This week’s market report provides information on:

LOCAL STATUS

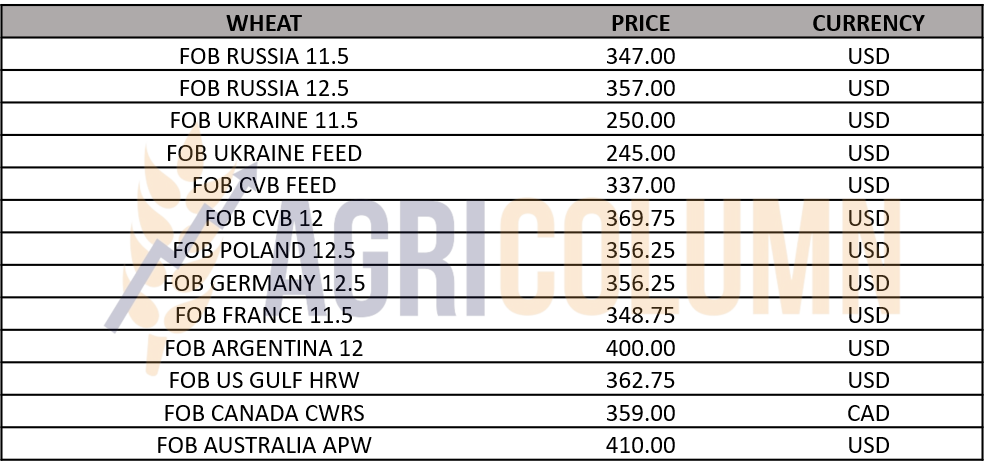

The indications of wheat in the port of Constanța remain set at the level of 340-350 EUR/MT. The indications for feed wheat also remain at a negative difference of 20 EUR/MT compared to the quotations for the milling quality.

A phenomenon of retention is manifested with great power, which means that Romanian farmers do not want to sell wheat in any form at this price level. It is a phenomenon that I mentioned in the last issue, but now it has worsened. The concluded contracts are executed, but nothing more.

Wheat is stored in farm warehouses and this means that it will be very difficult to get out. Farmers have seen price declines in recent times and are unwilling to sell their goods at this level, given that set-up costs have been extremely high and harvesting has been costly due to the price of fuel.

Harvest estimates are at the same level as before. 9 million tons is a level that Romania seems to reach. But judging by the pace, wheat has already been harvested in a proportion of 70-73% in Romania. Thus, we will soon be able to highlight the final figures.

CAUSES AND EFFECTS

Harvest pressure associated with the WASDE report slows wheat prices on Euronext, but not in the Black Sea basin. Quotations from the port of Constanța are not granted with Euronext and we see how the exporters do not find the goods for the shipments scheduled during this period.

The queues of trucks that exceed 6-10 km outside the port of Constanța and line up on the A2 highway slow down deliveries. The mix of Romanian and Ukrainian goods, which is to be delivered by rail, car and via barges, delays deliveries to the wheat export terminals that have scheduled cargo ships at this time.

The retention of goods that Romanian farmers are currently practicing will be able to generate a reversal of the trend after August 12th. At that time, the USDA will release a new WASDE report that will conclude the volume of crops in the northern hemisphere and provide a much clearer picture of crops in the southern hemisphere.

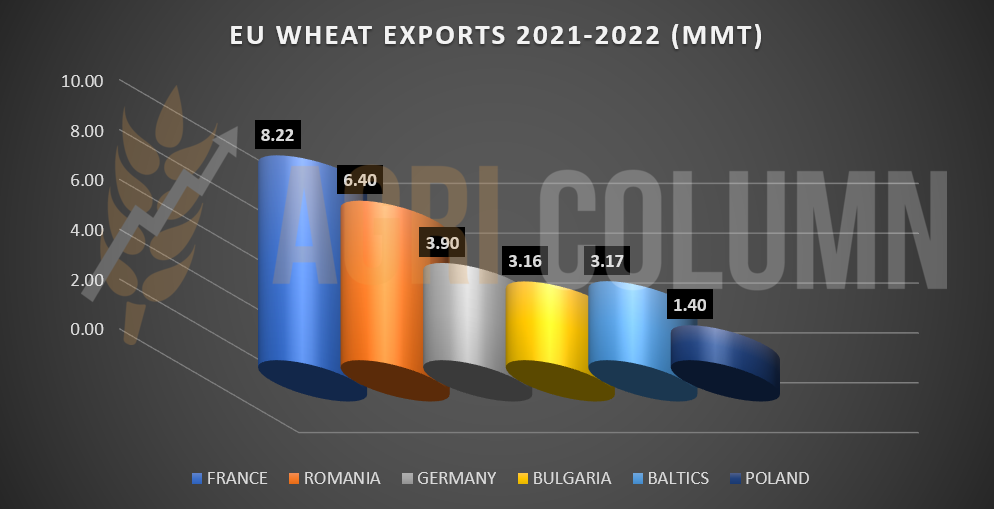

Now that the 2021-2022 season is fully over in terms of exports, we total the final figures and close with the graphic image of a successful season of Romanian wheat sales.

REGIONAL STATUS

RUSSIA generates through IKAR (analysis house) a volume forecast of Russian wheat that seems truly Homeric. 90 million tons of wheat and 50 million tons of exports in the 2022-2023 season. The numbers are extremely high and we have never seen Russia at this level.

But according to ProZerno monitoring, wheat prices have begun to fall dramatically in Russia. In the Volga, Chernozem, Siberia and Urals regions, the price of wheat has visibly depreciated by between 355 and 590 EUR/MT. It is an effect of the harvest pressure, collateral with the ambition of the Russian Federation to export over 4 million tons in August 2022.

USDA indicates maximums of 85 million tons for the 2017-2018 and 2020-2021 seasons. WASDE July 2022 positioned Russia at the level of 81.5 million tons of production and an export program of 40 million tons.

90 million tons is an extremely high level and we are not sure that these figures indicate the reality, namely that it is only about Russian wheat. Our feeling is that 8-9 million tons are added from the dowry of Ukraine for the simple reason that this is exactly what is happening at the moment – Ukraine is being robbed of its own wheat. It can be certified how the goods are harvested and loaded into trucks carrying Russian flags and then directed to destinations under the tutelage of the Russian Federation.

UKRAINE is degraded by 2 million tons by WASDE July 2022 and reduced to 19.5 million tons. The causes are multiple: entire fields affected and destroyed by bombing and armored ground units, as well as by unexploded ordnance. Ukrainian exports are still set at 10 million tons.

