This week’s market report provides information on:

LOCALLY

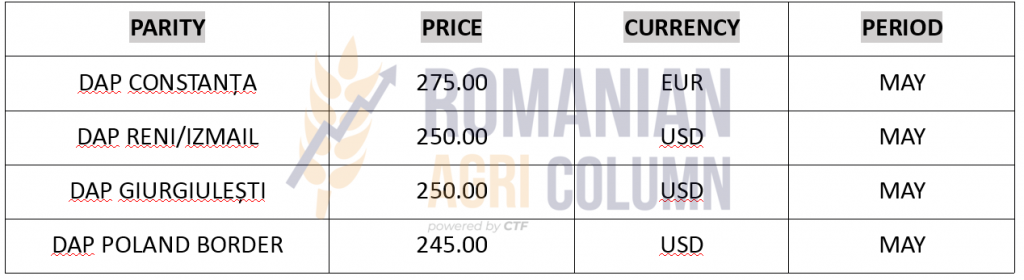

The local market is still on holiday for the most part. The difference between the Orthodox Easter holiday and May 1, International Labor Day, made a bridge to extend the holiday. However, the indications of the Port of Constanța for the old crop milling wheat amount to the level of 365 EUR/MT.

For the new wheat crop, the indications are 365 EUR/MT for milling wheat and 355 EUR/MT for wheat with feed quality.

In the case of the 2022 wheat crop, provided that May 2022 provides sufficient rainfall, we dare to advance figures exceeding 9 million tons, more precisely to have a crop of 9.2 million tons. This would practically mean a recovery of the forecast gap from the autumn of 2021. Then, due to the lack of precipitation, the sowing works were prolonged a lot and we had an uneven emergence and even a non-emergence in certain areas.

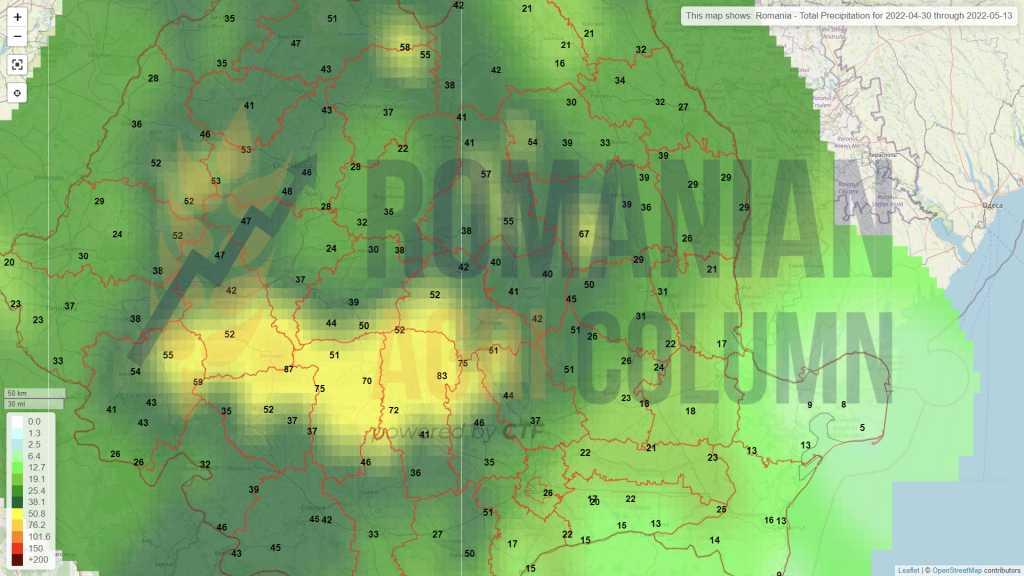

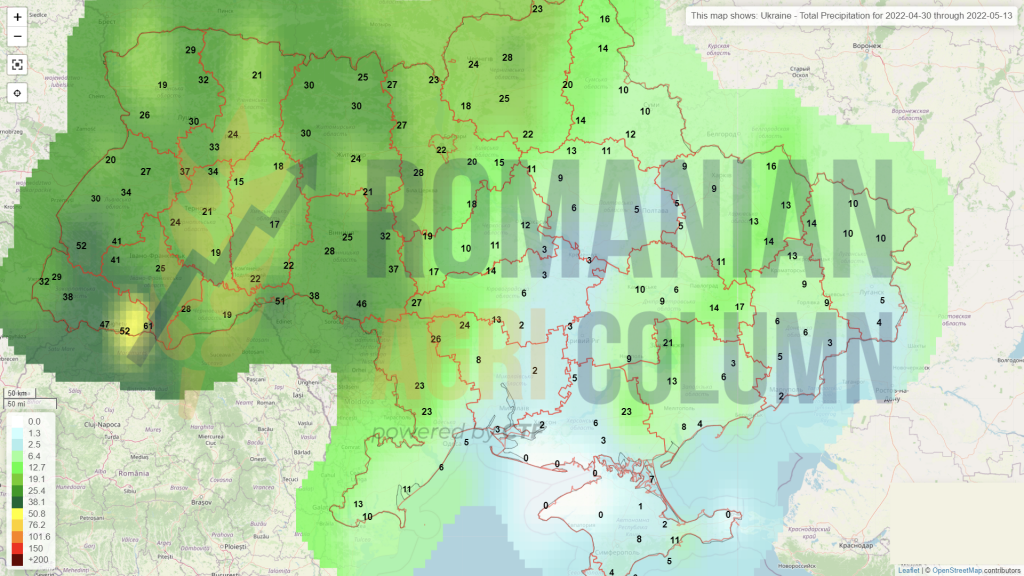

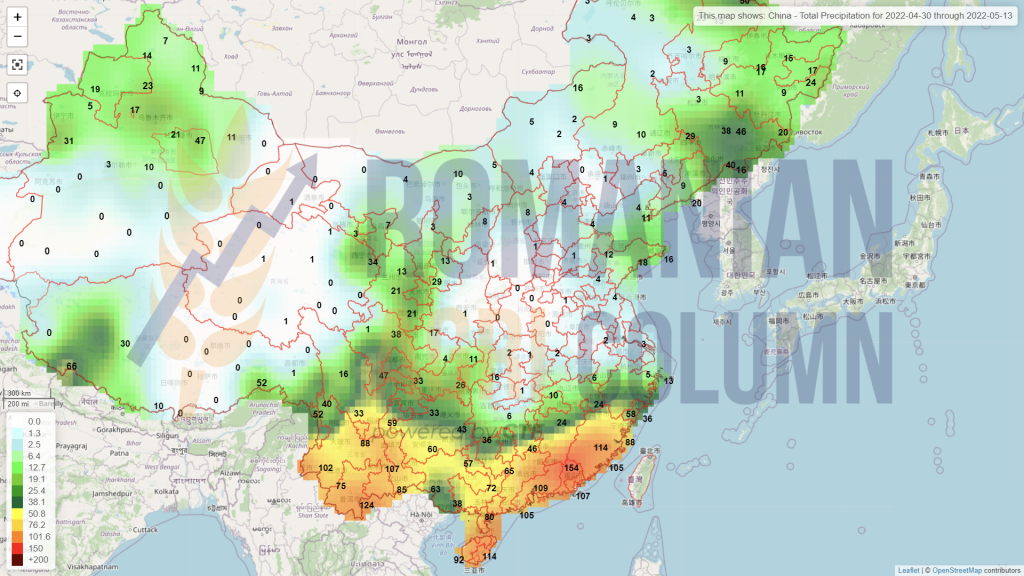

However, we have enough areas affected by pedological drought and the area is very well known: in the middle of Moldova, bordered to the south by Focșani, to the north by Neamț and to the east by Vaslui and Galați. There the problems are still persistent, but the precipitation has started to arrive in Romania. We have national rainfall of 15-30 liters/sqm, in some places the level reaches 60 liters/sqm. For the time being, the coastal area of Romania is still bypassed by rains. The same spectrum applies to the Tulcea region.

Let’s now have an overview of Ukraine’s intention to transit Romania to the port of Constanta. You can find the general details below in the regional analysis, but here, at the local one, we want to raise some questions. We mention that our analysis is oriented towards the particular interests of Romania in terms of food security, including in this spectrum Romanian farmers and traders.

Romania states its intention to support the commercial flow of raw materials that will come by land, via rail and car, as well as by transhipment in Giurgiulesti. It is a natural thing to help a country devastated by the Russian invasion. It is a necessary empathy shown to a neighbor who has extremely serious problems.

From the statements of the Deputy Minister of Agricultural Policy and Food Security of Ukraine, Mr. Taraş Vysotsky, we note something that raises reasonable concerns, along with the above factors, namely that they are willing to discount the goods by up to 50 EUR/MT to have logistic access to export because of the high level of prices globally.

We already have an extremely serious problem here. First of all, we must explain that farmers in Ukraine do not have the same costs of setting up crops as farmers in Romania. Romania is part of the European Union and thus the costs of setting up crops are much higher. Also, fertilizers have a high cost level in Romania compared to Ukraine, which has a well-developed industry. Romania has serious problems today due to the lack of fertilizer production facilities, due to the shutdown of the largest local producer. We put in the picture the fuel costs that do not suffer comparison between the two countries. In general, Ukrainian farmers have much lower costs than Romanian farmers in terms of investment in production per hectare.

And if the Ukrainian goods will form a flow on the corridor to the port of Constanța or even in the domestic market, then the Romanian farmers will suffer a deep degradation in terms of sales prices. It is logical that the exporter will choose to buy much cheaper goods from Ukraine than the Romanian ones. This was practically the Black Sea basin complex, in which we also play as a country. In this way, Romanian farmers will have to sell at much lower prices in order to become competitive, in a situation that they did not create and in which they are clearly disadvantaged by the costs of setting up and EU membership.

It is therefore a situation in which no party is to blame. Farmers in Ukraine are pressured to sell at much lower prices because otherwise they remain with the goods in stock, Romanian farmers will feel the pressure, in turn.

