This week’s market report provides information on:

LOCAL STATUS

The indications of the port of Constanța suddenly melted on Friday afternoon under the recoil effect generated by the agreement between Ukraine and the UN with Turkey as a broker on the one hand, together with Russia’s agreement with the UN, also mediated by Turkey as an intermediary. Thus, we predict the market in the opening of the week located at a level of 335 EUR/MT, in the CPT Constanța parity. Wheat with feed quality is still quoted with a discount of 20 EUR/MT compared to milling wheat.

However, the level is higher than the EURONEXT SEP22 closing indications of Friday, July 22, 2022, by at least 10 EUR/MT. The fundamentals of the physical market, i.e. supply versus demand take precedence over the technicalities generated by the stock market.

The local market will be adjusted accordingly, but here the quality of the wheat takes precedence. Processing units generate demand parameterized by the gluten factor and the alveographic index W. In the case of gluten, the requirement is a minimum of 24, and in the case of W, wheat must not have a value below 180. A note regarding the value of gluten: it is not about measuring gluten by the wet method (silage), but its determination is carried out by the dry gluten method related to the processing units. As a price level, wheat processing units are quoting between 335 and 345 EUR/MT.

But Romanian farmers do not have a particular appetite for selling wheat volumes, counting on the fact that the crop was thinned by unfavorable weather conditions from the time of sowing to harvesting, and we will have a wheat crop level adjusted to the level of 9 million tons.

CAUSES AND EFFECTS

The understanding and the act signed by each of the parties involved in the war, Ukraine and Russia, provides a moment of relief globally and thus the market reacts according to this moment. The release valve of some potential volumes from Ukraine generates the fall of the European stock market and subsequently the North American one.

The retention practiced by Romanian farmers is penalized these days by the effect of the treaty called “Initiative for the safe transportation of Ukrainian goods”, but it is not the only aspect that penalizes the price. The European Central Bank increased the interest rate by 0.5%, in an attempt to curb the galloping inflation.

Farmers in Bulgaria and Poland practice the same system of retention of goods, stimulated by the reduced volumes in the European Union, but on the wave generated by the signing of the Safe Transport Initiative, the price of wheat falls, technically corrected and by the increase in interest at the level of the European Central Bank. And there is something else on the horizon, but we will discuss this in the regional section.

REGIONAL STATUS

RUSSIA indicates through Rusagrotrans a wheat crop level of Homeric proportions, namely 92.6 million tons. The difference between the USDA’s July 2022 estimate and this estimate is about 11 million more tons. It is a very large amount of goods, which will effectively flood the Black Sea basin, because Russia will have to export, and the underground negotiations carried out between the parties and overseen by Sergei Shoigu from the Russian side have aspects that we must certainly expose, even if they are not clearly expressed. It is, moreover, logical, since the negotiations were conducted for Ukrainian goods, not for Russian ones.

UKRAINE indicates a less happy status of wheat volumes. Today, according to the relevant Ukrainian ministry, we see a harvested volume of 3.8 million tons of wheat, with an average yield of 3.15 tons/ha from 25% of the expected areas (4.9 million ha). Through a simple mathematical formula, we can estimate a total harvest volume of 15.2 million tons, down from the provisional estimate of 19.5 million tons, according to the latest WASDE report. And we see how part of the Russian crop potential is diminished by the Ukrainian minus, quantified in numbers at 4.3 million tons. The Ukrainian volume of 5.5 million tons left unexported from last season should not be neglected either. Added to 15.2 million tons, this volume will raise Ukraine’s crop to 20.7 million tons.

The EUROPEAN UNION is on the same level of 125 million tons total volume of soft wheat, France being at the moment at the level of 86-88% harvesting level, according to France AgriMer.

TENDERS

EGYPT. Following Mr. Biden’s visit with his Egyptian counterpart, Abdel Fattah El-Sisi, on July 17, Egypt’s prime minister says the value of American investment has increased by $15 billion in 2021-2022 compared to 2020-2021. Driven by the visit of Mr. Biden, GASC Egypt generated on July 19, 2022 an attempt to purchase through GASC (we emphasize the word „attempt”, because it was doomed to failure). GASC has made the decision to initiate a tender open only to US, Canadian, Australian, Brazilian and Argentine origins. Knowing the crop timing, we immediately noticed that Brazil, Argentina and Australia were entered as ghosts, their harvest period being after the delivery period mentioned by GASC.

This first aspect made us circumspect and we noticed in the first line of offers a totally unknown company, Egyptian African CO. We concluded quickly that it was acting as a submarine in the auction, that is, it would try to lower the price offers as much as possible. Total disappointment was expressed by canceling the tender. The US wheat was bid at a spread of more than 40 to 60 USD/MT in CIF parity to the current price level. It was a clear sign of reduced competitiveness for logistical reasons. US wheat has a transport indication of 48-65 USD/MT, and the lowest offer in FOB North American origin was at the level of 395 USD/MT above the value of the Black Sea basin (367-373 USD/MT).

The day after the failure of the open tender, on July 20, 2022, Egypt returned to a direct tender process, where it purchased a volume of 640,000 tons of wheat, originating in Russia, France plus two lots from Lithuania and Greece, at the value of 403 USD/MT CIF.

420,000 tons were awarded by France, 160,000 tons by Russia, Lithuania won 30,000 tons and Greece !!! 30,000 tons. The negotiating submarine, Egyptian African Co, was present and paid for the consignments from Lithuania and Greece. Otherwise, French wheat was distributed between Cargill (180,000 tons), Lecureur, Olam, Viterra and Soufflet (60,000 tons each). The Russian one was distributed between Aston (60,000 tons), Grain Export (60,000 tons) and GTCS (40,000 tons).

On July 21, 2022, GASC Egypt purchased another 120,000 tons of wheat, a mix of French-Russian origin again, at the level of 402.5 USD/MT CIF. Apart from the spot deliveries originating in Lithuania and Greece that will take place in the second half of August, the rest of the deliveries span from September 15 to November 15, 2022. We thus total a volume of 760,000 tons purchased by GASC Egypt.

MIT JORDANIA also had an attempt to purchase wheat that did not materialize.

EURONEXT MLU22 SEP22 –325.75 EUR (minus 25 EUR) (EFFECT OF ISTANBUL AGREEMENT!!)

EURONEXT WHEAT TREND CHART – MLU22 SEP22

GLOBAL STATUS

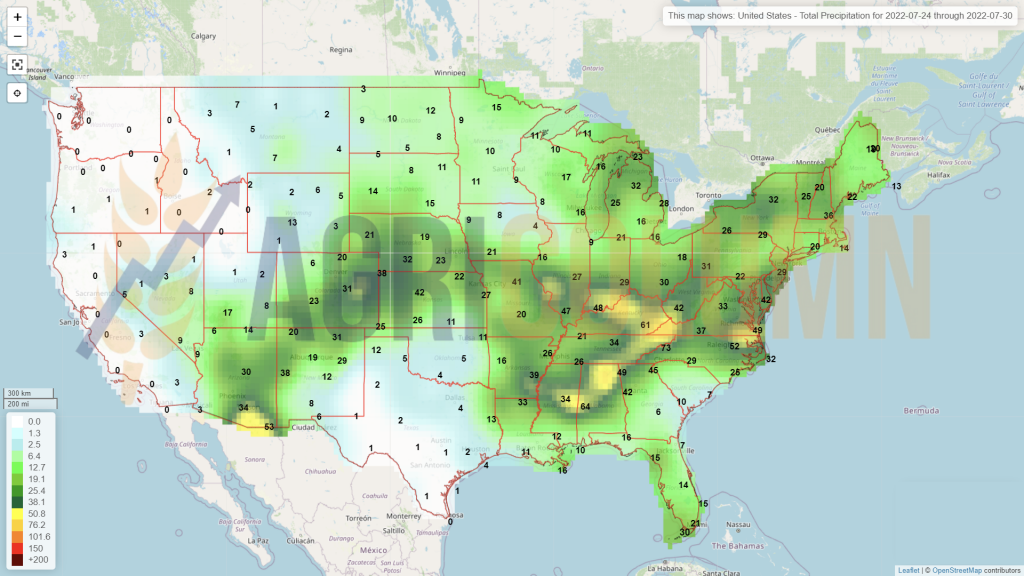

The US is ramping up its wheat export volumes to destinations such as China, in particular. The US winter wheat harvest level has exceeded 75-77% and soon this process will come to an end. Forecasts remain stable at 48 million tons, helped by the emergence and development of spring wheat, which has partially recovered losses suffered by winter wheat.