The EUROPEAN UNION is reduced by 5 million tons in the production of soft wheat, from 130.4 million tons to 125 million tons. France is falling to the level we have been estimating for some time, namely 33 million tons.

TENDERS

MIT JORDAN purchased 60,000 tons at a level of 413 USD/MT in CFR Aqaba parity for delivery November 1-15, 2022 from Ameropa SA. The second bidder generated a price of 439.5 USD/MT (CHS).

EURONEXT WHEAT MLU22 SEP22 – 325.5 EUR (minus 17.25 EUR)

WHEAT TREND GRAPHIC – MLU22 SEP22 | 10 million tons of Ukrainian wheat no longer weigh so much in the global share. Another factor is the reduction of the Russian tax.

REGIONAL STATUS

USA. WASDE in July 2022 raises the North American wheat crop forecast to 48 million tons, 1 million tons more than last month, on a premise of good spring wheat development. It is a compensation that partially solves the problem of American winter wheat, in the context of the global balance.

CANADA also receives an additional 1 million tons in the wheat production forecast, so that the forecast rises to the level of 34 million tons. It is, moreover, a welcome and deserved upgrade to the Canadian account, taking into account the climate regime that has favored the development of wheat cultivation.

ARGENTINA has certified that it will not sow the forecasted area. From the forecast of 6.5 million hectares, Argentina drops to 6.2 million hectares, so that the decrease in production can be clearly seen on the horizon. The latest estimates on Argentine production are reduced from 18.5 million tons to 17.7 million tons, according to BAGE (Buenos Aires Grain Exchange)

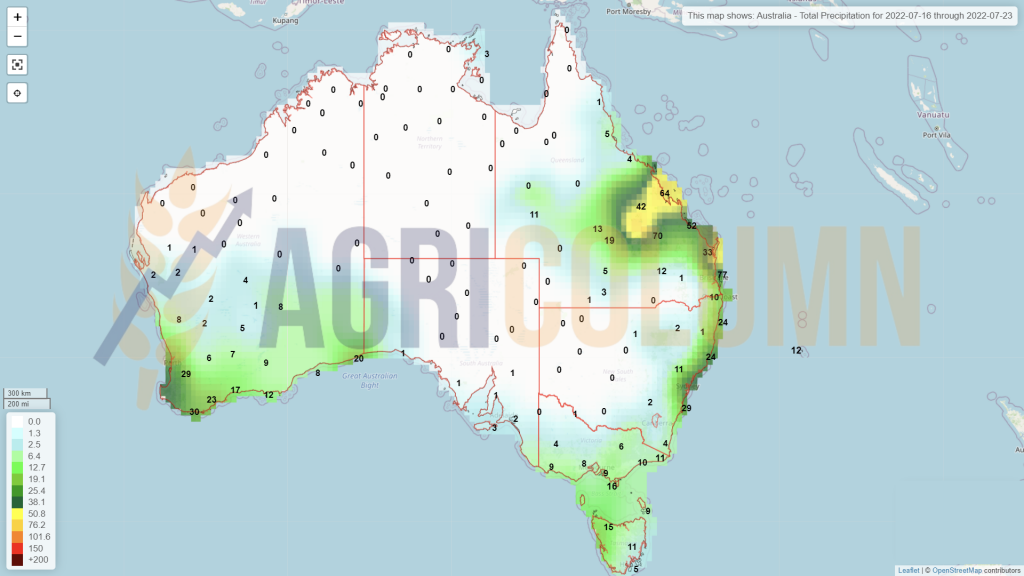

AUSTRALIA remains in the same positive forecast trend of 33 million tons, favored by the rainy climate.

CBOT ZWU22 SEP22 – 776 c/bu (minus 18 c/bu = 6.6 USD)

CBOT WHEAT TREND GRAPHIC – ZWU22 SEP22 | By comparison, we are at the trading level before the Russian invasion.

WHEAT PRICE INDICATIONS IN MAIN ORIGINS

CAUSES AND EFFECTS

We therefore have a decreasing global projection by 1.79 million tons, from 773.43 million tons to a level of 771.64 million tons. The decline in global production is shared between the European Union (Spain, Italy and Germany), Ukraine and Argentina, which, as we know from previous reports, will not sow the number of hectares allocated to wheat due to water shortages.

Ukraine is reduced by 2 million tons to 19.5 million tons, and Argentina is currently losing a potential of 100,000 hectares that will not be sown. The growth is distributed between the USA, Canada and partly Russia. Canada receives a crop upgrade of 1 million tons, up to the level of 34 million tons. The US also has an increase of about 1 million tons, and Russia only 0.5 million tons.

corrections that occurred in Euronext and CBOT are a direct result of the action of the trading algorithms that are granted according to the programming to which they were subjected. Any headline is interpreted, any potential for decline generated by news coming from the hot spots of the world are strong signals of profit taking and exit.

We see this YO-YO effect manifesting itself in an accelerated way. The cadence of decreases and increases enters the regime of hours, not days, as we were used to until now. The speed is generated by the fear of funds that the recession may occur at any time.

WASDE, in turn, generated a more than neutral report, which led to a decrease in wheat values in Euronext and CBOT. But this is happening with accurate science in the USDA’s attempts to keep the market under control. July, traditionally, generates calm and tranquility. By calculation, everything looks somewhat balanced compared to the previous month. A decrease of 1.79 million tons in production is offset by a correction in global consumption which miraculously decreases by exactly 1.77 million tons, just enough so that we do not have figures identical to the decrease in production, but which is granted with stocks increasing by 0.67 million tons.

Thus, we see as a sum of the three factors that we have more wheat in the world with about 0.47 million tons, which naturally leads to a neutrality of the ratio. However, it generated a rather sharp drop of 11 EUR in EURONEXT, 15 minutes after its release.

We should see things before they happen and we believe that this month has generated a decrease to facilitate an increase in the next month. August WASDE generates the final harvest volumes in the northern hemisphere and certifies the seeding extent in Argentina.

At the same time, we see an acceleration in US wheat exports and a more pronounced forecast of Canadian wheat exports, to the detriment of other origins.