In this way, many farms will not be able to support production costs due to the low level of selling price, in a market that puts them in obvious difficulty and the end of many farms in Romania will be a certainty in a very short time window.

It is a very serious warning signal and our leaders must take it into account and manage it accordingly. In other words, you want to cross my country, but you are actually disturbing and ruining my entire food safety system and putting a lot of pressure on my logistics and infrastructure, which will surely give way.

However, things can be managed with a lot of attention to detail and structure. Nobody says that Ukrainian farmers should not be helped, but they should be helped and nothing else.

What did Romania gain? Some farms will be shut down and, implicitly, the national food security system will be endangered, the infrastructure will fail and it will have to be repaired or replaced, because we have been doing this for decades.

Port facilities are managed by companies that essentially make a profit. And maybe, why not, given the extraordinarily large volumes in Ukraine, there will be an effective move in the Port of Constanta of Ukraine’s interests, while we will look at each other as usual for the simple fact that we have no unity and consistency in anticipation. As well as the proverbial lack of solidarity of farmers who consider that where their land begins there, their interests begin.

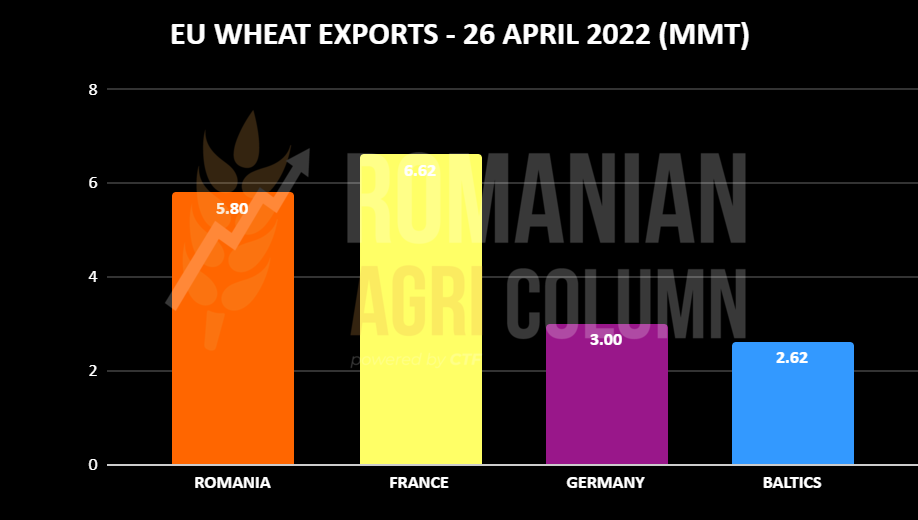

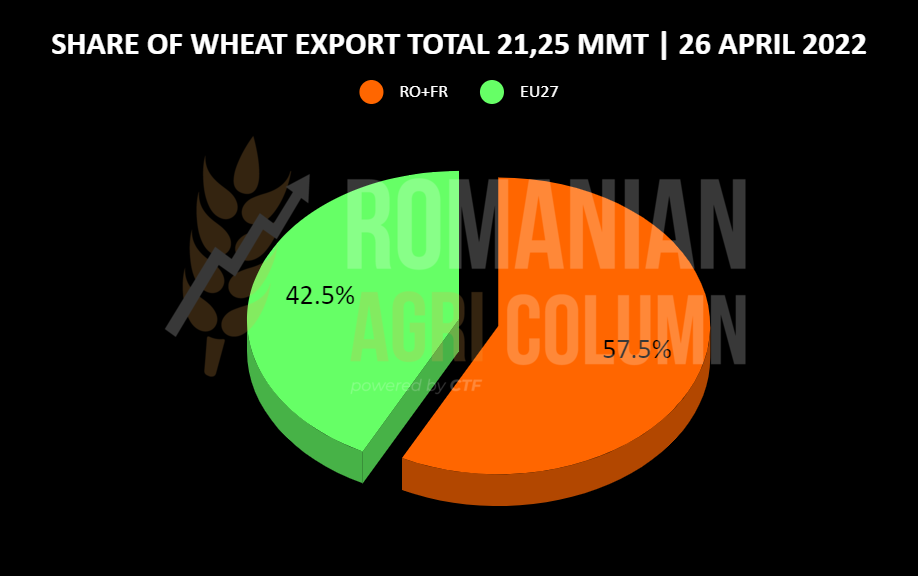

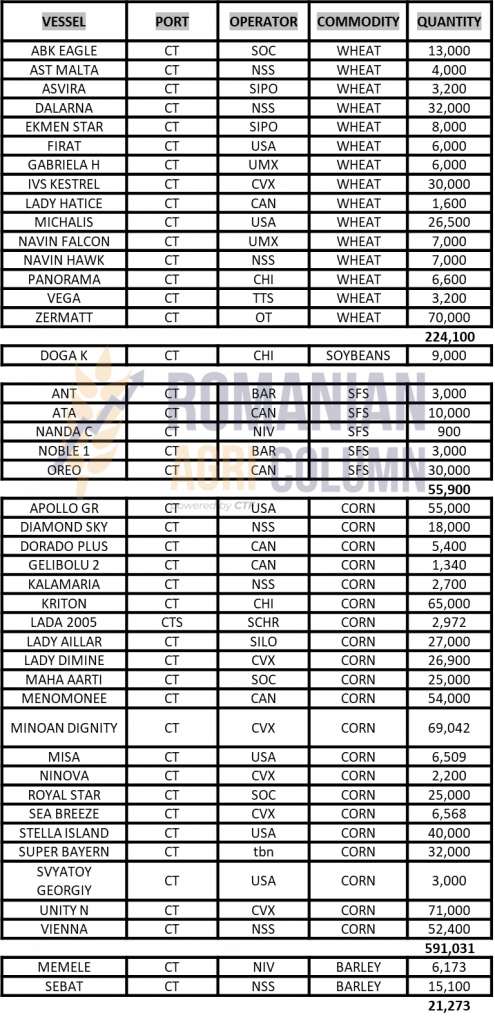

Regarding the 2021-2022 season, Romania reached an export level of 5.7 million tons, according to DG EU, ranking second after France, which has an export level of 6.53 million. tons.

Thus, out of a total of 21.25 million tons exported to the European Union, France and Romania combined have a percentage of 58%. The chart we insert exemplifies this. The two countries represent the European “powerhouse” in terms of wheat exports.

REGIONALLY

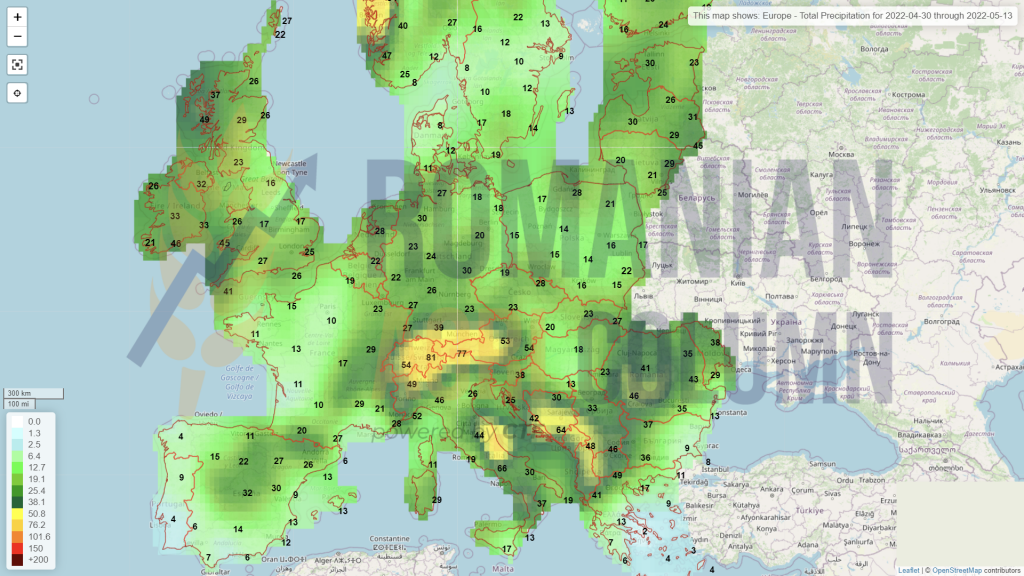

Wheat cultivation is doing very well in the European Union. Apart from the forecast decline due to the lack of rainfall during the winter, indications from Germany and France are very good. Spain remains affected by the drought for the time being and the forecast volume will certainly not be achieved. The Baltic States and Poland will also have some declines caused by previous cold snaps. However, as a general note, the European Union remains at 134 million tons. But if it rains in May, those numbers will improve.

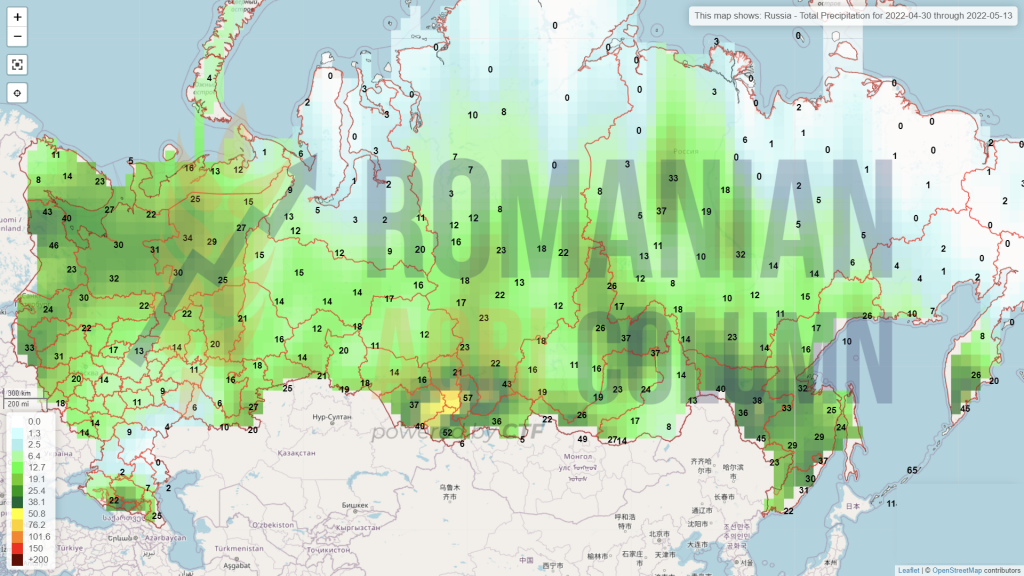

Russia will generate a forecast volume of 85 million tons, according to its own analysts, but we must wait to see these figures and realized. Future WASDE reports will certify the volumes to be completed in stages. The climate was generous with Russia during the winter, and the wheat developed smoothly.

