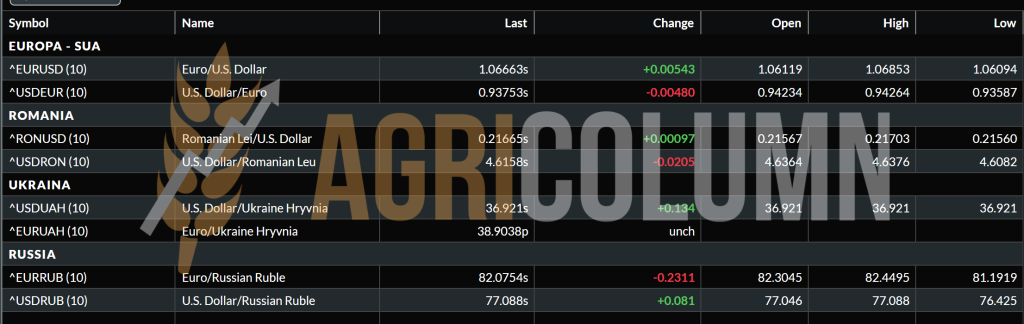

This week’s market report provides information on:

The decision of the European Commission to allocate to Romania an amount of 10 million euros as compensation for the distortion effect created by the Ukrainian transit of goods is nothing more than a pale consolation shown to a faithful partner, which respected its commitments to the European Union.

We can say without error that this amount, no matter that it is less than what was granted to Poland, Bulgaria and other states, is nothing more than crumbs thrown from the table of the rich to loyal and respectable partners.

In a properly rated environment, this would not have happened. Respectable names in the European Parliament clearly pointed out that those corridors of solidarity did not unfold according to the original principles.

More than 14 million tons of goods of Ukrainian origin passed through Romania, and Romania was seriously affected.

We are talking about distortions created at the price level, logistics costs, reduced potential for the delivery of Romanian goods due to congestion at the unloading points. To these, we add storage costs for Romanian goods, as well as those generated by preserving the identity of the products. Let’s not forget the costs generated by the delays in the due date of the input invoices (fertilizers and all the complex necessary for the establishment of a hectare), all mixed with the unnatural desire of Romanian farmers to believe that prices are actually falling, that the market is regulated according to interests other than those of their.

And all these are rewarded with 10 million euros. Thanks to the European Commission for the appreciation! It is effectively a measure of how we are viewed from the warm armchairs of Brussels. Us and the Eastern column, Poland, Hungary, Bulgaria, Slovakia, Czech Republic, etc.

We remember the European slogans – 20 million tons in 3 months. It sounded superb in the buildings of Brussels, but then I asked: How and with what?

Romania has no railway infrastructure and no wagons. Romania does not have land infrastructure and not enough trucks. Romania does not have a developed river transport infrastructure or sufficient barges.

Romania does not have enough qualified personnel at the border points to be able to take over, check and certify Ukrainian goods. And no reception capacity in the port of Constanța (the chaos created by queues can be seen from afar).

I then supported some guidelines for the development of Romania:

- EU to send at least 5,000-8,000 wagons for transfer;

- EU to build buffer depots at the border for unloading and collection;

- EU to develop projects to restore the railway infrastructure;

- EU to transfer 7,000-10,000 trucks for the transfer of goods;

- EU to send qualified staff for border support;

- EU to develop road infrastructure projects in Romania;

- The EU should help the infrastructure of the port of Constanța by expanding the reception capacity, IT systems and the percentage allocation of unloading access to Ukrainian goods, in agreement with Romanian ones.

None of this happened. Absolutely nothing, just total chaos and now a cheap tip of 10 million euros, which, if you divide by the number of hectares allocated to large crops in Romania, does not exceed 1.2 EUR/hectare. If you divide by the total tons produced by Romania in 2022, it means 0.45 EUR/MT. So, nothing.

And the story continues and will continue. Ukrainian goods have been given another year of duty suspension, and the suspension of the sanitary-veterinary certificate is also moving forward. All this on the altar of the god EURO. All this for the EURO god to prosper in front of the officials in the European Commission, some people appointed to the position with clear and unequivocal mandates.

What we are doing now is not venting anger, but simply exposing the Truth.

We ask the farmers of Western Europe: What will you do when it’s your turn, when you face unfair competition (because that’s what it’s all about)?

Pandora’s box is now open and once again we ask the farmers of Western Europe: What will you do when it reaches you? Because, based on how the harvests are presented so far in the European Union, the indication is of normality, by no means of a drought as in the case of corn in the previous season.

And let’s not forget the rapeseed. In the previous season, the Union imported 3.7 million tons of rapeseed, and this season, so far, it has 5.7 million tons. And was there a drought in the case rapeseed? We don’t think so, we believe that the cheap commodity was favored to maximize the profit of operators in the European processing industry. And Ukrainian goods were cheap enough. And as a final detail, last season, imports from Ukraine of rapeseed reached 1.62 million tons, and now they are at the level of 2.87 million tons. The numbers speak for themselves: cheap commodity, short positions when selling oil, a high crush margin…

Pivny -Odessa- Chornomorsk Solidarity Corridor. As I said, a picture is worth a thousand words.

We propose to sit together, to discuss, to see how we can reach the states of normality by creating assets. We want to help, but investment is needed.

We are not holding out for money or compensation, but we want to build together because Romania is a fortress on the eastern flank of NATO, alongside our comrades from Poland.

LOCAL STATUS

The indications of the Port of Constanța vary between values ranging from 248 to 252 EUR/MT. The new crop is valued at levels of 238-242 EUR/MT. Naturally, all indications are in CPT parity.

CAUSES AND EFFECTS

A small carousel, insignificant I might say, coordinates the local wheat market. It is nothing but the reflection of the CBOT in Euronext and further in the physical market. It’s all about the wordplay between the warring parties in the conflict, Russia as the aggressor and Ukraine as the victim of Russian aggression. In other words, we are dealing with a simple rise and fall in a 3-4 EUR/MT range after the massive liquidations in March. The main parameter remains the availability of the goods in the physical market. The final moment of these movements was March 18, 2023, when the Cereal Corridor was officially extended. The Ukrainian side, along with the UN and Turkey, support the extension for 120 days, while the Russian side fined only 60 days by notification. But let’s not forget that Russia is not a signatory to the agreement between Ukraine, the UN and Turkey.

At the same time, the old Romanian crop plays the role of weight in the price equation. The pace of Romanian exports is extremely slow. The total export up to this moment has accumulated a value of about 2.63 million tons. Under these conditions, with a domestic consumption of 3.5 million tons and a crop level of 9 million tons, we obviously have an imbalance.

