of 370 EUR/MT. There is still time until the continental harvest, but things will not change for the better, they will even degrade in terms of volumes.

LOCALLY

The indications of the port of Constanța vary between values of 325-335 EUR/MT. It all depends on the need of the exporter to ship. Lots with prices of 338 EUR/MT are also slipped into this ensemble. The season is in full swing and the shipment is taking place at a brisk pace. Last week, we noticed a volume of 325,000 tons of corn that had left or was in operation, waiting to be shipped from Constanța.

The new crop is moving very slowly in terms of prices. Indications vary between buyers on a range between 300 and 315 EUR/MT. The certainty in displaying this low price level is the fact that the sowing is nearing the end in Romania and the calculation basis remains the estimate of 15 million tons. But without rain, things may change.

REGIONALLY

THE EUROPEAN UNION remains at an estimated 72 million tons of maize production and reduces its import level to 15 million tons for the 2021-2022 season.

UKRAINE will generate only 20-22 million tons of corn, a minus of 18-20 million tons compared to last season, when they had a record production of 40 million tons. But their bumper crop is at least 10 million tons, that is, the surplus that remained unexported and for which the green corridor is created, that corridor designated for the extraction of Ukrainian goods, which we talked about in the wheat chapter.

RUSSIA will generate 14.5 million tons of wheat, but their corn export level is set at a maximum of 5 million tons, although aberrant statements indicate that they will take Ukrainian corn and sell it in China. Let’s hope that won’t happen. You can’t steal someone’s work under any circumstances.

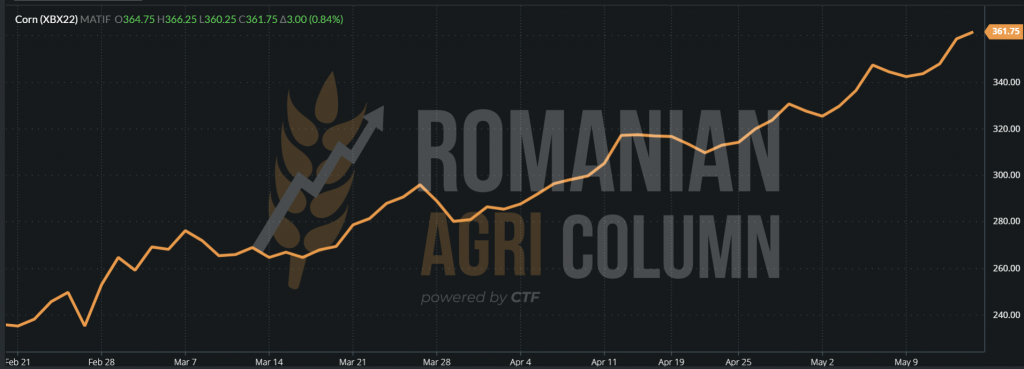

EURONEXT rises following WASDE report MAY 2022. The new crop is close to the old crop: XBM22 JUN22 – 360.25 EUR vs XBX22 NOV22 – 361.75 EUR

XBX22 CORN NOV22 – 361.75 EUR (+3 EUR). And we were wondering why the discount charged by Romanian buyers in the port of Constanta is 60 EUR? Is it based on the discount of Ukrainian goods?

CORN TREND GRAPHIC – XBX22 NOV22

GLOBALLY

In the US, the WASDE report confirms and supports the estimate we made 30-35 days ago for American corn. The American corn crop will be 364-366 million tons, compared to 382 million tons last season. Why this? In short, we have an aggregation of two factors. The first is the reduction in the area of maize due to the costs of fertilizers (the difference in area has migrated to soybeans). The second factor is the decrease of the production index per hectare to the level of 177 bu/acre, i.e., to 11.1 tons/hectare. So a production deficit of 17-18 million tons, according to our estimate.

BRAZIL remains at 116 million tons, according to the WASDE report. But CONAB indicates it at 114 million tons. The drought in Brazil persists and we will see a decrease in the forecast for Safrinha. For the next season, the indication is 126 million tons, but there is still a long way to go. For now, we note the forecast.

ARGENTINA is still maintained at 53 million tons for this season, but the forecast for next season raises it to a level of 55 million tons.

