This week’s market report provides information on:

LOCAL STATUS

The indications of the port of Constanța are at the level of 332-335 EUR/MT, in total agreement with Euronext, using the DEC22-18 EUR formula. Feed wheat starts to be penalized by 25 EUR/MT. But on Monday, when this report will be released on the platform, we will see price increases in the CPT Constanța parity, a fact due to the American NASS (National Agency for Statistical Services) report. This report records a decline in US wheat production.

The domestic market boils down to levels of 300-320 EUR/MT. The behavior of processors to buy enough to keep processing active for 30-45 days indicates a knowledge of the fact that Romania has large stocks of wheat.

This total also includes 227,000 tons of wheat from Ukraine that feeds processing in the Northeast. The goods are offered (as is natural to penetrate the market) at lower levels compared to goods of Romanian origin.

CAUSES AND EFFECTS

Stocks of goods in Romanian farms are high enough to calm the domestic market. With an export level at the end of September of a maximum of 1.5 million tons, Romania is following the export plan. The initial estimate of 2 million tons out of a total of 5 million tons was not achieved. The conclusion is very clear. Romanian wheat is expensive in the competition from the Black Sea basin.

And what is seen is not likely to bring big surprises in this regard. There will be two months in which the destinations will ask for goods, but, certainly, as I wrote before, Russian wheat is far ahead in this competition.

The domestic market is also saturated, and the way it stands today does not indicate that it is suffering from raw material supply anxiety. Only the exacerbation of Russia could generate large increases in the price of wheat, namely the use of nuclear weapons. But then we discuss other parameters that are no longer related to our daily activity and will generate chain effects in the Black Sea basin.

REGIONAL STATUS

RUSSIA cuts its export tax on wheat once again. This is set, according to the MOEX index, at 42.4 USD/MT.

EURONEXT MLZ22 DEC22 –356.75 EUR (+4.5 EUR)

EURONEXT WHEAT TREND CHART – MLZ22 DEC22

GLOBAL STATUS

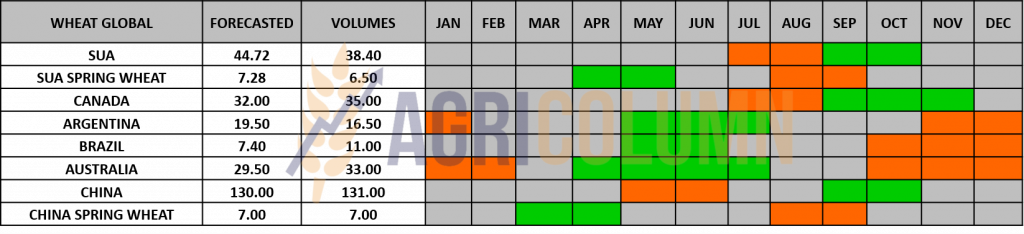

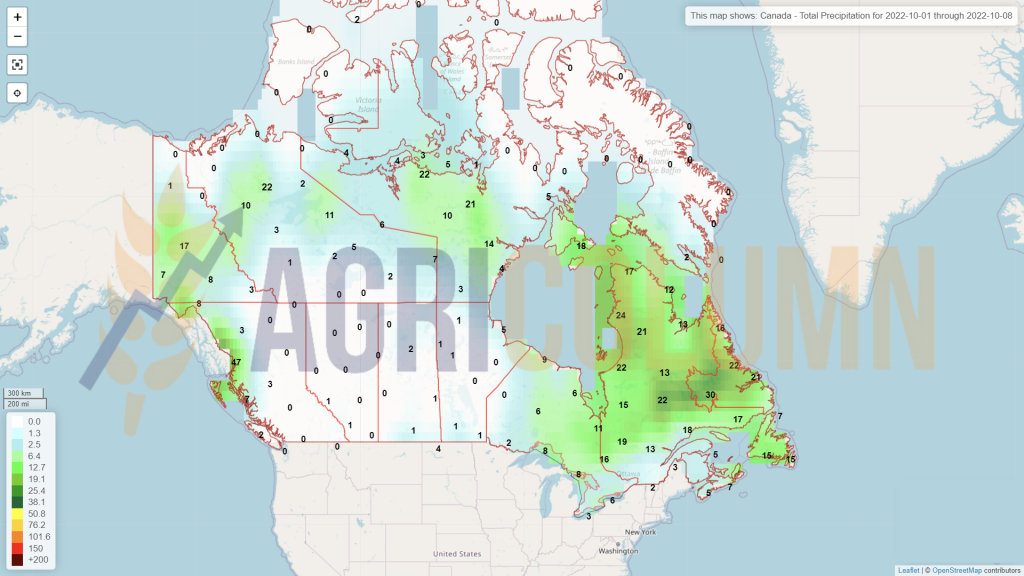

CANADA continues to harvest and wheat in Manitoba has been spared from the effects of Hurricane Fiona.

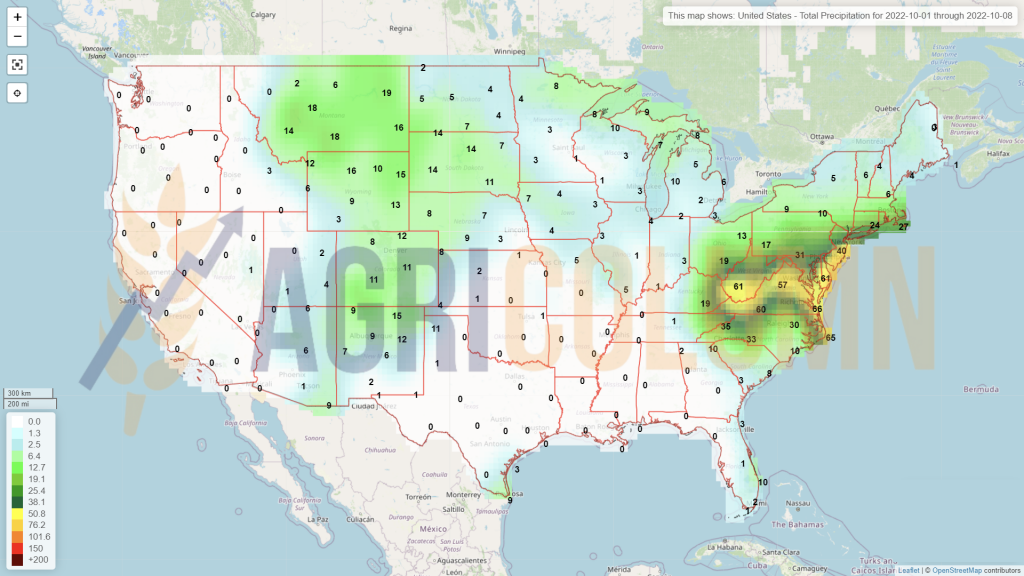

USA has also finished harvesting spring wheat, but the US Inventories Report generated by the National Agency for Statistical Services (NASS) cuts dramatically from US production, to be exact, by 3.6 million tons, bringing total production to a level of 44.9 million tons.