Time is short until the new crop, and if Romania managed to export 0.63 million tons in 2.5 months, we don’t see how it could continue to perform. Our estimates are a minimum of 1-1.5 million tons that will remain unsold from the 2022 harvest volume and that will create pressure on the price of the 2023 crop. To all this, we also add the 810,000 tons imported from Ukraine, during March 2022 – March 2023.

REGIONAL STATUS

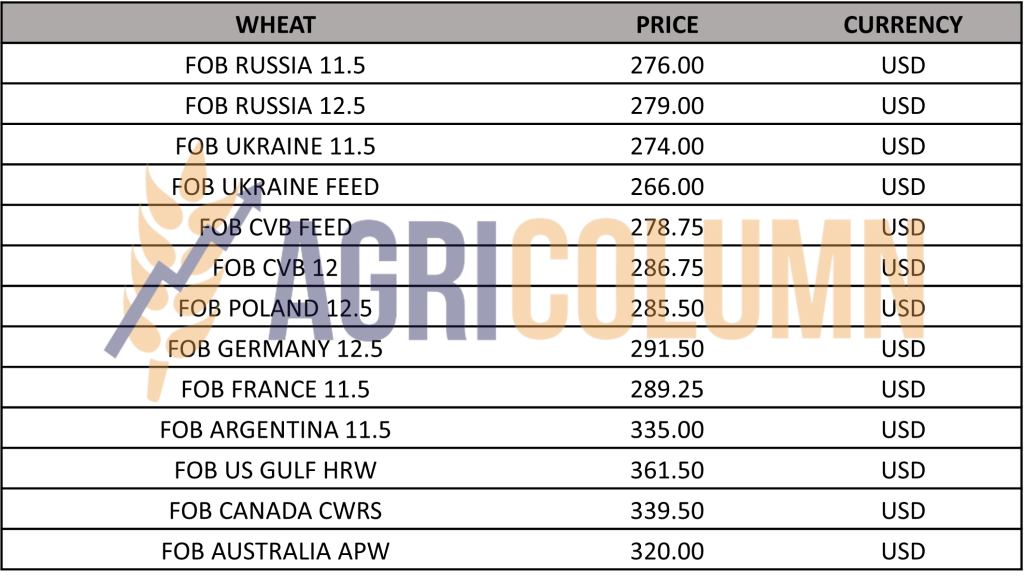

RUSSIA. Russian wheat price indications are under maximum pressure. Quotations pointed to 279 USD/MT FOB parity for 12.5 PRO grade, down 9 USD/MT. We highlight here the effect of Ukraine, which competed extremely vigorously in the last tender in Egypt.

In addition, the pace of Russian exports must be increased in order to be able to move the millions of tons of wheat that burden Russia’s stocks and, implicitly, will give increased weight in the context of the new crop.

Russia intends to export wheat through Berdyansk, a former Ukrainian port – to understand why it is strangling the Corridor. Thus, they will be the first exporters from the Black Sea. Apart from the established Russian ports of Novorossiysk, Tuapse, Taman, Caucasus, Rostov-on-Don, they advance into the basin through this former Ukrainian port of Zaporizhzhia.

That is precisely why Russia is harassing the corridor, to gain time for export and to strangle the transfer of Ukrainian goods to destinations. Moreover, Russia wants to assess its own spring wheat crop and its development to enter the new agricultural year sales. Any harassment or delay to the Corridor is a bonus for Russia. That’s leaving aside the baseless reasons they’ve been clamoring for a very long time.

UKRAINE started the spring sowing campaign about 10 days ago. As for the price of Ukrainian wheat, it is set at the level of 274 USD/MT, FOB POC (Pivny -Odessa- Chornomorsk), in a slight decrease compared to the previous days. What is interesting to note is Ukraine’s approach to the Egyptian tender. Effectively, they discounted the wheat extremely much, under the condition that the payment term is 180 days, that is, 6 months. If we also add the time until the delivery period, we have a share of about 8-12 USD/MT of financing cost in the price of goods sold in Egypt. The transfer of the goods will be carried out by the Egyptian national shipping company NNC (National Naval Company) and we have no doubt that the two ships of 60,000 tons each will not fly through the famous Grain Corridor. Russia will not and will not stop you from these two lots. It’s simple, they don’t want to upset Egypt with anything at all, in terms of future sales.

The EUROPEAN UNION indicates a common wheat export level of 21.54 million tons, including durum wheat as well as other derivatives such as flour, but in equivalent tons of wheat, we reach a level of 22.57 million tons. Cumulatively, imports are at the level of 7.18 million tons. The condition of crops is in the same favorable parameters.

EURONEXT – MLK2323 MAY23 – 265.5 EUR (+3.75 EUR vs. previous week)

EURONEXT WHEAT TREND CHART – MLK2323 MAY23

GLOBAL STATUS

USA: Mixed conditions in the Central Plains, where the cold is combined with parts that are subject to snowfall, parts that are still dry, and some areas receive some precipitation.

CBOT WHEAT – ZWK23 MAY23 – 710 c/bu (+31 c/bu = +11.4 USD vs last week)

CBOT WHEAT TREND CHART – ZWK23 MAY23

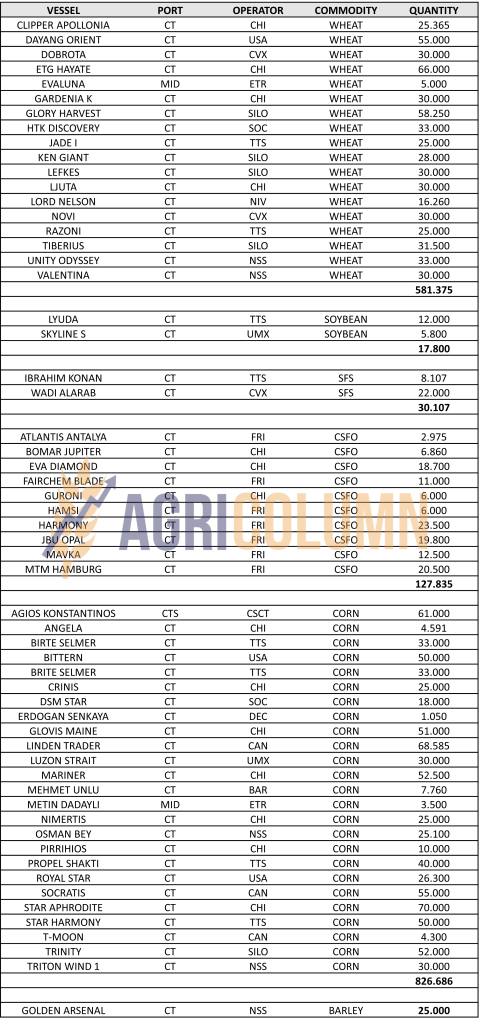

TENDERS AND TRANSACTIONS

GASC EGYPT purchased 2 batches of 60,000 tons of Ukrainian wheat from the Nibulon company:

- FOB price = 279 USD/MT,

- freight cost = 19.22 USD/MT

- Total CIF = 298.72 USD/MT.