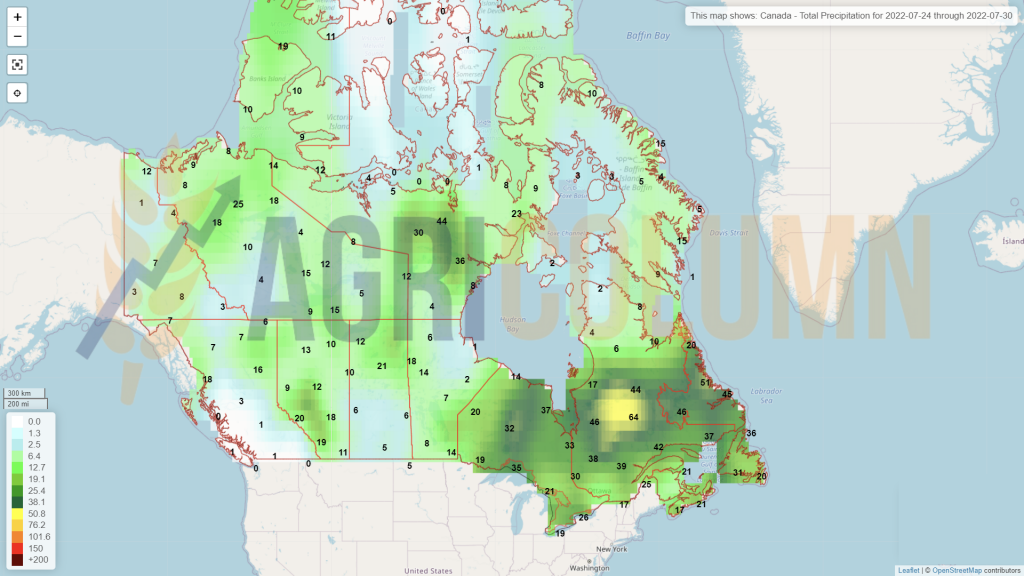

CANADA remains at the same forecast level of 34 million tons, with weather helping the wheat crop.

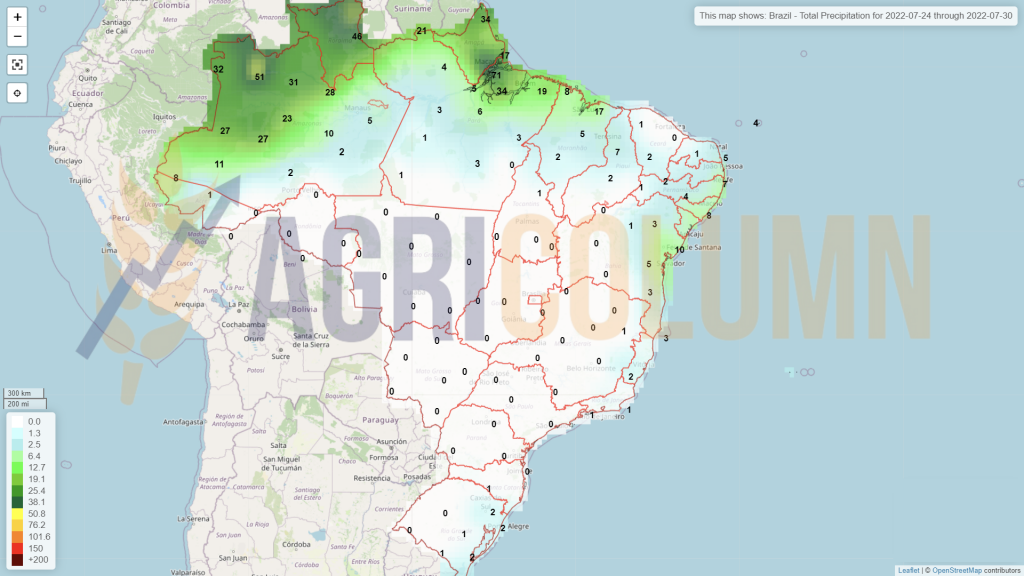

BRAZIL is outside the harvesting window.

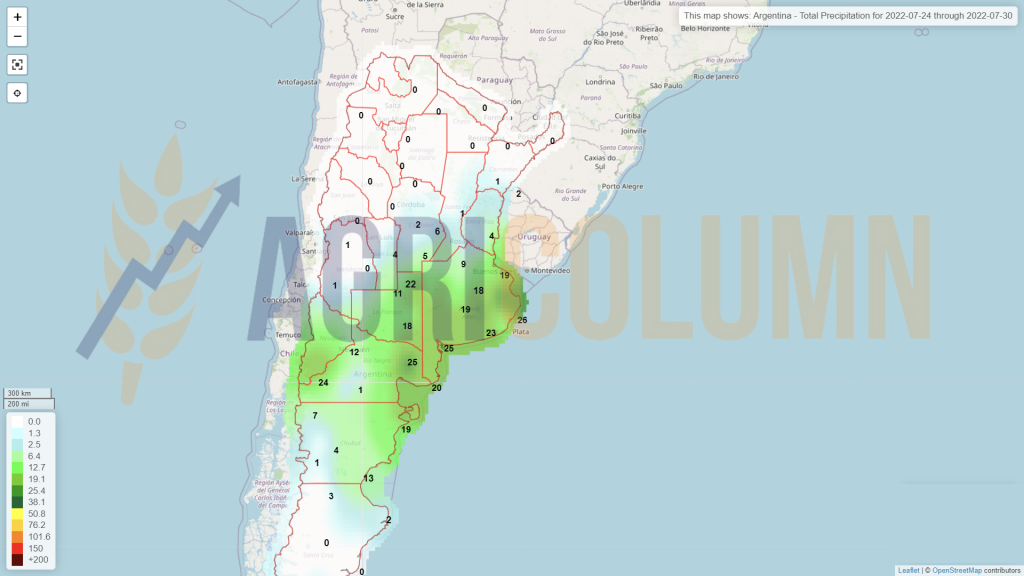

ARGENTINA is having problems and is still lowering the area intended for sowing by another 100,000 hectares, to the level of 6.1 million ha. In total, we have a degradation in terms of sowing plan by 400,000 hectares, they start from an estimate of 6.5 million ha.

AUSTRALIA also looks very positive. 33 million tons remains the volume forecast.

CBOT ZWU22 SEP22 – 759 c/bu (minus 47 c/bu = minus 17.25 USD)

CBOT WHEAT TREND CHART – ZWU22 SEP22

CAUSES AND EFFECTS

Before developing the regional topic, we must keep our eyes wide open to China, which has purchased over 1 million tons from the US and at least 7 wheat ships from France. The goods are in demand, and China is doing the right thing – stock piling of wheat. This aspect should not be ignored under any circumstances.

The long-rumored initial assumption, namely an agreement to create a humanitarian corridor to extract Ukrainian goods, was signed on July 22, 2022. The name Safe Corridor Initiative, however, suggests otherwise.

Ships with captive cargo from Ukrainian ports must leave. Depreciated goods or not, they must go. Many of them are not owned by Ukrainian entities and the owners are from third parties. Depreciated goods from them will be directed to poor countries.

