This week’s market report provides information on:

LOCAL STATUS

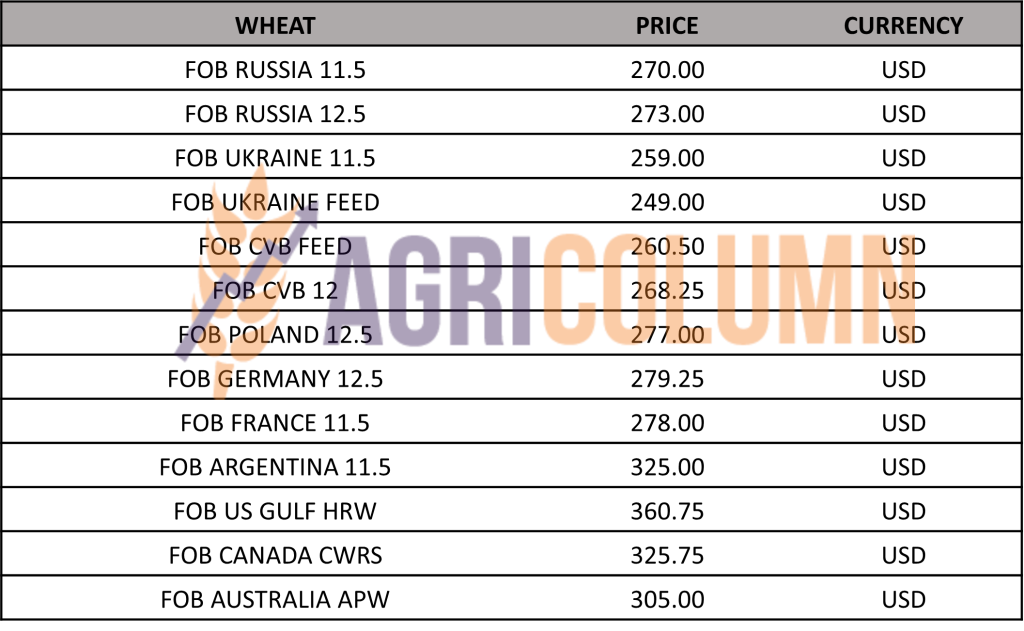

The indications of the Port of Constanța are, depending on the buyer, in a margin of 230-232 EUR/MT in CPT parity. The discount for feed quality is 7-8 EUR/MT.

The new wheat crop is valued around the same price level, with an upper limit set at 227-228 EUR/MT and with a discount of 6-7 EUR/MT for feed wheat, both indications having the CPT Constanța parity as a reference.

CAUSES AND EFFECTS

Romanian wheat started to accelerate in sales. We note that Romania exceeded the threshold of 3.2 million tons of export wheat. But not much time separates us from the new crop and we find ourselves in the same scenario. 4 million tons is perfectly feasible to be shipped, but the delay is so great that the gap will not be recovered. And the crop premises lead us to figures close to 10 million tons, to which we add a volume of at least 1.2-1.5 million tons that will remain unsold from the 2022 harvest, a year full of perhaps improbable situations for some, but perfectly predictable for others. In May, traditionally, there are not too many sales. The situation is a recurring one every year, turning into a settled custom where what was not sold forward until May is not sold until harvest.

REGIONAL STATUS

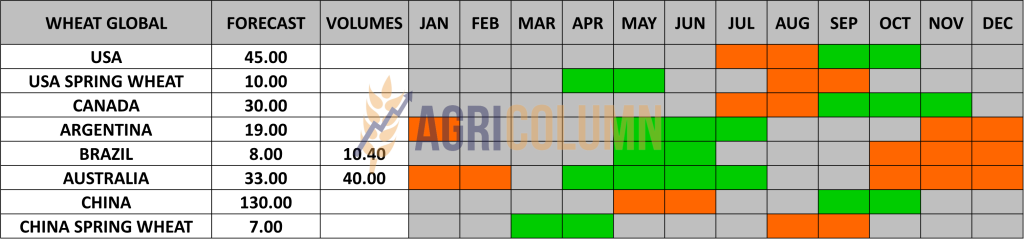

RUSSIA remains in the same pre-Easter parameters, namely with that cap set at a minimum FOB sale of 275 USD/MT and an unchanged forecast of 86.8 million tons, which will be upgraded from controlled territories in Ukraine, i.e., a minimum of 6 million tons.