ARGENTINA is going through a critical period. Argentine wheat is in danger. An area of 500,000 hectares is in a critical state in terms of water reserves. La Nina bites with all its might from the Argentinian potential.

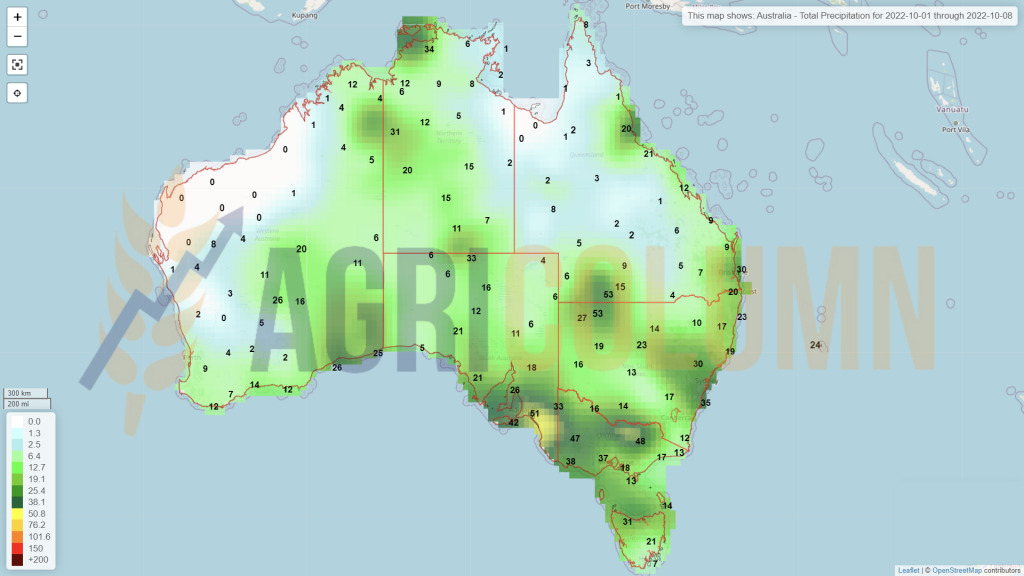

AUSTRALIA, on the other hand, receives excess rainfall from La Nina. If there is a deficit somewhere, there is a surplus elsewhere. It’s the reverse of physics as we learned it in school. The volume potential is not compromised, but the quality will certainly suffer. Australian wheat will be washed of protein and the danger of warping is also present.

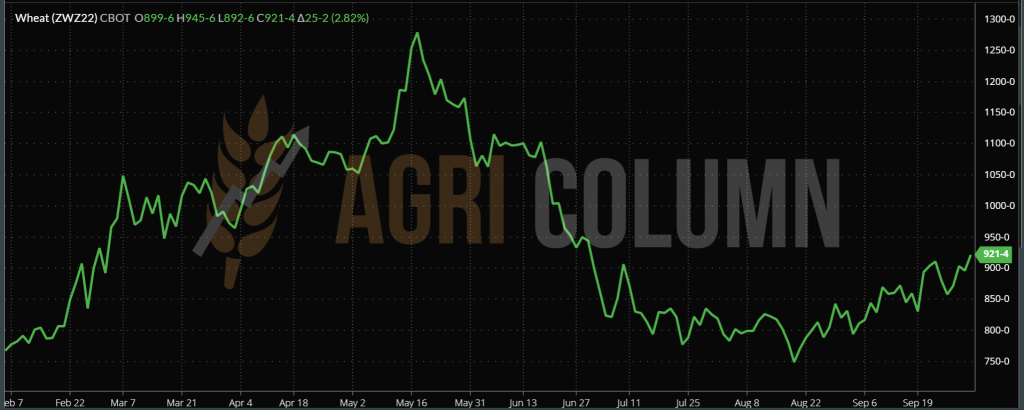

CBOT WHEAT – ZWZ22 DEC22 – 921 c/bu (+25 c/bu = +9.18 USD)

CBOT WHEAT TREND CHART – ZWZ22 DEC22

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

CAUSES AND EFFECTS

RUSSIA, which generates the largest volume of cargo, could also be the biggest reason why the price could rise. The use, even in the form of a threat, of nuclear power instantly ignites the Euronext and CBOT exchanges.

Algorithms generate long positions and specula generate profit, after a few days when the general mood relaxes. This YO-YO game does nothing but fill the accounts of hedge funds, and some of them certainly have Russian roots.

The physical market switches between 5 and 10 EUR/MT, nothing more. It’s the time of the year when all Destinations are waiting to see a price leveling off and possibly a drop. This can be clearly seen from what happened in the last week, namely an attempted tender organized by MIT JORDAN, which did not materialize due to the lack of meeting the conditions (minimum 3 participants).

Another direct sale to Russia is causing some buzz. We are referring to the 2 million tons of wheat sold to Afghanistan. A fair and concrete question about this transaction would be: what are the Talibans paying with? In what currency and how? Or somehow in barter? As a joke, cannabis would be a potential barterable commodity, as nothing else would exist in those places. And as an irony of fate, the same Afghanistan that drove the Russians out will now receive wheat and energy from them. On the exchange of what?

The clear indications from the NASS report are for production to decline in the US and we see it falling to the 44.9 mil. tons level, almost in line with the 44.5 mil. tons figure we’ve been carrying since the spring.

But FEAR will dominate in the next period. The fear that Putin will access the nuclear weapon in any form. Then the story changes completely. Then things will go into a deep deadlock, because NATO will not allow the use of nuclear weapons, and we will be able to witness very harsh countermeasures, which may lead to something we do not want.

The Green Corridor has about 50 days left until it expires, and normally it has to continue. Things must be balanced; Russia must export wheat and Ukraine corn. Russia needs the corridor to support its cargo (wheat) shipments, and its closure could create new problems in terms of sanctions on Russia.

We have hybrid warfare factors in the wheat equation, factors that go beyond the tariff sphere. There are factors that try to forcefully redefine borders and the balance of global power. One thing, however, is obvious and cannot be denied: Russia has entered the territory of another sovereign state. No motivation can be accepted, as the Kremlin leader says, such as having its territory taken from the Soviet Union in 1990. This is not a reason that can be accepted, and the use of force will generate nothing but a similar response.

CONCLUSION

All of Putin’s aberrant speech, all of the September 30, 2022 propaganda, and the ceremonial performed meant nothing by 7:00 p.m. That’s when the NASS released final US wheat production figures, and they were down 3.6 million tons from a comforting 48.5 million tons to 44.9 million tons. It was a moment that set off fireworks in the CBOT, the excitement absolutely running high. We will all see positive corrections in the price of wheat on Euronext today, and naturally some of the excitement will also remain in the CBOT.

Here’s how from just 3.6 million tons, wheat gets a boost. How long will it last? It all depends on the demand from the destinations, i.e. how much they will be willing to pay for the physical goods. However, the macro fundamentals remain broadly the same. The last surprise on the list is Argentina, but we still have a break until then.