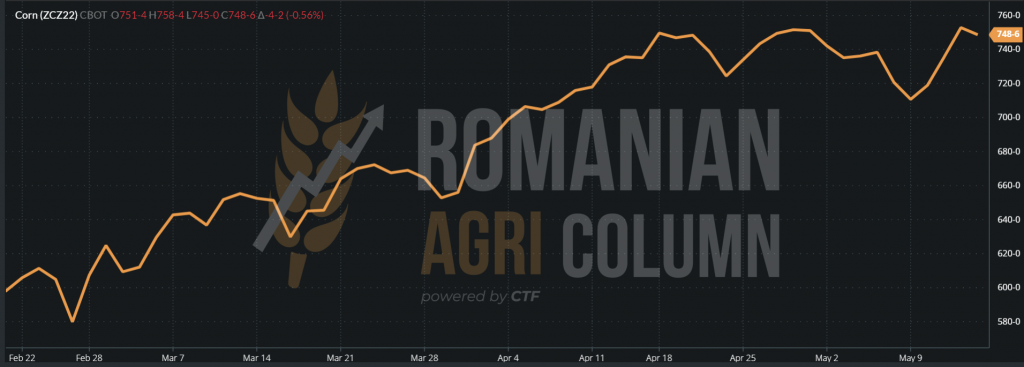

CBOT ZCZ22 DEC22 – 748 c/bu (294.5 USD)

GRAPHIC TREND CORN – ZCZ22 DEC22

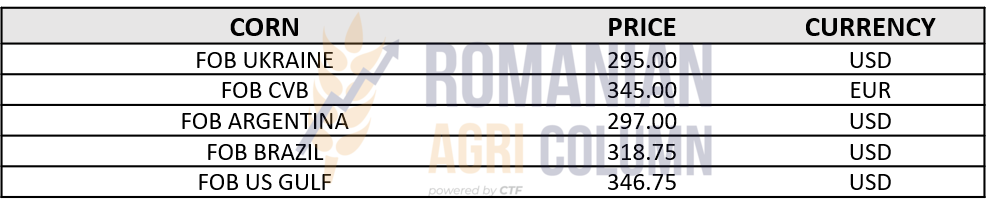

CORN INDICATIONS IN MAIN ORIGINS

ANALYSIS

- The Ukrainian crisis and the creation of the green corridor bring corn to the fore. The gap left by Ukraine is trying to be filled. The euphoria was generated by the publication of the plan, but will be followed by deep disappointments. These are just political statements, with no applicability in practice.

- WASDE indicates a decrease of 17 million tons in the future American crop. Smaller area and lower productivity are the causes of this minus.

- Brazil and Argentina promise to harvest 12 million tons more next season to make up for the US deficit. We’ll see what La Nina says. If it converts to El Nino.

LOCALLY

There’s only a month and a few days left until the rapeseed harvest. According to our forecast, Romania will generate 1.3 million tons. The USDA is estimating even more, about 1.4 million tons. We remain true to our forecast, given the lack of rainfall and the fact that part of the surface has been turned upside down and sown with sunflower seeds.

These days, we see the same level of AUG22 minus 4 EUR offered to farmers. Of course, processors can reach the equivalent of AUG22, but it’s all about the direct negotiation of each. As we notified and nuanced many numbers ago, whoever signed the AUG22 minus X mechanism only had to win over the one who fixed it directly. Those who followed our instructions and did not sign at the level of AUG22 minus 15 or AUG22 minus 20 EUR won.

Rapeseed remains a vital element in a farm’s profit and loss account. The model indicates a maximum cost of 1,200 EUR/hectare, and the revenues are translated into 3 tons of rapeseed, plus the area subsidy.

REGIONALLY

The European Union’s rapeseed crop is showing signs of weakness. We have given this subject a fairly wide scope in previous reports, and it is now being confirmed. European production is reduced to 17 million tons, compared to the forecasted 18.5 million tons. The drought in the western part of the continent, combined with the freezing rain at the end of March, the accumulation of winter frost problems in the northern areas, including Poland, add up to the first reduction.

Ukraine will generate a volume of 2.85 million tons, but its export will be a problem. You will certainly be given priority over corn and wheat, as biodiesel refineries in Europe need raw materials after coming out of annual reviews. But our estimates give a volume of 2 million tons that can be harvested and delivered.

