Cezar Gheorghe, the author of AGRIColumn, and the editorial team express their pain and solidarity towards the Turkish people, who are hardly tried and pained by the loss of human and material lives. The Turkish people are wonderful, with warm hearts, with an open soul and always with a smile on their face. Our soul is full of pain and compassion for these wonderful people and for this beautiful country, which we know and visit every year since 2007.

You will come back, you will be reborn, and you will be strong, just like Turkey is, a beautiful country full of serene hearts and wonderful people.

Romanian Agri Trade Summit, one of the largest events addressed to International Agribusiness, will take place on February 22, 2023 in Bucharest.

The initiative aims to reconfirm Romania’s strategic role in global agribusiness and to bring together the most important players in the dynamic grain market – top Farmers, Traders, Processors and Distributors.

This week’s market report provides information on:

LOCAL STATUS

The indications of the Port of Constanța agree with the Euronext benchmark and we see how they start to increase by 4-6 EUR/MT on average. Thus, the level may also reach 281 EUR/MT at some points.

The new crop sales level remains agreed in the same formula linked to Euronext and the agreement is reflected in the level of 253-255 EUR/MT for new crop wheat deliveries in CPT Constanța parity.

CAUSES AND EFFECTS

The increase of 4-5 EUR/MT was expected in light of the latest statements by Russia as well as ground movements in the Luhansk region. They are also generated by the movements created by the latest international tenders, as well as by a volume of 500,000 tons sold for export by the US in the last period. It’s a breath of fresh air for the US, given its extremely poor sales results.

It’s typical of this time of year and it’s a time when things start to move. The grain corridor will expire on March 19, 2023, and the Russian style is starting to make its presence felt with veiled threats that they are unhappy and that Russia has not benefited from any incentives in this agreement. The stimulus required by the Russians was somewhat separate from the subject. They wanted and still want the liquid fertilizers to transit through Ukraine to a port terminal to be exported, because through Russia it is not possible, because of the sanctions. But this old subject can only be achieved through certain parameters that must be respected. The first is for Russia to release many prisoners of war from the Mariupol-Azovstal area, and the second for an American company to take control of these fertilizer flows in a logistical and distribution sense. It’s just that Russia doesn’t want to release the designated prisoners, and Russia now also has the same set of fertilizer and payment sanctions.

Romania, however, in this whole picture, indicates a major weakness and, if the Romanian farmers do not want to sell the wheat between now and March 25-30, 2023, Romania will not be able to fulfill its export volume. Therefore, we will be left with a volume of 1.5-1.8 million tons unsold from the 2021-2022 crop, which will weigh heavily on the price of the new 2023 crop.

Romania has so far exported a volume of 2.28 million tons of wheat and has an import level of 700,000 tons. Only farmers can solve this status. Any delay will generate financial costs and problems in raising the price of the new 2023 crop.

REGIONAL STATUS

RUSSIA. In the reporting week to February 8, wheat volumes from four deep-sea Russian ports (Novorossiysk, Kavkaz, Taman and Tuapse) reached 866,915 tons, with Egypt the main destination, with around 337,050 tons of wheat heading to this country.

Egypt was followed by Turkey with 146,310 tons, the United Arab Emirates with 81,300 tons, Pakistan with 67,410 tons, and 63,000 tons went to Greece, while about 50,000 tons were listed as being directed to Bangladesh, South Africa, Israel, and Libya.

In addition, port line data showed that about 1.8 million tons of Russian wheat is currently loading and due to depart before mid-February.

The data did not mention any destination for most of the declared volumes of 903,350 tons, while Egypt was reported as the destination for 191,000 tons of wheat, Yemen for 187,200 tons, Pakistan for 118,408 tons and Turkey for 101,200 tons.

In addition, some smaller consignments of around 60,000 tons were destined for Sudan, Bangladesh, Saudi Arabia, Tanzania, and Libya.

UKRAINE is nearing the end of its wheat volume for export. It exported 9.89 million tons of wheat. The total volume of grain exports since the beginning of the 2022-2023 marketing year is 27.69 million tons (29.4%/11.520 million tons less than in the same period of the previous marketing year).

THE EUROPEAN UNION exceeds 19 million tons of exported milling wheat volume. Bringing in durum wheat, as well as derivatives calculated in tons, we arrive at a volume of 20 million tons exported. In terms of imports, the Union exceeded the barrier of 5 million tons. Cumulating durum wheat and derivatives, we arrive at around 6 million tons.

Weekly wheat exports from the European Union fell to 166,621 tons in the week ended February 6, down 44% from the previous week, according to European Commission data released on Tuesday.

The previous week’s total was revised up by 15,870 tons to 300,555 tons.

The total figure for wheat exports for the current marketing year now stands at 19.04 million tons or 6.7% above last year’s rate. In the reporting week, the main exporter of wheat was Poland with 65,780 tons, France with 34,012 tons and Romania with 31,642 tons.

Morocco was still the main end point for EU wheat, with 2.76 million tons purchased. Morocco was followed by Algeria with 2.6 million tons, Egypt with 1.6 million tons, Nigeria with 1.56 million tons and Saudi Arabia with 982,270 tons.

EURONEXT – MLH23 MAR23 –297 EUR

EURONEXT WHEAT TREND CHART – MLH23 MAR23

GLOBAL STATUS

USA. At just 1.08 million tons, US wheat exports in December were the lowest for ANY month since January 1972 and the lowest for December since 1967.

CANADA. Wheat exports totaled 354,700 tons, down 10% from last week, but cumulative exports are up 69% to 10.3 million tons. The weekly pace of durum wheat exports was 97,100 tons, down 49.5% from the previous week, but total exports for the current marketing year stand at 2.8 million tons, more than double the from last year, 1.3 million tons. Statistics Canada reported December 31 wheat stocks ->22.3 million tons (up about 1/3 from last year’s 16.8 million tons)

ARGENTINA is out of season.

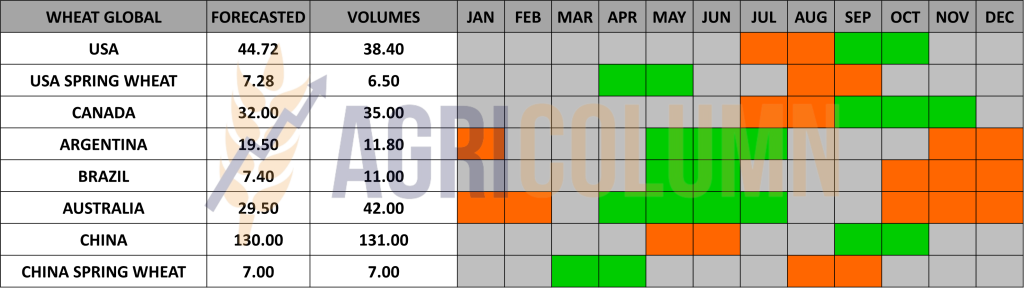

AUSTRALIA is starting to be recognized by the USDA and we are seeing its volume forecast start to rise to 38 million tons. Of course, this forecast is not final, and we will see positive revisions to the Australian crop.

CBOT WHEAT – ZWH23 MAR23 – 786 c/bu

CBOT WHEAT TREND CHART – ZWH23 MAR23

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

TENDERS AND TRANSACTIONS

MIT JORDAN has canceled its tender for 120,000 tons of wheat from 7 February 2023.

OAIC ALGERIA has so far purchased approx. 400,000 tons at a level of 329-332 USD/MT CFR. The final estimate could be 500,000 tons. The origin is optional, but at this price, it appears to be a large Russian part.

