Romanian Agri Trade Summit, one of the largest events addressed to International Agribusiness, will take place on February 22, 2023 in Bucharest.

The initiative aims to reconfirm Romania’s strategic role in global agribusiness and to bring together the most important players in the dynamic grain market – top Farmers, Traders, Processors and Distributors.

This week’s market report provides information on:

LOCAL STATUS

The indications of the Port of Constanța revolve around the values of 285 EUR/MT, with a discount of at least 20 EUR/MT for the lower quality of feed.

New crop quotations remain at the same parameters, i.e., MLU23 SEP23 minus 30 euros. Putting the numbers together, we arrive at a level of 245 EUR/MT.

CAUSES AND EFFECTS

As we anticipated, there has been and is currently no fundamental that could generate traction in the price of wheat. Its price potential is effectively limitless at this point. Stocks are high in the country and reluctance to sell is also high. These stocks of goods have a particularly high financial burden. Financing them still costs money today. The level of interest is aligned with that of inflation and impacts the price of goods. But the value of stocks is falling, and if in July 2021, the level of estimate for guarantees was high, today it is dramatically lower.

In other words, this deadlock solves absolutely nothing. Interest is piling up, the price is degrading, and the payment terms are approaching. Moreover, the season of spring work and sowing of crops will soon come. Then new costs will encumber farm balance sheets and negatively balance debt versus potential income.

It should also be noted that the autumn crops were sown at very high costs, generated by the inflationary level and the effects of the regional crisis. This means another problem at the farm level, one that can potentially be solved by higher productivity so that the cost difference is covered.

The rains arrived exactly as we predicted and abundantly watered a large part of Romania. 30-50 liters is a significant amount, especially since the outside temperature was positive and the earth was able to quietly drain the beneficial rain.

In short, as a general conclusion, the wheat must find its way as quickly as possible. Romania is lagging behind in terms of export level. On December 31, 2022, we had 2 million tons exported, compared to 4 million a year ago, on the same date.

REGIONAL STATUS

RUSSIA is in the same situation. It sells all forms of wheat, and their expectations from the WASDE report, generated by the USDA on January 12, 2023, was to consider another increase of about 10 million tons, that is, from 91 million tons in December 2022, to 101 million tons in January 2023. But no one can be fooled. We know misinformation is rampant, but we remain rational. By raising the harvest volume, Russia wants nothing more than to generate dependence on destinations. By generating dependency, you create the conditions to dictate the market. Their problem is that the whole world knows that Russia robbed Ukraine of about 8-10 million tons of wheat.

UKRAINE is no different from a week ago, apart from the fact that WASDE generated an update on the wheat crop of 0.5 million tons. Ukraine increases production in 2022 from 20.5 million to 21 million tons.

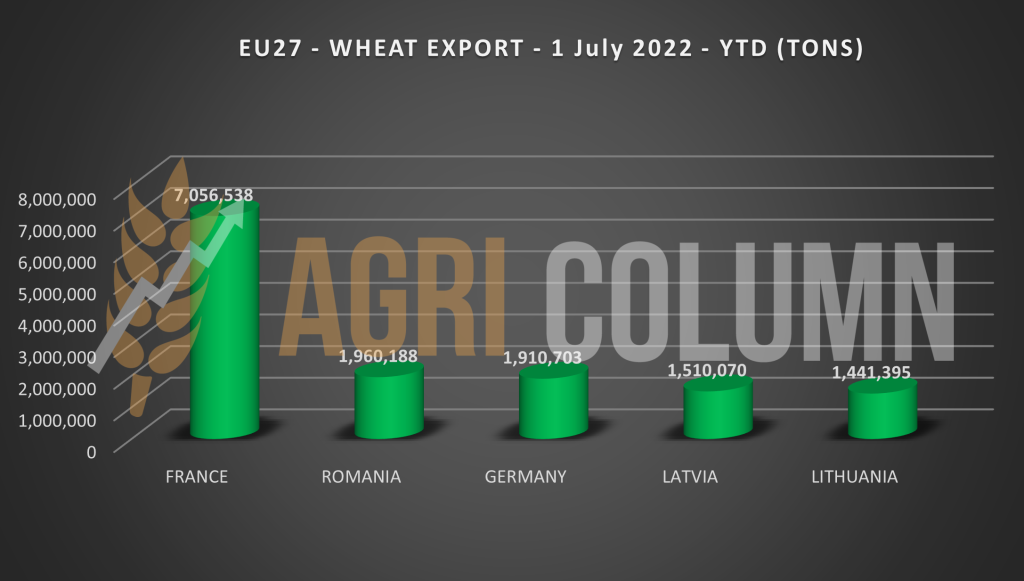

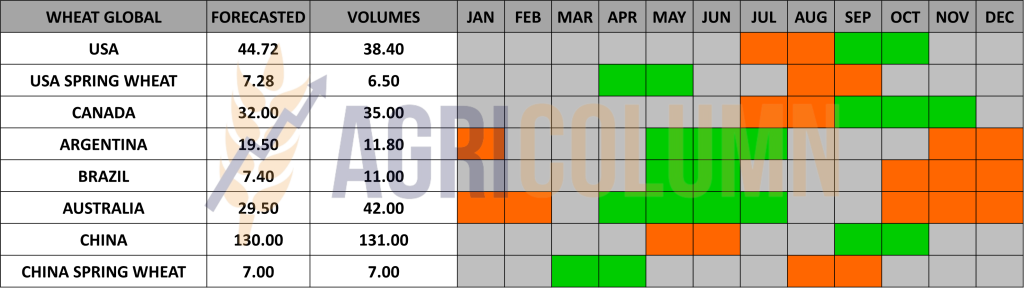

The EUROPEAN UNION is updated, in turn, with 0.4 million tons of wheat through re-evaluation. The export level is set at 17 million tons at the moment. In the chart below, we have the ranking of exporters and see how France breaks the 7-million-ton threshold, and then the distance to second place is extraordinarily wide at 5 million tons.

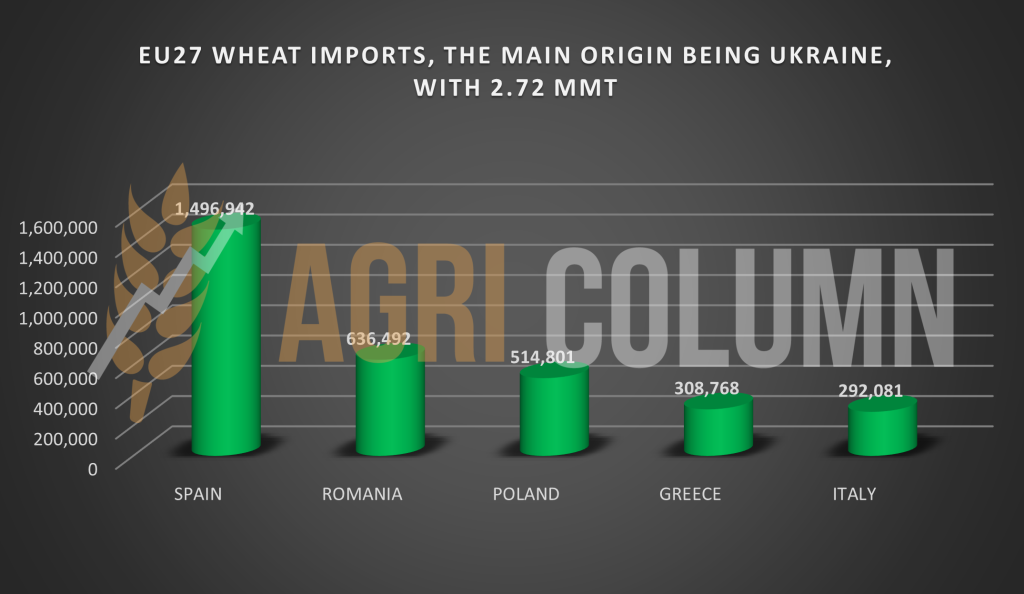

This is a good time to generate visual information, and we will do so in what follows. We have in the graph below the main beneficiaries of wheat imports from Ukraine:

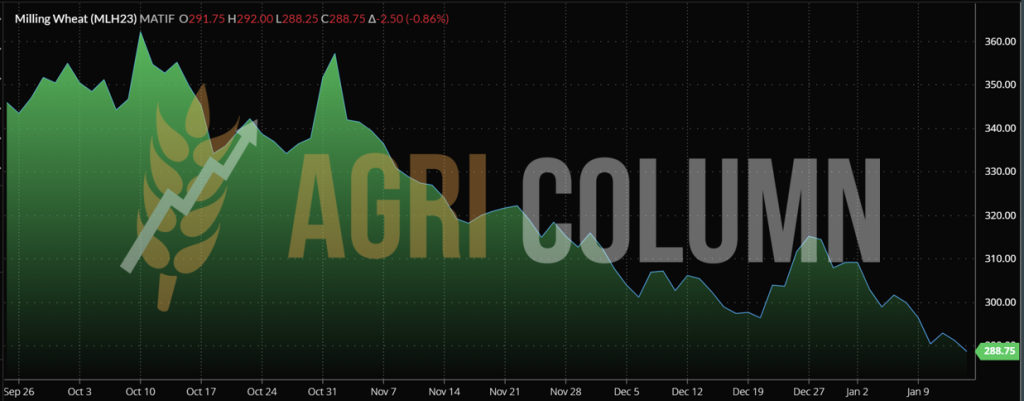

EURONEXT – MLH23 MAR23 –288.75 EUR

EURONEXT WHEAT TREND CHART – MLH23 MAR23

GLOBAL STATUS

U.S. is in the same position for the fall seeded wheat crop – mixed conditions and essentially no change from last week. In contrast, the obvious lack of competitiveness of American wheat is noted. The level of American exports is below expectations. To make the picture complete, American farmers (a part of them, of course) borrow the behavior of those in Eastern Europe, in this case, they do not sell wheat, they sit and wait on stocks. The disappointment of the price drops also touched the most mature, so to speak, farmers. The relaxation of the summer and the fact that the price level was extremely high caused the American farmers to follow, for the most part, the same route. It was apparent that US wheat was effectively “artificially inflated” by the Black Sea headlines, and the effect is clearly visible now that the lack of competitiveness is causing the CBOT to literally bleed wheat quotes.

ARGENTINA is a closed chapter on wheat. Out of season, we might say. From now on, Argentina is looking towards March, when summer normally ends in the Southern Hemisphere, and the subsequent La Nina season, with its disastrous effects on Argentine crops.

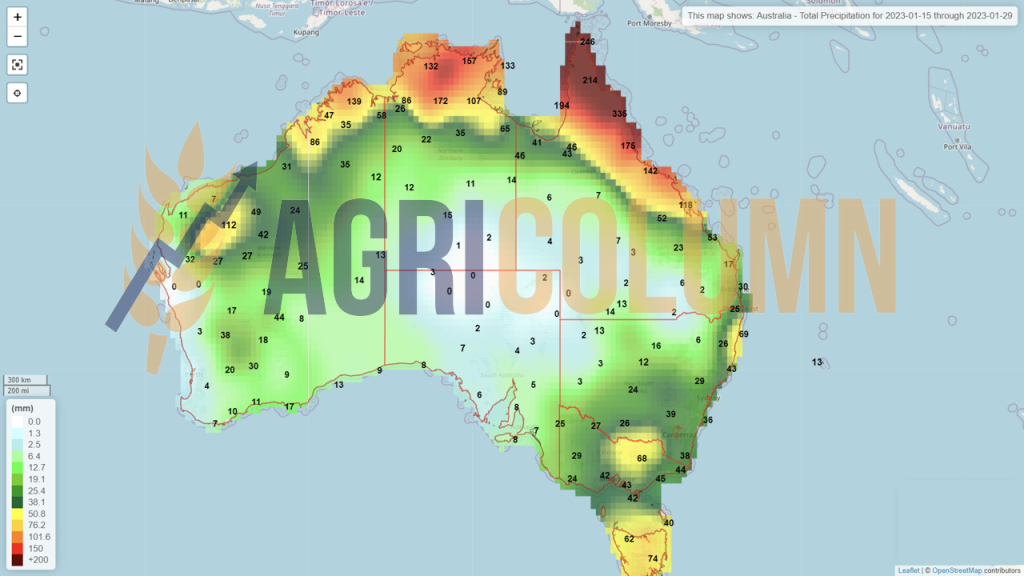

AUSTRALIA is not recognized by WASDE in its report. It’s hilarious not to recognize an overharvest at Antipodes. WASDE puts Australia at 36.6 million tons, compared with 42 million, according to local analysts.

INDIA is also under the radar after wheat production is expected to hit a record next harvest as record high prices and favorable weather conditions prompted farmers to expand planting areas of high-yielding varieties. Higher wheat production could encourage India to consider lifting a ban on exports of the staple and help ease concerns about persistently high food price inflation. India banned exports in May 2022 after a spike in temperatures cut production to 95 million tons, according to local analysts, or 100 million tons, according to the USDA.

CBOT WHEAT – ZWH23 MAR23 – 743 c/bu

CBOT WHEAT TREND CHART – ZWH23 MAR23

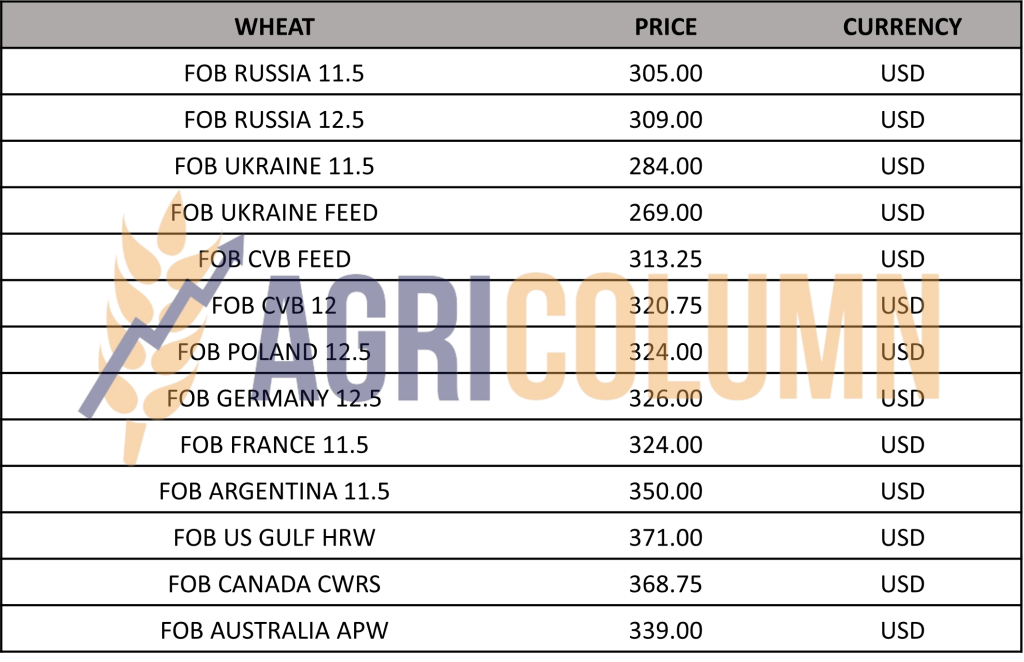

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

TENDERS AND TRANSACTIONS

GASC Egypt purchased 120,000 tons of wheat of Russian origin from ASTON. Egypt’s purchase price is 337 USD/MT at C&F parity. The payment will be made through the World Bank, so it is CAD (Cash Against Documents).

TMO Turkey. In the January 12 tender, Turkey’s TMO bought two lots of wheat, 220,000 tons and 225,000 tons, respectively, for two delivery periods: February 1-March 15 and March 1-31. For the first delivery period, prices on a C&F basis ranged from 323.2 USD/MT (Tekirdag) to 326 USD/MT (Iskender). On an EXW basis, prices ranged from 329.5 USD/MT (Izmir) (-14.5 USD/MT compared to November 29 purchase) to 331 USD/MT (Trabzon). For the second delivery period, prices on a C&F basis ranged from 324.2 USD/MT (Tekirdag) (-5.7 USD/MT compared to November 29 purchase) to 329.6 USD/MT Mersin (-6.3 USD/MT from November 29 purchase).

CAUSES AND EFFECTS

The WASDE report generated absolutely no hint or nuance of wheat price potential. WASDE effectively did nothing but time the information, just like it does every time. At the moment though, it has blocked two Origins, namely Russia and Australia.

Why do we say it blocked them? Mathematics never lies, and if we calculate Ukraine, which did not reach a crop of 33 million tons of wheat like last season, but only 21 million tons, it is obvious that that cargo is somewhere. 10-11 million tons cannot disappear into thin air. They cannot evaporate, no matter how much destruction the Russians are supposed to have done on Ukrainian territory. This volume was clearly transferred to Russia, and that is why Russia claims a production of 101-102 million tons, instead of the 91 million tons that is recognized by the USDA. So, we keep this block in mind and move on.