The payment term is 180 days from delivery, which will lead to a financing cost of 8-12 USD/MT to the Seller’s account.

What is interesting to see here is that the transport will be carried out by NNC Egypt, which will ensure extremely fast transfer through JCC Istanbul, i.e. the inspection point.

TUNISIA purchased 234,000 tons of wheat at prices between 292 and 306 EUR/MT CNF, for delivery in April-May. Most likely, no more than 50 thousand tons of Russian origin, judging by the names of the winners. The rest is European wheat, which makes sense given that the purchase was financed by a partner bank of the European Commission.

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

CAUSES AND EFFECTS

The world is watching the Corridor. Its extension is clear, but the period is not defined. Russia only wants 60 days, the UN and Ukraine want 120 days. And this and feeds the headlines that feed the stock market trading algorithms.

And the most vehement seems to be CBOT. Why? Simple, because there were extremely many positions liquidated in March and now re-entry is inevitable. But the carousel we viewed last week did nothing but feed the fund accounts through successive inflows and outflows.

On top of this, we have the bankruptcy of Silicon Valley Bank, which puts even more pressure on the FED in the upcoming March 22nd meeting. What position will the FED take? Will interest rates continue to rise? By how much? The options are 0.5% or 0.25%, but we think the second option is the most plausible at the moment due to banking pressure. The US banking systems are well shaken and the FED will choose a suspension path, a moment of respite and consolidation granted to American banks.

We have one more parameter to discuss, namely the cost of establishing crops. We are talking here about the European Union and the USA, as well as the rest of the countries affected by the global energy crisis produced by Russia. Crop establishment costs were extremely high in the fall of 2022, and they act as a long-term hitter.

These costs must be dissipated. But with these prices that have effectively fallen from above, over a period of time, let’s call it an average, their dissipation in a system cannot be carried out lightly. That is why we foresee that, in any conclusion, the establishment costs must be taken into account, wherever these costs are located on the globe. Whether we’re talking about the Northern Hemisphere, whether we’re talking about Asia or South America or Australia. We thus have a landmark that must be taken into account, because otherwise, bankruptcies among farmers, globally, could turn out to be a snowball that will roll downhill, becoming a problem in the world supply of agricultural raw materials.

Otherwise, the markers are well defined for the starting price of the new crop. There will be harvest pressure, there will be fierce competition in the Black Sea basin, and this means nothing but Free Trade, that is, a Free Market, an absolutely normal and beneficial thing for everyone.

LOCAL STATUS

The price indications of feed barley are around 220 EUR/MT, CPT Constanța.

The new crop has an indication of 212 EUR/MT, CPT Constanța.

REGIONAL STATUS

No essential changes. In the Northern Hemisphere, spring barley has entered the seeding process.

TENDERS AND TRANSACTIONS

MIT JORDAN purchased 50,000 tons of barley from Ameropa at 275.5 USD/MT, CFR Aqaba, delivery in the first half of September.

BARLEY PRICE INDICATIONS IN MAIN ORIGINS

GLOBAL STATUS

No essential changes.

LOCAL STATUS

Corn indications in the port of Constanța drop to the level of 240-242 EUR/MT.

The new crop is valued at 225 EUR/MT, in the same parity, CPT Constanța.

CAUSES AND EFFECTS

Irrigated corn could become the profit center of farmers, in the perspective of the new crop. It is the yield that will decide this. In the perspective of price declines we have visualized, production is the only driver of profit growth.

Otherwise, the road of the old crop is conditioned by the supply need of the European Union and, implicitly, by the effects of the decisions on the Corridor.

REGIONAL STATUS

THE EUROPEAN UNION imported a level of 19 million tons, with an intake of 9.65 million tons originating in Ukraine and 7.7 million from Brazil. We see a slowdown in the import of corn into the European Union, a sign that the need has obviously been covered.

What will come next will not generate such a high level in terms of volume. And, in the perspective of the new crop, estimating a permissive weather, we wonder where the Ukrainian corn will go. A party sure in the Union, but the difference which routes will take?

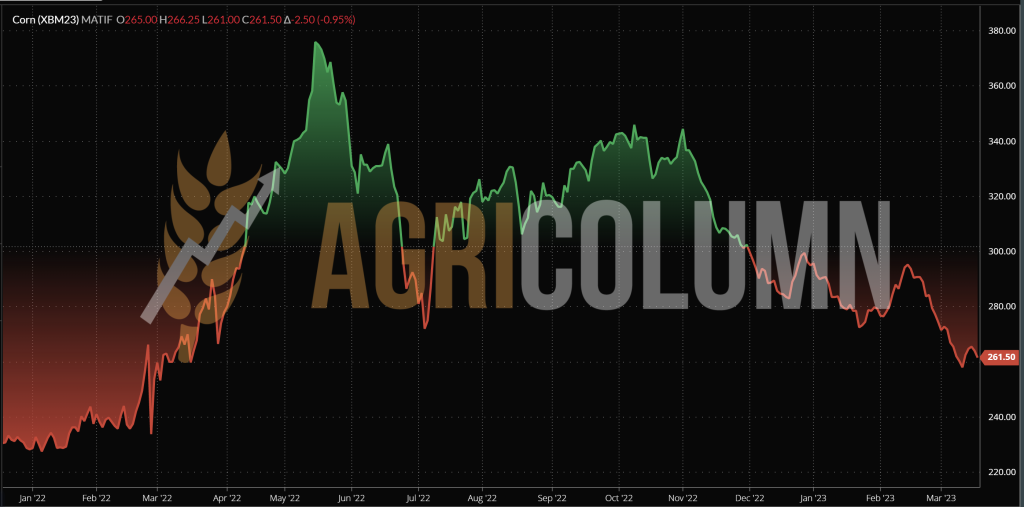

EURONEXT CORN – XBM23 JUN23 – 261.5 EUR (+3.5 EUR vs last week)