CAUSES AND EFFECTS

Extract from the previous issue of AGRIColumn 5/2023:

“Only the expansion of the conflict on the ground will give a boost to the price of wheat, but it will be short and intense. But then, seeing the aggregated factors (volume of goods, energy price, fertilizer price, old stocks), there is only one indicator: The only way is down, back to where we came from.”

TODAY

Russia will leave the trenches and try to attack before the tanks and other equipment arrive. The weather in Ukraine is dry and icy, so conducive to ground attack. The thaw is a major disadvantage for the Russians.

The winter offensive, so to speak, has already begun, with ground attacks in 5 directions in Luhansk, all coordinated with a missile attack, about 70 in number, on Ukraine. The targeted areas were also those very close to the border with Romania. The information leads to the fact that a Russian missile swept 35 km north of Romania’s border, then straightened its trajectory towards Ukraine. It’s a signal to NATO, for sure.

Simultaneously with the Russian statements addressed through the TASS agency, the classic propaganda, in which they try to show that they are the masters in the Black Sea and can blackmail the trajectory of Ukrainian goods, the Kremlin’s house analysts begin to show their arrogance and influence on the markets. The classic Maskirovka was set in motion. It was logical for it to happen this way, but we must not fall prey to Russian disinformation and games. We have learned it and recognize it too well.

On February 10, 2023, the movements on the stock exchanges also began. The massive liquidations for March 2023 are approaching and the intense activity is seen to be augmented by what is happening regionally. We will also see intense roll-over activity, the classic moves in the subsequent month, i.e., MAY23.

On a local level, Romania is in maximum delay regarding the wheat export forecast for this season. Our estimates lead to a volume of at least 1.5 million tons that will remain unexported. It is volume that will create difficulty in finding potential high value from a price point of view, alongside the new crop on the horizon, a crop that presents itself under favorable auspices at this time.

SUMMARY

THERE WILL BE A WINDOW OF OPPORTUNITY THAT WILL NOT LAST FOR VERY LONG.

The engagement on the ground will not be able to be sustained for long by Russia. This massed human resources and logistics in Mariupol. They also have a reserve in Belarus, but this will only be used for diversion and distraction.

Stock markets have already bought into the headlines and are reacting, the CBOT in particular with an increase of 11-11.5 USD on the MAR23 indication.

As the ground offensive continues, the weather will play the role of referee. Today is cold and dry. The heating will not support the movement of Russian or Ukrainian armored vehicles. When the Russians leave the trenches, they will be overexposed.

We must remember that the wheat is in Russia and the latter will have to sell wheat at any price. The fact that they increased the fee is irrelevant. It only affects the Russian farmer and nothing else. This infamous tax actually supports the war effort. Russian wheat is quoted at 300 USD/MT in FOB parity.

The sum of the above is also complemented by the EUR/USD parity. The US dollar is gaining momentum and we have the indication of 1:1.067. At 318 USD/MT FOB Constanța, it translates into 298 EUR/MT higher than the previous day’s 1.09 parity by 6.3 EUR/MT. Correlating the indications, we arrive at a level of 284-286 EUR/MT for the goods delivered these days in the CPT Constanța parity.

LOCAL STATUS

Feed barley price indications are stagnant around 242-244 EUR/MT.

REGIONAL STATUS

UKRAINE exported 1.83 million tons of barley. The total volume of grain exports since the beginning of the 2022-2023 marketing year is 27.69 million tons (29.4%/11.520 million tons less than in the same period of the previous marketing year).

THE EUROPEAN UNION exported 4,059 tons of barley in the reporting week, bringing the total for the marketing year to 3.16 million tons, down 40.1% from last year.

Since the start of the new marketing year, Saudi Arabia has bought 1.03 million tons of barley from the EU, while China has reserved 527,287 tons, Jordan 402,551 tons, Iran 350,419 tons and Tunisia 254,215 tons.

BARLEY PRICE INDICATIONS IN MAIN ORIGINS

GLOBAL STATUS

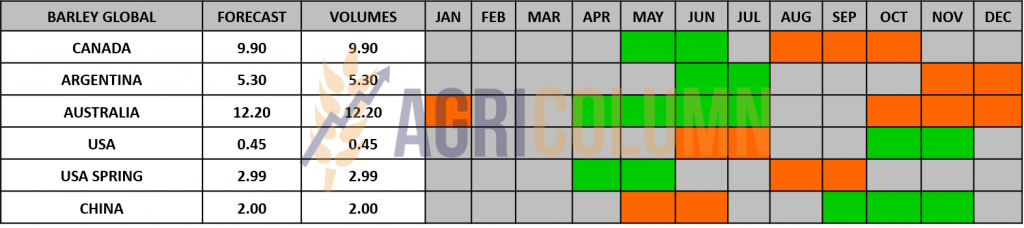

CANADA. Barley exports for the week totaled 47,400 tons, with cumulative exports at 1.7 million tons, up from 1.6 million tons last year.

AUSTRALIA. Australian feed barley gained around 10 USD/MT FOB over the past month, with the complex underpinned by renewed expectations of a near-term return of Chinese buyers, while recovering wheat prices added further interest.

Bids reached 285-290 USD/MT FOB WA for March shipping, compared with ideas heard around 270 USD/MT in mid-January when first rumored as China eased its unofficial import ban of Australian coal.

The apparent thaw in trade relations also comes as Australia-based industry sources expect the World Trade Organization to deliver its final report on China’s restrictions on Australian barley before the end of March. China used to be the main market for Australian barley before the restrictions were imposed in 2021, importing an average of about 2.3 million tons over the past five years before the ban.

LOCAL STATUS

Corn indications in the port of Constanța are at the level of 263-265 EUR/MT.

CAUSES AND EFFECTS

The corn shows the same consistency we’re used to, but it doesn’t find the traction it needs to climb further up the ladder. Surely it will find a support in wheat because wheat is a driver in the market. And given how the market manifests itself these days, we will certainly see slightly more generous indications compared to the previous days.

Romania shows no signs of recovery. It is in the same net importer status. MAR22-FEB23 volumes reached 1.15m tons as imports and an export volume of just 0.38 mil. tons.

REGIONAL STATUS

UKRAINE exported 15.85 million tons of corn.

The total volume of grain exports since the beginning of the 2022-2023 marketing year is 27.69 million tons (29.4%/11.520 million tons less than in the same period of the previous marketing year).

Maize guidance prices for February delivery from Black Sea ports reached 255-280 USD/MT FOB. Merchant purchase prices in the Odessa Greater and Danube ports increased to 190-220 USD/MT CPT-port (compared to 190-210 USD/MT CPT-port a week ago).

The EUROPEAN UNION reached the level of 17 million tons of imported corn, compared to only 9.88 million tons the previous season, on the same date. Ukraine has an export volume in the Union of about 8 million tons, the other big exporter in the Union being Brazil, with a volume of 7.4 million tons.

EURONEXT CORN – XBH23 MAR23 –291.75 EUR

EURONEXT CORN TREND CHART – XBH23 MAR23

GLOBAL STATUS

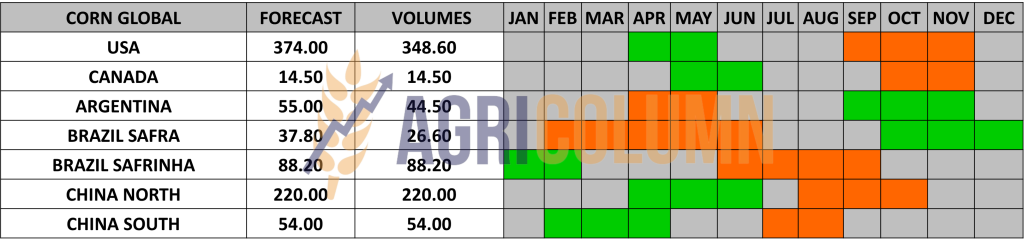

ARGENTINA. ROSARIO GRAIN EXCHANGE cut its corn production forecast to 42.5 million tons, down from last month’s forecast of 7.5 million tons – the lowest in five years and a decline of 15% to 50 million tons in 2022. The USDA said the average yield of 6,410 kg/ha was the fourth lowest on record in about 15 years, which comes despite huge technological advances in the production process of the crop, the increase in fertilization rates and the fact that late sowings represent almost 75% of the area sown nationally.