Russia’s forecasts are not supported by WASDE yet. It is natural that you cannot support 90 million tons of harvest volume forecast. But in August, things will certainly settle, just as last year they were suddenly degraded by 12.5 million tons, we could see a sharp increase in Russian production. We insert here an excerpt from our special edition dedicated to WASDE August 2021:

“Russia was adjusted negatively from 85 million tons to 72.5 million tons, representing a cut of 12.5 million tons. Canada is also on the same downward trend, from 31.5 million tons to 24 million tons, a decrease of 7 million tons. The United States also cut its own production, adjusting negatively by another 1.35 million tons, to the level of 46.2 million tons. ”

The July 2022 WASDE shade predicts a scenario in which we will have the following factors:

- Price enhancement following the certification of volumes in the European Union.

- Implicitly a decrease in the volumes generated by the European Union.

- Enhancement of volumes from Russia (adjacent to volumes extracted from Ukraine)

- The Russian tax that gives way to a room for maneuver of 70 USD/MT, which causes the price of wheat, as it did when it was imposed and the price increased.

- Enhancing the volumes generated by Canada, Australia and the USA.

- A continuous headline on how Ukraine will agree with Russia and Turkey as arbitrators to create an export corridor. These endless meetings and negotiations are just a sterile effect of diplomacy. Indeed, Ukraine will not accept anything from Russia until it leaves Ukrainian territory, including Crimea. We all know that Russia will not do this in any way. And the referee, Turkey, is just doing an image exercise, in an effort to gain a regional position in this context. We all know that Turkey is going through a period of extreme inflation for a very long time, and their national currency is constantly devaluing.

- FEDERAL RESERVE will arrive on July 26-27 with a new interest rate announcement, and some sources indicate an increase of 100 points, ie 1%. This would have a major effect of lowering stock market indications by liquidating positions by funds.

Everything we have accumulated above sends us to some conclusions:

- The world needs price correction to generate vital food in disadvantaged areas. Social peace is very important. No one wants escalation of tensions in developing countries and implicitly out of control social riots.

- Compared to the above point, however, we have an opponent, the Russian Federation, who blackmails these tensions, wanting to control these vital areas of the world for its benefit. And if we only take Russia’s ambitious plan to export 50 million tons (40 Russian and 10 Ukrainian), this volume represents 25% of the global wheat trade.

- The lower volumes of wheat in the European Union are offset by other areas of origin such as the USA, Canada, Australia and Russia, so there is a balance and we must be realistic in this regard.

- Extremely high inflation is a major global problem, and the FED effort will yield results, as it has done every time it has intervened. After all, stock markets grew through the savagery of investment funds, which targeted the positive margin for printed money. Let’s be realistic and remember the moments of December 2019, the moments before the outbreak of the pandemic and the prices of wheat at that time.

So what do we have? A potential for a decrease compared to a potential for a price increase. Everything is mixed in the factors described above and the share of decrease is quoted at 65% compared to the share of increase of 35%. But as we can see, it is trying to go down in parking lots, such as from 415 EUR to 375 EUR and stayed for a while. Then at 340-350 EUR and has been sitting on this plateau for some time. There is still time until August 12, but this weather may be altered by the FED soon, more precisely on July 26-27, 2022.

LOCAL + REGIONAL STATUS

The indications of the port of Constanța shyly rise above the level of 300 EUR/MT, more precisely to 303 EUR/MT in the CPT parity. It is an effect of strengthening the USD against the EUR rather than a pressing demand.

Romanian farmers show the same effect of retention as in the case of wheat, generated by the memory of the moments when barley was quoted at the level of 340-350 EUR/MT.

But the market does not grant desire to reality. Destinations receive much cheaper freight offers and we note a transaction concluded with MIT Jordan for 60,000 tons of barley with Bunge, without predefined origin, at the price of 352 USD/MT CFR Aqaba. This price leads to a level of 280-285 EUR/MT equivalent of CPT Constanța, although, certainly, the origin has 1% chances to be Romanian, given the local specifics of the Bunge company, which does not have as object of activity the grain trade, but only the one with oilseeds.

In Russia, too, barley prices are deteriorating, followed by wheat prices. The quantified degradation in figures is between 335-500 RUB/MT, at a level of 58 RUB/1 USD.

CAUSES AND EFFECTS

Barley is also part of the feed wheat trajectory and the difference from Euronext of minus 40 EUR is clearly represented in the prices offered in the CPT Constanța parity. Demand will exist, but the agreement between feed wheat and barley will hold up even if barley has a negative global balance. In the end, it all comes down to replacing barley with feed wheat.

BARLEY INDICATIONS IN MAIN ORIGINS

In order to move on and open the 2022-2023 season in terms of statistics, we must close 2021-2022 and the graph we generated expresses in a single image the richness of the Romanian crop from the previous season.

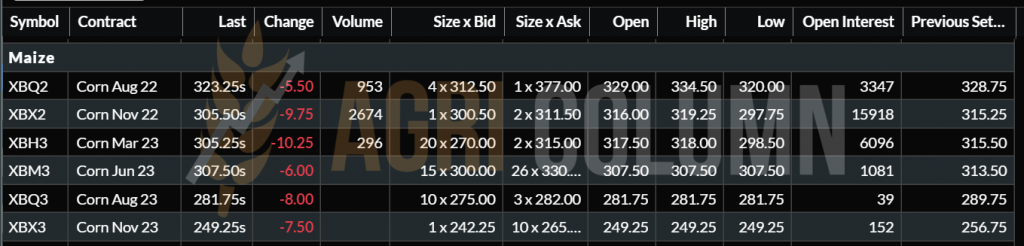

LOCAL STATUS

The indications of the port of Constanta reflect the quotations of corn in Euronext. Thus, we see quotations of 290-292 EUR/MT. It is the usual matrix: EURONEXT minus 10 EUR/MT. We also have cross-Ukrainian quotations valued at 255 EUR/MT, which puts the price of Romanian goods under intense pressure. To understand where the equalization takes place, we just need to remind you that the goods in Ukraine have operating rates of 30 EUR/MT. Thus, the value becomes substantially equal to the Romanian one, and the port services operator sums up the operating revenues in the operational plan.

Internally, Romania has serious problems that develop every day. The corn crop decreases more day by day, effectively melting under intense heat and lack of rainfall. Drought is wreaking havoc on Romanian corn crop. At least 10-12 counties watch helplessly as everything dries up, as everything melts in the sun.

At this moment, we do not believe that Romania will be able to exceed a level of 11 million tons of harvest volume, especially since no precipitation is announced, and moreover, a new heat wave will cross our country.