EURONEXT CORN TREND CHART – XBM23 JUN23

GLOBAL STATUS

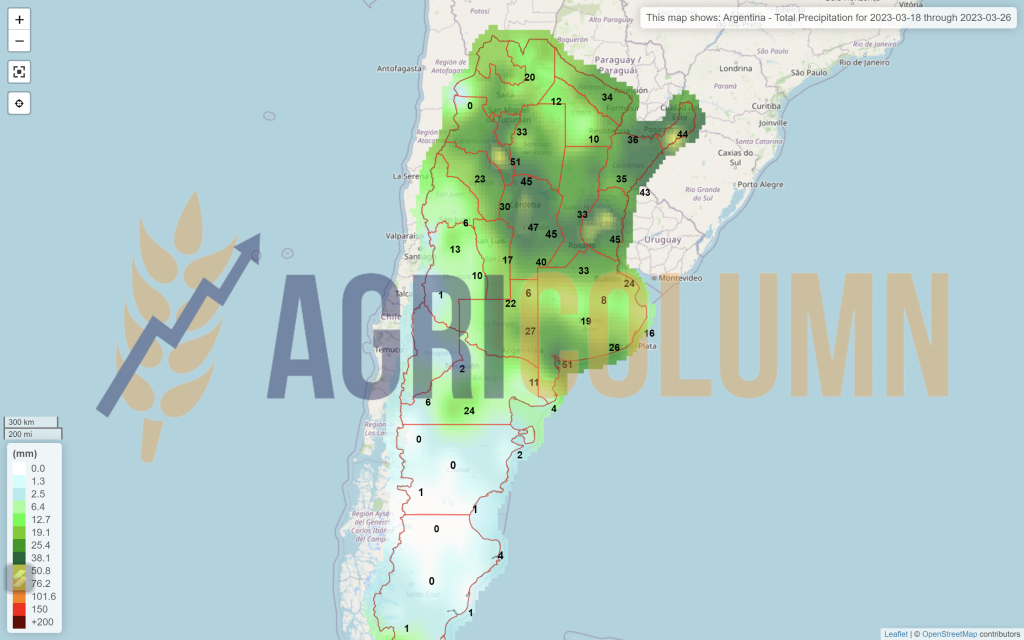

ARGENTINA is in the same state we have known for a very long time – drought and degraded crops.

The USA performs and does it well. In four consecutive days, the US sells 2.11 million tons of corn to China.

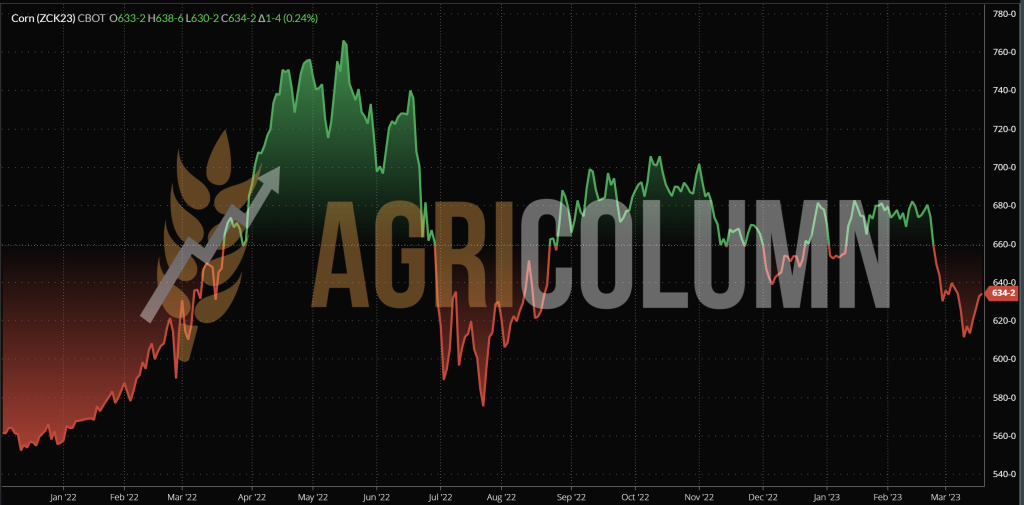

CBOT CORN ZCK23 MAY23 – 617 c/bu (+/-0 vs. last week)

CBOT CORN TREND CHART – ZCK23 MAY23

CORN PRICE INDICATIONS IN MAIN ORIGINS

CAUSES AND EFFECTS

EXTRACT from the previous issue: “What’s next? A calm and calm period in the corn price market. The calm will be generated by the fact that we have factors that are easily perceptible.”

Things went according to what I specified. Nothing new except the US sales performance. The Chinese giant has woken up from the sleep caused by the effects of the ZERO COVID policy and is terribly hungry. This appetite was extremely well calculated, however. They didn’t want to look for food until they saw the downward spiral effect of corn prices generated by the March liquidation. An excellently directed policy of China.

What does this tell us? It indicates exactly the stabilization we were talking about. Setup costs during the Russian energy crisis need to be dissipated, but farmers also have a threshold of pain and bearability, so levels will oscillate within this perimeter.

We look forward to March 31, 2023, when NASS will release the US stocks report and seeding forecasts. From a cost perspective, corn ranks best in the preferences of US farmers. Their national average is 11 tons per hectare, which propels corn to the top of the farm profit center.

We notice the same thing in Brazil, where seeded corn, Safrinha, is already sold, with China being the main buyer in this region of the world. So we do not foresee turbulence in the immediate period and we are referring to a window of 7-10 days.

LOCAL STATUS

Old-crop rapeseed quotations in CPT Constanța parity are at the level of 435 EUR/MT.

The new crop is indicated with a discount of 35 EUR/MT compared to the AUG23 reference, in CPT Constanța parity and minus 45 EUR/MT compared to the AUG23 reference for delivery to the processing units.