Meanwhile, for the 2021/22 corn crop, Argentine producers have sown 8.6 million ha.

“Unfortunately, since the middle of last week, stressed crops have been observed again,” the BCR said, adding that with “no significant rain expected for another 10-15 days and with another heat wave, the morale of producers has returned to despair”.

In the last WASDE report, the Argentine crop was reduced from 49.5 million tons to 45.5 million tons. Naturally, there is a discrepancy between the two reports of 3 million tons to be precise, but they will be adjusted as time goes by.

BRAZIL. CONAB cuts Brazilian corn crop to 123.7 million tons vs 125 million tons USDA January. Sowing is difficult due to late soybean harvest. Safrinha seeding level is 12%.

Parana, Brazil, increased the condition of the first corn crop, Safra, by 2% to 82% from the 74% average of the last 5 years, Safrinha, the second corn crop, at 4% seeding from the 15% average, soybeans 2% harvested vs. 11% average. Western Paraná must plant its second corn crop. The deadline is February 28. Soy is 30 days late. Math is not in favor of the farmers. We are on the 13th of February.

Brazil’s corn exports reached 4.9 million tons in January, above deliveries of 2.2 million tons in the same month in 2022 and in line with estimates from the association of grain exporters Anec, the association said in its latest report published on Wednesday.

Japan was the top buyer with 21%, followed by Colombia (11%), China and Vietnam (10%).

Last year, Iran, Japan and Spain were the main buyers of Brazilian corn.

Just a few months after the first cargoes were delivered in November and December, China became the ninth most important market, with 1.69 million tons purchased.

USA. Weekly net corn sales of 1,160,300 tons for 2022/23 fell 27% from the previous week but still beat analysts’ forecasts of 900,000-1.1 million tons, US Department of Agriculture data showed on Thursday ( USDA).

Weekly US corn exports of 394,900 tons were down 34% from the previous week, and cumulative exports now total 13 million tons – down 37% from 20.71 million tons at the same time last year.

SOUTH AFRICA. South Africa’s Crop Estimates Committee (CEC) released its final 2022 crop release on Thursday, putting the country’s corn production figure at 15.47 million tons, just 82,800 tons more than the last estimate.

The maize crop consists of 7.85 million tons of white maize and 7.62 million tons of yellow maize, harvested from 2.62 million hectares, with yields last reported at 5.87 tons/ha.

CBOT CORN ZCH23 MAR23 – 680 c/bu

CBOT CORN TREND CHART – ZCH23 MAR23

CORN PRICE INDICATIONS IN MAIN ORIGINS

CAUSES AND EFFECTS

Maize is still shown to be stable. The WASDE report showed that corn has the platform it is currently sitting on. Everything is played in South America. I come back with the wording “South American tango” because it is the expression of the moment.

Argentina is in trouble and is down dramatically to 42.5 million tons. Brazil also has problems in some areas. And what is not seen, is said. In some areas, trucks are stuck in mud for miles on the plains. They cannot move forward as they are effectively stuck on the rain-clogged roads. Soybeans therefore cannot be taken to warehouses to start sowing Safrinha, the second corn crop.

We are, for South America, in the weather market 100%.

But in the Black Sea basin, we are in the geopolitical factor.

Today we have apparent stability. But the traction on the part of the wheat can be seen and the tangent with the regional conflict will be pronounced, with the intensification of the fighting on the ground. Any penalty to the flow of Ukrainian goods by preventing it will automatically be reflected in the price.

Also, liquidations of EURONEXT and CBOT positions for the month of MAR23 begin. The translation by roll-over to MAY23 is also executed during this period. The demand is there in the physical market and will continue, but Brazil is playing its part on the stage at the moment, and the focus of the giant China is there for some time to come.

The three factors mentioned, weather market, geopolitics, and the speculative support corn on the same platform. Any change to either of the first two will work either way. If it is to be negative, i.e., improving conditions, it will reduce the price level and vice versa.

LOCAL STATUS

Rapeseed quotations in the port of Constanța were granted with the increase on EURONEXT. We thus have a level of 525 EUR/MT for the goods delivered in CPT Constanța parity. Processors remain at the same levels of MAY23 minus 25 EUR, i.e. 525 EUR/MT.

CAUSES AND EFFECTS

All quiet on the rapeseed front. It is further penalized by Australian and Ukrainian imports into the European Union. The shy growth was driven by only marginal traction from soybeans. However, an extra 5.5 EUR/MT is not negligible. There are still no premises for a dramatic decline, but signs of growth are delayed due to imports from the European Union.

EURONEXT RAPESEED – XRK23 MAY23 – 550.5 EUR

EURONEXT RAPESEED TREND CHART – XRK23 MAY23

REGIONAL STATUS

No change from last week in the European outlook, nor in Ukraine and Russia for rapeseed. The state of vegetation is in the same normal regime for this period. The coverage request is executed at a normal rate, referring to the processing units.

GLOBAL STATUS

CANADA, off season

AUSTRALIA, off season.

ICE CANOLA RSH23 MAR23 –832.2 CAD

ICE CANOLA TREND GRAPH – RSH23 MAR23

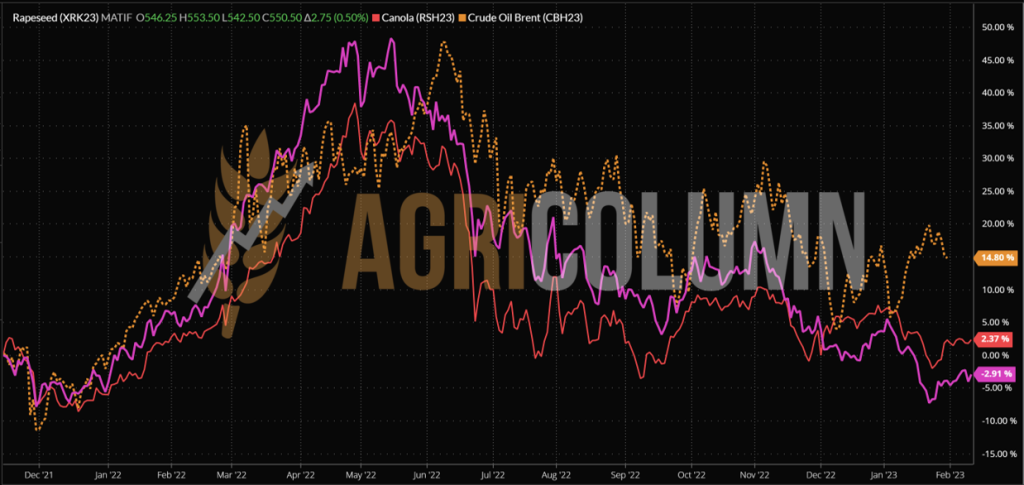

COMPARATIVE GRAPH. PETROL-RAPESEED-CANOLA CORRELATION

CAUSES AND EFFECTS

Euronext indications gained more consistency, up to the 550 EUR level. In the Canadian stock market, on the other hand, we will report from the Wednesday before to the month of MAY23. MAR23 will expire and what is happening there are liquidations of positions.