About the three ports allocated for shipping, however, it’s a completely different scenario. Odessa, Yuzhny and Chornomorsk combined can ship about 20-22 million tons per year. But these figures are estimates generated under certain conditions such as: peace, undamaged port infrastructure, demined port area, the possibility of delivering goods from the interior to the port, undamaged interior infrastructure. This accumulation of factors indicates that, in fact, the primary concern is only the movement of captive ships within the range of the designated ports, and that’s about it. It’s a mouthful of oxygen and nothing more. We can even speculate that if the port area of Odessa is cleaned, it makes it easier for Russia to attack. The disappearance of foreign ships from the landscape would be beneficial for the Russians in their attempt to conquer Odessa.

We must state very clearly, however, that this Initiative is expressed in two segments – one is signed by Ukraine-UN and Turkey as mediator, and the other by Russia-UN and Turkey as mediator.

WHAT DOES UKRAINE GAIN?

Apart from the potential departure of captive ships, nothing else. Preparation for export can take up to three months, demining, restoration of port facilities, return of operating personnel to the port, arrival of goods from the country, are operations that require time. And Russia is not stopping. A few hours after the signing of the Initiative, they bombarded Odessa with missiles, as well as the port. So the signal is clear, only the ships. What is outside the ships will clearly be subject to Russian rules of war.

We also estimate a very slow process of estimating the costs of insuring ships that will leave the three ports. A number of insurers are interested in providing cover for grain shipments from Ukraine after an agreement was reached, Lloyd’s claims. Ships that could leave with cargoes of grain from Ukraine should do so several weeks apart. Details, including commercial contracts, of the Ukrainian grain deal are still to be worked out and insurers will assess each cargo individually, according to the Lloyd’s official. Here we clearly see that the 120 days allocated to this corridor will run out very quickly, without major movements in terms of exports.

WHAT DOES RUSSIA GAIN?

First, they will get the sanctions on Russian ships lifted and they will be able to ship grain wherever they want. Grains were never sanctioned, only ships and the SWIFT payment system, from which Russia was disconnected. In addition, they will exploit, albeit unofficially, the occupied zones, in the sense that they will actually take Ukrainian grain and export it through Mariupol and Berdyansk, absolutely without any embarrassment.

They will be able to ship and collect anywhere in the world. Let’s not forget that clandestine transports have been the prerogative of Russia for a long time, the latter behaving like a real trafficker.

On top of that, we assume that Russia also got sanctions lifted on the sale and export of fertilizers, which is a big win. Today, Russian fertilizers that are in stocks in other countries are blocked. And the port of Constanța has a substantial lot blocked from trading.

We need to understand the pressure that Russia has been under lately with the volume of harvest volumeit is generating. With no chance of shipping due to naval sanctions and extremely high insurance costs (Panamaxes did not enter the Sea of Azov to Novorossiysk, Tuapse, Taman and the Caucasus, shipowners did not take this risk), the Russians are effectively sitting on mountains of wheat.

As much as India, Pakistan and Kazakhstan formed the corridors, they had an insurmountable problem, namely the price of the goods associated with the logistics cost. Their goods were offered at a discount in order to be picked up, and the logistics cut a large portion of the price, due to the risks associated with routes behind the curtain of sanctions.

The fact that they are not competitive is clear from the action taken to re-calculate the export duty. With the ruble much stronger than before the conflict, due to its lack of tradability with foreign goods, Russian farmers receive much less per ton of wheat than before the invasion of Ukraine. Before the invasion, 1 USD was worth 75 RUB, and today 1 USD is worth 58 RUB, so when calculating the price in USD for 1 ton of wheat, a Russian farmer receives much less money expressed in rubles, because what else could they use in Russia?

“The Russian Federation needed less than 24 hours to question the agreements and commitments it made to the UN and Turkey in a document signed yesterday in Istanbul with a missile attack on the port area from Odessa.

The Russian missile is Volodymyr Putin’s “respect” to UN Secretary General António Guterres and Turkish President Recep Erdogan, who made great efforts to get the agreement and to whom Ukraine is grateful. Ukraine expressed the need for a smooth implementation of the agreements for the resumption of safe exports of Ukrainian agricultural products on the Black Sea from three ports. We urge the UN and Turkey to ensure that Russia honors its commitments to the safe operation of the grain corridor.

If the agreements are not respected, Russia will be held fully responsible for worsening the world food crisis.” Excerpt from the statement released by the Government of Ukraine, after Russia bombed Odessa again, wanting to remind who is in control.

We are inserting for your reading the content of the act signed in Istanbul by the Ukrainian side, by the UN and assisted by the representative of Turkey.

Initiative on The Save Transportation of Grain and Foodstuff from Ukrainian Ports1. The parties of this initiative are the Republic of Turkey, the Russian Federation and Ukraine and the UN Secretary-General. 2. This Initiative is based on agreements of parties of the The International Convention for the Safety of Life at Sea, 1974, as amended, SOLAS, Regulations XI-2/11 and The International Ship and Port Facility Security Code (ISPS Code), Part B, paragraph 4.26. 3. The purpose of this Initiative is to facilitate the save navigation for the export of grain and related foodstuffs and fertilizers, including ammonia from the Ports of Odesa, Chernomorsk and Yuzhny (“the Ukrainian ports”) 4. The Parties recognize the role of the Secretary General of the United Nations in securing the discussions for this initiative and request his further assistance in its implementation, in the furtherance of the humanitarian mission of the United Nations and subject to its authorities and mandates. 5. To achieve the purposes of this Initiative, and to provide for the save navigation of vessels carrying grain and foodstuffs, the Parties agree as follows: Primary aspects of the InitiativeA. This Initiative assumes that all Parties will provide maximum assurances regarding a save and secure environment for all vessels engaged in this Initiative. Prior to operations commencing and coordination structure will be established. A Joint Coordination Center (JCC) shall be set up in Istanbul under the auspices of the United Nations and includes representatives of the Parties and the United Nations. The JCC shall conduct general oversight and coordination of this Initiative. Each Party of the United Nations will be represented in the JCC by one senior official and an agreed upon, required number of personnel. B. Inspection teams will be set up in Turkey. The inspection teams on Turkey will consist of representatives from all Parties and the UN. Vessels will transit to an enter the Ukrainian ports in the line with the JCC approved schedule upon the vessels’ inspection by an Inspection Team. The primary responsibility of the Inspection Teams will be to check for the absence of unauthorized cargoes and personnel on board vessels inbound or to outbound from the Ukrainian ports. C. All activities in Ukrainian territorial waters will be under authority and responsibility of Ukraine. The Parties will not undertake any attacks against merchant vessels and the other civilian vessels and port facilities engaged in this Initiative. Should demining be required, a minesweeper of another country, agreed by all Parties, shall sweep the approaches to the Ukrainian ports, as necessary. D. Merchant vessels will be prior registered in the JCC, verifying their details and confirming their loading port, having liaised closely with port authorities. Vessels will be technically monitored for the duration of their passage. Vessels will proceed through the maritime humanitarian corridor, agreed by all Parties. The JCC will develop and disseminate a detailed operational and communications plan, including identification of safe harbours and medical relief options. E. To prevent any provocations and incidents, the movement of vessels transiting the maritime humanitarian corridor will be monitored by the Parties remotely. No military ships, aircraft, unmanned aerial vehicles (UAV) may approach the maritime humanitarian corridor closer than a distance agreed by the JCC, without the authorization of the JCC, and after consultation with all Parties. F. Should any suspicious activities, or non-compliance with the rules of this operation or emergencies occur on a vessel transiting the maritime humanitarian corridor, depending on its location, upon the request of a Party to the JCC and under international maritime law, the Parties will provide the required assistance to the crew or conduct an inspection against the security guarantees. G. All merchant vessels taking part in this Initiative shall be subject to inspection conducted by an Inspection Team in the harbours determined by Turkey at the entry/exit to/from the Turkish strait. H. This Initiative will remain in effect for 120 days from the date of signature by all Parties and can be extended automatically for the same period, unless one of the Parties notifies the other of the intent to terminate the initiative, or to modify it. I. Nothing in this Initiative will be deemed as a waiver, express or implied, of the privileges and immunities of the United Nations, and the Parties will ensure that the Initiative does not entail any liabilities for the United Nations. |

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

LOCAL STATUS

The local price of barley has been in a continuous swing with more or less interest. On Friday, its indication was 285 EUR/MT in the CPT Constanța parity. However, the agreement with wheat will generate a decrease of at least 1 EUR5/MT and we will see barley at the threshold of 270-273 EUR/MT during the release day of the AGRI COLUMN report, today, 25 July 2022.