LOCAL STATUS

The indications of the port of Constanța remained during this time between the two reports at levels of 270-275 EUR/MT. Nothing has generated an obvious demand to change this status.

As we said in the previous editions, barley stocks still exist at the local level, and the Romanian export is at the level of 650,000 tons up to this moment. From a crop of 1.6 million tons and with a maximum domestic consumption of 300,000-350,000 tons, we have a surplus of stocks, to which we add a Ukrainian import of 60,000 tons.

The future does not look good for barley. There is no change on the horizon. The result of the last tenders did not generate expectations of an increase, but, on the contrary, of a decrease.

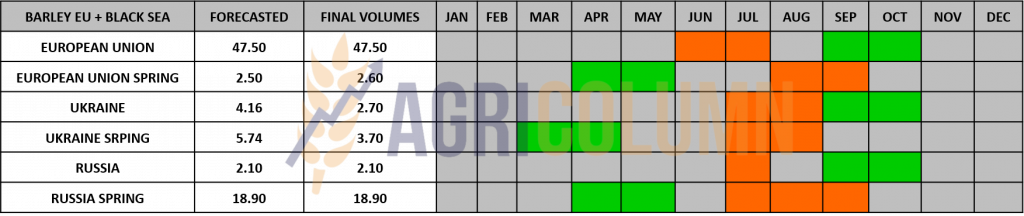

REGIONAL STATUS – OUT OF HARVEST

GLOBAL STATUS

USA has finished harvesting barley, CANADA is underway for another 2-3 weeks. Then subsequently, the southern hemisphere starts with the AUSTRALIA exponent. CHINA is for information only, not being the origin but the destination (for Australian barley in general).

BARLEY PRICE INDICATIONS IN MAIN ORIGINS

CAUSES AND EFFECTS

Barley’s price path does not look bright at the moment. It is rather on a downward trend generated by the potential for substitution with feed wheat. Even the established formula DEC22 EURONEXT WHEAT DEC22 minus 40 EUR is no longer valid at the moment.

LOCAL STATUS

The indications of the port of Constanța are heating up like engines already. The price increased by 15 EUR/MT within a few days and reached 300 EUR/MT. Everything is augmented by the liquidity of the goods, more precisely by the demand for them. As with wheat, NASS comes in and corrects, raising the price potential of corn. A shortfall in North American stocks will generate a price boost that will be seen in abundance in the period ahead.

In the country, the price levels practiced by local traders indicate values of 265-275 EUR/MT in FCA Farm parity. Processors and livestock indicate higher levels due to spot interest in corn.

Nationally, the harvest reached around 25-28%. Everything is going slowly because of the rains that furrow the western area of Romania. The volume level remains unchanged at 8.2 million tons. The import of Ukrainian corn reached the figure of 320,000 tons.

CAUSES AND EFFECTS

The price of corn is starting to rise and has some supporting factors at the moment. These factors are of the order of global volumes and regional weather. In the current assemblage, the main lever being the weather at the regional level, we estimate a weighted increase in the next period, of around 10-20 EUR/MT.

REGIONAL STATUS

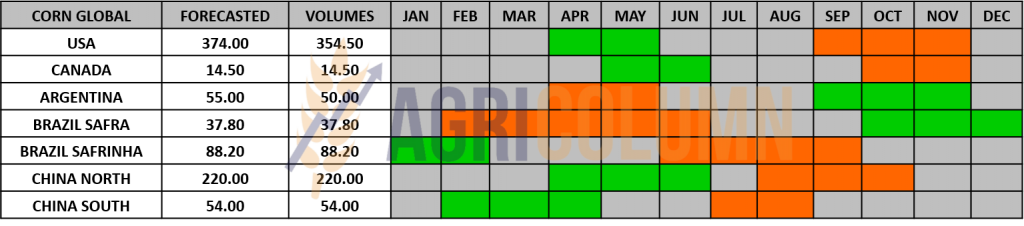

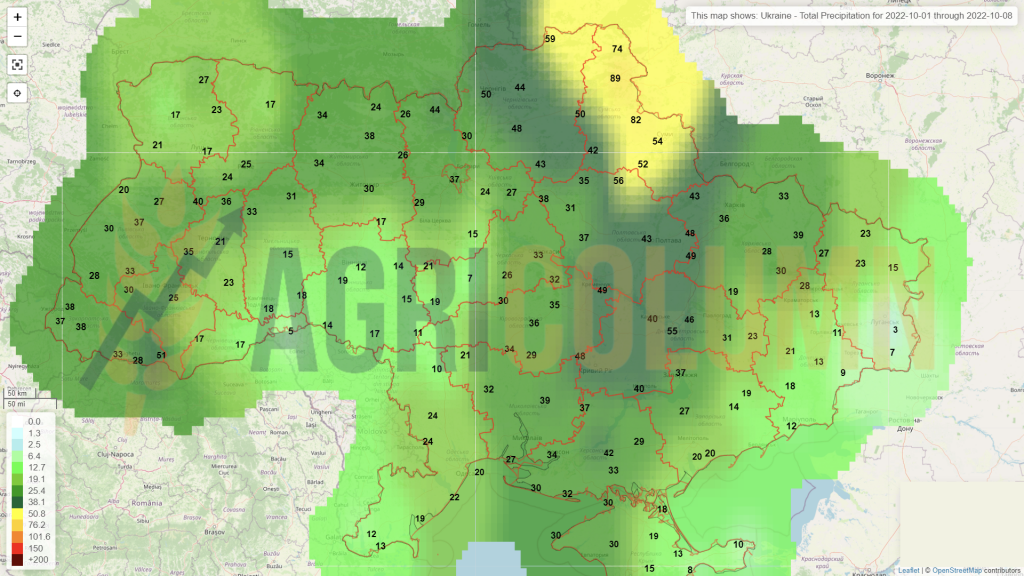

UKRAINE will generate 32 million tons of corn in terms of harvest volume. Ukrainian farmers have carried out the so-called “kick off” of the harvest campaign and started this process, but the rain is a detail that will delay the harvest.