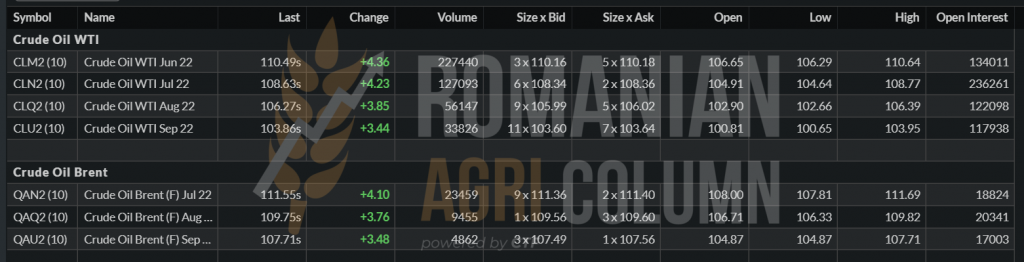

EURONEXT responds to the complex of information consisting of: the decrease in volume in the European Union, Ukraine’s export estimate, the increase in oil by 4 USD/barrel and the Canadian canola which is indicated by the USDA at 19 million tons. Let’s remember the past issues when we wrote: canola reduces its surface area in Canada by 7%. In addition, Germany’s statements about changing the destination of rapeseed for food use were, as usual, just statements and that’s it. We got used to politics.

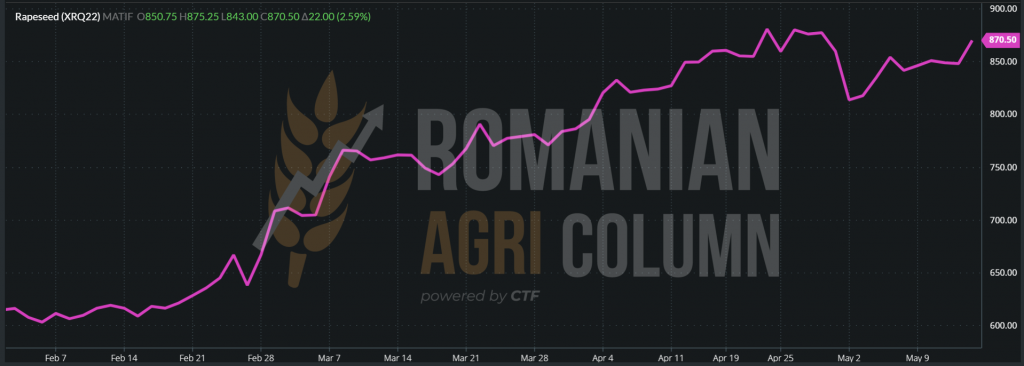

XRQ22 AUG22 – 870.5 EUR (+22 EUR)

RAPESEED TREND GRAPHIC – XRQ22 AUG22

And in the future, the rapeseed will be extremely stable and we expect support for the next period, a slight stabilization during the harvest, if all the conditions are calm (weather, oil and political factor), and from the beginning of November, a new rally growth. The factories will make the change from processing the sunflower seeds to rapeseed and the demand for coverage will be at another level.

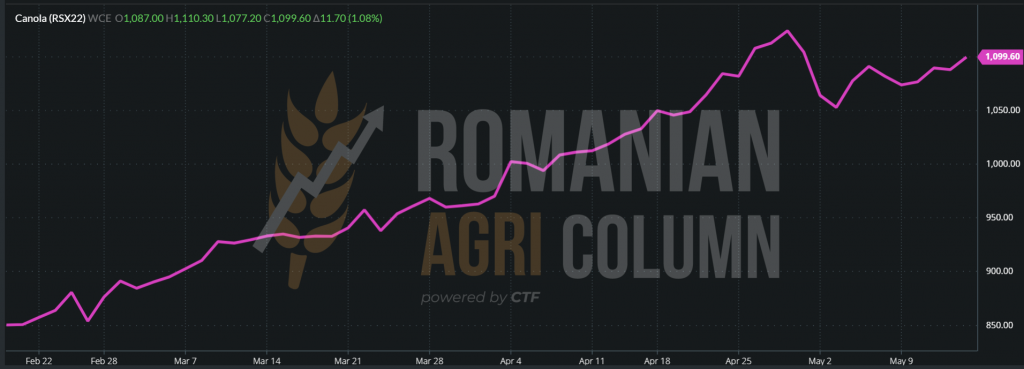

CANOLA RSX22 NOV22 – 1,099.6 CAD (+11.7 CAD)

CANOLA TREND GRAPHIC. The same route as the European rapeseed.

ANALYSIS

- Rapeseed continues to be supported due to the combined factors: EU, Canada, Oil.

- The stagnation was a moment of waiting generated by the evaluation in the EU.

- There are no strong enough reasons why rapeseed is not consolidating much better after October 2022.

LOCALLY

Indications of the old sunflower crop are declining due to the time window and the level of supply required. The time allotted for processing is melting every day and the June revision is approaching. Thus, the AMJ strip (April-May-June) is almost complete. The levels indicated by the buyers these days are 760 USD/MT CPT Constanța.