REGIONAL STATUS

UKRAINE generates an update of the barley crop and we observe a status of the Ukrainian crop of 2.8 million tons of barley, with an average yield of 3.1 tons/ha, from 46% of the area sown with barley. The previous year, the yield was 4.18 tons/ha.

But Ukrainian commodities are developing the same border pressure and we see barley offers at 165 USD/MT CPT Reni and 200 USD/MT FOB Chilia.

We also note an attempt for a tender by MIT Jordan which did not materialize in any way. Probably the price was the main source of the cancellation of the tender. The participants were numerous and we list here Bunge, Viterra, Ameropa, Australian Grains and Soufflet.

CAUSES AND EFFECTS

Barley has the path marked by the evolution of the price of feed wheat and this is felt in the daily quotations, which oscillate in accordance with the latter. The domestic market generates demand, and the barley volume will be in demand with August and September, followed by the seasonality of January-February 2023.

BARLEY INDICATIONS IN MAIN ORIGINS

LOCAL STATUS

Corn indications at the port of Constanța are at 285-287 EUR/MT. As an indication, there is no longer any crop inverse between the old crop and the new crop, only interest, meaning that not all buyers are buying old crop corn anymore.

ROMANIA has extraordinarily big problems. The drought savaged corn nationwide, ravaging the crop in its own way. Entire counties suffer from soil drought established over time, starting with the winter without precipitation and culminating in the heat zone of over 38-40 degrees that we cross in a total lack of precipitation.

We can say that this effect of pedological drought has not been encountered in the last twenty years at a local level on such an extensive surface. Entire counties are effectively destroyed by drought combined with sweltering heat, amid a total lack of rainfall. Areas that traditionally did not suffer from drought, today are effectively calamity.

The area of the western belt of Romania, starting from the northwest (Bihor county) and going down to the southwest (Timiș county) is compromised. The area of the Southern belt, starting from the southern area of Olt county and up to Călărași county, is also in maximum difficulty. Bărăgan is also exposed and all of Moldova is severely affected by the drought on its entire surface. Even the Transylvanian Plateau, which traditionally, due to the relief, benefits from precipitation, is seriously affected. And, of course, we also have Dobrogea, which traditionally suffers from a lack of precipitation.

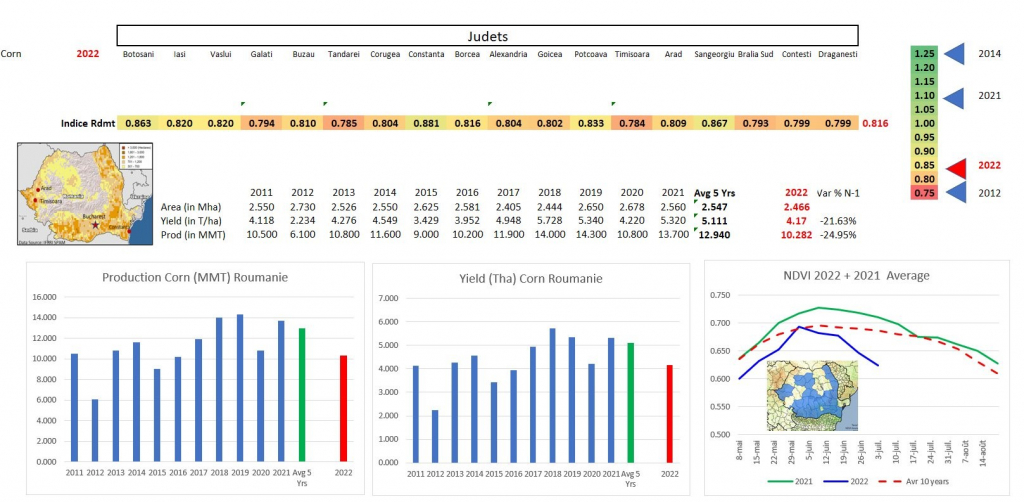

In these disastrous conditions, Romanian corn actually melts under the high temperatures. And from the beautiful forecast of 14.5 million tons, we are today at the level of 10.3 million tons. But all the chances are and will materialize to reach the level of 8 million tons. According to Murphy, what starts bad ends worse. In order to have a correct picture generated by the numbers, we insert, courtesy of Visio-Crop (www.visio-crop.fr), graphic figures that will reveal the size of the Romanian crop at this moment and, as I said, not everything is finished.

As you can see, we are quoted at a maximum yield of 4.17 tons/hectare and have an estimated production of 10.28 million tons, up from 13.7 million tons in 2021 and a five-year average of close to 13 million tons.

CAUSES AND EFFECTS

Farmers must be extremely cautious and not expose themselves through forward sales to what they cannot execute. Farmers who have signed should try to execute the contracts, and if not possible, to initiate mediation discussions within the delivery period, certainly not at the end. The minister declares that no state of calamity is imposed, but instead promotes the idea of restricting the export of corn in the most overt way possible. Well, if there is no state of calamity, why are you introducing the idea of export restrictions? Cancellation by contradiction or how to interpret the minister’s words? Frankly, we do not know in whose name the minister is speaking.

What else can be done? Nothing at all. The weather does its own calculations for us. And we do not enter her positive page in any way. What are the authorities doing? And I would answer: what else could they do? Apart from the classic populist corn walks, they have nothing to do today. We are helpless and tributary to a system that we have been propagating for over 32 years, a system made up of a lack of skills, technical qualities and understanding, a system based on personal interests and political dictates, a system that has grafted incompetence at every level and lack of national interest.

We are at the moment when the authorities are discussing irrigation systems, completely forgetting about the atomization at the national level of those who own the land. It is completely ignored that the national irrigation system is only on paper in the executive but is completely absent from the physical plan. Destroyed, stolen, devoid of any maintenance factor. Sporadically, it works through the care of groups of farmers, but what remains is an energy-hungry system that consumes energy and wastes water. Romania can do more than sterile political statements year after year. How do walks through the corn help us? How does the internecine struggle for power decorated with trails between the National Anti-coruption Direction and the field for cheap and outdated propaganda help us? How does it help us that televisions are run through the corn field for the cheap and sensational circus at the same time? We are all to blame for what is happening today. We were careless spectators and reluctant to take initiatives, to demand, to unite Romanian sovereign interests and now we find ourselves at this moment.

Make no mistake, an irrigation system is built from scratch, just like a circulatory system, which first needs an assessment of the areas where drought is most exacerbated and repetitive. Then a mapping must be generated of the arteries that will cross the country and, implicitly, the areas with the biggest problems. After that, the locations must be established where the water accumulation basins will be formed from the precipitation, from the river courses and how this water will be dispersed.

However, the routes must be governed by efficiency, low energy consumption and controlled dispersion of water so as not to waste it. Farmers must be engaged in this action, if it is going to take place, technicians and specialized firms must consult and train farmers to become the main actors in this action. Costs must be reimbursed and money must be spent sparingly.