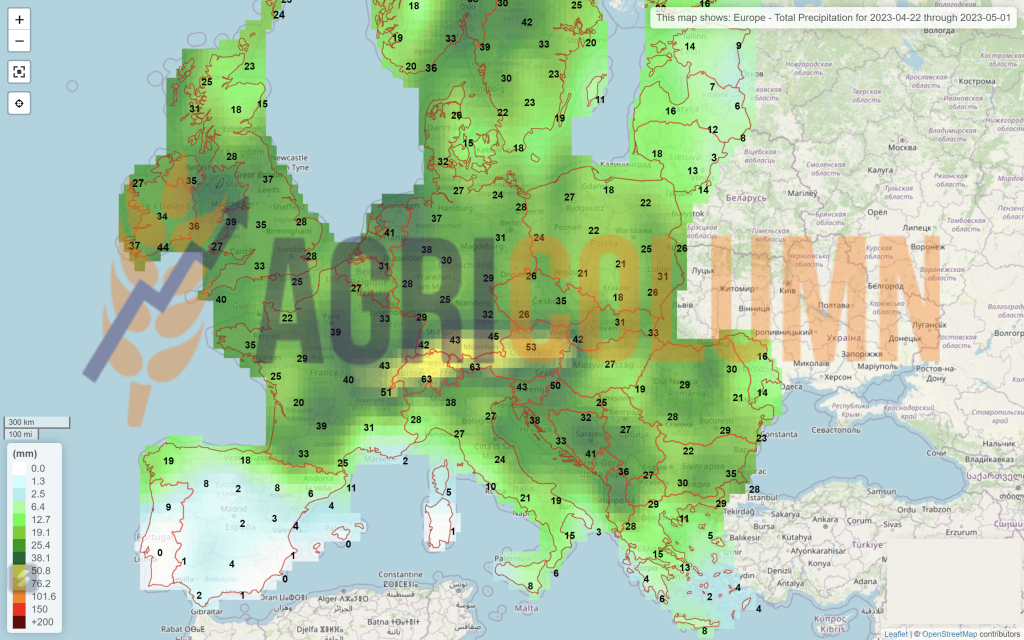

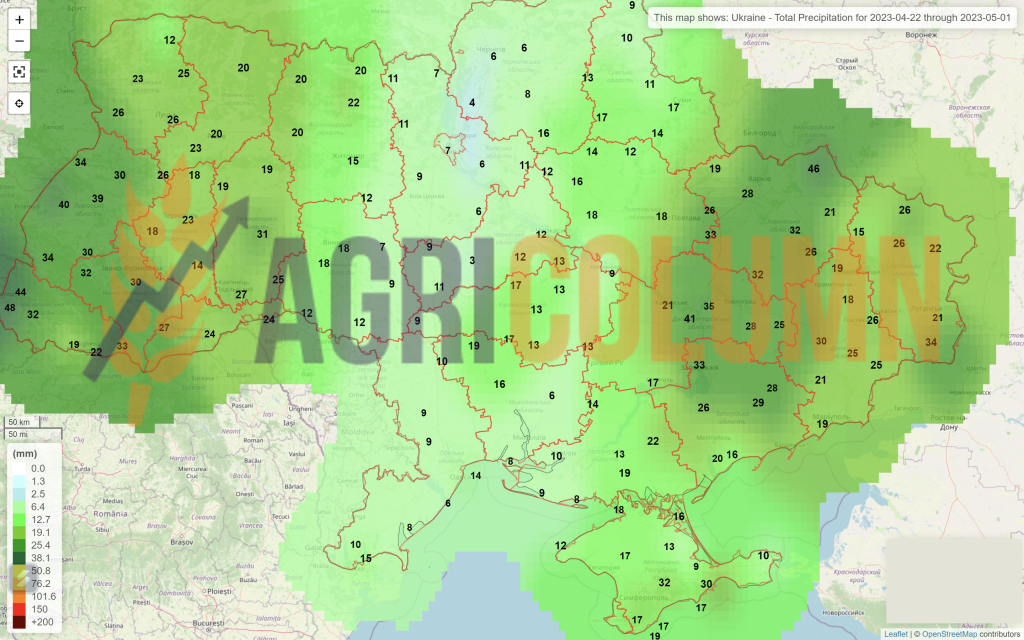

UKRAINE has received sufficient rainfall and the vegetation remains in good condition at this time. Due to the increase in productivity per hectare, we remain at the level of 20.5-20.7 million tons of production in the controlled territories.

THE EUROPEAN UNION does not see negative changes at the vegetative level, except for Spain, which is responsible for 4% of the total volume of the Union, which, translated into figures, means 5-5.2 million tons. Certainly, however, they will not have a total wheat loss, and other areas of the Union will have better yields than what is estimated today. We also include here the volumes not sold by Romania and Bulgaria.

As for EU export, it reached the total level of 25 million tons, with an imported volume of 8.7 million tons. The variation of exports compared to the previous year in the same period (YOY) is positive, of 6%. But import also has an extremely high share at Union level, 156% higher than last year in the same period (YOY). Of the import origins, naturally, Ukraine has the largest share, with 4.48 million tons of the total EU import. Looking at the numbers, we can see that the level of wheat imports from Ukraine has dropped considerably. Naturally, we are approaching the end of the cycle period and all eyes are on the new crop.

EURONEXT – MLK2323 MAY23 – 242.50 EUR

EURONEXT WHEAT TREND CHART – MLK2323 MAY23

GLOBAL STATUS

The USA currently has a good to excellent rating of 27%, down from 2 weeks ago. The current problems are related to the weather. Winter still doesn’t want to leave the US and the snow continues to be present, along with the cold, in the North and Northwest areas of the US.

BRAZIL. Brazilian farmers will harvest a record 11.3 million tons of wheat in the 2023/2024 season, compared to 11 million tons the previous year. Farmers will expand seeded area by 6.1% to 3.48 million hectares, citing “optimism” among wheat producers this year on expectations that costs will remain stable and demand strong, although wheat prices have lowered.

To understand the differences, in 2020-2021 they had a crop of 6.25 million tons, and in 2021-2022 a crop of 7.5 million tons, both with a yield of 2.7 tons per hectare. This season, a yield of 3.5 tons/ha is predicted, similar to that of the 2022-2023 crop.

CBOT WHEAT – ZWK23 MAY23 – 661 c/bu

CBOT WHEAT TREND CHART – ZWK23 MAY23

TENDERS AND TRANSACTIONS

MIT JORDAN purchased 60,000 tons of wheat from CHS, delivery period September 16-30, 2023, at the price of 303.3 USD/MT, CFR Aqaba parity. It’s yet another indication that puts extra pressure on the pre-season. Let’s note that the price of this sale was lower than the previous one by 2.2 USD/MT, also having a much more distant delivery period (end of September).

MIT JORDAN organized the second tender and purchased another 50,000 tons of wheat from Farm Sense Bulgaria at a price level of 303 USD/MT, delivery period October 2023, in the CFR Aqaba parity. It is, in fact, another price drop. Let’s note here the differential carry cost from the auction above and subsequently the financial cost.

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

CAUSES AND EFFECTS – THE STORY

We foresee a not too happy scenario in the coming months. Russia has every chance to take the decision to close the Corridor. It is, in a sense, a decision that must position it in the outpost of sales in the Black Sea basin, and if it doesn’t, then it will have a traffic problem with the new crop.