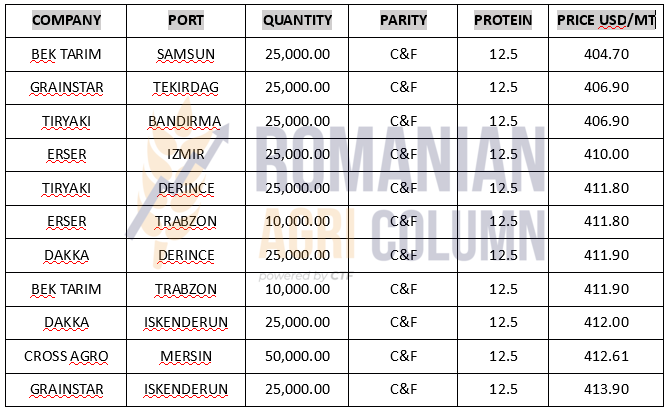

TURKEY purchased, subject to final validation, 270,000 tonnes of milling wheat (12.5% Pro):

SERBIA. On April 20, the Ministry of Agriculture said that the Serbian government had approved monthly quotas for the export of 150,000 tons of wheat, 150,000 tons of corn, 20,000 tons of flour and 8,000 tons of refined sunflower oil. “For an application from an exporter, a maximum of 20% of the approved quantities for a group of products will be available for export every month. If the exporters do not export or exceed the approved quantities, they will not be able to submit an export application next month”, the press release reads. Applications can be submitted during the period 20-25 of the month for the following month. For May, applications can be submitted between April 22-28.

UKRAINE, as we noted in previous issues, will generate only 19.5 million tons of wheat in 2022. However, this production may decrease due to the fact that many fields are mined and their demining requires time and resources.

Since January 2022, we have generated a projection on what will happen and we have disseminated it in the Romanian media. It has come true and we return with it to understand how complex the logistical factor is and how Ukraine intends to develop its relationship with the port of Constanța.

Russia will completely cut off access to Ukraine to the Black Sea. It was a logical move to continue the occupation of the Crimean peninsula in 2014. The total collapse and collapse of the export pipelines of cereals and oilseeds, as well as crude oil are the factors that effectively collapse the economy based on the production and export of raw materials and processing of Ukrainian agriculture. Ukraine’s agricultural economy is dependent on exports of wheat, corn, barley, rapeseed and sunflower oil. Their forecasts of export volumes in the agricultural year 2021-2022 were as follows: 24.6 million tons of wheat, 33 million tons of corn, about 5.8-6 million tons of sunflower oil. We know that Ukraine has a policy of protectionism with regard to sunflower seeds (it does not reimburse VAT on the export of raw materials and adds 10% export tax to the final price of the goods). These forecasts were abruptly halted by the Russian invasion, effectively leaving wheat at a peak of 18 million tonnes, with a remaining non-export of about 7 million tonnes of wheat. Maize, in turn, was stopped from exporting at a level of 18.8-19 million tons. So we are talking about a level of about 13 million tons left un exported. As far as oil is concerned, we all know that the Russian army destroyed facilities and terminals belonging to Ukrainian multinational subsidiaries in the Nykolaiev area, as well as the fact that they actually blocked more than 360,000 tons of crude oil to be delivered to port facilities. We have seen and felt the consequences on the vegetable oil market.

As a move of Ukraine, we anticipated the attempt to create a freight transport-export corridor via Constanța, on various routes: CF Halmeu, Dornești, Reni, by car through Sculeni and Leuseni and tranboard in barges in Giurgiulesti. We anticipated this trajectory generated by the general blockage of access to the Black Sea and we anticipated most of the obstacles in the way of this corridor (logistical, of course). Let’s take each one in turn and analyze them:

The car logistics route involves extraordinarily high costs, of about 210-240 EUR/MT from Ukraine to the port of Constanta, considering the center of Ukraine as a delivery area. Martial law does not allow drivers to leave Ukrainian territory. We also discuss the transit through Transnistria, which is an additional difficulty. There have been cases in which drivers actually left the trucks with goods, after passing through Romania.

The railway route involves huge difficulties, and this is due to the railway gauge difference between Ukraine and the European Union. With a potential of a maximum of 150 European gauge wagons, which totals a maximum of 10,000 tons (a Ukrainian wagon has a maximum capacity of 70 tons), this is like a fragile stream of freight. If we bring into question part of the Romanian logistics complex called rail freight, we are already at an impasse. The average speed level for one year in rail freight transport in Romania does not exceed 20 km/h.

The logistics route with transboard in barges to Giurgiulești can be an alternative, provided that it can receive and transboard the goods in large volumes. The port traffic is very narrow and the port facilities are underdeveloped. Moreover, if we take into account the availability of barges to which we add the coastal vessels that can load in this port of Prut, we also find that it is insufficient.

And now, after this detailed introduction, let’s point out some of the huge problems that Ukraine is facing during this period:

About 20 million tons of goods are in the inner silos and will be added to a crop that will be a maximum of 60-65% of the potential of this country.

According to APK-Inform, more than 30,000 wagons were piled up at the border points in western Ukraine, said Ukrzaliznytsia’s deputy commercial director Valery Tkachov.

As of April 4, there were 23,195. The number increased to 30,271 wagons on April 27 (+ 30.5%). In particular, the number of grain wagons increased from 1,988 to 5,185 during this period. Larger volumes of agricultural goods are heading to Romania and Moldova. The Izov – Hrubeszew checkpoint (Poland) is the busiest. It takes 20 days to get through it.

Freight is stuck in the 57 ships in Ukrainian ports on the Black Sea, and more than likely they will be irreparably damaged. You can’t store corn, wheat and vegetable oil in barns indefinitely. 2-3 months can ensure the preservation of the product’s identity, but then, once the transition from winter to summer, there are problems of temperature differences that affect the identity of the products.

In winter, towards spring, condensation is created in the metal barns of the ships and the aeration cannot be carried out. The transition to the heat in May will cause the goods to heat up, for the same reasons – the metal barns of the ships. Without going into too much detail, things are simple and clear – a transport ship is a transit medium, not a storage medium.

According to the Deputy Minister for Agricultural Policy and Food Security of Ukraine, the intentions are clearly expressed for the use of Romania and the port of Constanța as a corridor for export. And his statements indicate some definite things, and the first of them is a lasting conflict.

In other words, Ukraine can no longer rely in any way on its Black Sea ports (not to mention the Sea of Azov). This is certain and unquestionable. Anyone who believes that this war will end before 2023 is an optimist. No one wants a prolonged conflict, but all information leads in this direction.

So we have a first confirmed parameter, namely that Ukraine will no longer have access to ports at all, and Constanța is their only efficient option. There is still a Nordic flow, but logic says you have to go down, not up and then down, if we are talking about the destinations where Ukrainian goods usually go.

Also from those statements, we note the intention to build transboard facilities and temporary buffers for Ukrainian goods at the border with Romania, with an investment intention of 100 million USD. Not much, but not nothing. With this money you can build at least 10-12 facilities with a capacity of at least 120,000-150,000 tons. This means that we are approaching a volume level of about 1.5-1.8 million tons.

We go further and also note the intention of transit to the port of Constanța of monthly volumes of at least 500,000-600,000 tons of goods. Things are already getting very complicated here, for several reasons, and the first one is the logistics one (transport by rail). 500,000 tons means no more and no less than 10,000 freight cars. And, taking as a benchmark a size of at least 5-7 days from the border crossing points where these facilities will be located, and at the other end the port of Constanța, we already have a surplus of traffic in demand of at least 3,000-3,300 wagons.

Can Romania provide such a thing? Can the infrastructure support a surplus of wagon demand? Can the Romanian infrastructure provide support for moving this number constantly at least 3 times a month from the loading points to the port of Constanța? Can the port of Constanța receive an additional influx of goods, knowing all the precarious state of the port’s triage?

There are unanswered questions, but if this happens, there will be blockages that are hard to imagine, there will be a shortage of wagons locally, and logistics costs will increase due to the demand for wagons.

Also, the port of Constanța will be subjected to extreme pressure. At the moment, we all know that about 90% of the port facilities for exporting grain and oilseeds are owned by multinational companies in the field. And 10% are also used by multinational companies in peak exports, when their terminals will not cope with the influx of goods.

In other words, the Romanian port facilities are not within the reach of Romania, and the latter cannot condition their operation. Not to mention the operating costs, which will increase exponentially due to demand and lack of space availability. To these we add the costs of electricity and fossil fuels, which are used in port terminals.

Normally, the port of Constanța is blocked extremely often during the summer, but also in autumn, winter and part of March (exactly harvest, when delivery and after the holidays, when the agricultural year of sale continues). And if we calculate the export levels of cereals and oilseeds, without adding the flows from Serbia and Hungary, we conclude a level of 16-17 million tons of Romanian goods. But if there is an initial flow of Ukrainian goods, we come to figures that make everyone shiver. An additional flow of about 7 million tons will put a lot of pressure on the infrastructure of Constanța port.