Water is expensive and will become extremely expensive. Today, in an effort to secure water prices, municipalities in some California cities as well as avocado farmers are hedging the price of water on the NYSE (New York Stock Exchange). Exactly as in the price securing model for farm goods that we promote and execute through AGRI Column and through the Romanian Farmers’ Club.

Without becoming cataclysmic, we argue that water will become extremely expensive and scarce, and will bring generations of misunderstandings and conflicts with it. By 2040-2045, the problems will be dramatically exacerbated and we will see what we are writing about today, namely WATER listed on the stock exchange, WATER the cause of misunderstandings and conflicts.

However, I would dare to project an image of a Romania that in three years, could have a competitive irrigation system, a Romania that can generate, thanks to water and technology, a yield of 8.4-8.5 tons per hectare of wheat, and I ask, what do you think of the figure of 22,000,000 tons of corn? But for wheat, what do you think of a yield of 6.5 tons, which leads to 14,000,000 tons of wheat? And then, in the chain, sunflowers and rapeseed, followed by barley? A Romania that can produce 48,000,000 tons of goods?

It’s not utopia, it’s a reality that we can reach if we all work together, the farmers, the professional associations, the Ministry of Agriculture, the competent people in the technical field, the entire political class, who must effectively harness this national security project.

At the same time, it is necessary to develop the processing as well as the trade routes of the value-added products. Why? For the simple reason that we must believe in our global role, in our privileged position at the Black Sea, in the fact that we must have the courage to understand our mission and role as a source of sustainable and predictable food.

REGIONAL STATUS

The EUROPEAN UNION cuts corn production once again, down to 65.4 million tons. And I would call them optimistic. All of Europe, from the Iberian Peninsula to its eastern border, which is Romania, is nothing but rock milling by the hot and merciless sun, scorched by wildfires and heat deaths. We will not have 65.4 million tons of production at the European level, but at most 55 million tons. We will see soon. Maize is effectively lost in the Union and this is visible at the level of every member country. If we add Serbia to this production system, you’ll see how things scale up.

UKRAINE must be watched very carefully. They also have days without precipitation and very high temperatures. It will not rain exactly at the critical moments and the temperatures will also reach areas of 36-37 degrees Celsius on Ukrainian territory.

Weekly grain exports from Ukraine double, the share to Romania increases to 47%. Ukraine’s weekly grain exports more than doubled from the week of July 21 to 695,203 tons, bringing total exports for the start of the 2022-2023 season to 1 million tons, with more than 47% of Ukrainian grain going to Romania, government data shows.

As of July 1, 2022, corn exports amounted to 707,826 tons, with over 47% or 334,745 tons of corn exported to Romania and 17% or 120,202 tons to Poland, while the share exported to Hungary decreased to 9% or 43.45 tons.

RUSSIA, as we well know, has already degraded by 1 million tons, up to 14.5 million tons, and things may continue to degrade the corn crop.

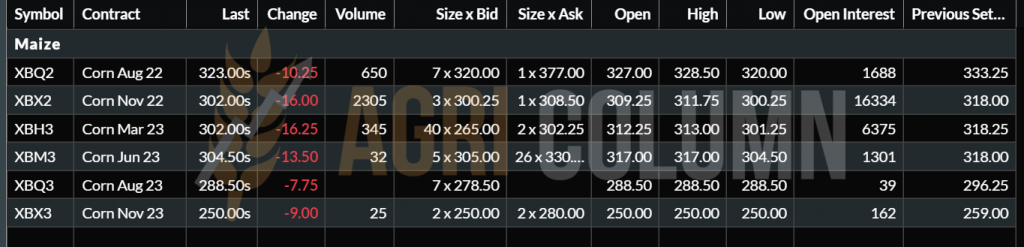

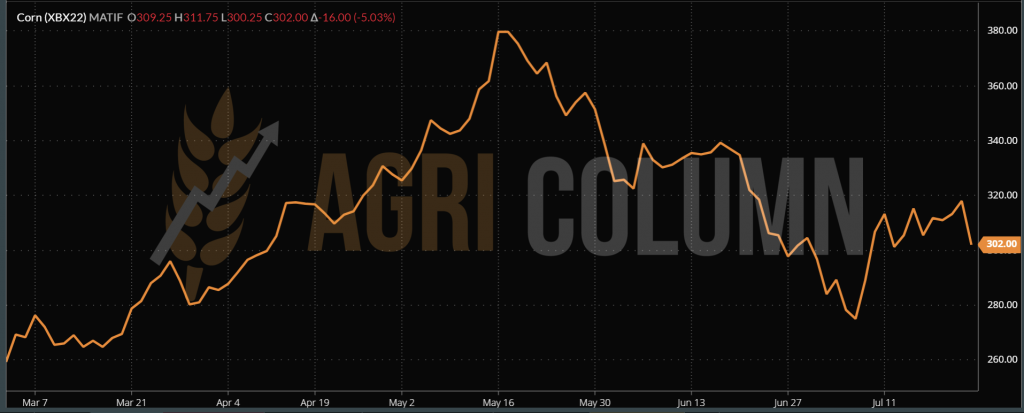

EURONEXT XBX22 NOV22 – 302 EUR (minus 16 EUR)

EURONEXT CORN TREND CHART – XBX22 NOV22

GLOBAL STATUS

The US is entering a spiral of controversy. On the one hand, we have the precipitation forecasts that overlap with the heat waves crossing the USA and where temperatures of 37-38 degrees Celsius are recorded. On top of the above comes a picture provided by a North American consulting firm that indicates a drop in yield from 177 bu/acre to 171.4 bu/acre. If this is true, it will decrease US production by 11 million tons, from 373 million tons to 361 million tons. The yield per hectare could decrease from 11.1 tons/ha to 10.74 tons/ha. Let’s not forget that August is coming, the month that generates the biggest problems for American corn.

SOUTH AMERICA is unchanged as Safrinha nears the end of harvest and total Brazilian production remains set at 116m tons. Next season is represented only by numbers and that’s about it for now in Brazil and Argentina.

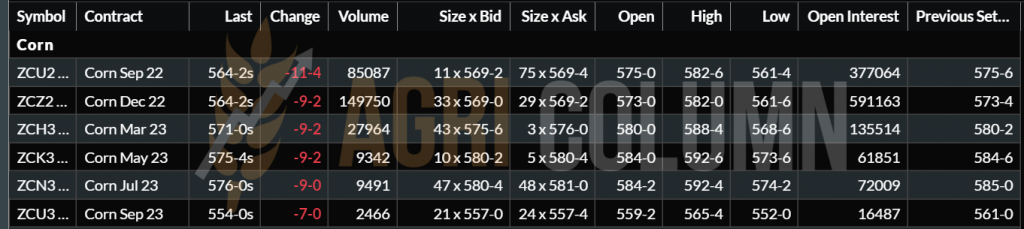

CBOT ZCZ22 DEC22 – 564 c/bu (minus 9 c/bu = 3.55 USD)

CBOT CORN TREND CHART – ZCZ22 DEC22

CAUSES AND EFFECTS

EUROPE is suffering terribly from the drought and a minus of 24-25 million tons from the initial forecast will weigh extremely heavily on the global corn balance.

The AMERICAS are still at potential levels in terms of production, and the weather factor will play the first role in this scene. Weather will dictate final volumes and drive corn prices globally.

UKRAINE, in the light of the latest events, could relax the markets, but here we have two fundamental markers, namely:

- the permissiveness of Russia in complying with the agreement and it is seen that it has no intention and interest to do so, after the action of sending a missile to the port of Odessa;

- the weather in Ukraine, which must be kept under constant observation.

CHINA will be a price support factor. It will look for origins in the Black Sea basin, due to the logistical effect – lower costs compared to North and South American origins. We know China’s insatiable appetite and foresee its appearance in the Black Sea basin.

The relaxation that the stock markets indicate is extremely volatile. We will see another rally due to that Russian missile. Uncertainty whets the appetite of speculators through trading algorithms.