The indications of the new crop are maintained at the level of 730-740 USD/MT and we will see in maximum 15 days how only the new crop will be quoted, which will be under the pressure of the processing factor. Traditionally, processors will try, but that doesn’t mean they will be able to keep the market as low as possible. This happens repeatedly every year. There is even an unwritten rule that says, “I don’t want to buy the first 20,000 expensive tons, I want the next 20,000 cheaper.”

But we have the weather factor, which can ruin all the buyers’ accounts. If the evolution is not good in terms of rainfall, we can see the rally starting before harvest. If the heat dominates the second half of July, we will also have a rally. The calatidium will shrink and look like a daisy. This means a decrease in the potential of the Romanian crop.

REGIONALLY

UKRAINE will generate a maximum crop level of 9.7-9.8 million tons of sunflower seeds and with last year’s difference of about 4 million unprocessed tons, will have a level of 13.7 million tons.

The information we have says that processing has resumed in non-conflict areas, with raw material prices of 16,000 UAH, i.e., the equivalent of 530 USD/MT. Crude oil is offered at a price of 1,600-1,800 USD/MT EX-PLANT.

But logistically, it’s very difficult. About 110,000 tons of raw material crossed Romania in April. And the unsigned testimonies of a seller say of amounts of over 120 USD/MT logistic cost to the border with Romania. Barges are double the price of transport. The transboarding in Reni/Giurgiulesti reached the aberrant amounts of 30 EUR/MT.

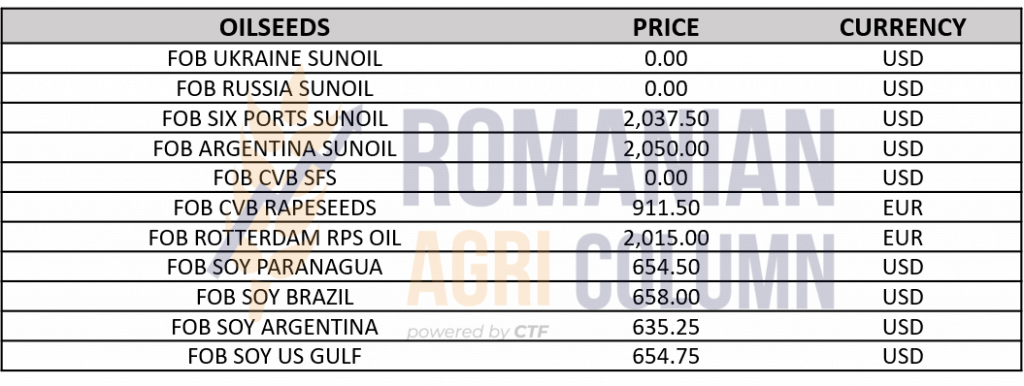

CSFO AND OILSEEDS INDICATIONS IN MAIN ORIGINS

ANALYSIS

- It is too early to talk about crop development in Romania.

- It is also early to talk about the EU crop, but let’s not forget that it is not raining in France or in Spain.

- Ukraine is the hot spot for European supply of sunflower oil.

- Price evolution will exist. Our vision leads it to a minimum level of 800-820 USD/MT.

LOCALLY + REGIONALLY + GLOBALLY

WASDE has shown us a growing global production compared to the 2021-2023 season. We are talking about a difference of about 45 million tons, starting from an estimate of May 2021 of 350 million tons and comparing with the estimate of May 2022 of 395 million tons.

The increases will be generated by the countries that have faced drought, namely Brazil, Argentina and Paraguay. They will generate, in the order indicated, a forecast level of crop of 149 million tons (+24 million), 51 million tons (+9 million), respectively 10 million tons (+5.8 million).

The United States will generate an additional 5.6 million tons, totaling 126.3 million tons of soybeans. The increase will come from the larger area resulting from the abandonment of the maize crop, due to the high costs of fertilizers.

The 2022-2023 crop vision is very good at the moment and you will find details about global consumption levels and stocks in the WASDE report released before this market report.