Water as the main ingredient, water as an added value to the seed that has been planted, water as the main element of feeding the population has been ignored for years by both the authorities and many farmers. We recall here the political constraints and incompetence fueled by divergent interests, which led to the exclusion of irrigation from the National Plan for Resilience. Those who fueled the exclusion of irrigation are well known, we do not name them here.

What we must understand, however, is that without firm measures and without investments in major infrastructure, we are heading for a collapse of Romanian agriculture. Farmers will gather around projects of interest, there is no doubt, they understand the importance of water as a vital element in agriculture.

The vital arteries that can supply capillaries with WATER are the major projects of this country at the moment. The Siret-Bărăgan canal is the most representative example. This is a vital artery that crosses Moldova and descends into Bărăgan. This vital artery can provide the much-desired support to the counties it crosses, the support given to Moldova so hit by fate every year.

History reminds us every day that we need to understand and learn from it, but history does not forgive fools, certainly not. It is taking revenge in its own way and today we see the result of the ignorance and lack of understanding of the forerunners who led this country. It is the result of customs that materialized indifference, which led to absolutely ridiculous actions, such as the priests going out into the field to invoke the rains.

After 2000 years, did we get to the same place we left? Should we invoke divinity to rain? It is absolutely out of the human power of understanding that went through the dark years of the Middle Ages.

Humanity experienced the Renaissance through its first exponent, Johannes Gutenberg, a metallurgist who in 1455 printed the Mainz Bible, inventing the printing press and thus paving the way for knowledge.

And the industrial revolution, which began with James Watt, a Scottish inventor and visionary who created the first steam engine in 1776, paved the way for combine harvesters and satellite systems that create support for the growth of mass crops.

And now are we going back to the priesthood to invoke the rains? What can these humble disciples of Jesus do? Are we so incomprehensible as not to see with our own eyes how indolence, indifference, personal interests, the lack of unity of farmers, an amalgam that has smoldered for years has actually exploded this year?

The climate is changing and we are witnessing a combined effect of industrialization and the end of a glacial period in Earth’s history, and WATER is becoming the most important human resource right now and in the years to come. Let us be aware of our contemporaneity with these changes on a global scale and not remain passive or indifferent. Only the common, conjugated effort, devoid of any partisan interests and channeled by the technicians, will snatch us from the clutches of the drought that grins for sure with a periodicity of maximum two years.

CAUSES AND EFFECTS

We maintain the same recommendation to farmers not to expose themselves and not to engage in forward contracts that will endanger not only the contractual execution, but also the profits already made from the first crops, rapeseed, barley and wheat. It’s logic. You sign a contract, hence your business partner expects you, the farmer, to honor it. And penalties for non-performance lead to a level of up to 45% of the value of undelivered goods.

A wise attitude would be for the goods not to be sold until they are harvested. In this way, the risks of contractual penalties are reduced. The market difference must also be taken into account. This sums up next to each ton of cargo, logically.

Buyers, in turn, have signed contracts for the delivery of these goods and we are very close to repeating the scenario of 2020, when, despite the desire of the Romanian government, the state of calamity was not approved due to factors we know very well.

REGIONAL STATUS

The EUROPEAN UNION reduces the volume forecast for maize by 1.4 million tons, from 66.8 to 65.4 million tons. Last year, at the same time, the forecast was 69.7 million tons. Judging by what is happening now in Europe, we can say from now on that this is only a minor cut. All of Europe is just a huge arid and dry place, the earth turned to stone and the heat literally suffocates, from the Iberian Peninsula to Romania, the old continent. The values allocated today as forecasts will condense even further in the next period. Weather forecasts indicate precipitation only in the Munich area and partly in Austria, Switzerland and Slovenia. Otherwise, zero rainfall in Spain, France, Hungary and Romania.

RUSSIA is degraded by 1 million tons in the case of maize crop, from 15.5 million tons to 14.5 million tons, with a duly reduced export potential, to the level of 3.8 million tons.

UKRAINE remains unchanged, with a volume projection set at 25 million tons and an export level of 9 million tons. This according to WASDE July 2022, but the Ukrainian domestic projection is 27.5 million tons and a huge effort to export at least 15-17 million tons of corn in the 2022-2023 season.

HUNGARY is actually melting in the face of the heat wave and yields are falling from day to day. The Pannonian Basin is within reach of heat and extreme pedological drought.

SERBIA is also suffering in this context and the USDA-generated projection of 7.2 million tons will not be fulfilled. Vojvodina, which traditionally generates 66% of corn production, suffers from a lack of rainfall and drought. Alongside in the same status is the Sumadije-Zapadne area, with a share of 18% of maize production in the total Serbian crop.

EURONEXT XBX22 NOV22 – 305.5 EUR (minus 9.75 EUR)

EURONEXT CORN TREND GRAPHIC – XBX22 NOV22

GLOBAL STATUS

USA, through WASDE, remains positive, with a generous crop, thanks to the larger sown area versus the forecast from March 1, 2022. The US currently maintains 373 million tons of corn production for the 2022-2023 season. US exports continue week by week at the usual pace, with small adjustments, but which ultimately summarizes the role of the US as the largest producer of corn globally.

BRAZIL also remains unchanged in current and future forecasts. We have 116-117 million tons for the two productions of the 2021-2022 season and a projection of 126 million tons for the 2022-2023 season.

ARGENTINA remains in the current forecasts, because they are outside the window of sowing the new crop. 55 million tons pass into Argentina’s account starting with September, the moment when the sowing will start.