Australia is also not recognized in terms of harvest volume. 15% more than estimates are a respectable threshold, from 36.6 million tons to 42 million tons. But WASDE remains blind and deaf to these record production levels.

Why this blockage? Why does the USDA through the WASDE report practice this plan? Do they have a reason to do it? We think so. First, the USDA always provides the information gradually. Wheat being a social element, it does not want to distort or create very large price variations on the stock market or the physical one.

I mentioned earlier that US wheat has been overvalued since the summer of 2022. The headlines dominated and the fireworks were on CBOT and subsequently EURONEXT. Hedge funds connected in various origins, speculated on the war, generating extraordinary profit rates, with the help of cheap money at first, and then with the support of the FED, which increased the monetary policy interest from time to time, but clearly mentioned that it would let the funds go out at terms from positions. This is the first factor in “we want a soft landing”.

An acknowledgment of the 10-11 million tons “transferred” by Russia to its account from Ukraine, aggregated with the 6.4 million tons in the Australian surplus, would have effectively collapsed the price of wheat on the markets (futures and physical). Wheat would have engaged in the slide and corn, in turn, so the impact would have been large and with very important repercussions in the physical market. Why do we support this?

- High levels of wheat stocks in Origins, achieved with high production costs.

- Corn also made with high production costs, not to mention the uncertainty in Argentina.

A steep decline would bankrupt farmers in many parts of the world. High production costs are a drag on marketing, and a sharp drop would drive many of them out of business. Funds have the same problem; a sudden drop would lead to immeasurable losses and we know that funds work on borrowed money.

The effect of this USDA policy of disseminating information in small portions, aggregated with the effects of FED decisions are like cholesterol. It works silently in the arteries and veins, you don’t feel it, you don’t notice it, but when you do the consultation or have the heart attack, you realize the cause, you understand cholesterol and the fact that its effect is irreversible.

“WE WANT A SOFT LANDING.” JEROME POWELL, FED CHAIRMAN.

And something else. Aren’t you surprised that there is no tender for the new wheat crop? Last seasons, at this time, we already had sales to Jordan and Saudi Arabia. Now it’s quiet. Silence is not good, because, as I wrote above, the effect is irreversible. So, the default wheat price and market will drop significantly in the new crop.

LOCAL STATUS

The price indications of feed barley in the CPT Constanța parity are at the level of 250 EUR/MT.

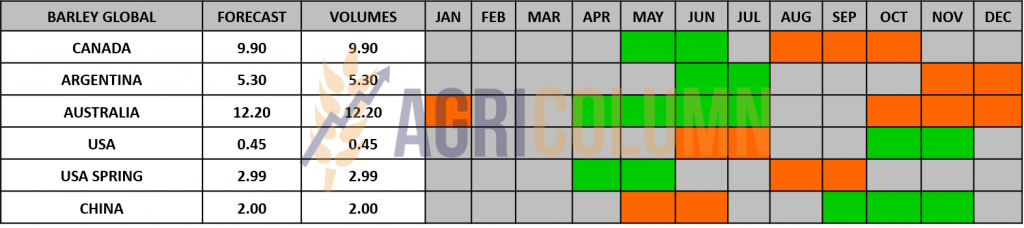

BARLEY PRICE INDICATIONS IN MAIN ORIGINS

GLOBAL STATUS

CAUSES AND EFFECTS

No news on the barley market at national or regional level. And this very thing, the silence, tells us that something is wrong. We remember too well that from December the international tenders for the new barley crop started. This year, however, there is silence, a silence into which I entered and discovered nothing. Why are no Destinations entering the New Crop tender?

Do you know the answer? For I have only one, namely:

The market will go down and the price will be much lower than what we see today.

LOCAL STATUS

Corn indications in the port of Constanța are at the level of 270 EUR/MT. We can clearly say that we are 10 EUR higher than before the holidays when 260 EUR/MT was the price level.

CAUSES AND EFFECTS

The South American origins are starting to show the problems we have been anticipating for a long time and a first tier has generated this price level. At the same time, we also note the decrease in the price difference between wheat and corn. Before the holidays, we had a spread of 40 EUR/MT, and today we note one of 15-17 EUR/MT. But the window will run out in a while, and we indicate a high of March 10-15, 2023. From there, another fundamental enters the market, and it will decide what happens next. But that giant sleeps for now, suffering from pandemic spikes. We recommend caution, as wheat could be a boulder around the neck of the corn price. In other words, don’t overextend the selling decision.

REGIONAL STATUS

UKRAINE does not see any changes between last week and today, at least none of substance, only that its export level will be updated by 3 million tons. Logically, it is what was harvested recently, and that corn will go to export.

RUSSIA brings no news to corn. 14 million tons.

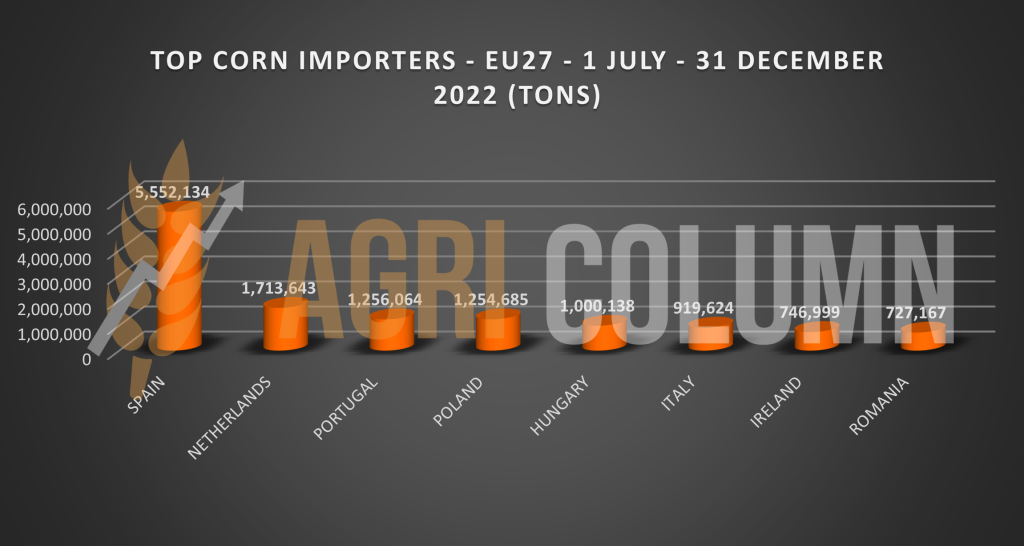

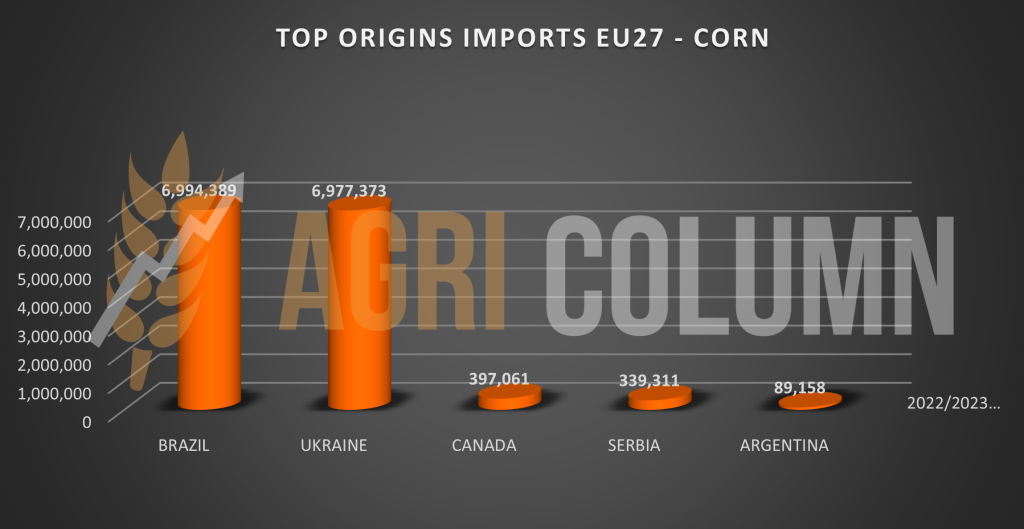

EUROPEAN UNION reached the level of 15.2 million tons in terms of corn imports. We insert the new values in the graph below and subsequently to this graph we will generate the top of the sources, i.e., from where and what quantities arrived in the European Union.

The graph above is interesting and illustrative.