Romania reached 440,000 tons of rapeseed import from Ukraine in the period MAR22-FEB23. For a better picture, throughout the 2021-2022 season, Romania imported 54,600 tons. This also includes the period MAR22-June 20, 2022, when goods from this origin began to enter.

The European Union has reached an extremely high import level. About 1.7 million tons arrived from Australia. 2.6 million tons arrived from Ukraine, and 0.2 million tons entered the European Union from Canada. We have a total import of 4.62 million tons to date. Comparatively, last year in the same period, we had 3.18 million tons. The price of rapeseed oil FOB Rotterdam fell by 12 EUR/MT to 1,060 EUR/MT.

CONCLUSIONS

The European Union is supplied from alternative sources, and this keeps the price level of rapeseed low. But alternative sources can’t sell cheap either, so today’s level remains for a while. A helping hand came from fossil energy, which posted modest but still gains in BRENT and WTI benchmarks.

LOCAL STATUS

Constanța port quotes sunflower seeds at values between 550-560 USD/MT.

Processors are correlating and indicating a trading basis of 545-550 USD/MT at DAP Processing Units parity.

CAUSES AND EFFECTS

Sunflower seeds are at times when the geopolitical factor exerts more influence than weather or volumes. Today’s momentum is one that should normally curve the price or hold it at best. But the processors are not covered enough, and on the horizon we are looking at Ukraine. For if the conflict on the ground intensifies, then the supply network of raw material and, implicitly, of oil could be strangled. Different signs emanate from that area, each with its own partisan interests, so to speak. If the transmission network is strangled, then demand will certainly increase, causing a jump in price. A positive thing is the strengthening of the USD against the EUR and, implicitly, against the RON. In other words, the exchange rate is favorable and the same level in USD generates higher income in RON for one ton of goods.

REGIONAL STATUS

UKRAINE. Sunflower oil exports in the week to February 8 totaled 65,614 tons, down 23% from last week. Most of February’s volume of 25,243 tons was destined for China, followed by Turkey.

This distribution of volumes confirms market information about the increasing interest of Chinese buyers in Ukrainian sunflower oil, a dynamic that was also supported by several transactions during the current week.

Weekly sunflower seed exports fell slightly from the previous week to 42,634 tons in the reporting period, bringing total exports from the start of 2022/23 to 1.4 million tons.

RUSSIA has increased its domestic production of crude sunflower oil to 6 million tons in 2022, an increase of 14.3% compared to 2021, the country’s Federal State Statistics Service (Rosstat) announced. The same trend was seen in the production of refined sunflower oil, where production rose to 2.5 million tons, or 5% above the 2021 level.

However, due to a good sunflower seed crop and sufficient carryover stocks, Russian processors increased sunflower seed processing as low early season prices supported processors.

Crude sunflower oil production also increased in December 2022, reaching 602,000 tons and up 4% from the same month in 2021.

At the end of 2022, the Oil and Fats Union of Russia forecast that the country will likely see a 10% increase in sunflower oil exports for the calendar year.

The main reason for the expected boom in exports was that the sector capitalized on the Russian invasion of Ukraine, which effectively made it impossible for Ukraine to maintain its position as world leader.

But opinion was divided on the issue, with consultancy Oleoscope estimating the volume of Russian sunflower oil exports in 2022 to around 3 million tons, which would actually represent a 5% reduction from 2021.

In 2022, Turkey was the main importer of Russian sunflower oil, importing 840,000 tons.

Also, according to recently released Chinese customs data, the country imported 213,000 tons of Russian sunflower oil in 2022.

GLOBAL STATUS

ARGENTINA marginally decreases the export value of sunflower seeds, due to the reduction of the harvest by 50,000 tons.

PRICE INDICATIONS FOR OILSEEDS AND CSFO IN MAIN ORIGINS

CAUSES AND EFFECTS

In the February report, USDA experts lowered their sunflower production forecasts for Argentina and the Russian Federation. But analysts believe that in the next balance sheet, forecasts for these countries will be reduced again and the overall sunflower balance sheet for 2022/23 will worsen.

Compared to January estimates, the forecast for world sunflower production in 2022/23 was cut by 0.31 million tons to 50.77 million tons (57.31 million tons in the 2021/2021 crop year 22 and 49.2 million tons in the merketing year 2020/21), especially for Argentina – by 0.2 to 4.4 (4.05) million tons and the Russian Federation – by 0.5 to 16 (15.6) million tons, although according to Rosstat data, at the end of December 15.3 million tons were harvested and 1 million hectares remained uncollected. For Ukraine, the crop forecast was increased by 0.4 to 10.4 (17.5) million tons.

Ukraine continues to restore power supply to industrial enterprises, which improves the prospects for sunflower processing, therefore the domestic processing estimate was increased by 0.5 million tons to 10 million tons.

Forecasts for global sunflower ending stocks were cut by 0.88 million tons to 4.85 million tons (8 million tons in 2021/22 and 2.6 million tons in 2020/21), especially for Ukraine – by 0.3 to 1.85 (4.69) million tons and the Russian Federation – by 0.5 to 0.74 (0.96) million tons.

Sunflower purchase prices in Ukraine during the week fell to 465-480 USD/MT ex-factory due to delayed ship actions to Black Sea ports and slower export of flour and oil. But for a month, sunflower prices rose by 3-5%.

The acceleration of sunflower exports in early January led processors to raise purchase prices, so resolving the port call issue will immediately boost sunflower demand, even with low sunflower oil prices due to a significant supply of cheap palm oil.

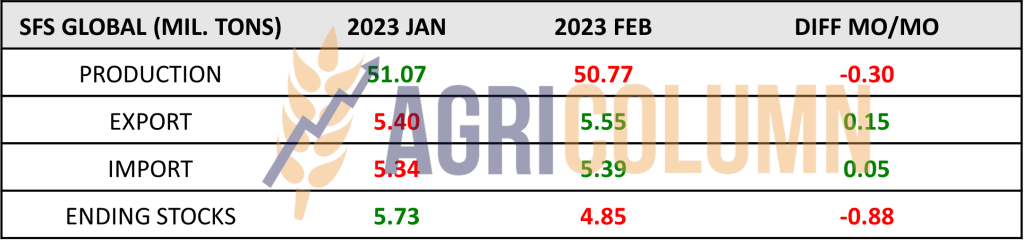

The table below clearly describes in numbers the global status of seed production and stocks. It will be the Geopolitical factor that will boost the market in the next 2-3 weeks.

LOCAL STATUS

In Romania, the price indications for soybeans are at the level of 560 USD/MT DAP processing units for non-GMO soybeans, with delivery after February 1, 2023. Between July 1, 2022 and February 5, 2023, 150,529 tons of soybeans were imported and 249,883 tons of soybean meal.

REGIONAL STATUS

THE EUROPEAN UNION. Weekly soybean imports to EU countries rose to 266,662 tons, up 4.13% from last week. Total soybean imports increased to 6.45 million tons, but they are 19.15% lower than last year at this time. The Netherlands remains this week as the number one importer of soybeans in the EU from July 1, 2022, but, of course, with an increase in volume to the level of 1.9 million tons.

Soybean meal imports into the EU in the last reporting week (January 29-February 5) were 245,789 tons. Thus, total imports reached 9.44 million tons, which means a decrease of 5.12% compared to last year.