CAUSES AND EFFECTS

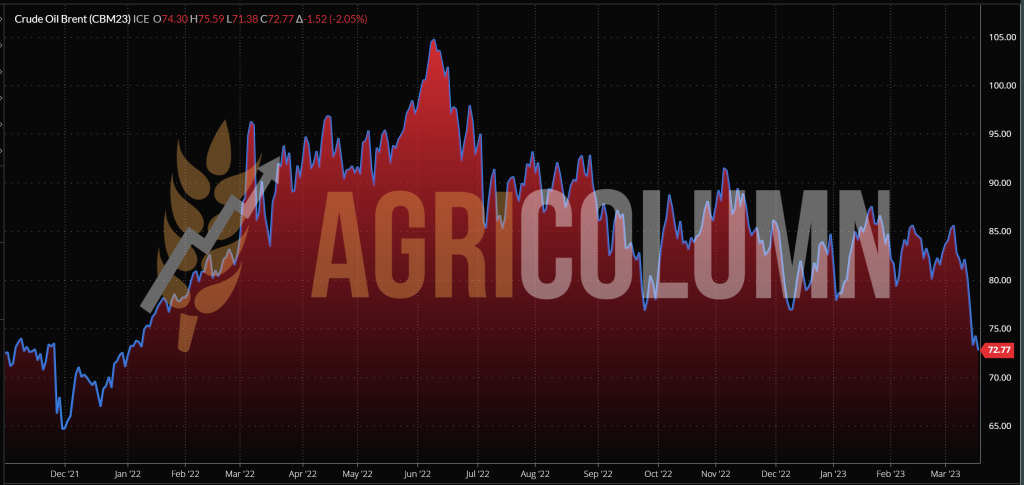

Rapeseed’s downward trajectory continues. Correlation with fossil fuel, against the background of its decline, negatively corrects rapeseed. Domestic buyers fine the price by 10 EUR/MT compared to Port buyers.

And here the logistical difference of 10 EUR/MT between the indication of the Port and the local ones of the processors can be seen very well. The effect of logistic coagulation towards Ukrainian goods is expressed by this formula. Our projections were leading to a EURONEXT AUG23 level of 470 EUR/MT, but close to harvest. This level, observing today’s quotations, has already been met. Whoever understood and sold forwards did very well.

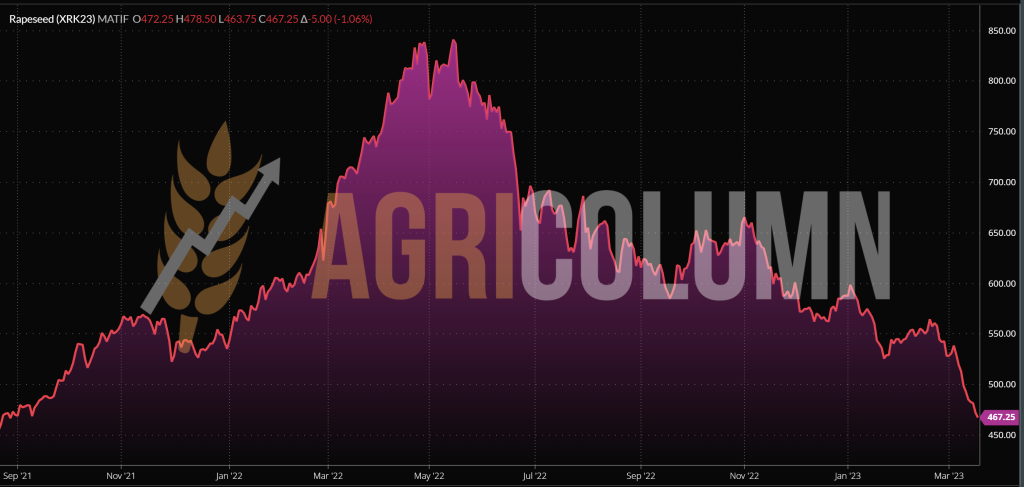

EURONEXT RAPESEED – XRK23 MAY23 – 467.25 EUR (-25.75 EUR vs last week)

EURONEXT RAPESEED TREND CHART – XRK23 MAY23

REGIONAL STATUS

The EUROPEAN UNION has so far imported a volume of 5.76 million tons:

- 86 from Ukraine and

- 33 million tons from Australia.

GLOBAL STATUS

Out of season.

ICE CANOLA RSK23 MAY23 –751.6 CAD (-26.2 CAD vs. last week)

CANOLA ICE TREND CHART – RSK23 MAY23

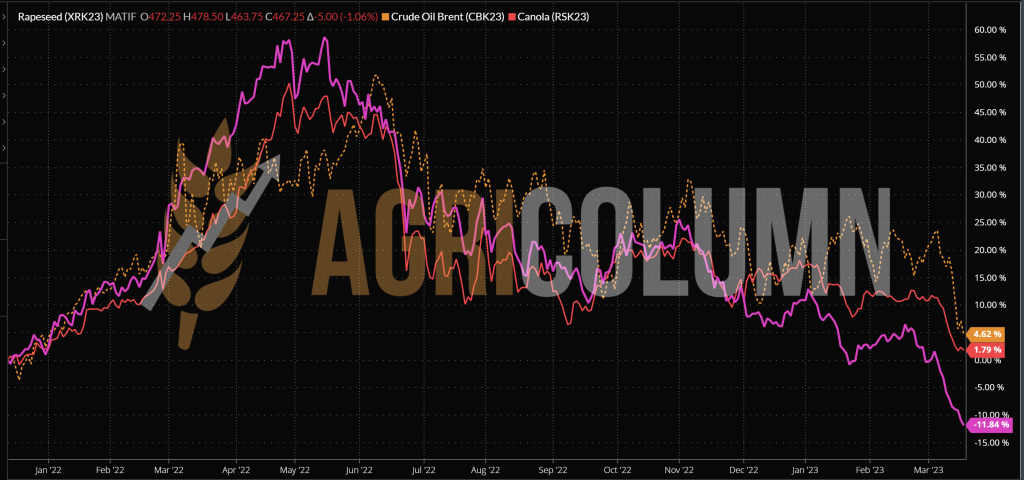

COMPARATIVE GRAPH. PETROL-RAPESEED-CANOLA CORRELATION

Hello, hello! We meet again! Said fossil fuel to rapeseed and canola.

CAUSES AND EFFECTS

- EURONEXT – 2 WEEKS – MINUS 70.75 EUR

VS

- ICE CANOLA – 2 WEEKS – MINUS 70.2 CAD

This comparison tells us a lot. And it was worth developing because we need to understand what will come next:

- Rapeseed looks great vegetatively in Europe.

- Rapeseed is looking great in Ukraine with new potential for spring sowing.

- Rapeseed is in good growing condition in Russia.

- We have a very high volume of Australian crop.

- The forecast is normal for the next season in Australia.

- The forecast is also normal in Canada next season.

For the first time in 25 years, rapeseed oil is lower in price than palm oil. And this demonstrates the cyclicality and erosion of anything that grows without measure.

914 EUR/MT FOB ROTTERDAM = rapeseed oil indication.

The two conjoint factors that worked in the last year, namely the size of the reduced crops (Canada) and the war in Ukraine, disappeared as if without noticing. But it wasn’t quite like that, things unfolded in clear stages and on landings.