In support of the scenario outlined above are the events of the last few days, which strengthen these predictions. Russia has fired two rockets and damaged a strategic bridge in the Ukraine (Odessa) region, according to local officials. It is an event that could affect Ukrainian plans to expand exports through Danube ports. The bridge over the Dniester estuary is part of the only fully controlled Ukrainian railway route to Ukrainian ports on the Danube, which Kiev considers a promising export route, in a situation where Black Sea ports are blocked. Ukraine, a large agricultural producer, used to export most of its goods through seaports, but since the Russian invasion in February, it has been forced to export by train across the western border or through its small Danube river ports. Railway data showed that about 1,000 wagons with various goods in mid-April, including 238 wagons with grain, were in Izmail station, Ukraine’s largest Danube port. Romania, a member of the EU, borders the Black Sea with Bulgaria, Turkey, Georgia and Ukraine. You can see how the southern communication route is actually cut off at this time. The routes to Giurgiulesti and Reni-Galati are effectively blocked.

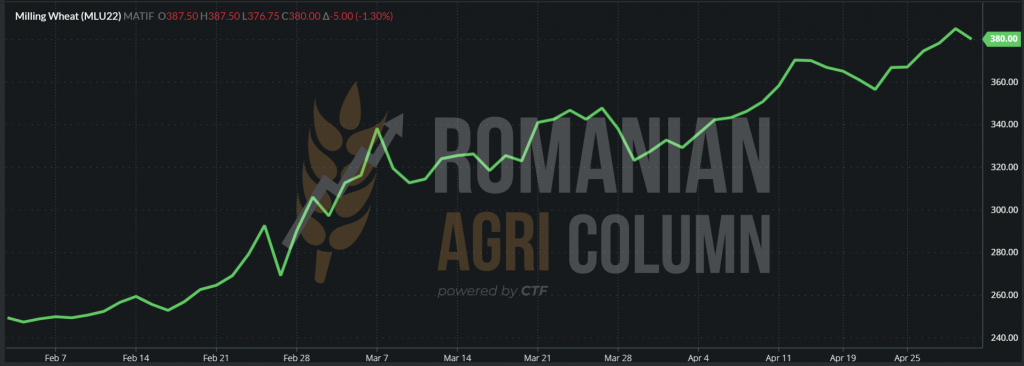

EURONEXT has been swinging in recent days between US news and the liquidation of MAY22 positions, so the ups and downs we have seen in recent days are a mix between the state of physical crop and the actions of investment funds, profit taking, roll over, sell off.

EURONEXT WHEAT SEP22 – 380 EUR (-5 EUR) at the end of April 29, 2022

MLU 22 SEP22 WHEAT TREND GRAPHIC (380 EUR)

GLOBALLY

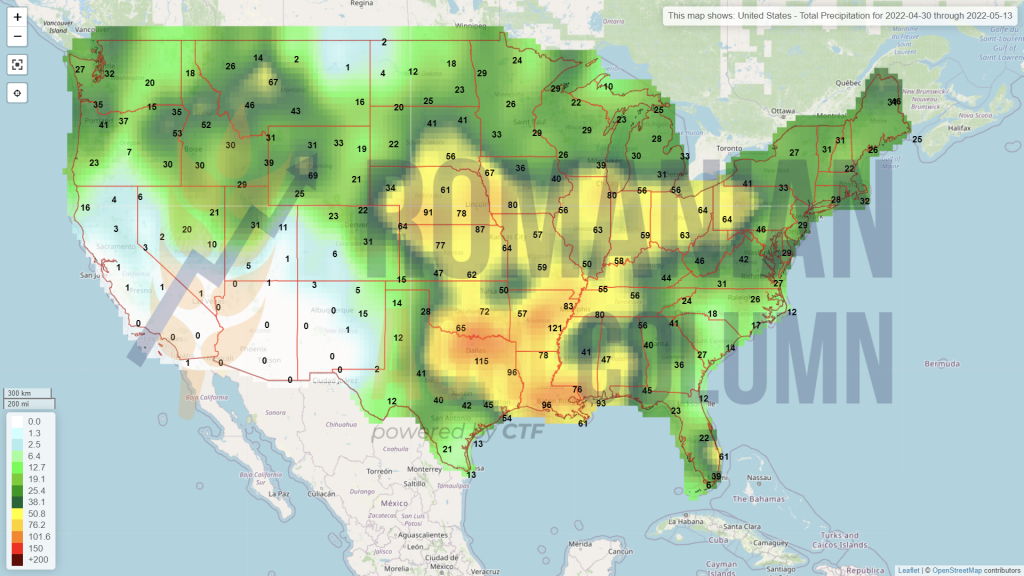

On the North American continent, we have once again confirmed the problems of the United States in terms of wheat crop. If a week ago its rating was 30% good and very good, the degradation continues, the reports indicating a level decreasing by 3%, up to 27%. In addition to this, which will lower the harvest volume forecast, we also have a delay in sowing spring wheat. According to reputable analysts, the percentage will drop to 25% next week due to very strong winds.

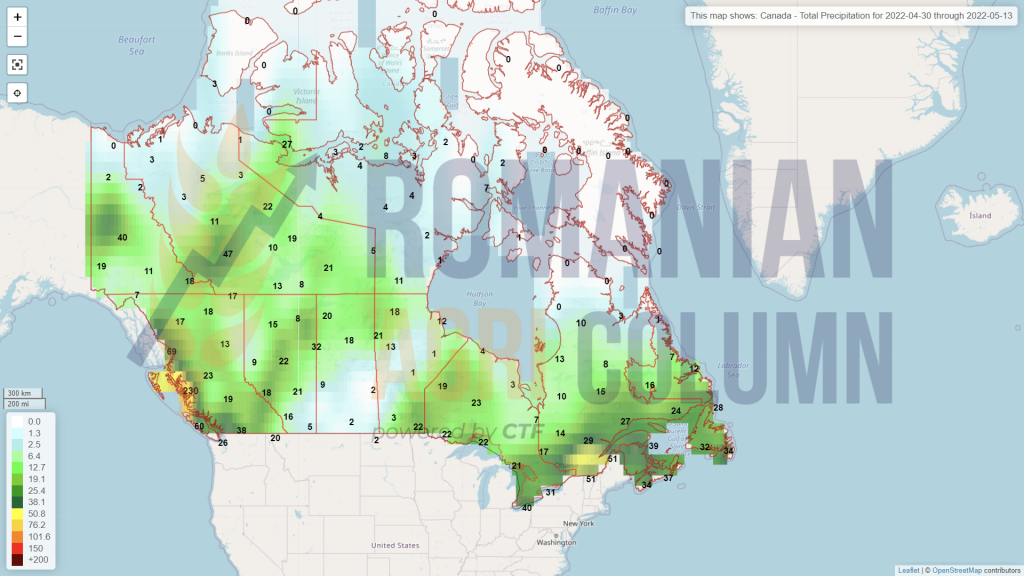

Canada indicates an increase in wheat acreage to 19.2 million hectares, including durum wheat. Of the total area, 13.85 million hectares is the area sown with winter wheat, as it is called on the North American continent. To this area we add 4.54 million ha sown with spring wheat. At the moment, about 16% of the surface is in severe drought, out of a total of 69% of the surface that is in an accentuated hydric stress. The weather will be the key to Canadian wheat production, estimated at 29 million tonnes at the moment. Major areas of Canadian wheat production are in Saskatchewan (45%), the provinces of Alberta (32%) and Manitoba (15%). Ontario is still on the list with 6%.

Argentina will reduce the area of wheat in 2022 from 6.7 to 6.5 million hectares. This will automatically lead to a decrease, but not a dramatic one, in the wheat crop. In the 2021-2022 season, Argentina’s wheat production reached 20.5 million tons.

India and Pakistan will be below 48-50 degrees Celsius in the next period, until April 30. We remind you that the harvest is in full swing for wheat, but the crop forecast is already reduced to 107-108 million tons. From what could the area supply the replacement for export? Kharif, the second corn crop, is sown from March to the end of July and represents 80% of production (total production Rabi + Kharif = 32.5 million tons). There will be problems here, for sure. In Pakistan, wheat harvesting began in April and lasts until mid-June. In total, the forecasted wheat crop is 27.5 million tons. Maize is sown from now until mid-August. Pakistan does not excel in corn production (maximum 8.5-8.7 million tons per season).