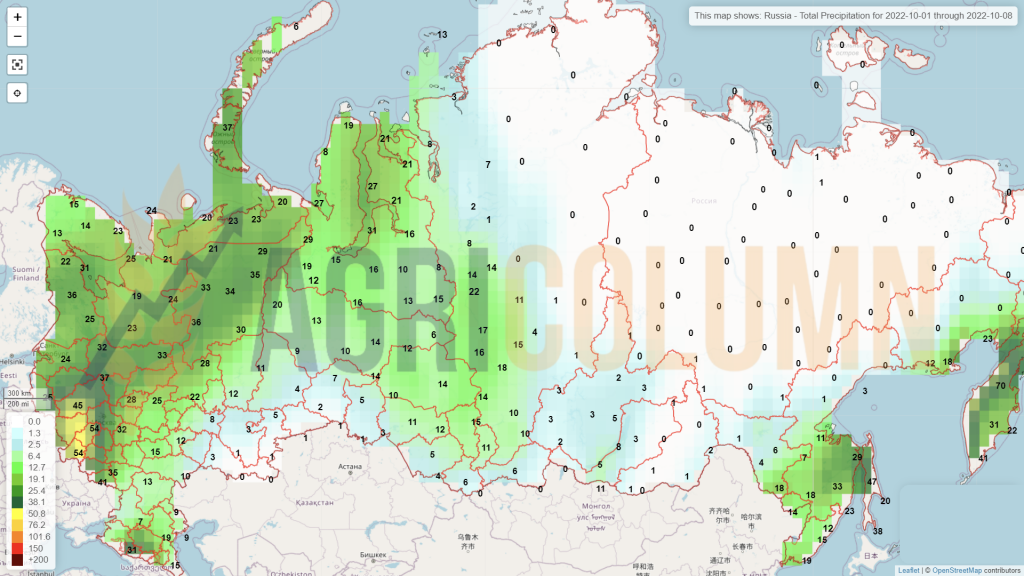

RUSSIA will also start harvesting. Weather permitting, they will certainly reach the estimated level of 15.5 million tons.

The EUROPEAN UNION is in the same status. It harvests but the volumes are not positively corrected. The differences will be highlighted in the next WASDE report. And we are referring to a minus of at least 4-5 million tons that must be highlighted, because the statistics are good, but the harvest volume always tells the truth.

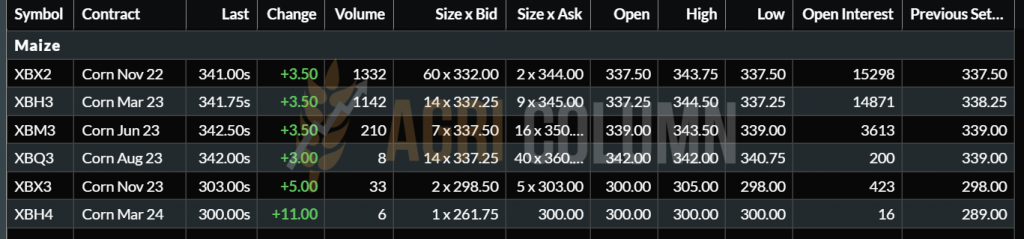

EURONEXT CORN – XBX22 NOV22 – EUR 341 (+EUR 3.5)

CORN TREND CHART EURONEXT

GLOBAL STATUS

USA corrects stock values through NASS (National Agency for Statistical Services). Thus, they decrease by 3.5 million tons and directly impact the CBOT indications.

ARGENTINA has started planting corn, but we know what problems exist in Argentina and, from the start, we must penalize the Argentine volume by 5 million tons, from 55 to 50 million tons.

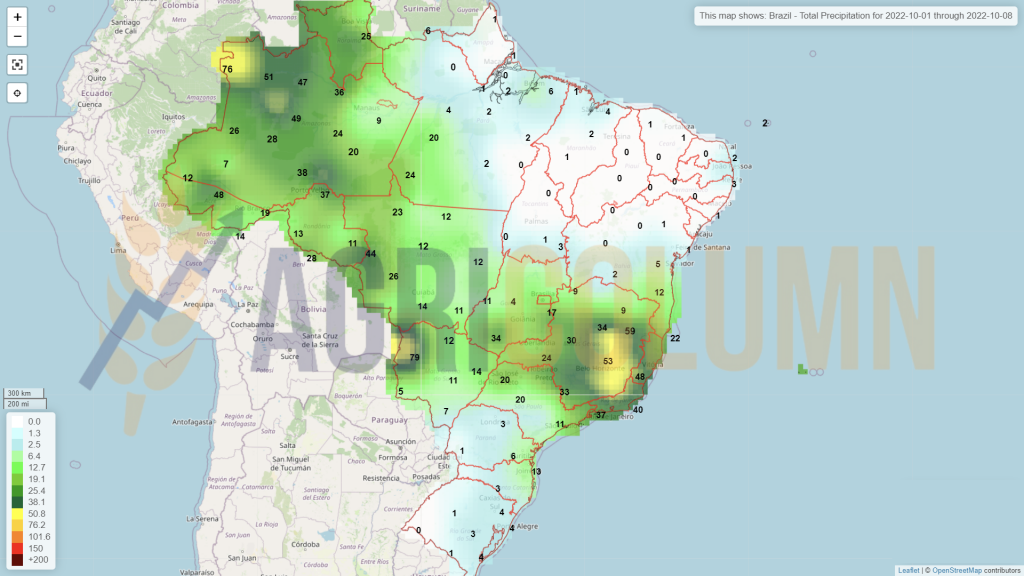

BRAZIL will also start planting corn soon. We are talking about Safra, the first corn harvest, which will open the scene of the South American opera. Will it be Samba do Brasil? The signs point to yes. Rainfall encourages optimism in this first sequence.

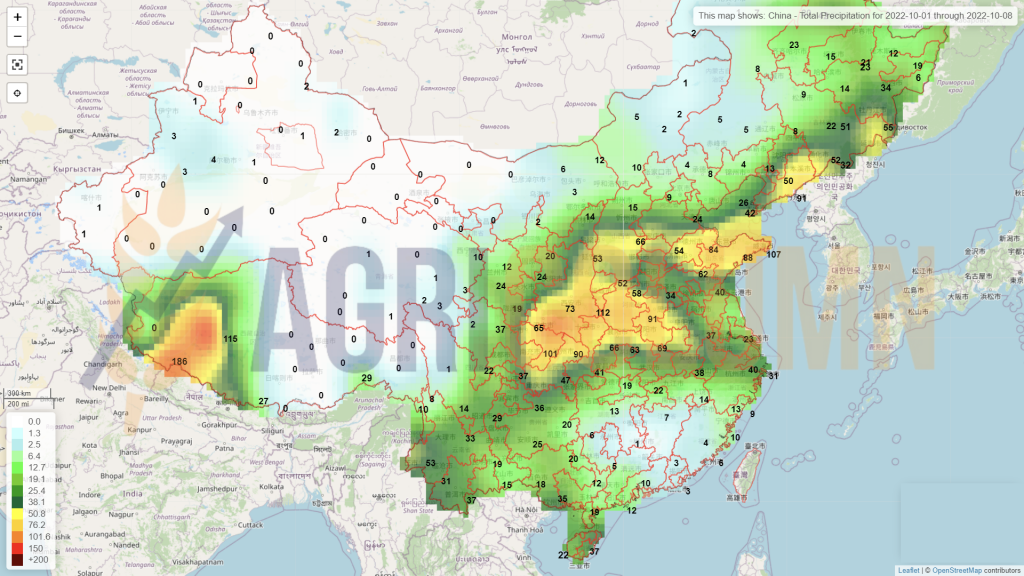

CHINA will close the harvest after October. It is not the origin, but any problem will generate a higher level of import.