The EUROPEAN CENTRAL BANK has raised interest rates by 0.5% and we are only two days away from the FED announcement which could push prices down due to the effect of the 0.75% interest rate hike.

CORN INDICATIONS IN MAIN ORIGINS (old crop)

LOCAL STATUS

Local indications extend to fairly large ranges. Starting from the prices offered by processors showing a minus compared to the EURONEXT indication of 30-35 EUR/MT, up to the EURONEXT indication plus 5 EUR/MT in the case of the Port of Constanța.

But we sense the subtle nuance created specifically to generate confusion. We are referring to the fact that some buyers are still referring to the XRQ22 AUG22 when in fact they should be referring to the XRX22 NOV22.

The XRQ22 AUG22 indication is expired and consumed. Therefore, it indicates a lower level than XRX22 NOV22. In this case, please do not accept correlation with AUG22, but with NOV22, in case of sales.

CAUSES AND EFFECTS

Processing units are covered for the first contract volumes to be processed in relation to buyers of rapeseed oil for biodiesel. Soon they will be processing sunflower seeds and canola will no longer be processed.

The resumption of the process will take place in November 2022 and, for this reason, we see the lack of interest expressed in the price of the processors.

But there are dark clouds on the horizon again, namely the sowing campaign 2022. How will the farmers sow in the actual rock called soil on the territory of Romania? How long will the seeding window be extended? When will the rains come? Because in August, they certainly won’t come, at least that’s what the forecasts look like.

EURONEXT XRX22 NOV22 – 637.5 EUR (plus 7.5 EUR)

RAPESEED EURONEXT TREND CHART – XRX22 NOV22

REGIONAL + GLOBAL STATUS

The EUROPEAN UNION is currently covered and the level of 17.9 million tons is maintained as the forecast volume.

CANADA is looking sensational to say the least and there is no doubt at the moment about the Canadian canola crop.

AUSTRALIA also has no doubts about the volumes.

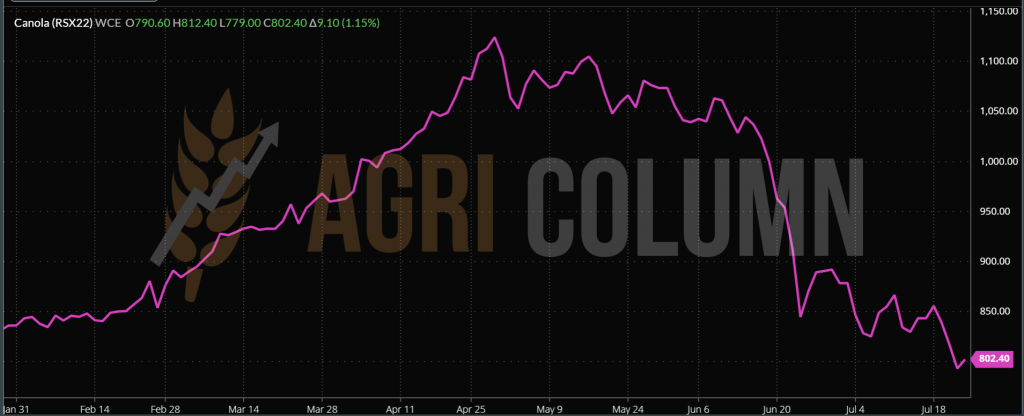

ICE CANOLA RSX22 NOV22 – 802.4 CAD (plus 9.1 CAD)

CANOLA TREND CHART CANADA – RSX22 NOV22

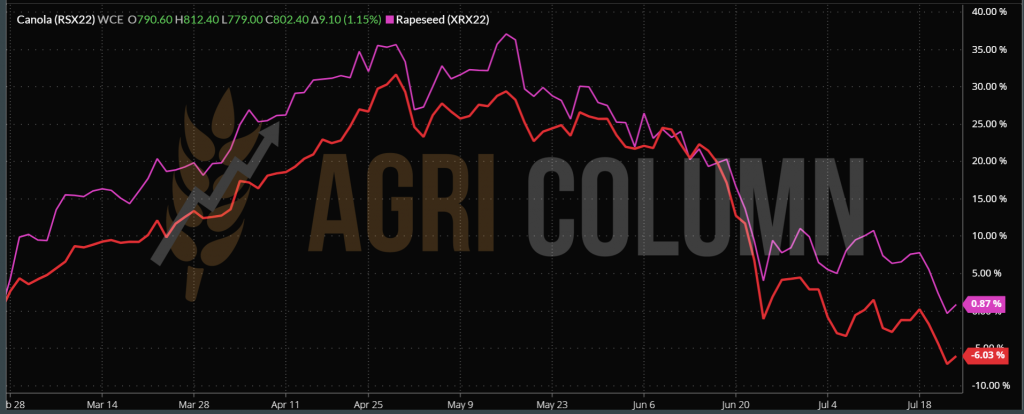

ICE CANOLA TREND GRAPH ASSOCIATED WITH EURONEXT RAPESEED

CAUSES AND EFFECTS

We see a devaluation of palm oil, which has fallen to the level of 3,700-3,800 MYR (Malaysian Ringgits), after a long period of resistance at levels above 5,000 MYR.

The supply of European units with goods until October degrades Euronext indications.

The prospect of very good crops in Canada and Australia lowers rapeseed on Euronext.

The oil goes down and therefore keeps the rapeseed low. Effectively, we are trading like before the war.

November, associated with seeding difficulties in Europe, could bring more consistency to Euronext indications.

The plus in the last session is technically associated with the need for hedge funds for AUG22.

LOCAL STATUS

The local market is still correlating new crop pressure and showing indications as follows: port in CPT is indicating 540-560 USD/MT, while processors are indicating 520-530 USD/MT in factories DAP parity.

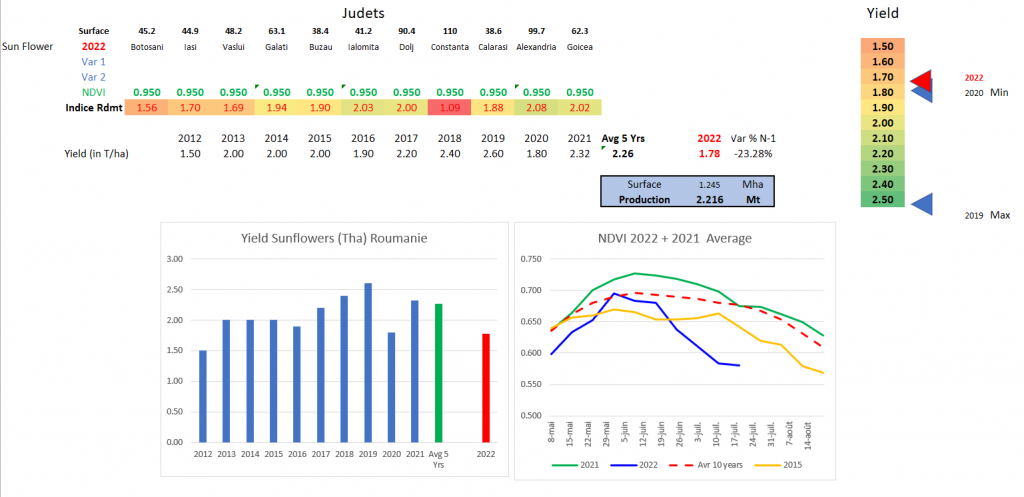

But the problems are quite serious regarding the sunflower crop. We hit the road full of excitement, fueled by the upside potential due to the disappearance of Ukraine’s crude oil flow. Farmers planted much larger areas of sunflower with this hope. The area increased to 1.35 million hectares. Everything looked very good. But the drought destroyed hopes of a bumper crop estimated at 3.6-3.65 million tons. Calatidium shrunk in the absence of soil water and rainfall to the size of a daisy. In many areas of the country, the sunflower did not even develop. It remained at knee level, effectively stunted, due to the heat and lack of water.