What’s next? A future erosion is possible, with at least another 20 EUR on Euronext, and only if the economic premises take into account the costs of establishing crops will we be able to see a brake and a stabilization. That’s how it should be. Across the globe, start-up costs have been impacted by Russia’s intervention in Ukraine.

We believe that there will certainly be a maximum downside threshold, driven by costs. Because otherwise no farm will be profitable and the road to a demand generated by a reduced supply will be paved again.

LOCAL STATUS

Constanța Port quotes sunflower seeds at values between 450-455 USD/MT.

CAUSES AND EFFECTS

EXCERPT FROM THE PREVIOUS ISSUE: “Farmers must sell the goods. The price of oil is low and the coverage is there. We are only 3 months away from processing until the annual reviews.”

The degradation is continuous and nothing can stop this degradation. Crude oil quotes are off due to lack of demand. Ukrainian goods are no longer in demand, and thus the seeds go the way of Romania and Bulgaria, at a very low price level. Port Constanța is still generous, but we must not forget that this coverage request will also end soon.

And we have one more thing to say, related to the new crop. Everyone will seed the sunflower at a high level. Russia, Ukraine, European Union. This aspect will automatically lead to a decrease in price and interest, against the background of a generous offer. Today, we already see the new crop at 420 USD/MT.

REGIONAL STATUS

UKRAINE. We are in the same situation where there are no offers to buy oil. As and when a price is still offered, but under 1,000 USD/MT FOB, while in CPT POC, the price is at 900 USD/MT.

GLOBAL STATUS

ARGENTINA has reached a harvest level of 50%. Sources indicate a total forecast of a minimum of 3.5 million tons, with a maximum of 3.7 million tons.

PRICE INDICATIONS FOR OILSEEDS AND CSFO IN MAIN ORIGINS

CAUSES AND EFFECTS

EXTRACT FROM THE PREVIOUS REPORT: “In the remaining time, there is not much that can happen. A possible closure of the corridor would cause a much greater influx of raw material on the established channels and, implicitly, a much lower price, against the background of the much more generous offer.”

This is exactly what is happening. The price has eroded substantially and has no future. Maybe 10-15 USD/MT after April. We emphasize “maybe“.

Italic logic says that with prices deteriorating and demand very low, we no longer have parameters for growth. What we have today could drive the price even lower:

- Farmers start planting sunflowers in the Northern Hemisphere.

- Argentina will generate 3.5-3.7 million tons, ahead of their initial forecast of 4.2 million tons. But their effect is late, they have no way to influence the market in any way.

- The month of April will be almost non-existent. The Easter holidays will cover ½ of the month, with the Catholic celebration on April 9 and the Orthodox on April 16, as well as the subsequent days off, which will cover half of the month.

- On March 22 begins the most important Muslim holiday, namely Ramadan, which will occupy this period until April 21, 2023.

So we have enough arguments to potentiate a lack of demand and interest in the next period. The sunflower seed life cycle has reached 85% of the way. And, always, this route ends in negative price terms because after April the new crop will be well seen.

And the new crop will have a minimum 30 USD/MT inverse from today, ie 420 USD/MT. The establishment costs of the new sunflower crop are below the level of the past, so the price projection is finding balance. It is the first crop that can be balanced on this route in the last 18 months.

LOCAL STATUS

In Romania, the price indications for soybeans are at the level of 515 USD/MT, DAP processing units for non-GMO soybeans.

REGIONAL STATUS

The EUROPEAN UNION reached an import level of 7.7 million tons. In terms of volume, we believe that a minimum of 1.5-2 million tons will be imported this season.

GLOBAL STATUS

ARGENTINA. BAGE – BUENOS AIRES GRAIN EXCHANGE again lowered the volume projection of the Argentine crop to the level of 25 million tons. This aspect will generate an import requirement of Argentina, a requirement that will be covered from Brazil, for sure. Because, in addition to Argentina, Paraguay is in obvious difficulty after the episode of 2 years ago. Their volume forecast drops by 20%, from 10 million tons to just 8 million tons.

CBOT SOY ZSK23 MAY23 – 1,476 c/bu (-31 c/bu compared to last week)

SOY TREND GRAPH – ZSK23 MAY23

CAUSES AND EFFECTS

Soy was supposed to maintain the trend of the other crops and thus, we record the decrease in indications.

Funds have played and are now taking profits in the short term, 31 c/bu (11.4 USD/MT) is a solid profit not to be missed.

March 31 will come with the North American stocks report, which will also initiate US soybean acreage, and what we are seeing now is one of the main effects of the NASS report.

Brazil is the second factor creating the trickle-down effect. 152 million tons is an extremely serious argument for an even more obvious decrease in the future.

19-26 March 2023

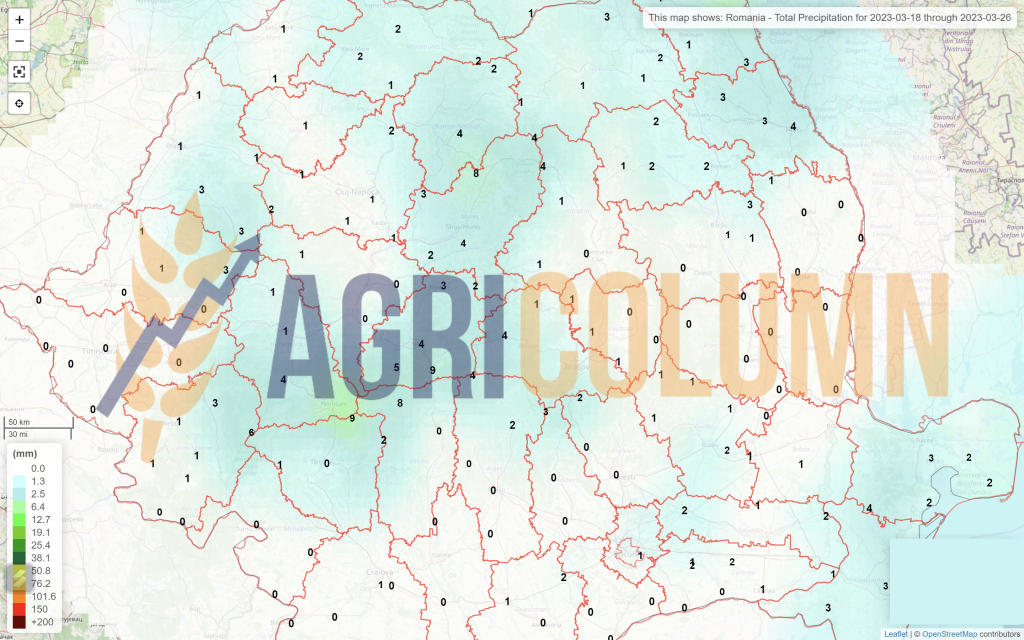

Romania (rain)