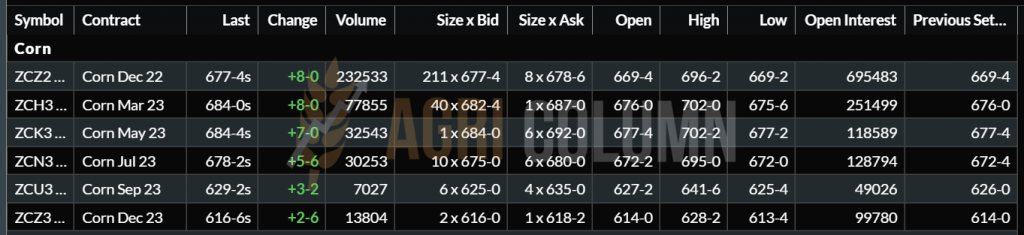

CBOT CORN – ZCZ22 DEC22 – 677 c/bu (+8 c/bu = +3.15 USD)

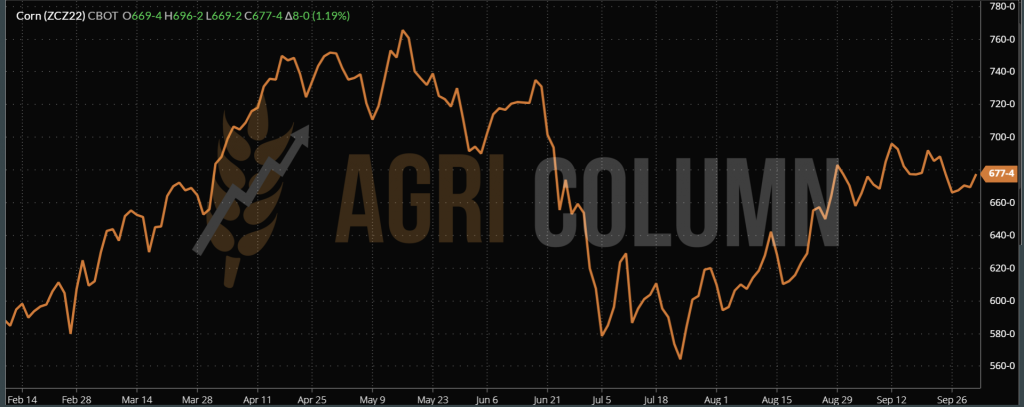

CBOT CORN TREND CHART – ZCZ22 DEC22

CORN PRICE INDICATIONS IN MAIN ORIGINS

CAUSES AND EFFECTS

UKRAINE. Starting from the east, we have the first comments regarding the Ukrainian harvest, which is experiencing weather problems at the moment. It is actually raining in Ukraine and the harvest will be very slow. Thus, the first prerequisites are created for increasing the nervousness of the demand, which will boost the faster arrival of the goods through the price. Then what will increase the price level will be the cost of drying the goods, taking into account the price of this service (expensive gas). So a first effect comes from two Ukrainian causes – weather and costs.

The EUROPEAN UNION will be fined by WASDE on 12 October 2022 by a minimum of 4-5 million tons, from 59 million tons to 55-54 million tons. Not even the USDA can keep track of everything. Physics dictates volume and so the numbers must be tuned accordingly.

USA generated a lower level of stocks by 3.5 million tons. The next milestone is the WASDE report on October 12, 2022. Then we will associate another decline in production levels, this time. It remains to be seen how much it will be estimated by WASDE. 3 million tons?

ARGENTINA is being crushed by La Nina. The planting season has started, but the soil water reserve is extremely low. Argentine analysts already see a minus in the crop forecast from 55 to 50 million tons. It is a weather effect and cannot be absorbed by another origin either.

CONCLUSION

All the complex described above must lead to an increase in the price of corn at the global level. If we add up the minuses, we have an aggregate figure of 16.5 million tons. It is a high figure, even under the condition of reducing consumption and replacing it with feed wheat. On CBOT, as in the case of wheat, an immediate increase in the level of indications was observed. It remains to be seen how much will remain after the emotion dissipates. In any case, the premises to reach a higher level of the price by 10-20 EUR/MT are perfectly realistic.

LOCAL STATUS

The indications of the port of Constanța remain faithful to the NOV22 formula minus 25-30 EUR/MT. For processors, we note indications according to the formula NOV22 minus 15 EUR/MT for goods delivered to processing units. Stocks continue to remain consistent at the level of farmers as well as local traders.

With regards to the autumn sowing, we can consider the rapeseed finished, to have a final figure on the total area that has been sown. Some figures go up to 670,000 hectares, this due to fears of pedological drought that may occur again in the spring-summer season, but also due to excessive heat, which could irreparably damage the spring crops and we refer specifically to corn culture. This change in the behavior of Romanian farmers is conditioned by the weather factor and is fully justified.

CAUSES AND EFFECTS

We predicted the change of interest in rapeseed and today we have a first effect of this prediction. More specifically, processing units are starting to show local interest in rapeseed again. Between October 5-10, 2022, they will carry out the processing exchange from sunflower seeds to rapeseed. It’s an aspect that arrived a bit earlier than we expected, but it’s also dictated by the regional weather factor. Local processors will take advantage of this unexpected weather break in the Black Sea basin and turn their attention to rapeseed.

We have to highlight here one more thing that we also anticipated and that caught up with us – traceability. We said from the first moments that the suspension of the quality regime and sanitary-veterinary certificates for Ukrainian goods will create huge problems. And we ended up in this position. For total clarification, we also note the import level of rapeseed from Ukraine, which stands at 300,000 tons, up to this point.

Contamination with GMO goods. Extremely many batches were introduced into Romania and mixed by local traders with batches of non-GMO, therefore compliant, Romanian goods. And these goods took the path of processing with the Origin Romania specification, contaminating and destroying the processing result.

The “positive release” tests performed on the oil show clearly and without doubt, through the purity test, that the product is GMO. What more can we say? That many lots have penetrated to the heart of Europe? That they, in turn, contaminated the products resulting from processing from Poland, Germany, Hungary and Bulgaria? Yes, this is exactly the end result of a faulty management of decisions at the European level, generated by people without any technical training in procedural and operational statutes.