Naturally, their demands are unsatisfied, but they have always known this too, using this Corridor and the threat only as a lever to increase the price in the physical market. It is clear to everyone that the 275 USD/MT base will not be sustainable, so it will have to close the Corridor in order to generate volume for itself.

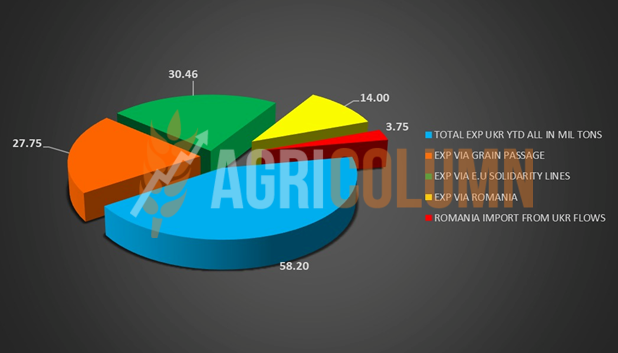

Ukraine has generated through the Corridor total volumes of 7.66 million tons of wheat, out of a total of 28 million export levels up to this date through the Corridor. And if the Corridor closes, the transfer will be possible through solidarity lines. But let’s consider their harvest volume this season, a crop that will reach a level of 21, maybe even 21.5 million tons, with an export level of at least 14 million tons, if not even higher, which will put extremely high pressure on the lines of European solidarity.

And these lines of solidarity revolted. Why? The neighboring countries allowed the transit also facilitated the explicit import of wheat into their territory. Price discounts for goods, combined with exorbitant price increases in transport, have caused damage that is difficult to quantify in this region. And the European Commission remained deaf to these obvious grievances, to the farmers’ protests, implicitly. The last straw for the farmers was the knowingly altered way from the start in which the level of compensation to be received by the affected countries, Romania, Poland, Hungary, Bulgaria, Slovakia and the Czech Republic, was calculated.

As a bloc, 5 out of 6 countries banned the import of goods from Ukraine, as well as their transit, triggering a crisis situation. What Russia failed to achieve, the European Commission masterfully achieved through its clearly wrong or malicious actions.

And thus, wheat experienced a spike on the stock exchanges, just as the fund liquidations for the month of May were starting. The trading algorithms did not miss the opportunity and marked new profits, because the end was predictable. One by one, the countries dropped the transit ban, maintaining only the import restriction on their territory.

The European Commission reacted in panic to this opposition block and generated a proposal for a new compensatory package of 100 million euros without specifying the calculation algorithm. And on top of that, it triggered a proposal to activate the safeguard clause by banning the import of wheat, corn, rapeseed and sunflower seeds to the five remaining countries in the bloc, as the Czech Republic effectively disappeared from the group. This activation should be valid until June 5, 2023.

But the group of five remaining countries reacted unitedly saying that if the products with import ban and the derivatives of these four products (oils, flour, meal), as well as products such as poultry meat, eggs, milk and products from milk and soft fruit, do not sign this agreement. The Commission’s response was unequivocal: “So we have a potential deal, we just need to finalize the list.” But if we don’t get along, we will go to the infringement procedure, that is, to the court. We therefore propose to establish at the conference of the ministers of agriculture on April 25, 2023 the finalization of the list and then the signing of the agreement, after which we amend the new regulation that must enter into force on June 5, 2023, an act that must continue to give the green light to the transit of Ukrainian goods.”

As for the letter of the 4 Prime Ministers and 1 President addressed to Ursula von der Leyen, this received a pitiful answer full of untruths. Not even a wise attempt to propose a constructive dialogue. Much wiser were the European Commissioners for Agriculture and the one for Trade, who admitted with subject matter and preached that the five countries are effectively flooded with cheap Ukrainian goods.

We must mention that Romania did not ban transit for a moment, nor did it block imports. We can judge this however you want, but the essence remains the 2017 association agreement as well as regulation 870/2022. And Ukraine has already denounced the European Commission for non-compliance with these agreements. But Romania, with all the huge problems created by the pressure of Ukrainian imports and transit, wanted to stay within the limits of these regulations. This creates dissatisfaction among Romanian farmers, rightfully so, but the flip side of the coin is the following: When we benefited from subsidies for years in a row, was it good to be in the European Union?

And the second parameter is the one that indicates the Health, Predictability and Sustainability of Romania in the European context.

These are things that may be unimportant to farmers, but tomorrow they may be of immeasurable value. Romania is, compared to the other 4 countries remaining in the negotiations, the only pole of stability in the Black Sea basin and Romania cannot afford to be dragged through European courts for non-compliance with the agreements. In the end, if we are to judge pragmatically, Romania remained in the negotiating bloc. The other countries have meanwhile relented and allowed transit again, and the time until the Commission’s decision regarding the import regime and their potential ban by June 5, 2023 is not long, a few days at most. How much cargo do you think will be able to enter Romania by then? We believe that not very much, because evaluating and following the numbers, we noticed a dramatic decrease in the import level, a fact caused by the approach to the new crop. But this is where the real problem begins. While everyone is fighting for money and the present, no one wants to see the future. And at this time, there is a present that indicates clear figures:

EXPORTS OF UKRAINE AND DISTRIBUTION THROUGH TRANSIT FLOWS AND RETENTION OF ROMANIA, EXPRESSED IN MILLION TONS:

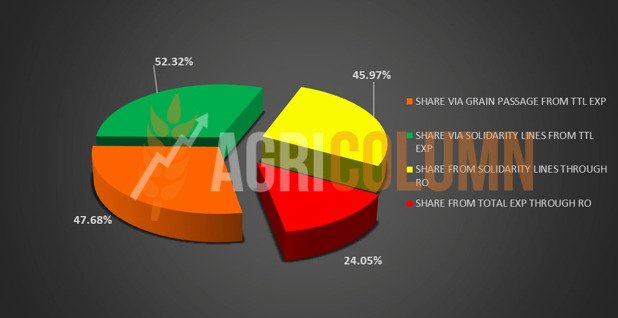

DISTRIBUTION OF UKRAINIAN EXPORTS EXPRESSED IN PERCENT:

As we said, no one sees the future, but we preview it and believe in the accuracy of our data and analysis. The scenario that will follow will be one that will make the lines of solidarity even more difficult:

- The closed corridor will generate transit through solidarity lines.