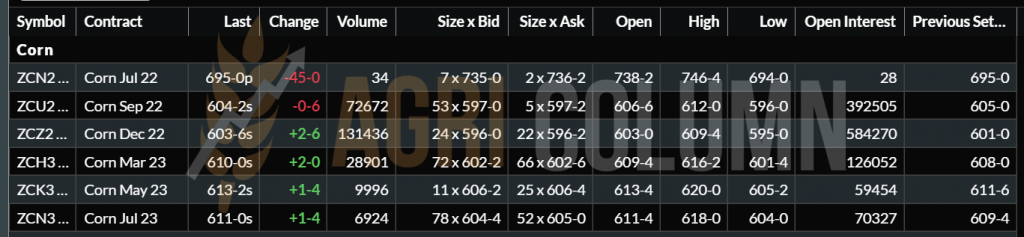

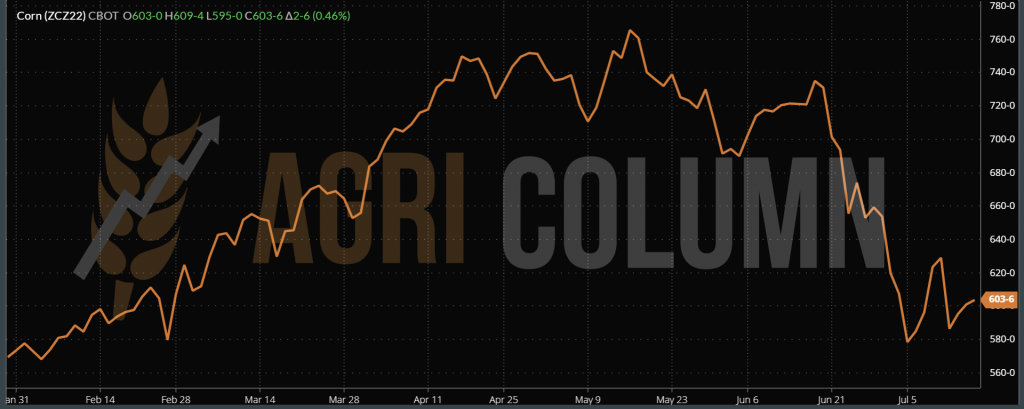

CORN – CBOT ZCZ22 DEC22 – 603 c/bu (+2 c/bu)

CORN TREND GRAPHIC – ZCZ22 DEC22

CORN INDICATIONS IN MAIN ORIGINS (old crop)

CAUSES AND EFFECTS

A global balance between production and consumption, according to WASDE July 2022, induces a state of equilibrium fueled by a surplus of stocks of about 2.5 million tons. But this balance is extremely fragile. The apparent silence actually heralds a potential storm. And we speak in metaphorical terms, because the drought will generate the storm that is forecast on the horizon. The drought will reduce the potential of volumes in the European Union, generate higher imports, especially in the Iberian Peninsula, and Ukraine will become a source of supply for the European Union.

The focus of the processors will be on this area of origin. Poland, Germany, in turn, have a supply interest. And because of the current situation with the lack of liquidity of Ukrainian farmers, the price of goods should be only a marginal element in the supply chain logistics equation. Today, the costs on the railway between Ukrainian farms and the port of Constanta, to take a fixed benchmark, are between 120-190 USD/MT, according to Elena Neroba, analyst at MaxiGrain Ukraine.

China will maintain its interest in the Black Sea. The logistics cost is much lower than that of North and South American origins. The first harvest will be in Southeast Europe and thus the companies that supply China will be the first to quote in the port of Constanta for the Ukrainian flow.

Overseas, in the US, however, things can constantly deteriorate. The first signs of a hot August are on the horizon. Forecasts indicate very high temperatures and a possible heat wave matched by the lack of precipitation. Thus, we will be able to witness decreases in the forecasted volumes in the USA and degradations of the production level per hectare, which will fuel the price progress.

But the counterweight exists in the FED institution, which by raising interest rates would actually move investment funds out of the field allocated to agribusiness raw materials. We do not insist on this topic, but balancing and connecting to reality is a necessity for the world’s population and this should be expressed through access to cheaper food than what we have known in the last two years.

And from the European Union we expect a return with our feet on the ground, because the Green Deal is a bridge too far away, and humanity cannot feed on insects and larvae. The origin of man and his genetics do not allow this radical movement.

LOCAL STATUS

The indications of rapeseed buyers are extremely different. Buyers in the country, the processing units in particular, display very high discount prices compared to Euronext. One of the processors is no longer purchasing rapeseed at this time. Discounts against Euronext are from minus 25 to minus 35 EUR/MT compared to AUG22.

The port of Constanța, on the other hand, becomes very competitive and the indications are offered without discount compared to AUG22, a sign that the European Union’s forecast was too optimistic.

We all need to know that starting today we will take XRX22 NOV22 as a benchmark, leaving behind XRQ22 AUG22, which is no longer valid for stock exchange transactions. Now only the positions open in Euronext for the players on the stock exchange will be liquidated. In the physical market, however, the XRX22 NOV22 is the next benchmark to follow.

CAUSES AND EFFECTS

As described in previous issues, the safety of a good rapeseed crop generates relaxation from domestic processors. Their logic is correct. You cannot move the crop difference of 1 million tons for instant export, especially in today’s circumstances, when the port of Constanța is effectively blocked. The goods will be available to farmers later. The decline in the market, which has dropped from stratospheric levels to what is being traded today, has led many farmers to hold back, that is, to store rapeseed volumes.

REGIONAL STATUS

Without creating animosity about our position on what the EU is reporting, we have consistently supported production of less than 18 million tons, more precisely 17.7-17.8 million tons. Now, the Union is falling sharply from 18.4 million tons to 18.1 million tons so that in the past days it returned below 18 million tons, ie to 17.9 million tons, at the moment. We say this at the moment because harvesting is ongoing in the European Union, and the excessive heat of the past as well as the areas where the storms took place should leave deeper traces than what is estimated today.

UKRAINE will generate a maximum of 1.65-1.85 million tons of rapeseed and its flow will be for export, especially to Poland and Romania. Rapeseed from Ukraine is offered at extremely high discounts compared to Euronext. In the Polish border, for example, it has a discount of 80-100 EUR/MT compared to the quotation AUG22 and subsequently NOV22. This volume of goods influences the processors in the purchase process, the price pressure being obvious in this case as well. Farmers in Poland and Romania also bear this pressure, by default.

EURONEXT XRX22 NOV22 – 680 EUR (+6,5 EUR)

EURONEXT TREND GRAPHIC – RAPESEED – XRX22 NOV 22

GLOBAL STATUS

CANADA indicates a thriving rapeseed health and Twitter abounds in photos with flowering canola fields. Yellow is the color of Canada today. The period from mid-August to October will be when Canadian farmers will harvest. The forecast remains set at 20-21 million tons at the moment.

AUSTRALIA also maintains the same positive rapeseed regime and estimates remain at 5.8 million tons of production.