Combined with soil drought and extreme heat, we will reduce harvest volume levels to around 2.4 million tons, with an even lower near-term potential of just 2.2 million tons. We will find ourselves in the 2020 scenario, for sure. But now we will have, in addition to the specter of a reduced volume of crop, the proximity of a war that will make volumes of raw material from Ukraine make their way through Romania, at discounted prices, which will put additional pressure on its price.

Also from the same source, @VisioCrop, we will insert the production graph related to Romania, with the clear mention that things can and will degrade further, perhaps below the level of 2.2 million tons.

REGIONAL STATUS

The EUROPEAN UNION is cutting production volume from the initial 10.9 million tons to 10.2 million tons. We suspect that this correction is only coming from Romania at the moment. But the Union is suffering in the same way, and we predict that France, Spain, Hungary and other countries will significantly reduce volume in the coming month.

UKRAINE shows signs of weakness. The forecast of 9.5 million tons is slowly turning into 8.5-8.7 million tons, at least for now. Let’s not forget that they are also going through a period of excessive heat and very little to no precipitation.

CAUSES AND EFFECTS

The harvest volume pressure that generated the steep price declines granted with the Ukrainian discounts remains in place. Added to these two factors is the price level at which oil from Ukraine is offered and the price level makes it possible for it to be used in the domestic processing units of Romania and Bulgaria. Thus, crude oil is quoted at 1,100 USD/MT FAS Izmail and 1,220 USD/MT CIF Ruse, Bulgaria.

For Europe, we find the following price indications:

- 1,250-1,270 USD/MT for Ukrainian crude oil delivered at CIF Mersin parity, August.

- High oleic oil has an indication of 1,550-1,700 EUR/MT DAP Germany, Belgium, The Netherlands, Spain, August-September delivery.

- Crude linoleic oil is offered at 1,450 EUR/MT in the same European destinations.

According to these quotations, we understand a price difference between HOSO and LINOLEIC of 100-250 EUR/MT and we believe that still in Romania, the bonus level for the HIGH OLEIC raw material is not granted according to the HoReCa demand in Europe. In Romania, a maximum of 40 USD/MT is currently in practice.

However, with the signing of the Transport Initiative and the release of export routes for Ukrainian goods, despite the Russian challenges, we will witness a process being reversed. So far, about 15-20% of processing units have resumed operations in Ukraine, after all halted processing in March due to Russia’s large-scale invasion, said Ukroliyaprom Association General Director Stepan Kapshuk, on July 15.

Before Russia’s large-scale invasion of Ukraine, factories processed about 50-70 thousand tons of sunflower seeds per day. Now those factories, which have resumed their activity, can process only 10-15 thousand tons of oilseeds.

Currently, another 20 factories are ready for launch, but are not put into operation because it is impossible to sell their final products.

As an effect of the above cause, Ukraine will reduce its export of raw material, instead generating crude oil, which will be shipped via Chornomorsk, if this agreement to extract Ukrainian goods will work. And in this way, the price of the Romanian raw material will know an upgrade.

The price increase will not only come from the slowdown of the Ukrainian flow, but also because of the reduced volume that everyone will want to access – processors for the domestic market, and exporters for the European intra-community market, knowing that Romania is a basin of origin. Competition between the domestic and intra-Community markets will generate the return of a higher level of sunflower seeds, all associated with a lower crop in the European Union.

CSFO AND OILSEEDS INDICATIONS IN MAIN ORIGINS

LOCAL STATUS

Processors’ indications for new crop soybeans remains at 560 USD/MT DAP Factory. Certainly, there is interest and a higher price from other traders, but processing facilities have the advantage of providing the necessary certification to access coupled support for soybeans.

REGIONAL + GLOBAL STATUS

The US sees itself in the same conditions as last week: a forecast level of 123 million tons and a vegetation stage on average for recent years. The previous week’s sales are up on the same period last year, with a total volume of 0.204 million tons for the 2021-2022 crop and a volume of 0.255 million tons for the 2022-2023 season.

BRAZIL begins its usual marketing program and we see a future crop upgrade that looks huge, from 149 million tons to 156 million tons, a jump of 7 million tons of soybeans, which is extremely much and pushes soybean prices down on the CBOT.

ARGENTINA is currently experiencing no changes to its future soybean crop. 51 million tons is still the indicated figure.

CHINA indicates cumulative US and BRAZIL purchases of 8.25 million tons, down 23% year-on-year. This quantity is divided as follows: 7.24 million tons origin BRAZIL (10.48 million tons June 2021) and 0.773 million tons origin USA (0.55 million tons June 2021).

For January-June 2022, China indicates purchases of 27.71 million tons (26.13 million tons last season) from Brazil and 17.54 million tons (21.57 million tons last season) from the US, via Karen Brown.

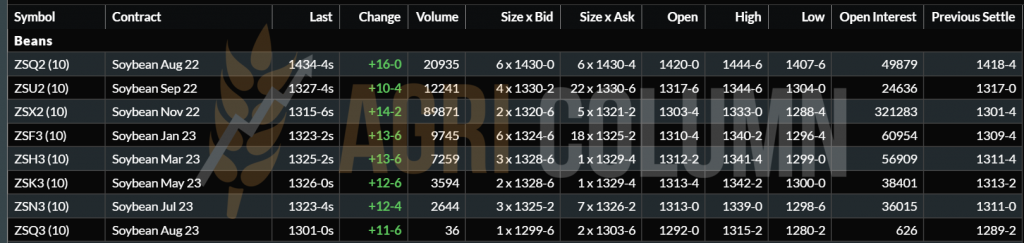

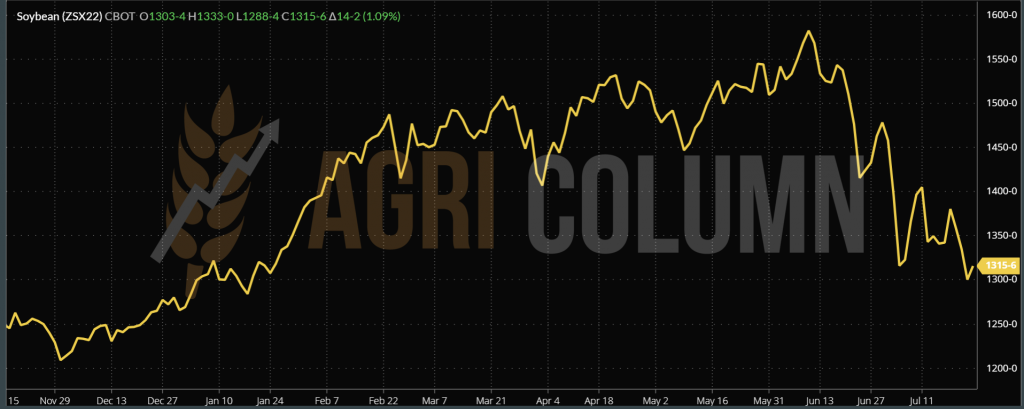

CBOT ZSX22 NOV22 – 1,315 c/bu (plus 14 c/bu = $5.9)

CHART – ZSX22 NOV22

CAUSES AND EFFECTS

The indication of China’s reduced use and, by implication, imports, is pushing soybean prices lower across the CBOT.

The indications of positive volumes, we can say untouched so far from Brazil, historically speaking, put the same pressure on the price, through the lens of the rich offer, associating in the commercial set the USA with the 123 million tons and Argentina with the 51 million tons.

For soybean sellers in Romania, a return of the price to last year’s levels is excluded at this time. The volumes in the two Americas are making buyers extremely relaxed at the moment. Only the weather factor will judge whether or not it is appropriate to intervene in the construction of the price in the future.