EURONEXT CORN – XBH23 MAR23 –280 EUR

EURONEXT CORN TREND CHART – XBH23 MAR23

GLOBAL STATUS

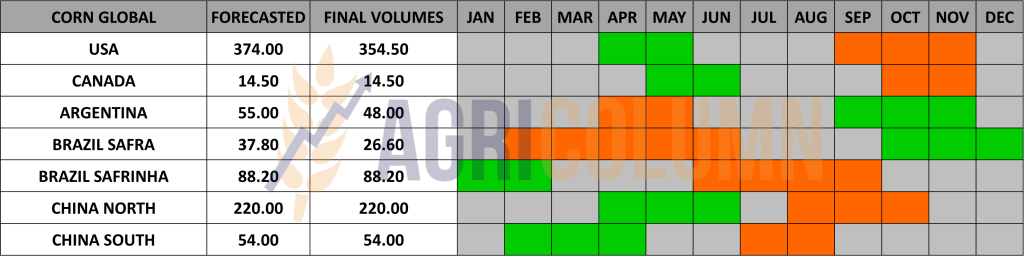

ARGENTINA was finally reflected in the WASDE figures, which generated a 3 mil. tons drop from 55 to 52 mil. tons. And we’re sure things won’t stop there. It’s just a stage drop, there will be more to come. Consolidation will be carried out at 42-43 million tons.

BRAZIL also takes a step back through WASDE and is reduced by 1 million tons, from 126 to 125 million tons.

The USA is degraded, in turn, but not by productivity, which is increasing, but by area. Thus, the USA decreases from 353.86 million tons to 348.75 million tons (a difference of 5.11 million tons).

CHINA comes and makes up for the North and South American drama with a surplus of 3.2 million tons, from 274, to 277.2 million tons.

CBOT CORN ZCH23 MAR23 – 654 c/bu (+1 c/bu)

CBOT CORN TREND CHART – ZCH23 MAR23

CORN PRICE INDICATIONS IN MAIN ORIGINS

CAUSES AND EFFECTS

Expectations related to WASDE, and the corn market are confirmed. They are routine declines, as everything is too visible in South America (Argentina). But it did not end there, the estimates went even lower than 3 million tons reaching 48 million tons, so another degradation of at least 4 million tons. Consolidation is seen at 42-43 million tons.

In the US, instead, the corn was given a “massage”. And knowing that Brazil is much more competitive than the US, so US sales are struggling, the USDA decided to decrease the acreage to increase the competitiveness of US corn. We have a minus of 5.11 million tons and a higher productivity, but a smaller area. Sounds like reconciliation to everyone.

In any case, corn received the support it deserved. The wait has begun to end and the focus in the next period is on two areas: South America and China, as one generates production and the other demand. And these two factors can influence the price of corn.

The problem remains with wheat, which could act as a brake on the price of corn. Feed wheat has a substitute role in feed and ethanol and the high volume of wheat can offset corn if its price is higher.

Two more amendments, one positive and one negative. The positive is that the difference between wheat and corn has narrowed a lot. Basically, the price of corn is somewhat equal to that of feed wheat. And the negative one is related to the EUR/USD parity, which reached 1.085, so the price in euros resulting from the conversion is reduced.

We see a trend towards a level of stability in the coming week. Amendments will be made only in the positive sense if there are any. Demand versus supply. South America versus China.

And a surprising fact, GASC EGYPT enters the tender for the purchase of corn, on January 19, 2023. The delivery parity will be C&F or CIF, as many suppliers have problems with insurance, but your payment will be CAD, that is, on delivery (cash against documents).

LOCAL STATUS

Rapeseed quotations in the port of Constanța are at the level of FEB23 minus 25 EUR/MT. This indication calculates a level of 550 EUR/MT. At the processing level, the quotations are FEB23 minus 35 EUR/MT, a fact due to the logistics cost (the difference between Constanța and the Processing Units).

The new crop is also prized. Primary guidance is AUG23 minus 30 EUR/MT. It is an initial indication that provides support in estimating farmers’ incomes.

CAUSES AND EFFECTS

At the moment, rapeseed is still under the influence of palm oil and fossil energy, and the trajectory is not a downward one at all, but it is influenced by the above. Demand will fuel future quotes and there is still time and room for growth compared to the pre-holiday period. Otherwise, our forecast is in agreement.

EURONEXT RAPESEED – XRK23 MAY23 – 570 EUR

EURONEXT RAPESEED TREND CHART – XRG23 FEB23

REGIONAL STATUS

No change compared to last week in the European outlook, nor in Ukraine and Russia for rapeseed. The state of vegetation is in the same normal regime for this period. The coverage request is executed at a normal rate, referring to the processing units.

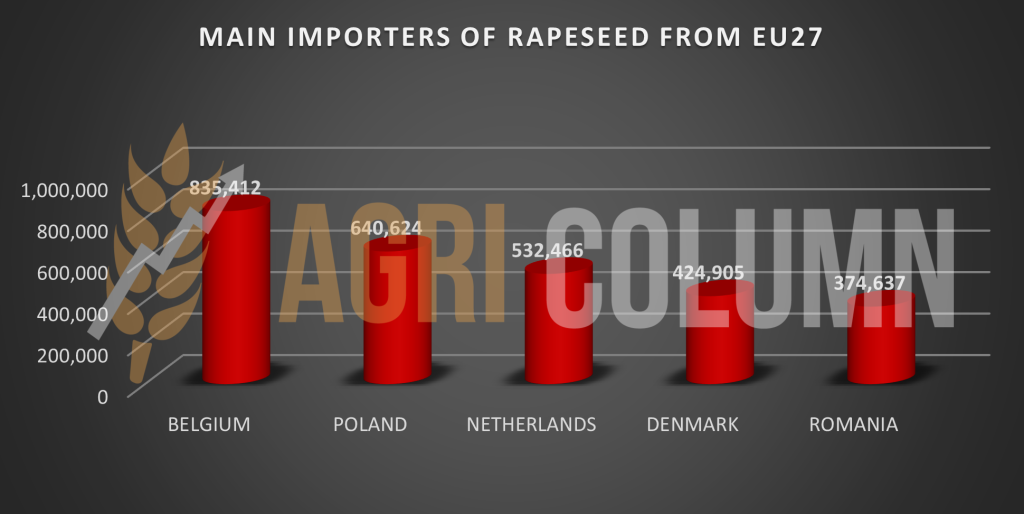

Regarding the old crop, we insert two graphs. The first emphasizes the importers of rapeseed originating in Ukraine and we see Romania with a level of 375,000 tons, in the fifth position. Romania is, as we know, a net exporter of rapeseed, under normal conditions.

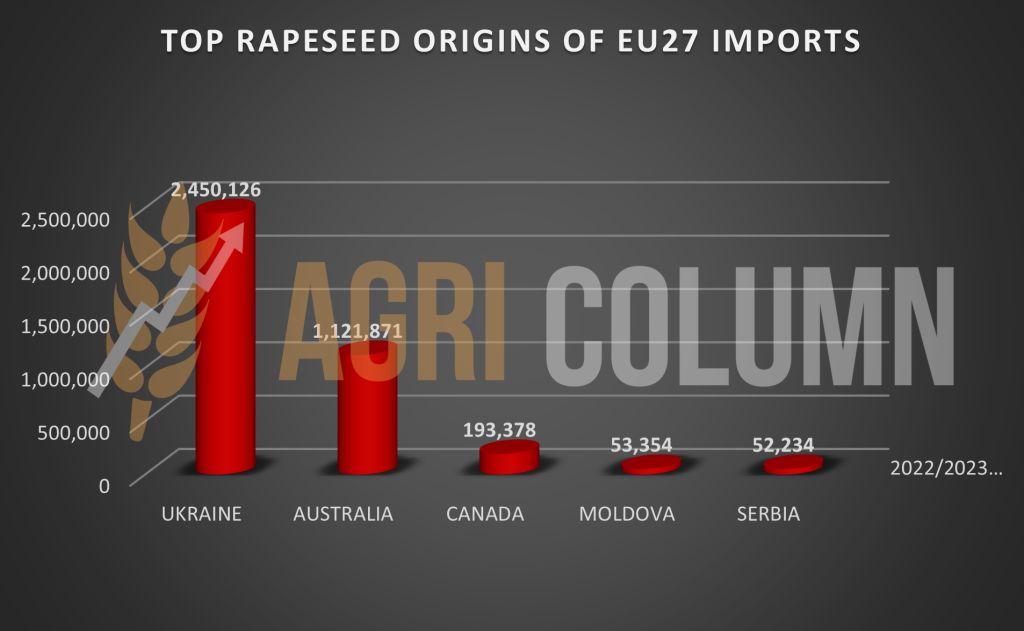

The second chart refers to ORIGINS and we can see where and what volumes the European Union imported from July 1 to December 31, 2022.