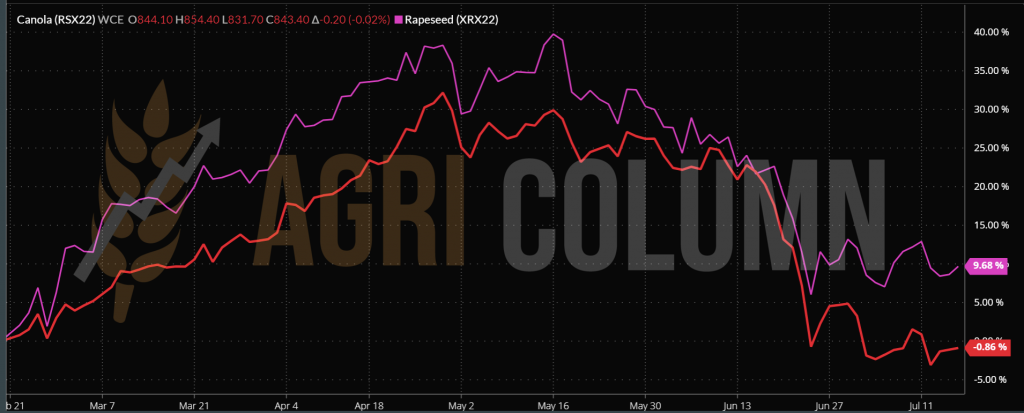

ICE CANOLA RSX22 NOV22 – 843.4 CAD

ICE CANOLA RSX22 NOV22 TREND GRAFIC

COMPARISON EURONEXT VS. ICE CANOLA – XRX22 VS RSX22 | HEAD TO HEAD

CAUSES AND EFFECTS

Palm oil reduces the level of rapeseed from 700 EUR to the current 680 EUR in Euronext quotes. It has great difficulty finding its way to exports to Indonesia and stocks have risen from 1.52 million tons to 1.66 million tons last month. This fact negatively influences the whole complex of vegetable oils, implicitly rapeseed oil.

Oil and its decrease to the level of 100 USD/barrel in Brent London quotations negatively influence the rapeseed quotations and contribute to the level difference between 700 and 680 EUR, indication NOV22 Euronext.

The Canadian crop that is seen on the horizon creates the same premises for relaxation from buyers.

On the other hand, Germany is increasing the level of rapeseed oil in the biodiesel blend. It was as if Germany was claiming that it would change the mix for biodiesel from rapeseed oil to 100% used cooking oil by 2030. At the time, we were claiming that it was just a political statement and that’s about it. Time has guaranteed what we said. Trucks run on diesel fuel, combine harvesters and tractors as well. As demand grew, it made sense for rapeseed oil to maintain its share in biodiesel.

Malaysia is facing particular problems with the workforce. It fails to agree with Indonesia from a bureaucratic point of view, and workers in Indonesia cannot meet the demand in Malaysia. This is a factor to watch out for, as it can create pressure that will alleviate Indonesia’s surplus stocks. The bureaucratic apparatus is used as a lever to delay the production of a third country to generate its own exports.

Rapeseed finds support at this level of 670-680 EUR, and demand will return by November 2022, when the processing units now covered in terms of stocks will return to the market for supply.

LOCAL STATUS

The local indications of sunflower seeds deteriorated to the level of 520-530 USD/MT in the parity of DAP Processor, as well as in CPT Constanța. The bonus for high oleic acid content is also around 40 USD/MT for goods with a minimum content of 80% oleic acid.

However, on the local market, the goods are not traded. The heat wave is worrying enough for farmers to remain reluctant to sell. Small lots are traded, but they do not represent an important share in the overall picture at national level. And on this occasion, we want to state a decrease in the volume potential of the Romanian sunflower harvest by at least 10-12% in the first estimate. That is a maximum of 3.25-3.3 million tons compared to 3.65 million tons initial estimate.

The problems generated by the heat and the total lack of precipitation will also affect the sunflower crop. The two factors will work simultaneously and, if no one pays attention to this today, the counties already affected by the extreme pedological drought show it in their own way through entire plots with insufficient development, small size for this period and a potential at least doubtful.

CAUSES AND EFFECTS

Decreasing the price of sunflower seeds are combined factors.

One of them is the decrease in the price of palm oil, which generates a decrease in the VEGOIL complex, on the principle of communicating vessels. Excess Indonesian goods are pushing the price on the vegetable oil market insistently. It is a first stress factor of the price of sunflower seeds.

The second factor is the goods from Ukraine which are offered at a substantial discount compared to the Romanian goods. When the Romanian goods were quoted at the level of 560-570 USD/MT, the one of Ukrainian origin indicated 515 USD/MT. We also saw a quotation of 460 USD/MT for October 2022 delivery, which is an extremely low level.

We must not forget that the goods are offered especially to the processing units, as, in fact, the whole process started from March 2022 until today. Otherwise, how can we explain the silence that followed the reduction of the availability of raw materials in Romania, which caused chaos in hypermarkets? Simple, by introducing raw materials from Ukraine into the processing circuit. This is the basis of today’s buyers, on the Ukrainian seed flows.

The third factor is undoubtedly the strengthening of the US dollar. The fact that it generates a much higher income in the national currency RON contributes in an amplified way to the decrease of the quotations of sunflower seeds.

In the compensatory things, we see, first of all, the European cultural specificity that does not have in the daily diet the palm oil, but the sunflower oil. And this is ignored by many market analysts. The European consumer wants sunflower oil, as well as those from Turkey and India.

The second compensation factor represents the decrease of the volume potential in Romania, but it is attenuated by the Ukrainian crop which will make the lack to be compensated extremely easily due to the proximity. The volumes will stop in Romania, first of all, even if the desire is for them to supply the European market.

Another compensation factor could come later from Asia, which will generate demand due to the lack of Indonesian personnel required in Malaysia. In other words, an increase in price due to demand due to the decrease in the volume of palm oil generated by Malaysia would be a support for the price of sunflower oil and, implicitly, of the raw material. But this factor is one that, if it materializes, will come quite late.

REGIONAL STATUS

UKRAINE is down in estimates from 9.5 million tons to 7.7 million tons. It is a dramatic decrease and the consequences will be seen in 2-3 months. The lack of a volume of 1.8 million tons of seeds will not be compensated by the residual volume remaining from last year.

The EUROPEAN UNION will reduce the volume of sunflower seeds. It’s only a matter of time before this happens. And we believe that at least 10% will disappear from the picture of the general harvest volume, ie from 10.9 million tons we will go down to 9.8 million tons.

ARGENTINA will generate a production of 4.2 million tons, representing a surplus of about 0.9 million tons compared to last season. This year, Argentine farmers increase the sowing area from 1.6 million ha to 2 million hectares. But sowing will take place after mid-September 2022.