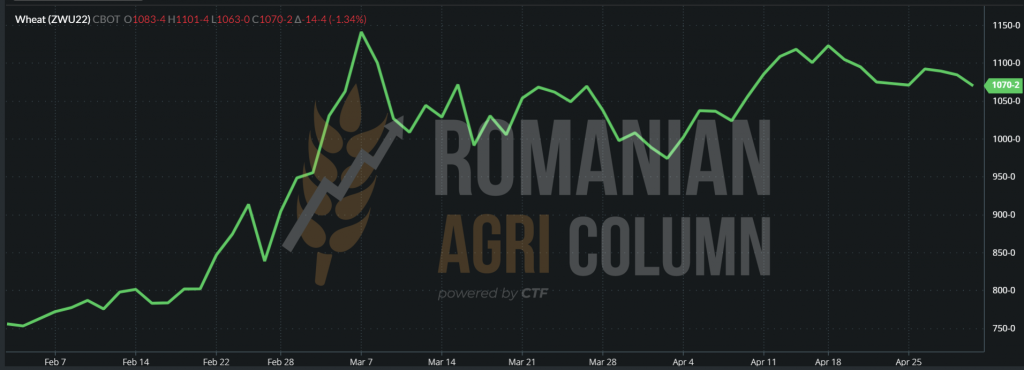

CBOT is performing the same exercise as Euronext, changing positions for MAY22. Once again, we notice the crop inverse in favor of the new crop: 1,056 c/bu MAY22 vs. 1,068 c/bu SEP22

WHEAT CBOT ZWK22 MAY22 – 1,056 c/bu (-17 c/bu) | ZWU22 SEP22 – 1,068 c/bu (-16 c/bu)

CBOT ZWU22 SEP22 WHEAT TREND GRAPHIC

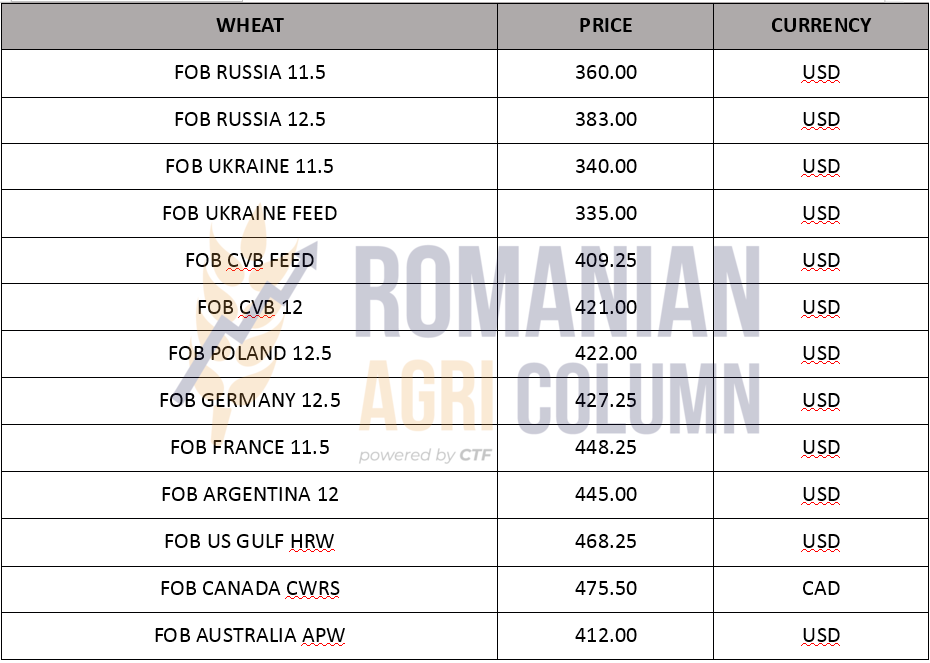

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

ANALYSIS

- The wheat crop is shrinking in volume. Ukraine is effectively trapped by Russia which destroys bridges across the Dnieper. The volumes that could cross to the ports near the Danube or to Giurgiulesti for transboard have no other option than in the scenario presented above.

- The US wheat crop continues to deteriorate. Moreover, the north of the Central Plains is exposed to very low temperatures as well as snowstorms, which leads to delays in sowing spring wheat.

- Canadian forecasts indicate problem areas at this time, but snow is a factor in delaying spring sowing, as in the northern United States.

- Argentina, by reducing the area destined for wheat sowing, will implicitly generate a lower production, which will, in turn, be included in the production decreases at the level of the North and South American continents.

- Demand remains within the same parameters and its consolidation will be governed by the weather and political factors. However, the political one shows us a dimension that will extend over time, so the pressure on volumes will remain constant from this point of view.

- The tender in Turkey is of Russian origin. How else? Small ships pass through Kerch and reach the Turkish coast.

The old barley crop has indications from only one buyer in the port of Constanța, at the level of 300 EUR/MT. Regarding the new crop, we see indications of 315-320 EUR/MT, a sign of the approaching time of delivery by companies that sold before the war in Ukraine and now must be covered. Our presumption is that problems will arise. Barley is not listed on the Stock Exchange, for a risk instrument such as a PUT to be used. Therefore, the price difference between the time of sale and the time of actual delivery could be significantly negative for the exporter. In this way, we encourage farmers to honor their signed barley contracts. It is a norm of maturity and a sign of trust between the parties participating in the agribusiness market.

LOCALLY

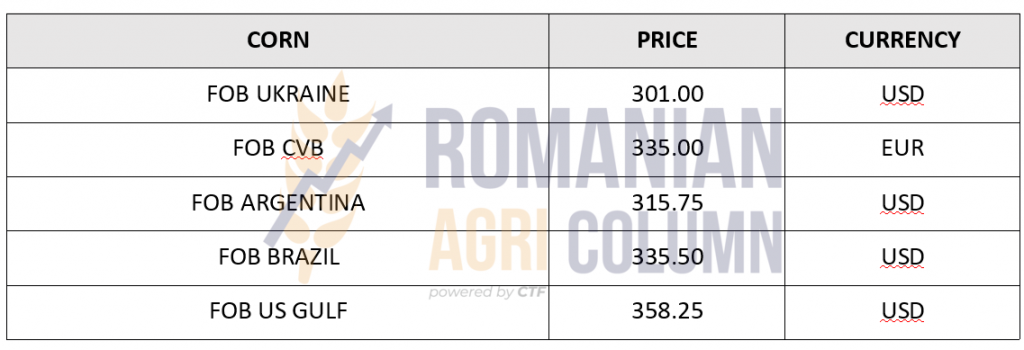

The old crop is traded around 320 EUR/MT in the CPT Constanța parity and is in agreement with the FOB market, which is at the level of 330-335 EUR/MT FOB CVB. The new corn crop is quoted, but on a wider price range. It is offered between 295-315 EUR/MT in the CPT Constanța parity.

Romania’s export level for the 2021-2022 crop was on April 26, 2022 at 3.72 million tons, but we can certainly add another 200,000 tons to this threshold. There is a difference in the collection of data which causes them to be aggregated late.

Romanian farmers still have to sow corn, but we see how the delay is dictated by the rainfall that fell in the last week and, of course, by the prolonged holiday on the occasion of the Orthodox Easter. In addition to this aspect, we can see a decrease, not very pronounced, of the area destined for corn in favor of sunflower crop, from an intention of 2.63 million ha to 2.58 million ha.

But the month of May is decisive. Precipitation will make a difference in Romanian corn production. And the precipitation register shows us a continuity, until May 13, 2022 at least.

REGIONALLY

Ukraine is sowing corn at a slower pace than last year due to the war in its territory. As of April 29, progress was 0.77 million ha. Last year, 1 million ha were sown in the same period. We remind you that the area sown last year was 5.4 million ha, and this year’s estimate is 3.3 million ha.

Ukrainian prices for the old corn crop are discounted due to the need to sell and the VAT tax regime. The price offers in various parities can be found below.

We also remind you of the existing roadblocks and the extremely large number of wagons blocked at the border (5,185 waiting wagons) and the 20-day border transit rate. It is not easy or convenient for anyone. This situation is very confusing. The number of waiting wagons totals about 360,000 tons of cargo.

EURONEXT has the same CBOT-influenced activity, which also liquidates MAY22. But the differences are not as great as in the case of wheat. We only see an inverse of 21.5 EUR between JUN22 and NOV22. The old corn crop still has a life cycle. The demand exists and we will see this in May. Then, as the harvests evolve, we will see how the certainties will generate a pressure on the price of corn.

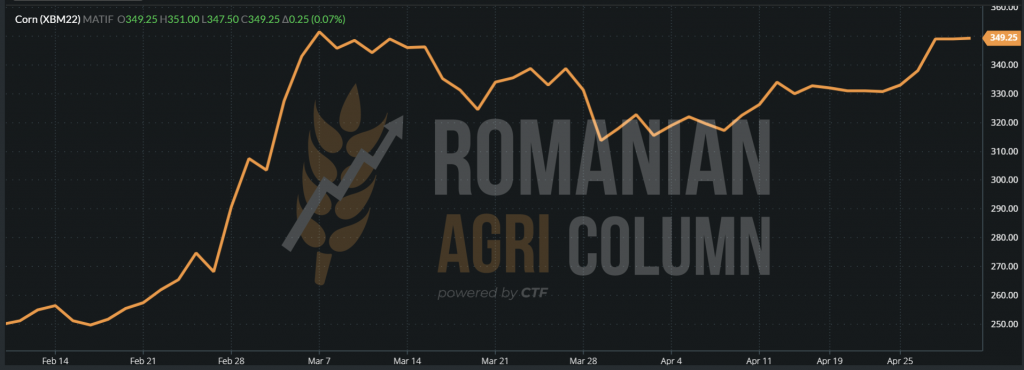

CORN – EURONEXT- XBM22 JUN22 – 349.25 EUR vs XBX NOV22 – 327.75 EUR

We notice the peak reached at this moment, a sign that the peak level generated by the war factor Ukraine has been found. It’s a good sell-off for stockholders.

May will define the request. However, China buys a lot from the USA and they also have a lockdown, which limits consumption. This lockdown also creates an extreme logistical deadlock in China’s port areas. In other words, China, through this lockdown, generates or at least wants a reflux of the price of corn.

XBM22 JUN22 EURONEXT CORN TREND GRAPHIC

GLOBALLY

BRAZIL is beginning to raise serious questions about Safrinha, the second corn crop. Persistent drought will bite into its promising potential. During this period, rainfall was about 40% lower than in a normal year. This is not a pleasant situation, especially in the Mato Grosso region. A rough estimate indicates a minus of 8-9% of Safrinha’s potential.

At the same time, extremes exist. Windstorms and hail destroyed a large area of corn from the second crop in the pollination phase in western Paraná. These events are common at this time of year, but in a localized way. The other day, the range was hundreds of miles.

The US has long delays in sowing corn (7% of the total area, 9% less than last year), but it is not too late. The delays are caused by snowstorms in the northern United States. The rhythm will definitely recover.