GLOBAL STATUS

CANADA, off season

AUSTRALIA, off season.

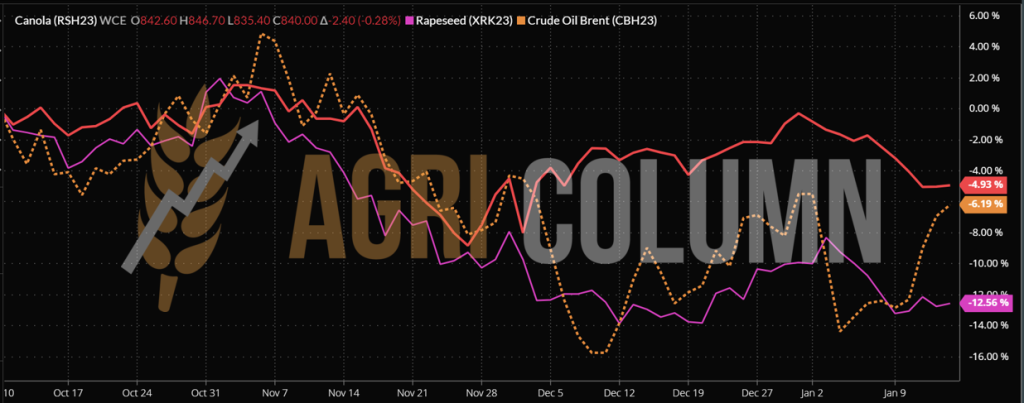

ICE CANOLA RSH23 MAR23 –840 CAD

ICE CANOLA TREND GRAPH – RSH23 MAR23

COMPARATIVE GRAPH. PETROL-RAPESEED-CANOLA CORRELATION

CAUSES AND EFFECTS

Trading sessions are crossed at these times by technical sequences. The transition from February indications to May indications for European rapeseed is done in italics, so the indication notes are altered by liquidations of positions and roll-overs by hedge funds.

The correlation in the physical market, however, remains as before linked to fossil energy and palm oil. The future traction factor must be soybeans, which, as we can see, are having problems caused by the weather in South America, more specifically Argentina and marginally Brazil.

LOCAL STATUS

The Port of Constanta raises its price indications regarding sunflower seeds. The trading basis is 560-565 USD/MT, but large lots may find a surplus in price.

High oleic sunflower seeds, HIGHOLEIC, are quoted at a base level of 580-585 USD/MT.

Processors are correlating and indicating a trading base of 555-560 USD/MT at DAP Processing Units parity.

CAUSES AND EFFECTS

What we were anticipating is starting to show in the indications, which is to raise the level by 25-30 USD/MT. And the route shows promise in the next period. Demand is steadily building, and both the EU and Romania point to a window that will maintain levels for a period that will last until around February 20-25, 2023. Our forecast is therefore warranted from this point of view.

REGIONAL STATUS

UKRAINE. Ukraine’s weekly sunflower exports rose more than fivefold to 46,445 tons in the week ending January 11, despite limited supply from Ukrainian sunflower sellers.

Romania received 40% or 21,916 tons of the volume of exports in January.

Since the start of the 2022/23 marketing year, 1.26 million tons of Ukrainian sunflower seeds have been exported, according to official data.

Weekly rapeseed exports more than doubled from the previous week to 31,726 tons, bringing total exports since the start of the season to 3.13 million tons.

Poland and Romania, with shares of 14,649 tons and 12,665 tons respectively, were the main buyers of Ukrainian rapeseed in January.

RUSSIA still sells sunflower oil without export tax and their advance is normal for this period.

The EU is in the off-season and demand for raw materials has started to show.

GLOBAL STATUS

ARGENTINA indicates nothing new in any sense in the period between the two reports.

PRICE INDICATIONS FOR OILSEEDS AND CSFO IN MAIN ORIGINS

CAUSES AND EFFECTS

Law 1866D in Ukraine will play an important role in the next period regarding the development of the price of sunflower seeds.

Thus, Ukraine issues Law 8166D regulating exports. In this way, the exporters are under the eyes of the authorities on two sides. One of them refers to the price level, which must be in line with the market and not undervalued as before. The second barrier is the one that generates control over revenues and targets the average exported volumes over the last 6 months.

How does the second control barrier manifest itself? For each exporter, the volume exported in the last 6 months will be taken into account and a monthly average will be made. If the average is exceeded in the following month, a fee (guarantee) of 14% of the value of the difference exceeding the monthly average will be applied. This guarantee should be returned (formally) when the payments for the exported goods credit the Ukrainian account of the exporter.

So, the effects will roll into a support of Romanian seed production, which could lead to other price levels for Romanian seeds.

LOCAL STATUS

In Romania, the price indications for soybeans are at the level of 540 USD/MT DAP processing units for non-GMO soybeans. Between July 1 and December 10, 2022, approximately 145,000 tons of soybeans were imported.

REGIONAL STATUS

EUROPEAN UNION. Imports of soybeans in EU countries in the first week of 2023 were 265,114 tons. Total soybean imports from July 1, 2022, increased to 5.8 million tons, 15.3% less than last year in the same period.

Weekly EU soybean meal imports were 218,412 tons, bringing total imports to 8.26 million tons, 4% lower than last year.

GLOBAL STATUS

USA. The US Department of Agriculture’s (USDA) weekly data on net sales fell slightly in the first week of the year. Reported net sales were 717,400 tons for the 2022/23 crop, slightly below last week’s 721,000 tons but between analysts’ expectations of 600,000 to 900,000 tons. China was the main destination with 676,600 tons reported, of which 52,000 were traded from Pakistan, followed by Germany (142,600 tons), Mexico (100,400 tons), Bangladesh (57,200 tons) and Spain (46,900 tons). At the same time, data for 2023/24 showed net sales of 66,000 tons, down from 151,000 tons last week.

The WASDE report (World Agricultural Supply and Demand Estimates) of the Department of Agriculture (USDA) in January surprised the market with reductions in US soybean ending stocks, production and exports. The country’s ending stocks for 2022/23 were set at 5.7 million tons, down 270,000 tons from the 6 million tons previously reported in the December report, due to lower supplies only partially offset by lower exports. US production figures fell to 116.38 million tons, down from estimates of 118.27 million tons published in December. US exports were cut to 54.16 million tons from 55.66 million tons, reflecting lower offers, reduced import demand from China and a higher export forecast for Brazil.

World soybean production was cut from 391.1 million tons in December to 388 million tons, while starting stocks rose 2.6 million tons from the previous report to 98.2 million tons, due to an upward revision to Brazil’s 2021/22 soybean crop. The agency also cut global soybean exports to 167.53 million tons from earlier estimates of 169.38 million tons.

BRAZIL. Brazil’s 2022/23 soybean planting has entered its final stage, with a completion rate of 98.9% of the projected 43.4-million-ton area, according to the country’s food agency, Conab.

In Mato Grosso, frequent rains restricted a significant part of the harvest, but also favored crop development. In Rio Grande do Sul, on the other hand, the poor distribution of rainfall prevents the completion of sowing and prevents the initial establishment of crops in many areas.

According to Conab, the soybean harvest is now estimated at 152.7 million tons, down from 153.5 million tons in December. The slight month-on-month drop is related to a reduction in expected yields as the effects of the drought in Rio Grande do Sul were considered.

Brazil’s soybean exports in 2023 were cut by Abiove by 1 million tons from its December forecast to 92 million tons. The forecast remains at a record high and is 16.6% higher than 2022 deliveries of 78.9 million tons.

ARGENTINA. Soybean production forecast for Argentina was cut to 41 million tons from the previous estimate of 48 million due to lower planted area, according to the Buenos Aires Grain Exchange (BAGE).

BAGE reduced the projected seeded area to 16.2 million hectares, 500,000 hectares less than previous estimates, due to lack of rainfall, high temperatures and the end of the sowing window in the central agricultural area.

The figure is higher than the 37 million tons estimated by the Rosario Stock Exchange (BCR), while the US Department of Agriculture’s (USDA) estimates of world supply and demand for agricultural products put the country’s production at 45.5 million tons.

Soybean planting in Argentina this week reached 89.1% of the expected area. According to BAGE, dry weather and high temperatures continue to hamper progress on soybean planting.

Crops rated good-excellent fell to 4%, while 56% of the area was rated poor, and areas rated good are now at 40%.