REGIONAL STATUS

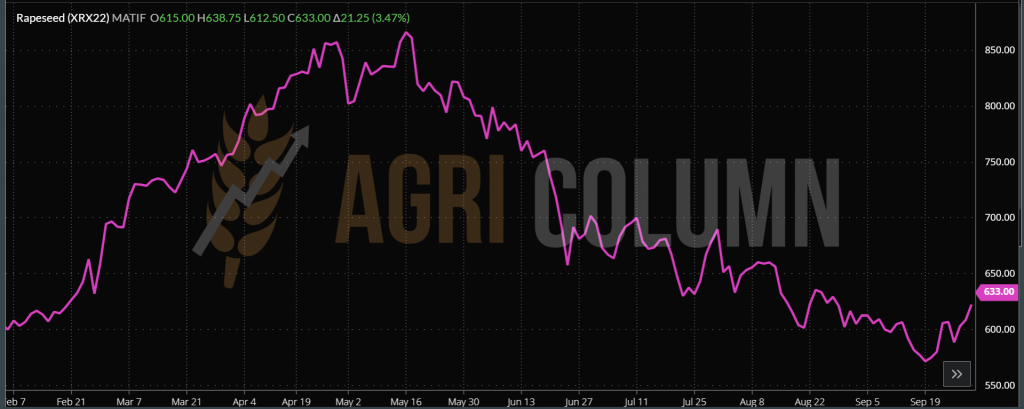

EURONEXT XRX22 NOV22 – 633 EUR (+21.25 EUR)

EURONEXT TREND CHART – XRX22 NOV22

GLOBAL STATUS

CANADA is still harvesting canola. Manitoba escaped the effects of Hurricane Fiona with no damage to canola fields. But they remain with that deficit of 0.4 million tons resulting from the overestimation of their own crop.

AUSTRALIA has a little longer to wait before entering the harvest season. Estimates are 6.7 million tons, but recent consistent rains could raise serious questions about possible damage. At this time, there is no information yet to question the Australian volume.

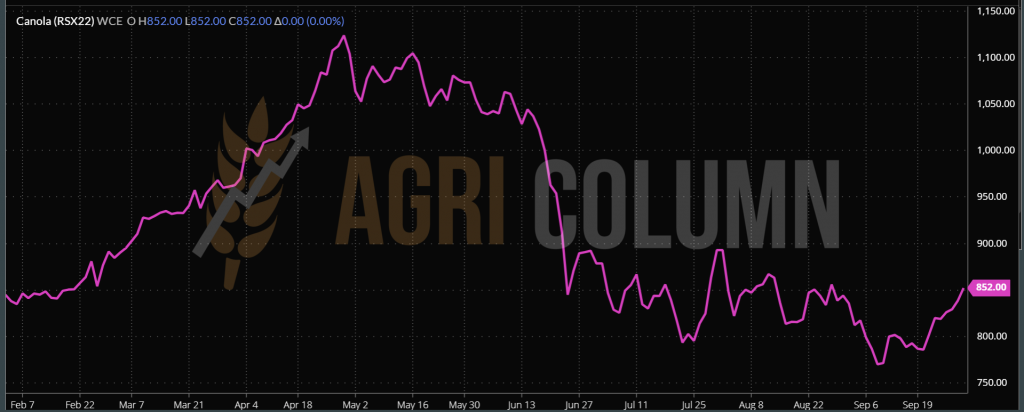

ICE CANOLA – RSX22 NOV22 –852 CAD

ICE CANOLA TREND CHART – RSX22 NOV22

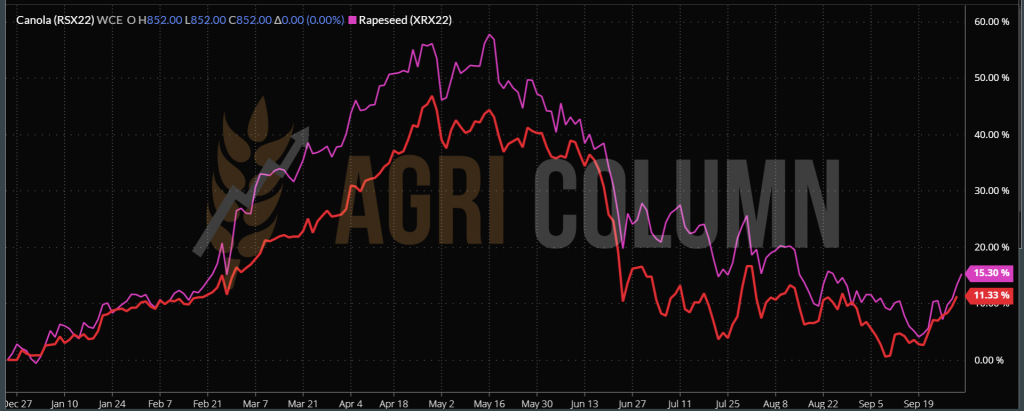

COMPARATIVE TREND GRAPH – EURONEXT XRX22 NOV22 – ICE CANOLA RSX22 NOV22

CAUSES AND EFFECTS

As for the price of canola, it is getting the traction we evoked in previous reports. Traction is generated by energy directly at these times and, as we see, the latter undergoes changes through price increases after the last destructive actions at the logistics level in the Baltic Sea (North Stream 1 and 2). The fear of possible further sabotage to the detriment of Norway, which is the largest consumer of European rapeseed oil (Norway refines extracted oil and formulates bio-diesel), is also a factor in the growth of rapeseed.

Another pull factor is the weather, which penalizes the flow of raw material (sunflower seeds) at the time of harvest in the Black Sea basin. Thus, due to the rains, sunflowers cannot be harvested in Ukraine or shipped as raw material to Romania and Bulgaria for processing. Processing units rethink their processing plan and perform the switch earlier. They will change processing from sunflower seeds to rapeseed. A not quite correct estimate of the Romanian crop level, which was clearly underestimated during the planning moments that took place in the spring, also contributes to this aspect.

The third pull factor is clearly the lower volume potential in Canada (0.4m tons) and we foresee some issues in the Australian crop as well, driven by the consistency of rains in this pre-harvest period.

CONCLUSION

Rapeseed is regaining traction and starting to come back. We certainly won’t see last spring’s levels again, but for a while, it provides consistency and perhaps decision-making power for those who stockpiled it to exploit higher price potential.

The price level of crude rapeseed oil in FOB Rotterdam parity also gained around 10 EUR/MT to 1,330 EUR/MT.

LOCAL STATUS

The price level offered by the port of Constanța received a boost and thus we see a minimum of 535 USD/MT offered for cargo delivered in CPT parity. Bonus quotes for HIGH OLEIC are also in the 80-90 USD/MT range. Processors are lining up and offering 530-535 USD/MT for the commodity delivered on DAP condition.

In Romania, we can say that the harvest has come to an end. Certain scattered areas are still to be harvested because we are talking about the second crop. But, as we estimate, we have a maximum of 2.2-2.25 million tons of sunflower seeds nationally, in terms of production.

Locally, prices jumped by around 10-15 USD/MT and it was only logical that this would happen as the harvest ended and the goods went to the warehouses of farmers or middlemen.

CAUSES AND EFFECTS

Locally, we admit that supply from Ukraine has created a serious distortion in the market. So far, our estimates lead to a level of around 350-380,000 tons of sunflower seeds that have been processed locally from Ukrainian provenance. This flow entered the Romanian processing units starting from April 2022.

On the other hand, the lack of decision of the Romanian farmers (and we are directly referring to the moments of sale) made the price spikes to be wasted. Sales control must be governed by correct information, planning and not by the senses or by the need for cash flow. We want a mature market; we want a fully sane agribusiness market. But we are just at the beginning.

We also record unpleasant episodes, with farmers who understand the business in this way and violate the contracts. We need to expose facts in order to learn from them. We must be aware of the effects of certain actions and understand that because of those causes, processors will be even more hermetic from an operational and procedural point of view.