CSFO AND OILSEEDS INDICATIONS IN MAIN ORIGINS

LOCAL + REGIONAL STATUS

Nothing new compared to last week. The price of soybeans is around 560-570 USD/MT, compared to an exchange rate of 1 USD = 4.92 RON.

Romania contributes 9% to the total of 3 million tons of soybeans produced in Europe, ie 270,000 tons. The largest contributor is Italy, with 35%, and France generates about 8%, followed by Croatia. As a non-member country of the Union, but with a large share, we see Serbia with 25% of the total European Union or rather the European territory.

GLOBAL STATUS

The US falls in the production forecast by 3.7 million tons, according to WASDE July 2022. Canada also contributes to this decrease in the production forecast by 0.3 million tons. The US generated a volume of 122.6 million tons.

BRAZIL and ARGENTINA remain unchanged in forecasts: 149 million tons Brazil and 51 million tons Argentina.

Global consumption remains stable, despite a marginal decrease of 0.16 million tons. So we have a level of 377.7 million tons of soybeans.

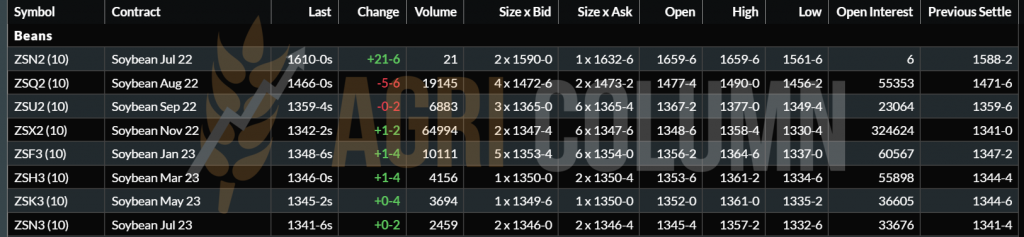

But in the conditions of generous harvests, soybeans go down dramatically on CBOT. The level of NOV22 is 1,342 c/bu, and the chart will show us the complete picture of what the price level was and what it looks like, at this moment. The risk remains only in time as a stress factor, because soybeans are the prerogative of the two Americas. On the other hand, China, by reducing demand, can contribute to lowering the price level.

CBOT ZSX22 NOV22 – 1,342 c/bu (+1 c/bu)

SOYBEAN TREND GRAPHIC ON CBOT – ZSX22 NOV22 | Quotations return to the level of the end of January 2022