- The cheapest route is through Romania compared to the other countries in the group of 5.

- According to the algorithm, Romania will receive an overload of at least 11-12 million tons, to which we add the 14 related to the current season. In total, there are 25-26 million tons.

- We also add Romanian goods to the algorithm, which will generate a volume of at least 22 million tons, if not 23-24 million tons.

And now let’s start asking the questions:

- Will the port of Constanța be able to support this volume of cargo?

- Will Romania be able to logistically manage this volume of goods?

- Will Romania be able to manage the already extremely high price of logistics?

THE ANSWER IS ONLY ONE AND THAT IS NO, DEFINITELY NOT.

Constanța Port cannot operate this volume. The port of Constanța has an upper limit of a maximum of 33-35 million tons, in the context in which the ships’ schedule would be exactly aligned in time and space. Constanța Port cannot receive such a large volume of cargo. Effectively, it is not ready, and there will be queues and rushes of trucks, as well as endless lines of barges.

The price of logistics will increase greatly because availability is reduced, and Ursula von der Leyen’s answer through the letter addressed to the 4 Prime Ministers and 1 President is so empty and devoid of nuance that everything is obvious. Mrs. von der Leyen says she will lean on logistics and focus on the subject. How, when trucks, wagons and barges are not built overnight, and EU countries will not send their logistics? Simple because they need it too.

The big losers will be the Farmers from Romania, the big losers of this 2023-2024 season will also be the Romanian farmers. Because the goods will not be able to be extracted from the harvesting areas for export, and they will generate losses, remaining in the hands of local buyers, who have already learned their lesson and will no longer be so aggressive in terms of price.

Everyone today is focusing on distributing the Commission’s money and other things, just like a group of children playing in the school yard, forgetting to look up to see what evil is coming upon them.

As for the volumes of goods in the world, the forecasts indicate sufficient quantities and, implicitly, a tendency to decrease the price level in the stock market indications, as well as in the physical market. Whoever carried out Hedge on wheat some time ago acted with discernment and wisdom, accounting to this day important sums. And there is still time, because the trend is one of decrease, taking into account the FED meeting from May 2-3, 2023.

LOCAL STATUS

Price indications of feed barley are around 200 EUR/MT in CPT Constanța parity. Crop inverse no longer exists, all buyers are waiting for the new crop.

REGIONAL STATUS

UKRAINE will generate cumulative volumes (including territories occupied by Russia) of 3.77 million tons, 1% more than the 5-year average.

THE EUROPEAN UNION increases the forecast level of the future barley crop to the level of 54 million tons. If we also take into account the countries that are not in this group, i.e. Great Britain, Serbia, Bosnia and Moldova, we will be able to add a volume of 7.9 million tons, lower than the previous season by 0.4 million tons.

BARLEY PRICE INDICATIONS IN MAIN ORIGINS

GLOBAL STATUS

No essential changes.

LOCAL STATUS

Maize remains anchored at the level of 230 EUR/MT for the goods delivered in the CPT Constanța parity.

The new corn crop is valued at 200 EUR/MT, representing a decrease of 7-10 EUR/MT between the last report and today.

CAUSES AND EFFECTS

The old corn crop still remains at the level mentioned above, helped by the regional context of the Black Sea basin as well as the shortage generated in Argentina. And our estimates for the price of the new crop are proving true as time goes on, namely that they will decrease. We had a level of 227 and reached 200 EUR/MT CPT Constanța. We are talking about 27 euros effectively lost in three weeks. And things will advance from two areas, the decrease in price and the increase in logistics cost.

REGIONAL STATUS

THE EUROPEAN UNION. A new crop forecast comes from the European Commission, and it places the future European Union corn harvest volume at 65 million tons, 4 million less than the 2021 level, a benchmark in terms of volume.

UKRAINE will generate a volume of at least 25 million tons of maize in the coming harvest and we may see this volume increase due to favorable weather and rainfall.

RUSSIA will generate, for its part, a volume of at least 15 million tons, with an export potential of 5 million tons.

EURONEXT CORN – XBM23 JUN23 –239.5 EUR

EURONEXT CORN TREND CHART – XBM23 JUN23

GLOBAL STATUS

ARGENTINA does not improve the crop premise in any way. The level of 36 million tons is lowered by local analysis houses to the level of 33 million tons.

BRAZIL is in a volume regime of about 130 million tons, cumulative Safra + Safrinha.

USA. The pace of planting is in line with previous years, but in certain areas, rainfall makes this process difficult. Water is very beneficial and this aspect is more important than the time of sowing. It is still early, for they have snow and cold. But I remember 2019 just as well, when they sowed in June and had a superb harvest. Cordonnier said then that the corn was on his ankle and he did not believe in it. But it was wrong. They sowed late in 2019 due to the non-stop rains. Then followed 3 years of La Niña. And now we have the same scenario: water plus El Niño.