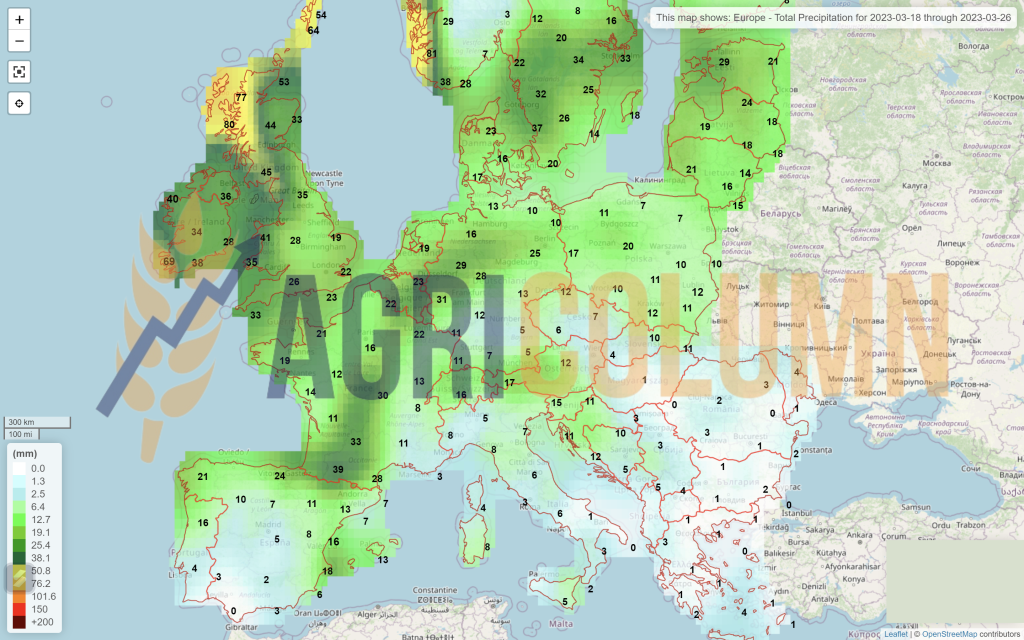

Europe (rain)

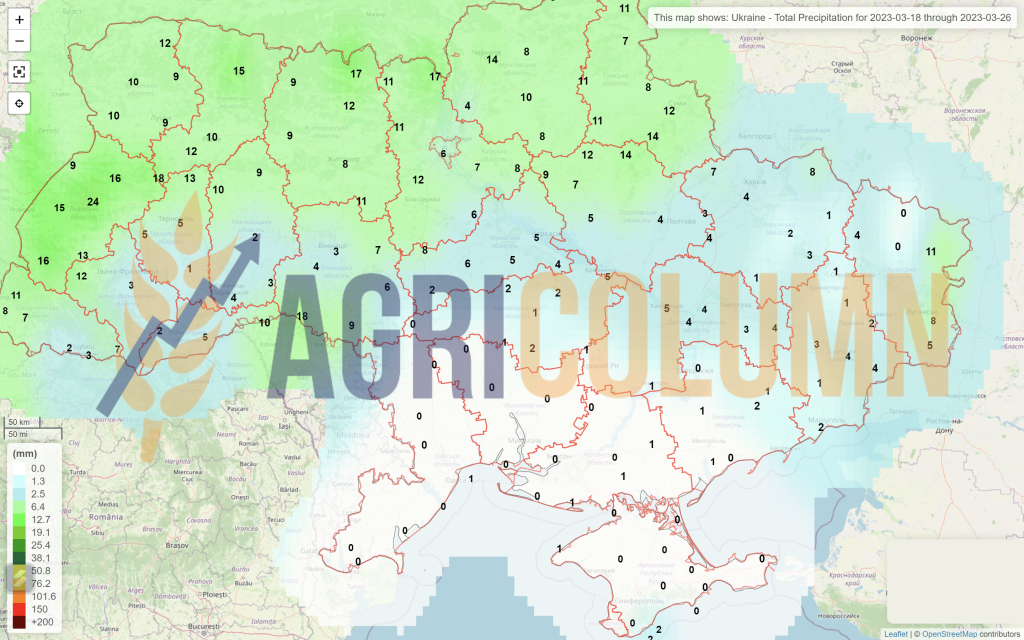

Ukraine (rain)

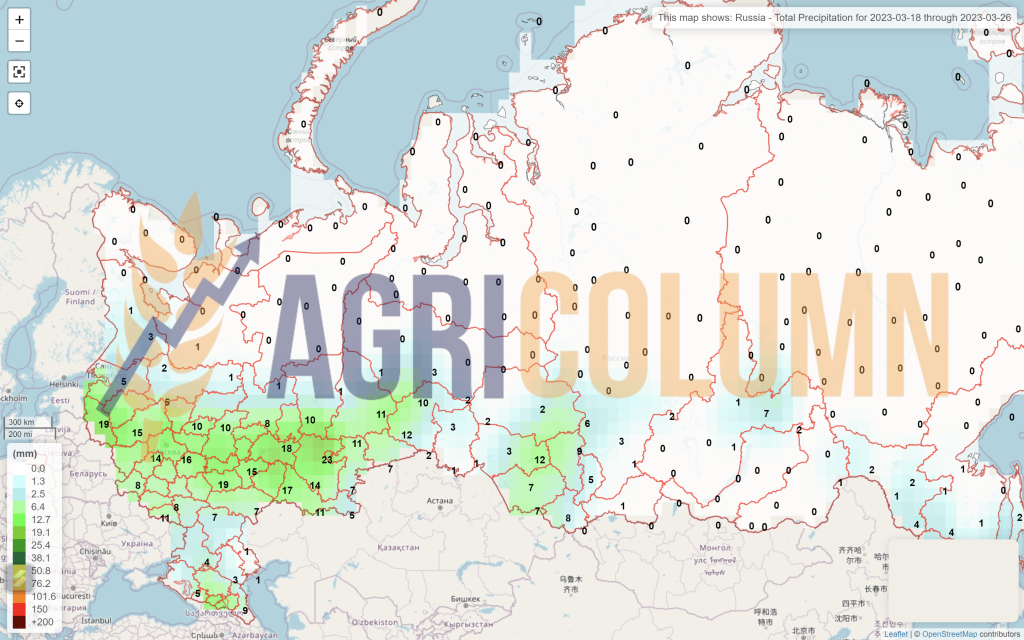

Russia (rain)