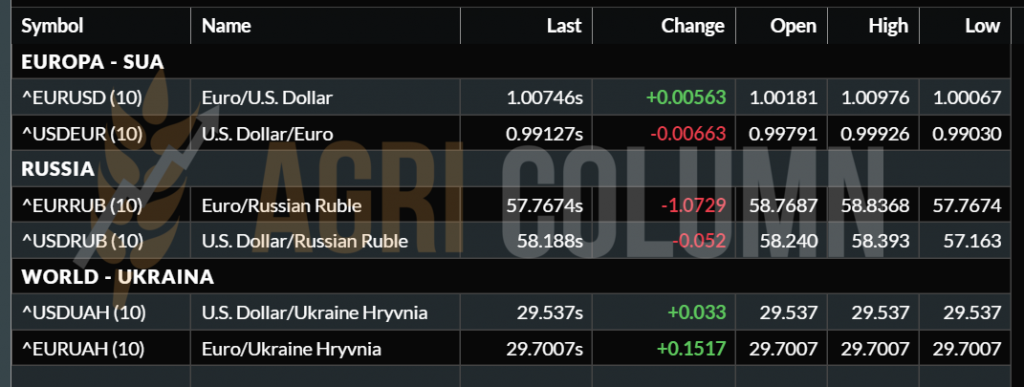

EURO/USD 1:1.007 | USD/RUB 1:58

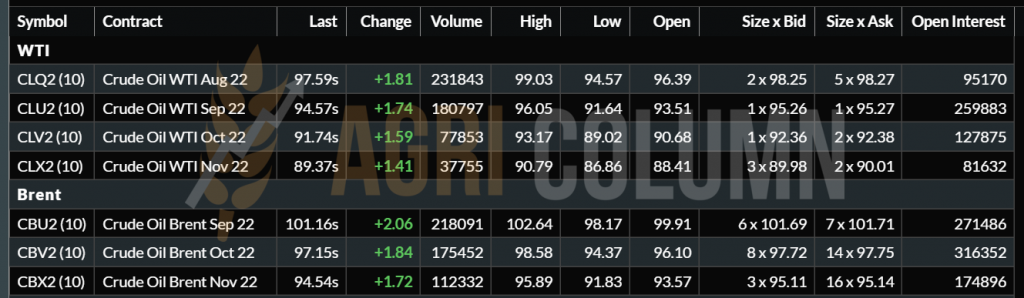

WTI 97.59 USD/barrel | BRENT 101.16 USD/barrel

16-23 July 2022

Romania

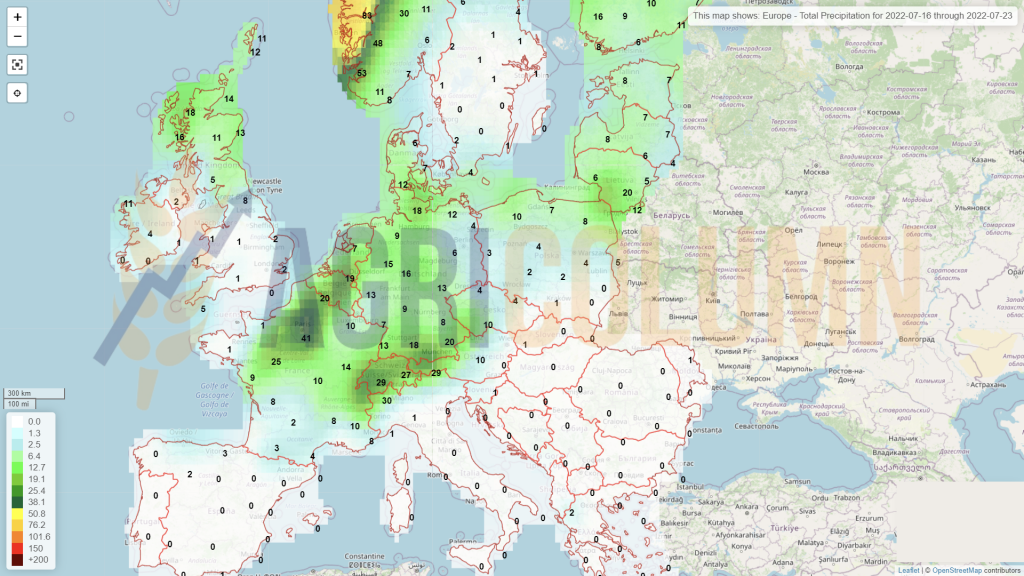

Europe

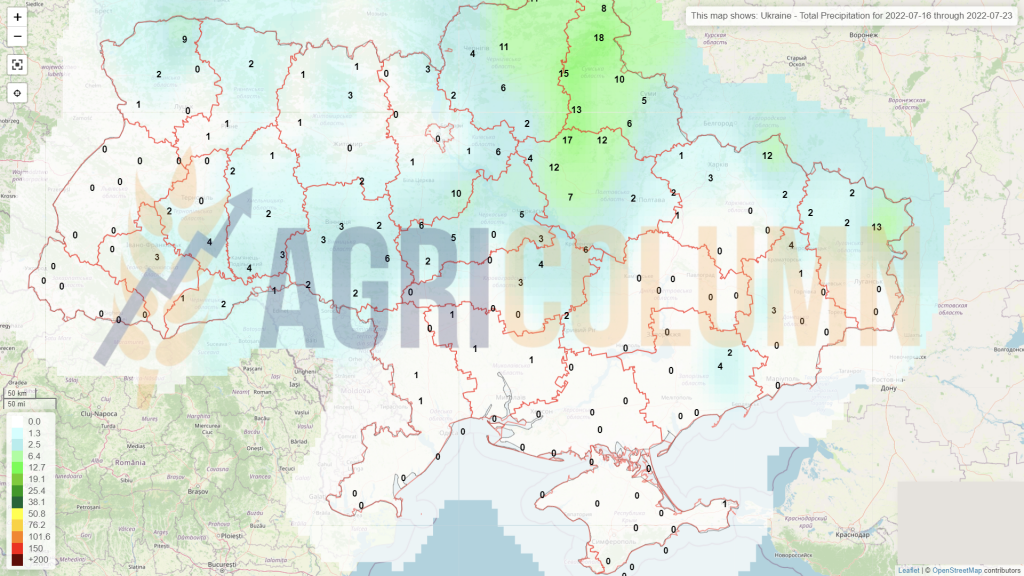

Ukraine

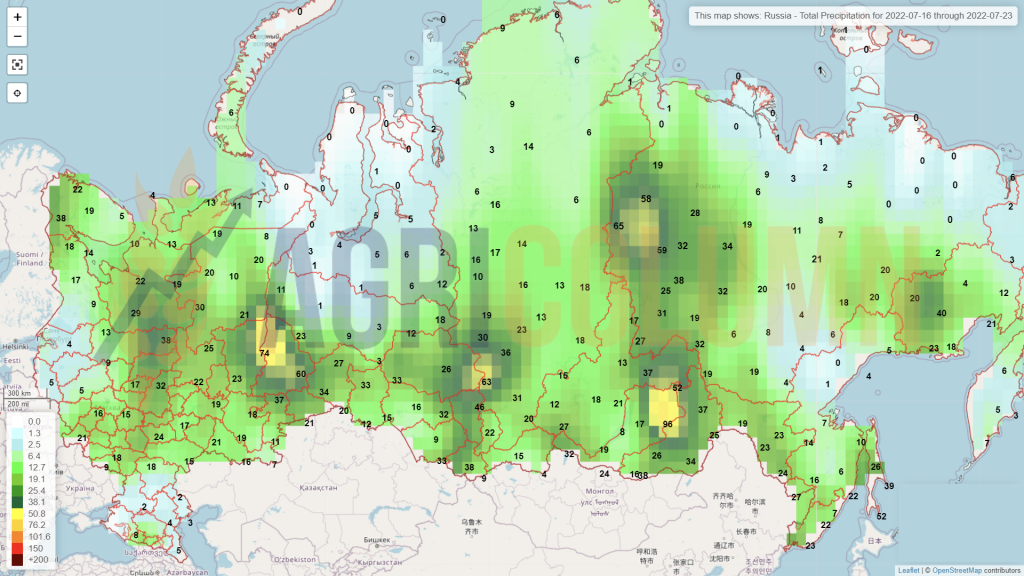

Russia

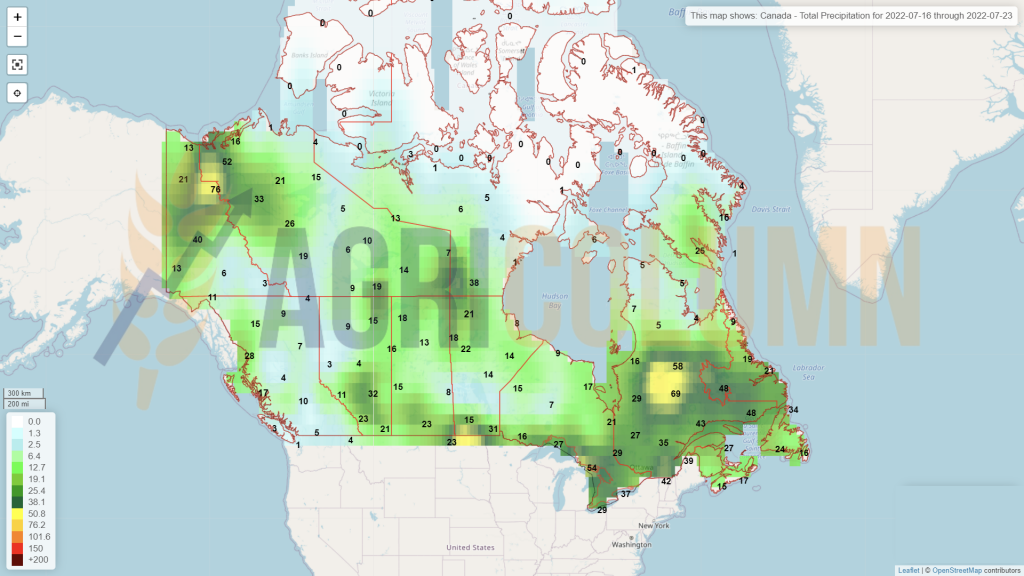

Canada

USA

Brazil

Argentina

China

Australia