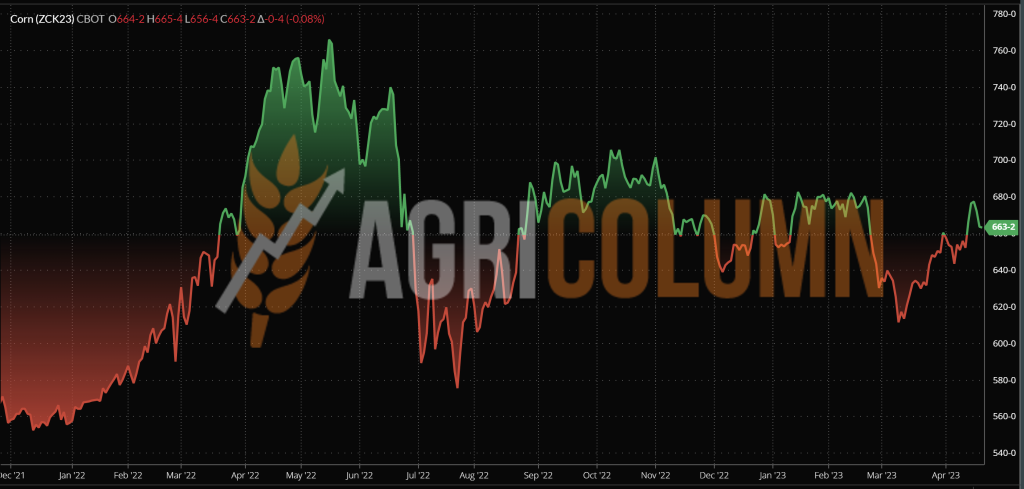

CBOT CORN ZCK23 MAY23 – 663 c/bu

CBOT CORN TREND CHART – ZCK23 MAY23

CORN PRICE INDICATIONS IN MAIN ORIGINS

CAUSES AND EFFECTS – THE STORY

Like wheat because of the tension in the European theater, corn generated a price spike. But things return to the same level as before. The crop inverse is increasing, and we will soon be able to see a much larger difference.

Production and potential figures point to confidence in the new corn crop across the Northern Hemisphere, with Brazil’s 130 mil. tons providing support in corn demand, mitigating the damage created in Argentina. But as time goes on and American farmers seed, we will see a decline in price indications.

In the wheat chapter, I pointed out the closed Corridor scenario and the figures show the following: 14.5 million tons of corn exported through the Corridor, 12.2 million tons extracted through solidarity lines. A total of 26.7 million tons of export Ukraine this season, up to this moment. The distribution will change completely and we will see how 14.5 million tons will be redistributed through solidarity lines.

As with wheat, the questions and answers are identical. But at the macro level, we have to see it this way. Of Ukraine’s total export, 53-54% are generated through solidarity lines, and 46-47% through the Corridor. In other words, more than 50% of Ukraine’s export is secured.

The corridor can therefore be closed. We can already see the lack of buyers and the fact that many ships no longer come to load. Effectively, they don’t have time to upload and wait for inspection until May 18, 2023.

The peak pressure SCENARIO will also intensify for corn, and volume and price pressure across the globe will fuel this. Naturally, the weather will be a key parameter, but only for short periods of time. El Nino has returned and replaced La Nina after 3 seasons. The price will not be fueled under a rich offer.

According to marinetraffic.com, the status of the POC (Pivnyi-Odessa-Chornomorsk) clearly shows the lack of activity in the mentioned area, in contrast to the area of the Constanța ports in Romania and the Chilia area, where you can clearly see the congestion of ships loading and waiting in the harbor road.

ODESSA AREA

SULINA-CHILIA AREA

CONSTANTA AREA

LOCAL STATUS

Old-crop rapeseed quotations in CPT Constanța parity are at the MAY23 level minus 40-50 EUR/MT. Subsequently, the new crop is valued at the level of AUG23 minus 40-50 EUR/MT.

CAUSES AND EFFECTS

Rapeseed is conditioned by the two parameters we know very well: fossil energy quotes and the VegOil complex. Both acted accordingly and caused spikes. The indication MAY23 remains a reference parameter, because the next trend will be determined around it, once the liquidation from the speculative funds begins.

EURONEXT RAPESEED – XRK23 MAY23 – 456.5 EUR

EURONEXT RAPESEED TREND CHART – XRK23 MAY23

REGIONAL STATUS

The EUROPEAN UNION remains in the same forecast status between 19.5-20.2 million tons. The Union has an impressive import volume, we could say, of 6.36 million tons mainly coming from 2 actors: Ukraine and Australia. Ukraine introduced a volume of 2.94 million tons into the Union, while Australia is at the level of 2.82 million tons.

GLOBAL STATUS

No references at this time, off season. Sowing will begin simultaneously in Australia and Canada.

ICE CANOLA RSK23 MAY23 –764.6 CAD

CANOLA ICE TREND CHART – RSK23 MAY23

COMPARATIVE GRAPH. PETROL-RAPESEED-CANOLA CORRELATION

CAUSES AND EFFECTS – THE STORY

The panic induced by the 5 member countries of the European Union that reacted en masse to the lack of reaction of the European Commission led to a new spike of rapeseed in Euronext. The fear that the minimum 3 million tons of rapeseed related to the 2023-2024 season will not be able to be brought to the Union has generated the price increase. And let’s not forget the spike caused by OPEC+.

But the tension is starting to dissipate, and the quotes are settling down. There remains unexpected support from palm oil, but we also estimate a negative impact coming from soybeans, which will be seen at the opening of the Euronext session on April 24, 2023.

Rapeseed is somewhat of a finished story, if we are talking about the old crop. The position liquidations remain on MAY23 and the effective transition to AUG23, where we do not see the crop inverse, a sign of stability on volume until this moment.

Destabilization could arrive rapidly during MAY23 through seedings in Canada and Australia. There is a reference point that can and we believe will cause declines in AUG23 indications.

So rapeseed cannot generate too many surprises at this moment apart from the logistical ones related to wheat and corn. The 45 EUR discount compared to Euronext also carries with it Romania’s failure to convert the values of Joules/kg into grams of CO2/kg of dry matter. And this has a weight of at least 20 EUR/MT, money extracted from the pocket of the Romanian farmer, of course.