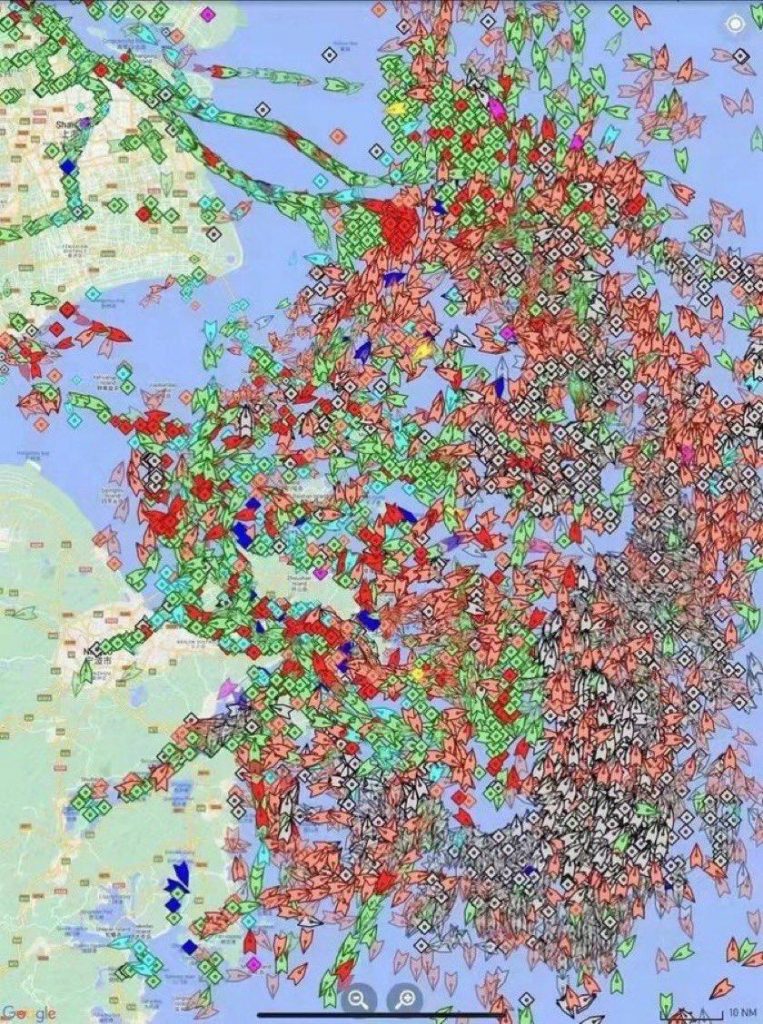

CHINA also has delays in sowing corn. Prolonged lockdown results in a shortage of labor in the field. During the winter, a large number of Chinese farmers work in cities, and at the moment, they are trapped in these cities without the possibility of leaving. Logistics creates great turbulence and this is already reflected in the availability of transport units globally. We insert a map of the agglomeration around the Chinese ports, for a good reflection. All dots, regardless of color, represent shipping units.

CBOT does not indicate turbulence due to the change of month. This is due to concerns about the Brazilian crop and the US delay in sowing.

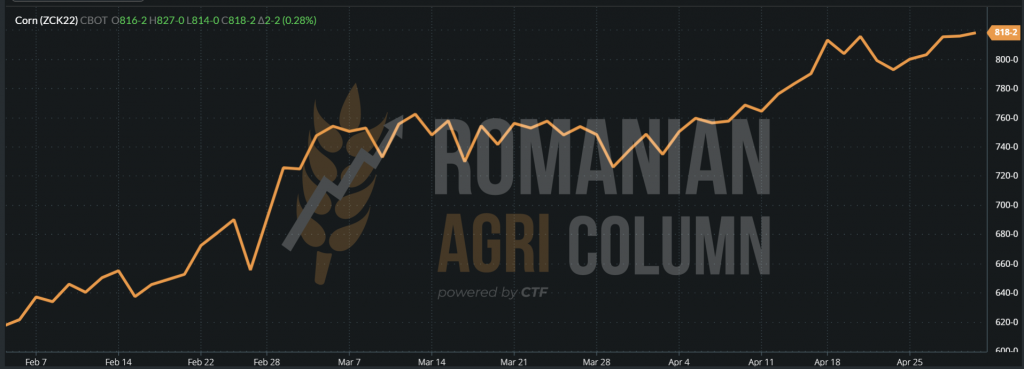

CBOT ZCK22 MAY22 – 818 c/bu (+ 2c)

As we can see in the corn chart, CBOT is at its highest level since the beginning of the Russian invasion. This gives a clear indication of sale, because the new crop is at the level of 751 c/bu, i.e. we have an inverse crop of 26.38 USD/MT. More precisely, the hopes in the new crop are in place and there are no problems.

ZCK22 MAY22 CBOT CORN TREND GRAPHIC

CORN INDICATIONS IN MAIN ORIGINS

ANALYSIS

- The old corn crop has supported demand. The US continues to record high sales to China and to unknown destinations, most likely in SE Asia.

- The premiere of the 100% local Comvex Terminal in the port of Constanța (the fastest in Europe), by loading a 71,000 ton Panamax with corn from Ukraine, based on the sale made by a Ukrainian company, is a start.

- The stability in CBOT is given by the premises of the second Brazilian crop, which indicates a decrease in potential by 8-9%, as well as by the delay in sowing the American corn.

- It is a high point in CBOT and EURONEXT. We are in a plateau phase, and the difference between corn and wheat is still large, considering the SEP22 wheat at the level of 380 EUR/MT and the NOV22 corn at the level of 327.75 EUR/MT. Will wheat raise corn? That’s what transactional logic sounds like. The difference of 52.25 EUR is significant at this time.

- May will generate a lot of answers regarding the course of the new corn crop. Ukraine will sow about 3.3 million hectares versus 5.4 million ha last year, but a large part of the 2021 corn volume is not yet exported. The US and Brazil are rather unknown factors at the moment, but by the end of the month we will have definite answers.

- Romania will also generate answers towards the end of the month. The precipitation will give a note about the Romanian production potential.

LOCALLY

The indications of the port of Constanța were given around AUG22 minus 5 EUR or, in some cases, AUG22 is the norm of purchase. Processors, in turn, indicate the level of AUG22 minus EUR 5, which clearly indicates the development rate for local rapeseed.

With a total of 417,000 hectares sown in the autumn, our estimates of the area re-sowed do not lead to a decrease of more than 25,000 hectares nationwide, i.e. areas converted by re-sowing with spring crops.

Rapeseed is flourishing and the local landscape has changed with the appearance of the gorgeous shade of yellow these days. It is the sign of spring that has settled, although rainfall and low temperatures have not allowed the more advanced development of the plants. We estimate that in the case of maintaining low temperatures, we may see a delay in development and implicitly a delay in harvesting.

REGIONALLY

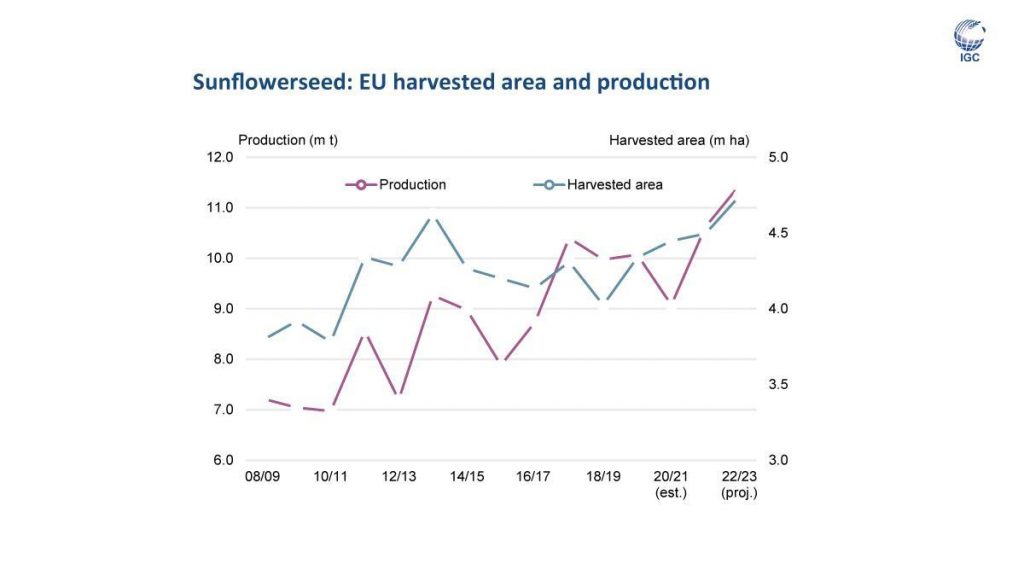

The European Union maintains its production forecast level at figures exceeding 18 million tons. The estimated value is 18.3 million tons, with minor problems due to the winter frost in some areas of northern Europe, but the overall picture is optimistic.

The turmoil is coming from Ukraine, which is facing difficulties that we all know, because of the war being waged on its territory. The decrease in production will implicitly generate a smaller harvest volume, around 2.88 million tons, while last year they registered a level of 3.4 million tons. We add to the low production and the very difficult export process, whether it is crude oil, crushed oil or raw material.

At the moment, however, we also have natural questions about the future of rapeseed oil. Under the current conditions in which the EU suffers from the supply of vegetable oil of Ukrainian origin, will the shortage be replaced by compensation or mixing with rapeseed oil? It is a question that generates a lot of discussion, knowing that rapeseed oil is intended for biodiesel. The paradigm of 2005-2007 returns, namely, what do we prefer? Food or transportation? The indications are that if the supply cannot be supplied, a substantial part of the crude rapeseed oil will be taken away for human consumption. It is not a novelty, the blending between sunflower and rapeseed oil existed in the 80’s, and the resumption of this way of supplying the demand will not create any discomfort, knowing the beneficial qualities of rapeseed in the context of mix.