Argentine soybean farmers’ sales are down for both old and new crops, according to data from Argentina’s Ministry of Agriculture. New crop soybean sales fell to 33,400 tons, in line with the 2021/22 crop, which fell to 143,000 tons.

CHINA. China’s Agricultural Outlook Committee raised its soybean production forecast for the 2022/23 marketing year in its latest monthly update of China’s agricultural supply and demand estimates (Casde). Production estimates for 2022/23 have been raised to 20.29 million tons from 19.48 million tons previously, as a result of higher yields and expected planting area. China’s soybean planting area in 2022 is estimated at 10.24 million hectares, and estimates for soybean imports and consumption were unchanged from last month at 95.2 million tons and 112.87 million tons.

China’s soybean processing volumes in the first week of the new year fell slightly from the previous week by 0.5 percent to 1.99 million tons, data from the National Cereals and Oil Information Center (CNGOIC) showed. The level was slightly lower than expected, likely due to the New Year holiday period, with CNGOIC expecting processing volumes to reach 2.05 million tons this week.

China’s soybean processing volume has hovered around 2 million tons for seven consecutive weeks, with large import shipments contributing to a higher processing level.

Domestic stocks of soybean meal and soybean oil also rose amid higher processing levels, with soybean meal stocks rising to 590,000 tons.

Meanwhile, soybean oil stocks also rose for a third straight week, up 4.41% to 710,000 tons, up 7.57% from the previous month but 7.79% lower small compared to last year. CNGOIC stated that the accumulation of soybean oil stocks has started to accelerate as the festive New Year period approaches.

For the 2022/23 marketing year, CNGOIC has forecast soybean imports to reach 95 million tons, while domestic soybean production will reach 20.29 million tons. But the information leads to a higher level once the pandemic peaks are passed.

CBOT SOYA ZSH23 MAR23 – 1,492 c/ bu (+21 c/ bu = +7.7 USD)

SOY GRAPHIC TREND – ZSH23 MAR23

CAUSES AND EFFECTS

Soy is positioned in the element to watch in the next period. The problems of South America and Argentina, in particular, mean that this commodity can become a driving factor in the VegOil complex, with applicability in the biofuels industry, but also in animal husbandry. Soybean meal is the main feed item globally, and the trend shown by CBOT quotes points to demand as well as fear for Argentine volume.