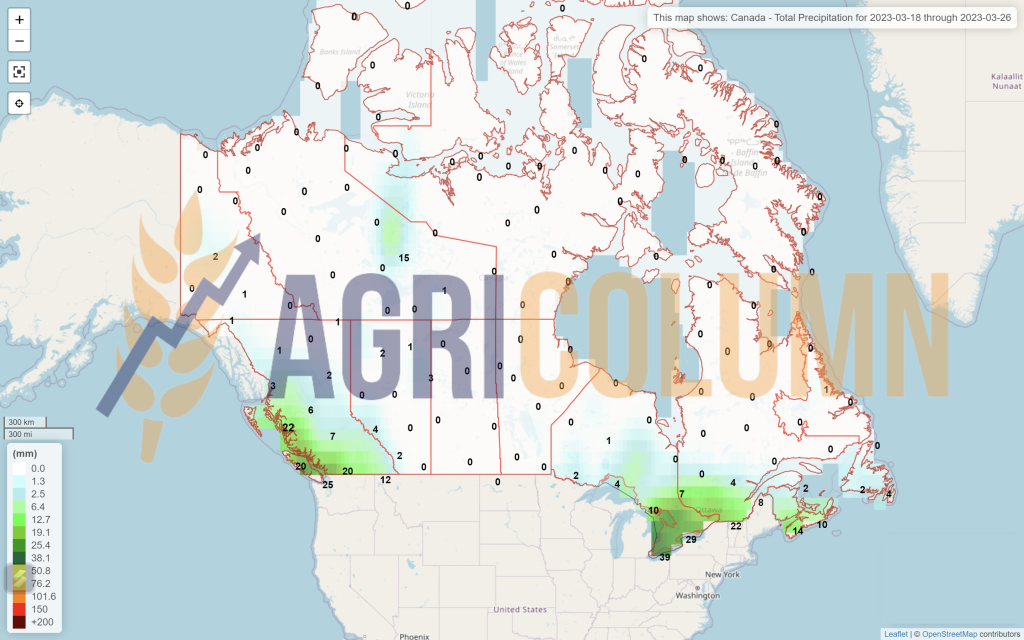

Canada (rain)

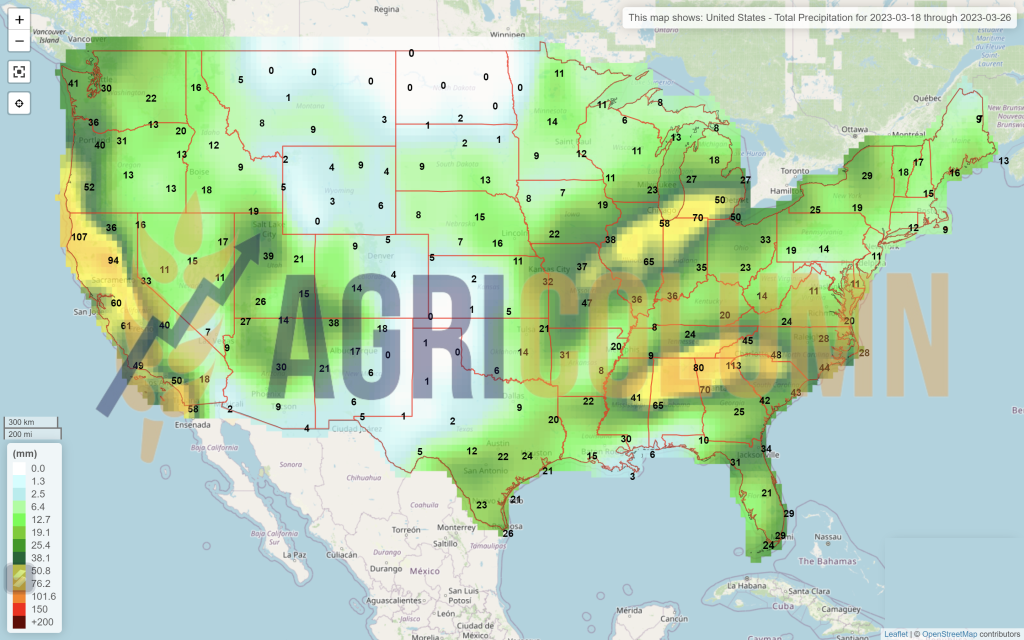

USA (rain)

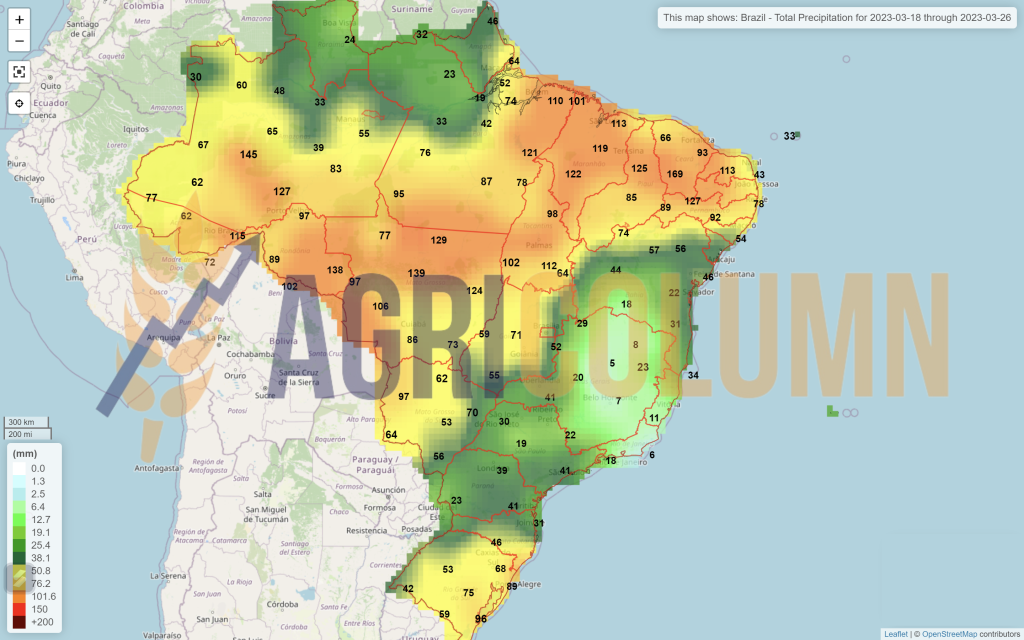

Brazil

Argentina

China (rain)

Australia