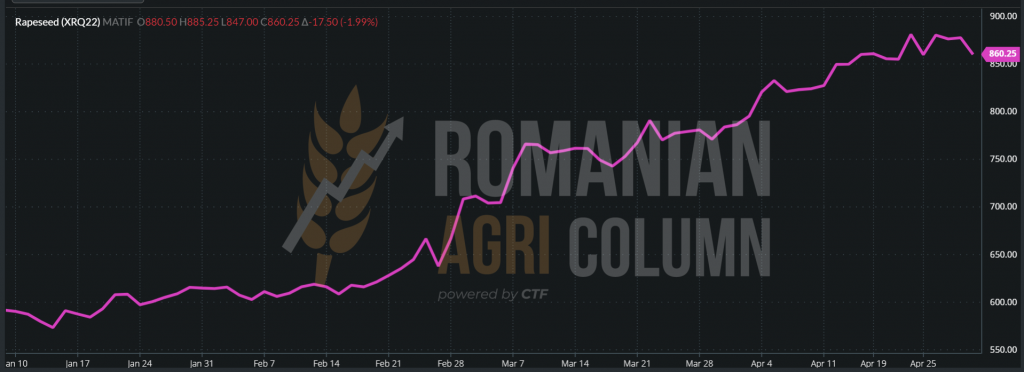

EURONEXT closes MAY22 sharply lower. Subsequently, AUG22 is corrected by 17.5 EUR in the negative. It is nothing more than the effective liquidation of open positions as early as MAY22. I have been emphasizing since April 20 that this moment will come. However, from Monday we will report directly to AUG22, the new crop being the trading parameter.

EURONEXT XRQ22 AUG22 – 860 EUR (-17,5 EUR)

RAPESEED TREND GRAPHIC – XRQ22 AUG22

GLOBALLY

CANADA reduces the surface of canola (Canadian Oil Low Acid – genetically modified rapeseed to reduce erucic acid content). Thus, the area sown with rapeseed is indicated at the level of 8.46 million ha from 9.05 million ha. So we have a gap of 592,000 acres in Canadian canola crop.

AUSTRALIA sows canola in slightly higher areas than last season. But the positive differences, if any, will amount to a maximum of several hundred thousand tons, insufficient to offset global demand. If we also discuss logistics, I think it is very clear that the volume of Australian canola was destined for Asia.

The canola stock market reacts identically as in the case of Euronext, by liquidating the open positions in MAY22, but there it does not move to the new crop, but in JUL22. The canola harvest in Canada starts somewhere after September 10, so the NOV22 quotation is the one that indicates the new crop.

ANALYSIS

We have a global picture of rapeseed production, demand and supply, which will lead us to a demand and support for rapeseed in the next period, as well as at the beginning of the harvest, after which things will slow down for a while due to change in processing with sunflower seeds. This period will start in August, and the application will disappear from the radar until around November 2022. Then the processing intentions will be reversed, usually in December, but the processing units must be covered from the point of view of raw material.

LOCALLY

Indications for the old crop of sunflower seeds have tempered. Flows of raw materials from Ukraine, combined with those of crude oil, have directly influenced local prices. The level of 780-800 USD/MT is the one that is common these days. The port of Constanța offers the highest level of the range exposed above.

The new crop of sunflower seeds has tempered for a while, in terms of price level. The indications of the processors are at the level of 730-740 USD/MT for the goods delivered in DAP Processor. Naturally, farmers were very busy with sowing and the interest in contracting in advance did not exist at a high level.

For High Oleic sunflower seeds, the bonus indications for the 81-82% level are 30-40 USD/MT, at the moment. This indication shows the request from the European HoReCa which, in the conditions of raising the health barriers caused by COVID-19, reaffirms its request and, implicitly, its support. Under these conditions we can reach levels close to 70-80 USD/MT bonus for oleic acid content, between August and December 2022.

Farmers in many parts of Romania, but especially in the south, have faced extremely serious problems with the Tanymecus pest. Invasion is actually the definition of this attack on sunflower. The pest is in the larval stage in the soil, taking advantage of the remnants left over from the harvest, and the lack of precipitation, as well as the positive temperatures during the winter, favored its further development. Farmers intervened, but in many cases, the damage caused the crop to be completely reversed in some plots.

The rainfall and the coming ones do nothing but strengthen the belief in a good crop, in a profit that will cover the costs of setting up. The level of sowing estimated in Romania at this time certainly exceeds 1.3-1.35 million hectares, and if the rainfall will feed the plants, we can generate a crop level that is close to 3.8-3.9 million tons.

REGIONALLY

In Ukraine, the seeding rate is very slow. The problems facing farmers are related to the sowing areas which are exactly in the regions where the battles take place and the areas where the front is located. Planting intentions are 4.4 million ha, compared to 6.8 million ha last year, with an estimated crop of 10 million tons, compared to last year, when figures close to 16.7 million tons were recorded.

Forecasts at EU level also indicate the strength and development of sunflower areas to counteract the adverse effects of Ukraine’s inability to deliver. Source: IGC.

What we need to keep in mind in the current context is that Indonesia has completely restricted the export of palm oil, whether it is refined or crude oil. This has disrupted the VEGOIL complex. However, things have not skyrocketed in the European region due to the cultural specificity of sunflower oil consumption and the fact that the European Union does not approve of palm oil due to deforestation and working conditions.

However, we see a jump in crude oil prices of 50-70 USD/MT for processors in Turkey and Bulgaria. Turkey has completed a tender for the purchase of 18,000 tons of crude oil with an average purchase price of 2,000 USD/MT, CIF delivery in Mersin and Tekirdag, May 16 – June 16, 2022.

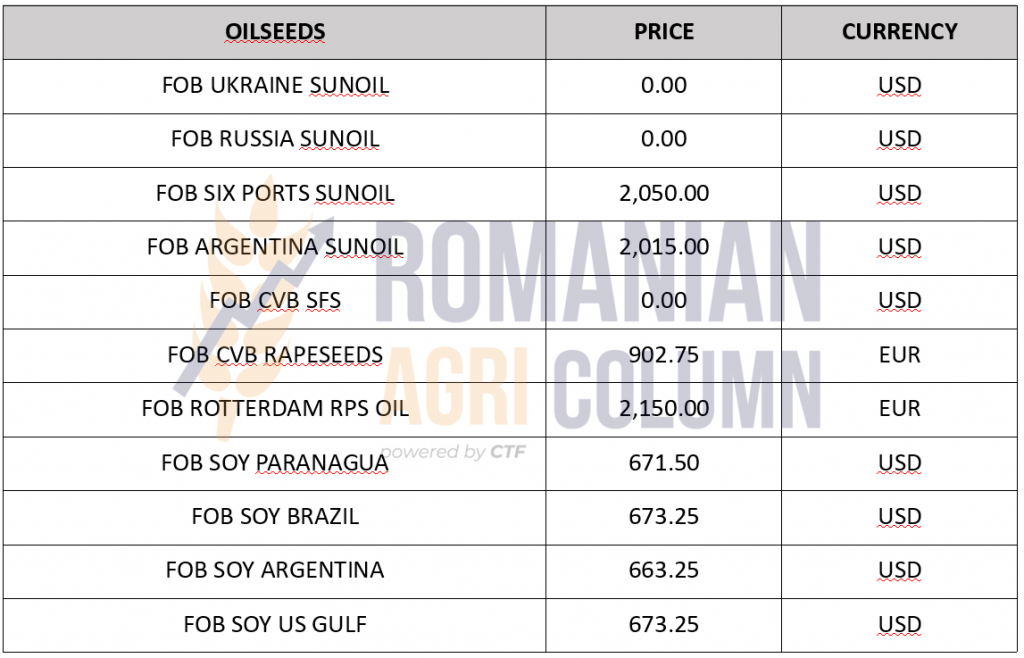

CSFO AND OILSEEDS INDICATIONS IN MAIN ORIGINS

ANALYSIS

- Competition for sunflower seeds will be generated by EU demand.

- Turkey will also be a player in the demand for raw materials.

- Russia will sell at the expense of Ukraine to India, so the volume there will be replenished.

- Russia will also sell in Turkey, the latest tender certainly having Russian origins.

- Things are calm today, but development will come along.

LOCALLY

Domestic processors are not currently showing any interest in soybeans. No price indication and no purchase. Identically, for the possible lots that were offered in the riparian countries, there is no interest for soy at this time.

The soybean area forecast to be sown in Romania amounts to 175,000 hectares. At a simple calculation, this area could generate a level of about 525,000 tons in harvest volume. However, the road is long and soybeans are a water-demanding plant, so only irrigated areas are sown with soybeans in 2022.

GLOBALLY

The United States continues to sell soybeans in large volumes to China. For weeks on end, sales exceeded forecasts. As for the pace of sowing in the US, it is lagging behind. The current estimate is 3% of the area, compared to 7% last year. However, recovery will be easy after bad weather.

ARGENTINA announces a reduction in processing to 38.7 million tons. The decrease comes from the reduction in the demand for meal in Paraguay.

BRAZIL is nearing the end of its soybean harvest. The other day, the harvest was at 96-98%.

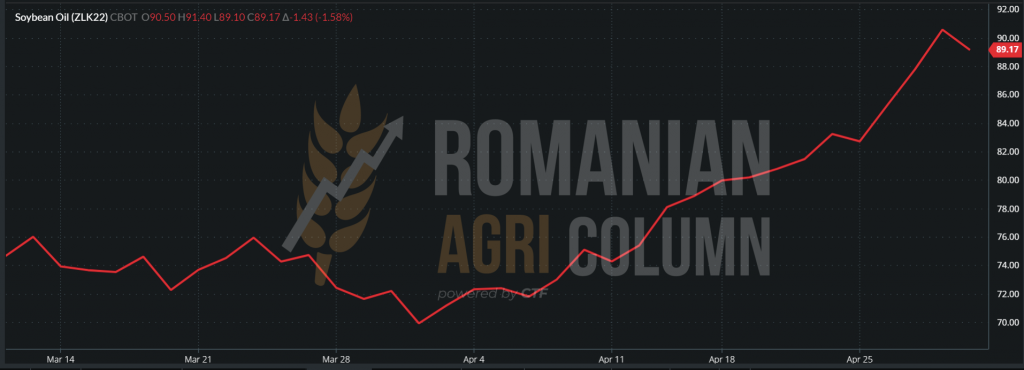

The Indonesian export restriction on palm oil has pushed up the price of soybean oil in the VEGOIL complex.