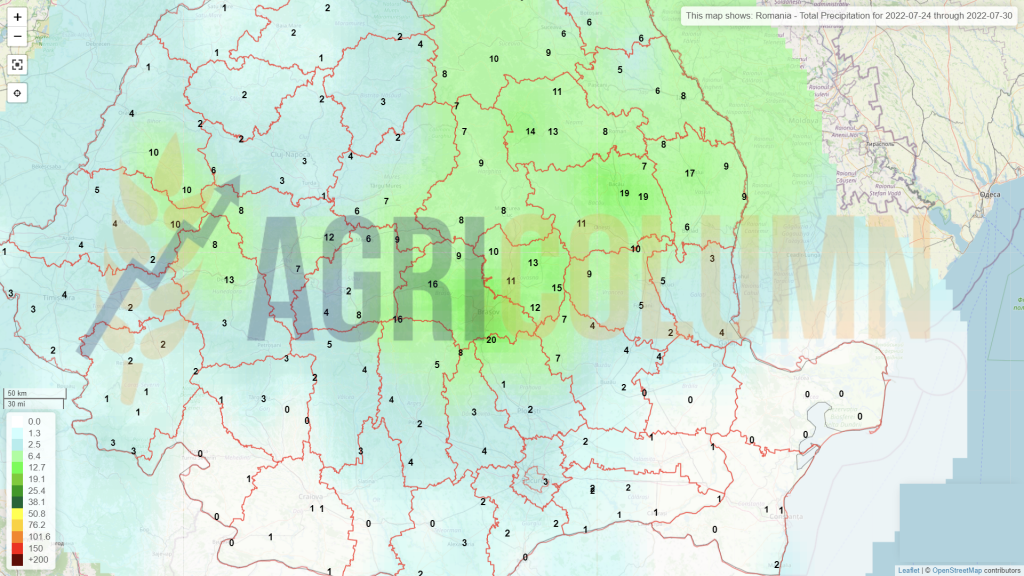

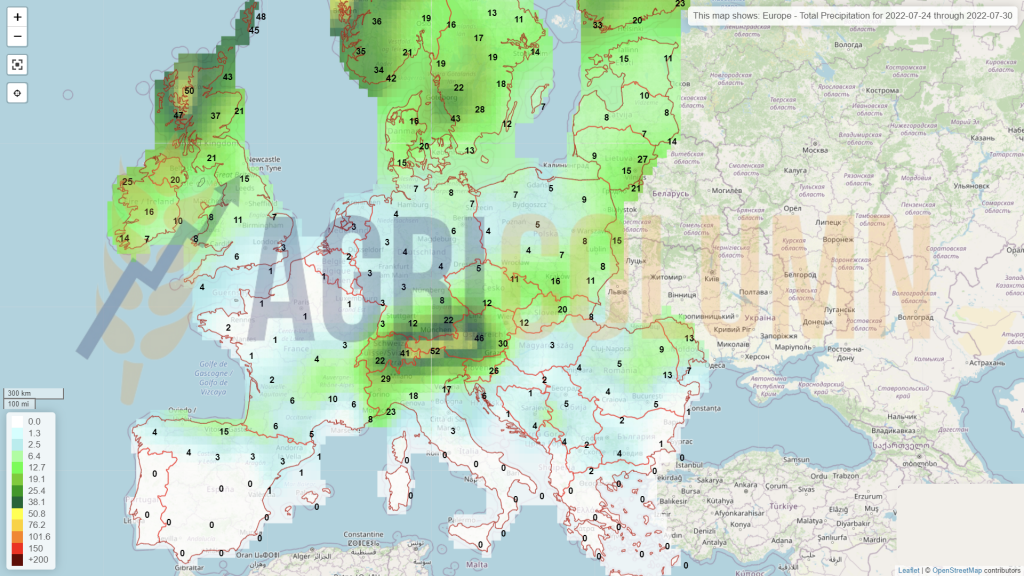

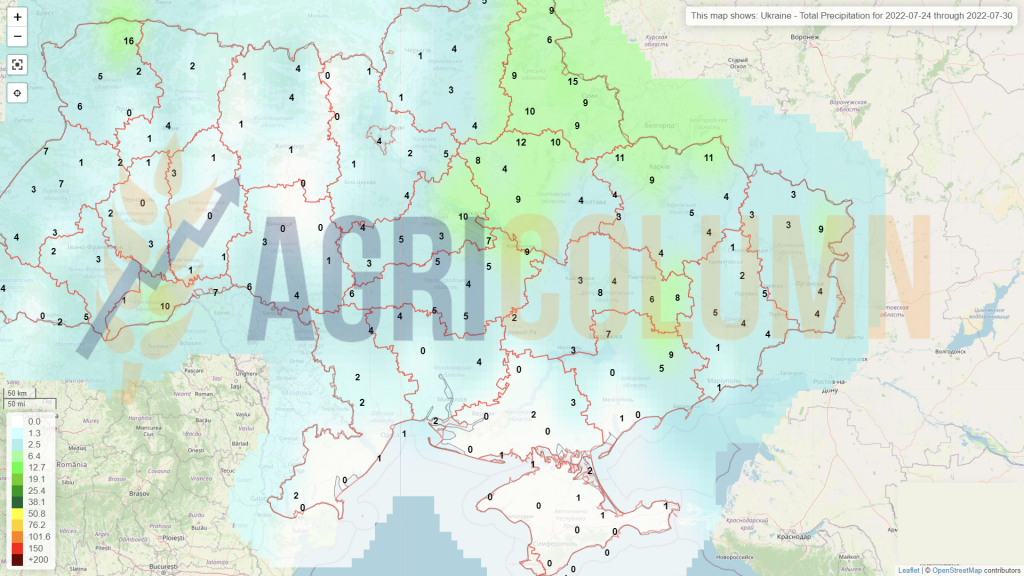

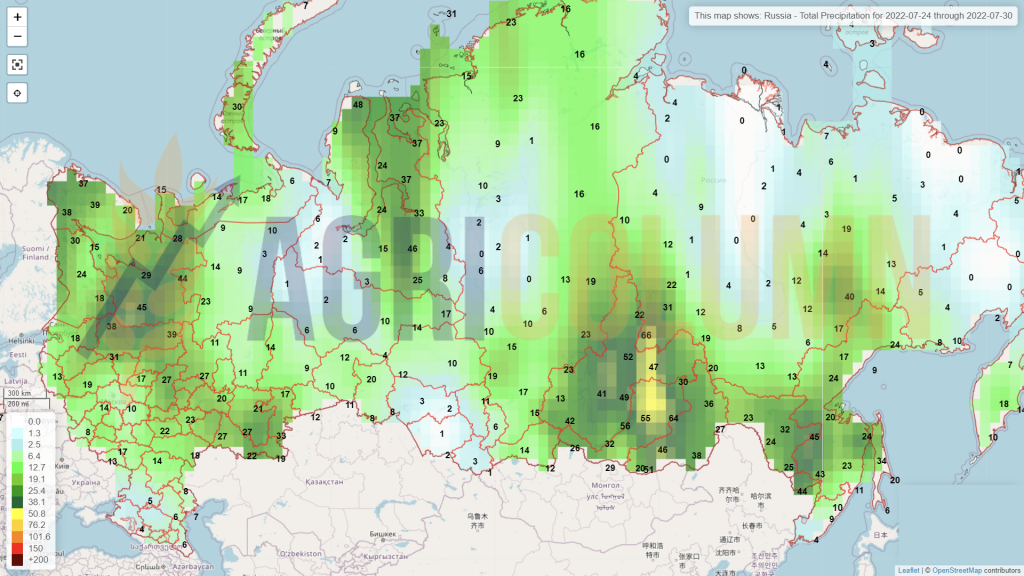

24-30 July 2022

Romania

Europe

Ukraine

Russia

Canada

USA

Brazil

Argentina

China

Australia