Moreover, the price of a barrel of oil diluted and thus generated less support for rapeseed. A barrel of oil in the quote Brent June 2023 is at $81.66, up from $87, a previous day’s peak.

LOCAL STATUS

Port Constanța quotes sunflower seeds at 420 USD/MT.

Processors also offer the same price level in parity DAP processing units.

CAUSES AND EFFECTS

Sunflower seeds remain at the same level as before the Orthodox Easter. No changes have been made in this regard. Supply is following its natural course and it is clear that the crop inverse is at least 20 USD/MT. But as the development in the Black Sea basin will advance, things may change against the seed price.

REGIONAL STATUS

UKRAINE. They will sow more than 6 million hectares of sunflower seeds, which will lead them to a production per hectare similar to that of the previous year at a volume of 13 million tons. But if the productivity per hectare increases as in 2021, we will clearly see figures close to 15 million tons.

RUSSIA will, by all our analysis, generate a crop of 16.5 million tons of sunflower seeds and will clearly influence the crude oil market regionally as well as in “friendly” destinations such as be India.

GLOBAL STATUS

ARGENTINA will close the harvest at the level of 3.8 million tons of seeds, so there will be no more influences from South America in this regard.

PRICE INDICATIONS FOR OILSEEDS AND CSFO IN MAIN ORIGINS

CAUSES AND EFFECTS – THE STORY

Global sunflower seed production will reach 54.8 million tons in 2023/24, according to the latest estimates by the International Grains Council (IGC). That would be an increase of 8 percent or 4 million tons from the current season, the March 23 report said.

Projected growth was based on anticipated yield increases, which were expected to return to near-average levels following disappointing heat-related results in 2022. Yield increases are expected particularly in Europe, with EU27 sunflower seed production estimated to increase by 1.1 million tons compared to the previous year.

Ukrainian production will increase by 1.5 million tons to 13.5 million tons, Russia is expected to harvest 15.8 million tons, an increase of 0.8 million tons.

I hope we all understand what will happen to the price of sunflower seeds in this context and what will come next. More specifically, closure of the Corridor would have the effect of spilling seeds and crude oil towards the lines of solidarity. This aspect will create pressure on local prices as well as the logistics cost which will increase in line with the availability of means of transport.

A higher production associated with remaining stocks in Bulgaria (about 1 million tons), Romania (minimum 0.4-0.5 million tons) will create a premise for a much lower price in the overall new crop of sunflower seeds. Some compensation would have to come from demand, but as we realized in the season we will soon end, destinations dictate, and discount palm oil has attracted a lot of buyers. Now, palm oil is generating a lack of production and by implication processing and export availability due to the weather in Indonesia. This still gives that 20 USD/MT support to sunflower seeds.

But the buyers of crude oil from the Black Sea basin, and we are specifically referring to Ukraine, have kind of disappeared in the premises of the closure of the Corridor. The last quotes were below 900 USD/MT and there weren’t many takers.

In conclusion, according to IGC forecasts, we will experience a downward slope in terms of the price of sunflower seeds related to the new crop. The old crop must be sold, because very soon the factories will enter the annual revisions and will start the new season with the processing of rapeseed, which will be harvested first from the group of 3 oilseeds.

LOCAL STATUS

In Romania, the price indications for soybeans are at the level of 500 USD/MT, DAP processing units for non-GMO soybeans.

Between July 1, 2022 and April 12, 2023, approximately 197,000 tons of soybeans were imported.

REGIONAL STATUS

EUROPEAN UNION. Total imports of soybeans in this trading season reached the level of 9.5 million tons. And soybean meal reached the level of 12.2 million tons. Spain, the Netherlands and Germany lead the list of soybean importers, while for soybean meal we highlight Spain and France.

GLOBAL STATUS

ARGENTINA. It is lowered immediately after the WASDE report by local analysis houses to the level of 23 million tons. The Dollar-Soy program is not producing the expected results, despite a parity of 300 pesos/1 USD against 230 pesos/1 USD, the normal exchange rate.

BRAZIL. The volume harvested in Brazil is extremely generous. They will exceed the figure of 156 million tons, which literally fuels and shakes the local price level.

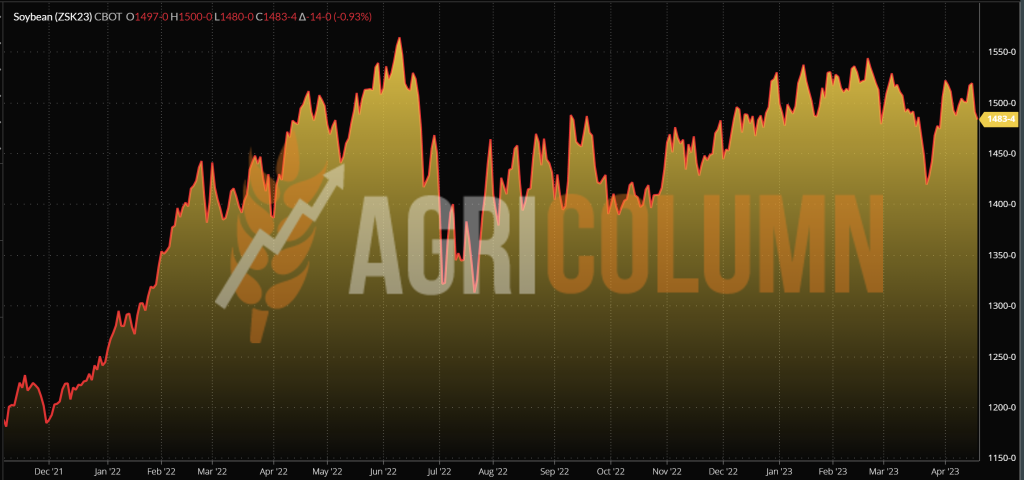

CBOT SOY ZSK23 MAY23 – 1,483 c/bu

SOYBEAN TREND GRAPH – ZSK23 MAY23

CAUSES AND EFFECTS – THE STORY

Brazil’s gigantic crop is penalizing the price, and we’re seeing this reflected in US stocks driving soybean purchases from Brazil. The 2 USD/bushel shipping cost has no impact so the flow is open.