GLOBAL STATUS

USA. Weekly US soybean export inspections were again reported at 1.8 million tons. Analysts’ expectations ranged between 1.6 and 1.9 million tons, according to data provided by the US Department of Agriculture (USDA). The main destination was again China with 1.1 million tons, and other relevant destinations were Mexico (256,698 tons), Italy (139,619 tons), Germany (85,555 tons), Indonesia (75,558 tons) and Japan (48,204 tons). Total inspections since the beginning of the 2022/2023 marketing year reached 37.8 million tons.

USDA’s weekly 2022/2023 soybean net sales data shows a level of 459,400 tons in the week ended February 2.

As for the year 2023/2024, net soybean sales of 185,000 were reported (132,000 tons to unknown destinations and 53,000 to China).

BRAZIL. Brazil’s 2022/2023 soybean harvest has reached 8.9% of the 43.4 million hectare area, according to the Conab agency. Last year, 16.8% of the area was harvested during this period. The stoppage of the rains allowed Mato Grosso to reach 25.3% of the area with the harvest. In Rio Grande do Sul, rainfall was beneficial, but the volume was not sufficient to reverse water stress in many regions.

Conab estimates Brazil’s soybean production for 2022/2023 at 152.88 million tons, up from its previous estimate of 152.71 million tons. If achieved, it would be a 22% increase over last season. Exports are estimated at 93.9 million tons.

ARGENTINA. The Buenos Aires Grains Exchange (BAGE) cut Argentina’s soybean production estimate to 34.5 million tons, while the World Agricultural Supply and Demand Estimates (WASDE) of the USDA, the outlook is reduced by 4.5 million tons to 41 million tons.

Drought and high temperatures led to yield declines. In addition, these conditions affected the establishment of the soybean acreage in the second crop, with cases of repeated reseeding being reported, which lasted even until the end of January, according to BAGE.

While rainfall is expected to stem losses at important stages of development, areas rated good to excellent have increased to 13%. Areas rated as average fell to 39% from 42% last week, and areas rated as poor increased to 48%.

Areas considered dry have now increased to 61%, and areas considered optimal and adequate are now 39%. Argentine farmers sowed 16.2 million ha of soybeans.

CHINA. Soybean processed volumes did not fully return to pre-holiday levels after the Lunar New Year festival but were at 1.28 million tons in the week to February 7, according to data from the National Grains and Oil Information Center (CNGOIC).

As of February 4, CNGOIC reported soybean stocks at 5.28 million tons, up from the year-ago period of 3.3 million tons.

Soybean meal stocks fell by 70,000 tons from last week to a total of 4.6 million tons. Livestock margins were unfavorable, the pig/grain ratio was low, which led to a decrease in feed demand. The Chinese state will purchase pork for reserves to control prices and this is expected to be favorable for pork prices.

Soybean oil stocks fell 5.47% from last week to 690,000 tons, although processing is expected to pick up as factories fully resume, which will push soybean oil stocks higher.

CBOT SOYBEAN – ZSH23 MAR23 – 1,542 c/bu

SOYBEAN GRAPHIC TREND – ZSH23 MAR23

EXTRA

UKRAINE

The Parliament of Ukraine has implemented a new amendment to the Fiscal Code and some legislative acts regarding the country’s export procedures during the martial law period on February 5, which will take effect one month after the date of publication.

According to the implemented changes, the export of grains and processed products can be carried out only after the party has made a preliminary export deposit of at least 14% of the customs value of the goods transport directly from the bank account of the exporter.

This would be seen as a guarantee by the government that the said company would return the earnings in foreign currency.

After the return of foreign currency funds for a commodity exported to Ukraine, the guaranteed amount from the previous export deposit will be returned to the exporter in full. In the case of a partial return, a refund will be issued in proportion to the amount returned. If the exporter violates the conditions for returning foreign currency earnings to the state, the amount of the previous export deposit will be transferred to the state budget of Ukraine.

UKRAINE

Ukraine is signing an agreement on goods access with the EU. By the end of 2023, Ukraine wants to sign an agreement that would allow Ukrainian goods to access the EU market (ACAA). As explained by the Minister of Economy, Iuliya Svyridenko, all industrial production will operate in accordance with EU rules.

Therefore, it will be profitable for European companies to locate production for the EU market in Ukraine. According to her, the ACAA agreement is an element of the intermediate stage between the Free Trade Agreement and full EU membership.

First of all, it is about equal rights of Ukraine with those of other EU member states in all spheres of movement of goods in telecommunications, energy, customs, food safety, etc.

HUNGARY

“The Hungarian government protects Hungarian producers from the inaction of Brussels, that is why in our country strict quality and safety controls of the grain food chain originating from Ukraine are being established”, – said the Minister of Agriculture of Hungary István Nagy.

He also emphasized that Hungarian farmers can only rely on the country’s government, because, according to him, the EU does not hear the voice of European farmers. “We cannot allow Hungarian farmers to suffer because the solidarity corridor is not working properly,” added the minister.

He said that Hungary will continue to provide all assistance and support to ensure that grain reaches its destination, consumers in Africa and the Middle East, but that it will introduce “very strict quality control” of grain coming from Ukraine to Hungary.