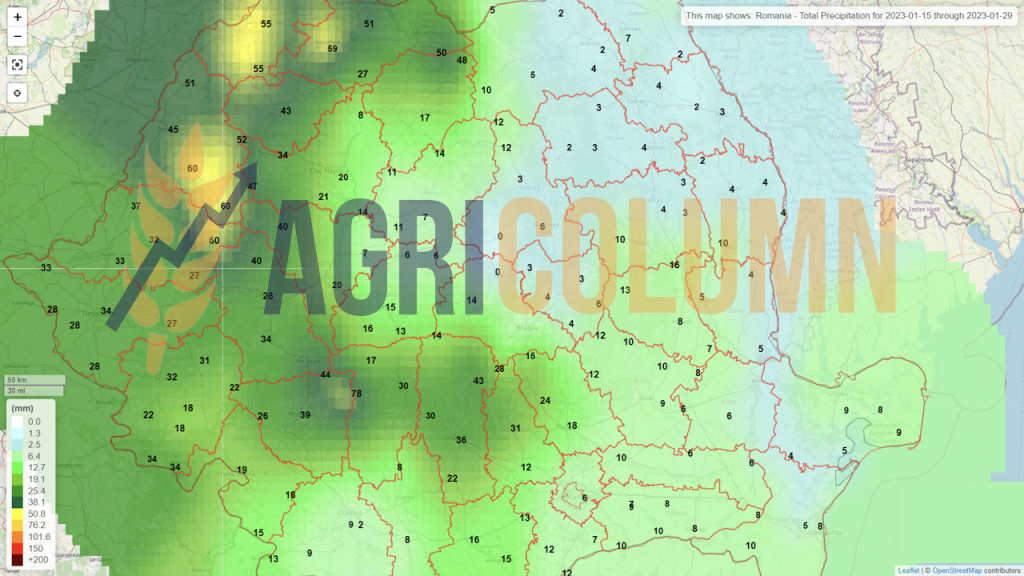

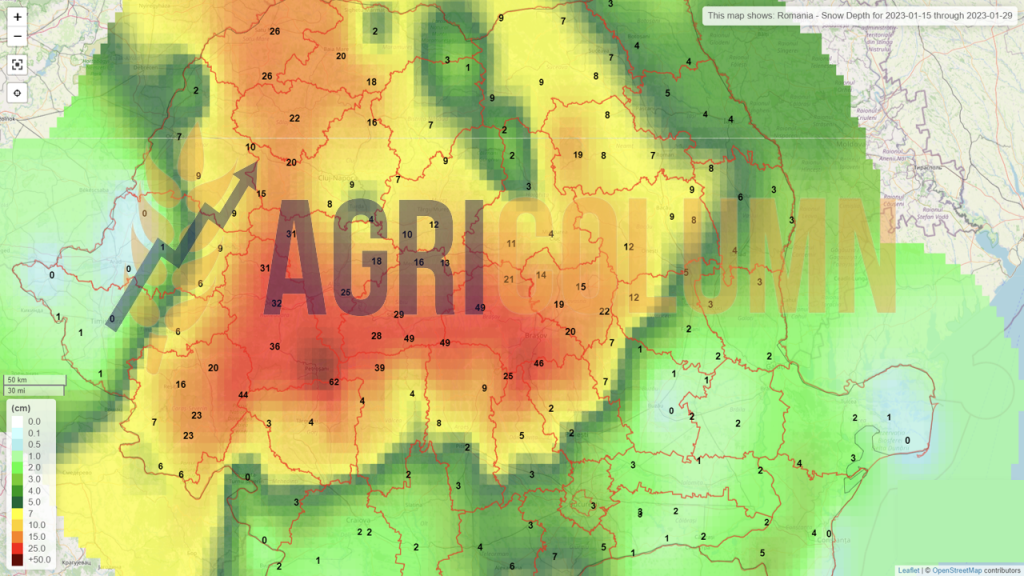

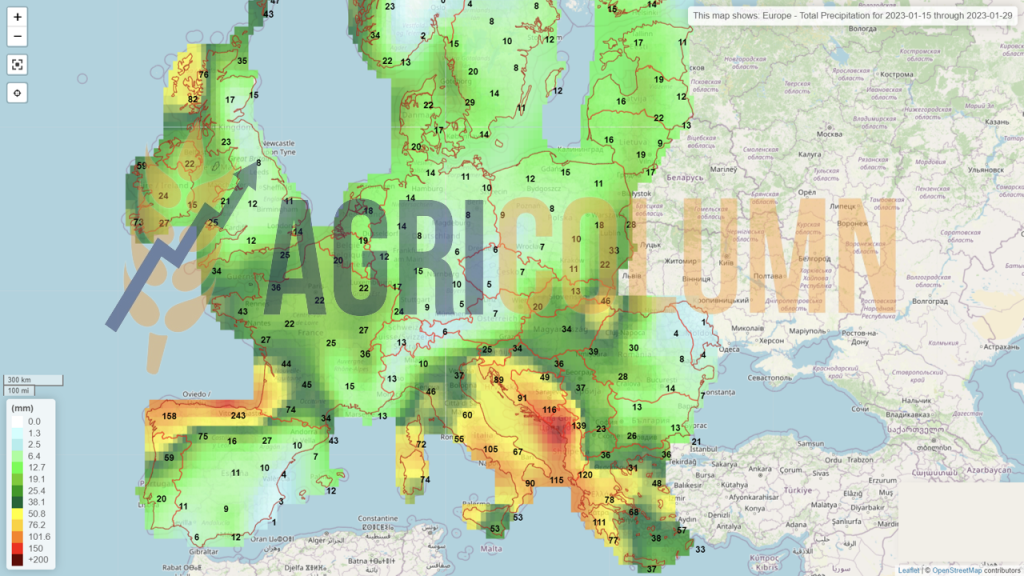

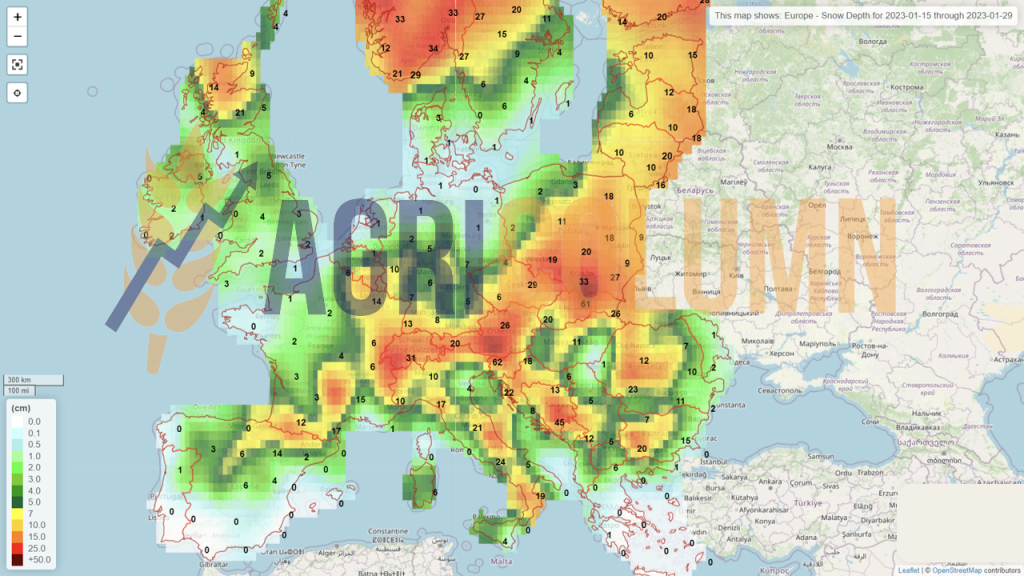

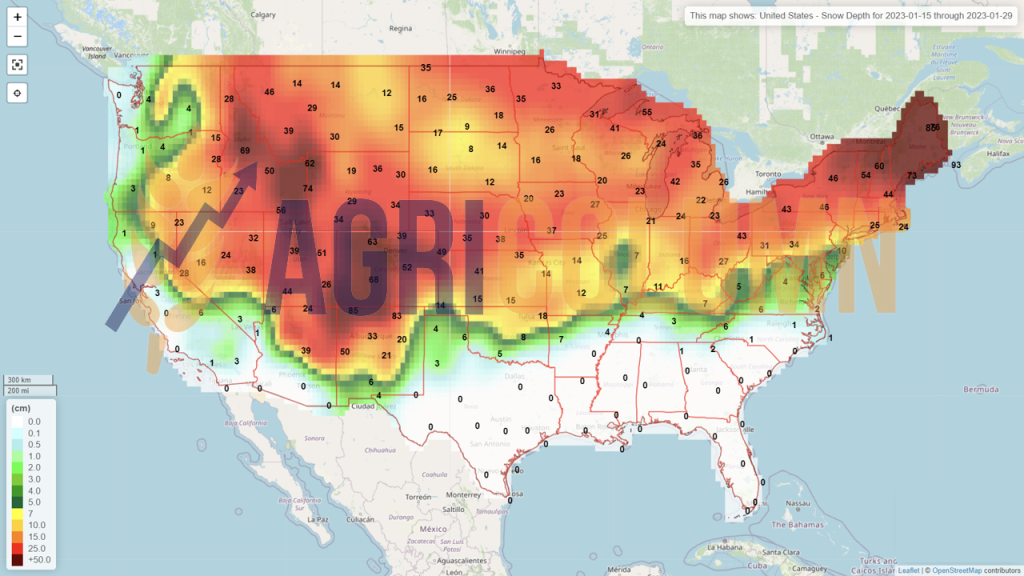

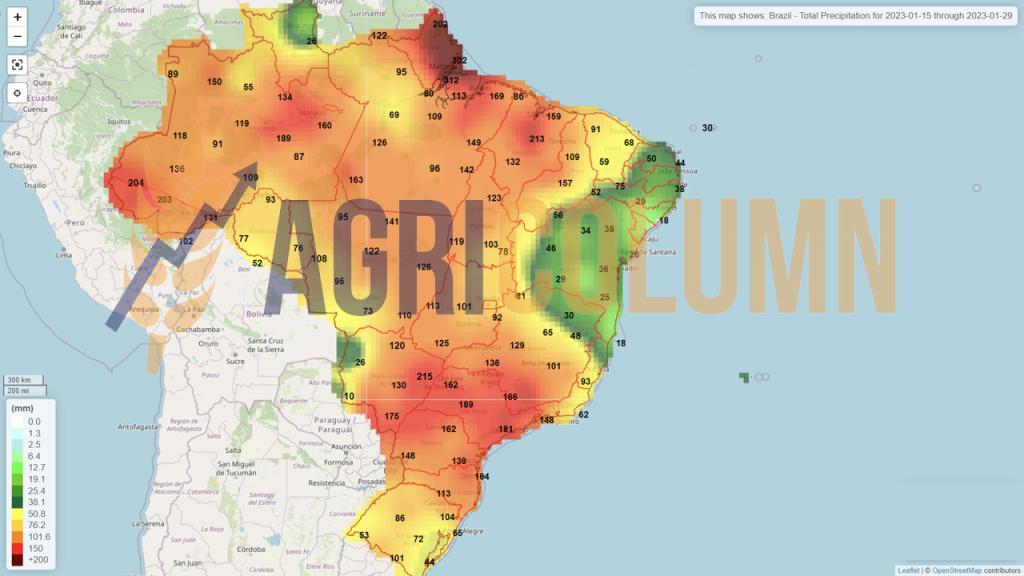

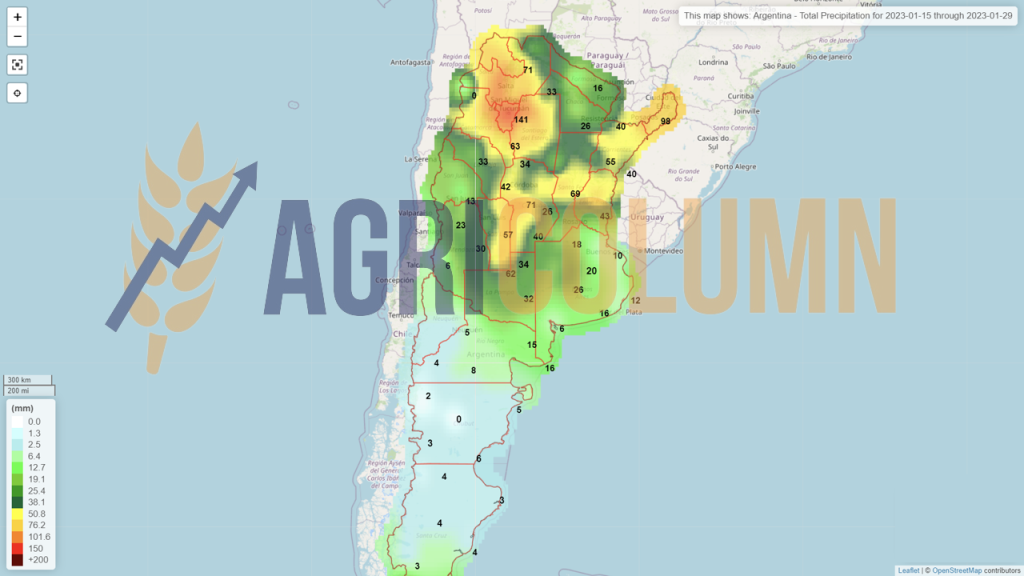

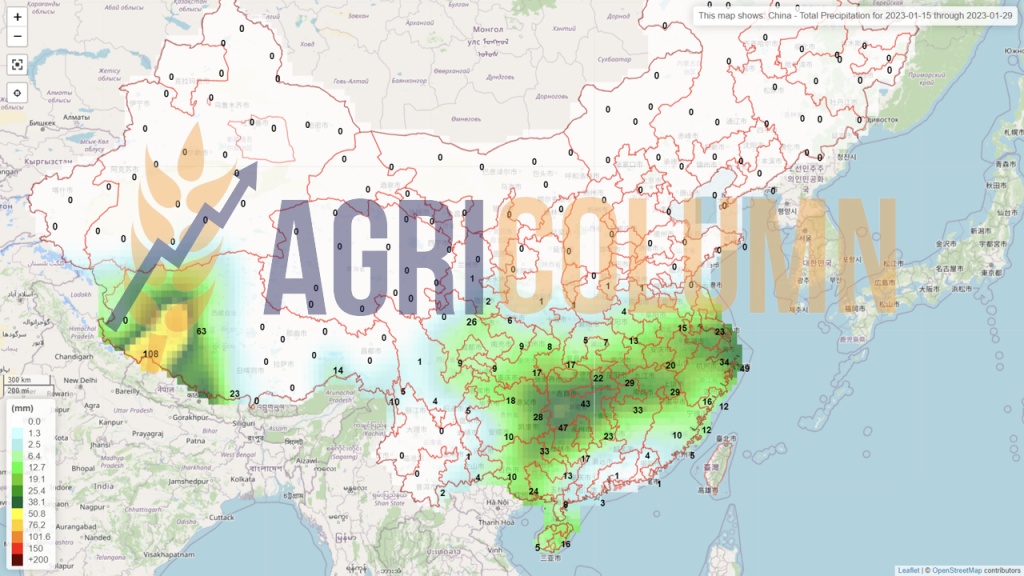

January 15-29, 2023

Romania (rain)