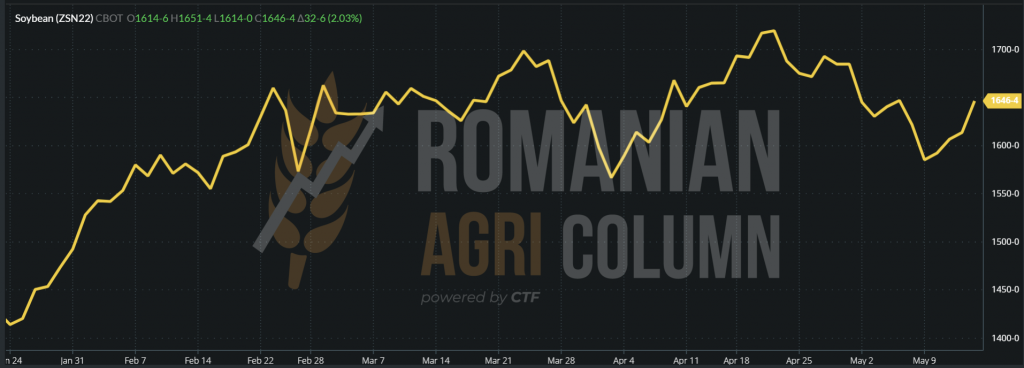

For now, let’s look at the post-report CBOT reactions and note the rally for the old crop, as well as the quotations for the new crop:

JUL22 1,646 c/bu = 604.8 USD (+32 c/bu ) vs. NOV22 1,498 c/bu = 550,4 USD (+17 c/bu = 55 USD)

SOYBEAN TREND GRAPHIC – ZSN22 JUL22

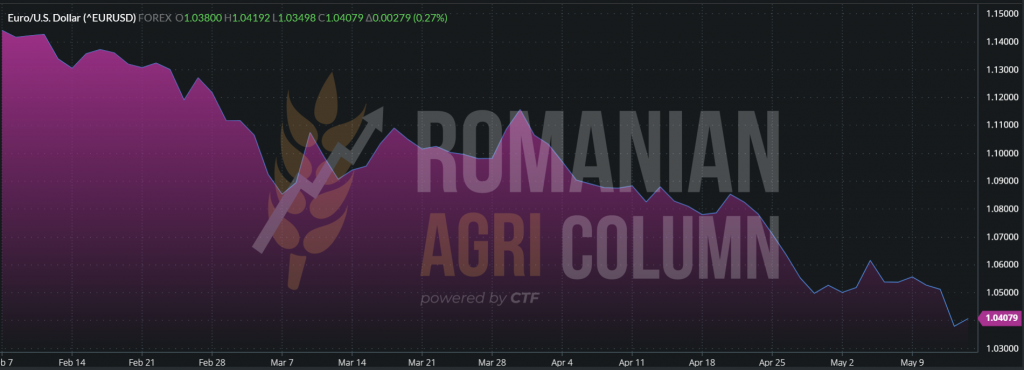

EUR: USD 1: 104 | USD: RUB 1:65

EUR-USD TREND GRAPHIC

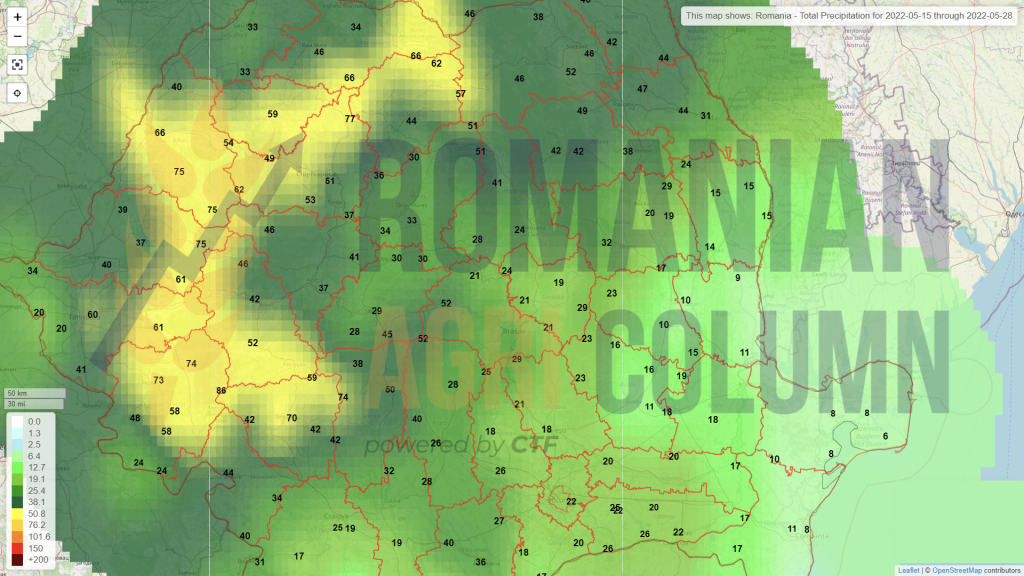

15-28 May 2022

Romania

Europe

Ukraine

Russia

Canada

USA

Brazil

Argentina

Southern Black Sea

North Africa

China

Australia