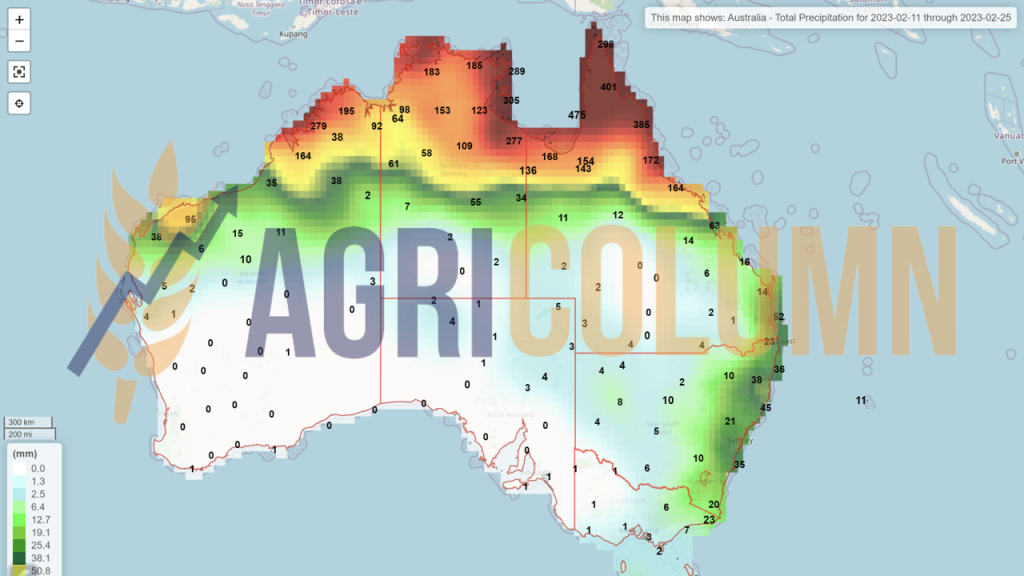

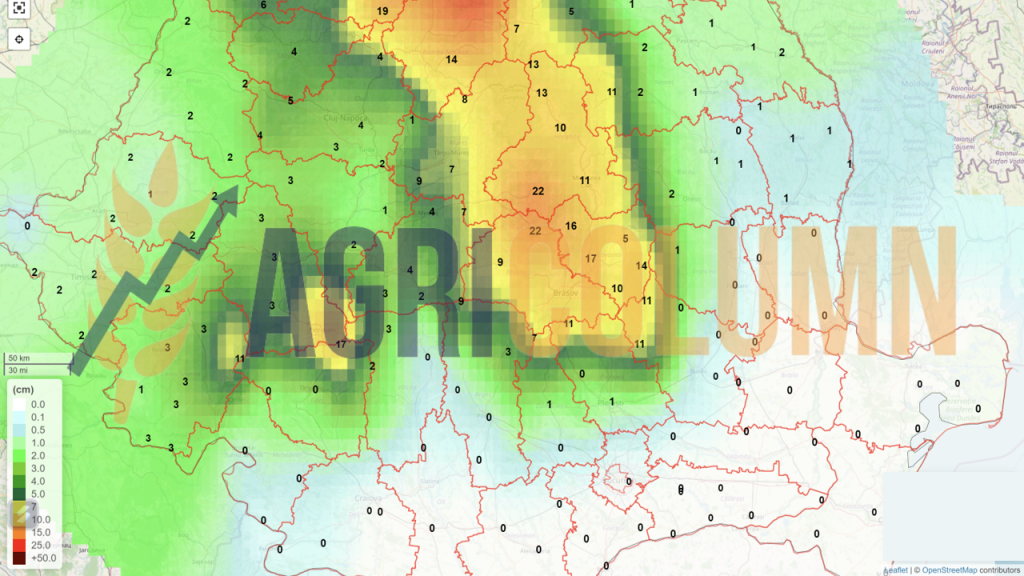

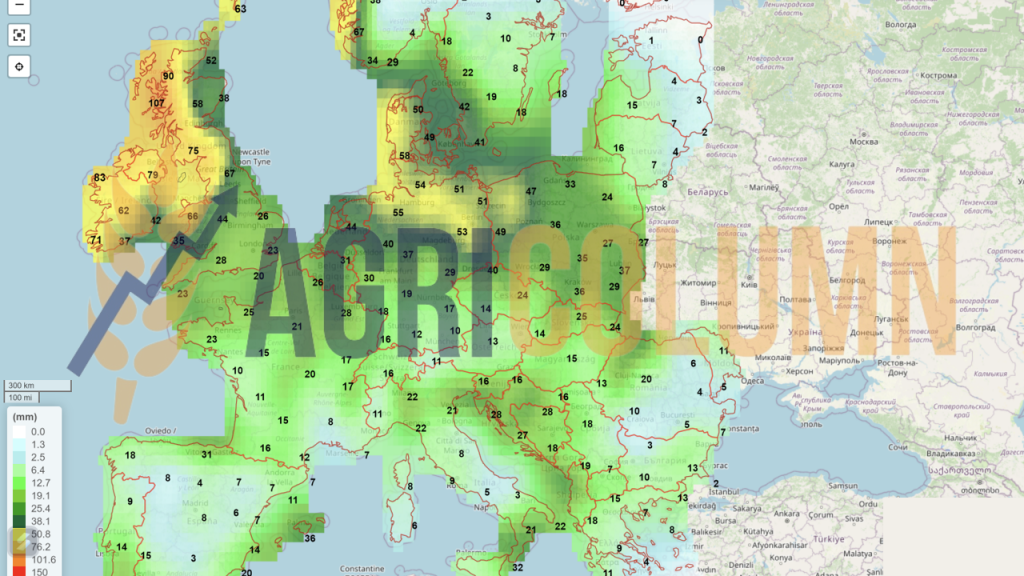

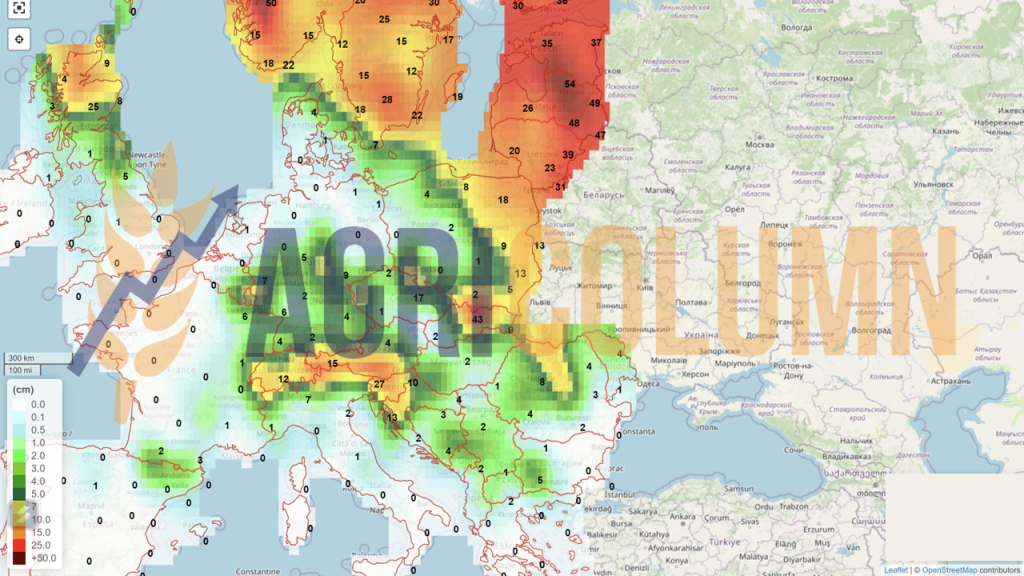

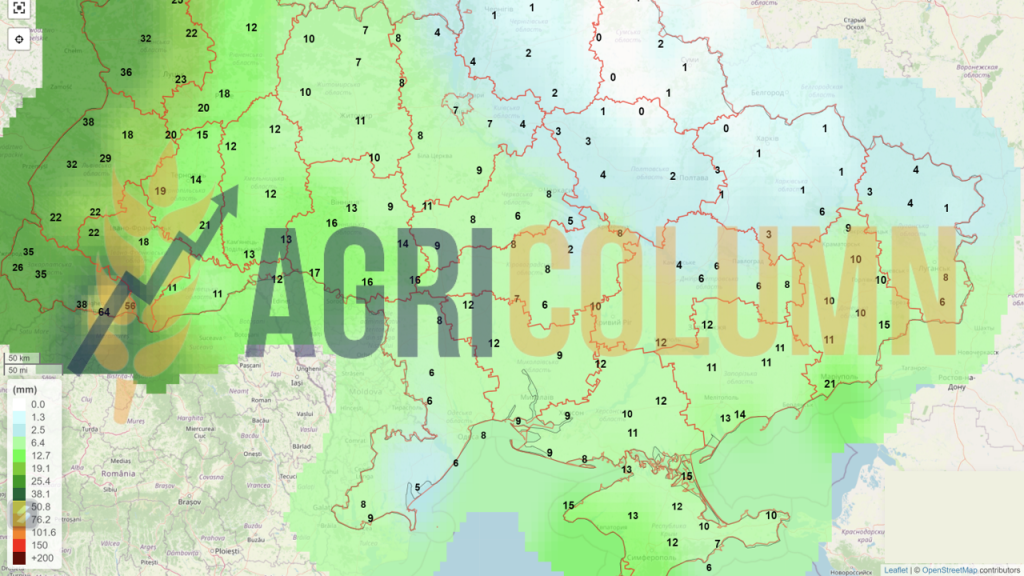

11-25 February 2023

Romania (rain)

Romania (snow)

Europe (rain)

Europe (snow)

Ukraine (rain)