Romania (snow)

Europe (rain)

Europe (snow)

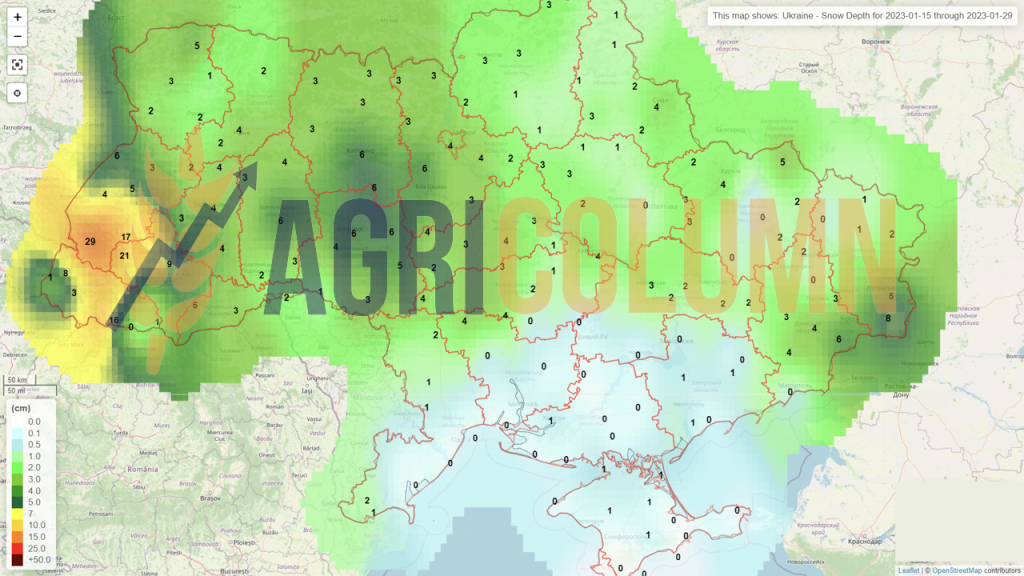

Ukraine (snow)

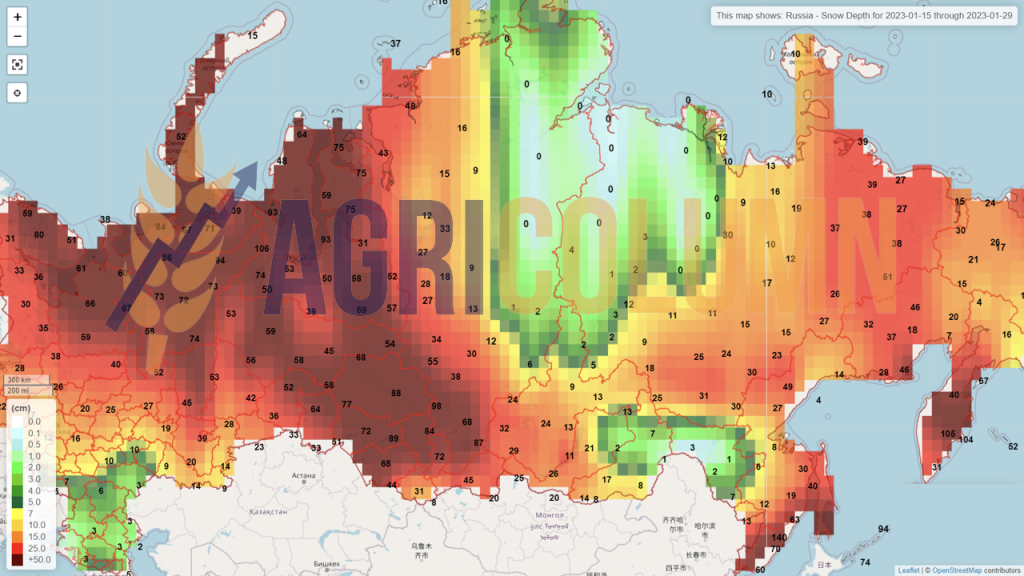

Russia (snow)

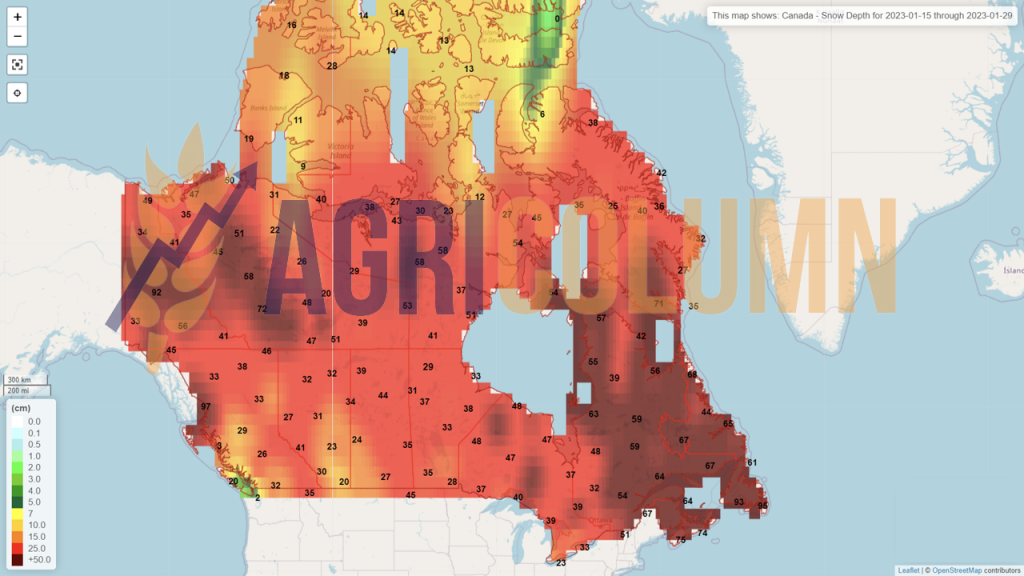

Canada (snow)

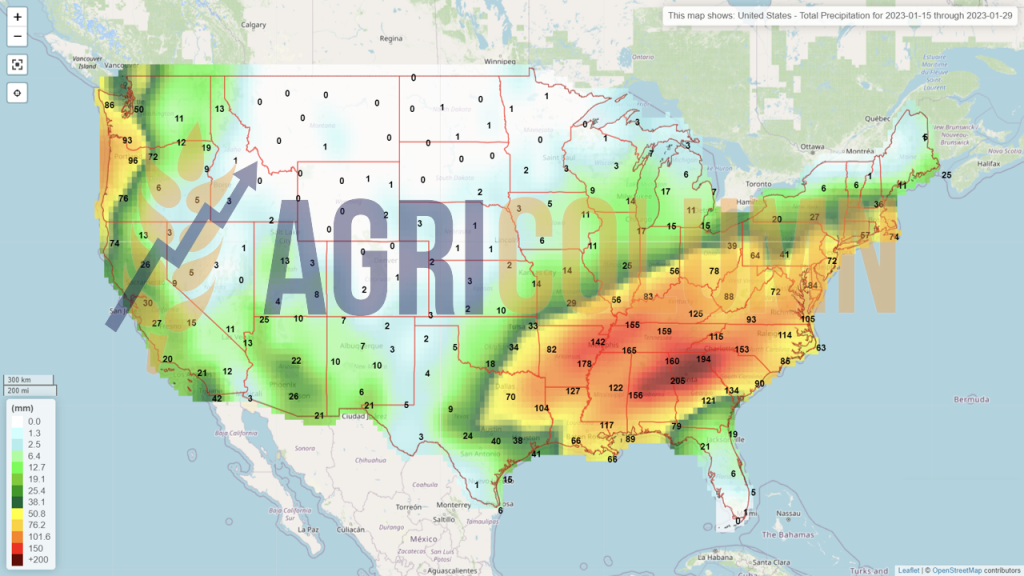

USA (rain)

USA (snow)

Brazil

Argentina

China (rain)

China (snow)

Australia