In short, with some support and knowingly, a partner farmer supplied the Linoleic commodity instead of the HighOleic commodity, creating serious damage to the processor. Linoleic-HighOleic cross-contamination degrades the batch of processed oil, and damages run into the hundreds of thousands of dollars, if not a million dollars.

Another case that particularly draws our attention is that of a farmer who delivered a mixture of 20 tons of sand and 5 tons of soybeans to the shelter of the night. Naturally, the pick-up bunker and by default the elevator instantly jammed and stopped working. The damage is also very significant: belt scrapers and elevator buckets broken by the weight of the sand, not to mention the sand that ended up in the soybean cells.

Why do we raise the flag and write about such cases? Because other farmers will suffer the effects because of them. Do we want to be treated fairly and build trust? How? By these attempts at cheap and primitive fraud? And we don’t use big words.

Until we regulate these attempts, we will not be able to generate Trust and Partnership, but will all be viewed with Suspicion. And yes, for a few cases, we will all be treated equally, because it’s much better to be safe than sorry, now looking through the processor’s mind.

REGIONAL STATUS

UKRAINE is experiencing extremely serious problems, namely the harvesting of sunflower seeds. The precipitation is not contained and the harvest cannot start in force or in full blast, as they say, and the forecasts indicate precipitation until October 13, 2022.

Ukrainian farmers are harvesting in windows and the harvest level is extremely low for this time period we are in. Out of a harvest potential of 10.5 million tons, Ukrainian farmers are at a maximum level of 1.5-1.6 million tons harvested.

And we are seeing the cascading effects of these rains – cargo with high humidity levels and an appetite for selling to the black market in such conditions. Drying costs are high due to the price of gases, and the price of goods is thus penalized.

The EUROPEAN UNION continues to harvest and process. The main focus is on the intra-Community transfer of goods from established origins, mainly Romania.

RUSSIA is also harvesting, and as mentioned, the crop level is estimated at 17.5 million tons. The weather permits the harvest and the advance is compliant. From October, the export duty on CSFO will be eliminated (zero), compared to 8,621.3 RUB/t (148 USD/t) in September.

TURKEY imposes a duty of 250 USD/MT on the import of sunflower oil from October. At first glance, one might think that it is a pressure factor for the price of sunflower seeds. But in fact, through this import tax, Turkey clearly indicates that it wants the raw material from Ukraine and Russia, maybe partly from Romania.

GLOBAL STATUS

The USA generates a volume of 1.25 million tons. It won’t count as an origin, it’s just the result of the excitement generated by the void initially left by Ukraine, due to the Russian invasion.

ARGENTINA which is in the process of seeding the sunflower crop and could become the X-Factor in the future sunflower seed price equation, which is clearly an unknown. The drought and the lack of water reserves in the soil, as well as the cold, can penalize the sowing process, but also the volume, estimated today at 4.2 million tons. The following month is decisive for Argentina, but La Nina is present for the third season in a row.

PRICE INDICATIONS FOR OILSEEDS AND CSFO IN MAIN ORIGINS

CAUSES AND EFFECTS

Rainfall in Ukraine reverses sunflower seed price trend. This is the central element of raising the price level. The wait rushes buyers and processors. Precipitation, however, is still seen until mid-October and the time horizon extends by another 15 days.

Processors are making the change in canola processing to save time, but this favors demand in the canola market and, naturally, the price strengthens.

Buyers, however, prefer to raise the price level by 10-15 USD/MT to attract volumes and be able to cover the promises of selling to destinations. They will not want to go higher as they wait for the overflow of Ukrainian crop, which cannot be fully processed domestically for logistical reasons. The export gate, namely Chornomorsk, the satellite of Odessa, has only 50 days of green corridor left, and the Mykolaiev counterpart, which massively exports crude oil, cannot operate.

Turkey, in the same way, by introducing the tax, clearly indicates the desire for internal processing of the raw material. And judging in this model, this will not penalize the price of oil in Ukraine (because it will be processed in lower volume for operational-logistical reasons), but support the raw material price.

Russia, by removing the 148 USD/MT export tax, wants to generate exports for the processed commodity. But it will run into the Turkish tariff barrier and the lack of operational capability, as well as the logistical precariousness of its ports. And after a while, we will see the raw material going out for export, but not earlier than the end of January.

CONCLUSION

Waiting for the Ukrainian cargo could strengthen the price of sunflower seeds. The need to carry out drying operations increases the price of goods, and the black market is especially tempting these days.

This expectation may not necessarily bring a deep degradation to the price, but rather a stabilization. But the price of palm oil is not an indicator that provides support in the price of sunflower oil for more than 2-3 weeks. It continues to decline and if today we view the Malaysian stock market at 3,350 MYR levels, the expectation is that this level will also reach 2,500 MYR.

So in the short term, we have a spike caused by the lack of raw material. 6PORTS indications rose 25 USD/MT to 1,250 USD/MT. But with Ukraine going into full blast harvesting, we could see a return to 510-520 USD/MT from 535-540 USD/MT today.

The X factor, that is, Argentina remains to generate value, but we still have to wait until then. If the value will be a negative one, as it indicates today, then there will be a new price support for sunflower seeds.

LOCAL STATUS

Price indications are positioned around 590-600 USD/MT in DAP Processor parity.

REGIONAL STATUS

The European Union is harvesting and in season, as are Russia and Ukraine.

GLOBAL STATUS

The US, following the NASS report, is generating a higher level of soybean stocks, which instantly penalized CBOT quotes.

China and Mexico bought soybeans from the US, and weekly sales for 2022-2023 were above trade expectations, coming in at around 1 million tons.

The soybean harvest will be late this year. The US harvest level stands at 8%, but the forecast looks favorable for progress.

ARGENTINA. The Buenos Aires Grain Exchange estimated Argentina’s soybean crop for the new 2022/23 season at 48 million tons, up 15.5% from last season’s 43.3 million tons, due to an increase in planted area.

Farmers in Argentina have so far sold 65.2% of the 2021/22 soybean crop. Argentina’s agriculture ministry said farmers sold 1.6 million tons of soybeans between September 15 and 21, a 30.4 percent drop from the previous week. The slowdown came after the country’s central bank decided to prevent the purchase of foreign currency for companies using the preferential exchange rate.

Drought and high fertilizer costs have turned farmers’ intentions toward soybeans, reducing acreage for wheat and corn.

BRAZIL is the world’s second largest soybean oil exporter after Argentina and is set to export 2.13 million tons of soybean oil and 18.8 million tons of soybean meal in 2022/23, according to data USDA.

Soybean processing capacity in Brazil is estimated at 194,400 tons/day, with most processing units located in the Mato Grosso, Parana, Rio Grande do Sul and Goias regions, which account for nearly 70% of the country’s total capacity. But last week, ten soybean processors in Brazil halted processing operations due to negative processing margins, which underscore weak domestic demand for biodiesel and high vegetable oil stocks, reducing the pace of local (in-country) processing by 15,000 tons/day.