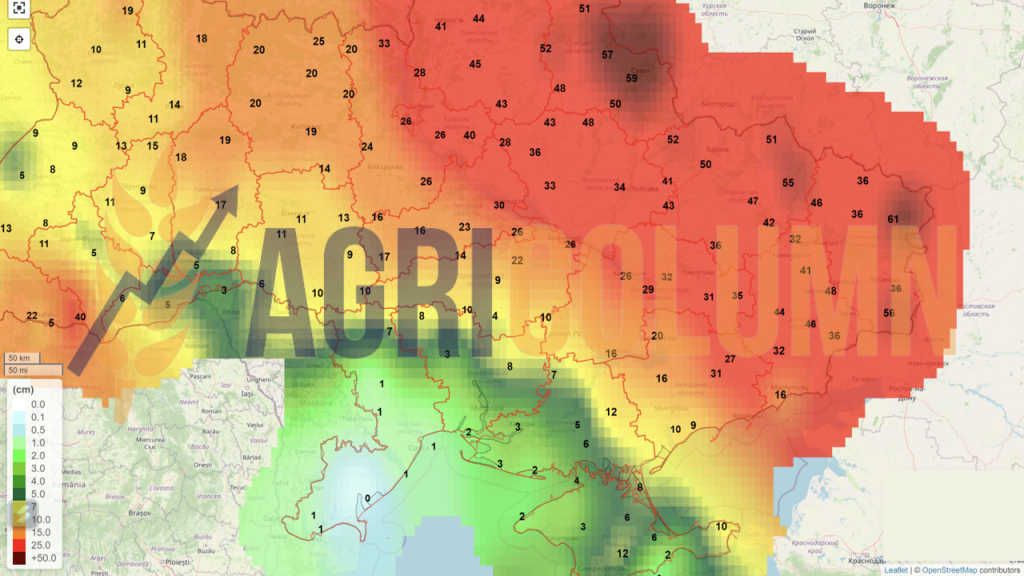

Ukraine (snow)

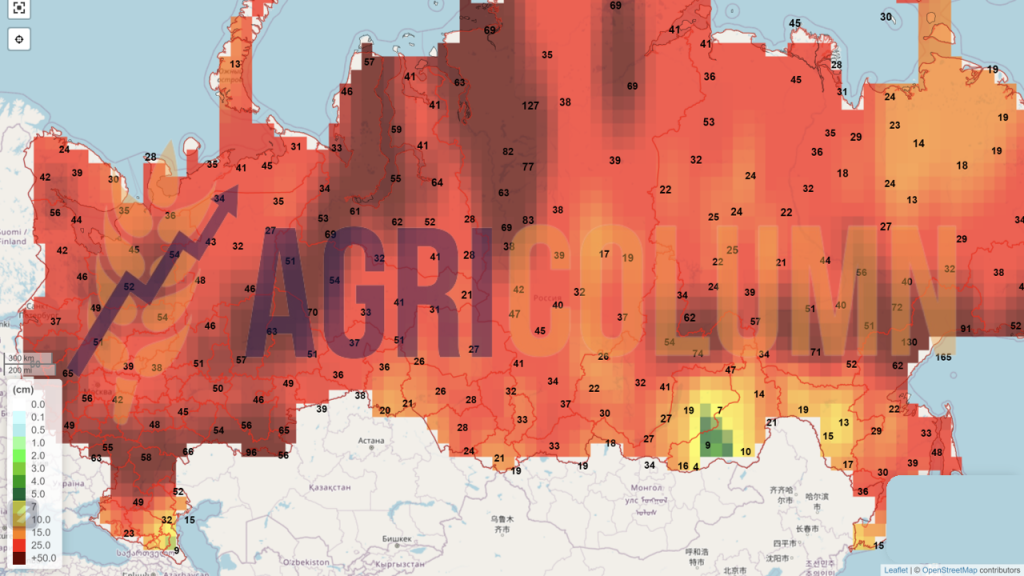

Russia (snow)

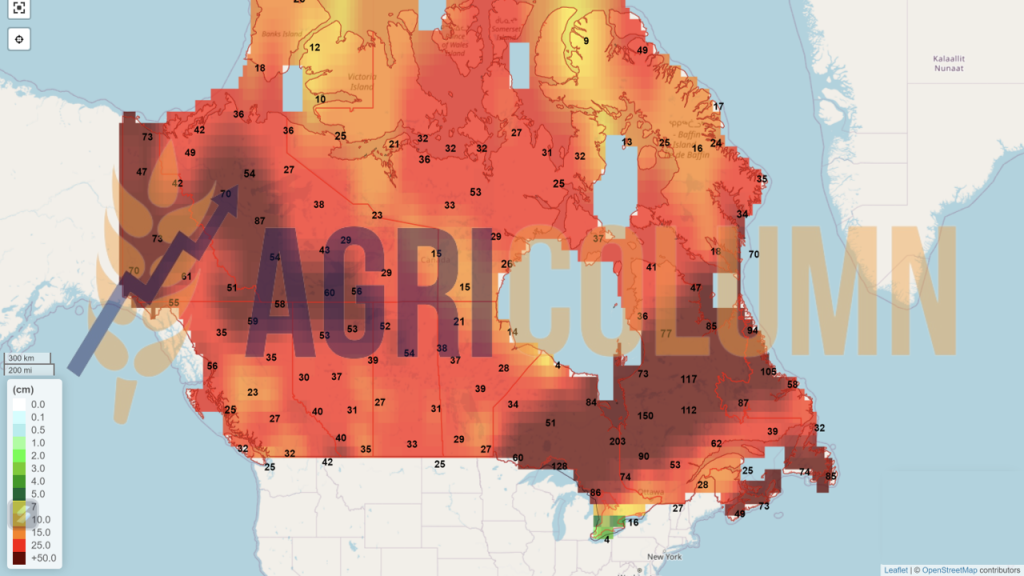

Canada (snow)