SOYBEAN OIL TREND GRAPHIC – ZLK22 MAY22

CBOT remains in support of soybeans. Let us recall the latest WASDE report which better outlined the South American problems and low soybean stocks globally.

CBOT SOYBEANS ZSK22 MAY22 – 1,708 c/bu (even on the last trading day MAY22 soybean remains strong)

ANALYSIS

- Soybeans remain a major global focus, mainly due to declining stocks and production.

- Delays in the US will be recovered, but the biggest enemy will be the weather beyond the summer of 2022.

- In Romania, demand will not return too soon. Processors are already focused on the new rapeseed crop, which will arrive in a maximum of 45 days.

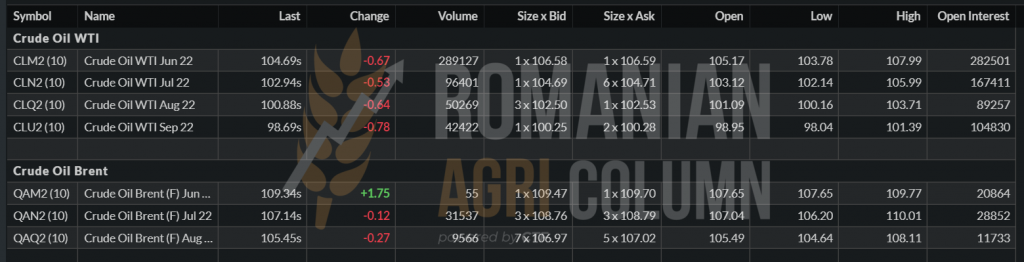

EUR/USD 1:1.05 | USD/RUB 1:71.34

BRENT and WTI are on the rise again. BRENT $ 109.34 | WTI $ 104.69

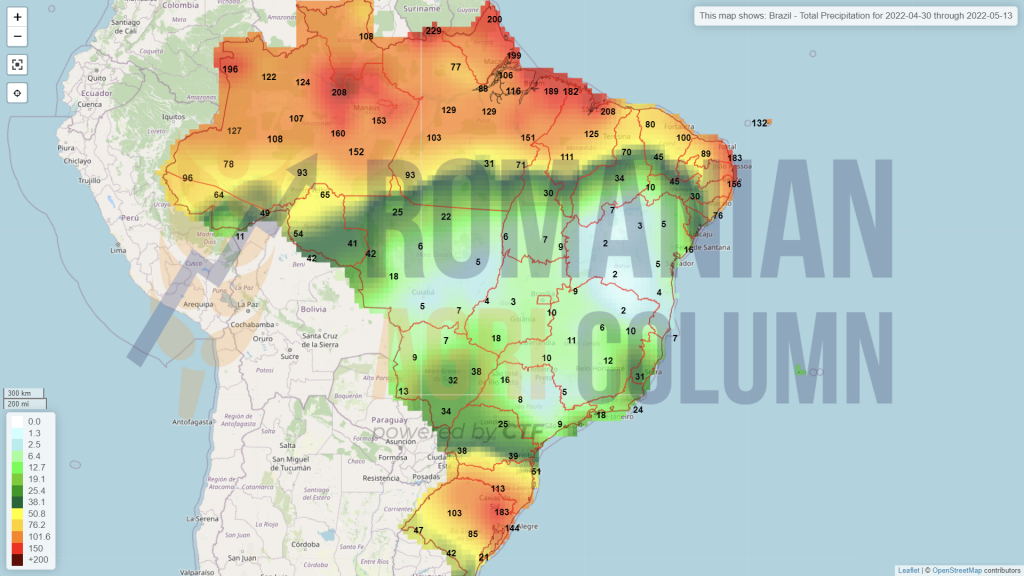

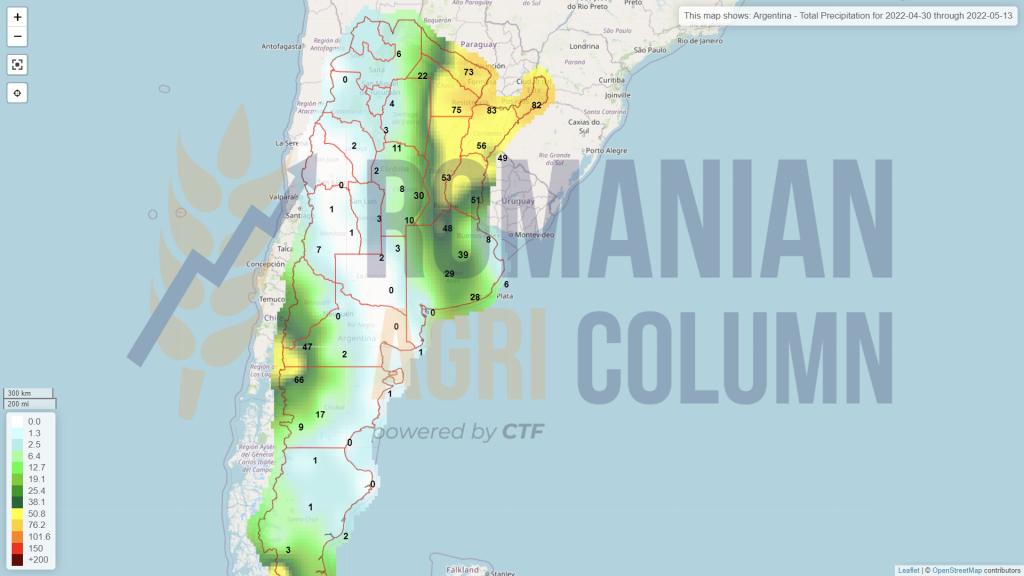

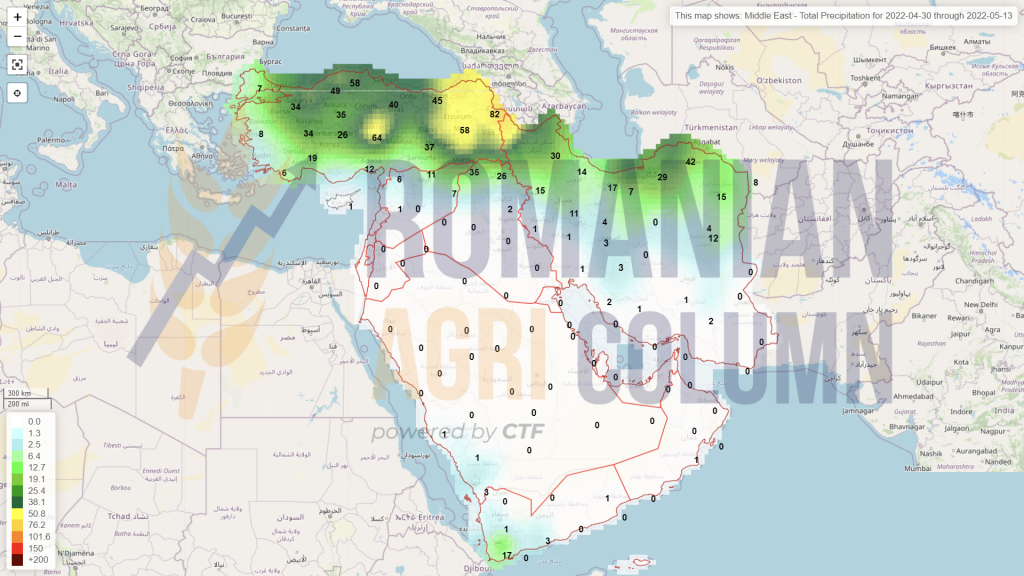

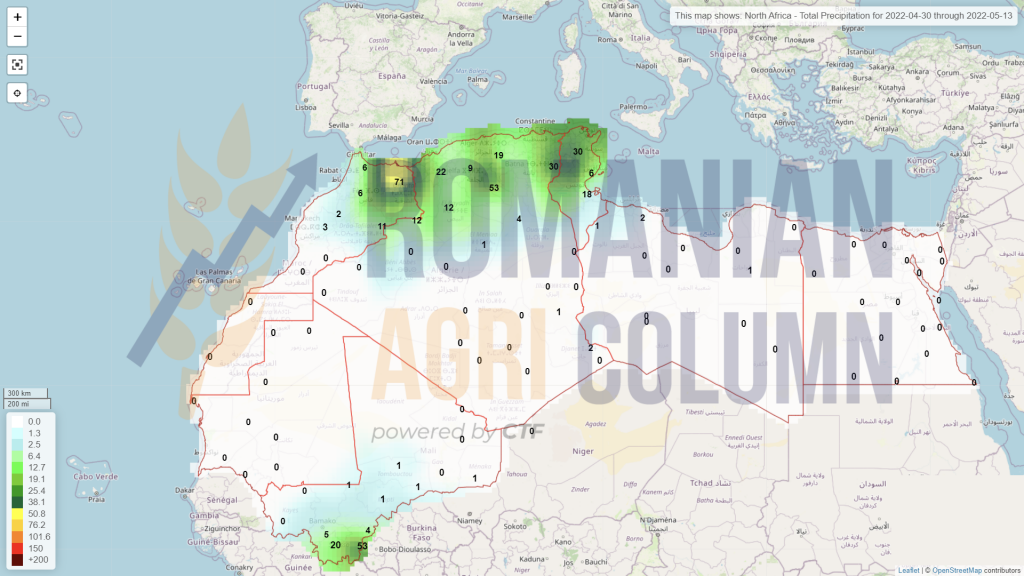

April 30 – May 13, 2022

Romania

Europe

Ukraine

Russia

Canada

USA

Brazil

Argentina

Middle East

North Africa

China

Australia