At the same time, the North American volume potential calculation makes the CBOT crop inverse extremely obvious, measuring MAY23 where the liquidations and roll-overs started with NOV23. The result is simple and clear, minus 200 c/bushel i.e., 73.5 USD/MT.

Clear notice therefore to the sellers of new crop soybeans in Romania as well as to the buyers of soybean meal for the animal husbandry industry. The former must secure the forward price, and scrap users must not over-expose themselves by long-term buying and fixed and high price. It all boils down to calculating the replacement level at the same level of protein content in soybeans and soybean meal.

EXTRA

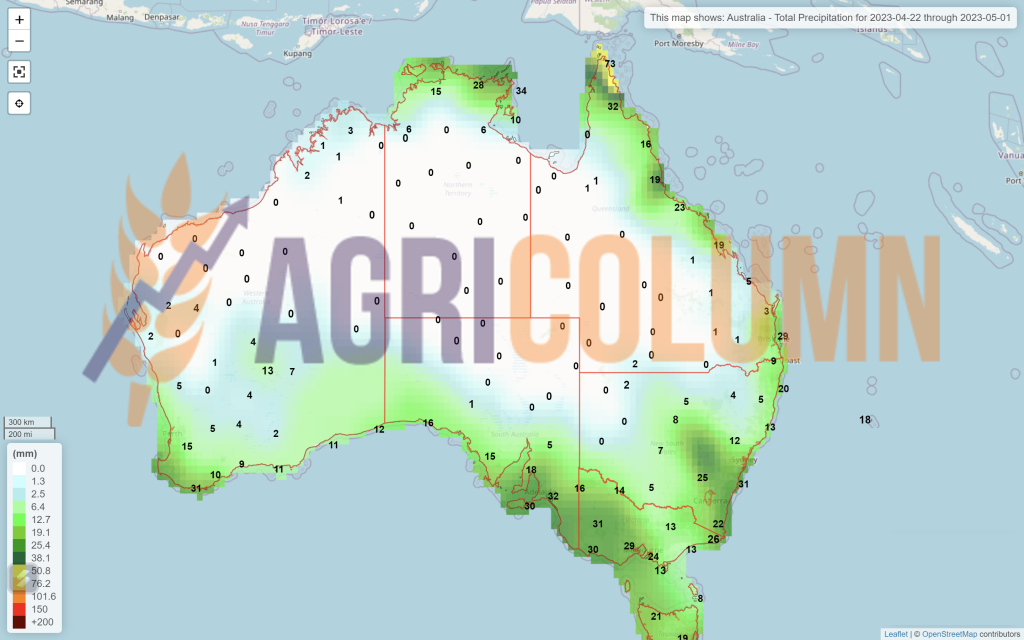

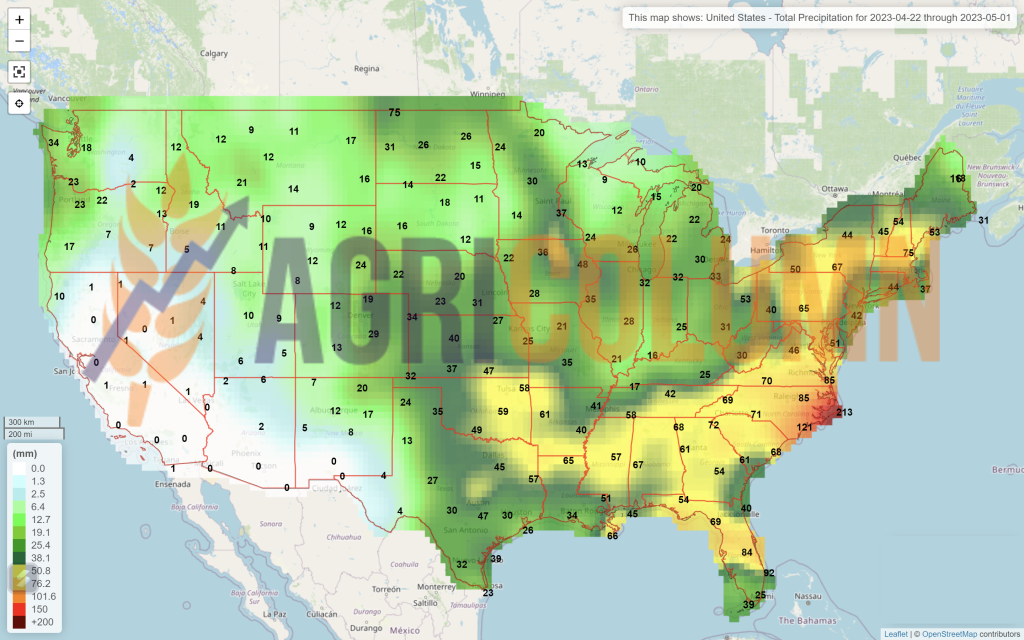

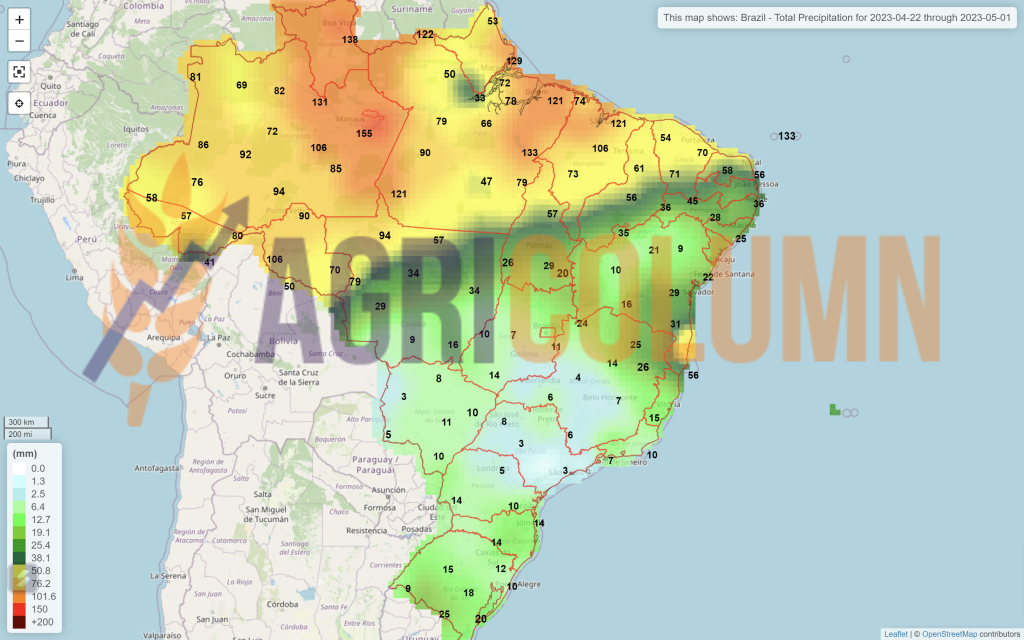

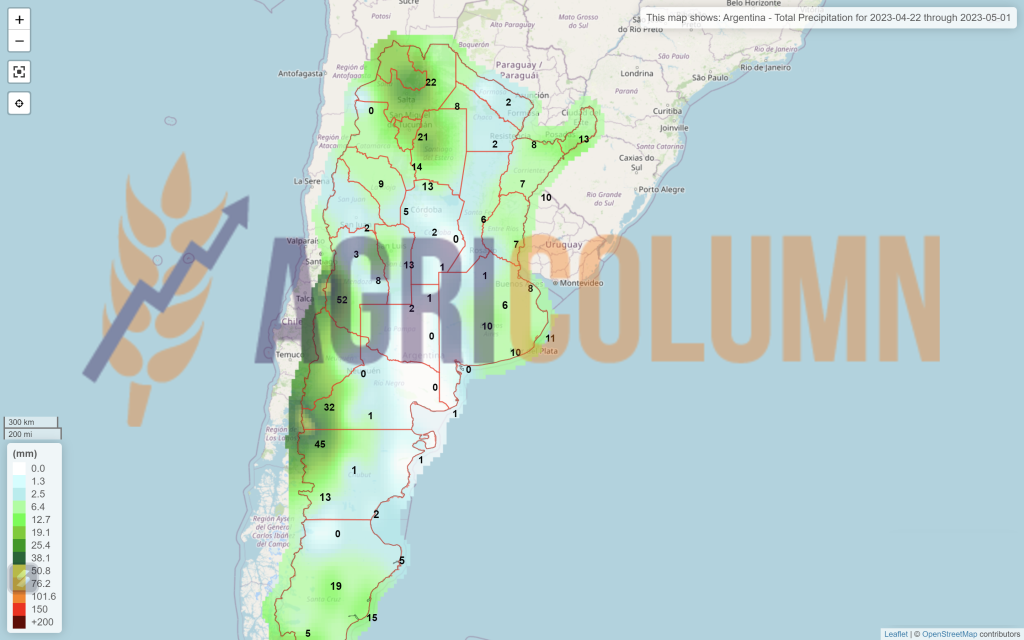

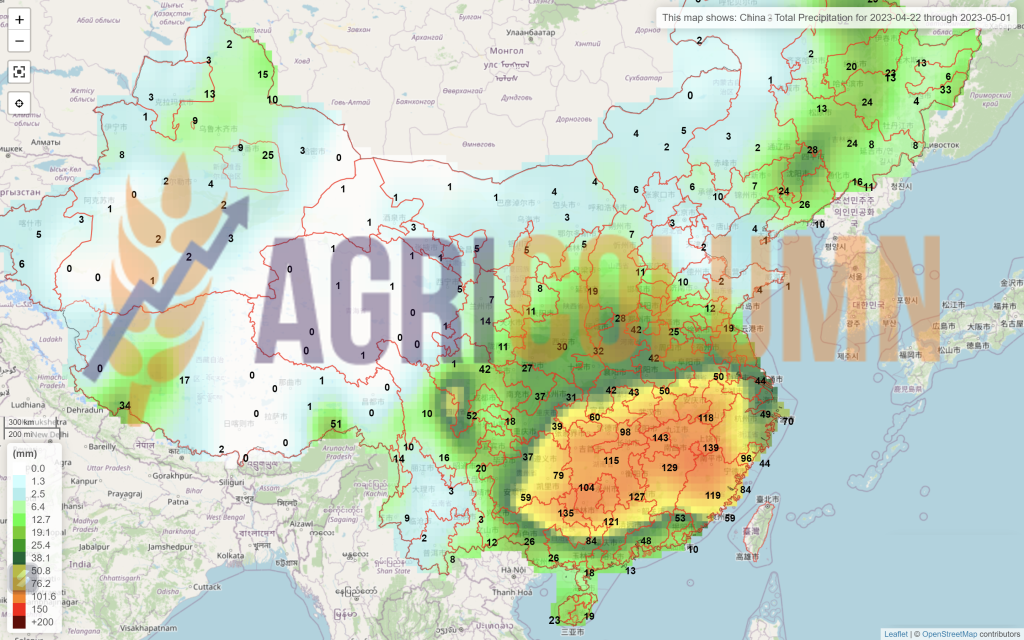

April 22 – May 1, 2023

Romania

Europe

Ukraine

Russia

Canada

USA

Brazil

Argentina

China

Australia