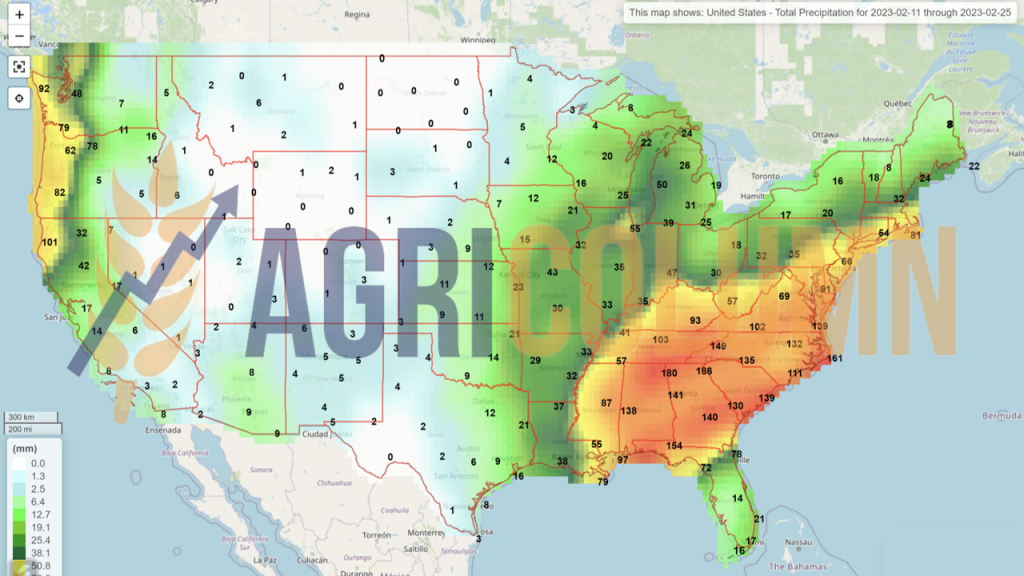

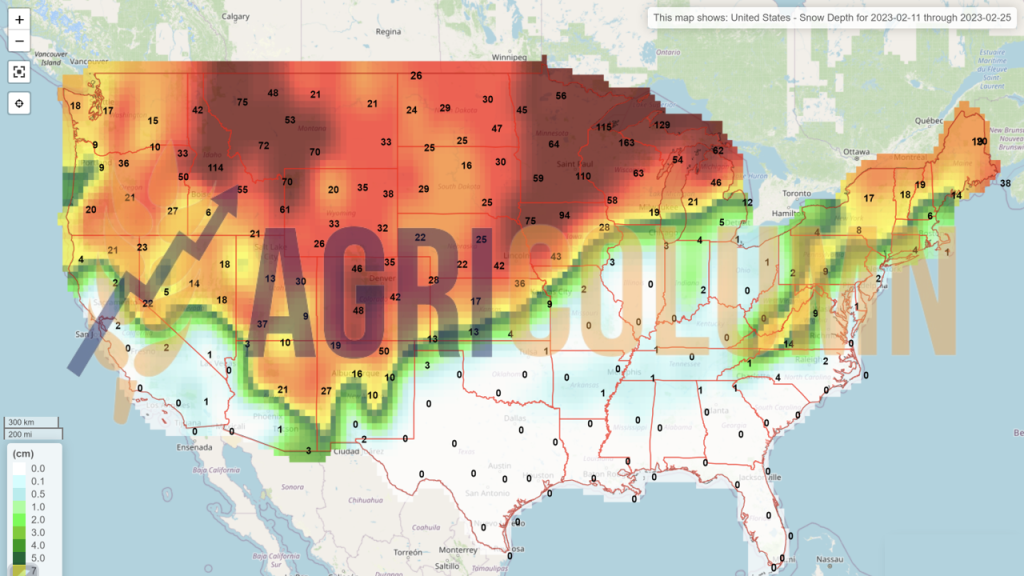

USA (rain)

USA (snow)

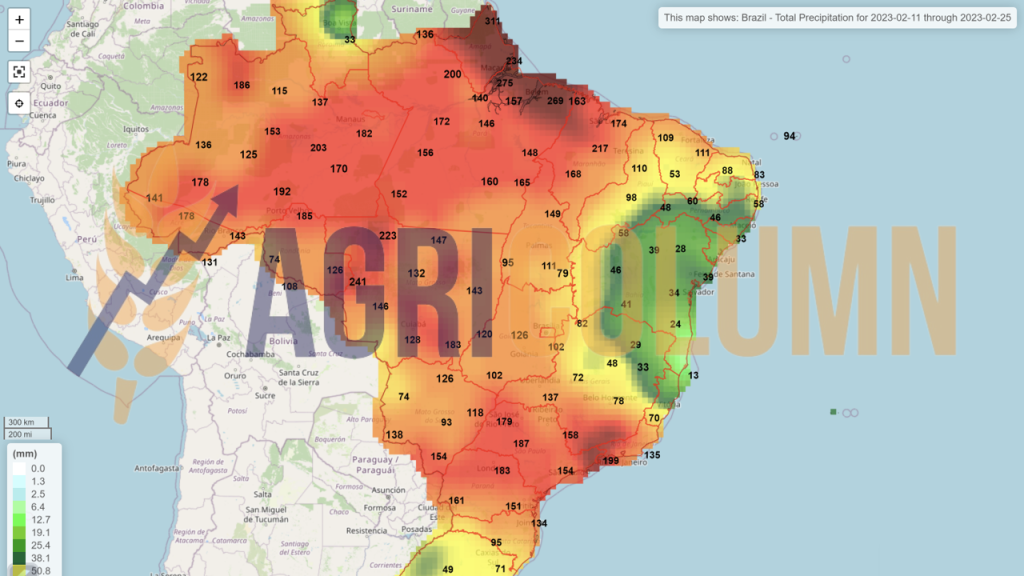

Brazil

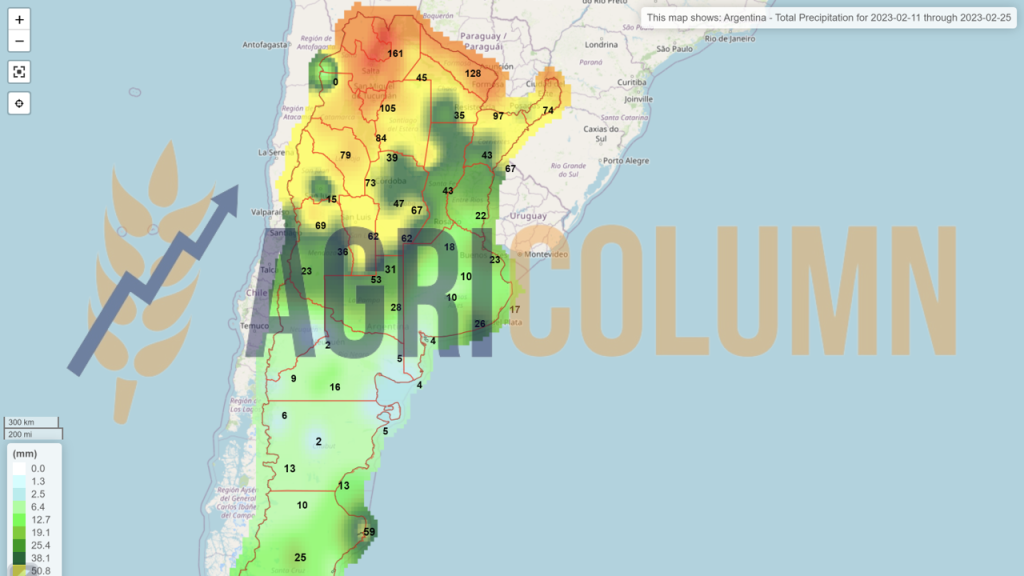

Argentina

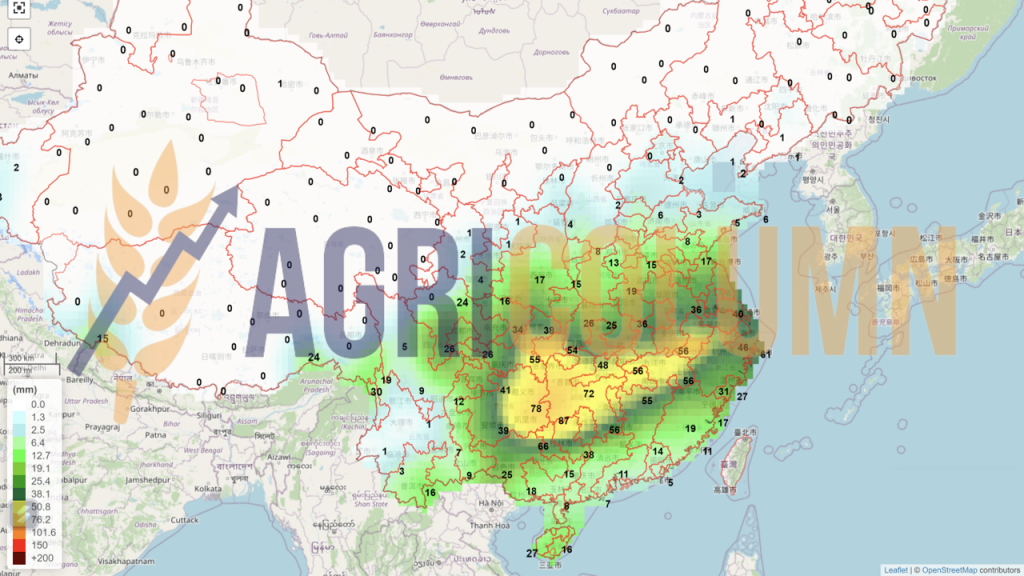

China (rain)

Australia