The Department of Rural Economy (DERAL) generates data at the Parana level and estimates soybean production 22/23 at 21.5 million tons compared to previous forecasts.

Mato Grosso has already planted 1.79% of the 11.8 million hectares planned for soybeans in the 2022/23 crop. Rains and better soil moisture are still expected in this region.

CHINA. There is so much talk about China successfully replacing soybeans with cheaper animal feed ingredients, but soybean meal prices in China have hit an all-time high as demand from farmers has increased, in the case of animal breeders. After a period of low soybean imports, hog prices are up 40% from last year and soybean imports are on the rise.

China is auctioning another 500,000 tons of imported soybeans from state-owned reserves. Since March, China has been regularly selling state-owned soybean stocks on the domestic market.

CBOT – ZSX22 NOV22 – 1,364 c/bu (-46 c/bu = -16.9 USD)

CBOT SOYBEAN TREND CHART – ZSX22 NOV22

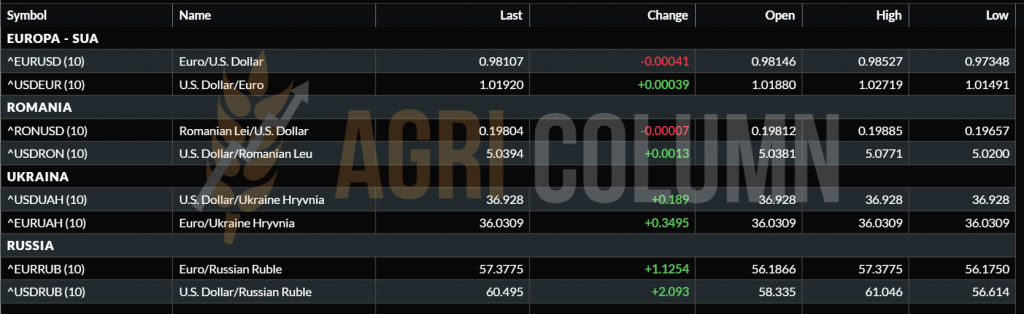

EUR/USD 0.98:1

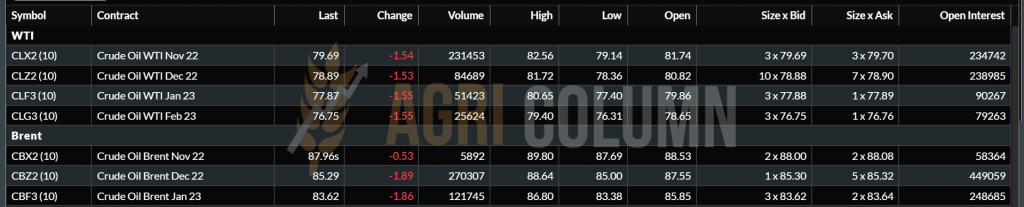

WTI 79.69 USD | BRENT 87.96 USD

1-8 October 2022

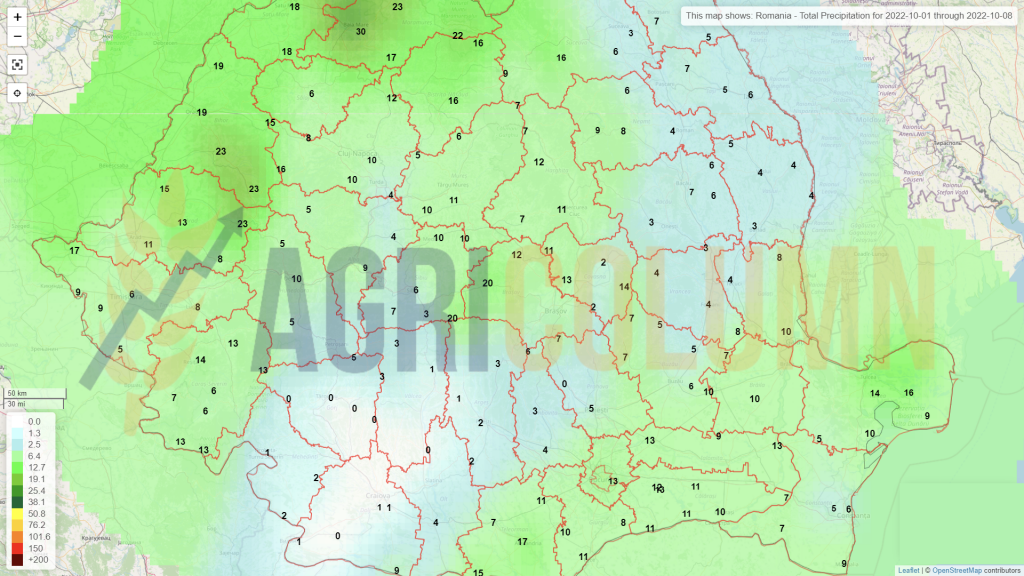

Romania

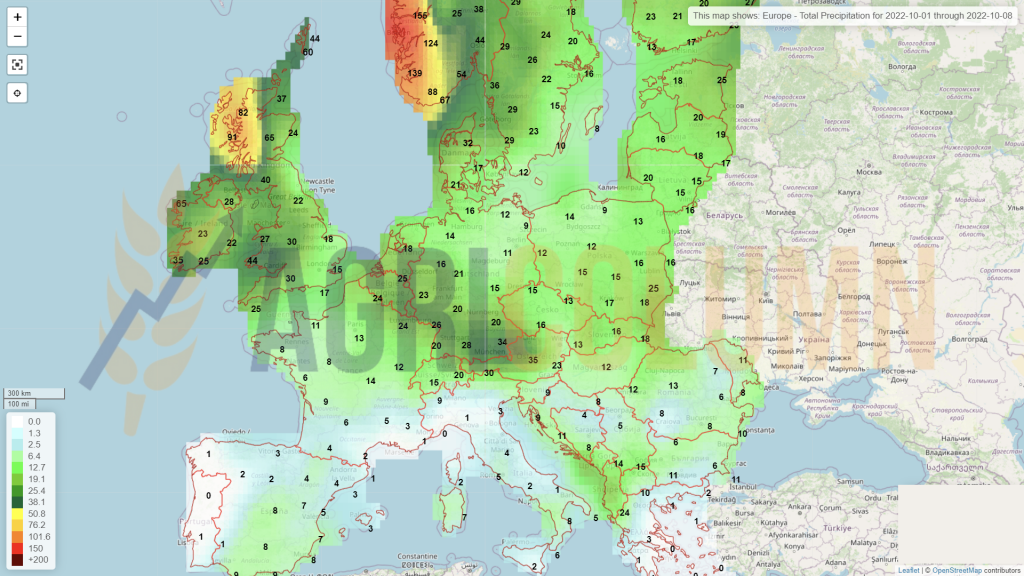

Europe

Ukraine

Russia

Canada

USA

Brazil

Argentina

China

Australia